Management Accounting for Cost and Control

VerifiedAdded on 2023/06/14

|28

|2831

|303

AI Summary

This project report covers various topics related to management accounting such as panopticism, control, checklist, manufacturing statement, income statement, labour cost concept, material control account, accrued payroll account, and payroll entries. It explains the importance of controlling in business, the concept of perpetual inventory stock, and the use of checklists. It also includes examples of manufacturing statements, income statements, and journal entries for payroll. The report is relevant for students studying management accounting in any college or university.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: Management Accounting

1

Project Report: Management Accounting for cost and control

1

Project Report: Management Accounting for cost and control

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Management Accounting

2

Contents

Question 1: Panopticism...................................................................................................3

Question 2: Control...........................................................................................................3

Question 3: Checklist........................................................................................................4

Question 4: Manufacturing statement and income statement...........................................4

Question 5: Labour cost concept......................................................................................9

Question 6: Material control account.............................................................................10

Question 7: Accrued payroll account.............................................................................11

Question 8: Payroll entries..............................................................................................13

Question 9:Activity based costing..................................................................................21

Question 10: Service department cost allocation............................................................21

References.......................................................................................................................26

2

Contents

Question 1: Panopticism...................................................................................................3

Question 2: Control...........................................................................................................3

Question 3: Checklist........................................................................................................4

Question 4: Manufacturing statement and income statement...........................................4

Question 5: Labour cost concept......................................................................................9

Question 6: Material control account.............................................................................10

Question 7: Accrued payroll account.............................................................................11

Question 8: Payroll entries..............................................................................................13

Question 9:Activity based costing..................................................................................21

Question 10: Service department cost allocation............................................................21

References.......................................................................................................................26

Management Accounting

3

Question 1: Panopticism

Panopticism is a hypothetical jail which has been projected by Jeremy Bentham. It

have round tires of cell adjacent a central surveillance tower. Panopticism is a process of

panopticon in which cost are controlled and reduced by the companies to maintain the

performance and the position of the company in the industry. Panopticism requires less staff

and the main motto of this process is to set the goals and achieve the goals in no cost. It

explains that the virtual and hypothetical control should be there in the organization to

maintain the performance of the staff and it would make a control over all the cost of the

company due to hypothetical perseverance (Garrison et al, 2010). Panopticism process

controls and monitors the activity of a business to manage the entire activities of the

company. It enhances the overall business and the management of the company to reduce and

manage the cost of the company.

Question 2: Control

Controlling is a significant part of business which extends the performance and the

management of an organization. The way toward controlling includes supervising, proposing,

monitoring and analyzing corrections in the business activity and the process of the company.

The administration bookkeeping framework controls the business procedures and exercises in

order to guarantee that the business goals are accomplished. For instance, the exception

reporting and variance analysis is gotten through the management accounting framework,

which help administration in assessing the slip by at the workplace. Further, the controls are

likewise set down to decrease the wastage and in this way, the general cost of manufacturing

(Ittner, Lanen & Larcker, 2002). The variance analysis assists in finding the reasons for

rebelliousness and shatter of controls, alongside giving answer for the same. Along these,

management accounting assists the administration in giving the controlling capacity in the

association, which is significant for the accomplishment of the gaols.

3

Question 1: Panopticism

Panopticism is a hypothetical jail which has been projected by Jeremy Bentham. It

have round tires of cell adjacent a central surveillance tower. Panopticism is a process of

panopticon in which cost are controlled and reduced by the companies to maintain the

performance and the position of the company in the industry. Panopticism requires less staff

and the main motto of this process is to set the goals and achieve the goals in no cost. It

explains that the virtual and hypothetical control should be there in the organization to

maintain the performance of the staff and it would make a control over all the cost of the

company due to hypothetical perseverance (Garrison et al, 2010). Panopticism process

controls and monitors the activity of a business to manage the entire activities of the

company. It enhances the overall business and the management of the company to reduce and

manage the cost of the company.

Question 2: Control

Controlling is a significant part of business which extends the performance and the

management of an organization. The way toward controlling includes supervising, proposing,

monitoring and analyzing corrections in the business activity and the process of the company.

The administration bookkeeping framework controls the business procedures and exercises in

order to guarantee that the business goals are accomplished. For instance, the exception

reporting and variance analysis is gotten through the management accounting framework,

which help administration in assessing the slip by at the workplace. Further, the controls are

likewise set down to decrease the wastage and in this way, the general cost of manufacturing

(Ittner, Lanen & Larcker, 2002). The variance analysis assists in finding the reasons for

rebelliousness and shatter of controls, alongside giving answer for the same. Along these,

management accounting assists the administration in giving the controlling capacity in the

association, which is significant for the accomplishment of the gaols.

Management Accounting

4

Question 3: Checklist

Checklist is a list of total items and things which are required to done the things or the

points which are required to be considered and used as a reminder. It is a type of job aid

which is used by the companies and the individuals to reduce the failure through

compensating the potential limits of attention and human memory. Van Halen’s checklist

theory explains that the band has been successful due to their checklist. The bank always used

to maintain a checklist before any concert so that the things could be managed and

performance could be at its best. It is quite tough for a band to manage such as big

equipments in smaller place but it used to easier for Van Halen’s due to their policy and the

checklist management (Weygandt, Kimmel & Kieso, 2015). However, it has also been found

that a checklist is only successful when it is properly followed.

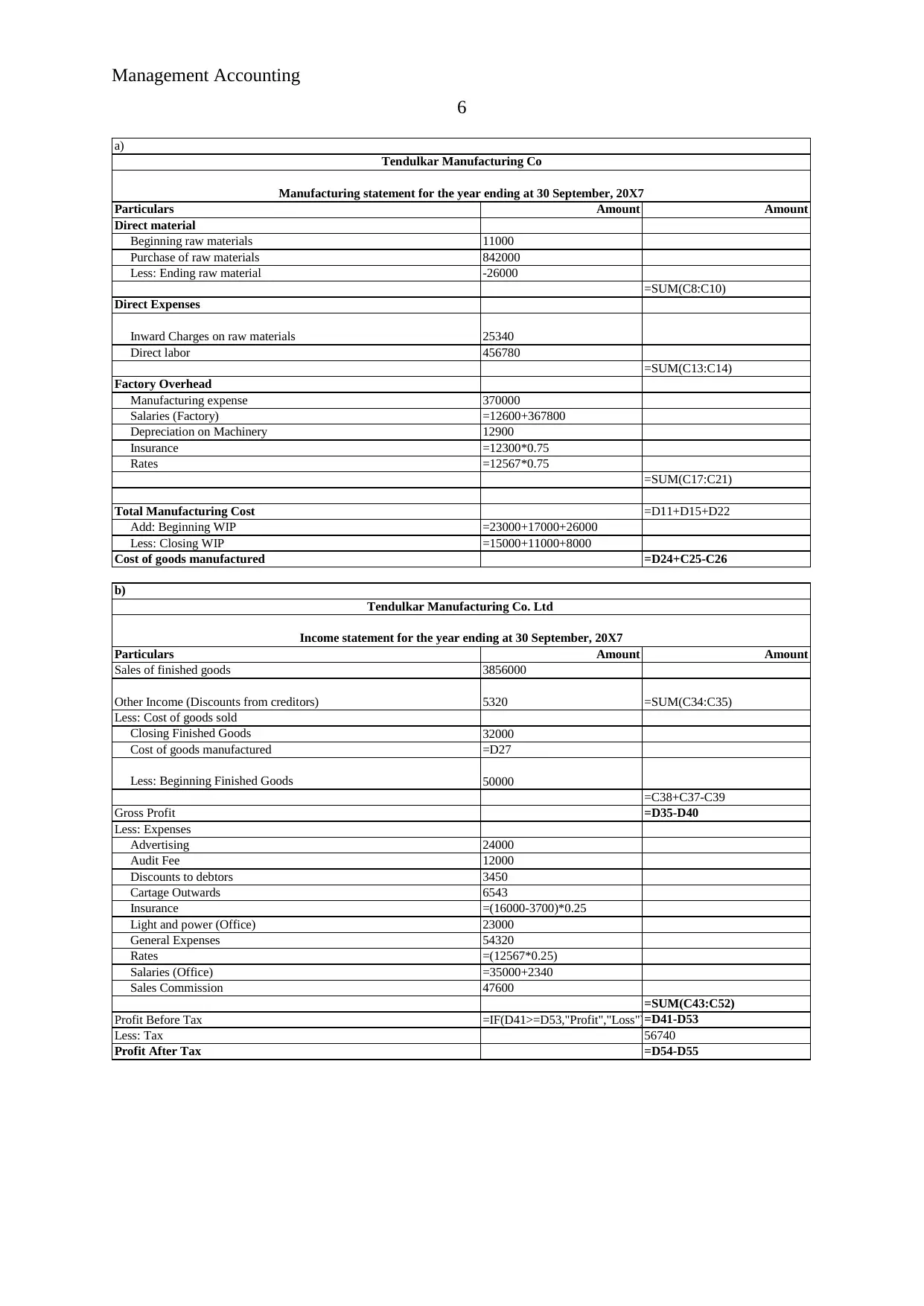

Question 4: Manufacturing statement and income statement

Normal Solution:

a)

Tendulkar Manufacturing Co

Manufacturing statement for the year ending at 30

September, 20X7

Particulars Amount Amount

Direct material

Beginning raw materials 11,000

Purchase of raw materials 8,42,000

Less: Ending raw material -26,000

8,27,000

Direct Expenses

Inward Charges on raw

materials 25,340

Direct labor 4,56,780

4,82,120

Factory Overhead

Manufacturing expense 3,70,000

Salaries (Factory) 3,80,400

Depreciation on Machinery 12,900

Insurance 9,225

Rates 9,425

7,81,950

4

Question 3: Checklist

Checklist is a list of total items and things which are required to done the things or the

points which are required to be considered and used as a reminder. It is a type of job aid

which is used by the companies and the individuals to reduce the failure through

compensating the potential limits of attention and human memory. Van Halen’s checklist

theory explains that the band has been successful due to their checklist. The bank always used

to maintain a checklist before any concert so that the things could be managed and

performance could be at its best. It is quite tough for a band to manage such as big

equipments in smaller place but it used to easier for Van Halen’s due to their policy and the

checklist management (Weygandt, Kimmel & Kieso, 2015). However, it has also been found

that a checklist is only successful when it is properly followed.

Question 4: Manufacturing statement and income statement

Normal Solution:

a)

