Management Accounting Application at Prime Furniture - Report

VerifiedAdded on 2023/06/18

|27

|3194

|314

Report

AI Summary

This report delves into the application of management accounting principles within Prime Furniture, a UK-based furniture company. It covers various management accounting techniques, including cost analysis using marginal and absorption costing, alongside an income statement. The report also explores different planning tools employed for budgetary control, highlighting their advantages and disadvantages. Furthermore, it compares Prime Furniture's financial performance with that of Capital Joinery, another organization, to illustrate the impact of effective management accounting practices in responding to financial challenges. Key areas of focus include financial planning, cost analysis, budgeting, and cash flow management, providing a comprehensive overview of how management accounting contributes to strategic decision-making and financial stability.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Task 2...............................................................................................................................................3

P3 Cost analysis using appropriate techniques of marginal and absorption costing and income

statement......................................................................................................................................3

M2 Management accounting techniques for financial reporting documents...............................3

P4 Advantages and disadvantages of different types of planning tools used for budgetary

control..........................................................................................................................................5

M3 Use of different planning tools and their application in preparing and forecasting of

budgets.........................................................................................................................................9

P5 Comparison of organisations using management accounting for responding to financial

problems......................................................................................................................................9

M4 Management accounting leading to success in response to financial problems in

organisation................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

Task 2...............................................................................................................................................3

P3 Cost analysis using appropriate techniques of marginal and absorption costing and income

statement......................................................................................................................................3

M2 Management accounting techniques for financial reporting documents...............................3

P4 Advantages and disadvantages of different types of planning tools used for budgetary

control..........................................................................................................................................5

M3 Use of different planning tools and their application in preparing and forecasting of

budgets.........................................................................................................................................9

P5 Comparison of organisations using management accounting for responding to financial

problems......................................................................................................................................9

M4 Management accounting leading to success in response to financial problems in

organisation................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

