Management Accounting Report: Costing, Budgeting, Analysis

VerifiedAdded on 2020/01/28

|16

|4276

|490

Report

AI Summary

This report provides a comprehensive overview of management accounting principles, focusing on costing and budgeting techniques. It begins by classifying costs based on behavior, function, and type, and then details various costing methods like job costing and unit costing, with an emphasis on variable and absorption costing. The report includes calculations of profitability under both variable and absorption costing methods under different scenarios. Furthermore, it explains the process of preparing and analyzing cost reports, identifying key performance indicators for improvement, and suggesting strategies for cost reduction and enhanced value. The report also covers the purpose and nature of the budgeting process, different budgeting methods, and the preparation of a cash budget. Finally, it analyzes variances, identifies possible causes, and recommends corrective actions, along with preparing a reconciled operating statement and reporting findings to management.

Management Accounting:

Costing and Budgeting

Costing and Budgeting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Classification of cost ............................................................................................................3

1.2 Different costing methods and explanation on use of same by the firm...............................3

1.3 Calculating cost using appropriate techniques......................................................................4

1.4 Analysis of cost data.............................................................................................................4

TASK 2............................................................................................................................................7

2.1 Preparation and analysis of cost reports................................................................................7

2.2 Performance indicators for identifying potential improvement............................................8

2.3 Suggestions to reduce quality enhanced value and quality ..................................................9

TASK 3............................................................................................................................................9

3.1 Purpose and nature of budget process...................................................................................9

3.2 Budgeting methods used in case study and comments on same...........................................9

3.3 Way for preparing a budget and and use of method for this purpose.................................10

3.4 Cash budget for the firm.....................................................................................................11

TASK 4..........................................................................................................................................12

4.1 Calculating variances and finding out possible causes and recommending corrective action

...................................................................................................................................................12

4.2 Preparing reconciled operating statement...........................................................................13

4.3 Reporting findings to management in accordance with responsibility center....................14

CONCLUSION..............................................................................................................................14

INDEX OF TABLES

Table 1: Trade payable budget.......................................................................................................11

Table 2: Raw material budget........................................................................................................11

Table 3: Production budget............................................................................................................12

Table 4: Sales budget.....................................................................................................................12

Table 5: Cash budget.....................................................................................................................12

Table 6: Variance calculation of May............................................................................................13

Table 7: Reconciled operating statement of May..........................................................................14

Table 8: Variance at 10% reduction in demand.............................................................................15

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Classification of cost ............................................................................................................3

1.2 Different costing methods and explanation on use of same by the firm...............................3

1.3 Calculating cost using appropriate techniques......................................................................4

1.4 Analysis of cost data.............................................................................................................4

TASK 2............................................................................................................................................7

2.1 Preparation and analysis of cost reports................................................................................7

2.2 Performance indicators for identifying potential improvement............................................8

2.3 Suggestions to reduce quality enhanced value and quality ..................................................9

TASK 3............................................................................................................................................9

3.1 Purpose and nature of budget process...................................................................................9

3.2 Budgeting methods used in case study and comments on same...........................................9

3.3 Way for preparing a budget and and use of method for this purpose.................................10

3.4 Cash budget for the firm.....................................................................................................11

TASK 4..........................................................................................................................................12

4.1 Calculating variances and finding out possible causes and recommending corrective action

...................................................................................................................................................12

4.2 Preparing reconciled operating statement...........................................................................13

4.3 Reporting findings to management in accordance with responsibility center....................14

CONCLUSION..............................................................................................................................14

INDEX OF TABLES

Table 1: Trade payable budget.......................................................................................................11

Table 2: Raw material budget........................................................................................................11

Table 3: Production budget............................................................................................................12

Table 4: Sales budget.....................................................................................................................12

Table 5: Cash budget.....................................................................................................................12

Table 6: Variance calculation of May............................................................................................13

Table 7: Reconciled operating statement of May..........................................................................14

Table 8: Variance at 10% reduction in demand.............................................................................15

INTRODUCTION

Management accounting is one of core branch of accounting that is used to measure

company performance. In this report, costs are classified on the basis of several factors and type

of costs that firm incurred is identified. Along with this, different costing methods are explained

in detail in the report. In the middle part of report budgets are prepared and their results are

interpreted in proper way. Finally, in the report variance analysis is done and comments are done

on same. In this report ways that firm can follow in order to improve its performance are also

described in detail.

TASK 1

1.1 Classification of cost

Costs can be classified on the basis of nature, function and behavior. These classifications

are given below. Behavior- On the basis of this category costs are classified a fixed, variable and semi

variable cost. Fixed cost is a cost that remain static and does not get changed. In case of

Bittern ltd fixed cost is given as £5000 per annum (Kaplan and Atkinson, 2015).

Whereas, in case of variable cost there are production and material cost. It is a cost that

keeps on changing consistently with variation in production. There is semi variable cost

in Bittern ltd which cover labor cost. Some part of this cost is fixed for the firm and

some part is variable. Hence, it can be said that costs of the firm are classified on the

basis of behavior. Function- On this basis cost is divided in to various departments that are running an

organization. Cost related to production, finance and marketing departments are included

in this category of cost.

Type- On the basis of this parameter cost are divided in to labor, material and production

expenses (DRURY, 2013). Labor cost include wages paid to employees and material cost

include cost of purchase of raw material. Hence, it can be said that these are the expenses

that are incurred by every type of organization.

1.2 Different costing methods and explanation on use of same by the firm

Different costing methods that are used by business firms are as follows.

Management accounting is one of core branch of accounting that is used to measure

company performance. In this report, costs are classified on the basis of several factors and type

of costs that firm incurred is identified. Along with this, different costing methods are explained

in detail in the report. In the middle part of report budgets are prepared and their results are

interpreted in proper way. Finally, in the report variance analysis is done and comments are done

on same. In this report ways that firm can follow in order to improve its performance are also

described in detail.

TASK 1

1.1 Classification of cost

Costs can be classified on the basis of nature, function and behavior. These classifications

are given below. Behavior- On the basis of this category costs are classified a fixed, variable and semi

variable cost. Fixed cost is a cost that remain static and does not get changed. In case of

Bittern ltd fixed cost is given as £5000 per annum (Kaplan and Atkinson, 2015).

Whereas, in case of variable cost there are production and material cost. It is a cost that

keeps on changing consistently with variation in production. There is semi variable cost

in Bittern ltd which cover labor cost. Some part of this cost is fixed for the firm and

some part is variable. Hence, it can be said that costs of the firm are classified on the

basis of behavior. Function- On this basis cost is divided in to various departments that are running an

organization. Cost related to production, finance and marketing departments are included

in this category of cost.

Type- On the basis of this parameter cost are divided in to labor, material and production

expenses (DRURY, 2013). Labor cost include wages paid to employees and material cost

include cost of purchase of raw material. Hence, it can be said that these are the expenses

that are incurred by every type of organization.

