Management Accounting: Costing, Journal Entries, and Overhead

VerifiedAdded on 2023/06/04

|16

|1670

|424

Report

AI Summary

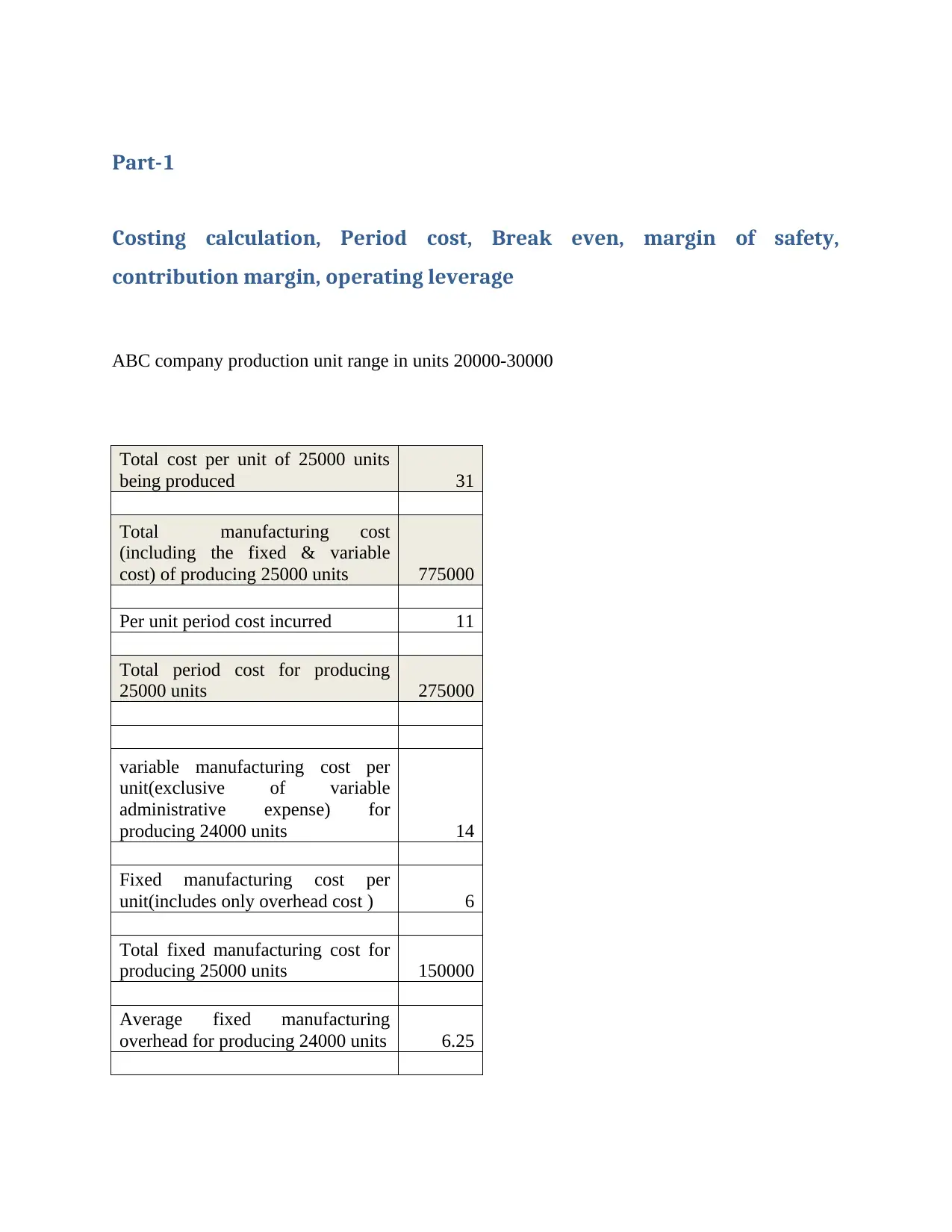

