Management Accounting: Cost Calculation, Schedule Preparation, and Profit Analysis

VerifiedAdded on 2023/06/18

|13

|2547

|227

AI Summary

This article covers the calculation of variable cost per occupied bed, total fixed operating cost, total operating cost at 70% occupancy, cost computation, schedule preparation, income statement preparation, profit analysis using absorption costing and marginal costing, break-even point calculation, and more related to management accounting.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

QUESTION 1..................................................................................................................................2

1)..................................................................................................................................................2

a) Calculation of Variable cost per occupied bed on a daily basis using high-low method........2

b) Calculation of total fixed operating cost per month using high-low method..........................2

2) Calculation of total operating cost at 70% occupancy............................................................2

3) Computation of following cost................................................................................................3

QUESTION 2..................................................................................................................................3

QUESTION 3..................................................................................................................................6

QUESTION 6..................................................................................................................................8

a) Calculation of Total Contribution for 2017.............................................................................8

b) Calculation of Break-even points in units...............................................................................9

c) Calculation of sales unit to make desired net profit................................................................9

d) Effect on break-even point if selling price reduced by 15%.................................................10

e) Calculation of break-even point in units if variable cost get increases by £2.25..................10

f) Meaning of contribution margin ratio and its uses in business planning...............................10

REFERENCES..............................................................................................................................12

1

QUESTION 1..................................................................................................................................2

1)..................................................................................................................................................2

a) Calculation of Variable cost per occupied bed on a daily basis using high-low method........2

b) Calculation of total fixed operating cost per month using high-low method..........................2

2) Calculation of total operating cost at 70% occupancy............................................................2

3) Computation of following cost................................................................................................3

QUESTION 2..................................................................................................................................3

QUESTION 3..................................................................................................................................6

QUESTION 6..................................................................................................................................8

a) Calculation of Total Contribution for 2017.............................................................................8

b) Calculation of Break-even points in units...............................................................................9

c) Calculation of sales unit to make desired net profit................................................................9

d) Effect on break-even point if selling price reduced by 15%.................................................10

e) Calculation of break-even point in units if variable cost get increases by £2.25..................10

f) Meaning of contribution margin ratio and its uses in business planning...............................10

REFERENCES..............................................................................................................................12

1

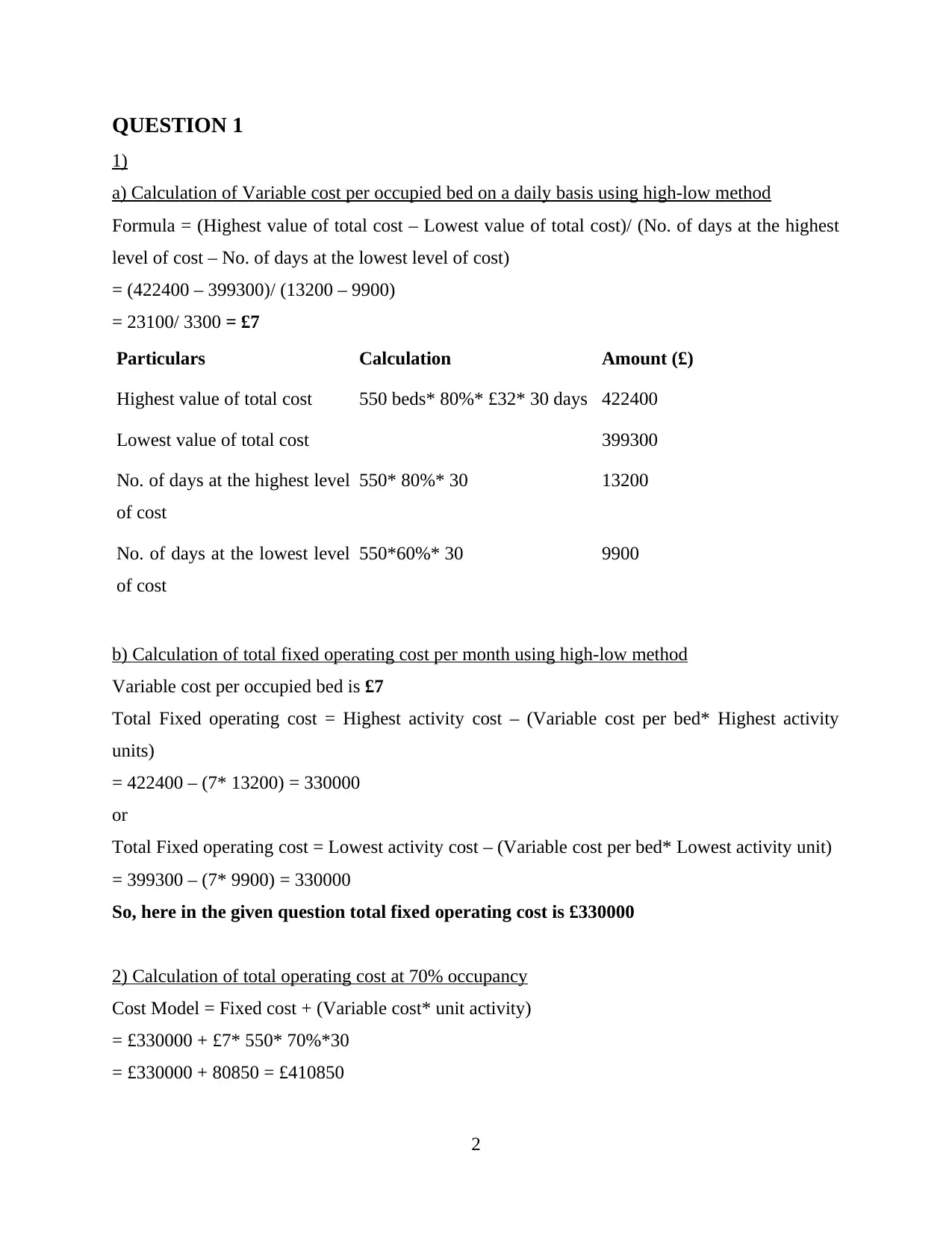

QUESTION 1

1)

a) Calculation of Variable cost per occupied bed on a daily basis using high-low method

Formula = (Highest value of total cost – Lowest value of total cost)/ (No. of days at the highest

level of cost – No. of days at the lowest level of cost)

= (422400 – 399300)/ (13200 – 9900)

= 23100/ 3300 = £7

Particulars Calculation Amount (£)

Highest value of total cost 550 beds* 80%* £32* 30 days 422400

Lowest value of total cost 399300

No. of days at the highest level

of cost

550* 80%* 30 13200

No. of days at the lowest level

of cost

550*60%* 30 9900

b) Calculation of total fixed operating cost per month using high-low method

Variable cost per occupied bed is £7

Total Fixed operating cost = Highest activity cost – (Variable cost per bed* Highest activity

units)

= 422400 – (7* 13200) = 330000

or

Total Fixed operating cost = Lowest activity cost – (Variable cost per bed* Lowest activity unit)

= 399300 – (7* 9900) = 330000

So, here in the given question total fixed operating cost is £330000

2) Calculation of total operating cost at 70% occupancy

Cost Model = Fixed cost + (Variable cost* unit activity)

= £330000 + £7* 550* 70%*30

= £330000 + 80850 = £410850

2

1)

a) Calculation of Variable cost per occupied bed on a daily basis using high-low method

Formula = (Highest value of total cost – Lowest value of total cost)/ (No. of days at the highest

level of cost – No. of days at the lowest level of cost)