1.2 Different costing methods and explanation on use of same by the firm

Different costing methods that are used by business firms are as follows.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Job costing- This is a method in which costs are determined for each and every order

individually because each job have its own specifications. This method of costing is used

in case of building repair projects etc. Contract costing- This costing method is used for for calculating cost for large size

projects. Each contract is assumed as separate unit for costing purpose (Zimmerman and

Yahya-Zadeh, 2011). This costing method is often used for construction of brides and

building etc.

Unit cost- Bittern ltd is using unit cost method and under for per unit of product that is

produced in an organization costing is done. Under this method of costing units are

prepared and there cost is computed. Thereafter, costs are divided by the number of unit

produced. By doing so cost of per unit is computed at Bittern ltd.

1.3 Calculating cost using appropriate techniques

In order to calculate cost appropriate methods are as follows. Variable costing method- This method is also know as direct costing method and under

this technique of cost computation fixed cost are not taken in to account and only variable

cost that are incurred during the production process are considered. Bittern ltd is using

this costing system in its business.

Absorption costing- It is known as full costing methods and under this method all sort of

costs are taken in to account in order to compute cost of production for the firm (Herman,

2011). Hence, it can be said that this method is inverse of variable costing method.

If we compare both methods then it can be said that in absorption costing all sort of costs

are considered but in variable costing system all costs are not taken in to account. Hence, in

terms of profit measurement it can be said that absorption costing system reveal actual profit

earned by the company.

1.4 Analysis of cost data

As per scenario given, Bittern Ltd sale a per unit of its product at a price of £25 per unit.

Earlier, it use a variable costing for cost computation and now it decided to evaluate the system

and to compare same with an absorption costing system (Gow, Ormazabal and Taylor, 2010).

The computaiton of Bittern’s profits in constant-price-level terms for a three-year tenure using

variable costing system and full-cost absorption costing system is given below.

individually because each job have its own specifications. This method of costing is used

in case of building repair projects etc. Contract costing- This costing method is used for for calculating cost for large size

projects. Each contract is assumed as separate unit for costing purpose (Zimmerman and

Yahya-Zadeh, 2011). This costing method is often used for construction of brides and

building etc.

Unit cost- Bittern ltd is using unit cost method and under for per unit of product that is

produced in an organization costing is done. Under this method of costing units are

prepared and there cost is computed. Thereafter, costs are divided by the number of unit

produced. By doing so cost of per unit is computed at Bittern ltd.

1.3 Calculating cost using appropriate techniques

In order to calculate cost appropriate methods are as follows. Variable costing method- This method is also know as direct costing method and under

this technique of cost computation fixed cost are not taken in to account and only variable

cost that are incurred during the production process are considered. Bittern ltd is using

this costing system in its business.

Absorption costing- It is known as full costing methods and under this method all sort of

costs are taken in to account in order to compute cost of production for the firm (Herman,

2011). Hence, it can be said that this method is inverse of variable costing method.

If we compare both methods then it can be said that in absorption costing all sort of costs

are considered but in variable costing system all costs are not taken in to account. Hence, in

terms of profit measurement it can be said that absorption costing system reveal actual profit

earned by the company.

1.4 Analysis of cost data

As per scenario given, Bittern Ltd sale a per unit of its product at a price of £25 per unit.

Earlier, it use a variable costing for cost computation and now it decided to evaluate the system

and to compare same with an absorption costing system (Gow, Ormazabal and Taylor, 2010).

The computaiton of Bittern’s profits in constant-price-level terms for a three-year tenure using

variable costing system and full-cost absorption costing system is given below.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