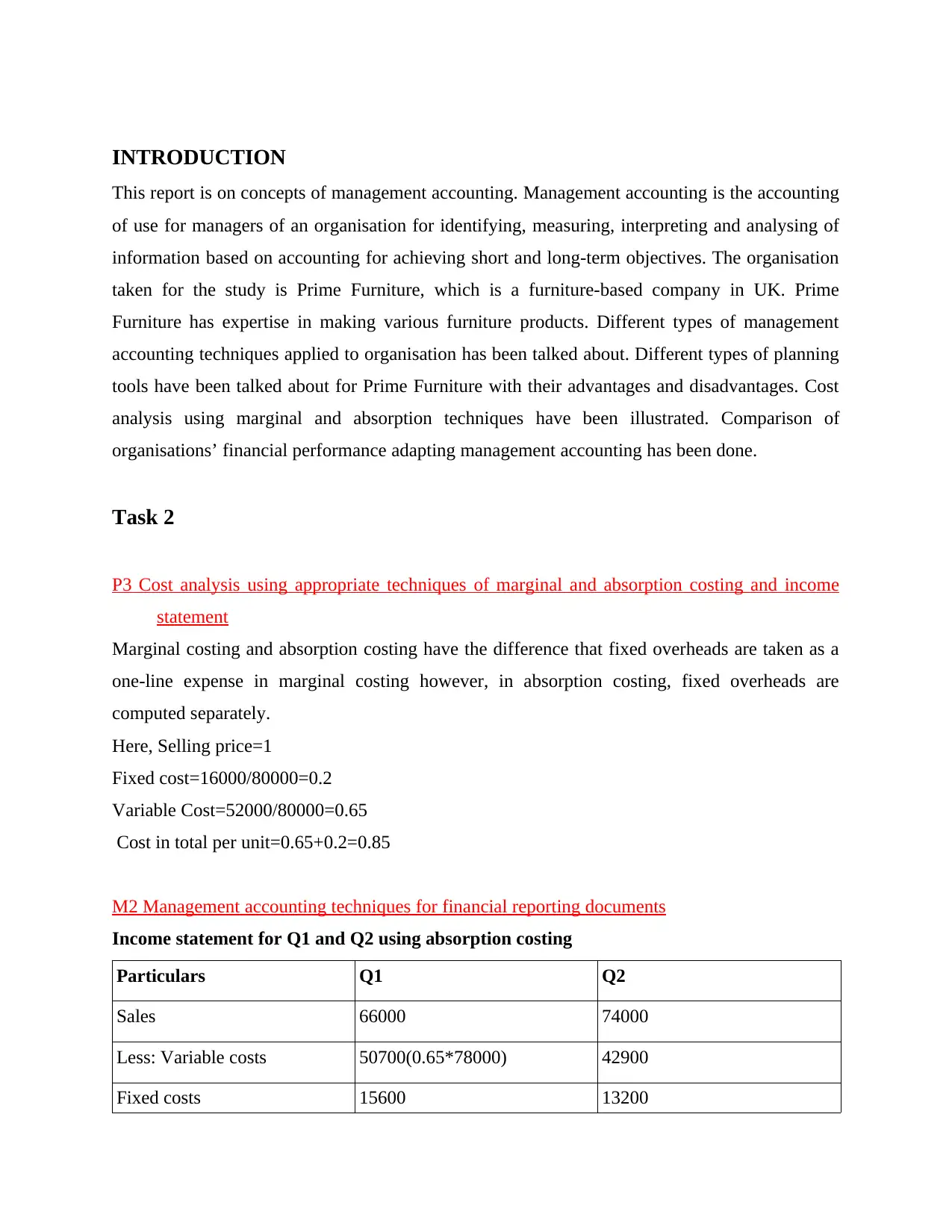

INTRODUCTION

This report is on concepts of management accounting. Management accounting is the accounting

of use for managers of an organisation for identifying, measuring, interpreting and analysing of

information based on accounting for achieving short and long-term objectives. The organisation

taken for the study is Prime Furniture, which is a furniture-based company in UK. Prime

Furniture has expertise in making various furniture products. Different types of management

accounting techniques applied to organisation has been talked about. Different types of planning

tools have been talked about for Prime Furniture with their advantages and disadvantages. Cost

analysis using marginal and absorption techniques have been illustrated. Comparison of

organisations’ financial performance adapting management accounting has been done.

Task 2

P3 Cost analysis using appropriate techniques of marginal and absorption costing and income

statement

Marginal costing and absorption costing have the difference that fixed overheads are taken as a

one-line expense in marginal costing however, in absorption costing, fixed overheads are

computed separately.

Here, Selling price=1

Fixed cost=16000/80000=0.2

Variable Cost=52000/80000=0.65

Cost in total per unit=0.65+0.2=0.85

M2 Management accounting techniques for financial reporting documents

Income statement for Q1 and Q2 using absorption costing

Particulars Q1 Q2

Sales 66000 74000

Less: Variable costs 50700(0.65*78000) 42900

Fixed costs 15600 13200

This report is on concepts of management accounting. Management accounting is the accounting

of use for managers of an organisation for identifying, measuring, interpreting and analysing of

information based on accounting for achieving short and long-term objectives. The organisation

taken for the study is Prime Furniture, which is a furniture-based company in UK. Prime

Furniture has expertise in making various furniture products. Different types of management

accounting techniques applied to organisation has been talked about. Different types of planning

tools have been talked about for Prime Furniture with their advantages and disadvantages. Cost

analysis using marginal and absorption techniques have been illustrated. Comparison of

organisations’ financial performance adapting management accounting has been done.

Task 2

P3 Cost analysis using appropriate techniques of marginal and absorption costing and income

statement

Marginal costing and absorption costing have the difference that fixed overheads are taken as a

one-line expense in marginal costing however, in absorption costing, fixed overheads are

computed separately.

Here, Selling price=1

Fixed cost=16000/80000=0.2

Variable Cost=52000/80000=0.65

Cost in total per unit=0.65+0.2=0.85

M2 Management accounting techniques for financial reporting documents

Income statement for Q1 and Q2 using absorption costing

Particulars Q1 Q2

Sales 66000 74000

Less: Variable costs 50700(0.65*78000) 42900

Fixed costs 15600 13200

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost of Goods for sales 66300(50700+15600) 56100(42900+13200)

Add: Opening stock 0 10200

Less: Closing stock 10200(0.85*12000) 3400(0.85*4000)

COGS 66300-10200=56100 56100+10200-3400=62900

Gross profit 9900(66000-56100) 11100(74000-62900)

