Management Accounting Report: Budget Analysis and Improvement Plan

VerifiedAdded on 2023/06/11

|13

|3852

|253

Report

AI Summary

This management accounting report provides a comprehensive analysis of Amana Ltd.'s financial performance in 2020, focusing on budget variances and productivity. It includes a monthly control summary comparing the initial budget, flexible spending plan, and actual results, highlighting both favorable and unfavorable variances. The report assesses Amana's productivity, attributing shortfalls to the COVID-19 pandemic's impact on sales and increased costs, and suggests strategies for improvement, such as offering online sales, adjusting pricing, and reducing variable expenses. The document also advises Mr. Amana on shifting sales to electronic channels and discusses the potential benefits of opening a personal online store versus selling on Amazon. It emphasizes the importance of cost control and revenue enhancement for Amana Ltd.'s future financial stability.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

Create a monthly control summary with the following information: initial budget, flexible

spending plan, and deviations:.....................................................................................................1

Create a statement on Amma's productivity in the year 2020, based on the budget analysis

generated in the above section:....................................................................................................4

Make suggestions to Amma's CEO on categories where they might enhance:...........................5

PART B...........................................................................................................................................7

Report to Mr. Amana...................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

Create a monthly control summary with the following information: initial budget, flexible

spending plan, and deviations:.....................................................................................................1

Create a statement on Amma's productivity in the year 2020, based on the budget analysis

generated in the above section:....................................................................................................4

Make suggestions to Amma's CEO on categories where they might enhance:...........................5

PART B...........................................................................................................................................7

Report to Mr. Amana...................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is one of the most important factors that can help an individual as

well as the team to take decisions in an appropriate and precise manner which can aid the firm in

taking an upper edge in the industry. The practise of giving budgetary and administrative data to

executives such that managers may take knowledgeable choices regarding the business is known

as managerial accountancy (Abou Taleb and Al Farooque, 2021). Expenditures, predictions, and

progress reviews are examples of this data. The emphasis is on brief run choices are among the

most important features of managerial accountancy. Managerial Accountancy Intelligence is

intended to assist executives in making superior day-to-day selections instead of longer

run conceptual ones. It often incorporates information on expenditures, earnings, profitability, as

well as other aspects which are important to the company's decision-makers. This document is

split into 2 sections. The initial section depicts the compilation of a monthly control analysis that

details Amana's Ltd.'s operation for the year 2020. The next section advises Mr. Amana as to

whether to open its personal internet store or offer on Amazon.

PART A

Create a monthly control summary with the following information: initial budget, flexible

spending plan, and deviations:

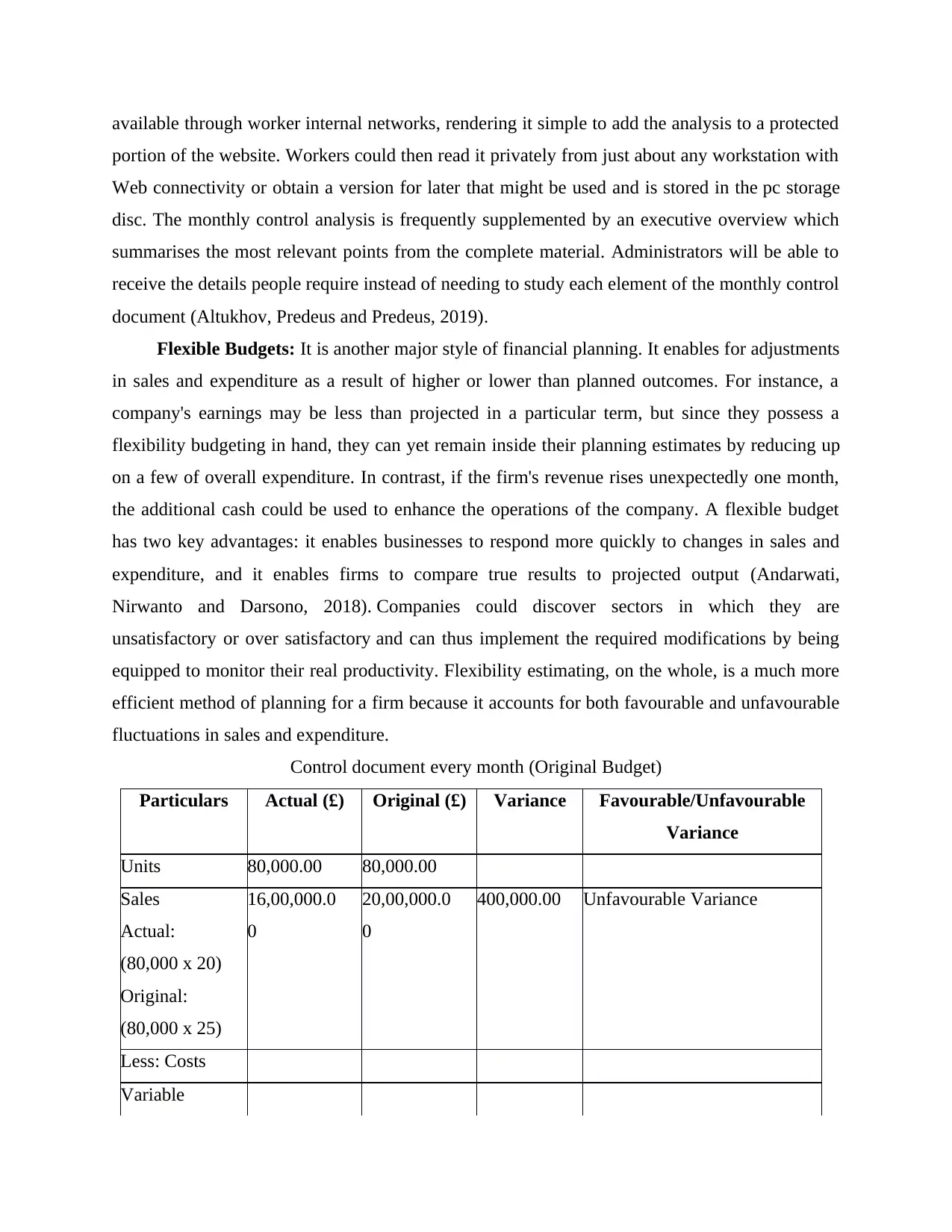

Monthly Control Analysis: A monthly control statement is a record which summarises