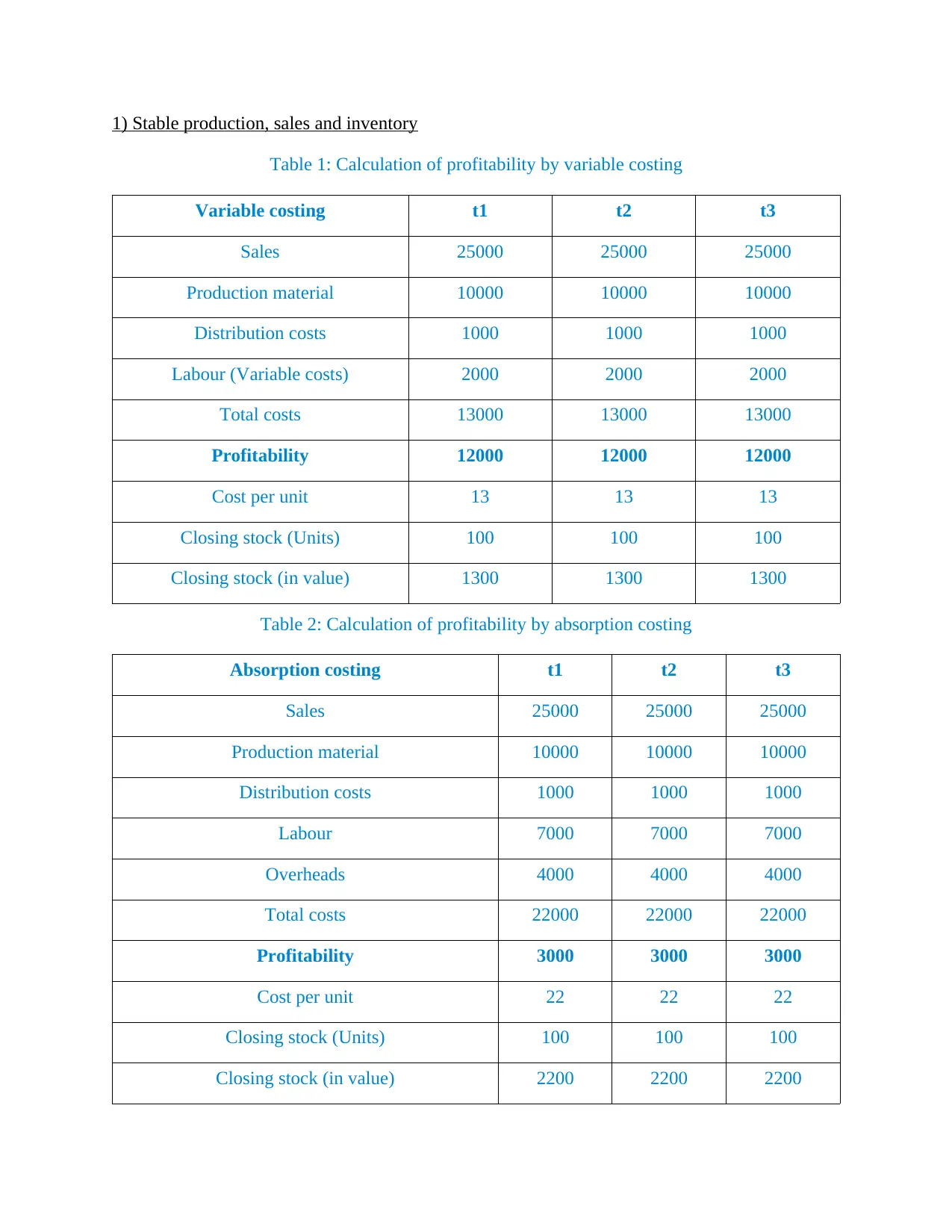

1) Stable production, sales and inventory

Table 1: Calculation of profitability by variable costing

Variable costing t1 t2 t3

Sales 25000 25000 25000

Production material 10000 10000 10000

Distribution costs 1000 1000 1000

Labour (Variable costs) 2000 2000 2000

Total costs 13000 13000 13000

Profitability 12000 12000 12000

Cost per unit 13 13 13

Closing stock (Units) 100 100 100

Closing stock (in value) 1300 1300 1300

Table 2: Calculation of profitability by absorption costing

Absorption costing t1 t2 t3

Sales 25000 25000 25000

Production material 10000 10000 10000

Distribution costs 1000 1000 1000

Labour 7000 7000 7000

Overheads 4000 4000 4000

Total costs 22000 22000 22000

Profitability 3000 3000 3000

Cost per unit 22 22 22

Closing stock (Units) 100 100 100

Closing stock (in value) 2200 2200 2200

Table 1: Calculation of profitability by variable costing

Variable costing t1 t2 t3

Sales 25000 25000 25000

Production material 10000 10000 10000

Distribution costs 1000 1000 1000

Labour (Variable costs) 2000 2000 2000

Total costs 13000 13000 13000

Profitability 12000 12000 12000

Cost per unit 13 13 13

Closing stock (Units) 100 100 100

Closing stock (in value) 1300 1300 1300

Table 2: Calculation of profitability by absorption costing

Absorption costing t1 t2 t3

Sales 25000 25000 25000

Production material 10000 10000 10000

Distribution costs 1000 1000 1000

Labour 7000 7000 7000

Overheads 4000 4000 4000

Total costs 22000 22000 22000

Profitability 3000 3000 3000

Cost per unit 22 22 22

Closing stock (Units) 100 100 100

Closing stock (in value) 2200 2200 2200

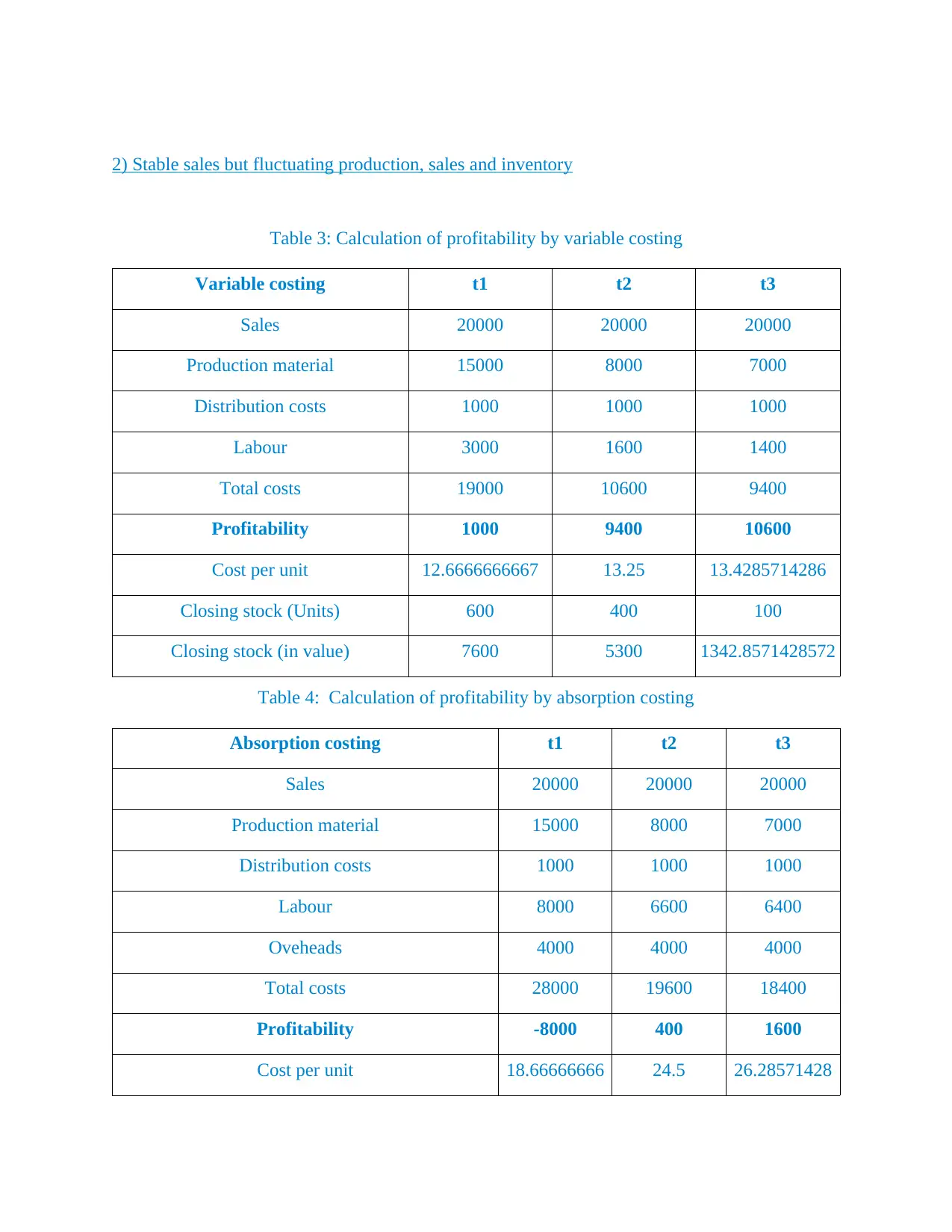

2) Stable sales but fluctuating production, sales and inventory

Table 3: Calculation of profitability by variable costing

Variable costing t1 t2 t3

Sales 20000 20000 20000

Production material 15000 8000 7000

Distribution costs 1000 1000 1000

Labour 3000 1600 1400

Total costs 19000 10600 9400

Profitability 1000 9400 10600

Cost per unit 12.6666666667 13.25 13.4285714286

Closing stock (Units) 600 400 100

Closing stock (in value) 7600 5300 1342.8571428572

Table 4: Calculation of profitability by absorption costing

Absorption costing t1 t2 t3

Sales 20000 20000 20000

Production material 15000 8000 7000

Distribution costs 1000 1000 1000

Labour 8000 6600 6400

Oveheads 4000 4000 4000

Total costs 28000 19600 18400

Profitability -8000 400 1600

Cost per unit 18.66666666 24.5 26.28571428

Table 3: Calculation of profitability by variable costing

Variable costing t1 t2 t3

Sales 20000 20000 20000

Production material 15000 8000 7000

Distribution costs 1000 1000 1000

Labour 3000 1600 1400

Total costs 19000 10600 9400

Profitability 1000 9400 10600

Cost per unit 12.6666666667 13.25 13.4285714286

Closing stock (Units) 600 400 100

Closing stock (in value) 7600 5300 1342.8571428572

Table 4: Calculation of profitability by absorption costing

Absorption costing t1 t2 t3

Sales 20000 20000 20000

Production material 15000 8000 7000

Distribution costs 1000 1000 1000

Labour 8000 6600 6400

Oveheads 4000 4000 4000

Total costs 28000 19600 18400

Profitability -8000 400 1600

Cost per unit 18.66666666 24.5 26.28571428

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