Less: Selling and

administration costs

5200 5200

Net Profit 4700 5900

Income statement for Q1 and Q2 using marginal costing

Particulars Q1 Q2

Sales 66000 74000

Less: Variable costs 50700 42900

Add: Opening stock 0 7800

Less: Closing stock 7800(0.65*12000) 2600(0.65*4000)

COGS 50700-7800=42900 48100(42900+7800-2600)

Contribution 23100(66000-42900) 25900(74000-48100)

Less: Fixed and administration

costs

5200 5200

Fixed costs 16000 16000

Net profit 1900 4700

Reconciliation of Profits

Particulars Q1 Q2

Add: Opening stock 0 10200

Less: Closing stock 10200(0.85*12000) 3400(0.85*4000)

COGS 66300-10200=56100 56100+10200-3400=62900

Gross profit 9900(66000-56100) 11100(74000-62900)

Less: Selling and

administration costs

5200 5200

Net Profit 4700 5900

Income statement for Q1 and Q2 using marginal costing

Particulars Q1 Q2

Sales 66000 74000

Less: Variable costs 50700 42900

Add: Opening stock 0 7800

Less: Closing stock 7800(0.65*12000) 2600(0.65*4000)

COGS 50700-7800=42900 48100(42900+7800-2600)

Contribution 23100(66000-42900) 25900(74000-48100)

Less: Fixed and administration

costs

5200 5200

Fixed costs 16000 16000

Net profit 1900 4700

Reconciliation of Profits

Particulars Q1 Q2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Marginal Cost profit 1900 4700

Add: Difference of units

produced

400(2000*0.2) 2800(14000*0.2)

2300 7500

Less: Opening stock 0 2400(12000*0.2)

2300 5100

Add: 2400 800(4000*0.2)

Absorption cost profit 4700 5900

It can be seen profits reported in absorption costing are higher.

P4 Advantages and disadvantages of different types of planning tools used for budgetary control

1. Financial Planning

The income statement, as well as the statement of financial position, are the two most important

statements of finance for shareholders to consider. For assessing the organisation's strengths and

shortcomings, the financial accounts are analysed over several periods. It may be utilised for

evaluation if an organisation’s operational costs are low or high, also the amount of receivables

and debt, fixed assets and variable costs, and, most crucially, the organisation's net gain, which is

utilised by investors and shareholders (Pradhan, Swain and Dash, 2018).

Benefits: a) Financial planning aids in cost projections, which will be useful in future initiatives.

b) Through financial analysis, it gives a look into how organisation can approach a project.

c) Planning financially assists in calculation the right rate of return on projects, and also the

management of cash flow and working capital.

Disadvantages:

a) Planning financially may go awry because of estimates that maybe or may not be sufficiently

right (Cuzdriorean, 2017).

Add: Difference of units

produced

400(2000*0.2) 2800(14000*0.2)

2300 7500

Less: Opening stock 0 2400(12000*0.2)

2300 5100

Add: 2400 800(4000*0.2)

Absorption cost profit 4700 5900

It can be seen profits reported in absorption costing are higher.

P4 Advantages and disadvantages of different types of planning tools used for budgetary control

1. Financial Planning

The income statement, as well as the statement of financial position, are the two most important

statements of finance for shareholders to consider. For assessing the organisation's strengths and

shortcomings, the financial accounts are analysed over several periods. It may be utilised for

evaluation if an organisation’s operational costs are low or high, also the amount of receivables

and debt, fixed assets and variable costs, and, most crucially, the organisation's net gain, which is

utilised by investors and shareholders (Pradhan, Swain and Dash, 2018).

Benefits: a) Financial planning aids in cost projections, which will be useful in future initiatives.

b) Through financial analysis, it gives a look into how organisation can approach a project.

c) Planning financially assists in calculation the right rate of return on projects, and also the

management of cash flow and working capital.

Disadvantages:

a) Planning financially may go awry because of estimates that maybe or may not be sufficiently

right (Cuzdriorean, 2017).

2. Analysis of costs

Raw materials, labour, and other variable charges are only a few of the direct and indirect costs

of production. Costing methods can be used to compute the overall cost of production, which is

then divide by produced total units. This aids in calculating per unit cost of output and also unit

pricing. This has benefited Prime Furniture's in identifying cost-cutting opportunities, for

example switching to a supplier giving low cost tender that meets the exact quality standards.