the firm's productivity during the previous month. It comprises earnings, expenditures, profit/loss

statistics, and also a selling breakdown per item category or function. A review of real outcomes

to projected amounts is also included in the study, noting those regions wherein real outcomes

varied from expectations (Al-Dmour, Zaidan and Al Natour, 2021). This enables managers to

spot any possible issues or opportunities for development promptly. The monthly control

summary has a variety of applications. It could be utilized to monitor performance toward certain

aims and initiatives, for example. It could also aid in the detection of patterns across duration,

enabling managers to take better, accurate and strategic decisions. The analysis could also be

employed as a technique for predicting upcoming results. The senior administrative executive is

usually in charge of the monthly control analysis, which he or she would evaluate with some

other representatives of higher administration prior releasing it across the organisation. It might

be mailed or displayed publicly for workers to review. Several firms have large datasets

Management accounting is one of the most important factors that can help an individual as

well as the team to take decisions in an appropriate and precise manner which can aid the firm in

taking an upper edge in the industry. The practise of giving budgetary and administrative data to

executives such that managers may take knowledgeable choices regarding the business is known

as managerial accountancy (Abou Taleb and Al Farooque, 2021). Expenditures, predictions, and

progress reviews are examples of this data. The emphasis is on brief run choices are among the

most important features of managerial accountancy. Managerial Accountancy Intelligence is

intended to assist executives in making superior day-to-day selections instead of longer

run conceptual ones. It often incorporates information on expenditures, earnings, profitability, as

well as other aspects which are important to the company's decision-makers. This document is

split into 2 sections. The initial section depicts the compilation of a monthly control analysis that

details Amana's Ltd.'s operation for the year 2020. The next section advises Mr. Amana as to

whether to open its personal internet store or offer on Amazon.

PART A

Create a monthly control summary with the following information: initial budget, flexible

spending plan, and deviations:

Monthly Control Analysis: A monthly control statement is a record which summarises

the firm's productivity during the previous month. It comprises earnings, expenditures, profit/loss

statistics, and also a selling breakdown per item category or function. A review of real outcomes

to projected amounts is also included in the study, noting those regions wherein real outcomes

varied from expectations (Al-Dmour, Zaidan and Al Natour, 2021). This enables managers to

spot any possible issues or opportunities for development promptly. The monthly control

summary has a variety of applications. It could be utilized to monitor performance toward certain

aims and initiatives, for example. It could also aid in the detection of patterns across duration,

enabling managers to take better, accurate and strategic decisions. The analysis could also be

employed as a technique for predicting upcoming results. The senior administrative executive is

usually in charge of the monthly control analysis, which he or she would evaluate with some

other representatives of higher administration prior releasing it across the organisation. It might

be mailed or displayed publicly for workers to review. Several firms have large datasets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

available through worker internal networks, rendering it simple to add the analysis to a protected

portion of the website. Workers could then read it privately from just about any workstation with

Web connectivity or obtain a version for later that might be used and is stored in the pc storage

disc. The monthly control analysis is frequently supplemented by an executive overview which

summarises the most relevant points from the complete material. Administrators will be able to

receive the details people require instead of needing to study each element of the monthly control

document (Altukhov, Predeus and Predeus, 2019).

Flexible Budgets: It is another major style of financial planning. It enables for adjustments

in sales and expenditure as a result of higher or lower than planned outcomes. For instance, a

company's earnings may be less than projected in a particular term, but since they possess a

flexibility budgeting in hand, they can yet remain inside their planning estimates by reducing up

on a few of overall expenditure. In contrast, if the firm's revenue rises unexpectedly one month,

the additional cash could be used to enhance the operations of the company. A flexible budget

has two key advantages: it enables businesses to respond more quickly to changes in sales and

expenditure, and it enables firms to compare true results to projected output (Andarwati,

Nirwanto and Darsono, 2018). Companies could discover sectors in which they are

unsatisfactory or over satisfactory and can thus implement the required modifications by being

equipped to monitor their real productivity. Flexibility estimating, on the whole, is a much more

efficient method of planning for a firm because it accounts for both favourable and unfavourable

fluctuations in sales and expenditure.

Control document every month (Original Budget)

Particulars Actual (£) Original (£) Variance Favourable/Unfavourable

Variance

Units 80,000.00 80,000.00

Sales 16,00,000.0 20,00,000.0 400,000.00 Unfavourable Variance

Actual: 0 0

(80,000 x 20)

Original:

(80,000 x 25)

Less: Costs

Variable

portion of the website. Workers could then read it privately from just about any workstation with

Web connectivity or obtain a version for later that might be used and is stored in the pc storage

disc. The monthly control analysis is frequently supplemented by an executive overview which

summarises the most relevant points from the complete material. Administrators will be able to

receive the details people require instead of needing to study each element of the monthly control

document (Altukhov, Predeus and Predeus, 2019).

Flexible Budgets: It is another major style of financial planning. It enables for adjustments

in sales and expenditure as a result of higher or lower than planned outcomes. For instance, a

company's earnings may be less than projected in a particular term, but since they possess a

flexibility budgeting in hand, they can yet remain inside their planning estimates by reducing up

on a few of overall expenditure. In contrast, if the firm's revenue rises unexpectedly one month,

the additional cash could be used to enhance the operations of the company. A flexible budget

has two key advantages: it enables businesses to respond more quickly to changes in sales and

expenditure, and it enables firms to compare true results to projected output (Andarwati,

Nirwanto and Darsono, 2018). Companies could discover sectors in which they are

unsatisfactory or over satisfactory and can thus implement the required modifications by being

equipped to monitor their real productivity. Flexibility estimating, on the whole, is a much more

efficient method of planning for a firm because it accounts for both favourable and unfavourable

fluctuations in sales and expenditure.