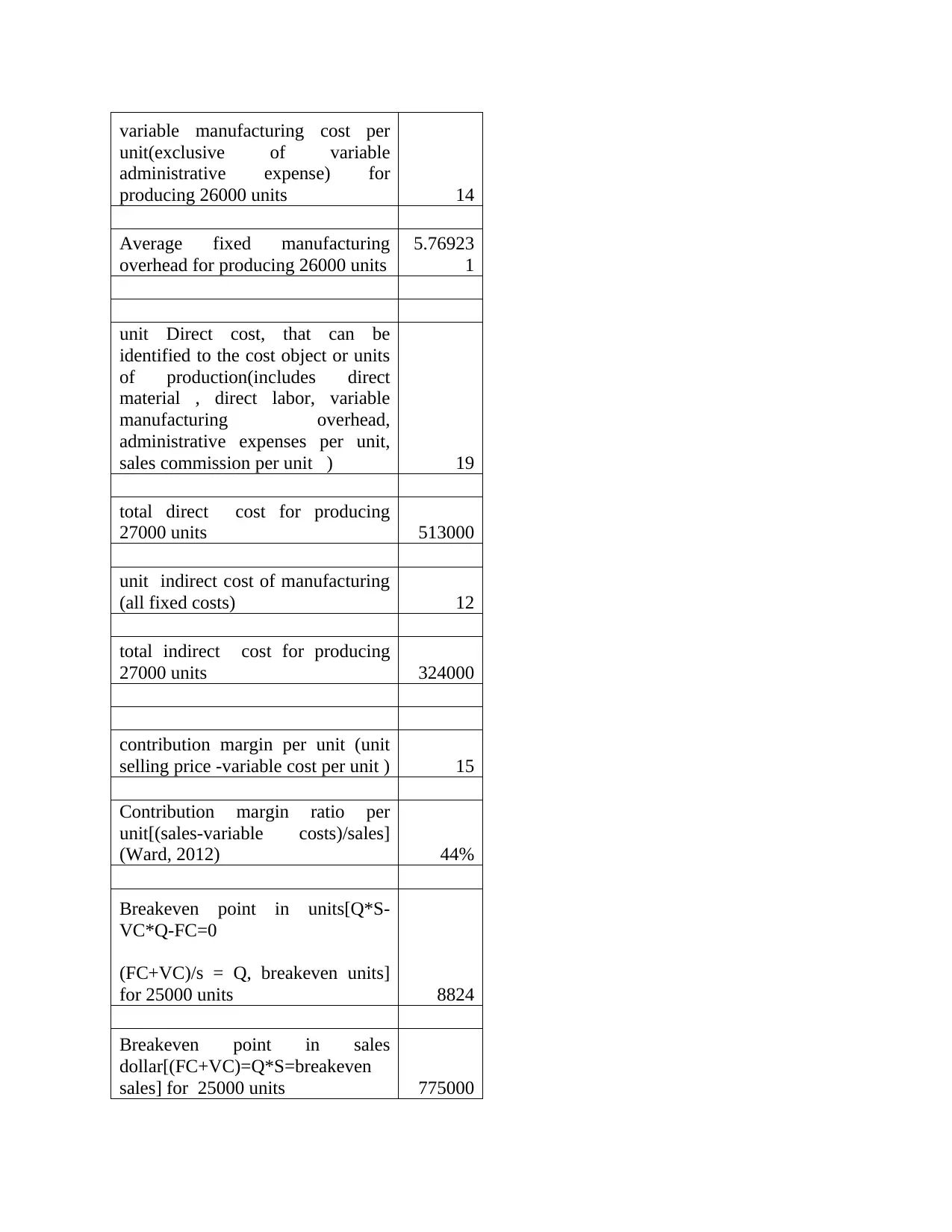

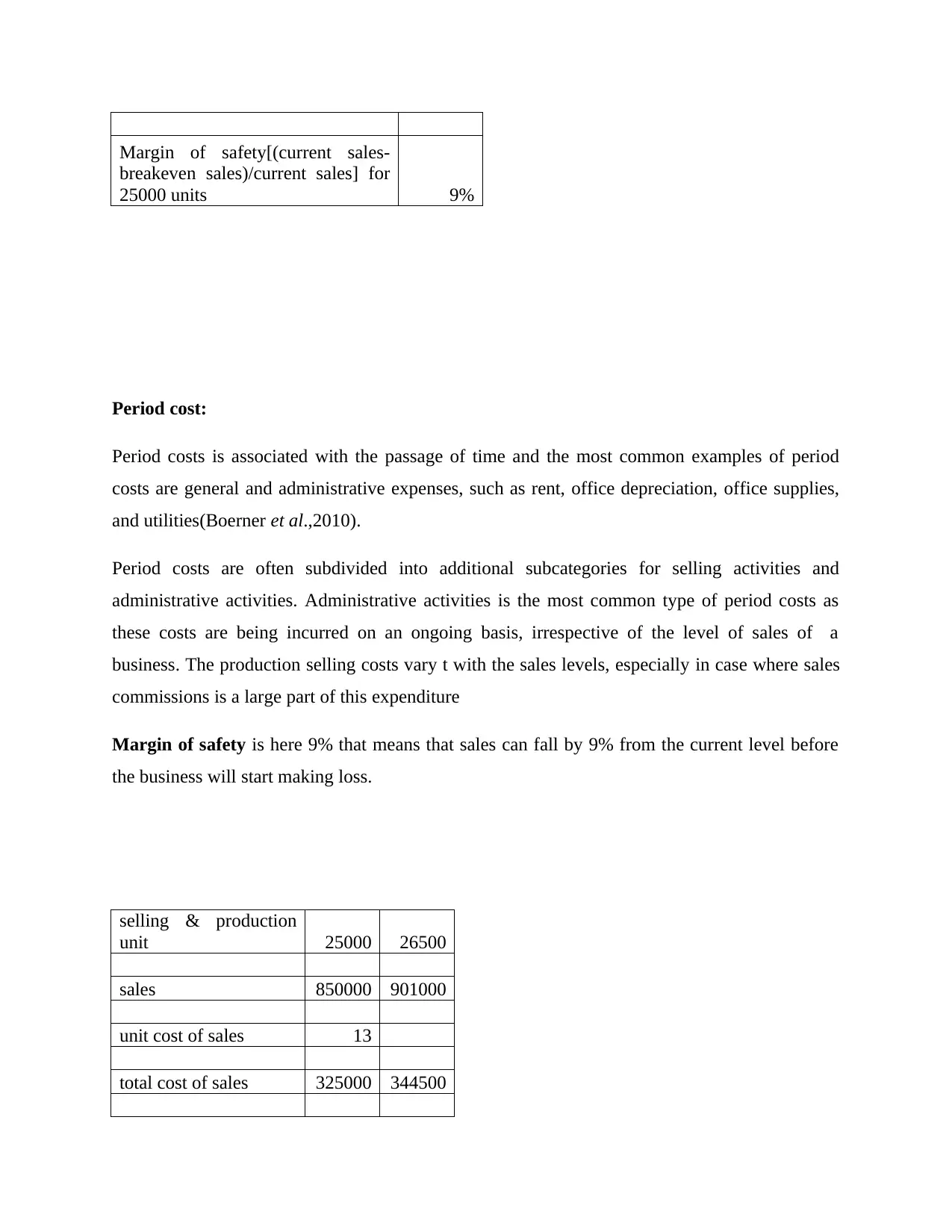

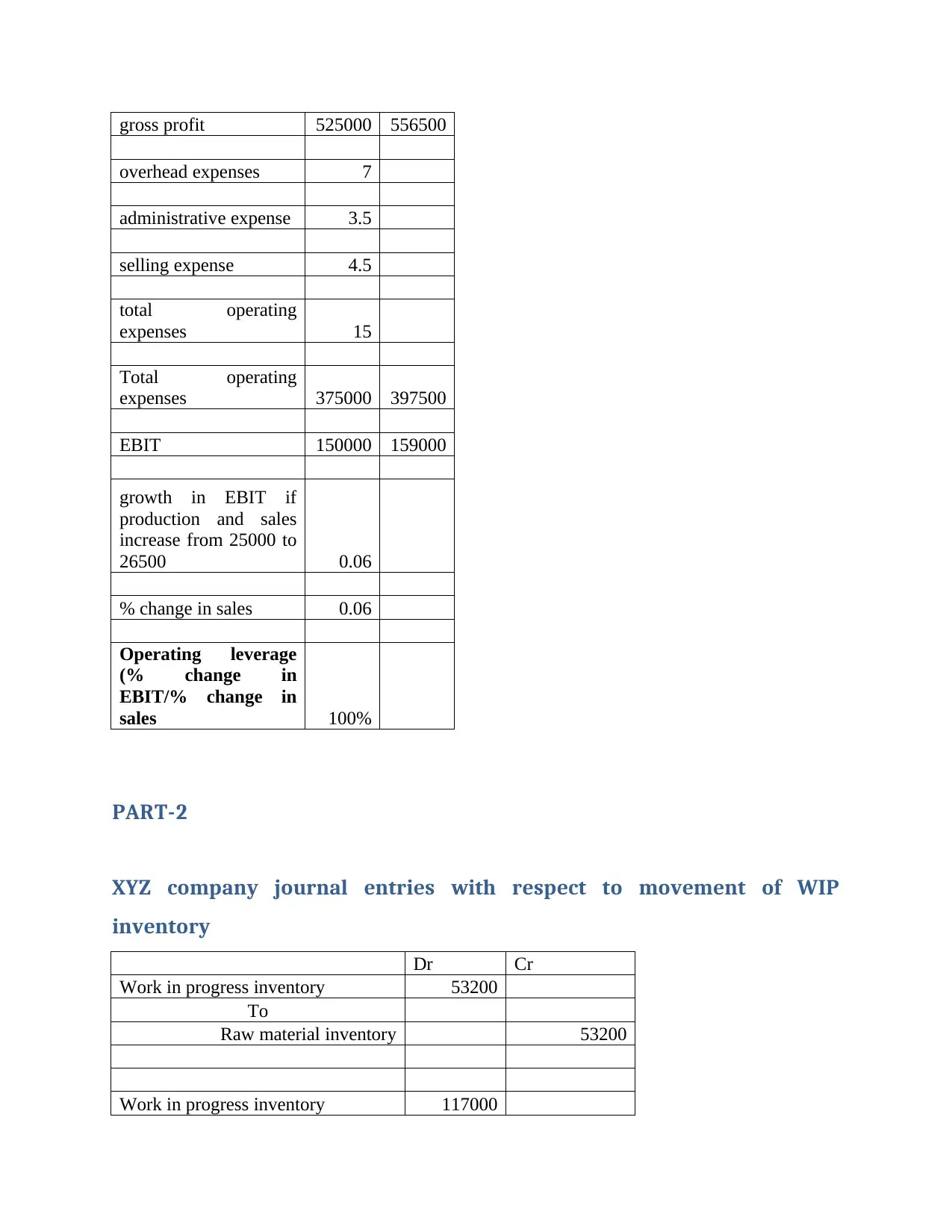

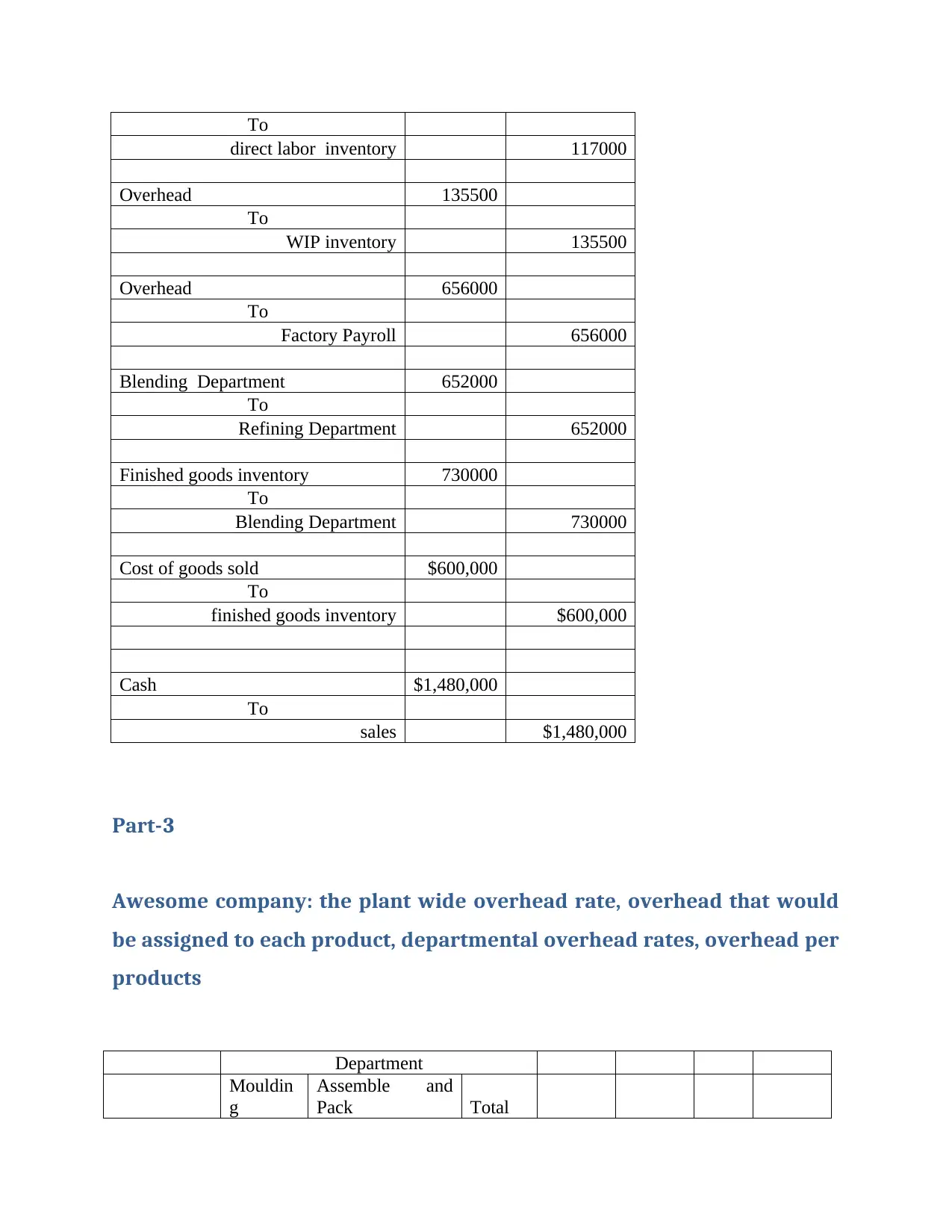