= (422400 – 399300)/ (13200 – 9900)

= 23100/ 3300 = £7

Particulars Calculation Amount (£)

Highest value of total cost 550 beds* 80%* £32* 30 days 422400

Lowest value of total cost 399300

No. of days at the highest level

of cost

550* 80%* 30 13200

No. of days at the lowest level

of cost

550*60%* 30 9900

b) Calculation of total fixed operating cost per month using high-low method

Variable cost per occupied bed is £7

Total Fixed operating cost = Highest activity cost – (Variable cost per bed* Highest activity

units)

= 422400 – (7* 13200) = 330000

or

Total Fixed operating cost = Lowest activity cost – (Variable cost per bed* Lowest activity unit)

= 399300 – (7* 9900) = 330000

So, here in the given question total fixed operating cost is £330000

2) Calculation of total operating cost at 70% occupancy

Cost Model = Fixed cost + (Variable cost* unit activity)

= £330000 + £7* 550* 70%*30

= £330000 + 80850 = £410850

2

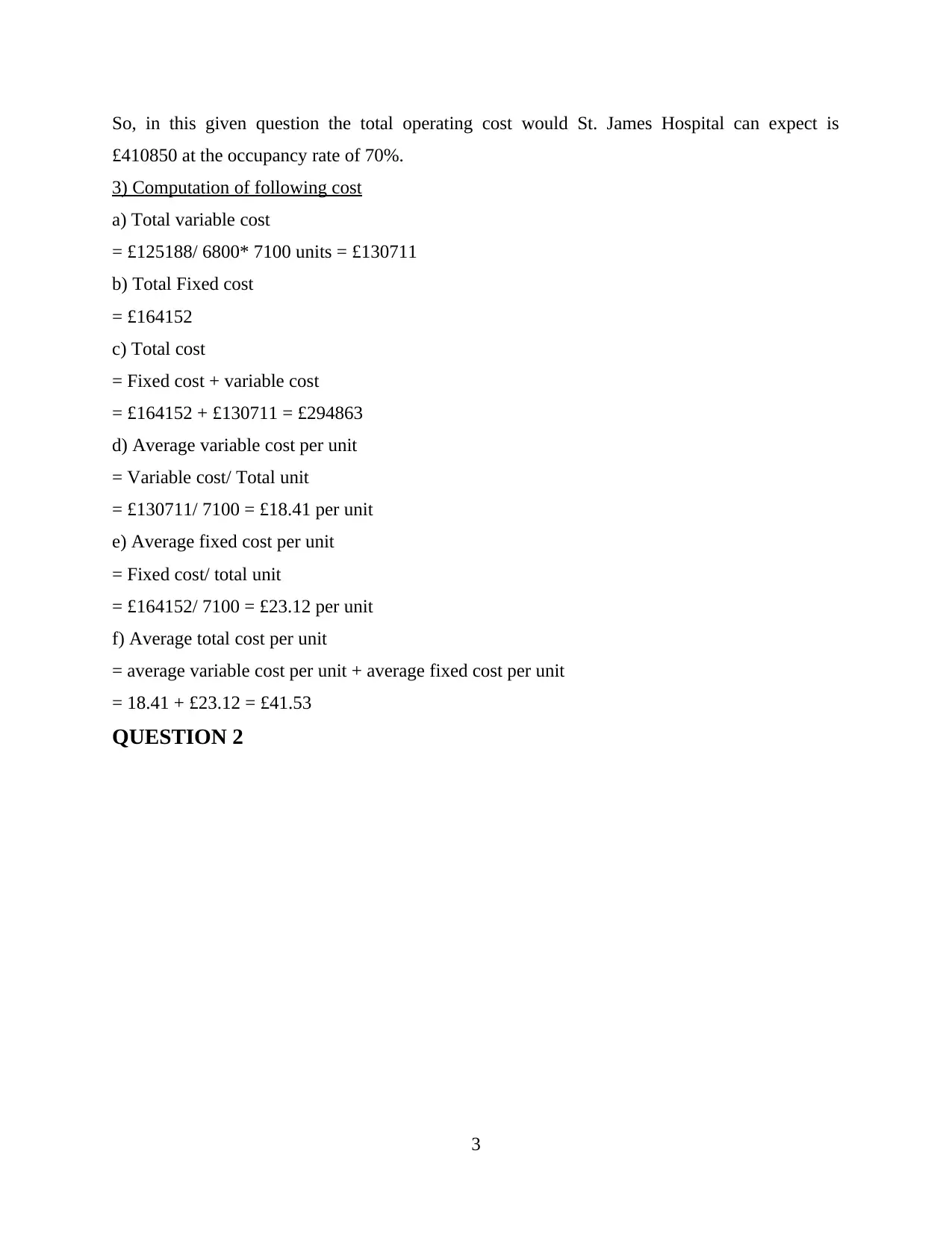

So, in this given question the total operating cost would St. James Hospital can expect is

£410850 at the occupancy rate of 70%.

3) Computation of following cost

a) Total variable cost

= £125188/ 6800* 7100 units = £130711

b) Total Fixed cost

= £164152

c) Total cost

= Fixed cost + variable cost

= £164152 + £130711 = £294863

d) Average variable cost per unit

= Variable cost/ Total unit

= £130711/ 7100 = £18.41 per unit

e) Average fixed cost per unit

= Fixed cost/ total unit

= £164152/ 7100 = £23.12 per unit

f) Average total cost per unit

= average variable cost per unit + average fixed cost per unit

= 18.41 + £23.12 = £41.53

QUESTION 2

3

£410850 at the occupancy rate of 70%.