67 57

Closing stock (Units) 600 400 100

Closing stock (in value) 11200 9800

2628.571428

5714

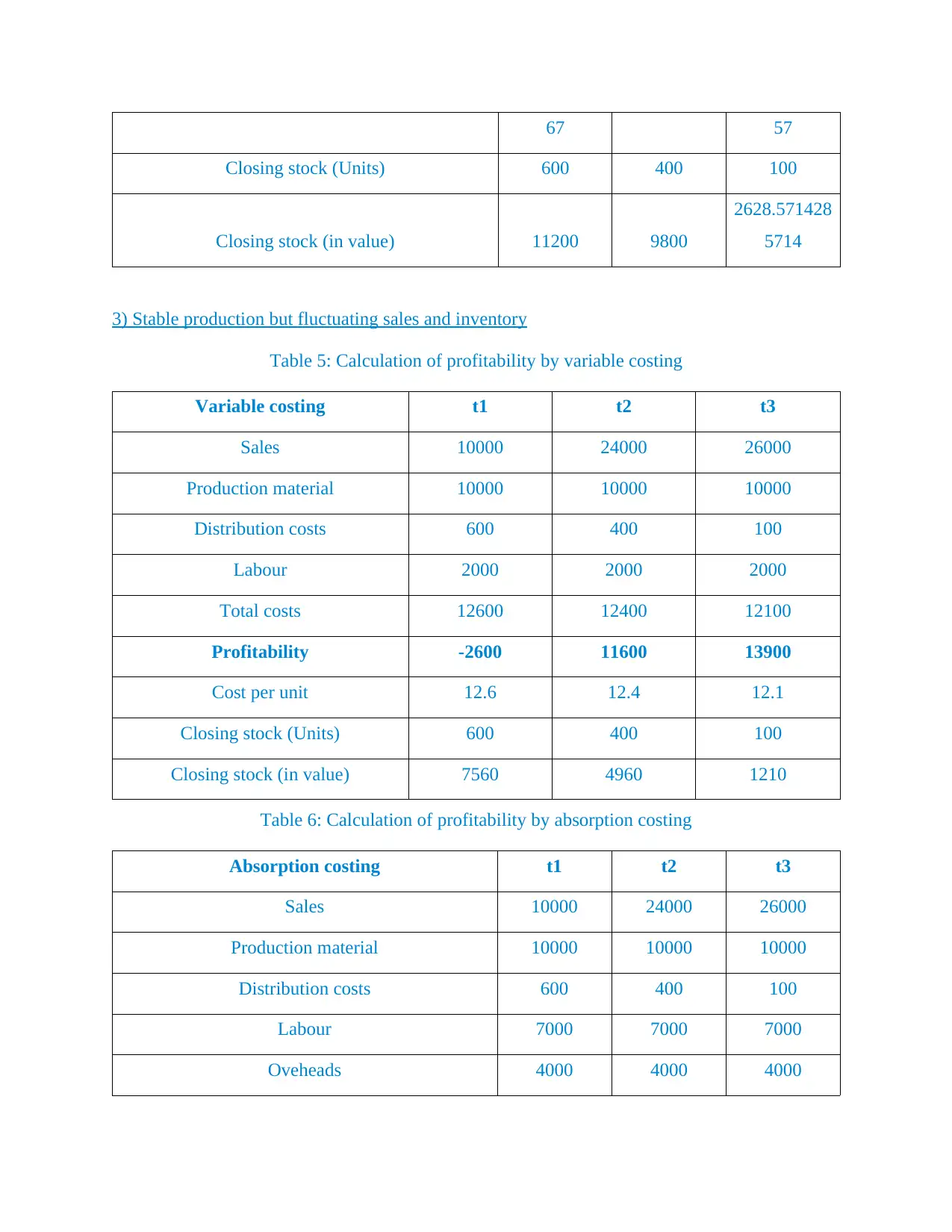

3) Stable production but fluctuating sales and inventory

Table 5: Calculation of profitability by variable costing

Variable costing t1 t2 t3

Sales 10000 24000 26000

Production material 10000 10000 10000

Distribution costs 600 400 100

Labour 2000 2000 2000

Total costs 12600 12400 12100

Profitability -2600 11600 13900

Cost per unit 12.6 12.4 12.1

Closing stock (Units) 600 400 100

Closing stock (in value) 7560 4960 1210

Table 6: Calculation of profitability by absorption costing

Absorption costing t1 t2 t3

Sales 10000 24000 26000

Production material 10000 10000 10000

Distribution costs 600 400 100

Labour 7000 7000 7000

Oveheads 4000 4000 4000

Closing stock (Units) 600 400 100

Closing stock (in value) 11200 9800

2628.571428

5714

3) Stable production but fluctuating sales and inventory

Table 5: Calculation of profitability by variable costing

Variable costing t1 t2 t3

Sales 10000 24000 26000

Production material 10000 10000 10000

Distribution costs 600 400 100

Labour 2000 2000 2000

Total costs 12600 12400 12100

Profitability -2600 11600 13900

Cost per unit 12.6 12.4 12.1

Closing stock (Units) 600 400 100

Closing stock (in value) 7560 4960 1210

Table 6: Calculation of profitability by absorption costing

Absorption costing t1 t2 t3

Sales 10000 24000 26000

Production material 10000 10000 10000

Distribution costs 600 400 100

Labour 7000 7000 7000

Oveheads 4000 4000 4000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total costs 21600 21400 21100

Profitability -11600 2600 4900

Cost per unit 21.6 21.4 21.1

Closing stock (Units) 600 400 100

Closing stock (in value) 12960 8560 2110

TASK 2

Note: (Presentation is available separately)

2.1 Preparation and analysis of cost reports

Following is the process for preparing and analyzing cost. Gathering information- In this stage Tesco managers will collect data related to sales

and cost earlier in previous year (Zang, 2011). This will help in preparation of cost

reports in legitimate way and will be used for making business decisions. Itemized tangible cost- In his stage table is prepared in which all tangible costs are listed.

It help managers in keeping record related to actual expenses that were made by the firm

in specific time period. Categorizing intangible cost- In this stage data related to all intangible expenses is

collected like expenses made to in relation to develop goodwill of the business. Inclusion

of these costs will help in computing actual product cost and will also help managers in

determining margin percentage on produced units. Presenting cost in systematic way- In this stage all tangible and intangible costs are

included in single table in order to get overview of entire cost that is incurred by firm in

its business. Hence, this table will be very helpful to managers in making cost related

decisions. Costing benefit analysis- This analysis will help managers of Tesco in identifying the

benefit that firm is getting on the cost that it is incurred in its business. By doing so firm

will come to know about the return that it is earning on the incurred cost.