Tendulkar Manufacturing Co

Manufacturing statement for the year ending at 30

September, 20X7

Particulars Amount Amount

Direct material

Beginning raw materials 11,000

Purchase of raw materials 8,42,000

Less: Ending raw material -26,000

8,27,000

Direct Expenses

Inward Charges on raw

materials 25,340

Direct labor 4,56,780

4,82,120

Factory Overhead

Manufacturing expense 3,70,000

Salaries (Factory) 3,80,400

Depreciation on Machinery 12,900

Insurance 9,225

Rates 9,425

7,81,950

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Management Accounting

5

Total Manufacturing Cost 20,91,070

Add: Beginning WIP 66,000

Less: Closing WIP 34,000

Cost of goods manufactured 21,23,070

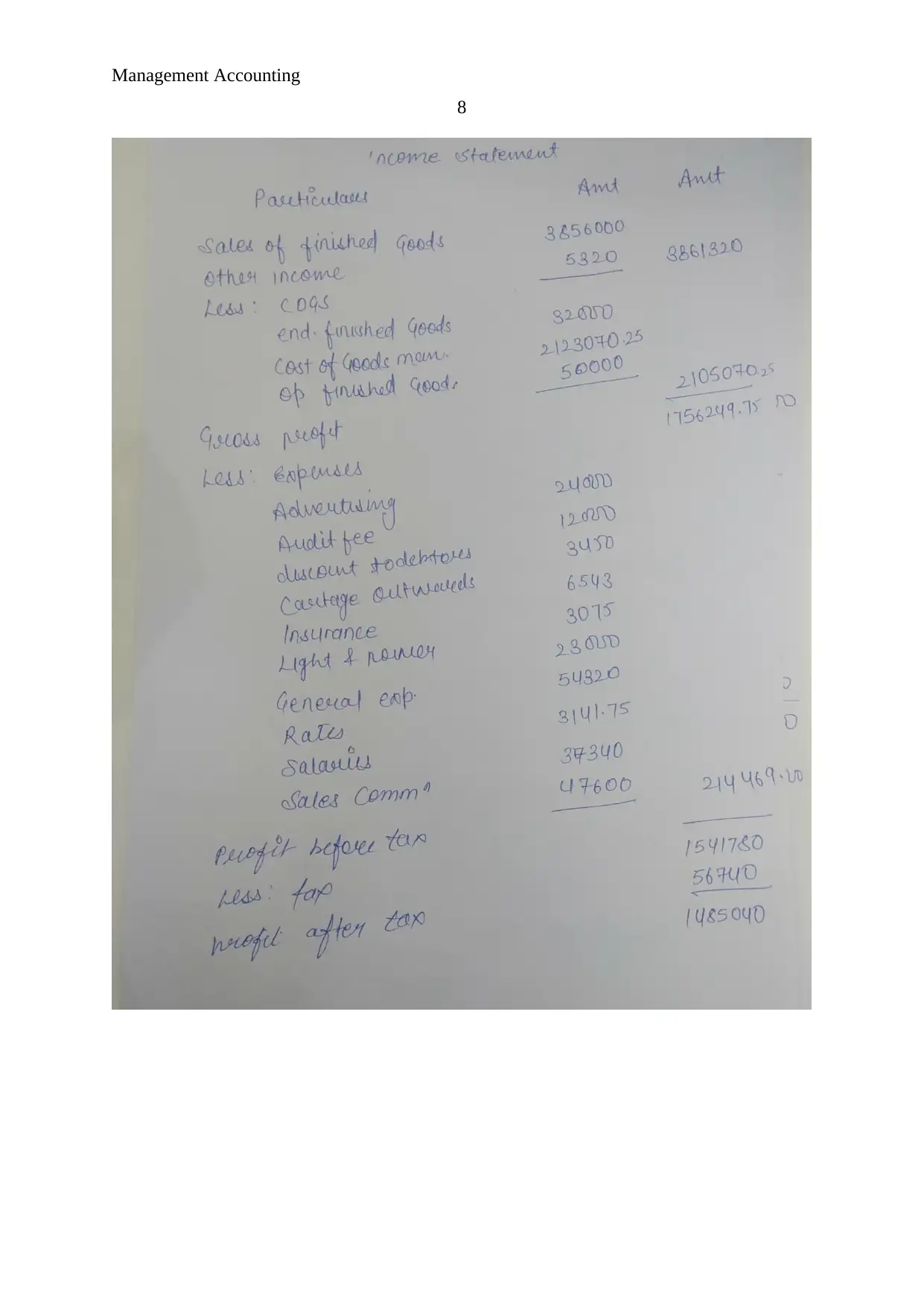

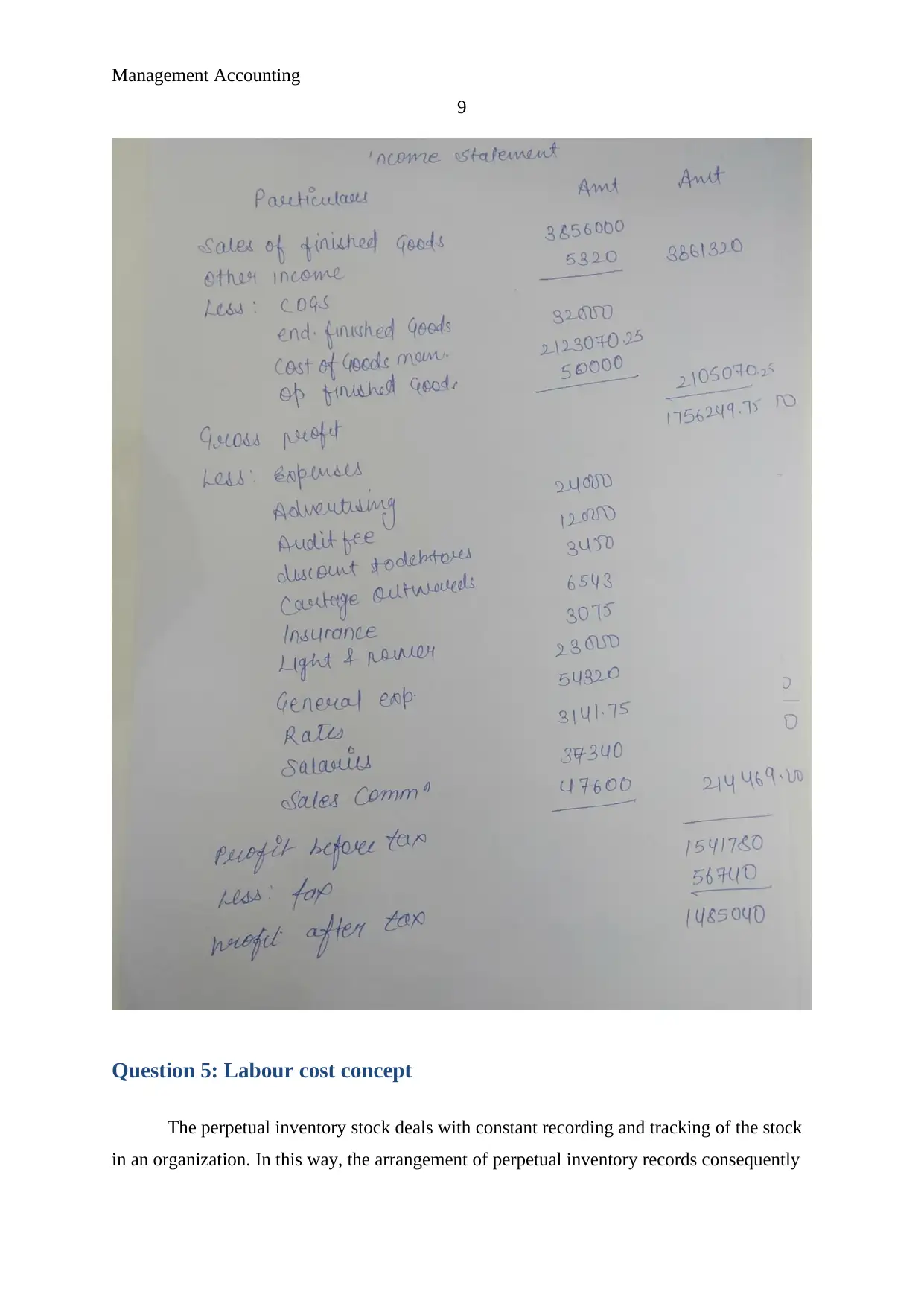

b)

Tendulkar Manufacturing Co. Ltd

Income statement for the year ending at 30 September,

20X7

Particulars Amount Amount

Sales of finished goods 38,56,000.00

Other Income (Discounts from

creditors) 5,320.00 38,61,320.00

Less: Cost of goods sold

Closing Finished Goods 32,000.00

Cost of goods

manufactured 21,23,070.25

Less: Beginning Finished

Goods 50,000.00

21,05,070.25

Gross Profit 17,56,249.75

Less: Expenses

Advertising 24,000.00

Audit Fee 12,000.00

Discounts to debtors 3,450.00

Cartage Outwards 6,543.00

Insurance 3,075.00

Light and power (Office) 23,000.00

General Expenses 54,320.00

Rates 3,141.75

Salaries (Office) 37,340.00

Sales Commission 47,600.00

2,14,469.75

Profit Before Tax Profit 15,41,780.00

Less: Tax 56,740.00

Profit After Tax 14,85,040.00

Formula view:

5

Total Manufacturing Cost 20,91,070

Add: Beginning WIP 66,000

Less: Closing WIP 34,000

Cost of goods manufactured 21,23,070

b)

Tendulkar Manufacturing Co. Ltd

Income statement for the year ending at 30 September,

20X7

Particulars Amount Amount

Sales of finished goods 38,56,000.00

Other Income (Discounts from

creditors) 5,320.00 38,61,320.00

Less: Cost of goods sold

Closing Finished Goods 32,000.00

Cost of goods

manufactured 21,23,070.25

Less: Beginning Finished

Goods 50,000.00

21,05,070.25

Gross Profit 17,56,249.75

Less: Expenses

Advertising 24,000.00

Audit Fee 12,000.00

Discounts to debtors 3,450.00

Cartage Outwards 6,543.00

Insurance 3,075.00

Light and power (Office) 23,000.00

General Expenses 54,320.00

Rates 3,141.75

Salaries (Office) 37,340.00

Sales Commission 47,600.00

2,14,469.75

Profit Before Tax Profit 15,41,780.00

Less: Tax 56,740.00

Profit After Tax 14,85,040.00

Formula view:

Management Accounting

6

Particulars Amount Amount

Direct material

Beginning raw materials 11000

Purchase of raw materials 842000

Less: Ending raw material -26000

=SUM(C8:C10)

Direct Expenses

Inward Charges on raw materials 25340

Direct labor 456780

=SUM(C13:C14)

Factory Overhead

Manufacturing expense 370000

Salaries (Factory) =12600+367800

Depreciation on Machinery 12900

Insurance =12300*0.75

Rates =12567*0.75

=SUM(C17:C21)

Total Manufacturing Cost =D11+D15+D22

Add: Beginning WIP =23000+17000+26000

Less: Closing WIP =15000+11000+8000

Cost of goods manufactured =D24+C25-C26

Particulars Amount Amount

Sales of finished goods 3856000

Other Income (Discounts from creditors) 5320 =SUM(C34:C35)

Less: Cost of goods sold

Closing Finished Goods 32000

Cost of goods manufactured =D27

Less: Beginning Finished Goods 50000

=C38+C37-C39

Gross Profit =D35-D40

Less: Expenses

Advertising 24000

Audit Fee 12000

Discounts to debtors 3450

Cartage Outwards 6543

Insurance =(16000-3700)*0.25

Light and power (Office) 23000

General Expenses 54320

Rates =(12567*0.25)

Salaries (Office) =35000+2340

Sales Commission 47600

=SUM(C43:C52)

Profit Before Tax =IF(D41>=D53,"Profit","Loss")=D41-D53

Less: Tax 56740

Profit After Tax =D54-D55

Tendulkar Manufacturing Co

Manufacturing statement for the year ending at 30 September, 20X7

Tendulkar Manufacturing Co. Ltd

Income statement for the year ending at 30 September, 20X7

a)

b)

6

Particulars Amount Amount

Direct material

Beginning raw materials 11000

Purchase of raw materials 842000

Less: Ending raw material -26000

=SUM(C8:C10)

Direct Expenses

Inward Charges on raw materials 25340

Direct labor 456780

=SUM(C13:C14)

Factory Overhead

Manufacturing expense 370000

Salaries (Factory) =12600+367800

Depreciation on Machinery 12900

Insurance =12300*0.75

Rates =12567*0.75

=SUM(C17:C21)

Total Manufacturing Cost =D11+D15+D22

Add: Beginning WIP =23000+17000+26000

Less: Closing WIP =15000+11000+8000

Cost of goods manufactured =D24+C25-C26

Particulars Amount Amount

Sales of finished goods 3856000

Other Income (Discounts from creditors) 5320 =SUM(C34:C35)

Less: Cost of goods sold

Closing Finished Goods 32000

Cost of goods manufactured =D27

Less: Beginning Finished Goods 50000

=C38+C37-C39

Gross Profit =D35-D40

Less: Expenses

Advertising 24000

Audit Fee 12000

Discounts to debtors 3450

Cartage Outwards 6543

Insurance =(16000-3700)*0.25

Light and power (Office) 23000

General Expenses 54320

Rates =(12567*0.25)

Salaries (Office) =35000+2340

Sales Commission 47600

=SUM(C43:C52)

Profit Before Tax =IF(D41>=D53,"Profit","Loss")=D41-D53

Less: Tax 56740

Profit After Tax =D54-D55

Tendulkar Manufacturing Co

Manufacturing statement for the year ending at 30 September, 20X7

Tendulkar Manufacturing Co. Ltd

Income statement for the year ending at 30 September, 20X7

a)

b)

Management Accounting

7

Manual:

7

Manual:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting

8

8

Management Accounting

9

Question 5: Labour cost concept

The perpetual inventory stock deals with constant recording and tracking of the stock

in an organization. In this way, the arrangement of perpetual inventory records consequently

9

Question 5: Labour cost concept

The perpetual inventory stock deals with constant recording and tracking of the stock

in an organization. In this way, the arrangement of perpetual inventory records consequently

Management Accounting

10

inventory and update the inventory system of the company. Since, the stock evidences are

reorganized on continuous premise, accordingly, it is required for the companies to update

and tally the inventory system to manage the performance of the company. It epxlians about

the cost of goods sold of the company (Coper and Kaplan, 2012).

Further, it explains that the overtime payment should be treated as overhead as this

cost could be controlled by the company.