3) Computation of following cost

a) Total variable cost

= £125188/ 6800* 7100 units = £130711

b) Total Fixed cost

= £164152

c) Total cost

= Fixed cost + variable cost

= £164152 + £130711 = £294863

d) Average variable cost per unit

= Variable cost/ Total unit

= £130711/ 7100 = £18.41 per unit

e) Average fixed cost per unit

= Fixed cost/ total unit

= £164152/ 7100 = £23.12 per unit

f) Average total cost per unit

= average variable cost per unit + average fixed cost per unit

= 18.41 + £23.12 = £41.53

QUESTION 2

3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

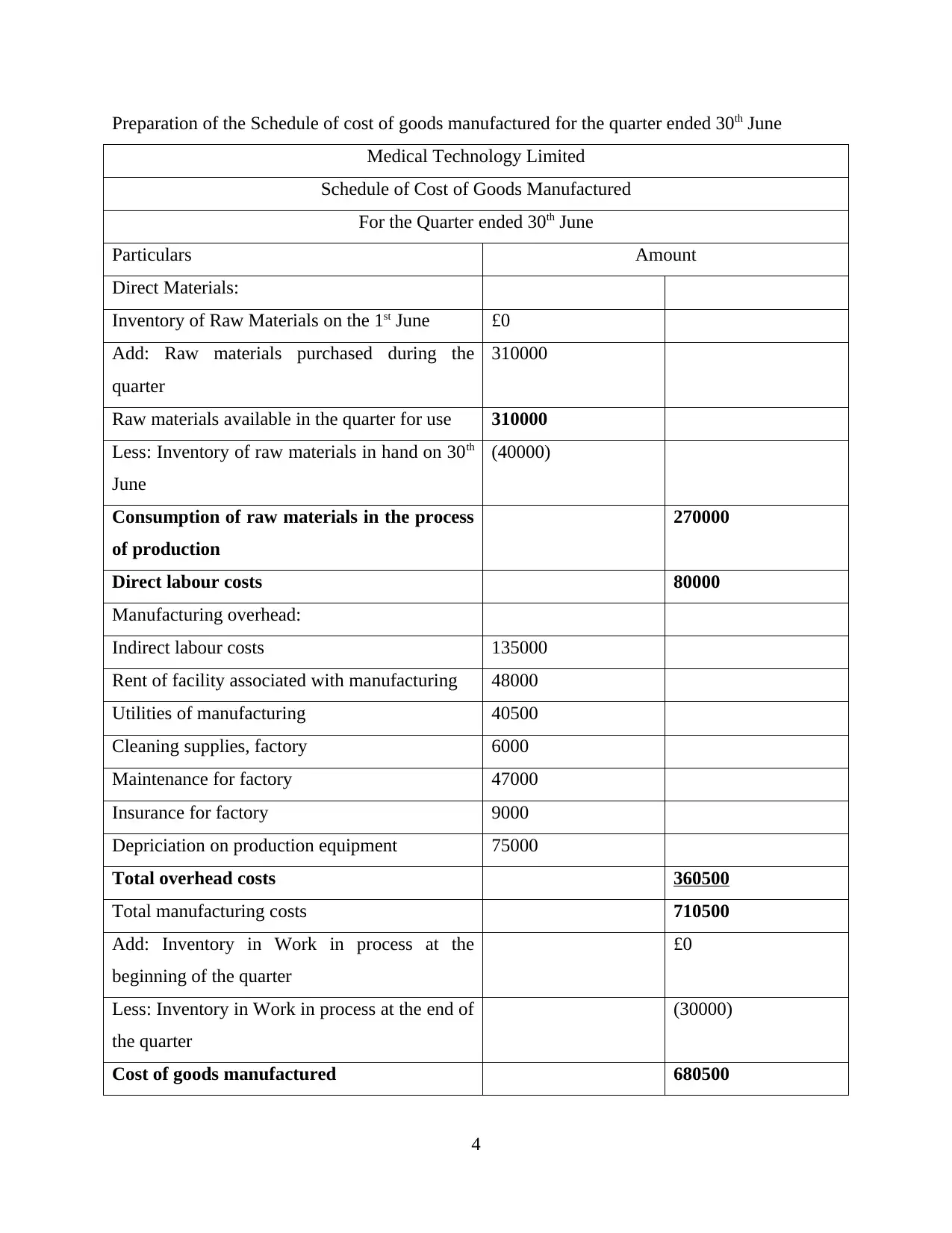

Preparation of the Schedule of cost of goods manufactured for the quarter ended 30th June

Medical Technology Limited

Schedule of Cost of Goods Manufactured

For the Quarter ended 30th June

Particulars Amount

Direct Materials:

Inventory of Raw Materials on the 1st June £0

Add: Raw materials purchased during the

quarter

310000

Raw materials available in the quarter for use 310000

Less: Inventory of raw materials in hand on 30th

June

(40000)

Consumption of raw materials in the process

of production

270000

Direct labour costs 80000

Manufacturing overhead:

Indirect labour costs 135000

Rent of facility associated with manufacturing 48000

Utilities of manufacturing 40500

Cleaning supplies, factory 6000

Maintenance for factory 47000

Insurance for factory 9000

Depriciation on production equipment 75000

Total overhead costs 360500

Total manufacturing costs 710500

Add: Inventory in Work in process at the

beginning of the quarter

£0

Less: Inventory in Work in process at the end of

the quarter

(30000)

Cost of goods manufactured 680500

4

Medical Technology Limited

Schedule of Cost of Goods Manufactured

For the Quarter ended 30th June

Particulars Amount

Direct Materials:

Inventory of Raw Materials on the 1st June £0

Add: Raw materials purchased during the

quarter

310000

Raw materials available in the quarter for use 310000

Less: Inventory of raw materials in hand on 30th

June

(40000)

Consumption of raw materials in the process

of production

270000

Direct labour costs 80000

Manufacturing overhead:

Indirect labour costs 135000

Rent of facility associated with manufacturing 48000

Utilities of manufacturing 40500

Cleaning supplies, factory 6000

Maintenance for factory 47000

Insurance for factory 9000

Depriciation on production equipment 75000

Total overhead costs 360500

Total manufacturing costs 710500

Add: Inventory in Work in process at the

beginning of the quarter

£0

Less: Inventory in Work in process at the end of

the quarter

(30000)

Cost of goods manufactured 680500

4

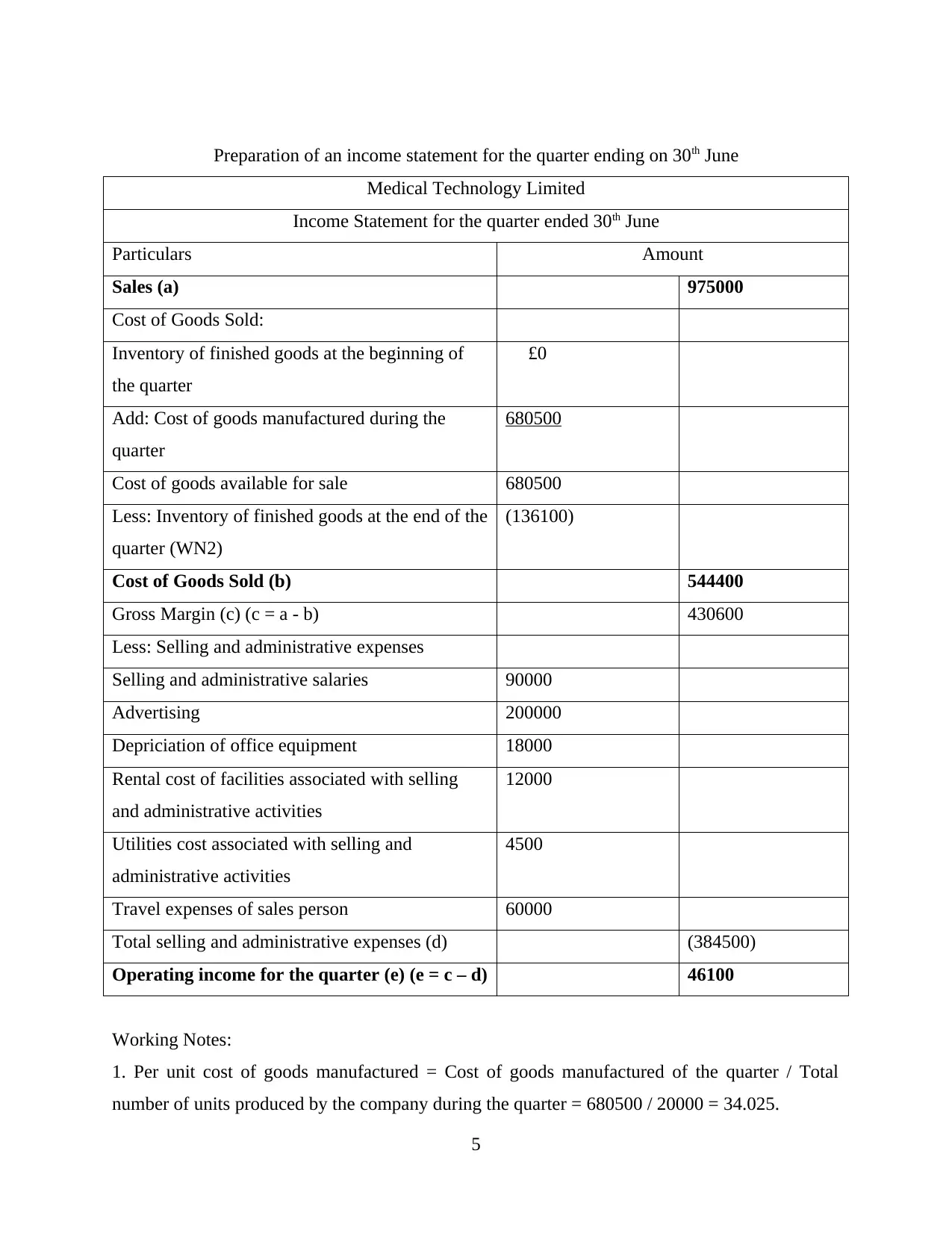

Preparation of an income statement for the quarter ending on 30th June

Medical Technology Limited

Income Statement for the quarter ended 30th June

Particulars Amount

Sales (a) 975000

Cost of Goods Sold:

Inventory of finished goods at the beginning of

the quarter

£0

Add: Cost of goods manufactured during the

quarter

680500

Cost of goods available for sale 680500

Less: Inventory of finished goods at the end of the

quarter (WN2)

(136100)

Cost of Goods Sold (b) 544400

Gross Margin (c) (c = a - b) 430600

Less: Selling and administrative expenses

Selling and administrative salaries 90000

Advertising 200000

Depriciation of office equipment 18000

Rental cost of facilities associated with selling

and administrative activities

12000

Utilities cost associated with selling and

administrative activities

4500

Travel expenses of sales person 60000

Total selling and administrative expenses (d) (384500)

Operating income for the quarter (e) (e = c – d) 46100

Working Notes:

1. Per unit cost of goods manufactured = Cost of goods manufactured of the quarter / Total

number of units produced by the company during the quarter = 680500 / 20000 = 34.025.

5

Medical Technology Limited

Income Statement for the quarter ended 30th June

Particulars Amount

Sales (a) 975000

Cost of Goods Sold:

Inventory of finished goods at the beginning of

the quarter

£0

Add: Cost of goods manufactured during the

quarter

680500

Cost of goods available for sale 680500

Less: Inventory of finished goods at the end of the

quarter (WN2)

(136100)

Cost of Goods Sold (b) 544400

Gross Margin (c) (c = a - b) 430600

Less: Selling and administrative expenses

Selling and administrative salaries 90000

Advertising 200000

Depriciation of office equipment 18000

Rental cost of facilities associated with selling

and administrative activities

12000

Utilities cost associated with selling and

administrative activities

4500

Travel expenses of sales person 60000

Total selling and administrative expenses (d) (384500)

Operating income for the quarter (e) (e = c – d) 46100

Working Notes:

1. Per unit cost of goods manufactured = Cost of goods manufactured of the quarter / Total

number of units produced by the company during the quarter = 680500 / 20000 = 34.025.

5

2. Cost of Inventory of finished goods at the end of the quarter = number of units of finished

goods remained at the end of the quarter * per unit cost of goods manufactured

= 4000 * 34.025 = 136100.

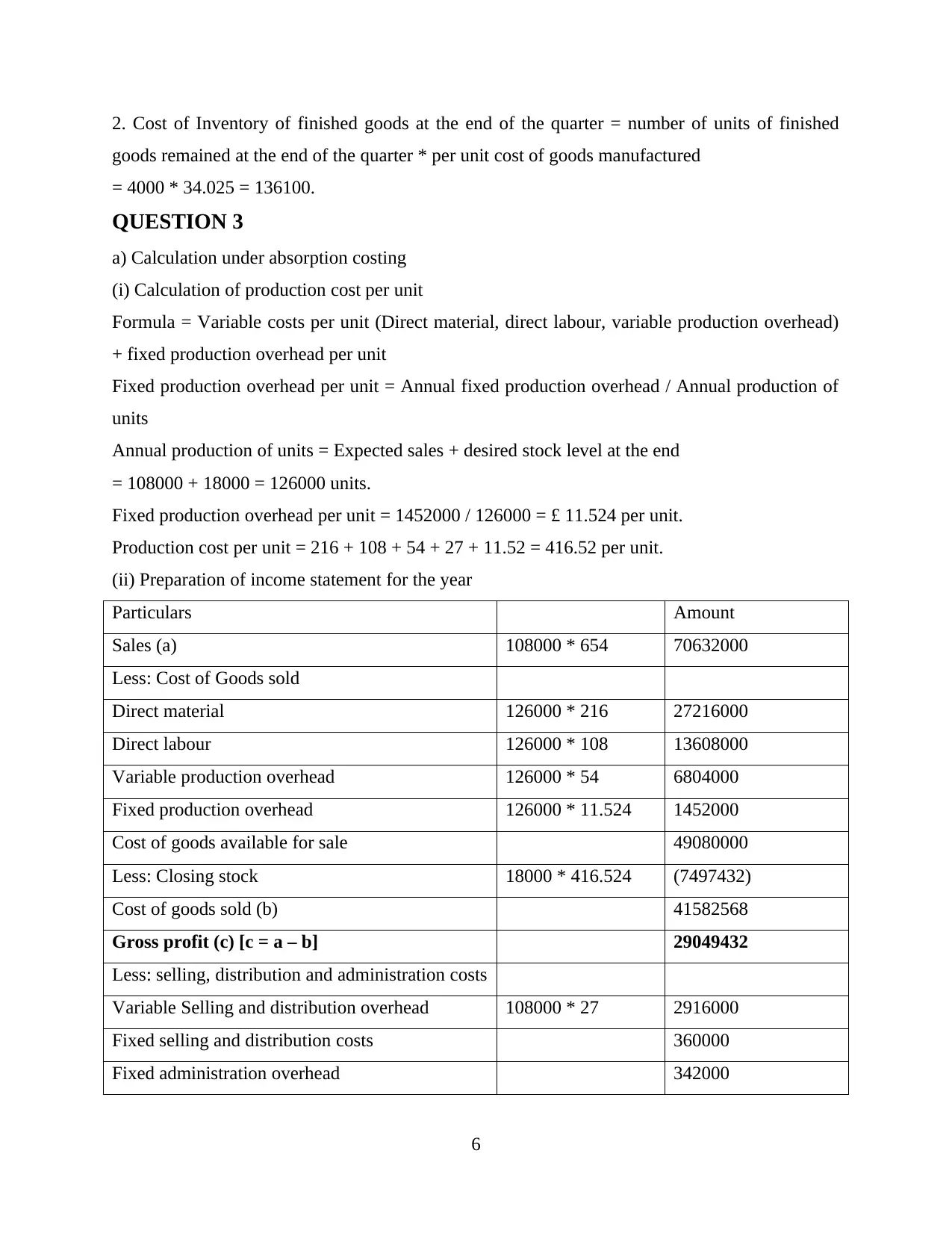

QUESTION 3

a) Calculation under absorption costing

(i) Calculation of production cost per unit

Formula = Variable costs per unit (Direct material, direct labour, variable production overhead)

+ fixed production overhead per unit

Fixed production overhead per unit = Annual fixed production overhead / Annual production of

units

Annual production of units = Expected sales + desired stock level at the end

= 108000 + 18000 = 126000 units.

Fixed production overhead per unit = 1452000 / 126000 = £ 11.524 per unit.

Production cost per unit = 216 + 108 + 54 + 27 + 11.52 = 416.52 per unit.

