Management Accounting I - Conventional Costing vs Activity Based Costing

VerifiedAdded on 2023/06/07

|9

|1905

|152

AI Summary

This article discusses the difference between conventional costing and activity based costing in Management Accounting I. It explains the advantages of using activity based costing and how to calculate overhead absorption rate and cost per unit. It also covers the challenges of aggressive accounting and budgeting with a cash-flow budget for Skyscraper Hotels and Resorts. The article includes references to relevant books and journals.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting I

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

MAIN BODY..............................................................................................................................................................................................3

REFERENCES............................................................................................................................................................................................1

MAIN BODY..............................................................................................................................................................................................3

REFERENCES............................................................................................................................................................................................1

MAIN BODY

Part A Case Study

1

Conventional costing and activity based costing are two different methods of accounting by which indirect costs of the

products are allocated to such products. Both of these methods are used to determine the production related overhead costs and

allocate it to products on the basis of cost –driver rate. The difference between the two methods are because of their complexities and

accuracy they give. Conventional costing is simple and less accurate while activity based costing is complex and have high accuracy.

The conventional costing assigns indirect costs to products on the basis of average rate that is capricious while in ABC costing

overheads are allocated to activities then to products on the basis of their activities usage, hence the accuracy is high.

There are various advantages that company can have if it uses activity based costing. To begin with the product cost derived

from ABC method is accurate. Adapting to this method brings reliability and accuracy in company’s costing method. This method is

focussed on relationship between cost and effect for incurrence of cost (Quesado and Silva, 2021). The basic idea that the method

follows and forms the basis is that the cost is incurred for the activities and not consumed by the products. A manufacturing

environment that consists of advancements in large amounts out of the total costs this particular method is used to get product costs in

a realistic manner. In firms where there are great diversities in the type of products or services offered or manufactured correct cost to

each can be determined (Al-Dhubaibi, 2021). Further the information about the cost function is gathered from this method. The real

cost nature can be identified and cost reduction becomes easier to identify such activities that are performed by the manufacturing firm

but does not add to the products’ value. The fixed overhead costs can be controlled using ABC method by the managers.

2

Total Overhead Calculation

Overheads $

Staff Support 180000

Part A Case Study

1

Conventional costing and activity based costing are two different methods of accounting by which indirect costs of the

products are allocated to such products. Both of these methods are used to determine the production related overhead costs and

allocate it to products on the basis of cost –driver rate. The difference between the two methods are because of their complexities and

accuracy they give. Conventional costing is simple and less accurate while activity based costing is complex and have high accuracy.

The conventional costing assigns indirect costs to products on the basis of average rate that is capricious while in ABC costing

overheads are allocated to activities then to products on the basis of their activities usage, hence the accuracy is high.

There are various advantages that company can have if it uses activity based costing. To begin with the product cost derived

from ABC method is accurate. Adapting to this method brings reliability and accuracy in company’s costing method. This method is

focussed on relationship between cost and effect for incurrence of cost (Quesado and Silva, 2021). The basic idea that the method

follows and forms the basis is that the cost is incurred for the activities and not consumed by the products. A manufacturing

environment that consists of advancements in large amounts out of the total costs this particular method is used to get product costs in

a realistic manner. In firms where there are great diversities in the type of products or services offered or manufactured correct cost to

each can be determined (Al-Dhubaibi, 2021). Further the information about the cost function is gathered from this method. The real

cost nature can be identified and cost reduction becomes easier to identify such activities that are performed by the manufacturing firm

but does not add to the products’ value. The fixed overhead costs can be controlled using ABC method by the managers.

2

Total Overhead Calculation

Overheads $

Staff Support 180000

In –house Computing 136400

Miscellaneous Office Charges 25600

Total 367600

All the overhead expenses that are incurred by the business are first summed up.

Calculation of Overhead Absorption Rate

Particulars M –commerce

marketing consulting

Accounting

Information Systems

Integration

Total

Production 1900 3100

Computer Hours per

unit

1.05 1.19

Total Computer Hours 1800 2600 4400

Overhead absorption rate = 367600 / 4400 = 83.54

The overheads total has been distributed in the activities of the consultancy firm.

Calculation of Cost per unit

Particulars M –commerce

marketing consulting

Accounting Information

Systems Integration

Overhead (computer hours *

$77.72)

1.05 * 83.54 1.19 * 83.54

Per Unit Cost 87.72 99.41

The cost is calculated for each of the units. Here billable hours in the unit.