Different types of costing used in Prime Furniture are:

Standard costing: The costing measure which helps find out whether the system is facing

deviations in performance. It sets costs which are predetermined and thus serve as a standard for

Prime Furniture to check on performance (Pradhan, Swain and Dash, 2018).

Normal costing

Direct costs are assigned to the jobs as they occur. Manufacturing overheads are applied to jobs

by predetermined rates of overheads.

Actual costing

Actual costs assign overheads manufacturing when the actual costs are known. These actual

costs are assigned to jobs.

Job costing: A project being segregated in small parts is known as job and the costs related to

each part of the job whether direct or indirect are covered in job costing. It helps to find out

whether the costs being spent on a project are in controlled manner or not and gives estimate of

the costs which will go in the project (Cuzdriorean, 2017).

Raw materials, labour, and other variable charges are only a few of the direct and indirect costs

of production. Costing methods can be used to compute the overall cost of production, which is

then divide by produced total units. This aids in calculating per unit cost of output and also unit

pricing. This has benefited Prime Furniture's in identifying cost-cutting opportunities, for

example switching to a supplier giving low cost tender that meets the exact quality standards.

Different types of costing used in Prime Furniture are:

Standard costing: The costing measure which helps find out whether the system is facing

deviations in performance. It sets costs which are predetermined and thus serve as a standard for

Prime Furniture to check on performance (Pradhan, Swain and Dash, 2018).

Normal costing

Direct costs are assigned to the jobs as they occur. Manufacturing overheads are applied to jobs

by predetermined rates of overheads.

Actual costing

Actual costs assign overheads manufacturing when the actual costs are known. These actual

costs are assigned to jobs.

Job costing: A project being segregated in small parts is known as job and the costs related to

each part of the job whether direct or indirect are covered in job costing. It helps to find out

whether the costs being spent on a project are in controlled manner or not and gives estimate of

the costs which will go in the project (Cuzdriorean, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