Calculating the payback time period- In order to analyze cost time period will be

identified within which firm will be able to recover cost incurred and will start earning

Profitability -11600 2600 4900

Cost per unit 21.6 21.4 21.1

Closing stock (Units) 600 400 100

Closing stock (in value) 12960 8560 2110

TASK 2

Note: (Presentation is available separately)

2.1 Preparation and analysis of cost reports

Following is the process for preparing and analyzing cost. Gathering information- In this stage Tesco managers will collect data related to sales

and cost earlier in previous year (Zang, 2011). This will help in preparation of cost

reports in legitimate way and will be used for making business decisions. Itemized tangible cost- In his stage table is prepared in which all tangible costs are listed.

It help managers in keeping record related to actual expenses that were made by the firm

in specific time period. Categorizing intangible cost- In this stage data related to all intangible expenses is

collected like expenses made to in relation to develop goodwill of the business. Inclusion

of these costs will help in computing actual product cost and will also help managers in

determining margin percentage on produced units. Presenting cost in systematic way- In this stage all tangible and intangible costs are

included in single table in order to get overview of entire cost that is incurred by firm in

its business. Hence, this table will be very helpful to managers in making cost related

decisions. Costing benefit analysis- This analysis will help managers of Tesco in identifying the

benefit that firm is getting on the cost that it is incurred in its business. By doing so firm

will come to know about the return that it is earning on the incurred cost.

Calculating the payback time period- In order to analyze cost time period will be

identified within which firm will be able to recover cost incurred and will start earning

profit (Bebbington, Unerman, and O'Dwyer, 2014). Hence, these are the steps that will

be followed in order to compute cost and analyzing same.

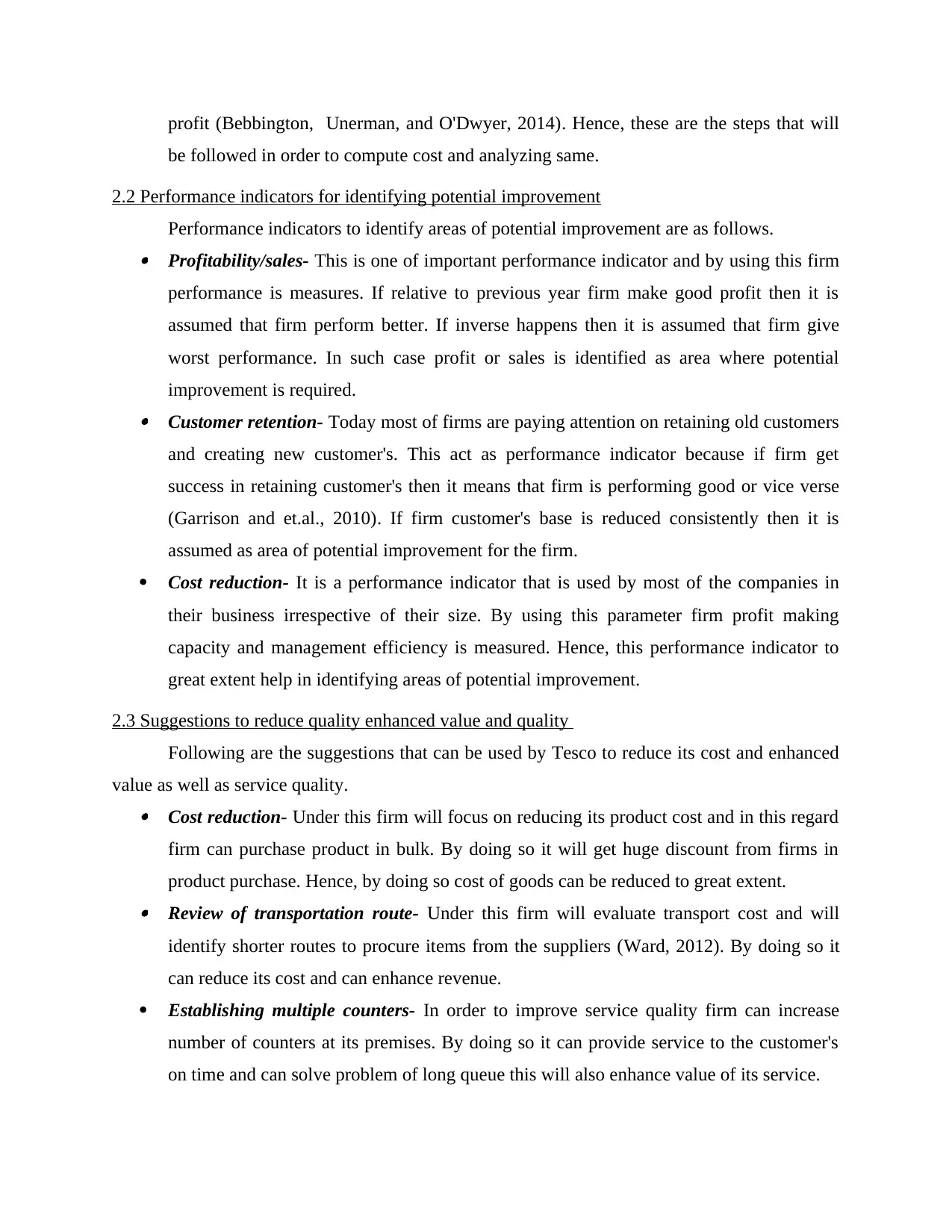

2.2 Performance indicators for identifying potential improvement

Performance indicators to identify areas of potential improvement are as follows. Profitability/sales- This is one of important performance indicator and by using this firm

performance is measures. If relative to previous year firm make good profit then it is

assumed that firm perform better. If inverse happens then it is assumed that firm give

worst performance. In such case profit or sales is identified as area where potential

improvement is required. Customer retention- Today most of firms are paying attention on retaining old customers

and creating new customer's. This act as performance indicator because if firm get

success in retaining customer's then it means that firm is performing good or vice verse

(Garrison and et.al., 2010). If firm customer's base is reduced consistently then it is

assumed as area of potential improvement for the firm.

Cost reduction- It is a performance indicator that is used by most of the companies in

their business irrespective of their size. By using this parameter firm profit making

capacity and management efficiency is measured. Hence, this performance indicator to

great extent help in identifying areas of potential improvement.

2.3 Suggestions to reduce quality enhanced value and quality

Following are the suggestions that can be used by Tesco to reduce its cost and enhanced

value as well as service quality. Cost reduction- Under this firm will focus on reducing its product cost and in this regard

firm can purchase product in bulk. By doing so it will get huge discount from firms in

product purchase. Hence, by doing so cost of goods can be reduced to great extent. Review of transportation route- Under this firm will evaluate transport cost and will

identify shorter routes to procure items from the suppliers (Ward, 2012). By doing so it

can reduce its cost and can enhance revenue.

Establishing multiple counters- In order to improve service quality firm can increase

number of counters at its premises. By doing so it can provide service to the customer's

on time and can solve problem of long queue this will also enhance value of its service.

be followed in order to compute cost and analyzing same.

