Management Accounting Report: Costing, Budgeting, and Inventory

VerifiedAdded on 2021/01/02

|15

|3716

|148

Report

AI Summary

This management accounting report delves into various aspects of financial management within an organization. It begins with an introduction to management accounting and its importance, followed by a discussion of cost classification, including fixed, variable, and semi-variable costs, along with their graphical representations and analysis. The report then explores different inventory valuation methods such as FIFO, LIFO, and the average cost method, providing detailed calculations and analyses. Performance measuring metrics, including customer experience, product quality, operational efficiency, and cost reduction, are also discussed, along with their success factors. The report further examines budgeting, defining its purposes and outlining different methods of budget preparation, including the creation of a cash budget and a budgeted income statement. Variance analysis and recommendations for cost reduction are also included, concluding with a comprehensive overview of the subject matter.

Management Accounting:

Costing and Budgeting

Costing and Budgeting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Fixed ,variable and semi-variable cost along with other ways of cost classification............1

1.2 Computation of total cost and unit cost.................................................................................2

1.4 Graphical representation and analysis...................................................................................3

1.3 Computation of inventory using various methods................................................................3

TASK 2............................................................................................................................................5

2.1 Report for various inventory methods...................................................................................5

2.2 Performance measuring metrics along with their success factors.........................................6

2.3 Suggestions of reducing cost.................................................................................................8

TASK 3............................................................................................................................................8

3.1 Definition and Purposes of budgets......................................................................................8

3.2 Various methods of preparing budget...................................................................................9

3.3 Preparation of various budgets..............................................................................................9

3.4 Preparation of cash budget..................................................................................................10

TASK 4..........................................................................................................................................11

4.1 Preparation of budgeted income statement.........................................................................11

4.2 Determination of variances and preparation of reconciled statement.................................12

4.3 Recommendations...............................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Fixed ,variable and semi-variable cost along with other ways of cost classification............1

1.2 Computation of total cost and unit cost.................................................................................2

1.4 Graphical representation and analysis...................................................................................3

1.3 Computation of inventory using various methods................................................................3

TASK 2............................................................................................................................................5

2.1 Report for various inventory methods...................................................................................5

2.2 Performance measuring metrics along with their success factors.........................................6

2.3 Suggestions of reducing cost.................................................................................................8

TASK 3............................................................................................................................................8

3.1 Definition and Purposes of budgets......................................................................................8

3.2 Various methods of preparing budget...................................................................................9

3.3 Preparation of various budgets..............................................................................................9

3.4 Preparation of cash budget..................................................................................................10

TASK 4..........................................................................................................................................11

4.1 Preparation of budgeted income statement.........................................................................11

4.2 Determination of variances and preparation of reconciled statement.................................12

4.3 Recommendations...............................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is a process of preparing managerial accounts and reports in

order to better management of the organisation. The aim objective of this project report is to

discuss and explain various budgetary methods along with several costing methods in order to

have a better understanding about organisational elements such as inventory, production,

budgetary control and financial statements. In this project report several inventory management

methods are explained along with various other questions which includes preparation of budgets,

cost reduction technique and others.

TASK 1

1.1 Fixed ,variable and semi-variable cost along with other ways of cost classification

a. Columnar table of fixed, variable and semi-variable cost

Fixed cost – These are the costs which are static in nature and does not change with

changing activity. This cost is does not depended on the volume of goods and services produced

by an organisation. These expenses are time related and referred as overhead costs. Some of the

examples of these costs are salaries, insurance, depreciation, rent etc (Bennett, 2013).

Variable cost – These costs are flexible in nature and change according to the level of

production and business operations. Variable or marginal costs increase and decrease according

to the business activities of an organisation. Some of the examples of these costs are direct

material, direct labour, production supplies, shipping costs etc.

Semi variable cost – Semi variable costs are the combination of both fixed and variable

costs. Part of these expenses are fixed which does not change and some part of these expenses

are variable which may change according to the level of business operations. Some of the

examples of these these expenses are commission charges and semi variable labour costs

(Bovens, 2014).

Fixed cost Factory rent

Power for sewing machine in

factory(per unit of electricity)

Variable cost Factory supervisor wages

Packaging material

1

Management accounting is a process of preparing managerial accounts and reports in

order to better management of the organisation. The aim objective of this project report is to

discuss and explain various budgetary methods along with several costing methods in order to

have a better understanding about organisational elements such as inventory, production,

budgetary control and financial statements. In this project report several inventory management

methods are explained along with various other questions which includes preparation of budgets,

cost reduction technique and others.

TASK 1

1.1 Fixed ,variable and semi-variable cost along with other ways of cost classification

a. Columnar table of fixed, variable and semi-variable cost

Fixed cost – These are the costs which are static in nature and does not change with

changing activity. This cost is does not depended on the volume of goods and services produced

by an organisation. These expenses are time related and referred as overhead costs. Some of the

examples of these costs are salaries, insurance, depreciation, rent etc (Bennett, 2013).

Variable cost – These costs are flexible in nature and change according to the level of

production and business operations. Variable or marginal costs increase and decrease according

to the business activities of an organisation. Some of the examples of these costs are direct

material, direct labour, production supplies, shipping costs etc.