Control document every month (Original Budget)

Particulars Actual (£) Original (£) Variance Favourable/Unfavourable

Variance

Units 80,000.00 80,000.00

Sales 16,00,000.0 20,00,000.0 400,000.00 Unfavourable Variance

Actual: 0 0

(80,000 x 20)

Original:

(80,000 x 25)

Less: Costs

Variable

Costs: 280,000.00 200,000.00 80,000.00 Unfavourable Variance

Materials 440,000.00 320,000.00 120,000.00 Unfavourable Variance

Labour 120,000.00 120,000.00 0 Nil

Overhead

Contribution 760,000.00 13,60,000.0 600,000.00 Unfavourable Variance

(Sales – 0

Variable

Costs)

Fixed

Overheads:

Warehouse 170,000.00 200,000.00 30,000.00 Favourable Variance

Rental 100,000.00 100,000.00 0 Nil

Insurance

Fulltime

Warehouse

Supervisor 35,000.00 50,000.00 15,000.00 Favourable Variance

Salary

Profit 455,000.00 10,10,000.0

0

555,000.00 Unfavourable Variance

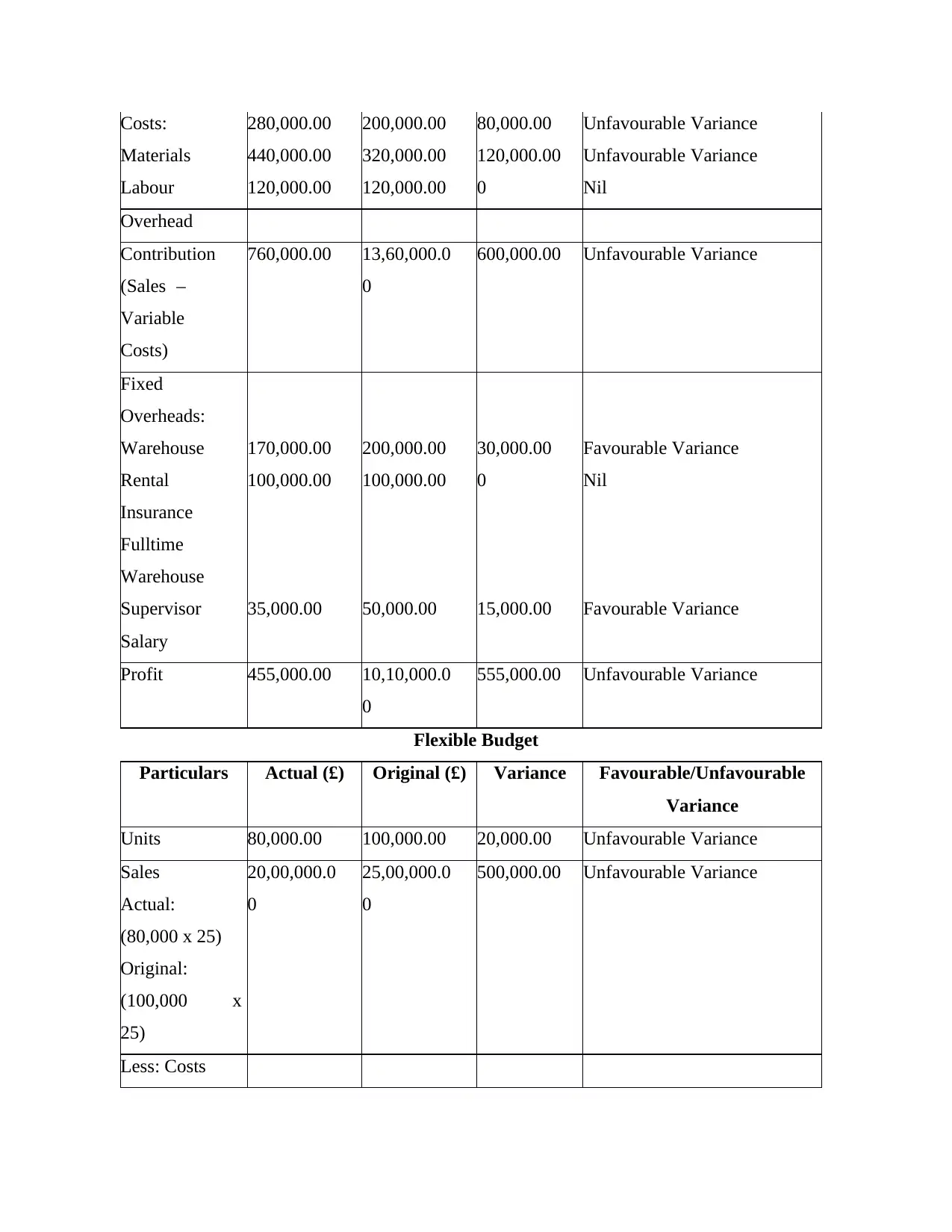

Flexible Budget

Particulars Actual (£) Original (£) Variance Favourable/Unfavourable

Variance

Units 80,000.00 100,000.00 20,000.00 Unfavourable Variance

Sales 20,00,000.0 25,00,000.0 500,000.00 Unfavourable Variance

Actual: 0 0

(80,000 x 25)

Original:

(100,000 x

25)

Less: Costs

Materials 440,000.00 320,000.00 120,000.00 Unfavourable Variance

Labour 120,000.00 120,000.00 0 Nil

Overhead

Contribution 760,000.00 13,60,000.0 600,000.00 Unfavourable Variance

(Sales – 0

Variable

Costs)

Fixed

Overheads:

Warehouse 170,000.00 200,000.00 30,000.00 Favourable Variance

Rental 100,000.00 100,000.00 0 Nil

Insurance

Fulltime

Warehouse

Supervisor 35,000.00 50,000.00 15,000.00 Favourable Variance

Salary

Profit 455,000.00 10,10,000.0

0

555,000.00 Unfavourable Variance

Flexible Budget

Particulars Actual (£) Original (£) Variance Favourable/Unfavourable

Variance

Units 80,000.00 100,000.00 20,000.00 Unfavourable Variance

Sales 20,00,000.0 25,00,000.0 500,000.00 Unfavourable Variance

Actual: 0 0

(80,000 x 25)