2.2 Performance indicators for identifying potential improvement

Performance indicators to identify areas of potential improvement are as follows. Profitability/sales- This is one of important performance indicator and by using this firm

performance is measures. If relative to previous year firm make good profit then it is

assumed that firm perform better. If inverse happens then it is assumed that firm give

worst performance. In such case profit or sales is identified as area where potential

improvement is required. Customer retention- Today most of firms are paying attention on retaining old customers

and creating new customer's. This act as performance indicator because if firm get

success in retaining customer's then it means that firm is performing good or vice verse

(Garrison and et.al., 2010). If firm customer's base is reduced consistently then it is

assumed as area of potential improvement for the firm.

Cost reduction- It is a performance indicator that is used by most of the companies in

their business irrespective of their size. By using this parameter firm profit making

capacity and management efficiency is measured. Hence, this performance indicator to

great extent help in identifying areas of potential improvement.

2.3 Suggestions to reduce quality enhanced value and quality

Following are the suggestions that can be used by Tesco to reduce its cost and enhanced

value as well as service quality. Cost reduction- Under this firm will focus on reducing its product cost and in this regard

firm can purchase product in bulk. By doing so it will get huge discount from firms in

product purchase. Hence, by doing so cost of goods can be reduced to great extent. Review of transportation route- Under this firm will evaluate transport cost and will

identify shorter routes to procure items from the suppliers (Ward, 2012). By doing so it

can reduce its cost and can enhance revenue.

Establishing multiple counters- In order to improve service quality firm can increase

number of counters at its premises. By doing so it can provide service to the customer's

on time and can solve problem of long queue this will also enhance value of its service.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

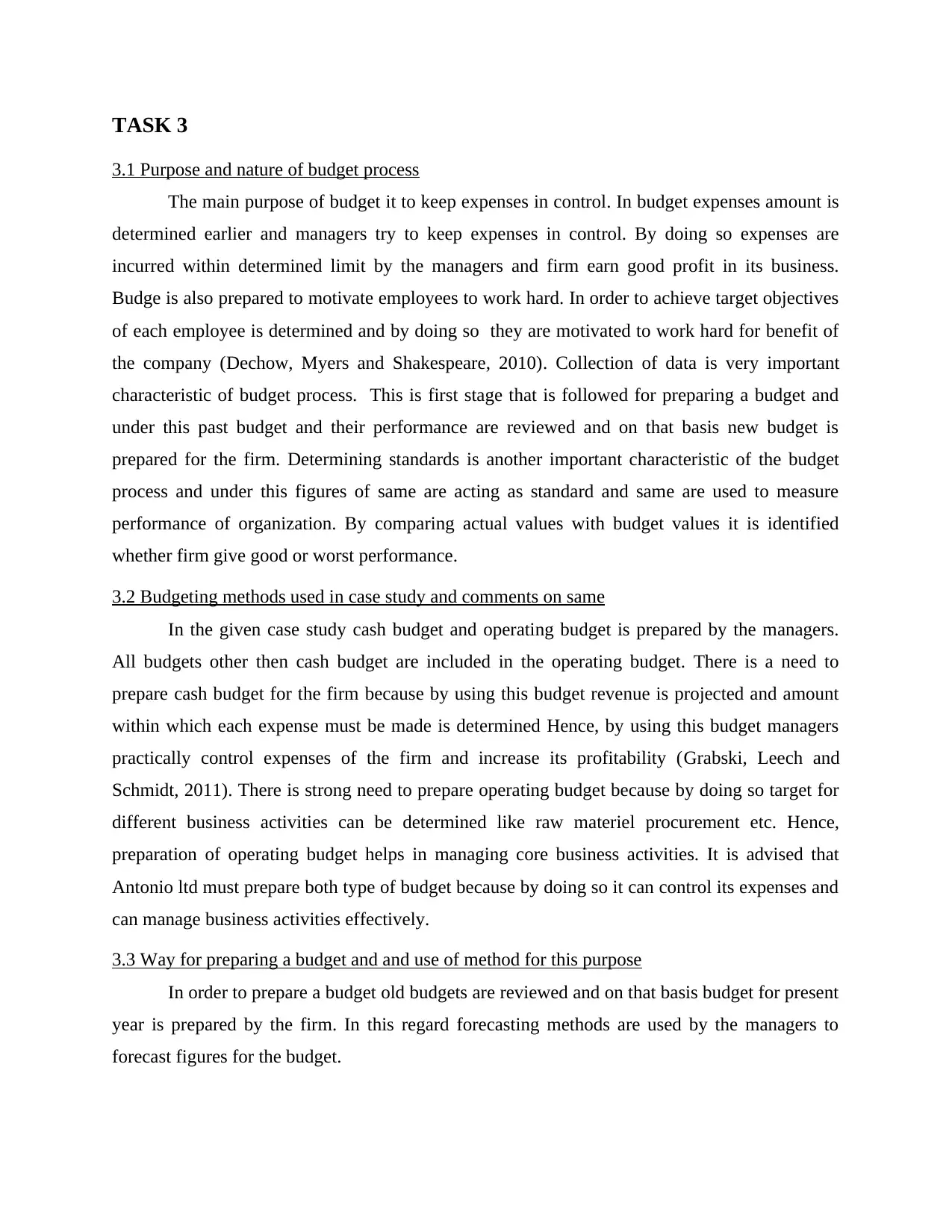

TASK 3

3.1 Purpose and nature of budget process

The main purpose of budget it to keep expenses in control. In budget expenses amount is

determined earlier and managers try to keep expenses in control. By doing so expenses are

incurred within determined limit by the managers and firm earn good profit in its business.

Budge is also prepared to motivate employees to work hard. In order to achieve target objectives

of each employee is determined and by doing so they are motivated to work hard for benefit of

the company (Dechow, Myers and Shakespeare, 2010). Collection of data is very important

characteristic of budget process. This is first stage that is followed for preparing a budget and

under this past budget and their performance are reviewed and on that basis new budget is

prepared for the firm. Determining standards is another important characteristic of the budget

process and under this figures of same are acting as standard and same are used to measure

performance of organization. By comparing actual values with budget values it is identified

whether firm give good or worst performance.

3.2 Budgeting methods used in case study and comments on same

In the given case study cash budget and operating budget is prepared by the managers.

All budgets other then cash budget are included in the operating budget. There is a need to

prepare cash budget for the firm because by using this budget revenue is projected and amount

within which each expense must be made is determined Hence, by using this budget managers

practically control expenses of the firm and increase its profitability (Grabski, Leech and

Schmidt, 2011). There is strong need to prepare operating budget because by doing so target for

different business activities can be determined like raw materiel procurement etc. Hence,

preparation of operating budget helps in managing core business activities. It is advised that

Antonio ltd must prepare both type of budget because by doing so it can control its expenses and

can manage business activities effectively.