(ii) Preparation of income statement for the year

Particulars Amount

Sales (a) 108000 * 654 70632000

Less: Cost of Goods sold

Direct material 126000 * 216 27216000

Direct labour 126000 * 108 13608000

Variable production overhead 126000 * 54 6804000

Fixed production overhead 126000 * 11.524 1452000

Cost of goods available for sale 49080000

Less: Closing stock 18000 * 416.524 (7497432)

Cost of goods sold (b) 41582568

Gross profit (c) [c = a – b] 29049432

Less: selling, distribution and administration costs

Variable Selling and distribution overhead 108000 * 27 2916000

Fixed selling and distribution costs 360000

Fixed administration overhead 342000

6

goods remained at the end of the quarter * per unit cost of goods manufactured

= 4000 * 34.025 = 136100.

QUESTION 3

a) Calculation under absorption costing

(i) Calculation of production cost per unit

Formula = Variable costs per unit (Direct material, direct labour, variable production overhead)

+ fixed production overhead per unit

Fixed production overhead per unit = Annual fixed production overhead / Annual production of

units

Annual production of units = Expected sales + desired stock level at the end

= 108000 + 18000 = 126000 units.

Fixed production overhead per unit = 1452000 / 126000 = £ 11.524 per unit.

Production cost per unit = 216 + 108 + 54 + 27 + 11.52 = 416.52 per unit.

(ii) Preparation of income statement for the year

Particulars Amount

Sales (a) 108000 * 654 70632000

Less: Cost of Goods sold

Direct material 126000 * 216 27216000

Direct labour 126000 * 108 13608000

Variable production overhead 126000 * 54 6804000

Fixed production overhead 126000 * 11.524 1452000

Cost of goods available for sale 49080000

Less: Closing stock 18000 * 416.524 (7497432)

Cost of goods sold (b) 41582568

Gross profit (c) [c = a – b] 29049432

Less: selling, distribution and administration costs

Variable Selling and distribution overhead 108000 * 27 2916000

Fixed selling and distribution costs 360000

Fixed administration overhead 342000

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

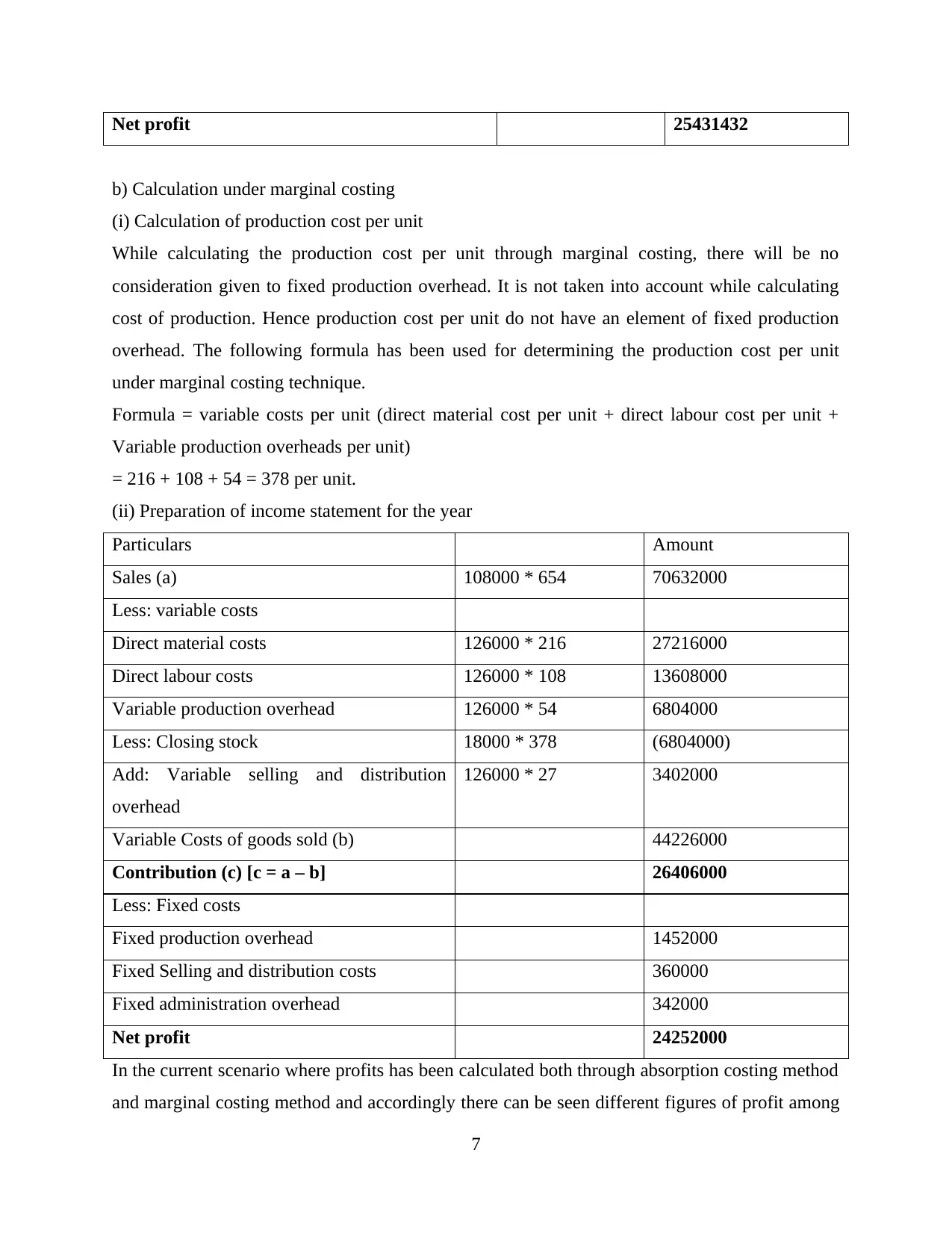

Net profit 25431432

b) Calculation under marginal costing

(i) Calculation of production cost per unit

While calculating the production cost per unit through marginal costing, there will be no

consideration given to fixed production overhead. It is not taken into account while calculating

cost of production. Hence production cost per unit do not have an element of fixed production

overhead. The following formula has been used for determining the production cost per unit

under marginal costing technique.

Formula = variable costs per unit (direct material cost per unit + direct labour cost per unit +

Variable production overheads per unit)

= 216 + 108 + 54 = 378 per unit.

(ii) Preparation of income statement for the year

Particulars Amount

Sales (a) 108000 * 654 70632000

Less: variable costs

Direct material costs 126000 * 216 27216000

Direct labour costs 126000 * 108 13608000

Variable production overhead 126000 * 54 6804000

Less: Closing stock 18000 * 378 (6804000)

Add: Variable selling and distribution

overhead

126000 * 27 3402000

Variable Costs of goods sold (b) 44226000

Contribution (c) [c = a – b] 26406000

Less: Fixed costs

Fixed production overhead 1452000

Fixed Selling and distribution costs 360000

Fixed administration overhead 342000

Net profit 24252000

In the current scenario where profits has been calculated both through absorption costing method

and marginal costing method and accordingly there can be seen different figures of profit among

7

b) Calculation under marginal costing

(i) Calculation of production cost per unit

While calculating the production cost per unit through marginal costing, there will be no

consideration given to fixed production overhead. It is not taken into account while calculating

cost of production. Hence production cost per unit do not have an element of fixed production

overhead. The following formula has been used for determining the production cost per unit

under marginal costing technique.