Semi variable cost – Semi variable costs are the combination of both fixed and variable

costs. Part of these expenses are fixed which does not change and some part of these expenses

are variable which may change according to the level of business operations. Some of the

examples of these these expenses are commission charges and semi variable labour costs

(Bovens, 2014).

Fixed cost Factory rent

Power for sewing machine in

factory(per unit of electricity)

Variable cost Factory supervisor wages

Packaging material

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Office rates

Material for clothes

Semi variable cost Telephone

Factory heating

Delivery drivers pay

b. Few other ways of classification costs

Fewer other ways of classification of costs

Costs are the expenses which are needed to be paid by the organisation. These costs can

be categorized by various ways and few of them are discussed below:

By Function – Under to this classification, costs are divided according to their related

functions for which they are incurred. Broad classes included in this classification are

production, administration, selling and distribution (Chiwamit, 2014).

By Nature - Expenditures occurred in an organisation can be classified according to their

nature of activity for which they are incurred, such activities are production,

administration, selling and distribution etc.

Level of controllability – Under this, expenses are divided into two classes. First

category is of costs which can be controlled by the management like direct labour, direct

material etc. whereas another category is of uncontrollable expenses such as salaries, rent

etc.

By time – According to this classification, expenses are divided into two categories and

they are historical costs and pre determined cost. Historical costs are the expenses which

are ascertained after they are incurred in past and predetermined costs are estimated or

projected cost which are ascertained for future using trend analyses.

By normality – Costs are classified as normal costs and abnormal costs under this

classification. Normal costs are the expenses which are incurred due to normal or regular

business operations and abnormal costs are the expenses which are incurred due to

irregular business situations such as fire or theft (Edwards, 2012).

1.2 Computation of total cost and unit cost

Computation of the Total cost for the production various units

Particular Units (15000) Units (20000) Units (25000)

2

Material for clothes

Semi variable cost Telephone

Factory heating

Delivery drivers pay

b. Few other ways of classification costs

Fewer other ways of classification of costs

Costs are the expenses which are needed to be paid by the organisation. These costs can

be categorized by various ways and few of them are discussed below:

By Function – Under to this classification, costs are divided according to their related

functions for which they are incurred. Broad classes included in this classification are

production, administration, selling and distribution (Chiwamit, 2014).

By Nature - Expenditures occurred in an organisation can be classified according to their

nature of activity for which they are incurred, such activities are production,

administration, selling and distribution etc.

Level of controllability – Under this, expenses are divided into two classes. First

category is of costs which can be controlled by the management like direct labour, direct

material etc. whereas another category is of uncontrollable expenses such as salaries, rent

etc.

By time – According to this classification, expenses are divided into two categories and

they are historical costs and pre determined cost. Historical costs are the expenses which

are ascertained after they are incurred in past and predetermined costs are estimated or

projected cost which are ascertained for future using trend analyses.

By normality – Costs are classified as normal costs and abnormal costs under this

classification. Normal costs are the expenses which are incurred due to normal or regular

business operations and abnormal costs are the expenses which are incurred due to

irregular business situations such as fire or theft (Edwards, 2012).

1.2 Computation of total cost and unit cost

Computation of the Total cost for the production various units

Particular Units (15000) Units (20000) Units (25000)

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(A)Direct Variable cost:

1. Material (@5 per units) 75000 100000 125000

2. Labour (@6 per units) 90000 120000 150000

Total variable cost 165000 220000 275000

(B) Fixed cost 50000 50000 50000

Total cost (A+B) 215000 270000 325000

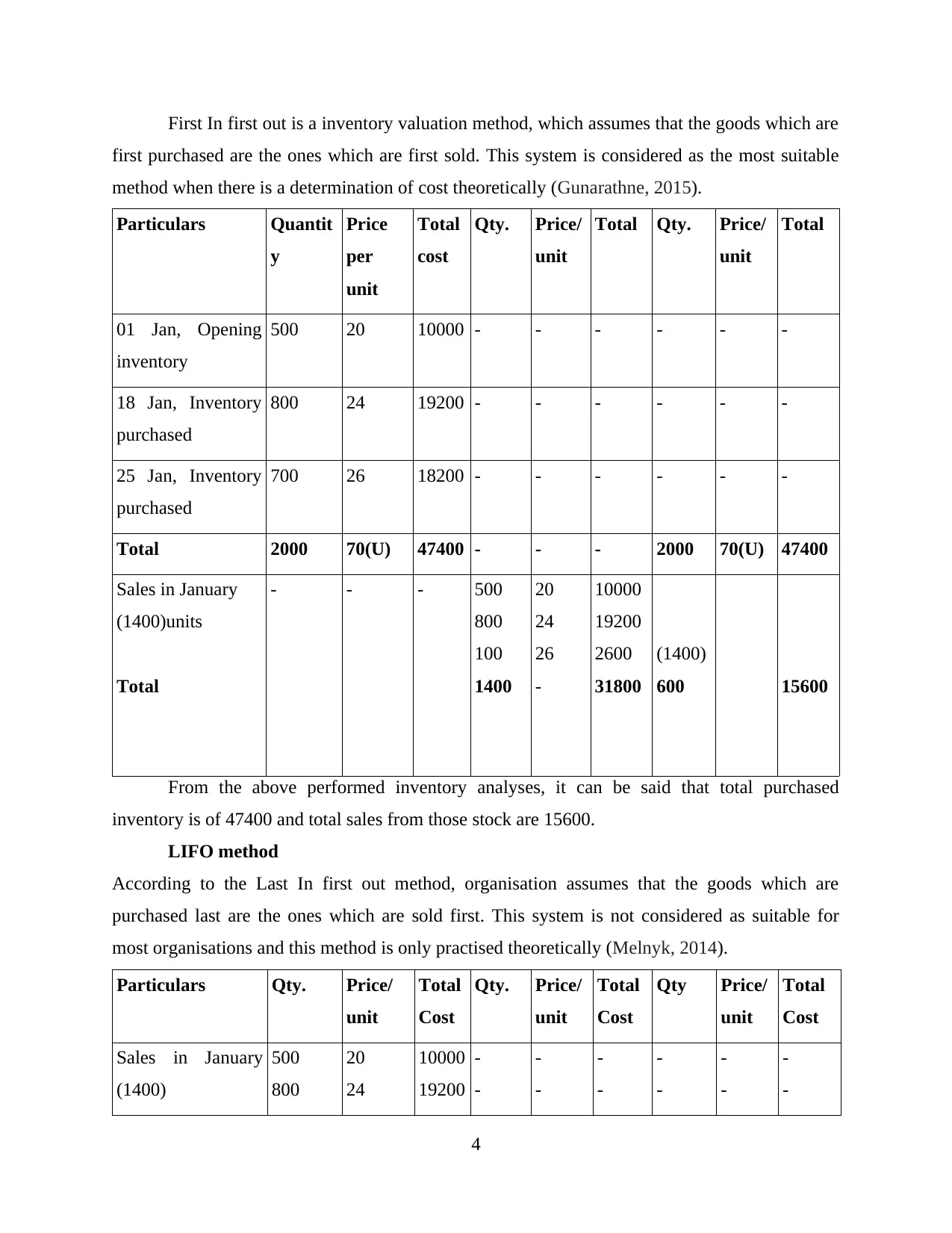

1.4 Graphical representation and analysis

Graphical representation of computation of total cost

1. Material (@5 per units)

2. Labour (@6 per units)

Total variable cost

(B) Fixed cost

Total cost (A+B)

0

50000

100000

150000

200000

250000

300000

350000

75000 90000

165000

50000

215000

100000 120000

220000

50000

270000

125000

150000

275000

50000

325000

Total cost of production

Units (15000)

Units (20000)

Units (25000)

From the above tabular presentation of calculation of total costs, it has been analysed that

if a production organisation manufacturers 15000 units then they will incur total cost of 215000

which is calculated from the sum of variable and fixed expenses. Accordingly if that organisation

will produce 20000 and 25000 units then the company has to bear total expenses of 270000 and

325000 respectively.

1.3 Computation of inventory using various methods

FIFO method

3

1. Material (@5 per units) 75000 100000 125000

2. Labour (@6 per units) 90000 120000 150000

Total variable cost 165000 220000 275000

(B) Fixed cost 50000 50000 50000

Total cost (A+B) 215000 270000 325000

1.4 Graphical representation and analysis

Graphical representation of computation of total cost

1. Material (@5 per units)

2. Labour (@6 per units)

Total variable cost

(B) Fixed cost

Total cost (A+B)

0

50000

100000

150000

200000

250000

300000

350000

75000 90000

165000

50000

215000

100000 120000

220000

50000

270000

125000

150000

275000

50000

325000

Total cost of production

Units (15000)

Units (20000)

Units (25000)

From the above tabular presentation of calculation of total costs, it has been analysed that

if a production organisation manufacturers 15000 units then they will incur total cost of 215000

which is calculated from the sum of variable and fixed expenses. Accordingly if that organisation

will produce 20000 and 25000 units then the company has to bear total expenses of 270000 and

325000 respectively.

1.3 Computation of inventory using various methods

FIFO method

3

First In first out is a inventory valuation method, which assumes that the goods which are

first purchased are the ones which are first sold. This system is considered as the most suitable

method when there is a determination of cost theoretically (Gunarathne, 2015).

Particulars Quantit

y

Price

per

unit

Total

cost

Qty. Price/

unit

Total Qty. Price/

unit

Total

01 Jan, Opening

inventory

500 20 10000 - - - - - -

18 Jan, Inventory

purchased

800 24 19200 - - - - - -

25 Jan, Inventory

purchased

700 26 18200 - - - - - -

Total 2000 70(U) 47400 - - - 2000 70(U) 47400

Sales in January

(1400)units

Total

- - - 500

800

100

1400

20

24

26

-

10000

19200

2600

31800

(1400)

600 15600

From the above performed inventory analyses, it can be said that total purchased

inventory is of 47400 and total sales from those stock are 15600.