Original:

(100,000 x

25)

Less: Costs

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

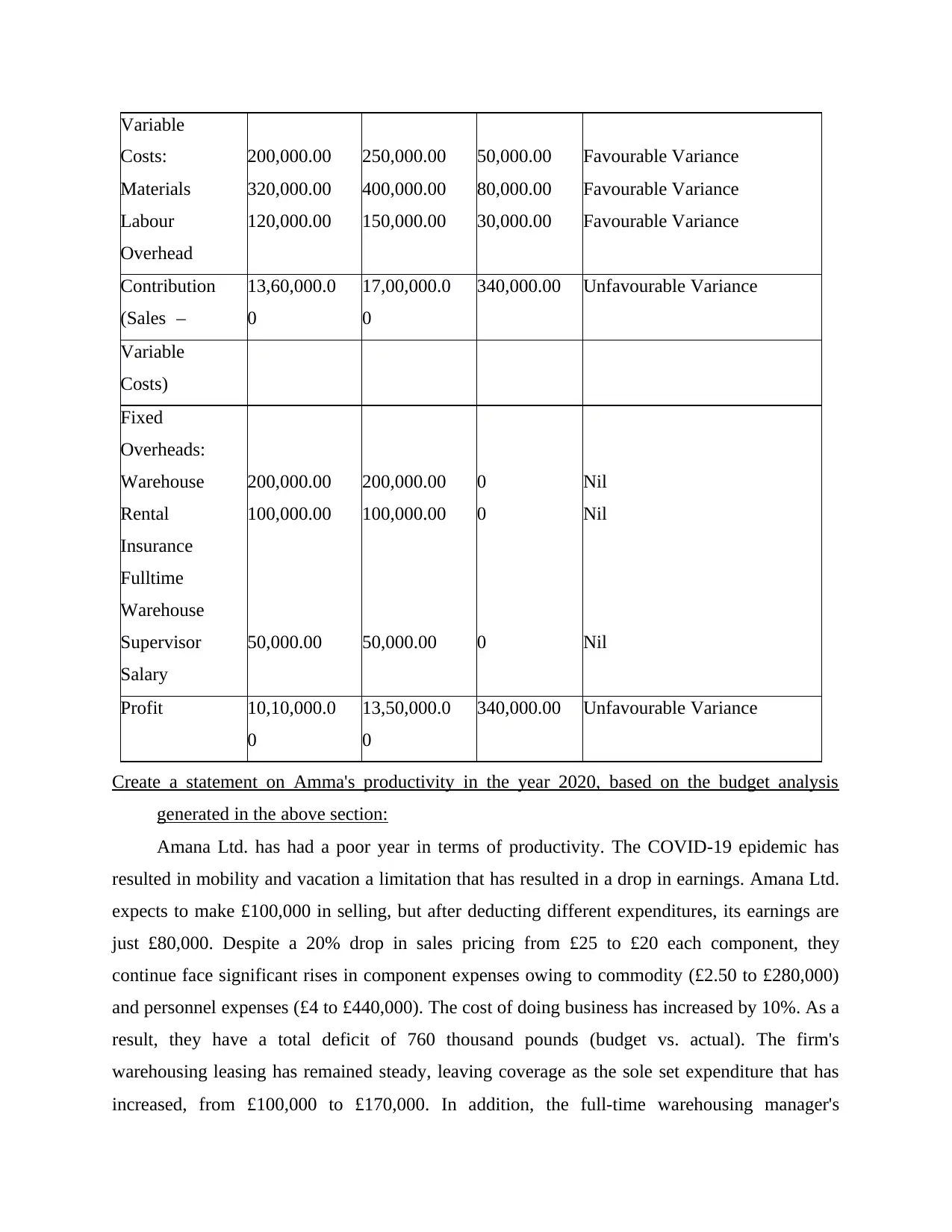

Variable

Costs: 200,000.00 250,000.00 50,000.00 Favourable Variance

Materials 320,000.00 400,000.00 80,000.00 Favourable Variance

Labour 120,000.00 150,000.00 30,000.00 Favourable Variance

Overhead

Contribution 13,60,000.0 17,00,000.0 340,000.00 Unfavourable Variance

(Sales – 0 0

Variable

Costs)

Fixed

Overheads:

Warehouse 200,000.00 200,000.00 0 Nil

Rental 100,000.00 100,000.00 0 Nil

Insurance

Fulltime

Warehouse

Supervisor 50,000.00 50,000.00 0 Nil

Salary

Profit 10,10,000.0 13,50,000.0 340,000.00 Unfavourable Variance

0 0

Create a statement on Amma's productivity in the year 2020, based on the budget analysis

generated in the above section:

Amana Ltd. has had a poor year in terms of productivity. The COVID-19 epidemic has

resulted in mobility and vacation a limitation that has resulted in a drop in earnings. Amana Ltd.

expects to make £100,000 in selling, but after deducting different expenditures, its earnings are

just £80,000. Despite a 20% drop in sales pricing from £25 to £20 each component, they

continue face significant rises in component expenses owing to commodity (£2.50 to £280,000)

and personnel expenses (£4 to £440,000). The cost of doing business has increased by 10%. As a

result, they have a total deficit of 760 thousand pounds (budget vs. actual). The firm's

warehousing leasing has remained steady, leaving coverage as the sole set expenditure that has

increased, from £100,000 to £170,000. In addition, the full-time warehousing manager's

Costs: 200,000.00 250,000.00 50,000.00 Favourable Variance

Materials 320,000.00 400,000.00 80,000.00 Favourable Variance

Labour 120,000.00 150,000.00 30,000.00 Favourable Variance

Overhead

Contribution 13,60,000.0 17,00,000.0 340,000.00 Unfavourable Variance

(Sales – 0 0

Variable

Costs)