Formula = variable costs per unit (direct material cost per unit + direct labour cost per unit +

Variable production overheads per unit)

= 216 + 108 + 54 = 378 per unit.

(ii) Preparation of income statement for the year

Particulars Amount

Sales (a) 108000 * 654 70632000

Less: variable costs

Direct material costs 126000 * 216 27216000

Direct labour costs 126000 * 108 13608000

Variable production overhead 126000 * 54 6804000

Less: Closing stock 18000 * 378 (6804000)

Add: Variable selling and distribution

overhead

126000 * 27 3402000

Variable Costs of goods sold (b) 44226000

Contribution (c) [c = a – b] 26406000

Less: Fixed costs

Fixed production overhead 1452000

Fixed Selling and distribution costs 360000

Fixed administration overhead 342000

Net profit 24252000

In the current scenario where profits has been calculated both through absorption costing method

and marginal costing method and accordingly there can be seen different figures of profit among

7

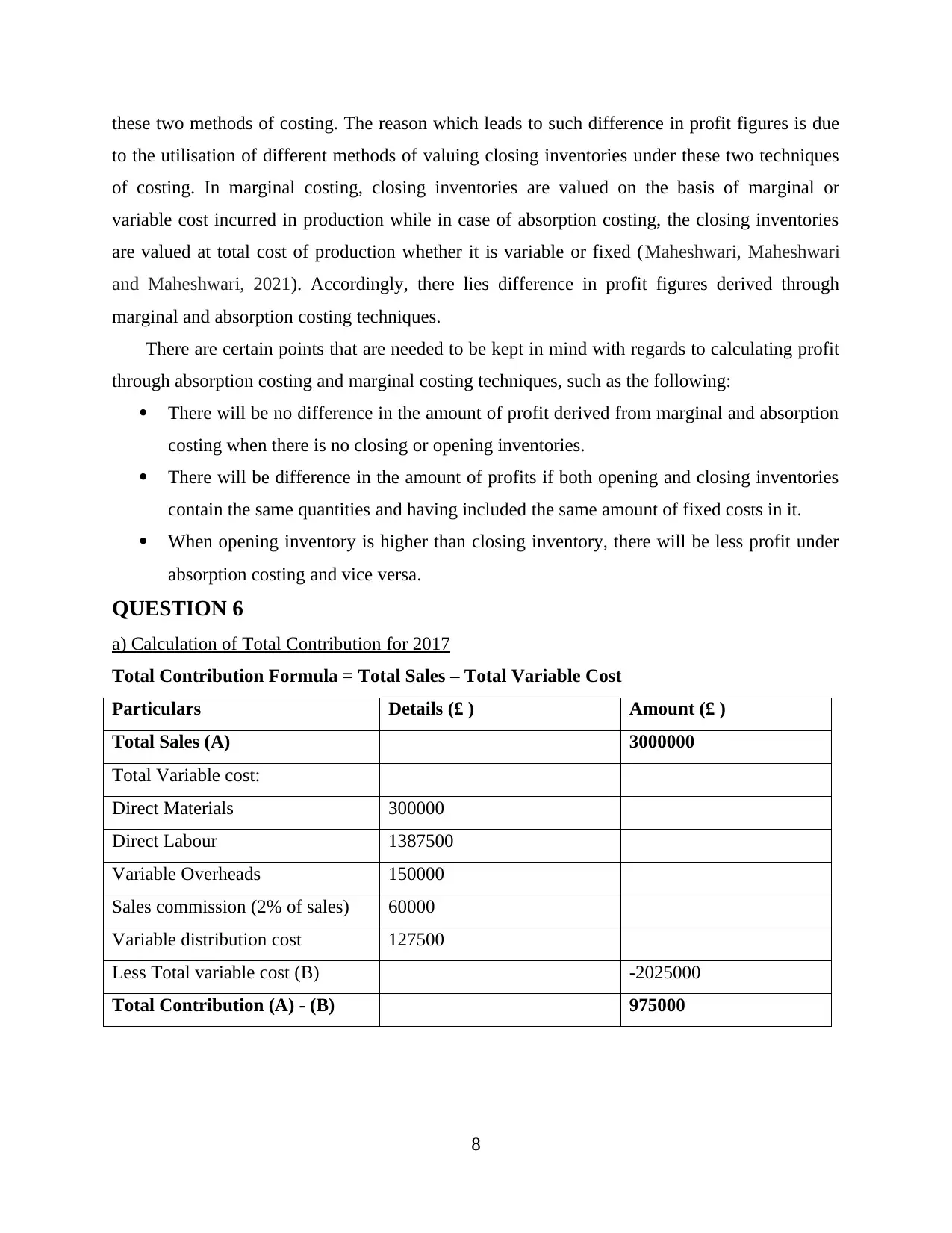

these two methods of costing. The reason which leads to such difference in profit figures is due

to the utilisation of different methods of valuing closing inventories under these two techniques

of costing. In marginal costing, closing inventories are valued on the basis of marginal or

variable cost incurred in production while in case of absorption costing, the closing inventories

are valued at total cost of production whether it is variable or fixed (Maheshwari, Maheshwari

and Maheshwari, 2021). Accordingly, there lies difference in profit figures derived through

marginal and absorption costing techniques.

There are certain points that are needed to be kept in mind with regards to calculating profit

through absorption costing and marginal costing techniques, such as the following:

There will be no difference in the amount of profit derived from marginal and absorption

costing when there is no closing or opening inventories.

There will be difference in the amount of profits if both opening and closing inventories

contain the same quantities and having included the same amount of fixed costs in it.

When opening inventory is higher than closing inventory, there will be less profit under

absorption costing and vice versa.

QUESTION 6

a) Calculation of Total Contribution for 2017

Total Contribution Formula = Total Sales – Total Variable Cost

Particulars Details (£ ) Amount (£ )

Total Sales (A) 3000000

Total Variable cost:

Direct Materials 300000

Direct Labour 1387500

Variable Overheads 150000

Sales commission (2% of sales) 60000

Variable distribution cost 127500

Less Total variable cost (B) -2025000

Total Contribution (A) - (B) 975000

8

to the utilisation of different methods of valuing closing inventories under these two techniques

of costing. In marginal costing, closing inventories are valued on the basis of marginal or

variable cost incurred in production while in case of absorption costing, the closing inventories

are valued at total cost of production whether it is variable or fixed (Maheshwari, Maheshwari

and Maheshwari, 2021). Accordingly, there lies difference in profit figures derived through

marginal and absorption costing techniques.

There are certain points that are needed to be kept in mind with regards to calculating profit

through absorption costing and marginal costing techniques, such as the following:

There will be no difference in the amount of profit derived from marginal and absorption

costing when there is no closing or opening inventories.

There will be difference in the amount of profits if both opening and closing inventories

contain the same quantities and having included the same amount of fixed costs in it.

When opening inventory is higher than closing inventory, there will be less profit under

absorption costing and vice versa.