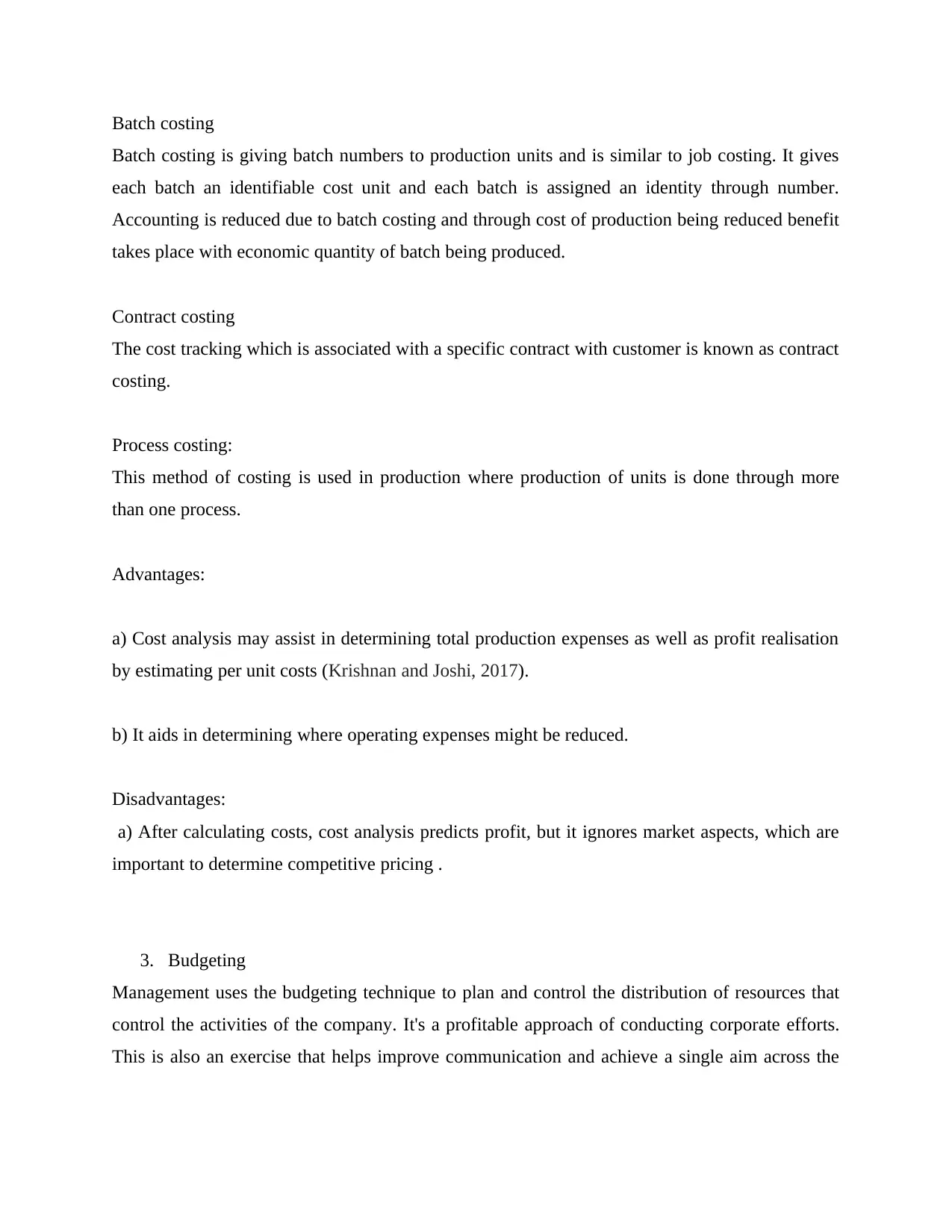

Batch costing

Batch costing is giving batch numbers to production units and is similar to job costing. It gives

each batch an identifiable cost unit and each batch is assigned an identity through number.

Accounting is reduced due to batch costing and through cost of production being reduced benefit

takes place with economic quantity of batch being produced.

Contract costing

The cost tracking which is associated with a specific contract with customer is known as contract

costing.

Process costing:

This method of costing is used in production where production of units is done through more

than one process.

Advantages:

a) Cost analysis may assist in determining total production expenses as well as profit realisation

by estimating per unit costs (Krishnan and Joshi, 2017).

b) It aids in determining where operating expenses might be reduced.

Disadvantages:

a) After calculating costs, cost analysis predicts profit, but it ignores market aspects, which are

important to determine competitive pricing .

3. Budgeting

Management uses the budgeting technique to plan and control the distribution of resources that

control the activities of the company. It's a profitable approach of conducting corporate efforts.

This is also an exercise that helps improve communication and achieve a single aim across the

Batch costing is giving batch numbers to production units and is similar to job costing. It gives

each batch an identifiable cost unit and each batch is assigned an identity through number.

Accounting is reduced due to batch costing and through cost of production being reduced benefit

takes place with economic quantity of batch being produced.

Contract costing

The cost tracking which is associated with a specific contract with customer is known as contract

costing.

Process costing:

This method of costing is used in production where production of units is done through more

than one process.

Advantages:

a) Cost analysis may assist in determining total production expenses as well as profit realisation

by estimating per unit costs (Krishnan and Joshi, 2017).

b) It aids in determining where operating expenses might be reduced.

Disadvantages:

a) After calculating costs, cost analysis predicts profit, but it ignores market aspects, which are

important to determine competitive pricing .

3. Budgeting

Management uses the budgeting technique to plan and control the distribution of resources that

control the activities of the company. It's a profitable approach of conducting corporate efforts.

This is also an exercise that helps improve communication and achieve a single aim across the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organization. In this aspect, the demands of various departments are assessed and then

accordingly budgets are made for the organisation.

Advantages of planning tools used for budgetary control:

a) Planning: It lays forth the company's goals and strategies for accomplishing them. It aids in

evaluating what is to be done at an early stage, and also costing and analysing sources of

funding.

b) Coordination: It measures how successfully an organisation's division or team together work

and is referred to as coordination. The committee delegated tasks and responsibilities to

departments and maintained contact with them (Terdpaopong, Visedsun and Nitirojntanad,

2019).

c) Analysis of variance: The method is utilised to figure out the divisions which stayed under

budget and who went over. The data is helpful in identification of divisions which have

performed adequately and the areas require more focus.

Demerits of planning tools used for budgetary control:

a) Inaccuracies in the project: Budgets are established for possible operations that require

estimations. Due to shifting market conditions, it's also feasible that the forecasts will be off.

Different divisions may have higher demands than those established.

b) Expensive process: Budgeting is expensive since each division, as well as several categories

that must be evaluated, must be considered. Conducting research and forecasting costs a lot of

money.

c)Revision is frequently required: As the circumstances of the organisation change, it is

necessary to modify the budget. As a result, it demands constant attention and interferes with

daily duties.

accordingly budgets are made for the organisation.