3

Miscellaneous Office Charges 25600

Total 367600

All the overhead expenses that are incurred by the business are first summed up.

Calculation of Overhead Absorption Rate

Particulars M –commerce

marketing consulting

Accounting

Information Systems

Integration

Total

Production 1900 3100

Computer Hours per

unit

1.05 1.19

Total Computer Hours 1800 2600 4400

Overhead absorption rate = 367600 / 4400 = 83.54

The overheads total has been distributed in the activities of the consultancy firm.

Calculation of Cost per unit

Particulars M –commerce

marketing consulting

Accounting Information

Systems Integration

Overhead (computer hours *

$77.72)

1.05 * 83.54 1.19 * 83.54

Per Unit Cost 87.72 99.41

The cost is calculated for each of the units. Here billable hours in the unit.

3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

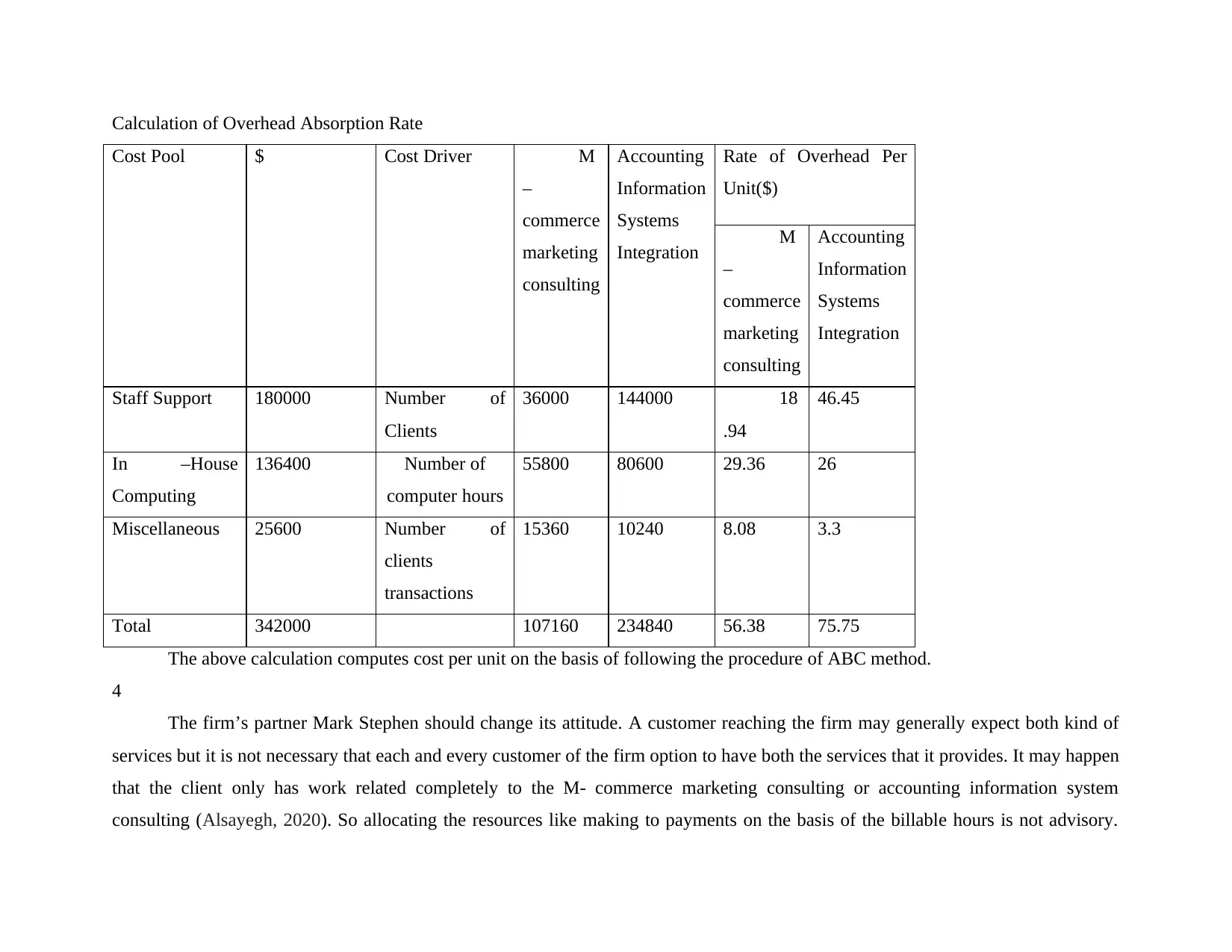

Calculation of Overhead Absorption Rate

Cost Pool $ Cost Driver M

–

commerce

marketing

consulting

Accounting

Information

Systems

Integration

Rate of Overhead Per

Unit($)