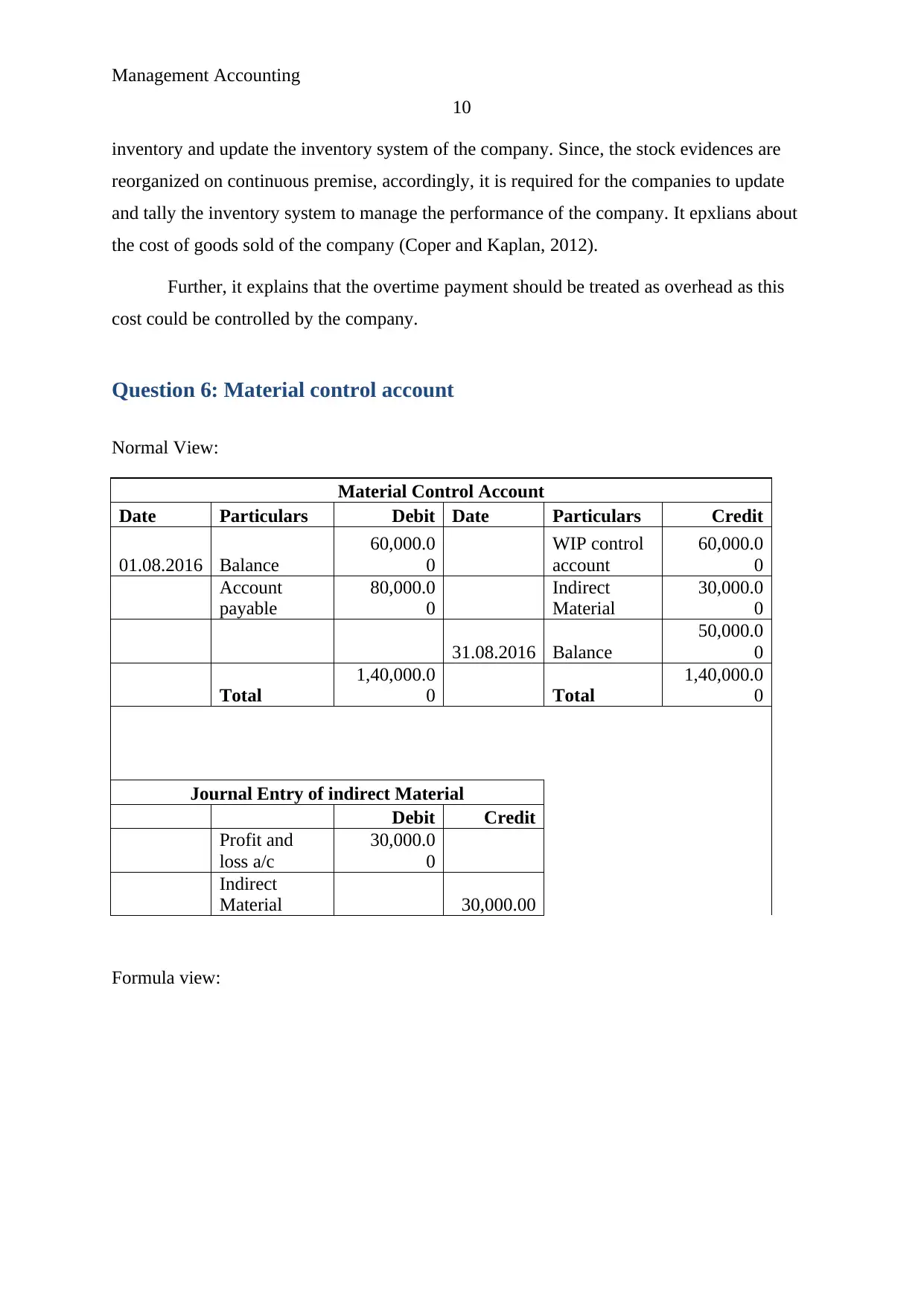

Question 6: Material control account

Normal View:

Material Control Account

Date Particulars Debit Date Particulars Credit

01.08.2016 Balance

60,000.0

0

WIP control

account

60,000.0

0

Account

payable

80,000.0

0

Indirect

Material

30,000.0

0

31.08.2016 Balance

50,000.0

0

Total

1,40,000.0

0 Total

1,40,000.0

0

Journal Entry of indirect Material

Debit Credit

Profit and

loss a/c

30,000.0

0

Indirect

Material 30,000.00

Formula view:

10

inventory and update the inventory system of the company. Since, the stock evidences are

reorganized on continuous premise, accordingly, it is required for the companies to update

and tally the inventory system to manage the performance of the company. It epxlians about

the cost of goods sold of the company (Coper and Kaplan, 2012).

Further, it explains that the overtime payment should be treated as overhead as this

cost could be controlled by the company.

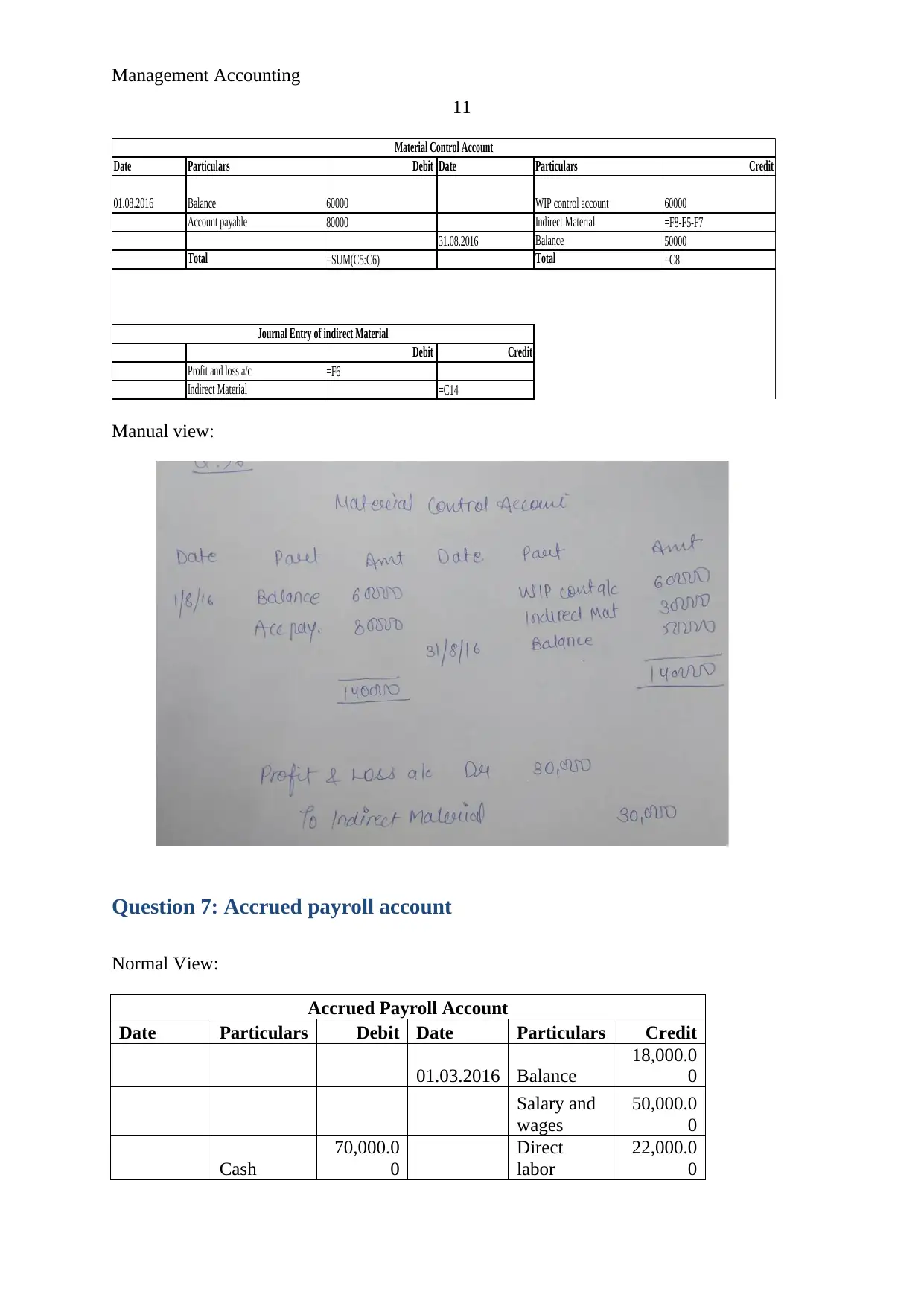

Question 6: Material control account

Normal View:

Material Control Account

Date Particulars Debit Date Particulars Credit

01.08.2016 Balance

60,000.0

0

WIP control

account

60,000.0

0

Account

payable

80,000.0

0

Indirect

Material

30,000.0

0

31.08.2016 Balance

50,000.0

0

Total

1,40,000.0

0 Total

1,40,000.0

0

Journal Entry of indirect Material

Debit Credit

Profit and

loss a/c

30,000.0

0

Indirect

Material 30,000.00

Formula view:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Management Accounting

11

Date Particulars Debit Date Particulars Credit

01.08.2016 Balance 60000 WIP control account 60000

Account payable 80000 Indirect Material =F8-F5-F7

31.08.2016 Balance 50000

Total =SUM(C5:C6) Total =C8

Debit Credit

Profit and loss a/c =F6

Indirect Material =C14

Material Control Account

Journal Entry of indirect Material

Manual view:

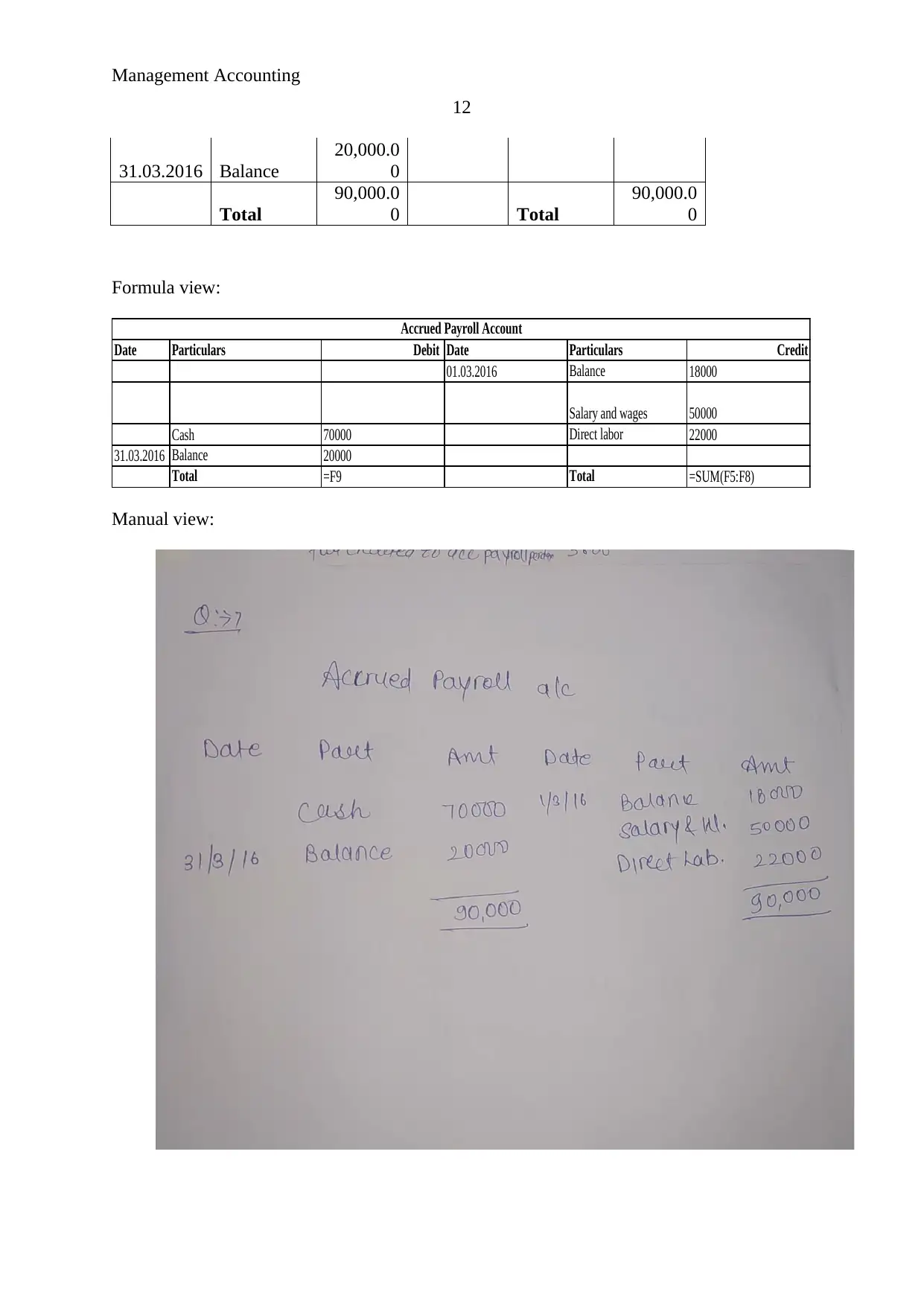

Question 7: Accrued payroll account

Normal View:

Accrued Payroll Account

Date Particulars Debit Date Particulars Credit

01.03.2016 Balance

18,000.0

0

Salary and

wages

50,000.0

0

Cash

70,000.0

0

Direct

labor

22,000.0

0

11

Date Particulars Debit Date Particulars Credit

01.08.2016 Balance 60000 WIP control account 60000

Account payable 80000 Indirect Material =F8-F5-F7

31.08.2016 Balance 50000

Total =SUM(C5:C6) Total =C8

Debit Credit

Profit and loss a/c =F6

Indirect Material =C14

Material Control Account

Journal Entry of indirect Material

Manual view:

Question 7: Accrued payroll account

Normal View:

Accrued Payroll Account

Date Particulars Debit Date Particulars Credit

01.03.2016 Balance

18,000.0

0

Salary and

wages

50,000.0

0

Cash

70,000.0

0

Direct

labor

22,000.0

0

Management Accounting

12

31.03.2016 Balance

20,000.0

0

Total

90,000.0

0 Total

90,000.0

0

Formula view:

Date Particulars Debit Date Particulars Credit

01.03.2016 Balance 18000

Salary and wages 50000

Cash 70000 Direct labor 22000

31.03.2016 Balance 20000

Total =F9 Total =SUM(F5:F8)

Accrued Payroll Account

Manual view:

12

31.03.2016 Balance

20,000.0

0

Total

90,000.0

0 Total

90,000.0

0

Formula view:

Date Particulars Debit Date Particulars Credit

01.03.2016 Balance 18000

Salary and wages 50000

Cash 70000 Direct labor 22000

31.03.2016 Balance 20000

Total =F9 Total =SUM(F5:F8)

Accrued Payroll Account

Manual view:

Management Accounting

13

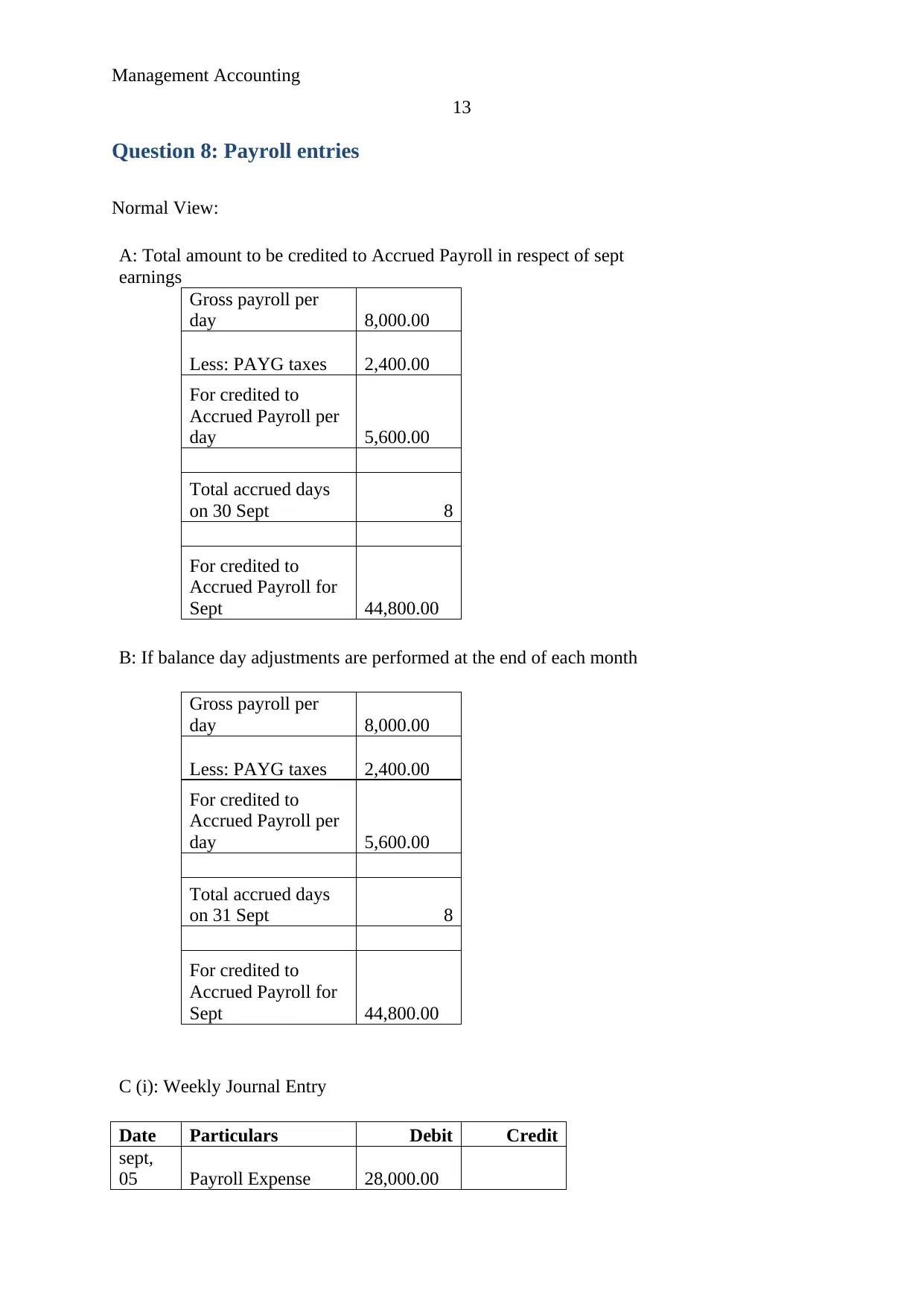

Question 8: Payroll entries

Normal View:

A: Total amount to be credited to Accrued Payroll in respect of sept

earnings

Gross payroll per

day 8,000.00

Less: PAYG taxes 2,400.00

For credited to

Accrued Payroll per

day 5,600.00

Total accrued days

on 30 Sept 8

For credited to

Accrued Payroll for

Sept 44,800.00

B: If balance day adjustments are performed at the end of each month

Gross payroll per

day 8,000.00

Less: PAYG taxes 2,400.00

For credited to

Accrued Payroll per

day 5,600.00

Total accrued days

on 31 Sept 8

For credited to

Accrued Payroll for

Sept 44,800.00

C (i): Weekly Journal Entry

Date Particulars Debit Credit

sept,

05 Payroll Expense 28,000.00

13

Question 8: Payroll entries

Normal View:

A: Total amount to be credited to Accrued Payroll in respect of sept

earnings

Gross payroll per

day 8,000.00

Less: PAYG taxes 2,400.00

For credited to

Accrued Payroll per

day 5,600.00

Total accrued days

on 30 Sept 8

For credited to

Accrued Payroll for

Sept 44,800.00

B: If balance day adjustments are performed at the end of each month

Gross payroll per

day 8,000.00

Less: PAYG taxes 2,400.00

For credited to

Accrued Payroll per

day 5,600.00

Total accrued days

on 31 Sept 8

For credited to

Accrued Payroll for

Sept 44,800.00

C (i): Weekly Journal Entry

Date Particulars Debit Credit

sept,

05 Payroll Expense 28,000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting

14

Cash 28,000.00

Sept,

12 Payroll Expense 39,200.00

Cash 39,200.00

Sept,

19 Payroll Expense 39,200.00

Cash 39,200.00

Sept,

26 Payroll Expense 39,200.00

Cash 39,200.00

Sept,

30 Payroll Expense 28,000.00

Accrued Payroll 28,000.00

Sept,

30 Payroll Expense 72,000.00

PAYG Taxes 72,000.00

Sept,

30 PAYG Taxes 72,000.00

Cash 72,000.00

Sept,

30 Income Summary 2,40,000.00

Payroll expense 2,40,000.00

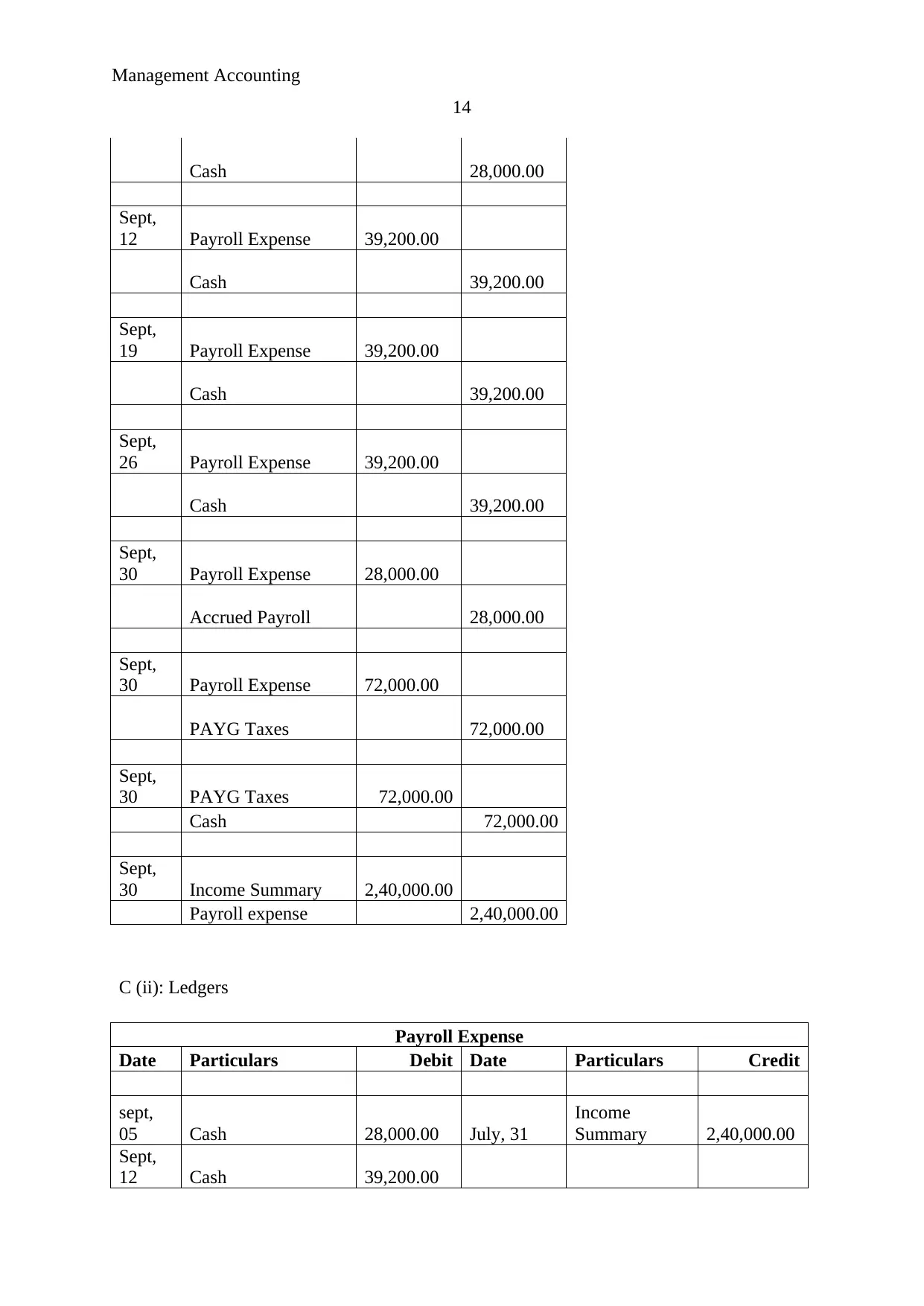

C (ii): Ledgers

Payroll Expense

Date Particulars Debit Date Particulars Credit

sept,

05 Cash 28,000.00 July, 31

Income

Summary 2,40,000.00

Sept,

12 Cash 39,200.00

14

Cash 28,000.00

Sept,

12 Payroll Expense 39,200.00

Cash 39,200.00

Sept,

19 Payroll Expense 39,200.00

Cash 39,200.00

Sept,

26 Payroll Expense 39,200.00

Cash 39,200.00

Sept,

30 Payroll Expense 28,000.00

Accrued Payroll 28,000.00

Sept,

30 Payroll Expense 72,000.00

PAYG Taxes 72,000.00

Sept,

30 PAYG Taxes 72,000.00

Cash 72,000.00

Sept,

30 Income Summary 2,40,000.00

Payroll expense 2,40,000.00

C (ii): Ledgers

Payroll Expense

Date Particulars Debit Date Particulars Credit

sept,

05 Cash 28,000.00 July, 31

Income

Summary 2,40,000.00

Sept,

12 Cash 39,200.00

Management Accounting

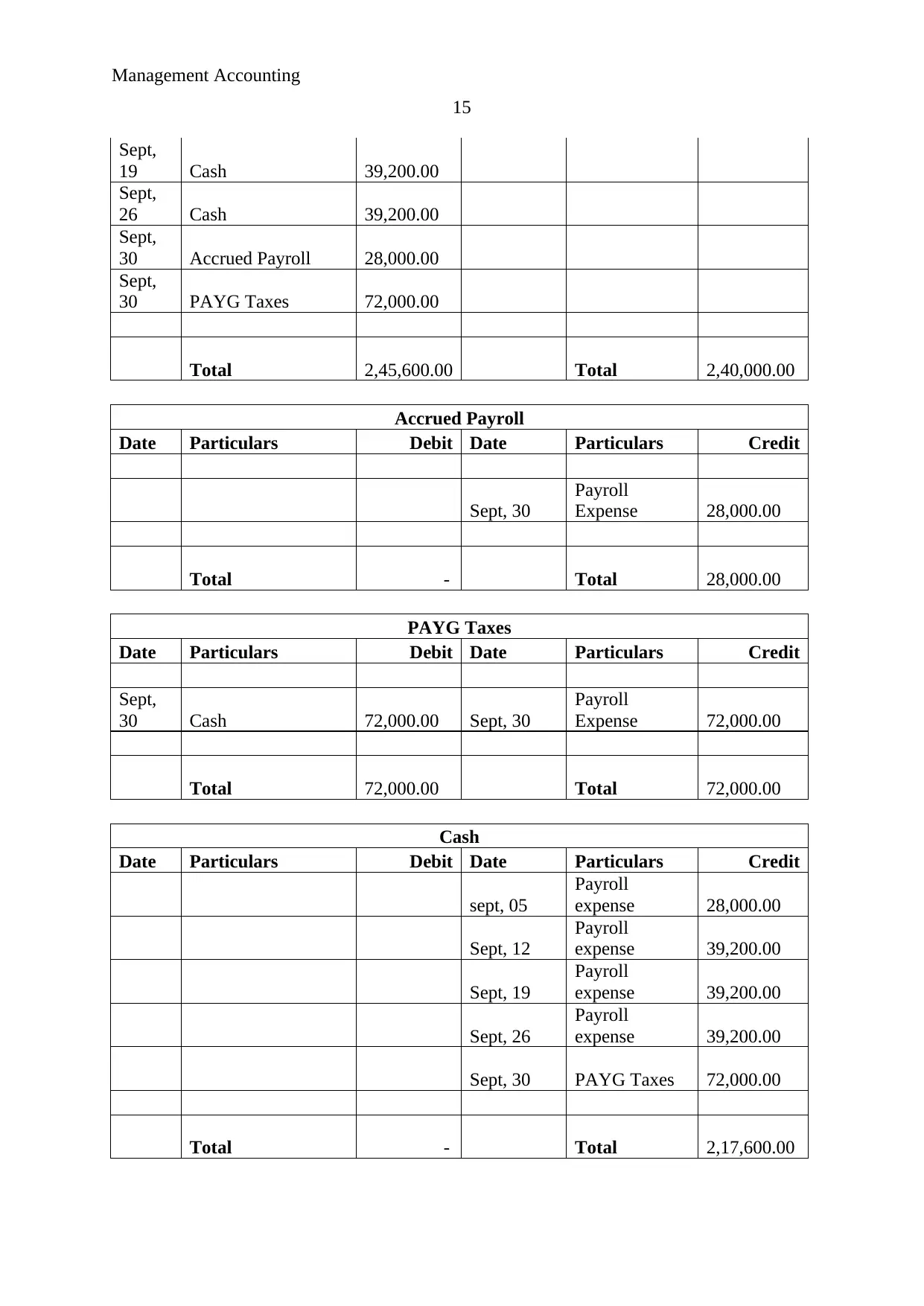

15

Sept,

19 Cash 39,200.00

Sept,

26 Cash 39,200.00

Sept,

30 Accrued Payroll 28,000.00

Sept,

30 PAYG Taxes 72,000.00

Total 2,45,600.00 Total 2,40,000.00

Accrued Payroll

Date Particulars Debit Date Particulars Credit

Sept, 30

Payroll

Expense 28,000.00

Total - Total 28,000.00

PAYG Taxes

Date Particulars Debit Date Particulars Credit

Sept,

30 Cash 72,000.00 Sept, 30

Payroll

Expense 72,000.00

Total 72,000.00 Total 72,000.00

Cash

Date Particulars Debit Date Particulars Credit

sept, 05

Payroll

expense 28,000.00

Sept, 12

Payroll

expense 39,200.00

Sept, 19

Payroll

expense 39,200.00

Sept, 26

Payroll

expense 39,200.00

Sept, 30 PAYG Taxes 72,000.00

Total - Total 2,17,600.00

15

Sept,

19 Cash 39,200.00

Sept,

26 Cash 39,200.00

Sept,

30 Accrued Payroll 28,000.00

Sept,

30 PAYG Taxes 72,000.00

Total 2,45,600.00 Total 2,40,000.00

Accrued Payroll

Date Particulars Debit Date Particulars Credit

Sept, 30

Payroll

Expense 28,000.00

Total - Total 28,000.00

PAYG Taxes

Date Particulars Debit Date Particulars Credit

Sept,

30 Cash 72,000.00 Sept, 30

Payroll

Expense 72,000.00

Total 72,000.00 Total 72,000.00

Cash

Date Particulars Debit Date Particulars Credit

sept, 05

Payroll

expense 28,000.00

Sept, 12

Payroll

expense 39,200.00

Sept, 19

Payroll

expense 39,200.00

Sept, 26

Payroll

expense 39,200.00

Sept, 30 PAYG Taxes 72,000.00

Total - Total 2,17,600.00

Management Accounting

16

Formula view:

16

Formula view:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

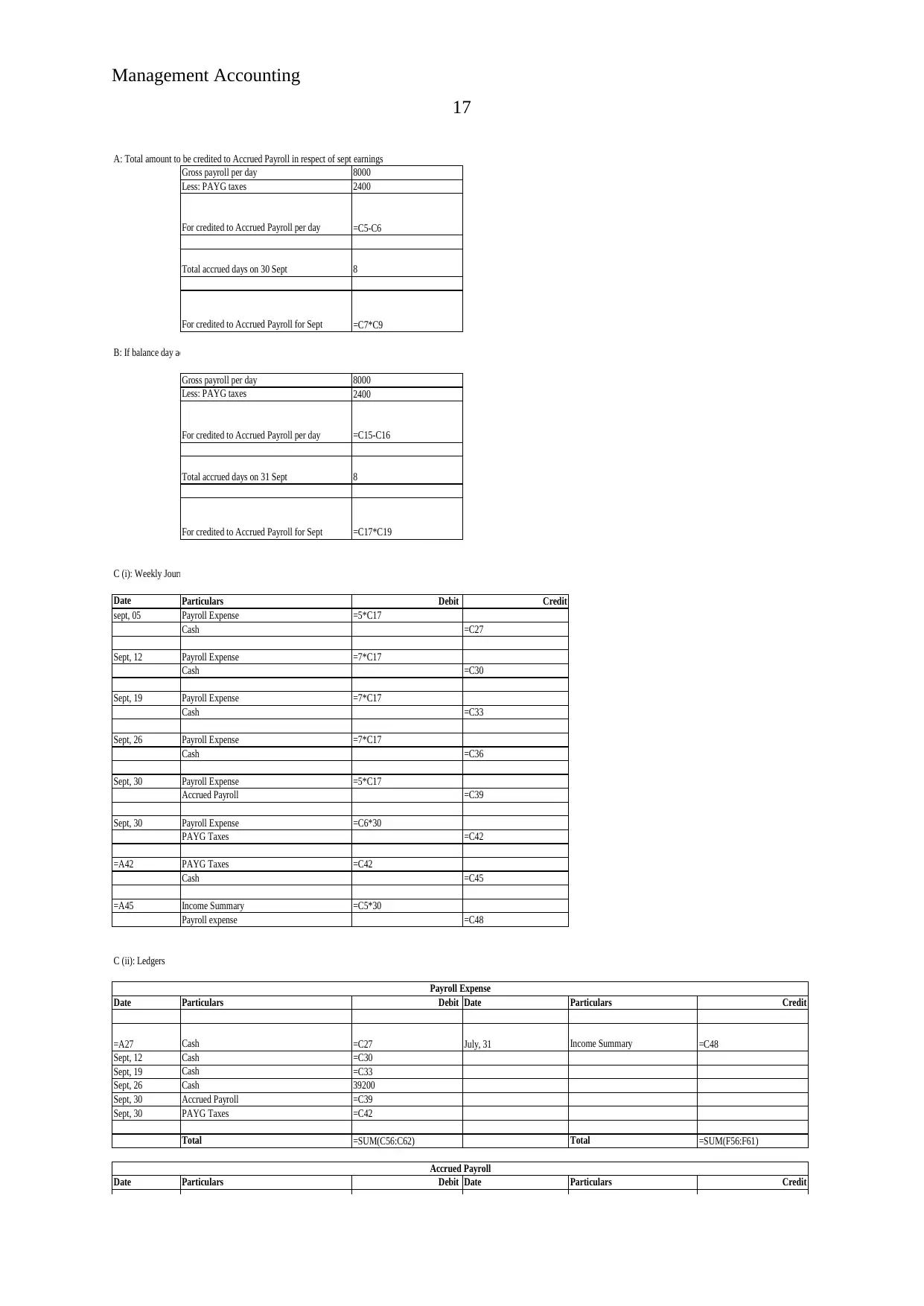

Management Accounting

17

Gross payroll per day 8000

Less: PAYG taxes 2400

For credited to Accrued Payroll per day =C5-C6

Total accrued days on 30 Sept 8

For credited to Accrued Payroll for Sept =C7*C9

B: If balance day adjustments are performed at the end of each month

Gross payroll per day 8000

Less: PAYG taxes 2400

For credited to Accrued Payroll per day =C15-C16

Total accrued days on 31 Sept 8

For credited to Accrued Payroll for Sept =C17*C19

C (i): Weekly Journal Entry

Date Particulars Debit Credit

sept, 05 Payroll Expense =5*C17

Cash =C27

Sept, 12 Payroll Expense =7*C17

Cash =C30

Sept, 19 Payroll Expense =7*C17

Cash =C33

Sept, 26 Payroll Expense =7*C17

Cash =C36

Sept, 30 Payroll Expense =5*C17

Accrued Payroll =C39

Sept, 30 Payroll Expense =C6*30

PAYG Taxes =C42

=A42 PAYG Taxes =C42

Cash =C45

=A45 Income Summary =C5*30

Payroll expense =C48

C (ii): Ledgers

Date Particulars Debit Date Particulars Credit

=A27 Cash =C27 July, 31 Income Summary =C48

Sept, 12 Cash =C30

Sept, 19 Cash =C33

Sept, 26 Cash 39200

Sept, 30 Accrued Payroll =C39

Sept, 30 PAYG Taxes =C42

Total =SUM(C56:C62) Total =SUM(F56:F61)

Date Particulars Debit Date Particulars Credit

Sept, 30 Payroll Expense =C61

Date Particulars Debit Date Particulars Credit

A: Total amount to be credited to Accrued Payroll in respect of sept earnings

Payroll Expense

Accrued Payroll

17

Gross payroll per day 8000

Less: PAYG taxes 2400

For credited to Accrued Payroll per day =C5-C6

Total accrued days on 30 Sept 8

For credited to Accrued Payroll for Sept =C7*C9

B: If balance day adjustments are performed at the end of each month

Gross payroll per day 8000

Less: PAYG taxes 2400

For credited to Accrued Payroll per day =C15-C16

Total accrued days on 31 Sept 8

For credited to Accrued Payroll for Sept =C17*C19

C (i): Weekly Journal Entry

Date Particulars Debit Credit

sept, 05 Payroll Expense =5*C17

Cash =C27

Sept, 12 Payroll Expense =7*C17

Cash =C30

Sept, 19 Payroll Expense =7*C17

Cash =C33

Sept, 26 Payroll Expense =7*C17

Cash =C36

Sept, 30 Payroll Expense =5*C17

Accrued Payroll =C39

Sept, 30 Payroll Expense =C6*30

PAYG Taxes =C42

=A42 PAYG Taxes =C42

Cash =C45

=A45 Income Summary =C5*30

Payroll expense =C48

C (ii): Ledgers

Date Particulars Debit Date Particulars Credit

=A27 Cash =C27 July, 31 Income Summary =C48

Sept, 12 Cash =C30

Sept, 19 Cash =C33

Sept, 26 Cash 39200

Sept, 30 Accrued Payroll =C39

Sept, 30 PAYG Taxes =C42

Total =SUM(C56:C62) Total =SUM(F56:F61)