Advantages of planning tools used for budgetary control:

a) Planning: It lays forth the company's goals and strategies for accomplishing them. It aids in

evaluating what is to be done at an early stage, and also costing and analysing sources of

funding.

b) Coordination: It measures how successfully an organisation's division or team together work

and is referred to as coordination. The committee delegated tasks and responsibilities to

departments and maintained contact with them (Terdpaopong, Visedsun and Nitirojntanad,

2019).

c) Analysis of variance: The method is utilised to figure out the divisions which stayed under

budget and who went over. The data is helpful in identification of divisions which have

performed adequately and the areas require more focus.

Demerits of planning tools used for budgetary control:

a) Inaccuracies in the project: Budgets are established for possible operations that require

estimations. Due to shifting market conditions, it's also feasible that the forecasts will be off.

Different divisions may have higher demands than those established.

b) Expensive process: Budgeting is expensive since each division, as well as several categories

that must be evaluated, must be considered. Conducting research and forecasting costs a lot of

money.

c)Revision is frequently required: As the circumstances of the organisation change, it is

necessary to modify the budget. As a result, it demands constant attention and interferes with

daily duties.

d)Budget making involves time, and small details have to be given for the same for being

accurate. It's important to assess the ongoing demand for various divisions and product

categories. As a result, the process is time-consuming.

M3 Use of different planning tools and their application in preparing and forecasting of budgets

Incremental Budgeting

The budgeting method uses traditional approach used in budget calculation. In the approach,

traditional budgeting uses an increment of a fixed percentage over the previous budgets to take

care of inflation. It does not go in a detailed approach and is based on assumptions that the

increment in budget will be sufficient for the organisation. It is simple to calculate although

cannot be relied up on (Krishnan and Joshi, 2017).

Zero based budgeting

It takes a comprehensive approach in which category wise demand of product is assessed and

valued of every department. It is based on scientific approach which assumes revenue and

expenses to be zero of the previous year and starts from scratch.

Capital Budget

This process is used for evaluation of major projects and investments. It focuses on identification

of cash inflows and outflows rather than revenues and expenses accounting. Cash flow which is

associated with actual cost and financing is undertaken.

P5 Comparison of organisations using management accounting for responding to financial

problems

Costing analysis

To determine the overall cost of production, Prime Furniture applied costing techniques. These

are numerous indirect and direct expenditures, like purchase of raw material, labour, and so on.

The calculations of these costs are done per unit and margin of gain on products is established.

accurate. It's important to assess the ongoing demand for various divisions and product

categories. As a result, the process is time-consuming.

M3 Use of different planning tools and their application in preparing and forecasting of budgets

Incremental Budgeting

The budgeting method uses traditional approach used in budget calculation. In the approach,

traditional budgeting uses an increment of a fixed percentage over the previous budgets to take

care of inflation. It does not go in a detailed approach and is based on assumptions that the

increment in budget will be sufficient for the organisation. It is simple to calculate although

cannot be relied up on (Krishnan and Joshi, 2017).

Zero based budgeting

It takes a comprehensive approach in which category wise demand of product is assessed and

valued of every department. It is based on scientific approach which assumes revenue and

expenses to be zero of the previous year and starts from scratch.

Capital Budget

This process is used for evaluation of major projects and investments. It focuses on identification

of cash inflows and outflows rather than revenues and expenses accounting. Cash flow which is

associated with actual cost and financing is undertaken.

P5 Comparison of organisations using management accounting for responding to financial

problems

Costing analysis

To determine the overall cost of production, Prime Furniture applied costing techniques. These

are numerous indirect and direct expenditures, like purchase of raw material, labour, and so on.

The calculations of these costs are done per unit and margin of gain on products is established.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This shows how costing helps the company in calculation of costs and identification of solutions

to cut variable expenses and increasing gain margins.

Capital Joinery previously lacked a cost-effective approach, and as a result, it faced stiff

market competition. It has learned how to establish a profit margin on its products while taking

all fixed and variable costs into account as a result of management costing, and sales revenue has

increased as a result.