M

–

commerce

marketing

consulting

Accounting

Information

Systems

Integration

Staff Support 180000 Number of

Clients

36000 144000 18

.94

46.45

In –House

Computing

136400 Number of

computer hours

55800 80600 29.36 26

Miscellaneous 25600 Number of

clients

transactions

15360 10240 8.08 3.3

Total 342000 107160 234840 56.38 75.75

The above calculation computes cost per unit on the basis of following the procedure of ABC method.

4

The firm’s partner Mark Stephen should change its attitude. A customer reaching the firm may generally expect both kind of

services but it is not necessary that each and every customer of the firm option to have both the services that it provides. It may happen

that the client only has work related completely to the M- commerce marketing consulting or accounting information system

consulting (Alsayegh, 2020). So allocating the resources like making to payments on the basis of the billable hours is not advisory.

Cost Pool $ Cost Driver M

–

commerce

marketing

consulting

Accounting

Information

Systems

Integration

Rate of Overhead Per

Unit($)

M

–

commerce

marketing

consulting

Accounting

Information

Systems

Integration

Staff Support 180000 Number of

Clients

36000 144000 18

.94

46.45

In –House

Computing

136400 Number of

computer hours

55800 80600 29.36 26

Miscellaneous 25600 Number of

clients

transactions

15360 10240 8.08 3.3

Total 342000 107160 234840 56.38 75.75

The above calculation computes cost per unit on the basis of following the procedure of ABC method.

4

The firm’s partner Mark Stephen should change its attitude. A customer reaching the firm may generally expect both kind of

services but it is not necessary that each and every customer of the firm option to have both the services that it provides. It may happen

that the client only has work related completely to the M- commerce marketing consulting or accounting information system

consulting (Alsayegh, 2020). So allocating the resources like making to payments on the basis of the billable hours is not advisory.

The professional time consumed for each of the department should be calculated separately so that the over payments to the activity

can be eliminated. If it is assumed by default that each customer of the company seeks both the services and in reality only one of the

service is used by the buyer, then the company will distribute the professional hours cost for both the services. Hence to sum up the

payments of the professional hours consumed must be allocated on the basis of the actual amount of hours worked by each service

department.

5

Aggressive accounting is a type of accounting practice that is specifically designed for the purpose of overstating financial

performance of a company. This type of accounting practice is similar to another practice that is creative accounting. Creative

accounting means delaying in recognizing loss can be done by the company. Spark and shipper company will hide the expenses it

incurs and represent an inflated price of earnings if it follows this practice.it is opposite of conservative accounting procedure. It is not

recommended for the company to use aggressive expansion strategy as there a number of challenges that are to be faced by the

business if it is decided to have aggressive expansion. The company will not find itself capable to meeting the demands of its new

customers (Tew and et.al., 2020). It will end up in having shortage of cash balances, requiring business to borrow funds in order to

meet its requirements. The capital requirements rise significantly with aggressive expansion techniques. The control over the business

activities may lose as it is required to delegate the activities and work of the business more importantly for the purpose of expansion.

Also there will be a huge increase in the potentiality to incur losses because of the adverse result compromise with the quality of

products and productivity of the company overall.

The fall in levels of employee morale is the biggest disadvantage of the process. Employees are one of the most essential

element of the company whose contribution to the success of the company is maximum. The most crucial challenge any enterprise

faces during its excessive growth is reduction in the employee morale. Internal reconstruction takes place while the company

experience quick growth that forms the reason behind cross – departmental disorganization and burnout of employees. Losing sight of

liquid flows is another challenge. One of the another adverse impact of aggressiveness nature of growth is high levels of employee

can be eliminated. If it is assumed by default that each customer of the company seeks both the services and in reality only one of the

service is used by the buyer, then the company will distribute the professional hours cost for both the services. Hence to sum up the

payments of the professional hours consumed must be allocated on the basis of the actual amount of hours worked by each service

department.

