ACC202 Management Accounting Group Assignment - Cost Analysis

VerifiedAdded on 2023/06/07

|16

|1716

|454

Homework Assignment

AI Summary

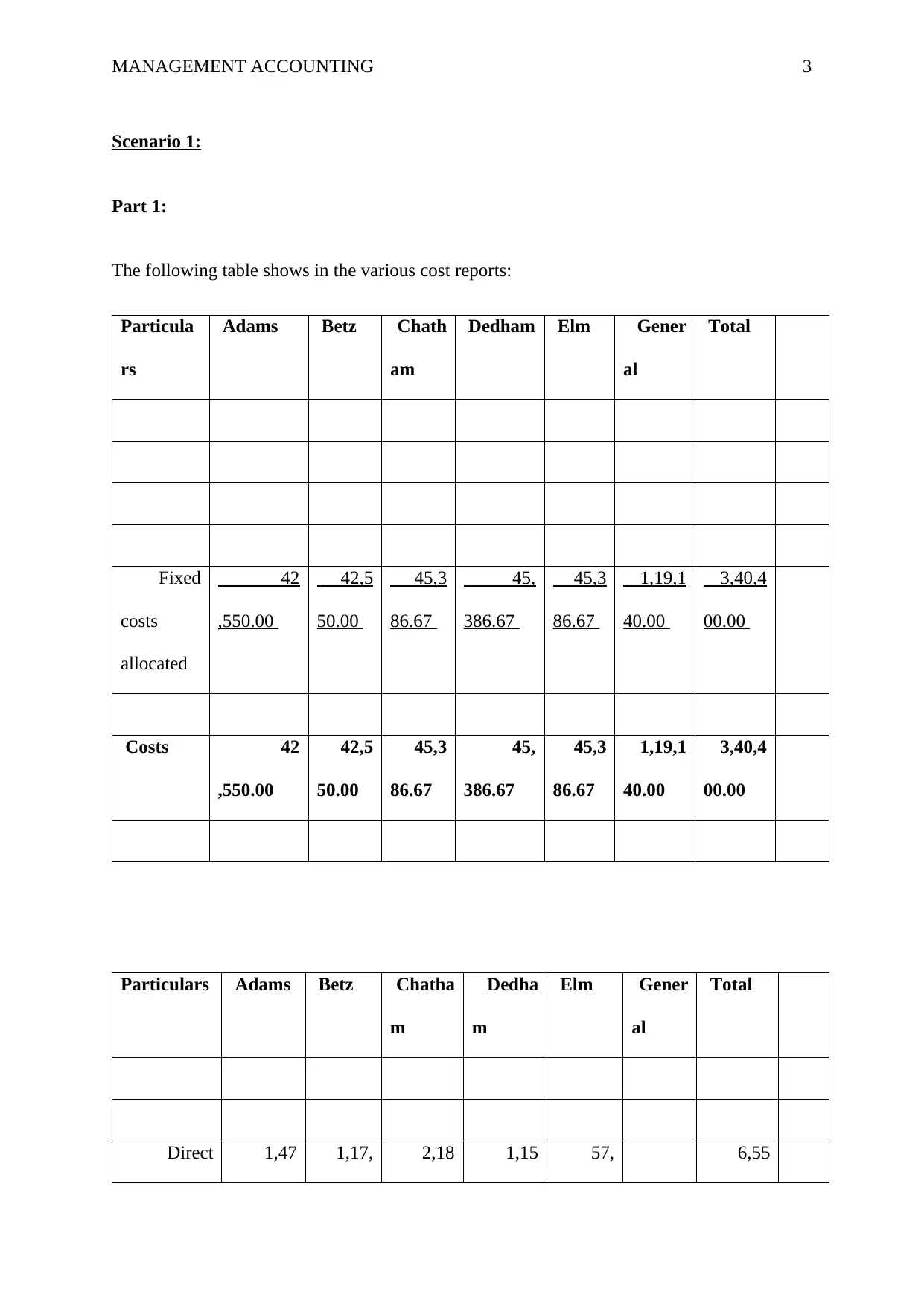

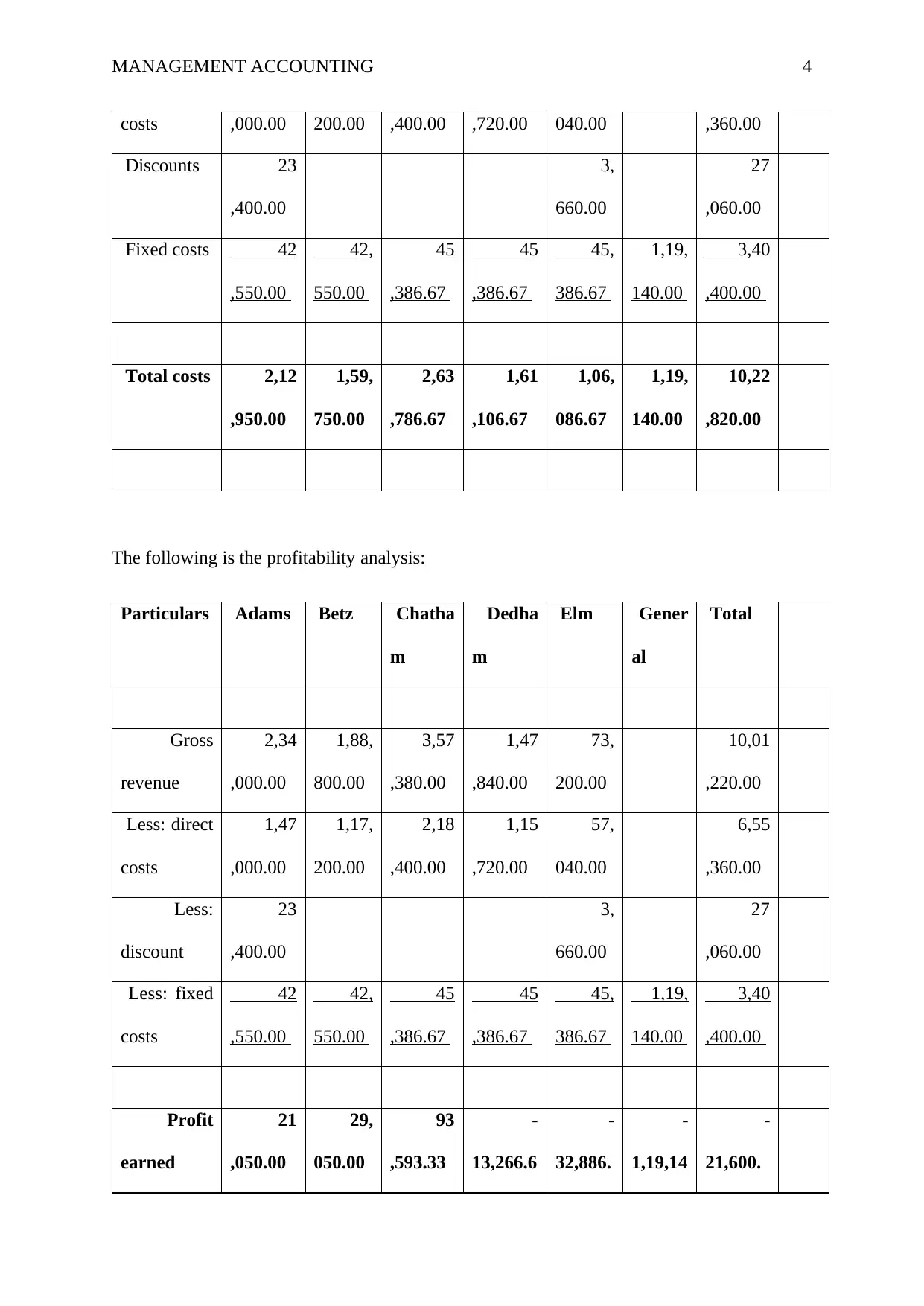