Date Particulars Debit Date Particulars Credit

Sept, 30 Payroll Expense =C61

Date Particulars Debit Date Particulars Credit

A: Total amount to be credited to Accrued Payroll in respect of sept earnings

Payroll Expense

Accrued Payroll

Management Accounting

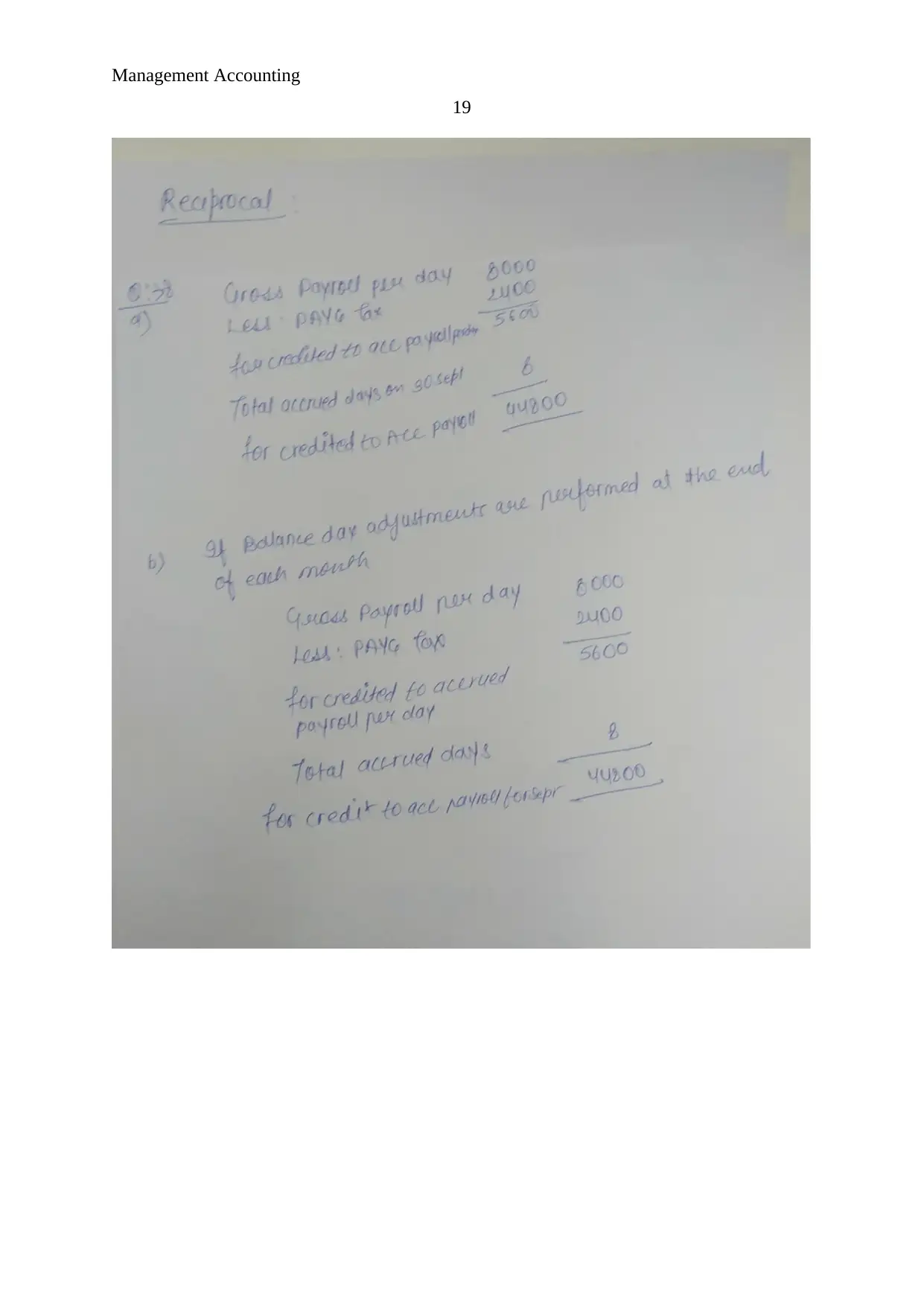

18

Manual solution:

18

Manual solution:

Management Accounting

19

19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

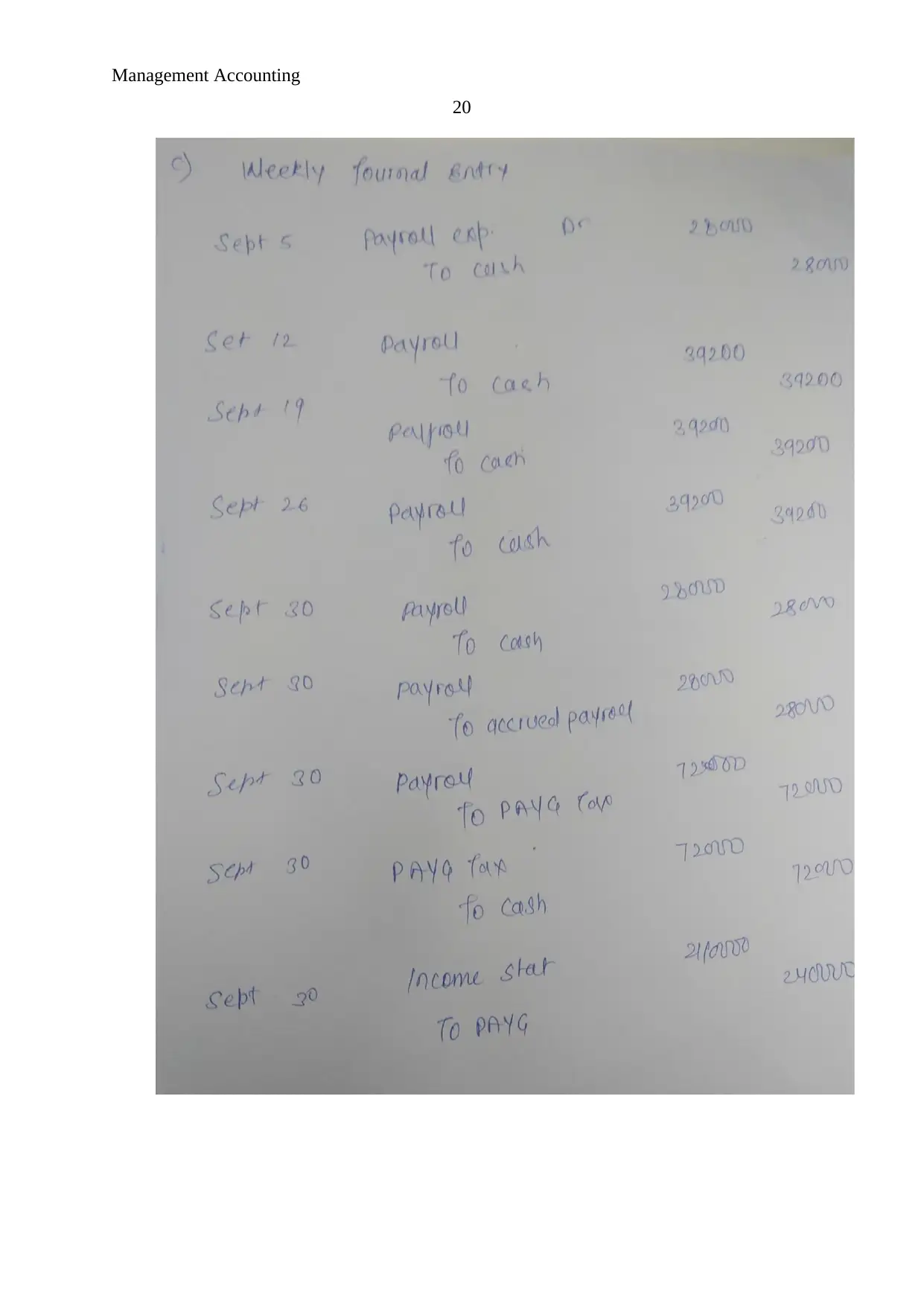

Management Accounting

20

20

Management Accounting

21

Question 9:Activity based costing

Refer to other file.

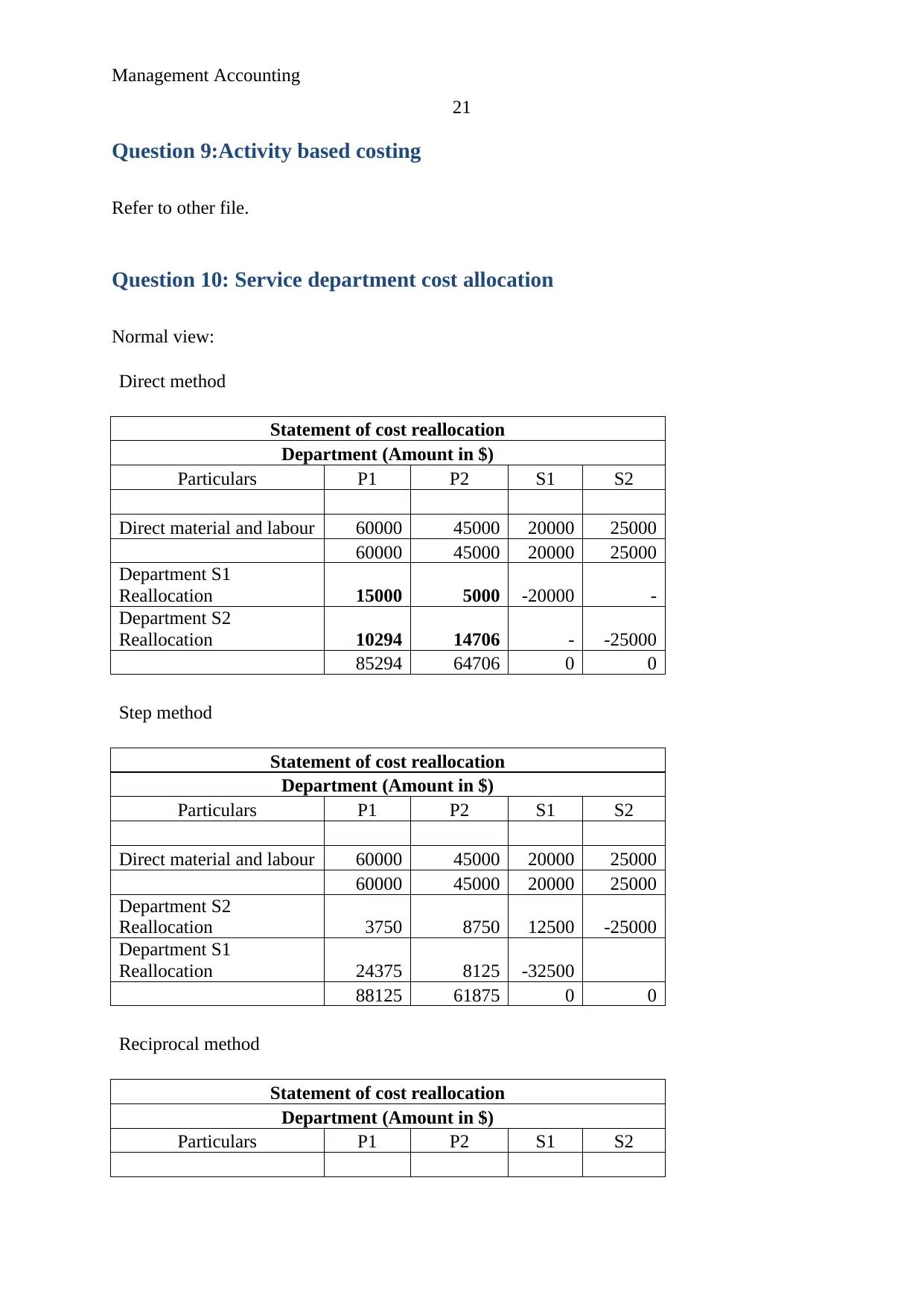

Question 10: Service department cost allocation

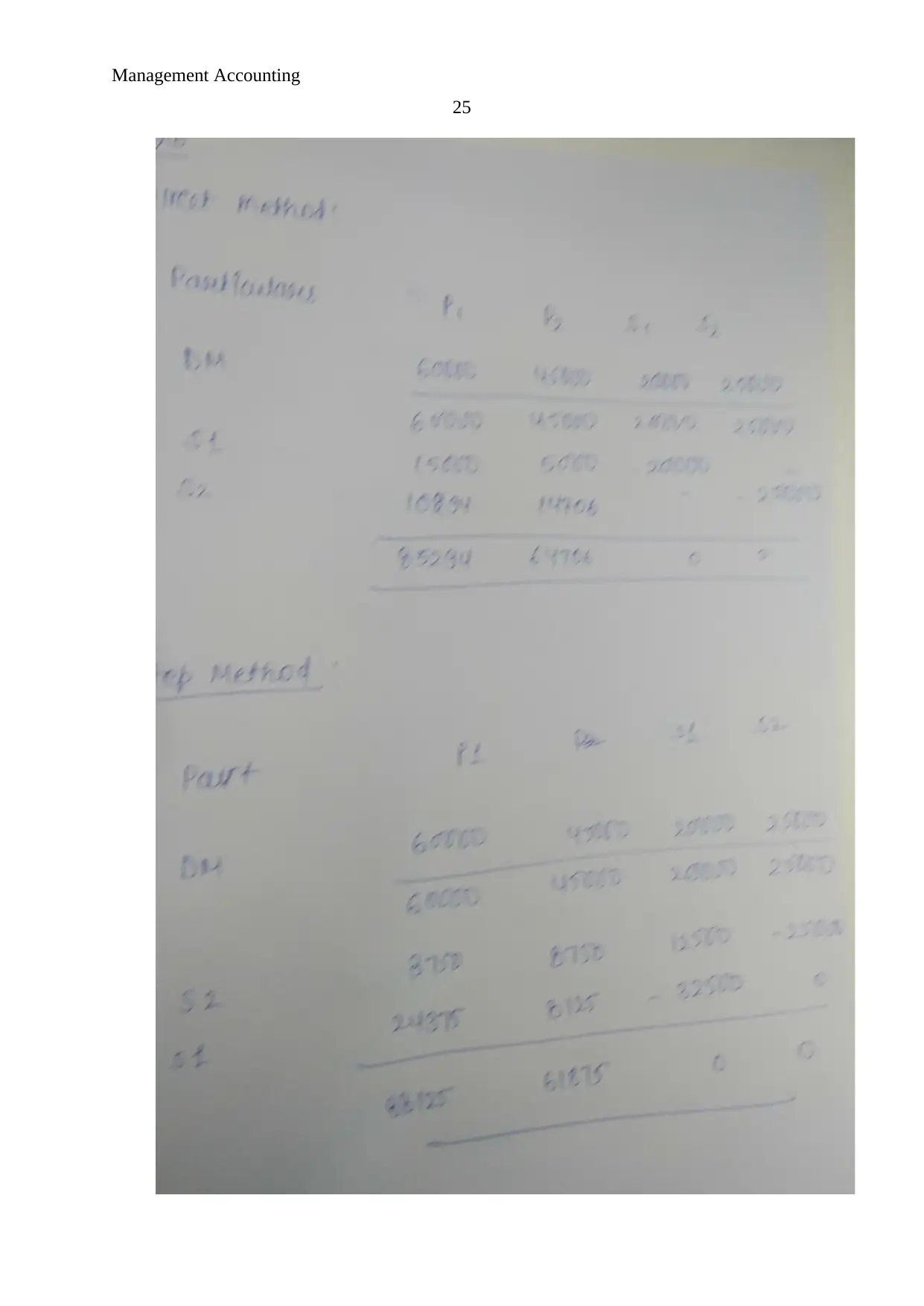

Normal view:

Direct method

Statement of cost reallocation

Department (Amount in $)

Particulars P1 P2 S1 S2

Direct material and labour 60000 45000 20000 25000

60000 45000 20000 25000

Department S1

Reallocation 15000 5000 -20000 -

Department S2

Reallocation 10294 14706 - -25000

85294 64706 0 0

Step method

Statement of cost reallocation

Department (Amount in $)

Particulars P1 P2 S1 S2

Direct material and labour 60000 45000 20000 25000

60000 45000 20000 25000

Department S2

Reallocation 3750 8750 12500 -25000

Department S1

Reallocation 24375 8125 -32500

88125 61875 0 0

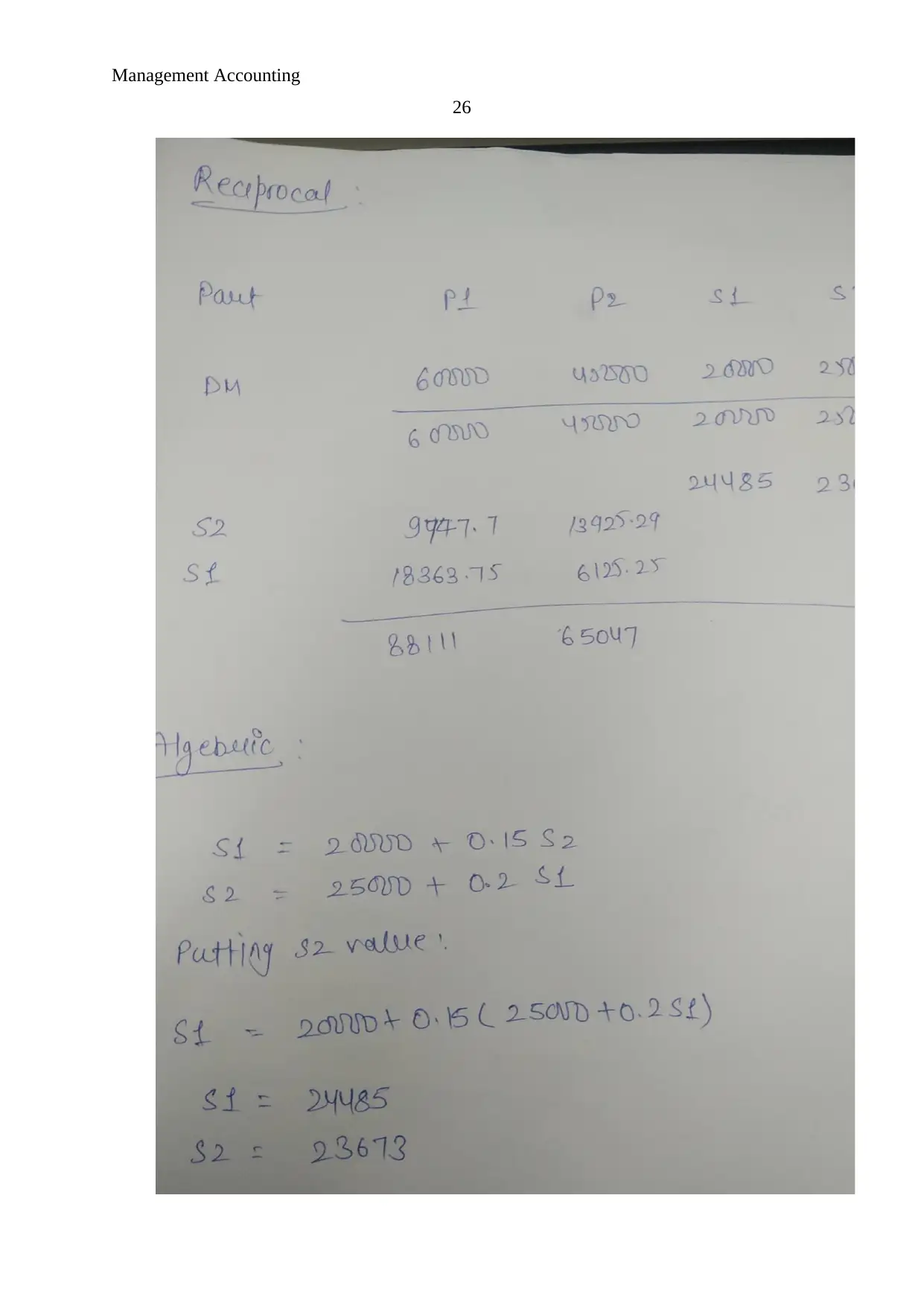

Reciprocal method

Statement of cost reallocation

Department (Amount in $)

Particulars P1 P2 S1 S2

21

Question 9:Activity based costing

Refer to other file.

Question 10: Service department cost allocation

Normal view:

Direct method

Statement of cost reallocation

Department (Amount in $)

Particulars P1 P2 S1 S2

Direct material and labour 60000 45000 20000 25000

60000 45000 20000 25000

Department S1

Reallocation 15000 5000 -20000 -

Department S2

Reallocation 10294 14706 - -25000

85294 64706 0 0

Step method

Statement of cost reallocation

Department (Amount in $)

Particulars P1 P2 S1 S2

Direct material and labour 60000 45000 20000 25000

60000 45000 20000 25000

Department S2

Reallocation 3750 8750 12500 -25000

Department S1

Reallocation 24375 8125 -32500

88125 61875 0 0

Reciprocal method

Statement of cost reallocation

Department (Amount in $)

Particulars P1 P2 S1 S2

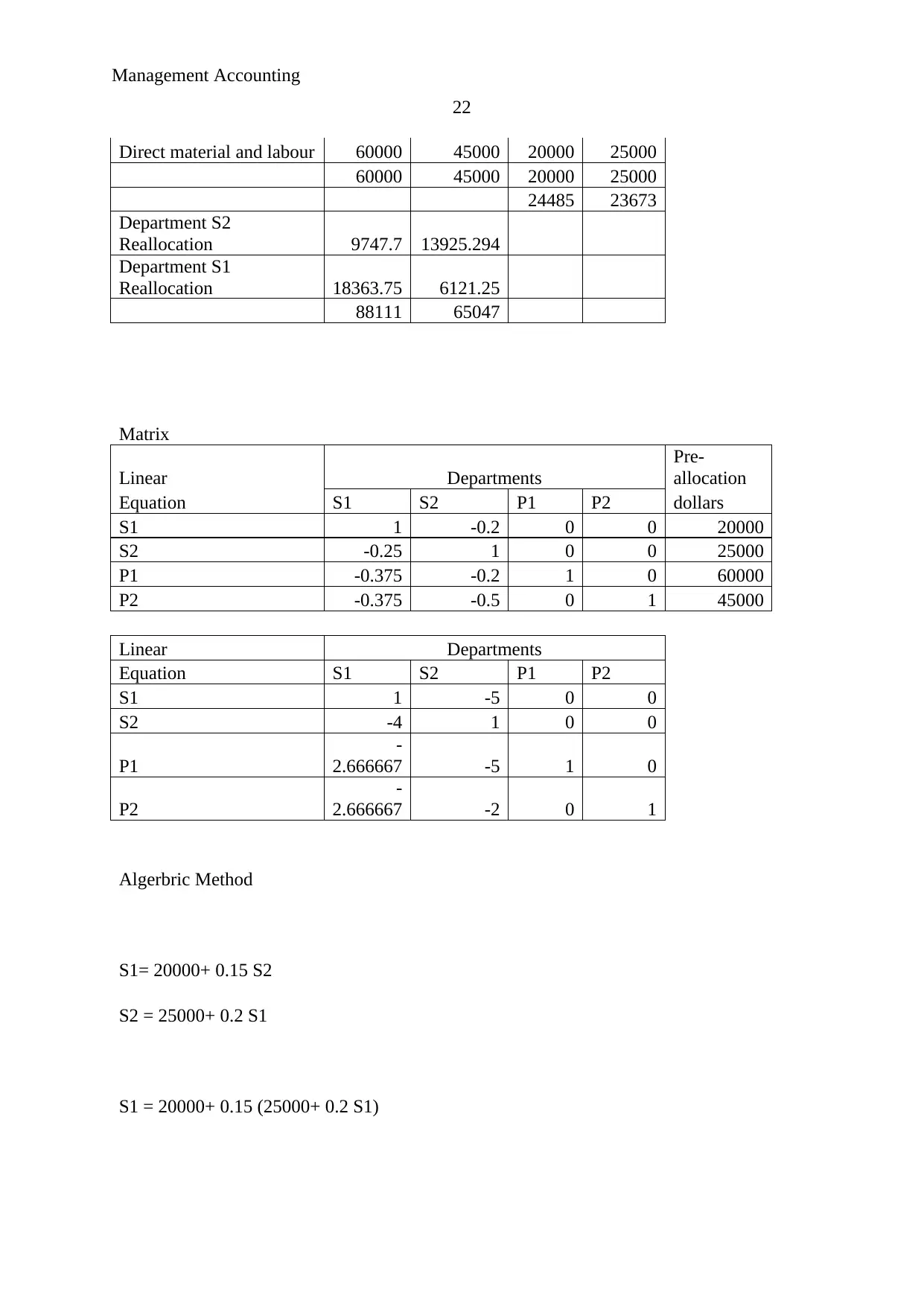

Management Accounting

22

Direct material and labour 60000 45000 20000 25000

60000 45000 20000 25000

24485 23673

Department S2

Reallocation 9747.7 13925.294

Department S1

Reallocation 18363.75 6121.25

88111 65047

Matrix

Linear Departments

Pre-

allocation

Equation S1 S2 P1 P2 dollars

S1 1 -0.2 0 0 20000

S2 -0.25 1 0 0 25000

P1 -0.375 -0.2 1 0 60000

P2 -0.375 -0.5 0 1 45000

Linear Departments

Equation S1 S2 P1 P2

S1 1 -5 0 0

S2 -4 1 0 0

P1

-

2.666667 -5 1 0

P2

-

2.666667 -2 0 1

Algerbric Method

S1= 20000+ 0.15 S2

S2 = 25000+ 0.2 S1

S1 = 20000+ 0.15 (25000+ 0.2 S1)

22

Direct material and labour 60000 45000 20000 25000

60000 45000 20000 25000

24485 23673

Department S2

Reallocation 9747.7 13925.294

Department S1

Reallocation 18363.75 6121.25

88111 65047

Matrix

Linear Departments

Pre-

allocation

Equation S1 S2 P1 P2 dollars

S1 1 -0.2 0 0 20000

S2 -0.25 1 0 0 25000

P1 -0.375 -0.2 1 0 60000

P2 -0.375 -0.5 0 1 45000

Linear Departments

Equation S1 S2 P1 P2

S1 1 -5 0 0

S2 -4 1 0 0

P1

-

2.666667 -5 1 0

P2

-

2.666667 -2 0 1

Algerbric Method

S1= 20000+ 0.15 S2

S2 = 25000+ 0.2 S1

S1 = 20000+ 0.15 (25000+ 0.2 S1)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Management Accounting