3.3 Way for preparing a budget and and use of method for this purpose

In order to prepare a budget old budgets are reviewed and on that basis budget for present

year is prepared by the firm. In this regard forecasting methods are used by the managers to

forecast figures for the budget.

3.1 Purpose and nature of budget process

The main purpose of budget it to keep expenses in control. In budget expenses amount is

determined earlier and managers try to keep expenses in control. By doing so expenses are

incurred within determined limit by the managers and firm earn good profit in its business.

Budge is also prepared to motivate employees to work hard. In order to achieve target objectives

of each employee is determined and by doing so they are motivated to work hard for benefit of

the company (Dechow, Myers and Shakespeare, 2010). Collection of data is very important

characteristic of budget process. This is first stage that is followed for preparing a budget and

under this past budget and their performance are reviewed and on that basis new budget is

prepared for the firm. Determining standards is another important characteristic of the budget

process and under this figures of same are acting as standard and same are used to measure

performance of organization. By comparing actual values with budget values it is identified

whether firm give good or worst performance.

3.2 Budgeting methods used in case study and comments on same

In the given case study cash budget and operating budget is prepared by the managers.

All budgets other then cash budget are included in the operating budget. There is a need to

prepare cash budget for the firm because by using this budget revenue is projected and amount

within which each expense must be made is determined Hence, by using this budget managers

practically control expenses of the firm and increase its profitability (Grabski, Leech and

Schmidt, 2011). There is strong need to prepare operating budget because by doing so target for

different business activities can be determined like raw materiel procurement etc. Hence,

preparation of operating budget helps in managing core business activities. It is advised that

Antonio ltd must prepare both type of budget because by doing so it can control its expenses and

can manage business activities effectively.

3.3 Way for preparing a budget and and use of method for this purpose

In order to prepare a budget old budgets are reviewed and on that basis budget for present

year is prepared by the firm. In this regard forecasting methods are used by the managers to

forecast figures for the budget.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