QUESTION 6

a) Calculation of Total Contribution for 2017

Total Contribution Formula = Total Sales – Total Variable Cost

Particulars Details (£ ) Amount (£ )

Total Sales (A) 3000000

Total Variable cost:

Direct Materials 300000

Direct Labour 1387500

Variable Overheads 150000

Sales commission (2% of sales) 60000

Variable distribution cost 127500

Less Total variable cost (B) -2025000

Total Contribution (A) - (B) 975000

8

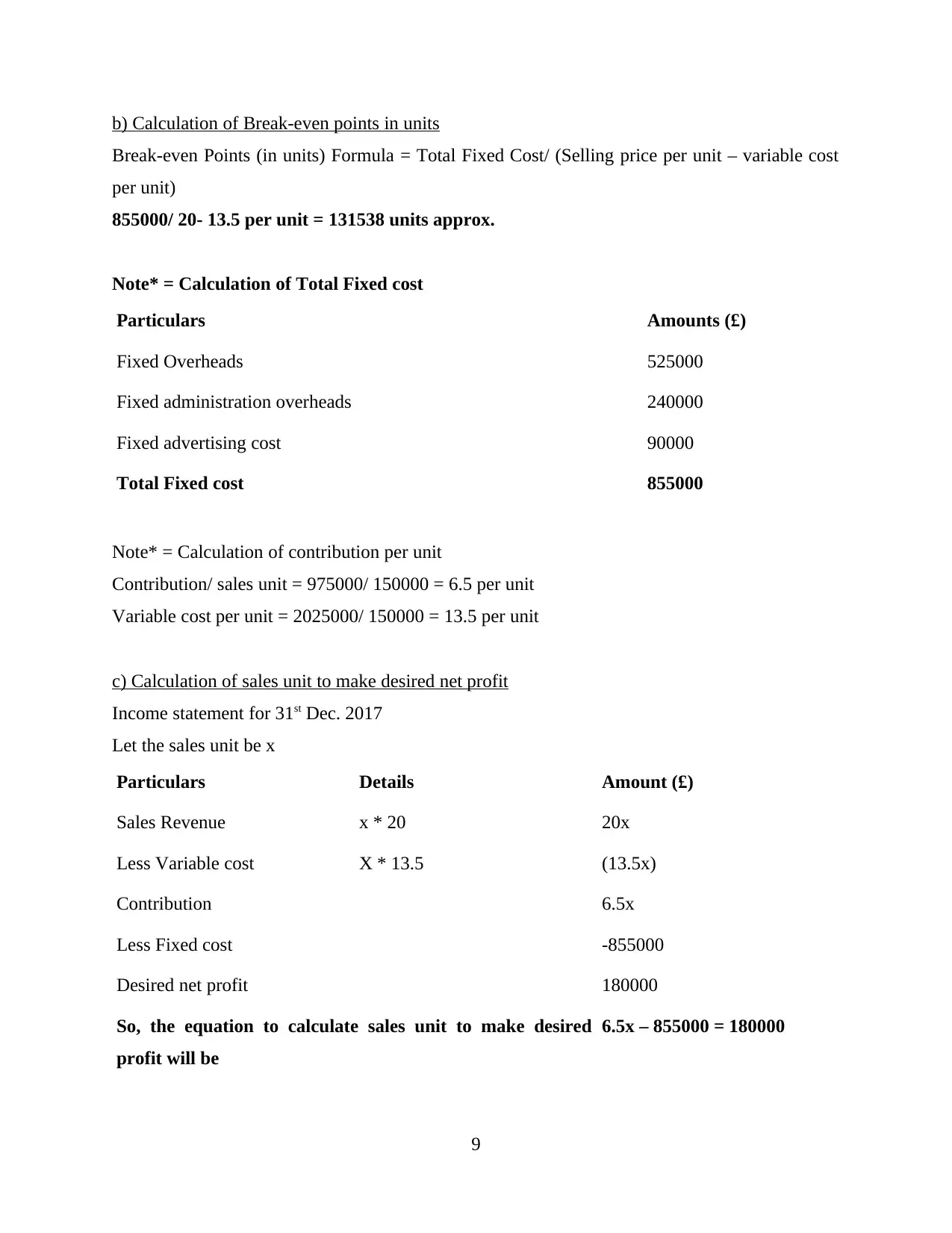

b) Calculation of Break-even points in units

Break-even Points (in units) Formula = Total Fixed Cost/ (Selling price per unit – variable cost

per unit)

855000/ 20- 13.5 per unit = 131538 units approx.

Note* = Calculation of Total Fixed cost

Particulars Amounts (£)

Fixed Overheads 525000

Fixed administration overheads 240000

Fixed advertising cost 90000

Total Fixed cost 855000

Note* = Calculation of contribution per unit

Contribution/ sales unit = 975000/ 150000 = 6.5 per unit

Variable cost per unit = 2025000/ 150000 = 13.5 per unit

c) Calculation of sales unit to make desired net profit

Income statement for 31st Dec. 2017

Let the sales unit be x

Particulars Details Amount (£)

Sales Revenue x * 20 20x

Less Variable cost X * 13.5 (13.5x)

Contribution 6.5x

Less Fixed cost -855000

Desired net profit 180000

So, the equation to calculate sales unit to make desired

profit will be

6.5x – 855000 = 180000

9

Break-even Points (in units) Formula = Total Fixed Cost/ (Selling price per unit – variable cost

per unit)

855000/ 20- 13.5 per unit = 131538 units approx.

Note* = Calculation of Total Fixed cost

Particulars Amounts (£)

Fixed Overheads 525000

Fixed administration overheads 240000

Fixed advertising cost 90000

Total Fixed cost 855000

Note* = Calculation of contribution per unit

Contribution/ sales unit = 975000/ 150000 = 6.5 per unit

Variable cost per unit = 2025000/ 150000 = 13.5 per unit

c) Calculation of sales unit to make desired net profit

Income statement for 31st Dec. 2017

Let the sales unit be x

Particulars Details Amount (£)

Sales Revenue x * 20 20x

Less Variable cost X * 13.5 (13.5x)