Fixed

Overheads:

Warehouse 200,000.00 200,000.00 0 Nil

Rental 100,000.00 100,000.00 0 Nil

Insurance

Fulltime

Warehouse

Supervisor 50,000.00 50,000.00 0 Nil

Salary

Profit 10,10,000.0 13,50,000.0 340,000.00 Unfavourable Variance

0 0

Create a statement on Amma's productivity in the year 2020, based on the budget analysis

generated in the above section:

Amana Ltd. has had a poor year in terms of productivity. The COVID-19 epidemic has

resulted in mobility and vacation a limitation that has resulted in a drop in earnings. Amana Ltd.

expects to make £100,000 in selling, but after deducting different expenditures, its earnings are

just £80,000. Despite a 20% drop in sales pricing from £25 to £20 each component, they

continue face significant rises in component expenses owing to commodity (£2.50 to £280,000)

and personnel expenses (£4 to £440,000). The cost of doing business has increased by 10%. As a

result, they have a total deficit of 760 thousand pounds (budget vs. actual). The firm's

warehousing leasing has remained steady, leaving coverage as the sole set expenditure that has

increased, from £100,000 to £170,000. In addition, the full-time warehousing manager's

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

compensation has been reduced by 20%, from £50,000 to £35,000 each year. Because they were

willing to offer merchandise at a cheaper cost whilst keeping the similar quantity of pieces

delivered, the firm's flexible estimate was much more realistic than their initial estimate

(Borthick and Pennington, 2017). The real outcomes reveal Amana's poor efficiency. Although

the sale pricing each item has increased, expenses have not been brought within line. The fixed

expenses have been brought within limits. Total productivity has fallen short of expectations.

Amana Ltd. is not as lucrative as it was in previous years, prompting them to rethink their

income and expense strategy in the future. Rather than presenting companies as per the plan to

a sector like travel, Amana Ltd. must concentrate more on consumption for their goods

(Sledgianowski, Gomaa and Tan, 2017). The corporation must lower item expenses and look for

other sources of components and resources (i.e. procuring things regionally). If Amana Ltd.

wants customers to keep acquiring relics, it might have to cut item costs throughout the range.

Amana Ltd. is now offering relics for £20 a piece, but it is expected to offer for £25 each

component in the future. There is a net deficit of £760,000 as a consequence of this (budget vs.

actual). A rise in materials and personnel prices, and also a rise in administrative expenditures,

has been the key contributors to this deficit. To address such deficits, Amana Ltd. must place a

greater emphasis on item consumption rather than sector placement, such as tourist. Companies

must cut units prices and look for other ways to get components and supplies (procuring from the

local supplier). If Amana Ltd. wants people to keep purchasing its items, they might have to cut

costs throughout the line. They can also explore extending into other sectors to generate various

kinds of earnings. Despite the fact that the COVID-19 epidemic seems to have had a detrimental

effect on the travel industry and Amana Ltd. in particular, there will definitely be prospects for

the business to recover if the appropriate modifications are made (Brink, Hobson and Stevens,

2017).

Make suggestions to Amma's CEO on categories where they might enhance:

Amana Ltd. is experiencing a difficult moment, and the firm's Chief Executive Officer

require to start taking certain tangible steps to assist the firm get back on the right track. In this

situation, growing income by providing additional pieces at a greater sales value whilst lowering

fluctuating expenses is critical (Roberts and Gnan, 2017). Amana could enhance their earnings in

a variety of different methods, including:

willing to offer merchandise at a cheaper cost whilst keeping the similar quantity of pieces

delivered, the firm's flexible estimate was much more realistic than their initial estimate

(Borthick and Pennington, 2017). The real outcomes reveal Amana's poor efficiency. Although

the sale pricing each item has increased, expenses have not been brought within line. The fixed

expenses have been brought within limits. Total productivity has fallen short of expectations.

Amana Ltd. is not as lucrative as it was in previous years, prompting them to rethink their

income and expense strategy in the future. Rather than presenting companies as per the plan to

a sector like travel, Amana Ltd. must concentrate more on consumption for their goods

(Sledgianowski, Gomaa and Tan, 2017). The corporation must lower item expenses and look for

other sources of components and resources (i.e. procuring things regionally). If Amana Ltd.

wants customers to keep acquiring relics, it might have to cut item costs throughout the range.

Amana Ltd. is now offering relics for £20 a piece, but it is expected to offer for £25 each

component in the future. There is a net deficit of £760,000 as a consequence of this (budget vs.

actual). A rise in materials and personnel prices, and also a rise in administrative expenditures,

has been the key contributors to this deficit. To address such deficits, Amana Ltd. must place a

greater emphasis on item consumption rather than sector placement, such as tourist. Companies

must cut units prices and look for other ways to get components and supplies (procuring from the

local supplier). If Amana Ltd. wants people to keep purchasing its items, they might have to cut

costs throughout the line. They can also explore extending into other sectors to generate various

kinds of earnings. Despite the fact that the COVID-19 epidemic seems to have had a detrimental

effect on the travel industry and Amana Ltd. in particular, there will definitely be prospects for

the business to recover if the appropriate modifications are made (Brink, Hobson and Stevens,

2017).

Make suggestions to Amma's CEO on categories where they might enhance:

Amana Ltd. is experiencing a difficult moment, and the firm's Chief Executive Officer

require to start taking certain tangible steps to assist the firm get back on the right track. In this

situation, growing income by providing additional pieces at a greater sales value whilst lowering

fluctuating expenses is critical (Roberts and Gnan, 2017). Amana could enhance their earnings in

a variety of different methods, including:

Offering things at a reduction of (£25-£5) for a short timespan of time could also be a

fantastic advertising approach that really could increase overall revenues and sometimes

even lure certain additional consumers who earlier couldn't afford to buy owing to

excessive pricing. Nevertheless, after the term concludes, this strategy may lead in a

significant stock of unused relics that could deplete the firm's operating assets. As a

result, this choice is not advised.