5

Aggressive accounting is a type of accounting practice that is specifically designed for the purpose of overstating financial

performance of a company. This type of accounting practice is similar to another practice that is creative accounting. Creative

accounting means delaying in recognizing loss can be done by the company. Spark and shipper company will hide the expenses it

incurs and represent an inflated price of earnings if it follows this practice.it is opposite of conservative accounting procedure. It is not

recommended for the company to use aggressive expansion strategy as there a number of challenges that are to be faced by the

business if it is decided to have aggressive expansion. The company will not find itself capable to meeting the demands of its new

customers (Tew and et.al., 2020). It will end up in having shortage of cash balances, requiring business to borrow funds in order to

meet its requirements. The capital requirements rise significantly with aggressive expansion techniques. The control over the business

activities may lose as it is required to delegate the activities and work of the business more importantly for the purpose of expansion.

Also there will be a huge increase in the potentiality to incur losses because of the adverse result compromise with the quality of

products and productivity of the company overall.

The fall in levels of employee morale is the biggest disadvantage of the process. Employees are one of the most essential

element of the company whose contribution to the success of the company is maximum. The most crucial challenge any enterprise

faces during its excessive growth is reduction in the employee morale. Internal reconstruction takes place while the company

experience quick growth that forms the reason behind cross – departmental disorganization and burnout of employees. Losing sight of

liquid flows is another challenge. One of the another adverse impact of aggressiveness nature of growth is high levels of employee

turnover ratio, making visibility in relation to cash flow vulnerable. The persons designated with the task of cash management may

leave and there creates the lack of communication regarding the person currently managing the cash flows of the company.

Furthermore, it results in a situation where company ends up in employing larger number of employees then it can actually

afford. Having a perspective of aggressive expansion of one service calls the need for hiring large number of employees in the view of

handling the increase level of operations increasing with the growth of company (Ware and et.al., 2020). Recruiting employees of

large number means expense incurrence over the training of employees, making payments against the expenses of benefits, holidays,

leave pay. Hence, over hiring of employees can be every costly for the firm.