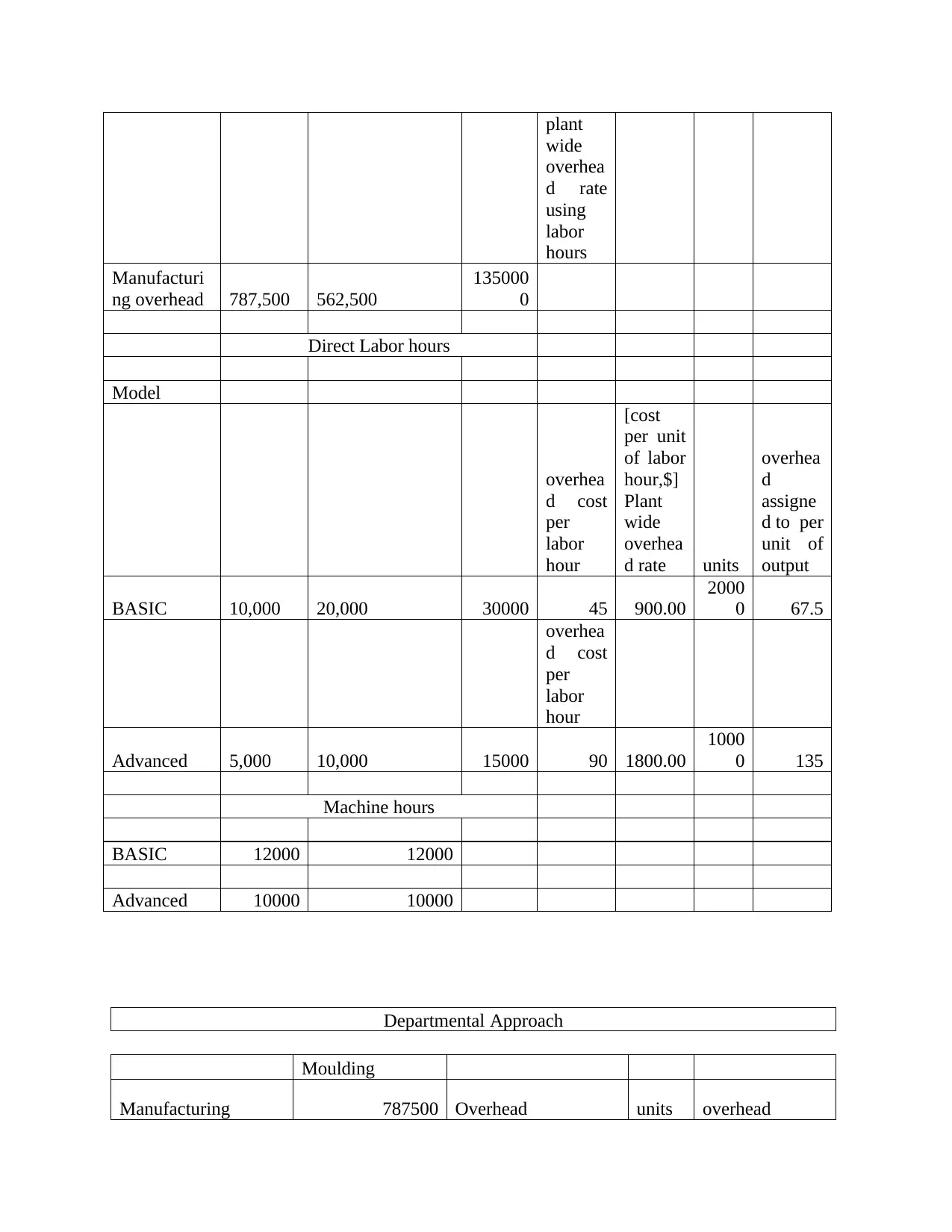

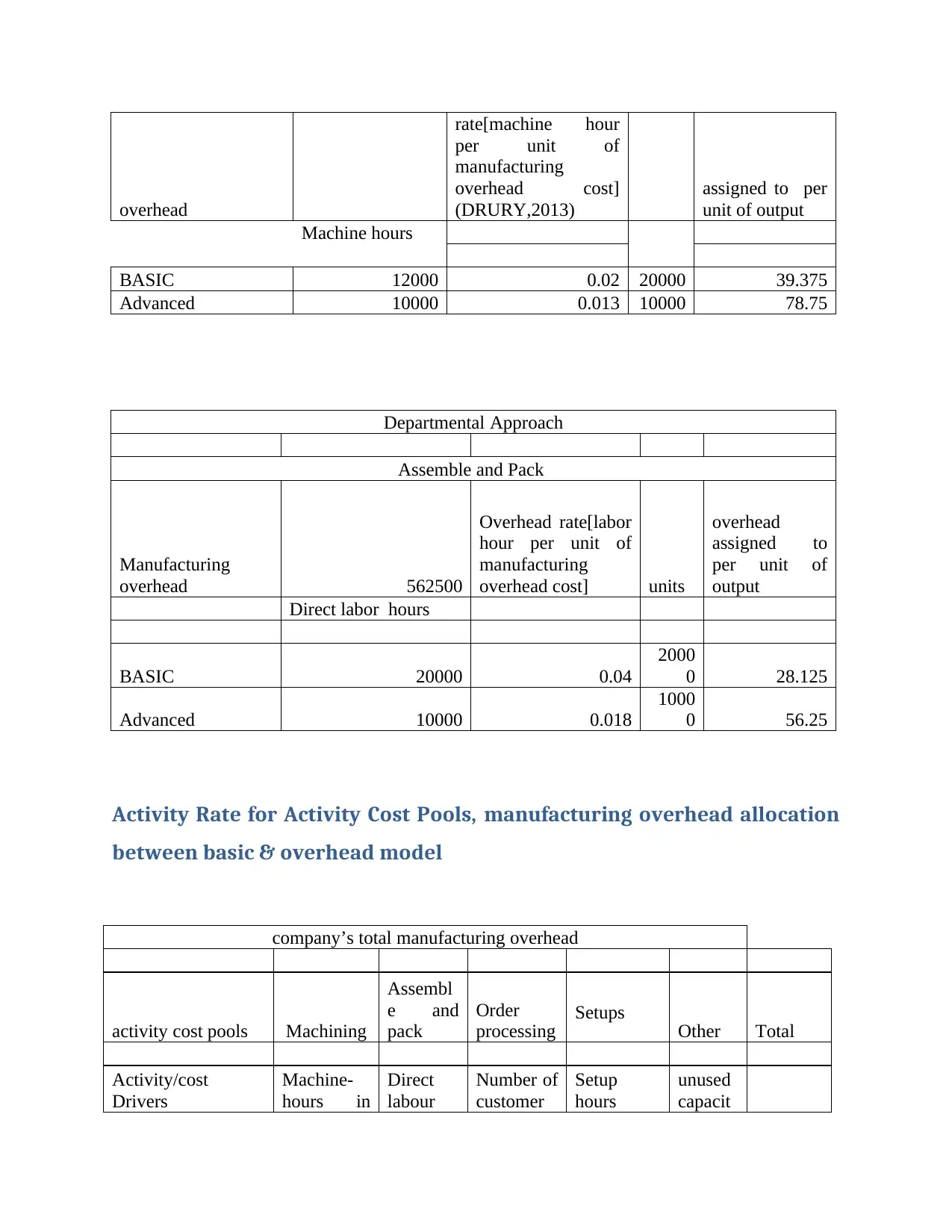

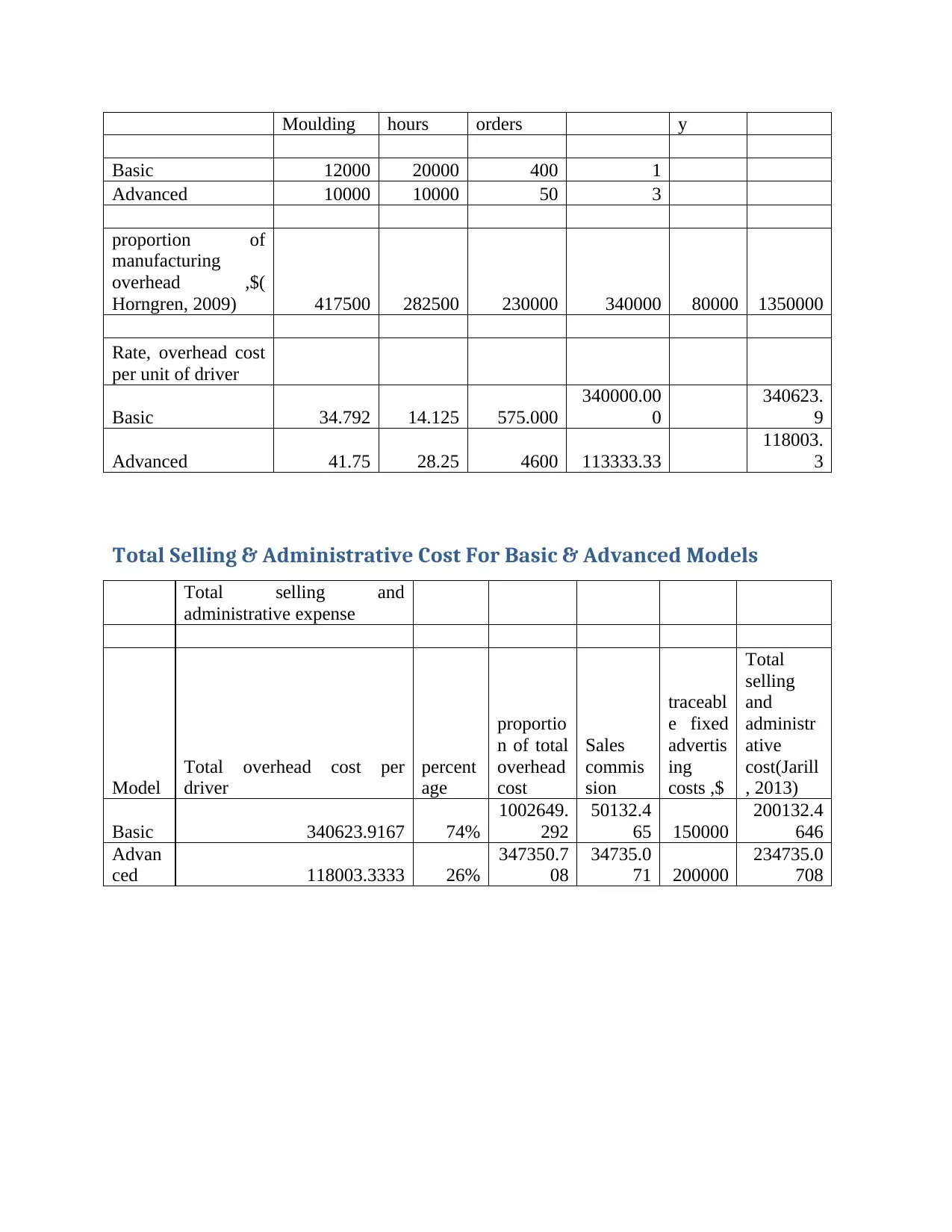

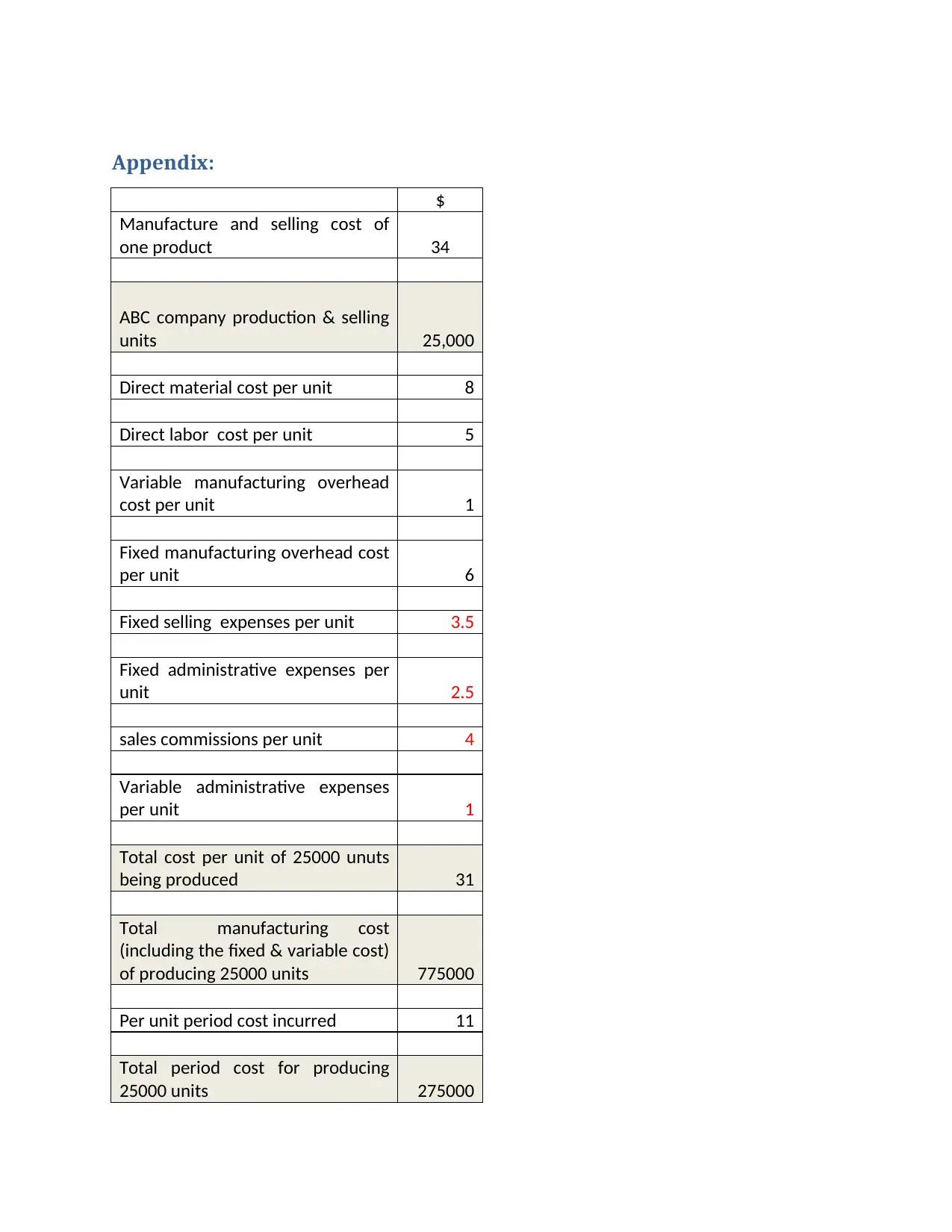

This management accounting report provides a detailed analysis of various cost accounting concepts. Part 1 focuses on costing calculations, including period costs, break-even analysis, margin of safety, contribution margin, and operating leverage for ABC company. Part 2 presents journal entries for XYZ company, specifically addressing the movement of Work in Progress (WIP) inventory. Part 3 delves into overhead analysis for Awesome Company, examining plant-wide and departmental overhead rates, and activity-based costing. The report includes calculations of overhead allocation, selling and administrative costs for basic and advanced models. The report also includes references and an appendix with additional data such as manufacturing and selling costs, and sales data for the models.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.