LIFO method

According to the Last In first out method, organisation assumes that the goods which are

purchased last are the ones which are sold first. This system is not considered as suitable for

most organisations and this method is only practised theoretically (Melnyk, 2014).

Particulars Qty. Price/

unit

Total

Cost

Qty. Price/

unit

Total

Cost

Qty Price/

unit

Total

Cost

Sales in January

(1400)

500

800

20

24

10000

19200

-

-

-

-

-

-

-

-

-

-

-

-

4

first purchased are the ones which are first sold. This system is considered as the most suitable

method when there is a determination of cost theoretically (Gunarathne, 2015).

Particulars Quantit

y

Price

per

unit

Total

cost

Qty. Price/

unit

Total Qty. Price/

unit

Total

01 Jan, Opening

inventory

500 20 10000 - - - - - -

18 Jan, Inventory

purchased

800 24 19200 - - - - - -

25 Jan, Inventory

purchased

700 26 18200 - - - - - -

Total 2000 70(U) 47400 - - - 2000 70(U) 47400

Sales in January

(1400)units

Total

- - - 500

800

100

1400

20

24

26

-

10000

19200

2600

31800

(1400)

600 15600

From the above performed inventory analyses, it can be said that total purchased

inventory is of 47400 and total sales from those stock are 15600.

LIFO method

According to the Last In first out method, organisation assumes that the goods which are

purchased last are the ones which are sold first. This system is not considered as suitable for

most organisations and this method is only practised theoretically (Melnyk, 2014).

Particulars Qty. Price/

unit

Total

Cost

Qty. Price/

unit

Total

Cost

Qty Price/

unit

Total

Cost

Sales in January

(1400)

