Management Accounting: Cost Analysis, Reporting, and Budgetary Control

Added on 2023-06-16

16 Pages4056 Words330 Views

TASK 1............................................................................................................................................3

P1. Management accounting and requirements of various types of management accounting

system.....................................................................................................................................3

P2. Several methods which are used for management accounting reporting.........................5

TASK 2............................................................................................................................................6

P3. Calculation of cost by using accurate techniques of cost analysis and prepare income

statement with the help of absorption and marginal costs......................................................6

Absorption costing...........................................................................................................................7

TASK 3............................................................................................................................................8

P4. Advantages and disadvantages of various kinds of planning tools which is used for

budgetary control....................................................................................................................8

TASK 4..........................................................................................................................................11

P5. Comparison of organisations and how they are adopting accounting system of

management to respond financial problems.........................................................................11

CONCLUSION..............................................................................................................................14

REFERENCE.................................................................................................................................15

INTRODUCTION

Management accounting refers to the process of offering lots of resources and financial

information to the managers of an organisation by which they can take appropriate decisions in a

perfect way. It is also known as managerial accounting which can be only used by the internal

P1. Management accounting and requirements of various types of management accounting

system.....................................................................................................................................3

P2. Several methods which are used for management accounting reporting.........................5

TASK 2............................................................................................................................................6

P3. Calculation of cost by using accurate techniques of cost analysis and prepare income

statement with the help of absorption and marginal costs......................................................6

Absorption costing...........................................................................................................................7

TASK 3............................................................................................................................................8

P4. Advantages and disadvantages of various kinds of planning tools which is used for

budgetary control....................................................................................................................8

TASK 4..........................................................................................................................................11

P5. Comparison of organisations and how they are adopting accounting system of

management to respond financial problems.........................................................................11

CONCLUSION..............................................................................................................................14

REFERENCE.................................................................................................................................15

INTRODUCTION

Management accounting refers to the process of offering lots of resources and financial

information to the managers of an organisation by which they can take appropriate decisions in a

perfect way. It is also known as managerial accounting which can be only used by the internal

team of company. According to this process of management accounting financial reports like

financial balance statement, invoice shared through the team members of an organisation. Along

with this there are some management objectives which is used to make appropriate decision to

develop effective growth of business. For better understanding of this topic ASDA has been

chosen as an organisation. Further discussion will be based on cost analysis in relation to

marginal and absorption cost (Aldehayyat and Maan, 2013). Along with various kinds of

planning tools and difference will be explained for adopting management accounting system to

responding of financial issues.

TASK 1

P1. Management accounting and requirements of various types of management accounting

system.

Management accounting is the process of identifying, analysing appropriate cost of

operations in order to make records, internal financial reports for accomplishing business goals

and objectives. On the other side, it helps organisations to make accurate costing method to use

effective information tool for gaining higher advantages perfectly. In context with ASDA they

define their overall business performance by using different types of tools and techniques like

forecasting, comparisons, budgeting aspects and so on. On the basis of this they can easily make

proper data and records in order to develop effective managerial operations for improving

manufacturing process of clothes (Anandarajan, Anandarajan and Srinivasan, 2012).

Wherein, management system involves in the internal system of an organisation by which

they can examine the overall performance of their business operations to achieve targeted goals.

In regards with ASDA through using these system of management accounting they can make

their business functions in a systematic manner. With the help of different objectives manager of

this respective company able to make decision without any issues into the marketplace. That's

why this company using both non financial and financial accounting tools for getting better

information towards their improvements in the process of running business. Apart from this there

are large number of effective combinations between different sectors of management accounting

by which organization can increase their viability at marketplace. As per the ASDA they are

properly using management accounting system to make their management inventory in an

financial balance statement, invoice shared through the team members of an organisation. Along

with this there are some management objectives which is used to make appropriate decision to

develop effective growth of business. For better understanding of this topic ASDA has been

chosen as an organisation. Further discussion will be based on cost analysis in relation to

marginal and absorption cost (Aldehayyat and Maan, 2013). Along with various kinds of

planning tools and difference will be explained for adopting management accounting system to

responding of financial issues.

TASK 1

P1. Management accounting and requirements of various types of management accounting

system.

Management accounting is the process of identifying, analysing appropriate cost of

operations in order to make records, internal financial reports for accomplishing business goals

and objectives. On the other side, it helps organisations to make accurate costing method to use

effective information tool for gaining higher advantages perfectly. In context with ASDA they

define their overall business performance by using different types of tools and techniques like

forecasting, comparisons, budgeting aspects and so on. On the basis of this they can easily make

proper data and records in order to develop effective managerial operations for improving

manufacturing process of clothes (Anandarajan, Anandarajan and Srinivasan, 2012).

Wherein, management system involves in the internal system of an organisation by which

they can examine the overall performance of their business operations to achieve targeted goals.