Financial Planning

By taking help of technologies like analysis of variance, organisation was able for planning from

financial aspect for the sub departments and got help in allocation of budgets. It helps in the

identification of the organisation's long-term and short-term liabilities. It has helped the company

in developing of financial policies and regulations for meeting targets (Amara and Benelifa,

2017).

With management accounting, Capital Joinery got off to a late start. As a result, it was

not uncommon for funds to be allocated in accordance with the section's requirements. However,

the company was able to correct its faults later on with the help of financial statement analysis,

and financial capital estimations are now performing well for the company. The return on

investment in R&D and projects is assessed using a rate of return, which prevents the company

from making less profitable selections.

Financial Analysis

In crisis period, Prime Furniture could do prediction of earnings of future, the capacity for

paying securities interest, and the solvency of the company. The business was able to check its

accounts receivable and make adjustments to its policy of credit in accordance. The research

assists the company in determination of ratios which should be improved for attracting addition

of investing (Doktoralina and Apollo, 2019).

Capital Joinery has profited from financial planning in terms of increasing the return on invested

capital. It has aided in the management of funding sources, the determination of income, and the

distribution of money to shareholders in the form of dividends.

to cut variable expenses and increasing gain margins.

Capital Joinery previously lacked a cost-effective approach, and as a result, it faced stiff

market competition. It has learned how to establish a profit margin on its products while taking

all fixed and variable costs into account as a result of management costing, and sales revenue has

increased as a result.

Financial Planning

By taking help of technologies like analysis of variance, organisation was able for planning from

financial aspect for the sub departments and got help in allocation of budgets. It helps in the

identification of the organisation's long-term and short-term liabilities. It has helped the company

in developing of financial policies and regulations for meeting targets (Amara and Benelifa,

2017).

With management accounting, Capital Joinery got off to a late start. As a result, it was

not uncommon for funds to be allocated in accordance with the section's requirements. However,

the company was able to correct its faults later on with the help of financial statement analysis,

and financial capital estimations are now performing well for the company. The return on

investment in R&D and projects is assessed using a rate of return, which prevents the company

from making less profitable selections.

Financial Analysis

In crisis period, Prime Furniture could do prediction of earnings of future, the capacity for

paying securities interest, and the solvency of the company. The business was able to check its

accounts receivable and make adjustments to its policy of credit in accordance. The research

assists the company in determination of ratios which should be improved for attracting addition

of investing (Doktoralina and Apollo, 2019).

Capital Joinery has profited from financial planning in terms of increasing the return on invested

capital. It has aided in the management of funding sources, the determination of income, and the

distribution of money to shareholders in the form of dividends.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cash and fund flow analysis

For analysing the changes in financial position among the two, Prime Furniture use fund flow

tools. It helped company in identification of sources of cash and determination of the funds

which can be boosted through fixed assets utilisation.

Many suppliers and creditors are dealt with by Capital Joinery. The study has aided the

organisation in estimating cash flows for future projects and demonstrating the profitability of

the work done. The company was able to channel cash expenses and save money as a result.

Marginal costing

Prime Furniture used marginal costing to realise profits on batches of production and benefited

by staying ahead in competition through profits in the industry.

Capital Joinery had previously used judgmental pricing based on market conditions, which did

not always work, but after employing this technique, it was able to perform a Break-even study

and implement marginal pricing to achieve long-term profitability. It was also able to work on its

Economic Order Quantity after reaching break-even, allowing it to get the proper quantity of

inventory and save money (Amara and Benelifa, 2017).

M4 Management accounting leading to success in response to financial problems in organisation

Taking example of Prime Furniture, it can be discussed how the techniques of management

accounting help in realising success.

Costing Analysis: The production which takes place in Prime Furniture has many costs attached

to it like direct and indirect costs. All the fixed and variable costs are taken in account has been

considered in the management accounting technique. The summation of these costs is done and

is then divided by number of units manufactured. This helps to find out about the cost per unit.

Prime Furniture thus knows where how much costs have gone in and knows where cost cutting

can be done. Also, it helps to set price once knowing the cost per unit of the product

(Terdpaopong, Visedsun and Nitirojntanad, 2019). Thus, management accounting techniques

have helped in realising cost cutting measures while setting benchmark for profitability.

For analysing the changes in financial position among the two, Prime Furniture use fund flow

tools. It helped company in identification of sources of cash and determination of the funds

which can be boosted through fixed assets utilisation.