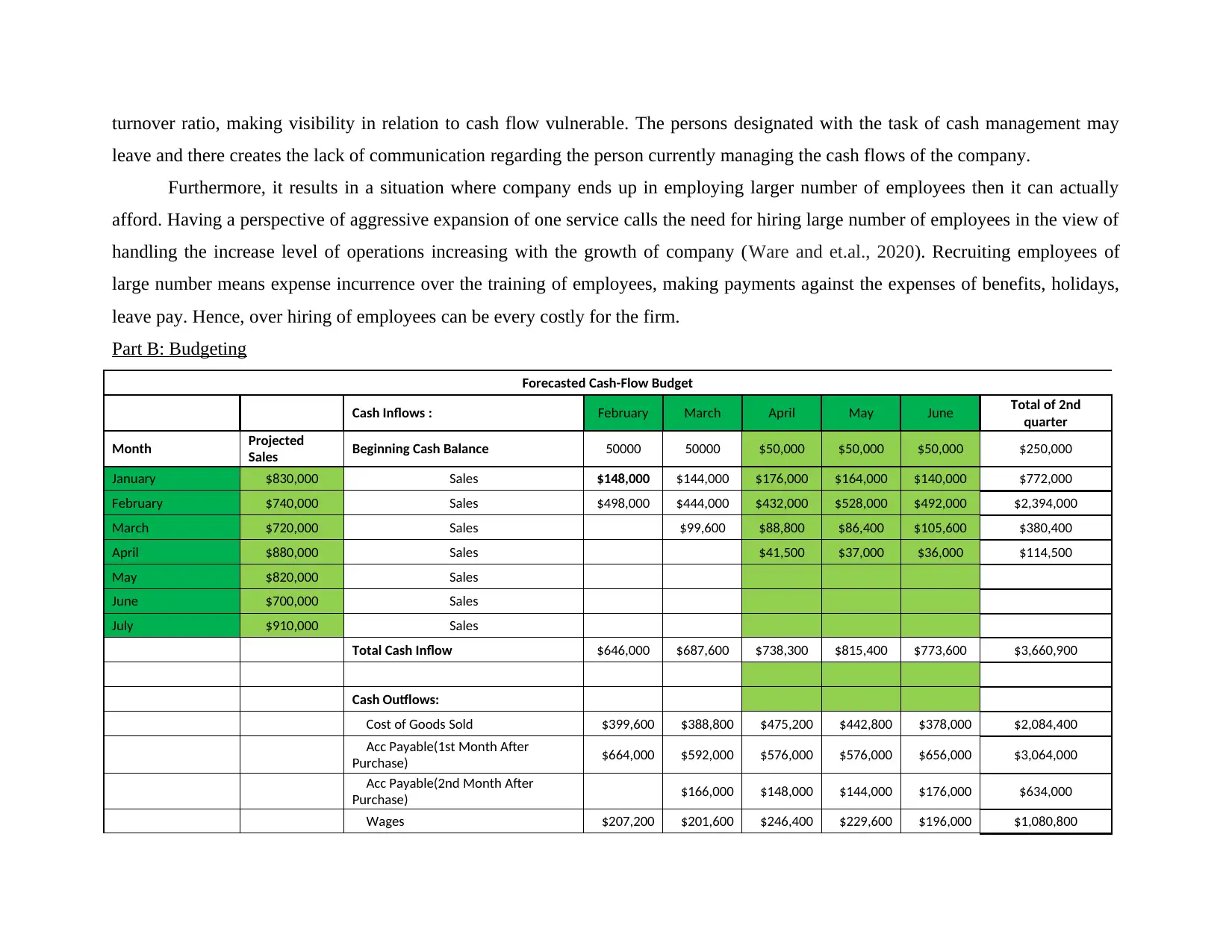

Part B: Budgeting

Forecasted Cash-Flow Budget

Cash Inflows : February March April May June Total of 2nd

quarter

Month Projected

Sales Beginning Cash Balance 50000 50000 $50,000 $50,000 $50,000 $250,000

January $830,000 Sales $148,000 $144,000 $176,000 $164,000 $140,000 $772,000

February $740,000 Sales $498,000 $444,000 $432,000 $528,000 $492,000 $2,394,000

March $720,000 Sales $99,600 $88,800 $86,400 $105,600 $380,400

April $880,000 Sales $41,500 $37,000 $36,000 $114,500

May $820,000 Sales

June $700,000 Sales

July $910,000 Sales

Total Cash Inflow $646,000 $687,600 $738,300 $815,400 $773,600 $3,660,900

Cash Outflows:

Cost of Goods Sold $399,600 $388,800 $475,200 $442,800 $378,000 $2,084,400

Acc Payable(1st Month After

Purchase) $664,000 $592,000 $576,000 $576,000 $656,000 $3,064,000

Acc Payable(2nd Month After

Purchase) $166,000 $148,000 $144,000 $176,000 $634,000

Wages $207,200 $201,600 $246,400 $229,600 $196,000 $1,080,800

leave and there creates the lack of communication regarding the person currently managing the cash flows of the company.

Furthermore, it results in a situation where company ends up in employing larger number of employees then it can actually

afford. Having a perspective of aggressive expansion of one service calls the need for hiring large number of employees in the view of

handling the increase level of operations increasing with the growth of company (Ware and et.al., 2020). Recruiting employees of

large number means expense incurrence over the training of employees, making payments against the expenses of benefits, holidays,

leave pay. Hence, over hiring of employees can be every costly for the firm.

Part B: Budgeting

Forecasted Cash-Flow Budget

Cash Inflows : February March April May June Total of 2nd

quarter

Month Projected

Sales Beginning Cash Balance 50000 50000 $50,000 $50,000 $50,000 $250,000

January $830,000 Sales $148,000 $144,000 $176,000 $164,000 $140,000 $772,000

February $740,000 Sales $498,000 $444,000 $432,000 $528,000 $492,000 $2,394,000

March $720,000 Sales $99,600 $88,800 $86,400 $105,600 $380,400

April $880,000 Sales $41,500 $37,000 $36,000 $114,500

May $820,000 Sales

June $700,000 Sales

July $910,000 Sales

Total Cash Inflow $646,000 $687,600 $738,300 $815,400 $773,600 $3,660,900

Cash Outflows:

Cost of Goods Sold $399,600 $388,800 $475,200 $442,800 $378,000 $2,084,400

Acc Payable(1st Month After

Purchase) $664,000 $592,000 $576,000 $576,000 $656,000 $3,064,000

Acc Payable(2nd Month After

Purchase) $166,000 $148,000 $144,000 $176,000 $634,000

Wages $207,200 $201,600 $246,400 $229,600 $196,000 $1,080,800

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

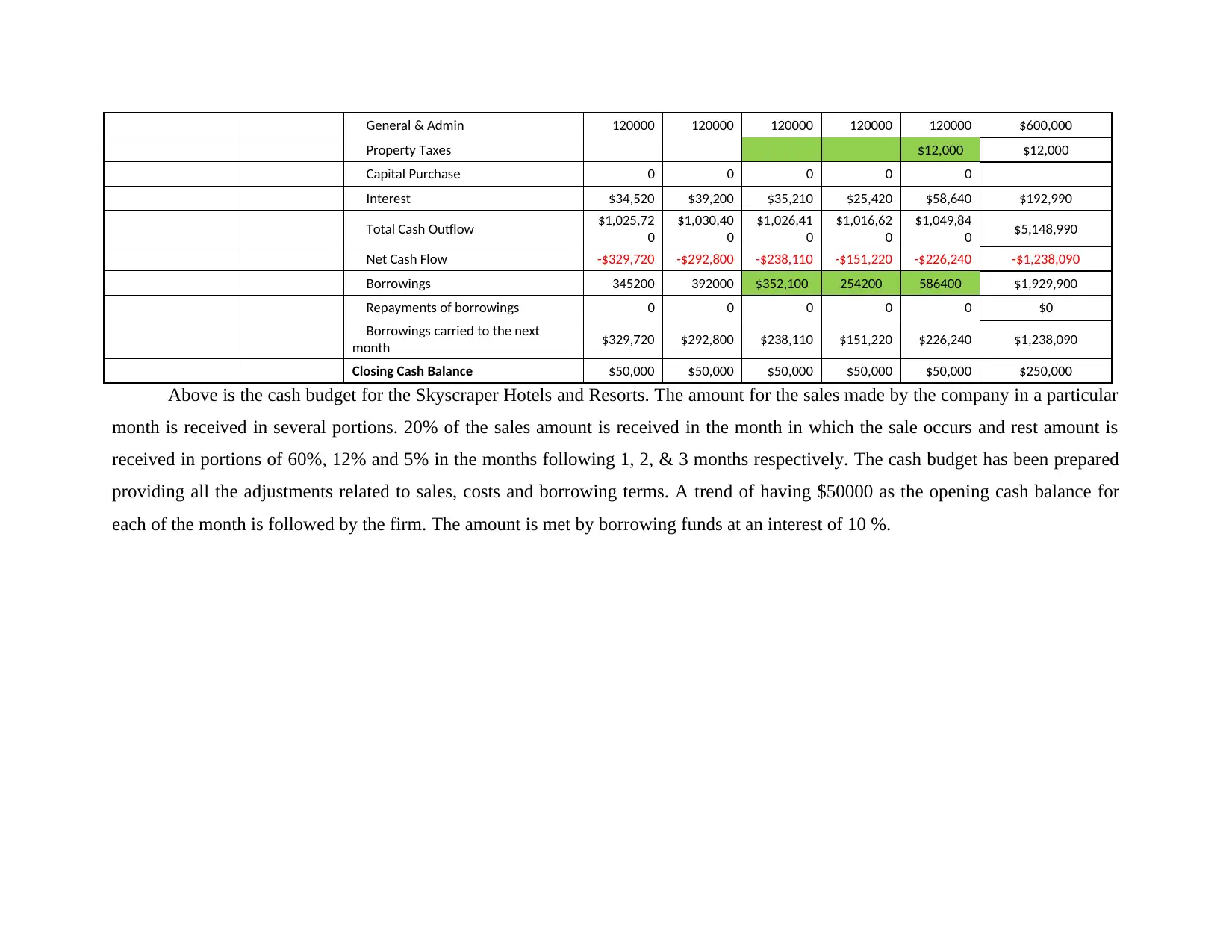

General & Admin 120000 120000 120000 120000 120000 $600,000

Property Taxes $12,000 $12,000

Capital Purchase 0 0 0 0 0

Interest $34,520 $39,200 $35,210 $25,420 $58,640 $192,990

Total Cash Outflow $1,025,72

0

$1,030,40

0

$1,026,41

0

$1,016,62

0

$1,049,84

0 $5,148,990

Net Cash Flow -$329,720 -$292,800 -$238,110 -$151,220 -$226,240 -$1,238,090

Borrowings 345200 392000 $352,100 254200 586400 $1,929,900

Repayments of borrowings 0 0 0 0 0 $0

Borrowings carried to the next

month $329,720 $292,800 $238,110 $151,220 $226,240 $1,238,090

Closing Cash Balance $50,000 $50,000 $50,000 $50,000 $50,000 $250,000

Above is the cash budget for the Skyscraper Hotels and Resorts. The amount for the sales made by the company in a particular