500

800

20

24

10000

19200

-

-

-

-

-

-

-

-

-

-

-

-

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

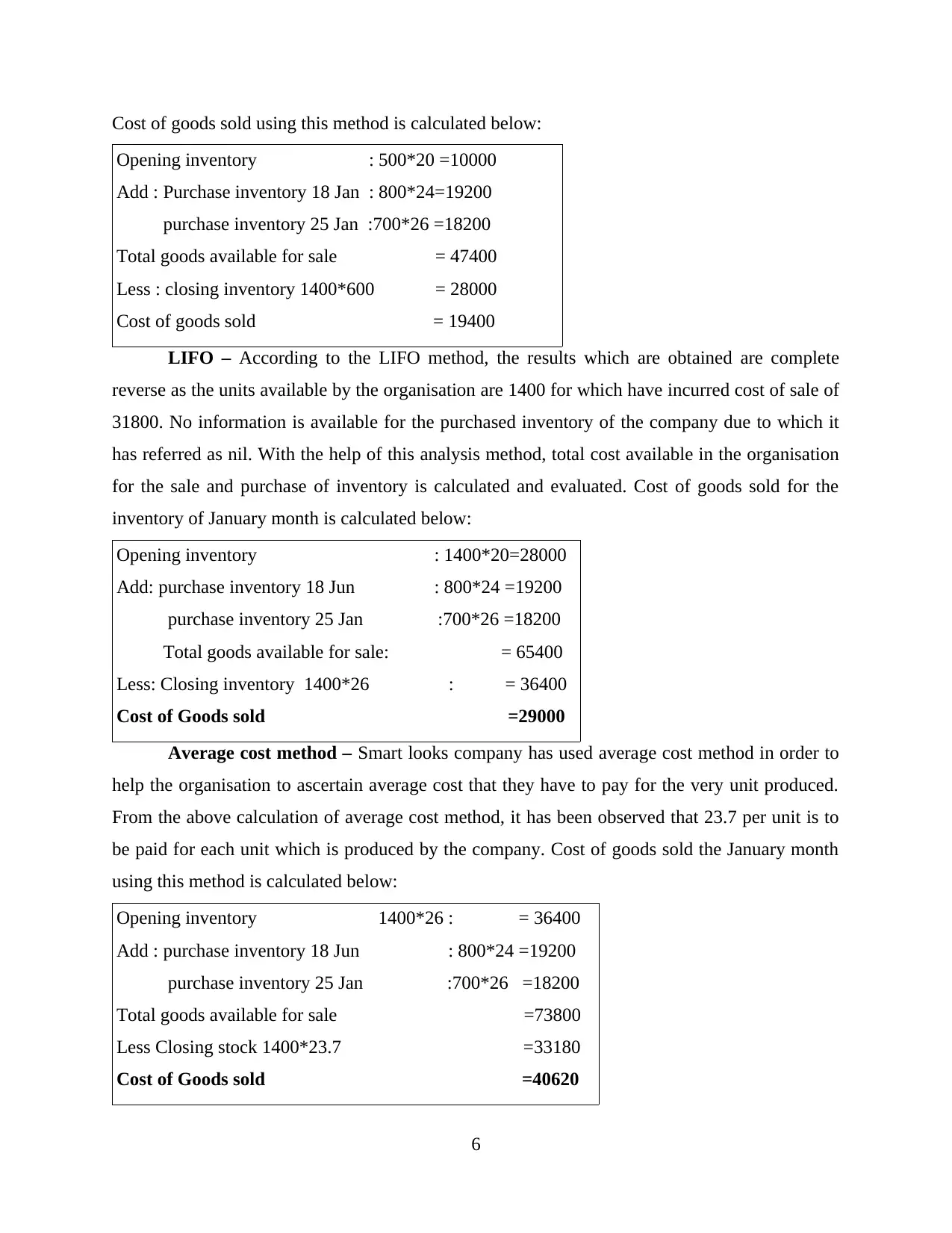

100 26 2600 - - - - - -

Total sales &

Balance

1400 - 31800 - - - 1400 - 31800

01 Jan, Opening

inventory

- - - 500 20 10000 - - -

18 Jan, Purchased

stock

- - - 800 24 19200 - - -

25 Jan, Purchased

stock

- - - 100 26 2600 - - -

Total cost 1400 31800 2000 - 31800 - - -

From the above calculation, it can be said that total sold goods for the month January

were 1400 from the total purchased stock of 2000 units.

Average cost method

This method is considered as the most suitable method as it includes calculation of

ending inventory cost. This system is practised by most of the organisation by dividing COGS

for sales from the units available for sales. By using this technique, weighted average cost per

unit can be ascertained.

Total Balance of the purchase of the inventory=47400

Number of unit available for the sale =2000

Average cost =Total cost of purchase/ No. of Units

= 47400/2000

= 23.7 per units.

TASK 2

2.1 Report for various inventory methods

FIFO – Smart look company has used various inventory management systems in order to

identify cost involved in inventories. According to the above performed FIFO analyses, sales

outcome is 2000 units from the total cost of 47400. Whereas, in the same organisation 1400 units

are sold by bearing total loss of 600 units due to which total cost is also decreased to 15600.

5

Total sales &

Balance

1400 - 31800 - - - 1400 - 31800

01 Jan, Opening

inventory

- - - 500 20 10000 - - -

18 Jan, Purchased

stock

- - - 800 24 19200 - - -

25 Jan, Purchased

stock

- - - 100 26 2600 - - -

Total cost 1400 31800 2000 - 31800 - - -

From the above calculation, it can be said that total sold goods for the month January

were 1400 from the total purchased stock of 2000 units.

Average cost method

This method is considered as the most suitable method as it includes calculation of

ending inventory cost. This system is practised by most of the organisation by dividing COGS

for sales from the units available for sales. By using this technique, weighted average cost per

unit can be ascertained.

Total Balance of the purchase of the inventory=47400

Number of unit available for the sale =2000

Average cost =Total cost of purchase/ No. of Units

= 47400/2000

= 23.7 per units.

TASK 2

2.1 Report for various inventory methods

FIFO – Smart look company has used various inventory management systems in order to

identify cost involved in inventories. According to the above performed FIFO analyses, sales

outcome is 2000 units from the total cost of 47400. Whereas, in the same organisation 1400 units

are sold by bearing total loss of 600 units due to which total cost is also decreased to 15600.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost of goods sold using this method is calculated below:

Opening inventory : 500*20 =10000

Add : Purchase inventory 18 Jan : 800*24=19200

purchase inventory 25 Jan :700*26 =18200

Total goods available for sale = 47400

Less : closing inventory 1400*600 = 28000

Cost of goods sold = 19400

LIFO – According to the LIFO method, the results which are obtained are complete

reverse as the units available by the organisation are 1400 for which have incurred cost of sale of

31800. No information is available for the purchased inventory of the company due to which it

has referred as nil. With the help of this analysis method, total cost available in the organisation

for the sale and purchase of inventory is calculated and evaluated. Cost of goods sold for the

inventory of January month is calculated below:

Opening inventory : 1400*20=28000

Add: purchase inventory 18 Jun : 800*24 =19200

purchase inventory 25 Jan :700*26 =18200

Total goods available for sale: = 65400

Less: Closing inventory 1400*26 : = 36400

Cost of Goods sold =29000

Average cost method – Smart looks company has used average cost method in order to

help the organisation to ascertain average cost that they have to pay for the very unit produced.

From the above calculation of average cost method, it has been observed that 23.7 per unit is to

be paid for each unit which is produced by the company. Cost of goods sold the January month

using this method is calculated below:

Opening inventory 1400*26 : = 36400

Add : purchase inventory 18 Jun : 800*24 =19200

purchase inventory 25 Jan :700*26 =18200

Total goods available for sale =73800

Less Closing stock 1400*23.7 =33180

Cost of Goods sold =40620

6

Opening inventory : 500*20 =10000

Add : Purchase inventory 18 Jan : 800*24=19200

purchase inventory 25 Jan :700*26 =18200

Total goods available for sale = 47400

Less : closing inventory 1400*600 = 28000

Cost of goods sold = 19400

LIFO – According to the LIFO method, the results which are obtained are complete

reverse as the units available by the organisation are 1400 for which have incurred cost of sale of

31800. No information is available for the purchased inventory of the company due to which it

has referred as nil. With the help of this analysis method, total cost available in the organisation

for the sale and purchase of inventory is calculated and evaluated. Cost of goods sold for the

inventory of January month is calculated below:

Opening inventory : 1400*20=28000

Add: purchase inventory 18 Jun : 800*24 =19200

purchase inventory 25 Jan :700*26 =18200

Total goods available for sale: = 65400

Less: Closing inventory 1400*26 : = 36400

Cost of Goods sold =29000

Average cost method – Smart looks company has used average cost method in order to

help the organisation to ascertain average cost that they have to pay for the very unit produced.

