BBAC501 Management Accounting: Cost Analysis, BEP & Performance

VerifiedAdded on 2023/06/10

|8

|1222

|461

Report

AI Summary

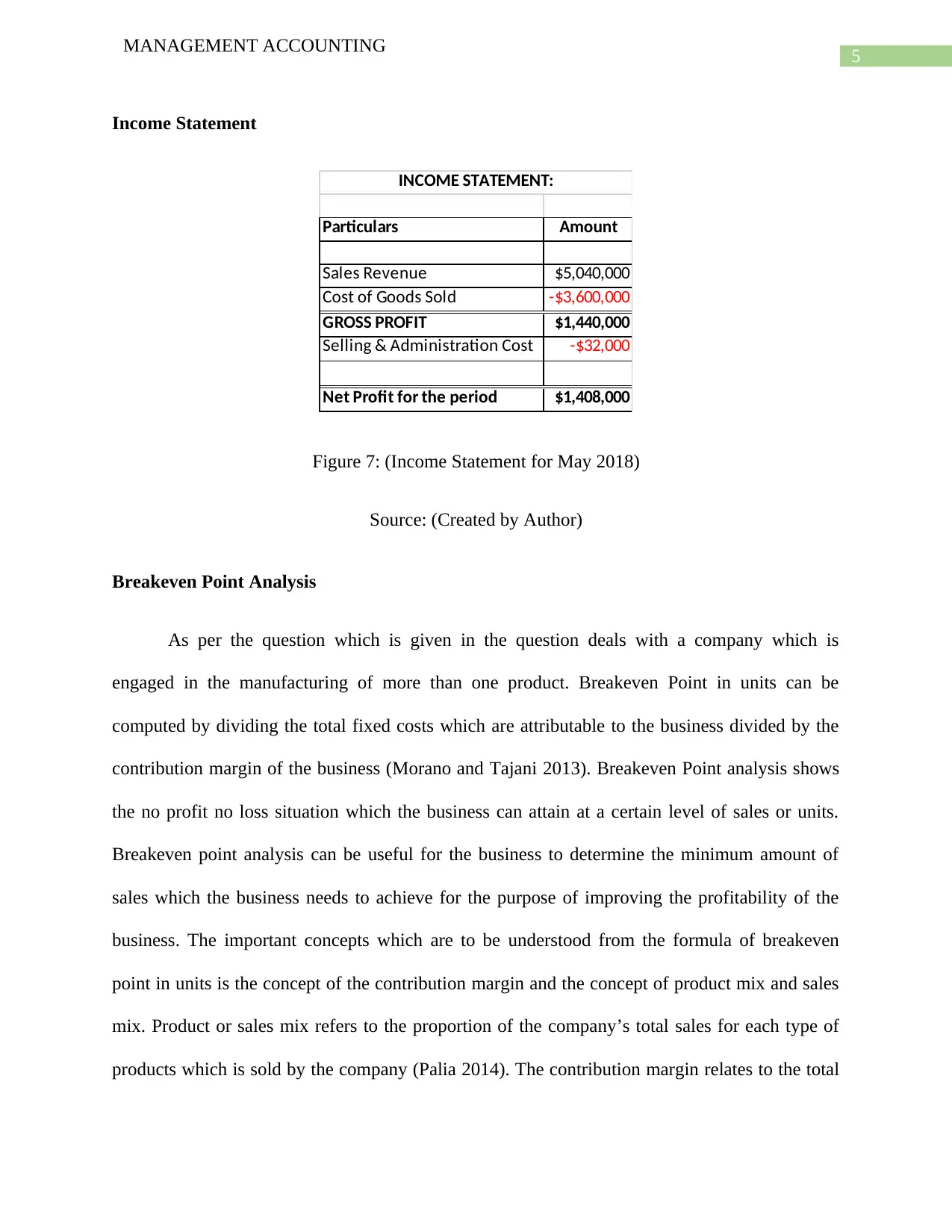

This management accounting report provides a comprehensive analysis of cost values, including the computation of closing Work-in-Progress (WIP) balance, direct labor cost, and sales revenue. It features key financial statements such as the Cost of Goods Sold and Goods Manufactured schedule and an Income Statement for May 2018. The report also includes a break-even point analysis, emphasizing its importance in determining minimum sales requirements for profitability. Furthermore, it discusses the relevance of non-financial performance measures, highlighting their role in evaluating overall business performance beyond monetary terms. Desklib offers a platform to access this and similar solved assignments, along with a variety of past papers.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.