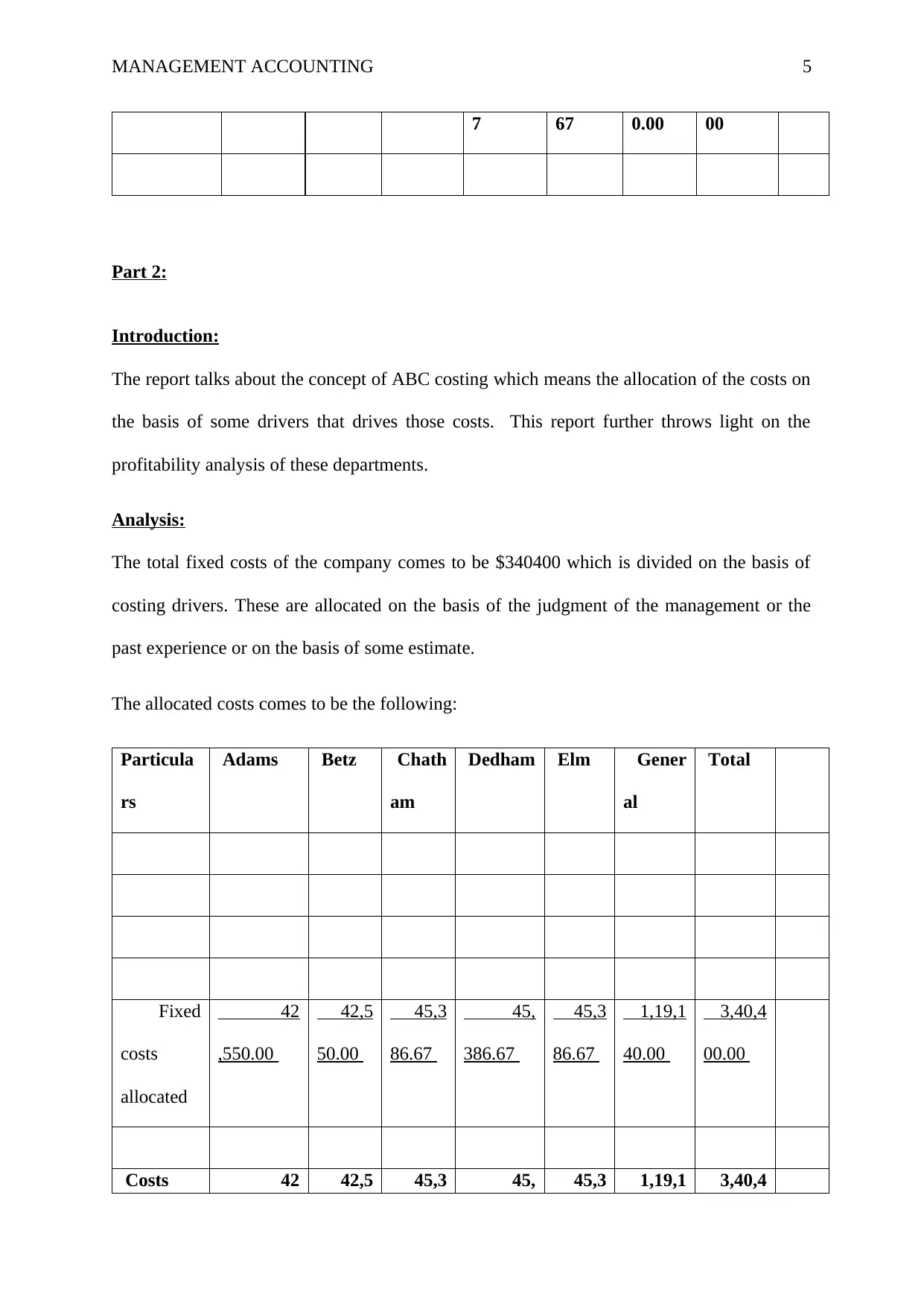

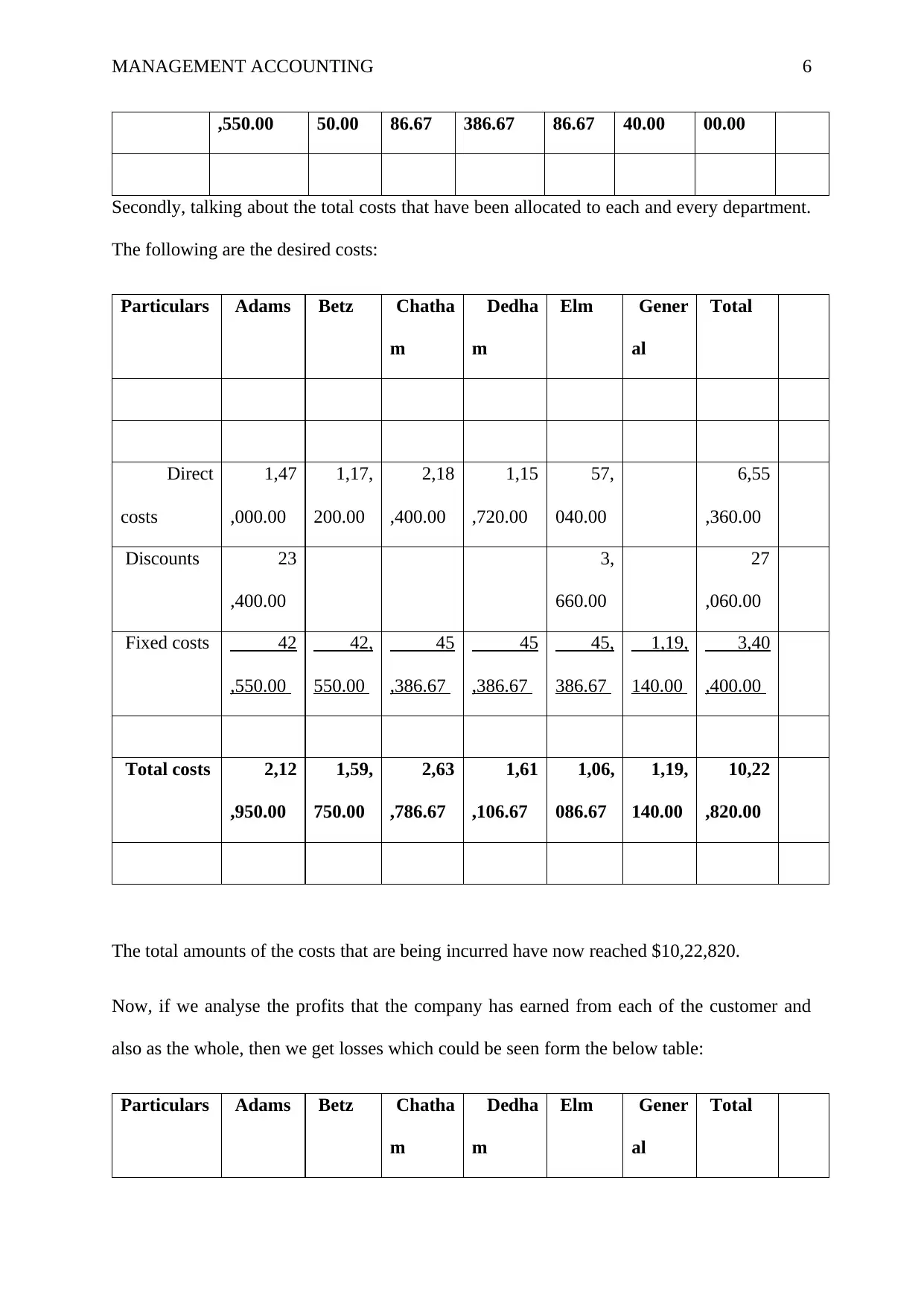

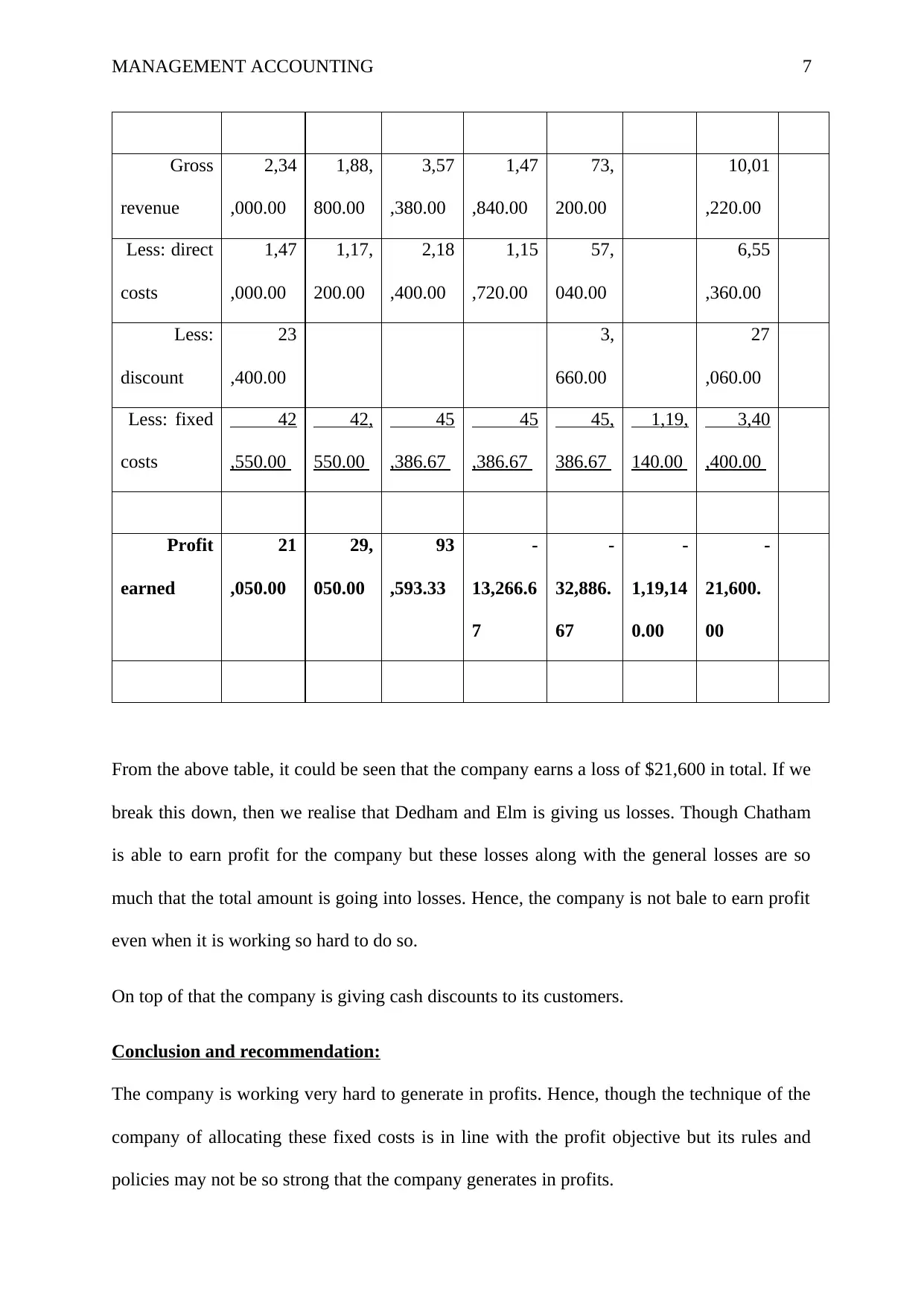

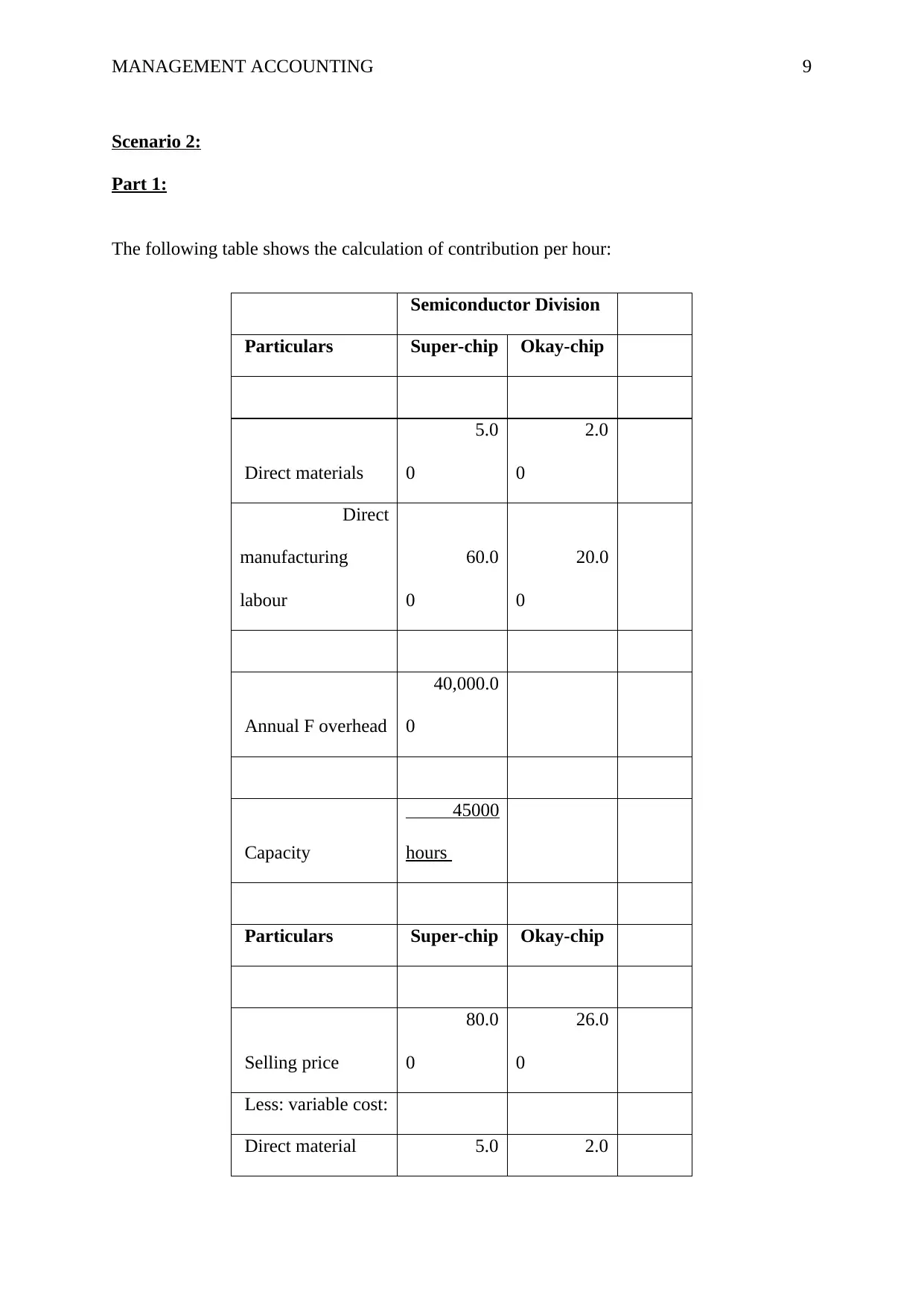

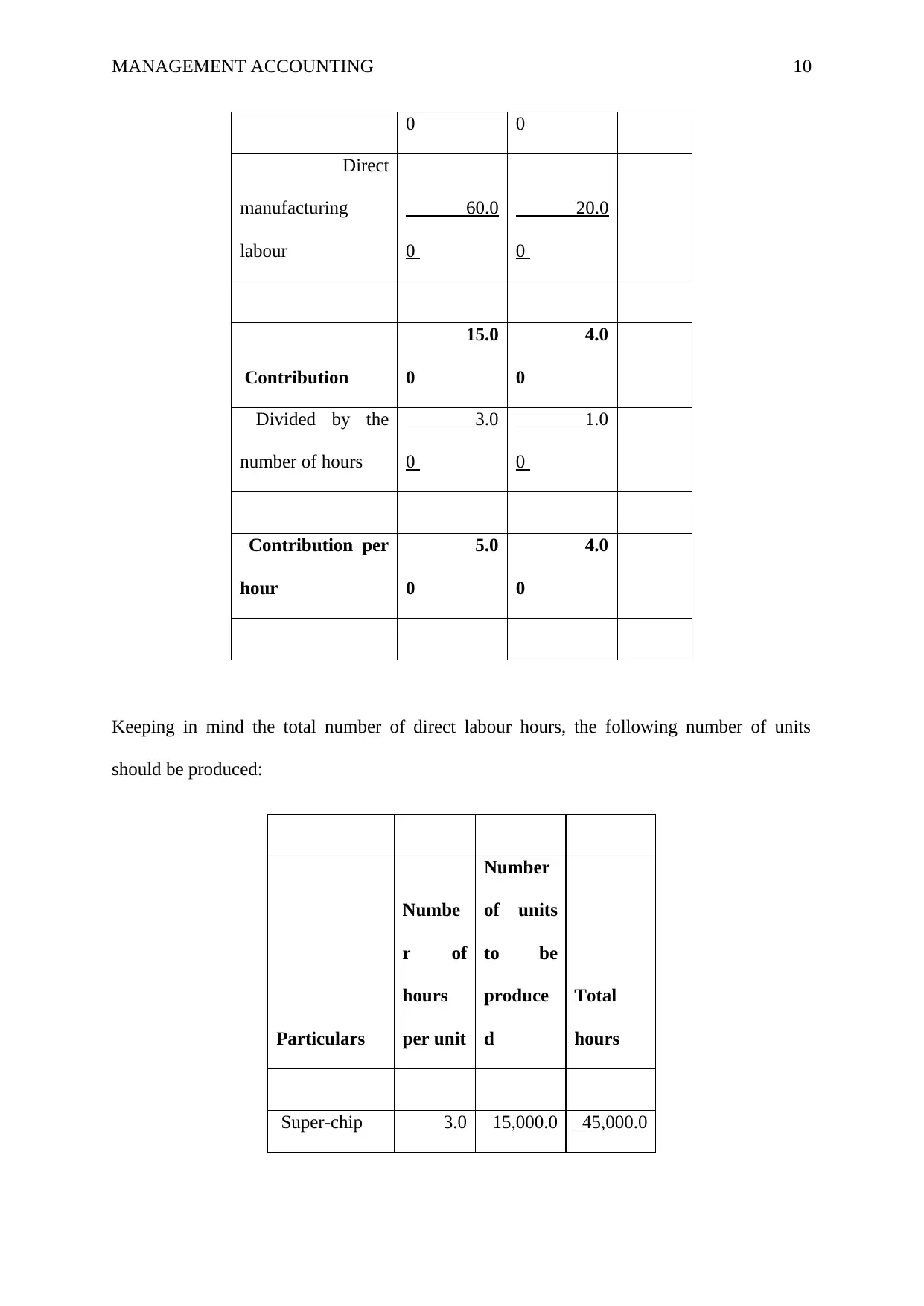