From the above calculation of average cost method, it has been observed that 23.7 per unit is to

be paid for each unit which is produced by the company. Cost of goods sold the January month

using this method is calculated below:

Opening inventory 1400*26 : = 36400

Add : purchase inventory 18 Jun : 800*24 =19200

purchase inventory 25 Jan :700*26 =18200

Total goods available for sale =73800

Less Closing stock 1400*23.7 =33180

Cost of Goods sold =40620

6

2.2 Performance measuring metrics along with their success factors

Customer experience

This term refers to the experience which is faced by the customer by the interaction from

organisational system. These experiences can be traced by the internal and personal reaction of

the clients. Smart look company considers customer experience as a prime element as it impacts

overall productivity and profitability of the organisation (Stergiou, 2013). Two success factors

inclined with this experience are:

When it comes to problem resolving issue, customer care executives should be quick and

prompt as client usually acts impatient and they requires their solution as soon as

possible.

Along with speedy solutions and suggestions, executives should behave in an proper

manner with right attitude and tone so that customers should feel respected and there will

be a chance of great feedback.

Supplier and product quality

For any company such as Smart looks, it is the most important element to produce quality

products so that they can grow in market and can gain brand equity. In order to produce quality

products, organisation needs to have an efficient supply chain management. Few success factors

of quality product are discussed below:

Product quality highly relied on proper communication system. As, if smart looks

company can well communicate about their quality factors then the have maximum

chances of manufacturing quality goods and services.

Along with proper communication, maintaining good relations with employees can also

helps in attaining quality products as they are the human assets of the organisation.

Operations efficiency

Operation efficiency is the ability of the Smart looks company which reflects productivity

and how well a organisation can perform their business activities. In order to improve this

efficiency, success factors are mentioned below:

Smart looks company should reduce the complexity in this business operations which

will provide a clear vision about various tasks and activities which are needed to be

performed to attain operational efficiency.

7

Customer experience

This term refers to the experience which is faced by the customer by the interaction from

organisational system. These experiences can be traced by the internal and personal reaction of

the clients. Smart look company considers customer experience as a prime element as it impacts

overall productivity and profitability of the organisation (Stergiou, 2013). Two success factors

inclined with this experience are:

When it comes to problem resolving issue, customer care executives should be quick and

prompt as client usually acts impatient and they requires their solution as soon as

possible.

Along with speedy solutions and suggestions, executives should behave in an proper

manner with right attitude and tone so that customers should feel respected and there will

be a chance of great feedback.

Supplier and product quality

For any company such as Smart looks, it is the most important element to produce quality

products so that they can grow in market and can gain brand equity. In order to produce quality

products, organisation needs to have an efficient supply chain management. Few success factors

of quality product are discussed below:

Product quality highly relied on proper communication system. As, if smart looks

company can well communicate about their quality factors then the have maximum

chances of manufacturing quality goods and services.

Along with proper communication, maintaining good relations with employees can also

helps in attaining quality products as they are the human assets of the organisation.

Operations efficiency

Operation efficiency is the ability of the Smart looks company which reflects productivity

and how well a organisation can perform their business activities. In order to improve this

efficiency, success factors are mentioned below:

Smart looks company should reduce the complexity in this business operations which

will provide a clear vision about various tasks and activities which are needed to be

performed to attain operational efficiency.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fixed costs such as storage cost and others must be effectively managed as the influence

growth of the company (Suomala, 2012).

Reducing maintenance spending

Smart looks company should cut down their expenses which are irrelevant or

unnecessary. Maintenance expenses highly impact an organisation as these expenses can be

decreased by proper management and controlling practices. Success factors related to

maintenance expenses are mentioned below:

Smart looks company should use computerised maintenance technology so that they can

control these expenses by using more reliable and accurate measures.

This organisation must include preventive maintenance in their operations, according to

which they should set a fixed schedule for checking of critical equipments.

Cost reduction and profitability increase

Cost included in business operations must be reduced by Smart looks company in order

to gain more profitability which will help the organisation in growth and development. Success

factor for this metric are:

In order to gain increased profitability, the above mentioned company should produce

more attractive and cost efficient products in order to attract customers.

Economy growth is also an success factor as, if the economy is growing then the demand

for luxury goods will also increase (Tucker, 2016).

2.3 Suggestions of reducing cost

In order to reduce the costs, few suggestions are mentioned below:

Smart looks company can reduce its supply expenses such as office supplies which can

be reduced by buying these goods in bulk through a specific vendor.

Production costs and financial expenses should be lowered by using updated technologies

along with using various policies such as optimum utilisation of the resources.

Value and quality can be enhanced by focusing on qualitative measures and not quantitative

measures as by producing quality products, organisation can gain trust of public which will

ultimately result in enhanced value of the company. This value can be increased using various

strategies of price constant and others (Zaleha Abdul Rasid, 2011).

