Management Accounting

Added on 2023-05-31

11 Pages2392 Words221 Views

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Management Accounting

Name of the Student

Name of the University

Authors Note

Course ID

1MANAGEMENT ACCOUNTING

Table of Contents

Part 1:.........................................................................................................................................2

1: Cost of Work in Process.....................................................................................................2

2: Cost of Finished Goods Inventories:..................................................................................2

Part 2:.........................................................................................................................................3

Introduction:...............................................................................................................................3

Concept of value chain:..............................................................................................................3

Value chain as cost estimation tool:...........................................................................................4

Segments of Value of Chain:.....................................................................................................5

Primary activities:..................................................................................................................5

Support Activities:.................................................................................................................6

Value Chain at BHP:..................................................................................................................7

Conclusion:................................................................................................................................8

References:.................................................................................................................................9

Table of Contents

Part 1:.........................................................................................................................................2

1: Cost of Work in Process.....................................................................................................2

2: Cost of Finished Goods Inventories:..................................................................................2

Part 2:.........................................................................................................................................3

Introduction:...............................................................................................................................3

Concept of value chain:..............................................................................................................3

Value chain as cost estimation tool:...........................................................................................4

Segments of Value of Chain:.....................................................................................................5

Primary activities:..................................................................................................................5

Support Activities:.................................................................................................................6

Value Chain at BHP:..................................................................................................................7

Conclusion:................................................................................................................................8

References:.................................................................................................................................9

2MANAGEMENT ACCOUNTING

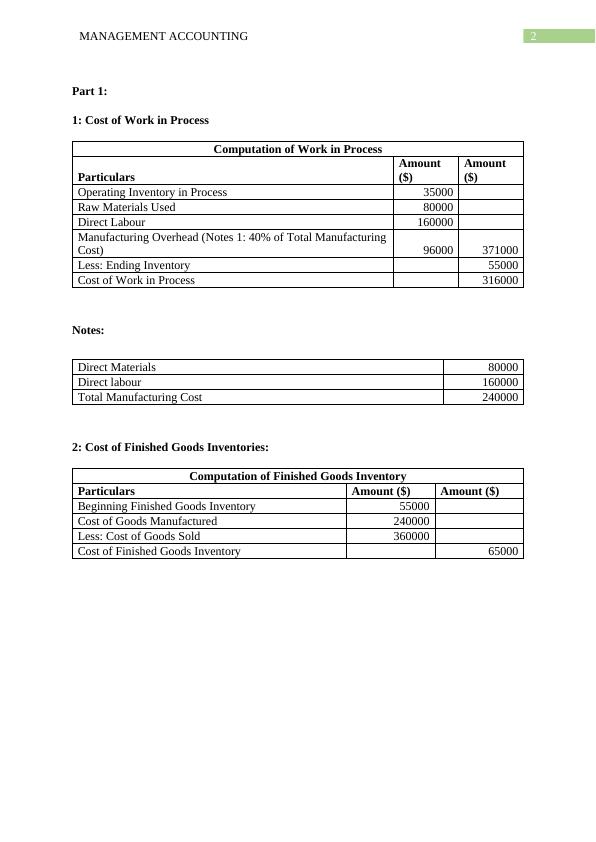

Part 1:

1: Cost of Work in Process

Computation of Work in Process

Particulars

Amount

($)

Amount

($)

Operating Inventory in Process 35000

Raw Materials Used 80000

Direct Labour 160000

Manufacturing Overhead (Notes 1: 40% of Total Manufacturing

Cost) 96000 371000

Less: Ending Inventory 55000

Cost of Work in Process 316000

Notes:

Direct Materials 80000

Direct labour 160000

Total Manufacturing Cost 240000

2: Cost of Finished Goods Inventories:

Computation of Finished Goods Inventory

Particulars Amount ($) Amount ($)

Beginning Finished Goods Inventory 55000

Cost of Goods Manufactured 240000

Less: Cost of Goods Sold 360000

Cost of Finished Goods Inventory 65000

Part 1:

1: Cost of Work in Process

Computation of Work in Process

Particulars

Amount

($)

Amount

($)

Operating Inventory in Process 35000

Raw Materials Used 80000

Direct Labour 160000

Manufacturing Overhead (Notes 1: 40% of Total Manufacturing

Cost) 96000 371000

Less: Ending Inventory 55000

Cost of Work in Process 316000

Notes:

Direct Materials 80000

Direct labour 160000

Total Manufacturing Cost 240000

2: Cost of Finished Goods Inventories:

Computation of Finished Goods Inventory

Particulars Amount ($) Amount ($)

Beginning Finished Goods Inventory 55000

Cost of Goods Manufactured 240000

Less: Cost of Goods Sold 360000

Cost of Finished Goods Inventory 65000

3MANAGEMENT ACCOUNTING

Part 2:

Introduction:

The notion of value chain is entirely based on the process view of the company, the

impression of viewing a manufacturing company as the system that are made up of the

subsystems each with the inputs, transformation procedure and outputs (Kaplan and Atkinson

2015). The activities of value chain are usually conducted to determine the cost and affects

profits. Majority of the organizations that are indulged in the hundreds of activities are

mainly engaged in the process of converting the inputs to outputs.

The corporate value chain, accounting and reporting standards enables the companies

to assess their whole value chain emission effect and recognizes where to place their focus.

The present report would be providing the useful framework of value chain and how the

concept of value chain is utilised to determine costs (Langfield-Smith et al. 2017). The report

would be describing each segments of value chain and would provide explanation regarding

costs in numerous segment of the value chain that are useful for managers. Additionally, BHP

has been selected to explain the main purpose of value chain in the manufacturing companies.

Concept of value chain:

Value chain is defined as the complete range of activities together with the design,

production, distribution and marketing conducted by the business to bring into the existence

the product and service from the concept to the delivery (Chak and Fung 2015). For corporate

firms that manufacture goods, the value chain beings with the use of raw materials to

manufacture their products and comprises of everything that is added prior to selling the

product to customers.

Part 2:

Introduction:

The notion of value chain is entirely based on the process view of the company, the

impression of viewing a manufacturing company as the system that are made up of the

subsystems each with the inputs, transformation procedure and outputs (Kaplan and Atkinson

2015). The activities of value chain are usually conducted to determine the cost and affects

profits. Majority of the organizations that are indulged in the hundreds of activities are

mainly engaged in the process of converting the inputs to outputs.

The corporate value chain, accounting and reporting standards enables the companies

to assess their whole value chain emission effect and recognizes where to place their focus.

The present report would be providing the useful framework of value chain and how the

concept of value chain is utilised to determine costs (Langfield-Smith et al. 2017). The report

would be describing each segments of value chain and would provide explanation regarding

costs in numerous segment of the value chain that are useful for managers. Additionally, BHP

has been selected to explain the main purpose of value chain in the manufacturing companies.

Concept of value chain:

Value chain is defined as the complete range of activities together with the design,

production, distribution and marketing conducted by the business to bring into the existence

the product and service from the concept to the delivery (Chak and Fung 2015). For corporate

firms that manufacture goods, the value chain beings with the use of raw materials to

manufacture their products and comprises of everything that is added prior to selling the

product to customers.

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Cost of Work in Process: 4 Value Chain as Cost Estimatorlg...

|11

|2355

|455

BAP22 - Management Accountinglg...

|9

|2231

|50

Value Chain in Manufacturing Accounting Contents Part 3: Cost 4 Segment of Value Chain 5 Purpose of Value Chainlg...

|10

|2186

|164

Value Chain Analysis and Cost Estimation for Natural Pulp Ltd and Austal Shipslg...

|9

|2055

|289

Marginal Costing, Absorption Costing, and Income Statementlg...

|13

|756

|77

Management Accounting (Task 2)lg...

|13

|545

|48