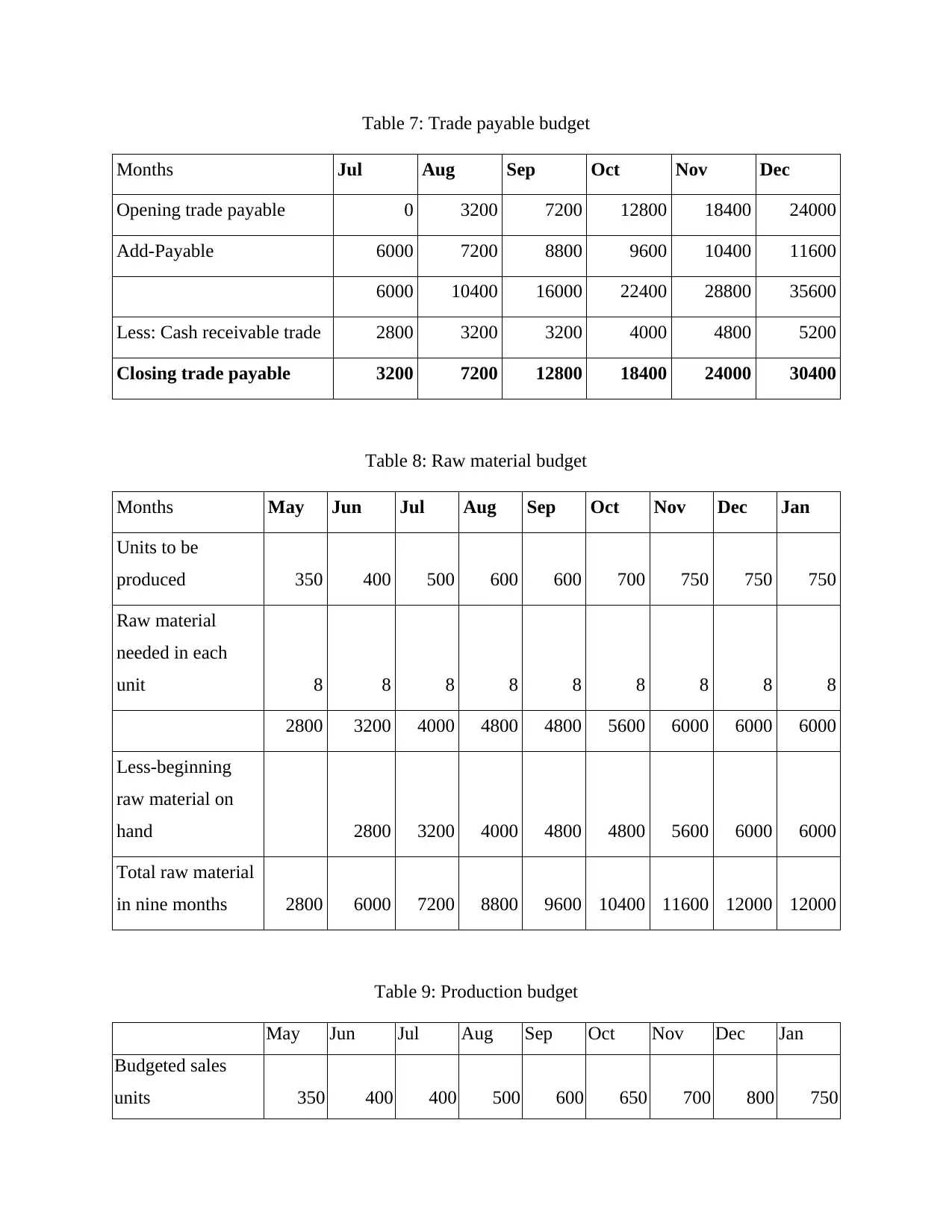

Table 7: Trade payable budget

Months Jul Aug Sep Oct Nov Dec

Opening trade payable 0 3200 7200 12800 18400 24000

Add-Payable 6000 7200 8800 9600 10400 11600

6000 10400 16000 22400 28800 35600

Less: Cash receivable trade 2800 3200 3200 4000 4800 5200

Closing trade payable 3200 7200 12800 18400 24000 30400

Table 8: Raw material budget

Months May Jun Jul Aug Sep Oct Nov Dec Jan

Units to be

produced 350 400 500 600 600 700 750 750 750

Raw material

needed in each

unit 8 8 8 8 8 8 8 8 8

2800 3200 4000 4800 4800 5600 6000 6000 6000

Less-beginning

raw material on

hand 2800 3200 4000 4800 4800 5600 6000 6000

Total raw material

in nine months 2800 6000 7200 8800 9600 10400 11600 12000 12000

Table 9: Production budget

May Jun Jul Aug Sep Oct Nov Dec Jan

Budgeted sales

units 350 400 400 500 600 650 700 800 750

Months Jul Aug Sep Oct Nov Dec

Opening trade payable 0 3200 7200 12800 18400 24000

Add-Payable 6000 7200 8800 9600 10400 11600

6000 10400 16000 22400 28800 35600

Less: Cash receivable trade 2800 3200 3200 4000 4800 5200

Closing trade payable 3200 7200 12800 18400 24000 30400

Table 8: Raw material budget

Months May Jun Jul Aug Sep Oct Nov Dec Jan

Units to be

produced 350 400 500 600 600 700 750 750 750

Raw material

needed in each

unit 8 8 8 8 8 8 8 8 8

2800 3200 4000 4800 4800 5600 6000 6000 6000

Less-beginning

raw material on

hand 2800 3200 4000 4800 4800 5600 6000 6000

Total raw material

in nine months 2800 6000 7200 8800 9600 10400 11600 12000 12000

Table 9: Production budget

May Jun Jul Aug Sep Oct Nov Dec Jan

Budgeted sales

units 350 400 400 500 600 650 700 800 750

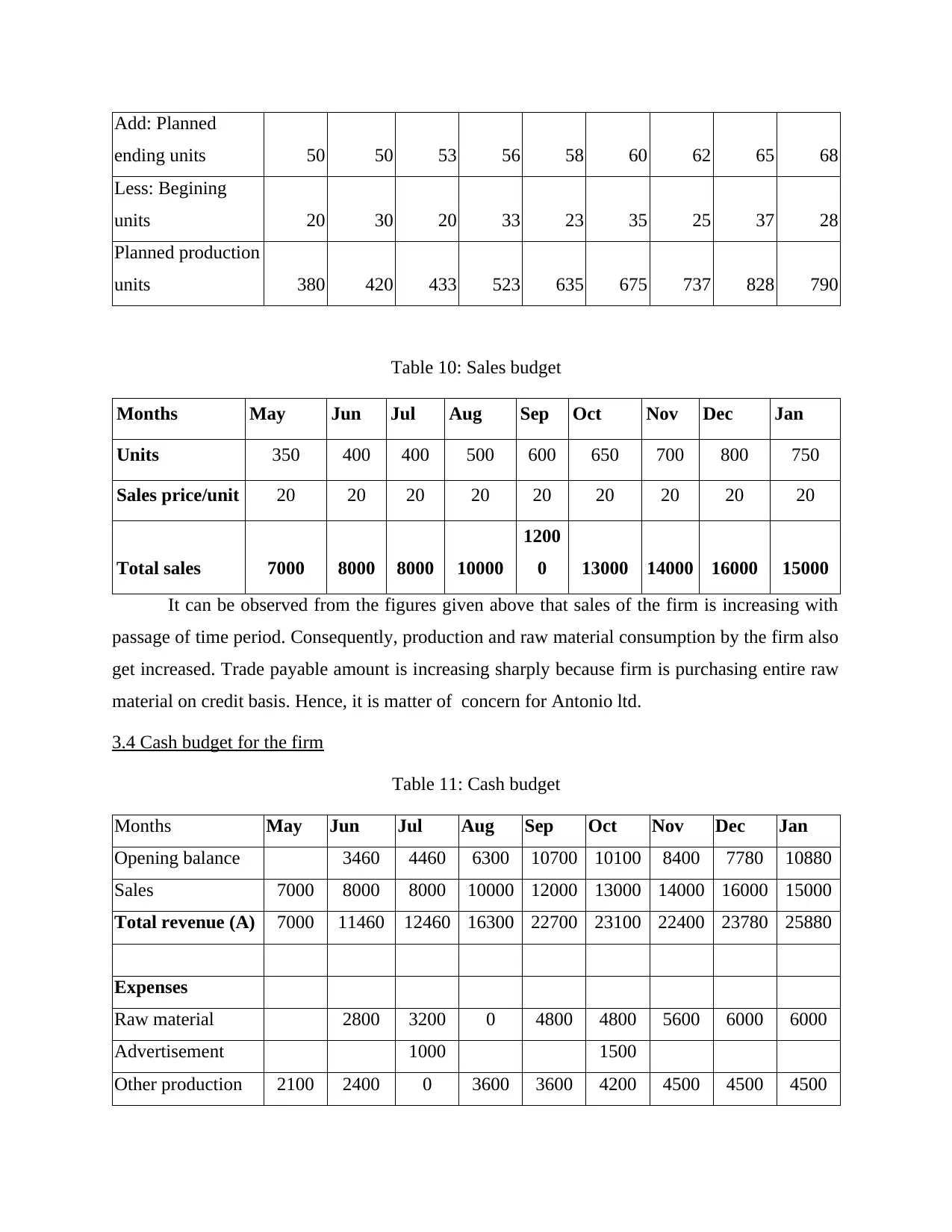

Add: Planned

ending units 50 50 53 56 58 60 62 65 68

Less: Begining

units 20 30 20 33 23 35 25 37 28

Planned production

units 380 420 433 523 635 675 737 828 790

Table 10: Sales budget

Months May Jun Jul Aug Sep Oct Nov Dec Jan

Units 350 400 400 500 600 650 700 800 750

Sales price/unit 20 20 20 20 20 20 20 20 20

Total sales 7000 8000 8000 10000

1200

0 13000 14000 16000 15000

It can be observed from the figures given above that sales of the firm is increasing with

passage of time period. Consequently, production and raw material consumption by the firm also

get increased. Trade payable amount is increasing sharply because firm is purchasing entire raw

material on credit basis. Hence, it is matter of concern for Antonio ltd.

3.4 Cash budget for the firm

Table 11: Cash budget

Months May Jun Jul Aug Sep Oct Nov Dec Jan

Opening balance 3460 4460 6300 10700 10100 8400 7780 10880

Sales 7000 8000 8000 10000 12000 13000 14000 16000 15000

Total revenue (A) 7000 11460 12460 16300 22700 23100 22400 23780 25880

Expenses

Raw material 2800 3200 0 4800 4800 5600 6000 6000

Advertisement 1000 1500

Other production 2100 2400 0 3600 3600 4200 4500 4500 4500

ending units 50 50 53 56 58 60 62 65 68

Less: Begining

units 20 30 20 33 23 35 25 37 28

Planned production

units 380 420 433 523 635 675 737 828 790

Table 10: Sales budget

Months May Jun Jul Aug Sep Oct Nov Dec Jan

Units 350 400 400 500 600 650 700 800 750

Sales price/unit 20 20 20 20 20 20 20 20 20

Total sales 7000 8000 8000 10000

1200

0 13000 14000 16000 15000

It can be observed from the figures given above that sales of the firm is increasing with

passage of time period. Consequently, production and raw material consumption by the firm also

get increased. Trade payable amount is increasing sharply because firm is purchasing entire raw

material on credit basis. Hence, it is matter of concern for Antonio ltd.

3.4 Cash budget for the firm

Table 11: Cash budget

Months May Jun Jul Aug Sep Oct Nov Dec Jan

Opening balance 3460 4460 6300 10700 10100 8400 7780 10880

Sales 7000 8000 8000 10000 12000 13000 14000 16000 15000

Total revenue (A) 7000 11460 12460 16300 22700 23100 22400 23780 25880

Expenses

Raw material 2800 3200 0 4800 4800 5600 6000 6000

Advertisement 1000 1500

Other production 2100 2400 0 3600 3600 4200 4500 4500 4500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.