Many suppliers and creditors are dealt with by Capital Joinery. The study has aided the

organisation in estimating cash flows for future projects and demonstrating the profitability of

the work done. The company was able to channel cash expenses and save money as a result.

Marginal costing

Prime Furniture used marginal costing to realise profits on batches of production and benefited

by staying ahead in competition through profits in the industry.

Capital Joinery had previously used judgmental pricing based on market conditions, which did

not always work, but after employing this technique, it was able to perform a Break-even study

and implement marginal pricing to achieve long-term profitability. It was also able to work on its

Economic Order Quantity after reaching break-even, allowing it to get the proper quantity of

inventory and save money (Amara and Benelifa, 2017).

M4 Management accounting leading to success in response to financial problems in organisation

Taking example of Prime Furniture, it can be discussed how the techniques of management

accounting help in realising success.

Costing Analysis: The production which takes place in Prime Furniture has many costs attached

to it like direct and indirect costs. All the fixed and variable costs are taken in account has been

considered in the management accounting technique. The summation of these costs is done and

is then divided by number of units manufactured. This helps to find out about the cost per unit.

Prime Furniture thus knows where how much costs have gone in and knows where cost cutting

can be done. Also, it helps to set price once knowing the cost per unit of the product

(Terdpaopong, Visedsun and Nitirojntanad, 2019). Thus, management accounting techniques

have helped in realising cost cutting measures while setting benchmark for profitability.

Investment analysis: Prime furniture gets assistance in investment options for buying a new

product or investment in expanding business like setting of a new branch. Through management

accounting techniques of investment like NPV which takes time value of money in consideration

and IRR which takes in account internal rate of return, organisation like Prime Furniture is able

to choose on the right projects for investment.

Inventory analysis: Prime furniture is able to maintain the right amount of inventory with use of

management accounting techniques which hep in calculation of Economic order quantity.

Economic order quantity helps in realising the right amount of inventory which is required.

Keeping inventory in excess can cause harm to the goods which may become damaged and costs

in excess too of maintaining them. They also take up extra space. Use of management accounting

helps organisation in saving on inventory costs and the same can be utilised elsewhere in other

operations thus ensuring sustainability (Maheshwari, Maheshwari and Maheshwari, 2021).

It may be concluded that management accounting has provided organisations with convenience

as well as profitability. Its tools have aided in the development of an easy-to-understand and

implement accounting strategy. Financial analysis along with budgetary control has aided in

directing investment in the appropriate direction while also reducing costs.

CONCLUSION

It can be concluded that management accounting is a vast subject which uses various techniques

proving to be advantageous for the organisation. Different planning tools for the organisation

were discussed, comparison of planning tools was done and their merits and demerits were

discussed. A comparison of companies was done on how they have used management accounting

for their benefits. Management accounting techniques used for organisation’s sustainability in

success was discussed. The report emphasised how management accounting practically assists an

organisation in overcoming problems as well as realise profitability.

product or investment in expanding business like setting of a new branch. Through management

accounting techniques of investment like NPV which takes time value of money in consideration

and IRR which takes in account internal rate of return, organisation like Prime Furniture is able

to choose on the right projects for investment.

Inventory analysis: Prime furniture is able to maintain the right amount of inventory with use of

management accounting techniques which hep in calculation of Economic order quantity.

Economic order quantity helps in realising the right amount of inventory which is required.

Keeping inventory in excess can cause harm to the goods which may become damaged and costs

in excess too of maintaining them. They also take up extra space. Use of management accounting

helps organisation in saving on inventory costs and the same can be utilised elsewhere in other

operations thus ensuring sustainability (Maheshwari, Maheshwari and Maheshwari, 2021).

It may be concluded that management accounting has provided organisations with convenience

as well as profitability. Its tools have aided in the development of an easy-to-understand and

implement accounting strategy. Financial analysis along with budgetary control has aided in

directing investment in the appropriate direction while also reducing costs.

CONCLUSION

It can be concluded that management accounting is a vast subject which uses various techniques

proving to be advantageous for the organisation. Different planning tools for the organisation

were discussed, comparison of planning tools was done and their merits and demerits were

discussed. A comparison of companies was done on how they have used management accounting

for their benefits. Management accounting techniques used for organisation’s sustainability in

success was discussed. The report emphasised how management accounting practically assists an

organisation in overcoming problems as well as realise profitability.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.