month is received in several portions. 20% of the sales amount is received in the month in which the sale occurs and rest amount is

received in portions of 60%, 12% and 5% in the months following 1, 2, & 3 months respectively. The cash budget has been prepared

providing all the adjustments related to sales, costs and borrowing terms. A trend of having $50000 as the opening cash balance for

each of the month is followed by the firm. The amount is met by borrowing funds at an interest of 10 %.

Property Taxes $12,000 $12,000

Capital Purchase 0 0 0 0 0

Interest $34,520 $39,200 $35,210 $25,420 $58,640 $192,990

Total Cash Outflow $1,025,72

0

$1,030,40

0

$1,026,41

0

$1,016,62

0

$1,049,84

0 $5,148,990

Net Cash Flow -$329,720 -$292,800 -$238,110 -$151,220 -$226,240 -$1,238,090

Borrowings 345200 392000 $352,100 254200 586400 $1,929,900

Repayments of borrowings 0 0 0 0 0 $0

Borrowings carried to the next

month $329,720 $292,800 $238,110 $151,220 $226,240 $1,238,090

Closing Cash Balance $50,000 $50,000 $50,000 $50,000 $50,000 $250,000

Above is the cash budget for the Skyscraper Hotels and Resorts. The amount for the sales made by the company in a particular

month is received in several portions. 20% of the sales amount is received in the month in which the sale occurs and rest amount is

received in portions of 60%, 12% and 5% in the months following 1, 2, & 3 months respectively. The cash budget has been prepared

providing all the adjustments related to sales, costs and borrowing terms. A trend of having $50000 as the opening cash balance for

each of the month is followed by the firm. The amount is met by borrowing funds at an interest of 10 %.

REFERENCES

Books and Journals

Quesado, P. and Silva, R., 2021. Activity-based costing (ABC) and its implication for open

innovation. Journal of Open Innovation: Technology, Market, and Complexity. 7(1).

p.41.

Alsayegh, M. F., 2020. Activity Based Costing around the World: Adoption, Implementation,

Outcomes and Criticism. Journal of Accounting and Finance in Emerging

Economies. 6(1). pp.251-262.

Al-Dhubaibi, A., 2021. Optimizing the value of activity based costing system: The role of

successful implementation. Management Science Letters. 11(1). pp.179-186.

Tew, B. Y. and et.al., 2020. Patient-derived xenografts of central nervous system metastasis

reveal expansion of aggressive minor clones. Neuro-oncology. 22(1). pp.70-83.

Ware, M. B. and et.al., 2020. Suppressive myeloid cells are expanded by biliary tract cancer-

derived cytokines in vitro and associate with aggressive disease. British journal of

cancer. 123(9). pp.1377-1386.

1

Books and Journals

Quesado, P. and Silva, R., 2021. Activity-based costing (ABC) and its implication for open

innovation. Journal of Open Innovation: Technology, Market, and Complexity. 7(1).

p.41.

Alsayegh, M. F., 2020. Activity Based Costing around the World: Adoption, Implementation,

Outcomes and Criticism. Journal of Accounting and Finance in Emerging

Economies. 6(1). pp.251-262.

Al-Dhubaibi, A., 2021. Optimizing the value of activity based costing system: The role of

successful implementation. Management Science Letters. 11(1). pp.179-186.

Tew, B. Y. and et.al., 2020. Patient-derived xenografts of central nervous system metastasis

reveal expansion of aggressive minor clones. Neuro-oncology. 22(1). pp.70-83.

Ware, M. B. and et.al., 2020. Suppressive myeloid cells are expanded by biliary tract cancer-

derived cytokines in vitro and associate with aggressive disease. British journal of

cancer. 123(9). pp.1377-1386.

1

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.