Offering items digitally to consumers who were unable to reach real businesses due to the

shutdown would assist Amana raise earnings by £100,000 whilst lowering static costs. As

a consequence, this choice is suggested (Cleve, 2017).

Reducing the sales pricing of every item from £25 to £30 while keeping the fluctuating

expenses the same would result in a £2 boost in contributions every item, resulting in a

net earnings gain of £40,000. This solution, though, may not be optimal because it may

reduce selling quantity, presenting Amana with a lesser inventory of things to offer. This

is not a viable choice (Massicotte and Henri, 2021).

Lowering the sales pricing from £25 to £30 whilst lowering fluctuating expenses from

£20 to £12 each piece would result in a boost of £8 each item in contribution, resulting in

a net earnings gain of £80,000. This choice would assist Amana cut expenditures while

also contributing more often to set overhead costs. This is the preferred alternative.

Variable expenses could indeed be cut in a number of different techniques, such as:

By decrease the quantity of full-time warehousing employees from four to three whilst

keeping all other factors constant, fluctuating expenses would be reduced by £120,000

per year. This approach is advised because it would assist Amana cut expenditures while

also contributing more often to permanent overhead costs (Dutta, Paitya and Majumdar,

2020).

Variable expenses would be reduced by £30,000 each year if administrative expenditures

are reduced from £1.50 each piece to £1 each item. This approach, although, may not be

possible because certain operational expenses are required for the business to perform

correctly like the instance can be of an insuring firm. This is not really a viable choice.

Material volatile expenses are reduced from £2.5 each piece to £2 each component

whereas other factors stay constant (sales costs and personnel cost stay constant). It

would really result in a £0.5 each piece improvement in contribution rate, resulting in an

fantastic advertising approach that really could increase overall revenues and sometimes

even lure certain additional consumers who earlier couldn't afford to buy owing to

excessive pricing. Nevertheless, after the term concludes, this strategy may lead in a

significant stock of unused relics that could deplete the firm's operating assets. As a

result, this choice is not advised.

Offering items digitally to consumers who were unable to reach real businesses due to the

shutdown would assist Amana raise earnings by £100,000 whilst lowering static costs. As

a consequence, this choice is suggested (Cleve, 2017).

Reducing the sales pricing of every item from £25 to £30 while keeping the fluctuating

expenses the same would result in a £2 boost in contributions every item, resulting in a

net earnings gain of £40,000. This solution, though, may not be optimal because it may

reduce selling quantity, presenting Amana with a lesser inventory of things to offer. This

is not a viable choice (Massicotte and Henri, 2021).

Lowering the sales pricing from £25 to £30 whilst lowering fluctuating expenses from

£20 to £12 each piece would result in a boost of £8 each item in contribution, resulting in

a net earnings gain of £80,000. This choice would assist Amana cut expenditures while

also contributing more often to set overhead costs. This is the preferred alternative.

Variable expenses could indeed be cut in a number of different techniques, such as:

By decrease the quantity of full-time warehousing employees from four to three whilst

keeping all other factors constant, fluctuating expenses would be reduced by £120,000

per year. This approach is advised because it would assist Amana cut expenditures while

also contributing more often to permanent overhead costs (Dutta, Paitya and Majumdar,

2020).

Variable expenses would be reduced by £30,000 each year if administrative expenditures

are reduced from £1.50 each piece to £1 each item. This approach, although, may not be

possible because certain operational expenses are required for the business to perform

correctly like the instance can be of an insuring firm. This is not really a viable choice.

Material volatile expenses are reduced from £2.5 each piece to £2 each component

whereas other factors stay constant (sales costs and personnel cost stay constant). It

would really result in a £0.5 each piece improvement in contribution rate, resulting in an

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

overall earnings rise of (£20,000). Yet, this can lead to low-quality items, lowering client

loyalty. This is not a viable choice (Maheshwari, Maheshwari and Maheshwari, 2021).

It is clear that Amana's CEO must concentrate on generating earnings whilst lowering

fluctuating expenses. The aforementioned alternatives could assist in achieving such goals and

improving the corporation's fiscal status (Emiaso and Egbunike, 2018).

PART B

Report to Mr. Amana

Mr. Amana's choice to shift 50 percent of his earnings from the traditional method to the

electronic channel is a wise approach. The offices of his business in Sussex, London town hall,

and Liverpool urban central square will only be capable of serving a small region of the

population. Whereas the existence of such locations can increase Amana Souvenirs' affinity

network, the ability to attract additional consumer groups will be limited, and the costs connected

with actual businesses will be considerable. Amana Decorations does have the potential to

significantly extend its industry and client network by channelling 50% of its own expected

revenues via a digital marketing strategy which focuses on the United Kingdom, Europe, and the

United States (Giacomini, Sicilia and Steccolini, 2016).

Simultaneously, this could plan to expand its overall operations in its existing physical

outlets in attempt to better serve local customers and supporters. Mr. Amana, the company

operator, must choose among retailing on Amazon and opening their personal internet store. The

corporation analysed the financial implications of every option while determining which one to

take. In regards of starting their personal internet business, Amana estimates that such an

additional £10,000 would be necessary for start-up expenditures, with an additional £100 per

month essential to continue it operating. In addition, the firm's proprietors are exploring

employing a full-time developer for £35,000 annually (Glushchenko, Yarkova and Kucherova,

2017). This will just add to the stress on the company, since this person could require regular

guidance and management. In addition, there would be the expense of the supply chain to

consider. It is projected that £150,000 will be required to build up a transportation mechanism

for consumers in the United Kingdom, Europe, and the United States. With all of those expenses

taken into account, it's clear that Amana will need £295,000 to open their personal digital

marketplace, which might contribute to a rise in earnings. Instead, if companies trade on

loyalty. This is not a viable choice (Maheshwari, Maheshwari and Maheshwari, 2021).

It is clear that Amana's CEO must concentrate on generating earnings whilst lowering

fluctuating expenses. The aforementioned alternatives could assist in achieving such goals and

improving the corporation's fiscal status (Emiaso and Egbunike, 2018).