In regards with ASDA through using these system of management accounting they can make

their business functions in a systematic manner. With the help of different objectives manager of

this respective company able to make decision without any issues into the marketplace. That's

why this company using both non financial and financial accounting tools for getting better

information towards their improvements in the process of running business. Apart from this there

are large number of effective combinations between different sectors of management accounting

by which organization can increase their viability at marketplace. As per the ASDA they are

properly using management accounting system to make their management inventory in an

effective manner (Christ and Burritt, 2013). Additionally, by adopting effective pricing method

respective company can enhance their value of firm and make proper costing method within the

particular time frame. It shows that present organisation needs to adopt all these managerial

accounting functions to improve their overall business organisations.

Principles and Origin of management accounting

As per this analysis the management accounting concept was origin through the England

during the time revolution of industries. It involves several activities and their implementation on

financial issues by which companies can improvised. There are few principles of management

accounting that affects organisations and make proper trust in relation with orientations within

the companies.

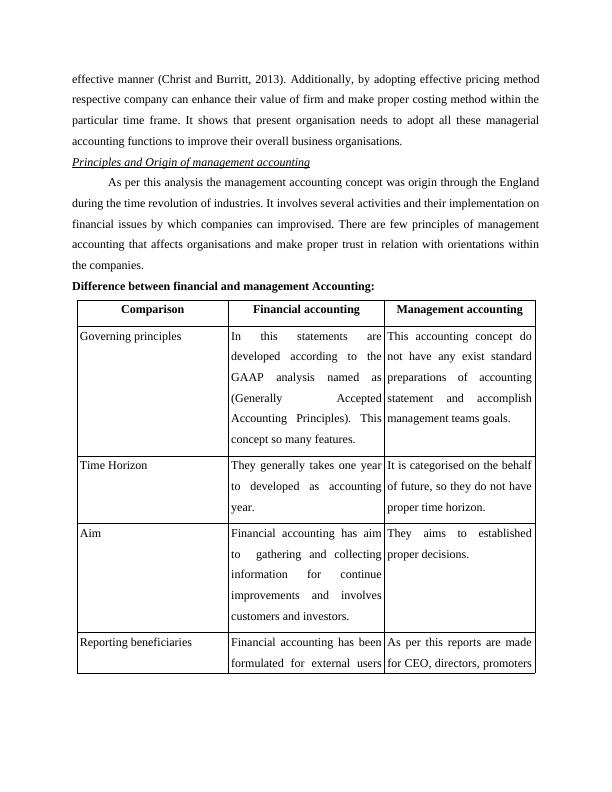

Difference between financial and management Accounting:

Comparison Financial accounting Management accounting

Governing principles In this statements are

developed according to the

GAAP analysis named as

(Generally Accepted

Accounting Principles). This

concept so many features.

This accounting concept do

not have any exist standard

preparations of accounting

statement and accomplish

management teams goals.

Time Horizon They generally takes one year

to developed as accounting

year.

It is categorised on the behalf

of future, so they do not have

proper time horizon.

Aim Financial accounting has aim

to gathering and collecting

information for continue

improvements and involves

customers and investors.

They aims to established

proper decisions.

Reporting beneficiaries Financial accounting has been

formulated for external users

As per this reports are made

for CEO, directors, promoters

respective company can enhance their value of firm and make proper costing method within the

particular time frame. It shows that present organisation needs to adopt all these managerial

accounting functions to improve their overall business organisations.

Principles and Origin of management accounting

As per this analysis the management accounting concept was origin through the England

during the time revolution of industries. It involves several activities and their implementation on

financial issues by which companies can improvised. There are few principles of management

accounting that affects organisations and make proper trust in relation with orientations within

the companies.

Difference between financial and management Accounting:

Comparison Financial accounting Management accounting

Governing principles In this statements are

developed according to the

GAAP analysis named as

(Generally Accepted

Accounting Principles). This

concept so many features.

This accounting concept do

not have any exist standard

preparations of accounting

statement and accomplish

management teams goals.

Time Horizon They generally takes one year

to developed as accounting

year.

It is categorised on the behalf

of future, so they do not have

proper time horizon.

Aim Financial accounting has aim

to gathering and collecting

information for continue

improvements and involves

customers and investors.

They aims to established

proper decisions.

Reporting beneficiaries Financial accounting has been

formulated for external users

As per this reports are made

for CEO, directors, promoters

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Management Accounting Systems and Techniques Solved Assignmentlg...

|21

|5729

|29

Management Accounting System & Techniqueslg...

|12

|3434

|110

Management Accounting Assignment PDF | AIRDRIlg...

|22

|4930

|76

Application of Management Accounting Systemlg...

|15

|4294

|24

Methods of Management Accounting Reporting - Doclg...

|18

|5490

|134

Management Accounting and Cost Analysis for Creams Limitedlg...

|17

|3891

|40