8

growth of the company (Suomala, 2012).

Reducing maintenance spending

Smart looks company should cut down their expenses which are irrelevant or

unnecessary. Maintenance expenses highly impact an organisation as these expenses can be

decreased by proper management and controlling practices. Success factors related to

maintenance expenses are mentioned below:

Smart looks company should use computerised maintenance technology so that they can

control these expenses by using more reliable and accurate measures.

This organisation must include preventive maintenance in their operations, according to

which they should set a fixed schedule for checking of critical equipments.

Cost reduction and profitability increase

Cost included in business operations must be reduced by Smart looks company in order

to gain more profitability which will help the organisation in growth and development. Success

factor for this metric are:

In order to gain increased profitability, the above mentioned company should produce

more attractive and cost efficient products in order to attract customers.

Economy growth is also an success factor as, if the economy is growing then the demand

for luxury goods will also increase (Tucker, 2016).

2.3 Suggestions of reducing cost

In order to reduce the costs, few suggestions are mentioned below:

Smart looks company can reduce its supply expenses such as office supplies which can

be reduced by buying these goods in bulk through a specific vendor.

Production costs and financial expenses should be lowered by using updated technologies

along with using various policies such as optimum utilisation of the resources.

Value and quality can be enhanced by focusing on qualitative measures and not quantitative

measures as by producing quality products, organisation can gain trust of public which will

ultimately result in enhanced value of the company. This value can be increased using various

strategies of price constant and others (Zaleha Abdul Rasid, 2011).

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

3.1 Definition and Purposes of budgets

a. Definition of budget

Budget is a estimation of future cost and incomes over a specific period of time which

shows future aims and objectives. It includes all forecasts about financial results and position of

an organisation (Wild, 2012).

b. Purpose of budget

Budgets are prepared in every organisation with few specific aims which are mentioned

below:

The main aim of preparing budgets are forecasting future incomes and expenditures

which helps an organisation like Smart looks in planning process. This process helps an

organisation's managers to predict future profit and loss. Budgets helps in preparation of

plans, policies, strategies etc.

Budgets are prepared with the goal of decision making. These estimations provides a

financial framework which assist in decision making process. These decisions are made

regarding spending funds on various business operations like promotion, advertising etc.

Another objective of budgets is to monitor and control business performance. The

purpose of budgeting is to enable the actual business performance to be measured against

the forecasted performance. This ultimately ascertains that the whether the business is

operating according to the expectations or not (Wouters, 2015).

3.2 Various methods of preparing budget

Zero based budget – According to this budget, all expenses must be justified for every

new accounting period. In budget is based on zero base by which every function with an

organisation is analysed (Zero based budgeting, 2018).

Fixed budget – Fixed budget is the static budget which does not change or flex when

sales or production units changes. Smart look company uses its budget to estimate

commission of their members.

Variable budget – This budget is also known as flexible budget, expenses are incomes

change according to the sales and production unit of the organisation.

9

3.1 Definition and Purposes of budgets

a. Definition of budget

Budget is a estimation of future cost and incomes over a specific period of time which

shows future aims and objectives. It includes all forecasts about financial results and position of

an organisation (Wild, 2012).

b. Purpose of budget

Budgets are prepared in every organisation with few specific aims which are mentioned

below:

The main aim of preparing budgets are forecasting future incomes and expenditures

which helps an organisation like Smart looks in planning process. This process helps an

organisation's managers to predict future profit and loss. Budgets helps in preparation of

plans, policies, strategies etc.

Budgets are prepared with the goal of decision making. These estimations provides a

financial framework which assist in decision making process. These decisions are made

regarding spending funds on various business operations like promotion, advertising etc.

Another objective of budgets is to monitor and control business performance. The

purpose of budgeting is to enable the actual business performance to be measured against

the forecasted performance. This ultimately ascertains that the whether the business is

operating according to the expectations or not (Wouters, 2015).

3.2 Various methods of preparing budget

Zero based budget – According to this budget, all expenses must be justified for every

new accounting period. In budget is based on zero base by which every function with an

organisation is analysed (Zero based budgeting, 2018).

Fixed budget – Fixed budget is the static budget which does not change or flex when

sales or production units changes. Smart look company uses its budget to estimate

commission of their members.

Variable budget – This budget is also known as flexible budget, expenses are incomes

change according to the sales and production unit of the organisation.