Contribution 6.5x

Less Fixed cost -855000

Desired net profit 180000

So, the equation to calculate sales unit to make desired

profit will be

6.5x – 855000 = 180000

9

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

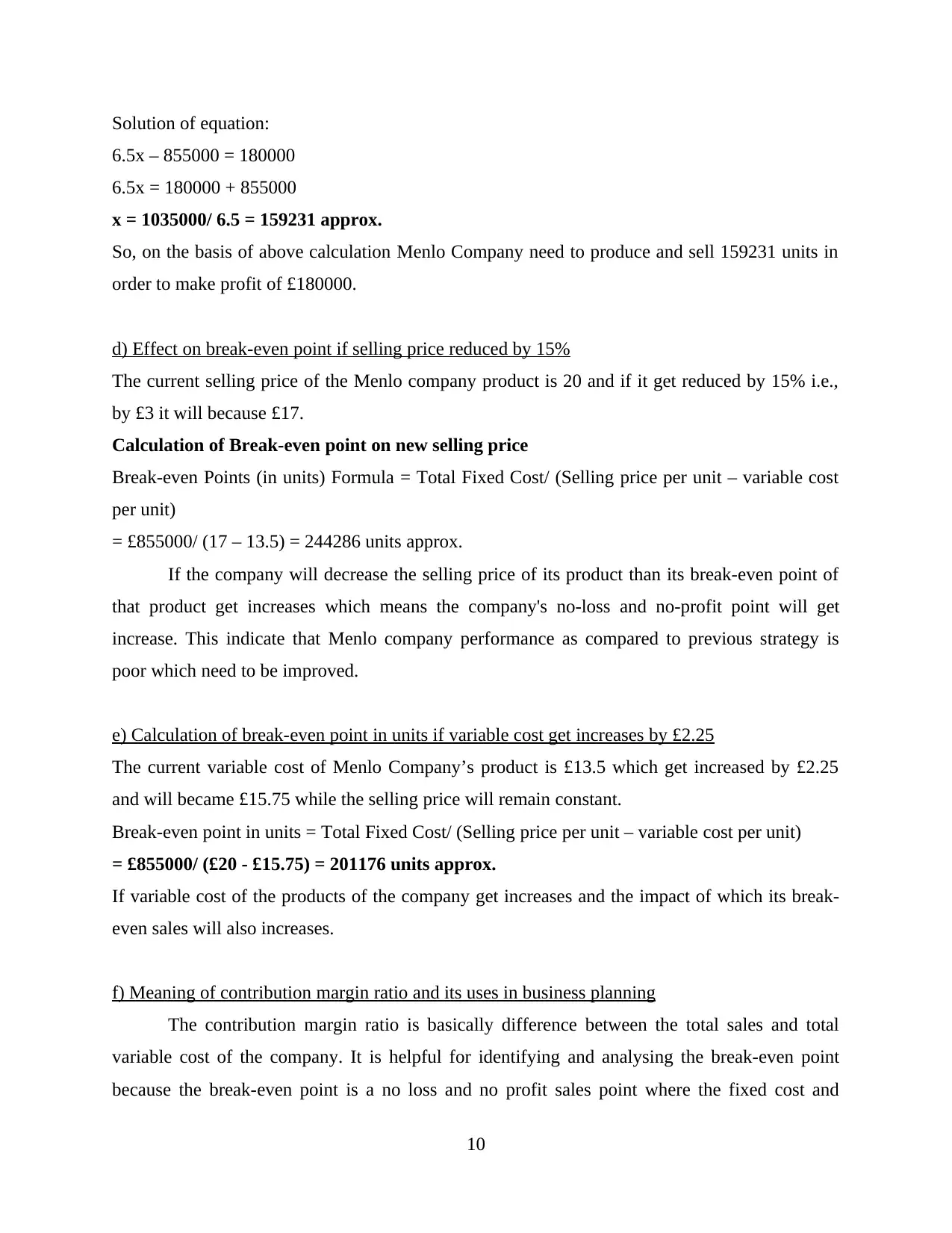

Solution of equation:

6.5x – 855000 = 180000

6.5x = 180000 + 855000

x = 1035000/ 6.5 = 159231 approx.

So, on the basis of above calculation Menlo Company need to produce and sell 159231 units in

order to make profit of £180000.

d) Effect on break-even point if selling price reduced by 15%

The current selling price of the Menlo company product is 20 and if it get reduced by 15% i.e.,

by £3 it will because £17.

Calculation of Break-even point on new selling price

Break-even Points (in units) Formula = Total Fixed Cost/ (Selling price per unit – variable cost

per unit)

= £855000/ (17 – 13.5) = 244286 units approx.

If the company will decrease the selling price of its product than its break-even point of

that product get increases which means the company's no-loss and no-profit point will get

increase. This indicate that Menlo company performance as compared to previous strategy is

poor which need to be improved.

e) Calculation of break-even point in units if variable cost get increases by £2.25

The current variable cost of Menlo Company’s product is £13.5 which get increased by £2.25

and will became £15.75 while the selling price will remain constant.

Break-even point in units = Total Fixed Cost/ (Selling price per unit – variable cost per unit)

= £855000/ (£20 - £15.75) = 201176 units approx.

If variable cost of the products of the company get increases and the impact of which its break-

even sales will also increases.

f) Meaning of contribution margin ratio and its uses in business planning

The contribution margin ratio is basically difference between the total sales and total

variable cost of the company. It is helpful for identifying and analysing the break-even point

because the break-even point is a no loss and no profit sales point where the fixed cost and

10

6.5x – 855000 = 180000

6.5x = 180000 + 855000

x = 1035000/ 6.5 = 159231 approx.

So, on the basis of above calculation Menlo Company need to produce and sell 159231 units in

order to make profit of £180000.

d) Effect on break-even point if selling price reduced by 15%

The current selling price of the Menlo company product is 20 and if it get reduced by 15% i.e.,

by £3 it will because £17.

Calculation of Break-even point on new selling price

Break-even Points (in units) Formula = Total Fixed Cost/ (Selling price per unit – variable cost

per unit)

= £855000/ (17 – 13.5) = 244286 units approx.

If the company will decrease the selling price of its product than its break-even point of

that product get increases which means the company's no-loss and no-profit point will get

increase. This indicate that Menlo company performance as compared to previous strategy is

poor which need to be improved.

e) Calculation of break-even point in units if variable cost get increases by £2.25

The current variable cost of Menlo Company’s product is £13.5 which get increased by £2.25

and will became £15.75 while the selling price will remain constant.

Break-even point in units = Total Fixed Cost/ (Selling price per unit – variable cost per unit)

= £855000/ (£20 - £15.75) = 201176 units approx.

If variable cost of the products of the company get increases and the impact of which its break-

even sales will also increases.

f) Meaning of contribution margin ratio and its uses in business planning

The contribution margin ratio is basically difference between the total sales and total

variable cost of the company. It is helpful for identifying and analysing the break-even point

because the break-even point is a no loss and no profit sales point where the fixed cost and

10

contribution is equal (Wang, Wang and Zhang, 2020). The contribution margin is changes as per

the change in the sales revenue and variable cost.

Uses of contribution margin ratio

This is used by the company to calculate the net profit by subtracting the fixed cost of the

company. Fixed cost generally remain constant at all level of the production activity. That's why

it is advisable to the company that their contribution margin of the product should be relativity

high (Aiello and et.al., 2017). since it must be sufficient to also cover fixed expenses and

administration overheads. Also, the measure is useful for determining whether to allow a lower

price in special pricing situations. In case if this margin is low or negative than it will cause

heavy loss to the company.

11

the change in the sales revenue and variable cost.

Uses of contribution margin ratio

This is used by the company to calculate the net profit by subtracting the fixed cost of the

company. Fixed cost generally remain constant at all level of the production activity. That's why

it is advisable to the company that their contribution margin of the product should be relativity

high (Aiello and et.al., 2017). since it must be sufficient to also cover fixed expenses and

administration overheads. Also, the measure is useful for determining whether to allow a lower

price in special pricing situations. In case if this margin is low or negative than it will cause

heavy loss to the company.

11

REFERENCES

Books and journals

Wang, S., Wang, X. and Zhang, J., 2020. Robust optimization approach to process flexibility

designs with contribution margin differentials. Manufacturing & Service Operations

Management.

Aiello, F. and et.al., 2017. Surgeon leadership in the coding, billing, and contractual

negotiations for fenestrated endovascular aortic aneurysm repair increases medical

center contribution margin and physician reimbursement. Journal of vascular

surgery. 66(4). pp.997-1006.

Maheshwari, S. N., Maheshwari, S. K. and Maheshwari, M. S. K., 2021. Principles of

Management Accounting. Sultan Chand & Sons.

12

Books and journals

Wang, S., Wang, X. and Zhang, J., 2020. Robust optimization approach to process flexibility

designs with contribution margin differentials. Manufacturing & Service Operations

Management.

Aiello, F. and et.al., 2017. Surgeon leadership in the coding, billing, and contractual

negotiations for fenestrated endovascular aortic aneurysm repair increases medical

center contribution margin and physician reimbursement. Journal of vascular

surgery. 66(4). pp.997-1006.

Maheshwari, S. N., Maheshwari, S. K. and Maheshwari, M. S. K., 2021. Principles of

Management Accounting. Sultan Chand & Sons.

12

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.