PART B

Report to Mr. Amana

Mr. Amana's choice to shift 50 percent of his earnings from the traditional method to the

electronic channel is a wise approach. The offices of his business in Sussex, London town hall,

and Liverpool urban central square will only be capable of serving a small region of the

population. Whereas the existence of such locations can increase Amana Souvenirs' affinity

network, the ability to attract additional consumer groups will be limited, and the costs connected

with actual businesses will be considerable. Amana Decorations does have the potential to

significantly extend its industry and client network by channelling 50% of its own expected

revenues via a digital marketing strategy which focuses on the United Kingdom, Europe, and the

United States (Giacomini, Sicilia and Steccolini, 2016).

Simultaneously, this could plan to expand its overall operations in its existing physical

outlets in attempt to better serve local customers and supporters. Mr. Amana, the company

operator, must choose among retailing on Amazon and opening their personal internet store. The

corporation analysed the financial implications of every option while determining which one to

take. In regards of starting their personal internet business, Amana estimates that such an

additional £10,000 would be necessary for start-up expenditures, with an additional £100 per

month essential to continue it operating. In addition, the firm's proprietors are exploring

employing a full-time developer for £35,000 annually (Glushchenko, Yarkova and Kucherova,

2017). This will just add to the stress on the company, since this person could require regular

guidance and management. In addition, there would be the expense of the supply chain to

consider. It is projected that £150,000 will be required to build up a transportation mechanism

for consumers in the United Kingdom, Europe, and the United States. With all of those expenses

taken into account, it's clear that Amana will need £295,000 to open their personal digital

marketplace, which might contribute to a rise in earnings. Instead, if companies trade on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Amazon, Amana should be aware that it could be required to spend £50,000 in Amazon delivery

charges. Furthermore, owing to intense rivalry among Amazon vendors, Amana is really only

expected to offer 65,000 pieces on the site (Hyndman, 2016).

This figure, however, is susceptible to change because it is mostly determined by

marketplace interest. Returning to expenses, it is clear that Amana will require to invest £50,000

in terms of selling its items on Amazon. If the business decides to offer via this internet

powerhouse, the overall expenditure will be £100,000. Therefore, Amana will have lower start-

up expenses if company opt to offer on Amazon. Their earnings and yields, on the other hand,

are probably to be lesser than it would be if company opened its own internet business. If, on the

other hand, the corporation decides to open their individual internet marketplace, they may

notice a rise in revenues and profitability (Kogut, Janshanlo and Czerewacz-Filipowicz, 2020).

This is because they would possess absolute discretion about what business offer, how much

company charge for it, and how they handle returns. Therefore, when deciding where and how to

market his items, Mr. Amana must thoroughly examine these considerations.

They could take the optimal decision for the respective firm by assessing the benefits and

drawbacks of both retailing on Amazon and establishing his personal digital marketplace. With

all of the aforementioned considerations in view, Mr. Amana should explore selling through

Amazon initially, for a minimum of 1-2 seasons (Kramer, Maas and Van Rinsum, 2016).

Although it is expected to experience stiff rivalry in this vendor sector, this would give Mr.

Amana with accurate information regarding the acceptability of the good or service of the

merchandise in the targeted regions, allowing him to tailor advertising strategies to boost

consumer recognition and engagement in the big scheme of things.

Mr. Amana could contemplate transitioning to a separate web retailer for Amana Treasures

following considerably boosting the company's recognition of the branding in the specific

customers for the initial 1-2 years (Liu and Sustik, 2021).

CONCLUSION

Managerial accountancy is a vital element of any firm, according to this paper. It aids

organisations in tracking their fiscal activity and making well-informed choices which boost

company's overall earnings and profitability. Accounting professionals record and process fiscal

information using a range of instruments and approaches, then offer information and suggestions

to firm founders and executives.

charges. Furthermore, owing to intense rivalry among Amazon vendors, Amana is really only

expected to offer 65,000 pieces on the site (Hyndman, 2016).

This figure, however, is susceptible to change because it is mostly determined by

marketplace interest. Returning to expenses, it is clear that Amana will require to invest £50,000

in terms of selling its items on Amazon. If the business decides to offer via this internet

powerhouse, the overall expenditure will be £100,000. Therefore, Amana will have lower start-

up expenses if company opt to offer on Amazon. Their earnings and yields, on the other hand,

are probably to be lesser than it would be if company opened its own internet business. If, on the

other hand, the corporation decides to open their individual internet marketplace, they may

notice a rise in revenues and profitability (Kogut, Janshanlo and Czerewacz-Filipowicz, 2020).

This is because they would possess absolute discretion about what business offer, how much

company charge for it, and how they handle returns. Therefore, when deciding where and how to

market his items, Mr. Amana must thoroughly examine these considerations.

They could take the optimal decision for the respective firm by assessing the benefits and

drawbacks of both retailing on Amazon and establishing his personal digital marketplace. With

all of the aforementioned considerations in view, Mr. Amana should explore selling through

Amazon initially, for a minimum of 1-2 seasons (Kramer, Maas and Van Rinsum, 2016).

Although it is expected to experience stiff rivalry in this vendor sector, this would give Mr.

Amana with accurate information regarding the acceptability of the good or service of the

merchandise in the targeted regions, allowing him to tailor advertising strategies to boost

consumer recognition and engagement in the big scheme of things.

Mr. Amana could contemplate transitioning to a separate web retailer for Amana Treasures

following considerably boosting the company's recognition of the branding in the specific

customers for the initial 1-2 years (Liu and Sustik, 2021).

CONCLUSION

Managerial accountancy is a vital element of any firm, according to this paper. It aids

organisations in tracking their fiscal activity and making well-informed choices which boost

company's overall earnings and profitability. Accounting professionals record and process fiscal

information using a range of instruments and approaches, then offer information and suggestions

to firm founders and executives.

REFERENCES

Books and journals

Abou Taleb, M. and Al Farooque, O., 2021. Towards a circular economy for sustainable

development: an application of full cost accounting to municipal waste recyclables.

Journal of Cleaner Production. 280. p.124047.