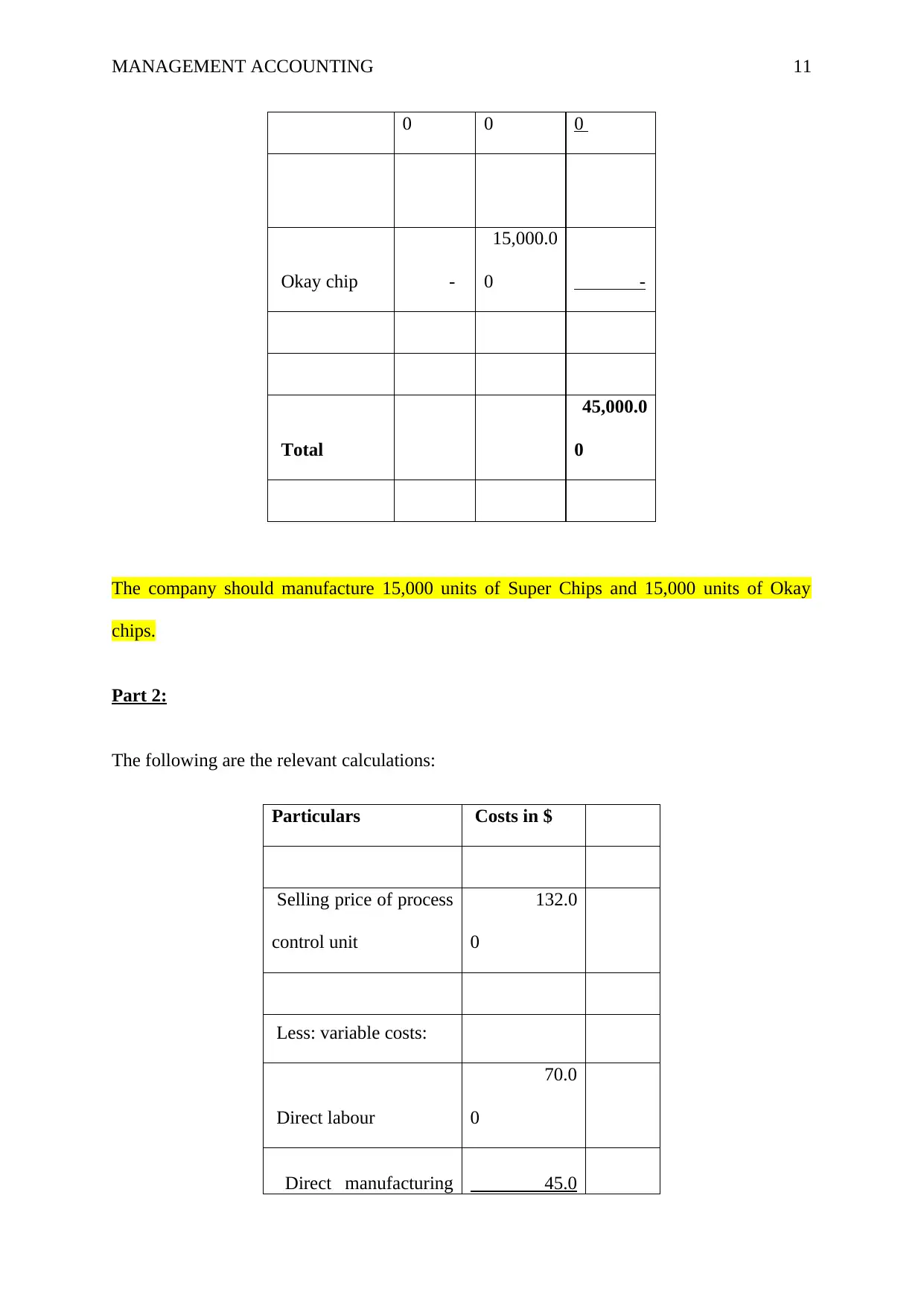

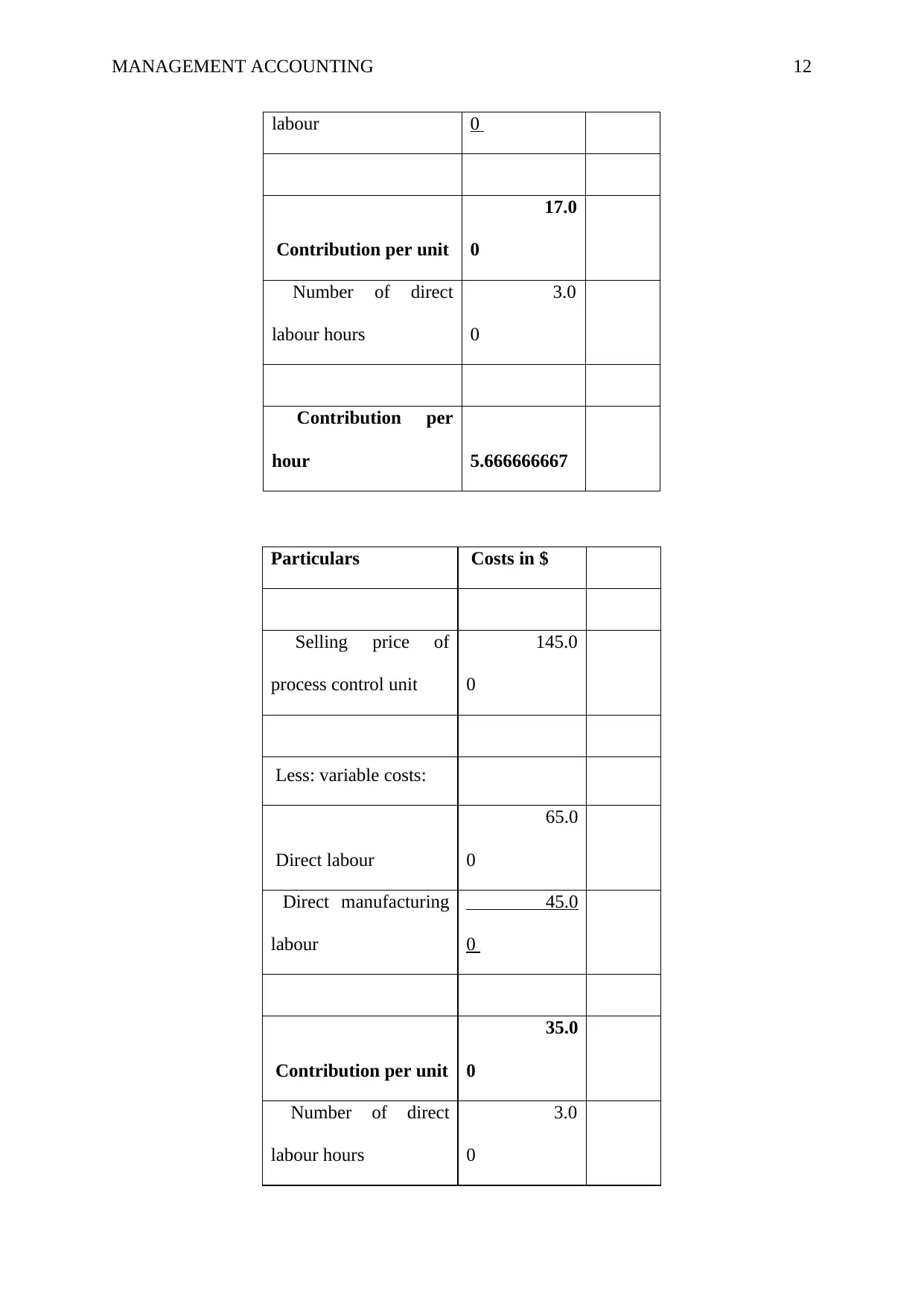

This document presents a comprehensive solution to a management accounting assignment (ACC202) covering two scenarios. Scenario 1 focuses on customer profitability analysis for an interior design business, exploring cost allocation, profit calculations, and recommendations for improvement. It utilizes Activity-Based Costing (ABC) to analyze costs and revenue across different customer segments, identifying loss-making areas and suggesting strategies to enhance profitability, such as increasing charges and reducing discounts. Scenario 2 delves into a semiconductor division, addressing production decisions based on contribution per hour, transfer pricing, and goal congruence. The analysis includes calculating contribution per hour, determining optimal production quantities for different chip types, and evaluating the impact of internal transfers on overall profitability. It emphasizes the importance of aligning decisions with the overall goals of the company, recommending transfer pricing strategies to maximize combined contributions and achieve goal congruence between divisions.

1 out of 16

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.