9

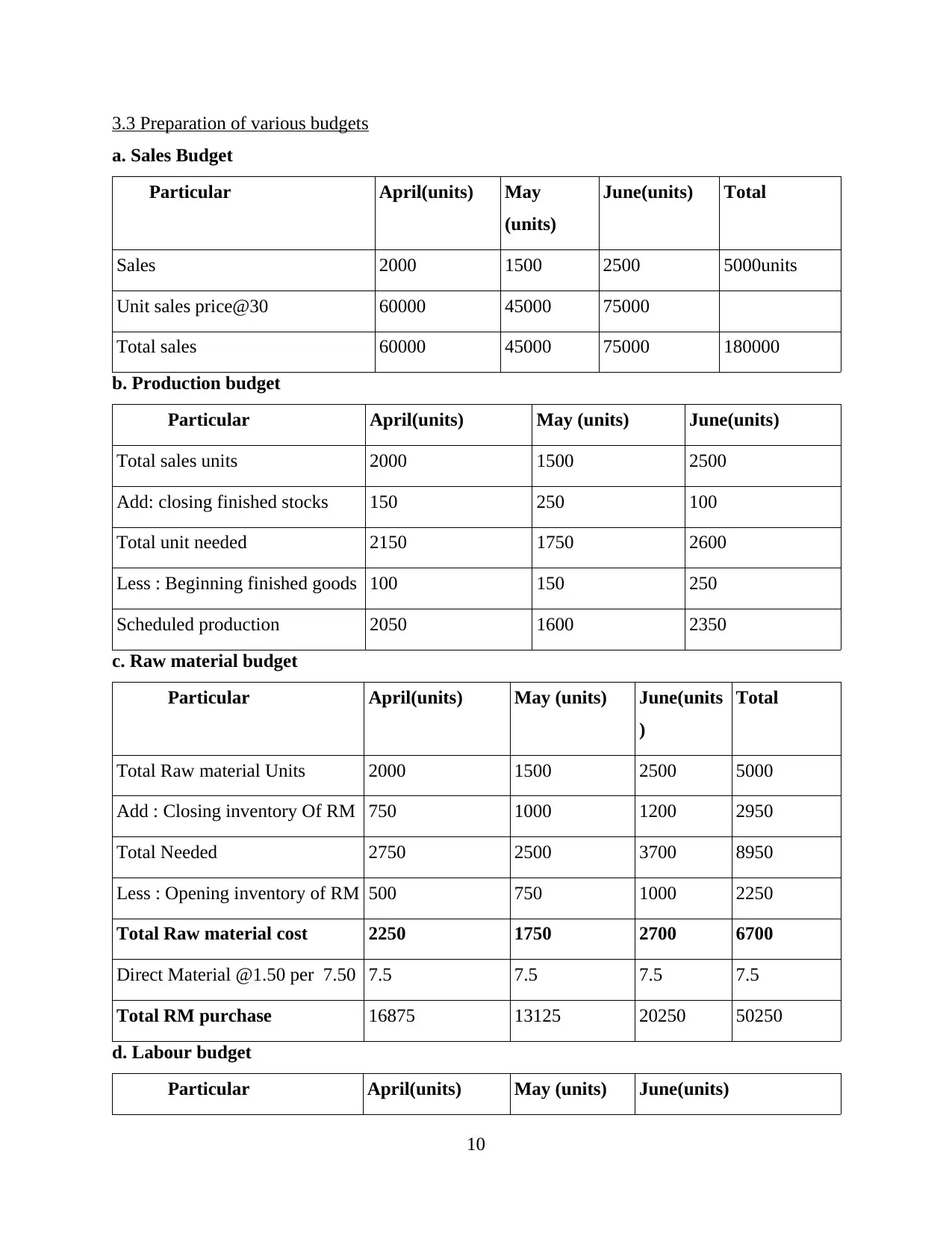

3.3 Preparation of various budgets

a. Sales Budget

Particular April(units) May

(units)

June(units) Total

Sales 2000 1500 2500 5000units

Unit sales price@30 60000 45000 75000

Total sales 60000 45000 75000 180000

b. Production budget

Particular April(units) May (units) June(units)

Total sales units 2000 1500 2500

Add: closing finished stocks 150 250 100

Total unit needed 2150 1750 2600

Less : Beginning finished goods 100 150 250

Scheduled production 2050 1600 2350

c. Raw material budget

Particular April(units) May (units) June(units

)

Total

Total Raw material Units 2000 1500 2500 5000

Add : Closing inventory Of RM 750 1000 1200 2950

Total Needed 2750 2500 3700 8950

Less : Opening inventory of RM 500 750 1000 2250

Total Raw material cost 2250 1750 2700 6700

Direct Material @1.50 per 7.50 7.5 7.5 7.5 7.5

Total RM purchase 16875 13125 20250 50250

d. Labour budget

Particular April(units) May (units) June(units)

10

a. Sales Budget

Particular April(units) May

(units)

June(units) Total

Sales 2000 1500 2500 5000units

Unit sales price@30 60000 45000 75000

Total sales 60000 45000 75000 180000

b. Production budget

Particular April(units) May (units) June(units)

Total sales units 2000 1500 2500

Add: closing finished stocks 150 250 100

Total unit needed 2150 1750 2600

Less : Beginning finished goods 100 150 250

Scheduled production 2050 1600 2350

c. Raw material budget

Particular April(units) May (units) June(units

)

Total

Total Raw material Units 2000 1500 2500 5000

Add : Closing inventory Of RM 750 1000 1200 2950

Total Needed 2750 2500 3700 8950

Less : Opening inventory of RM 500 750 1000 2250

Total Raw material cost 2250 1750 2700 6700

Direct Material @1.50 per 7.50 7.5 7.5 7.5 7.5

Total RM purchase 16875 13125 20250 50250

d. Labour budget

Particular April(units) May (units) June(units)

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.