Al-Dmour, A., Zaidan, H. and Al Natour, A. R., 2021. The impact knowledge management

processes on business performance via the role of accounting information quality as a

mediating factor. VINE Journal of Information and Knowledge Management Systems.

Altukhov, P. V., Predeus, N. V. and Predeus, J. V., 2019, June. Development of the Elements of

the Mechanism Accounting and Analytical Support of Economic Security of

Construction Enterprises. In IOP Conference Series: Earth and Environmental Science

(Vol. 272, No. 3, p. 032205). IOP Publishing.

Andarwati, M., Nirwanto, N. and Darsono, J. T., 2018. Analysis of factors affecting the

successof accounting information systems based on information technology on SME

managementsas accounting informationend user. EJEFAS Journal. (98). pp.97-102.

Borthick, A. F. and Pennington, R. R., 2017. When data become ubiquitous, what becomes of

accounting and assurance?. Journal of Information Systems. 31(3). pp.1-4.

Brink, A. G., Hobson, J. L. and Stevens, D. E., 2017. The effect of high power financial

incentives on excessive risk-taking behavior: An experimental examination. Journal of

Management Accounting Research. 29(1). pp.13-29.

Cleve, B., 2017. Film Production Management: How to Budget, Organize and Successfully

Shoot Your Film. Taylor & Francis.

Dutta, R., Paitya, N. and Majumdar, A., 2020. Ambipolar reduction methodology for SOI tunnel

FETs in low power applications: a performance report. Int J Recent Technol Eng. 8(5).

Emiaso, D. and Egbunike, A. P., 2018. Strategic management accounting practices and

organizational performance of manufacturing firms in Nigeria. Journal of Accounting

and Financial Management. 4(1). pp.10-18.

Giacomini, D., Sicilia, M. and Steccolini, I., 2016. Contextualizing politicians’ uses of

accounting information: reassurance and ammunition. Public Money & Management.

36(7). pp.483-490.

Glushchenko, A. V., Yarkova, I. V. and Kucherova, Y. P., 2017, December. The Role of the

Ecologically-Oriented Accounting Systems from the Perspective of Minimizing the

Strategic Risks in Terms of Ecologizing the Production. In Perspectives on the use of

New Information and Communication Technology (ICT) in the Modern Economy (pp.

741-747). Springer, Cham.

Hyndman, N., 2016. Accrual accounting, politicians and the UK—with the benefit of hindsight.

Public Money & Management. 36(7). pp.477-479.

Kogut, O. Y., Janshanlo, R. E. and Czerewacz-Filipowicz, K., 2020. Human capital accounting

issues in the digital economy. In Digital Transformation of the Economy: Challenges,

Trends and New Opportunities (pp. 296-305). Springer, Cham.

Kramer, S., Maas, V. S. and Van Rinsum, M., 2016. Relative performance information, rank

ordering and employee performance: A research note. Management Accounting

Research. 33. pp.16-24.

Books and journals

Abou Taleb, M. and Al Farooque, O., 2021. Towards a circular economy for sustainable

development: an application of full cost accounting to municipal waste recyclables.

Journal of Cleaner Production. 280. p.124047.

Al-Dmour, A., Zaidan, H. and Al Natour, A. R., 2021. The impact knowledge management

processes on business performance via the role of accounting information quality as a

mediating factor. VINE Journal of Information and Knowledge Management Systems.

Altukhov, P. V., Predeus, N. V. and Predeus, J. V., 2019, June. Development of the Elements of

the Mechanism Accounting and Analytical Support of Economic Security of

Construction Enterprises. In IOP Conference Series: Earth and Environmental Science

(Vol. 272, No. 3, p. 032205). IOP Publishing.

Andarwati, M., Nirwanto, N. and Darsono, J. T., 2018. Analysis of factors affecting the

successof accounting information systems based on information technology on SME

managementsas accounting informationend user. EJEFAS Journal. (98). pp.97-102.

Borthick, A. F. and Pennington, R. R., 2017. When data become ubiquitous, what becomes of

accounting and assurance?. Journal of Information Systems. 31(3). pp.1-4.

Brink, A. G., Hobson, J. L. and Stevens, D. E., 2017. The effect of high power financial

incentives on excessive risk-taking behavior: An experimental examination. Journal of

Management Accounting Research. 29(1). pp.13-29.

Cleve, B., 2017. Film Production Management: How to Budget, Organize and Successfully

Shoot Your Film. Taylor & Francis.

Dutta, R., Paitya, N. and Majumdar, A., 2020. Ambipolar reduction methodology for SOI tunnel

FETs in low power applications: a performance report. Int J Recent Technol Eng. 8(5).

Emiaso, D. and Egbunike, A. P., 2018. Strategic management accounting practices and

organizational performance of manufacturing firms in Nigeria. Journal of Accounting

and Financial Management. 4(1). pp.10-18.

Giacomini, D., Sicilia, M. and Steccolini, I., 2016. Contextualizing politicians’ uses of

accounting information: reassurance and ammunition. Public Money & Management.

36(7). pp.483-490.

Glushchenko, A. V., Yarkova, I. V. and Kucherova, Y. P., 2017, December. The Role of the

Ecologically-Oriented Accounting Systems from the Perspective of Minimizing the

Strategic Risks in Terms of Ecologizing the Production. In Perspectives on the use of

New Information and Communication Technology (ICT) in the Modern Economy (pp.

741-747). Springer, Cham.

Hyndman, N., 2016. Accrual accounting, politicians and the UK—with the benefit of hindsight.

Public Money & Management. 36(7). pp.477-479.

Kogut, O. Y., Janshanlo, R. E. and Czerewacz-Filipowicz, K., 2020. Human capital accounting

issues in the digital economy. In Digital Transformation of the Economy: Challenges,

Trends and New Opportunities (pp. 296-305). Springer, Cham.

Kramer, S., Maas, V. S. and Van Rinsum, M., 2016. Relative performance information, rank

ordering and employee performance: A research note. Management Accounting

Research. 33. pp.16-24.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.