23

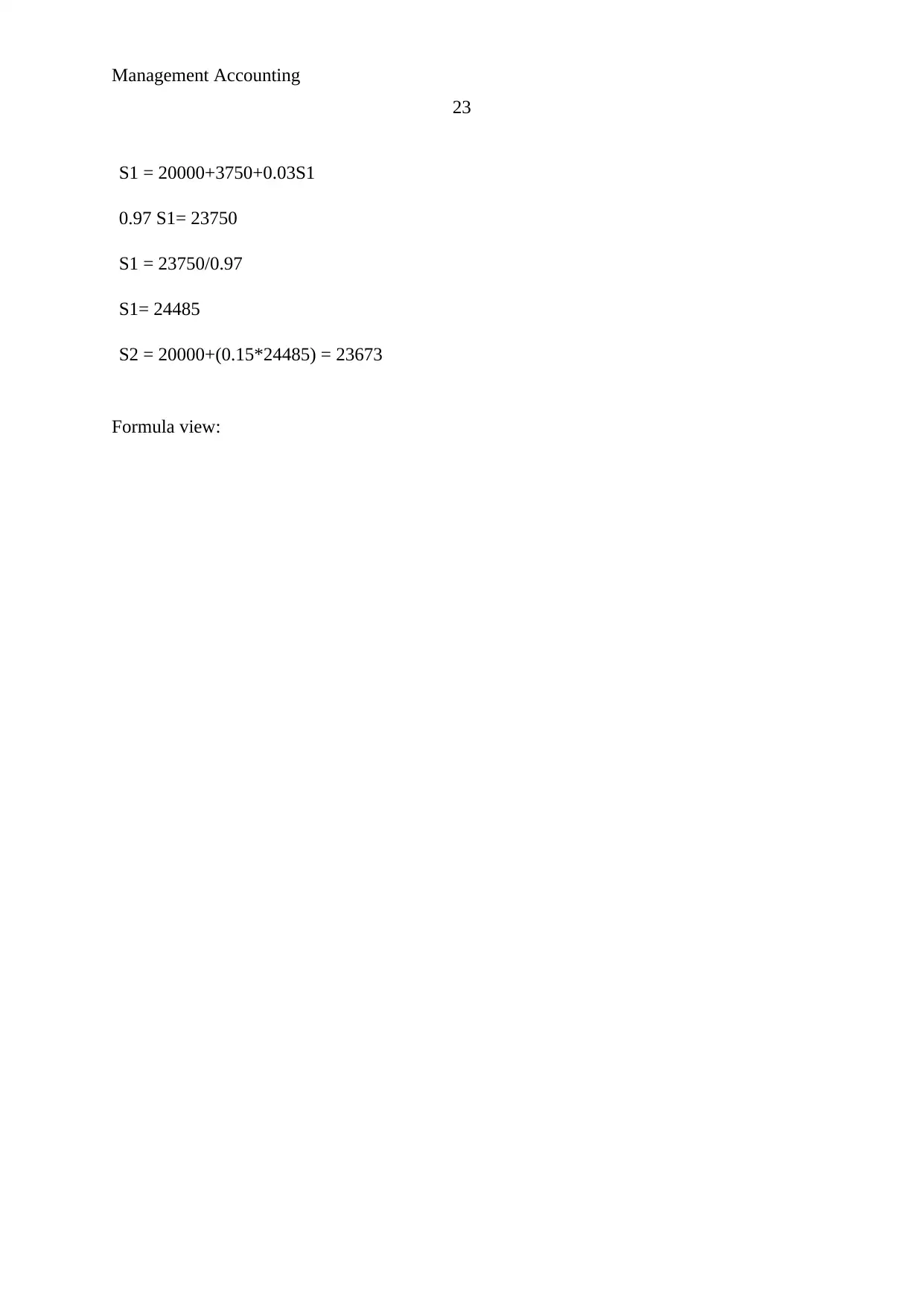

S1 = 20000+3750+0.03S1

0.97 S1= 23750

S1 = 23750/0.97

S1= 24485

S2 = 20000+(0.15*24485) = 23673

Formula view:

23

S1 = 20000+3750+0.03S1

0.97 S1= 23750

S1 = 23750/0.97

S1= 24485

S2 = 20000+(0.15*24485) = 23673

Formula view:

Management Accounting

24

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

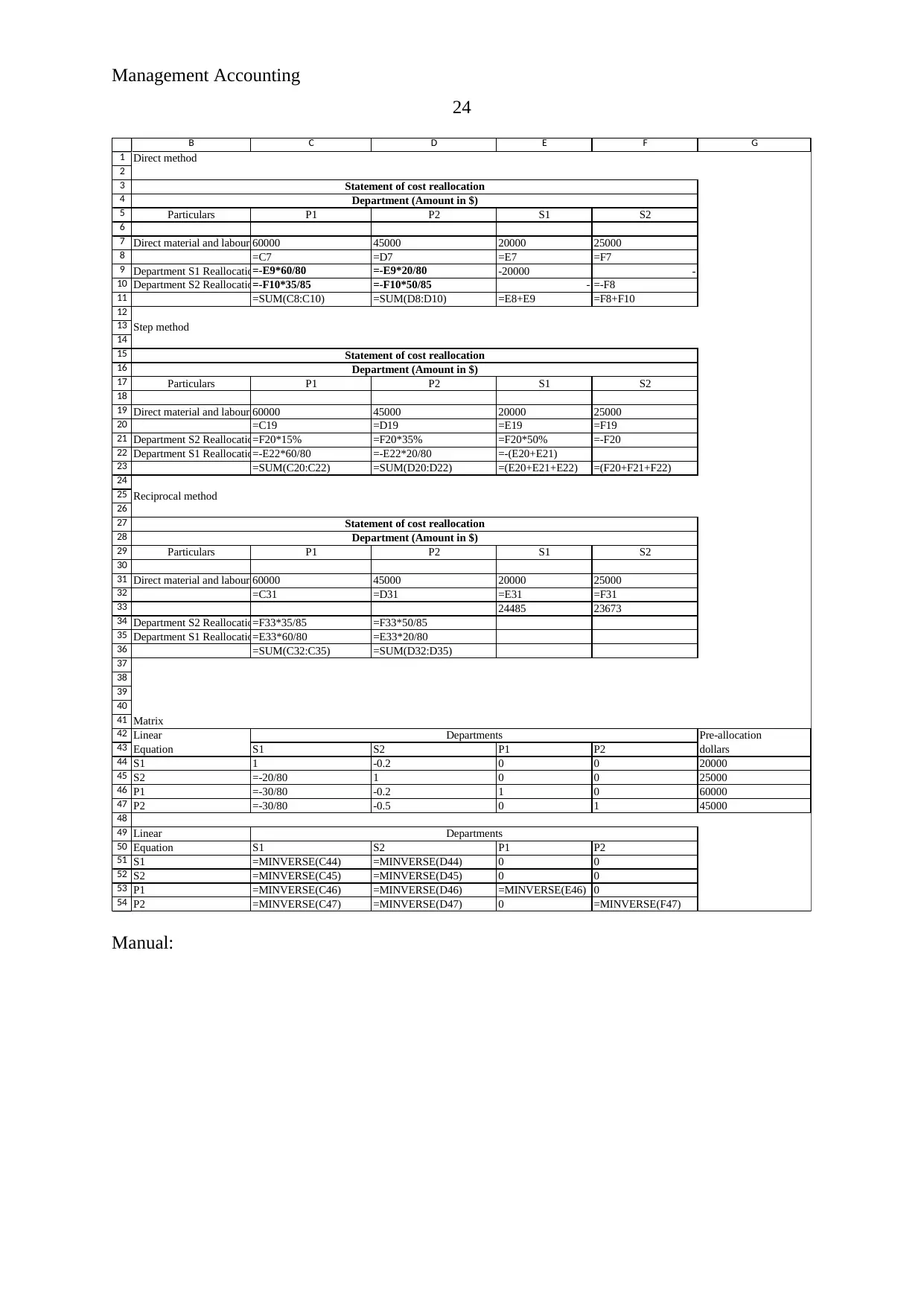

B C D E F G

Direct method

Particulars P1 P2 S1 S2

Direct material and labour 60000 45000 20000 25000

=C7 =D7 =E7 =F7

Department S1 Reallocation=-E9*60/80 =-E9*20/80 -20000 -

Department S2 Reallocation=-F10*35/85 =-F10*50/85 - =-F8

=SUM(C8:C10) =SUM(D8:D10) =E8+E9 =F8+F10

Step method

Particulars P1 P2 S1 S2

Direct material and labour 60000 45000 20000 25000

=C19 =D19 =E19 =F19

Department S2 Reallocation=F20*15% =F20*35% =F20*50% =-F20

Department S1 Reallocation=-E22*60/80 =-E22*20/80 =-(E20+E21)

=SUM(C20:C22) =SUM(D20:D22) =(E20+E21+E22) =(F20+F21+F22)

Reciprocal method

Particulars P1 P2 S1 S2

Direct material and labour 60000 45000 20000 25000

=C31 =D31 =E31 =F31

24485 23673

Department S2 Reallocation=F33*35/85 =F33*50/85

Department S1 Reallocation=E33*60/80 =E33*20/80

=SUM(C32:C35) =SUM(D32:D35)

Matrix

Linear Pre-allocation

Equation S1 S2 P1 P2 dollars

S1 1 -0.2 0 0 20000

S2 =-20/80 1 0 0 25000

P1 =-30/80 -0.2 1 0 60000

P2 =-30/80 -0.5 0 1 45000

Linear

Equation S1 S2 P1 P2

S1 =MINVERSE(C44) =MINVERSE(D44) 0 0

S2 =MINVERSE(C45) =MINVERSE(D45) 0 0

P1 =MINVERSE(C46) =MINVERSE(D46) =MINVERSE(E46) 0

P2 =MINVERSE(C47) =MINVERSE(D47) 0 =MINVERSE(F47)

Departments

Departments

Statement of cost reallocation

Department (Amount in $)

Statement of cost reallocation

Department (Amount in $)

Statement of cost reallocation

Department (Amount in $)

Manual:

24

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

B C D E F G

Direct method

Particulars P1 P2 S1 S2

Direct material and labour 60000 45000 20000 25000

=C7 =D7 =E7 =F7

Department S1 Reallocation=-E9*60/80 =-E9*20/80 -20000 -

Department S2 Reallocation=-F10*35/85 =-F10*50/85 - =-F8

=SUM(C8:C10) =SUM(D8:D10) =E8+E9 =F8+F10

Step method

Particulars P1 P2 S1 S2

Direct material and labour 60000 45000 20000 25000

=C19 =D19 =E19 =F19

Department S2 Reallocation=F20*15% =F20*35% =F20*50% =-F20

Department S1 Reallocation=-E22*60/80 =-E22*20/80 =-(E20+E21)

=SUM(C20:C22) =SUM(D20:D22) =(E20+E21+E22) =(F20+F21+F22)

Reciprocal method

Particulars P1 P2 S1 S2

Direct material and labour 60000 45000 20000 25000

=C31 =D31 =E31 =F31

24485 23673

Department S2 Reallocation=F33*35/85 =F33*50/85

Department S1 Reallocation=E33*60/80 =E33*20/80

=SUM(C32:C35) =SUM(D32:D35)

Matrix

Linear Pre-allocation

Equation S1 S2 P1 P2 dollars

S1 1 -0.2 0 0 20000

S2 =-20/80 1 0 0 25000

P1 =-30/80 -0.2 1 0 60000

P2 =-30/80 -0.5 0 1 45000

Linear

Equation S1 S2 P1 P2

S1 =MINVERSE(C44) =MINVERSE(D44) 0 0

S2 =MINVERSE(C45) =MINVERSE(D45) 0 0

P1 =MINVERSE(C46) =MINVERSE(D46) =MINVERSE(E46) 0

P2 =MINVERSE(C47) =MINVERSE(D47) 0 =MINVERSE(F47)

Departments

Departments

Statement of cost reallocation

Department (Amount in $)

Statement of cost reallocation

Department (Amount in $)

Statement of cost reallocation

Department (Amount in $)

Manual:

Management Accounting

25

25

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting

26

26

Management Accounting

27

References:

Cooper, R., & Kaplan, R. S. (2012). Activity-based systems: Measuring the costs of resource

usage. Accounting Horizons, 6(3), 1.

Garrison, R. H., Noreen, E. W., Brewer, P. C., & McGowan, A. (2010). Managerial

accounting. Issues in Accounting Education, 25(4), 792-793.

Ittner, C. D., Lanen, W. N., & Larcker, D. F. (2002). The association between activity‐based

costing and manufacturing performance. Journal of accounting research, 40(3), 711-

726.

Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2015). Financial & Managerial Accounting.

John Wiley & Sons.

27

References:

Cooper, R., & Kaplan, R. S. (2012). Activity-based systems: Measuring the costs of resource

usage. Accounting Horizons, 6(3), 1.

Garrison, R. H., Noreen, E. W., Brewer, P. C., & McGowan, A. (2010). Managerial

accounting. Issues in Accounting Education, 25(4), 792-793.

Ittner, C. D., Lanen, W. N., & Larcker, D. F. (2002). The association between activity‐based

costing and manufacturing performance. Journal of accounting research, 40(3), 711-

726.

Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2015). Financial & Managerial Accounting.

John Wiley & Sons.

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.