ACC200: Evaluating Costing Methods for Sewing Easy Ltd (Term 1 2018)

VerifiedAdded on 2023/06/12

|9

|1875

|367

Report

AI Summary

This report provides a comprehensive analysis of Sewing Easy Ltd's costing systems, comparing traditional costing methods with activity-based costing (ABC). It calculates the cost per unit for both Basic and Advance models under each system, analyzes the profitability of the Advance model, and explains the differences in overhead application. The report also discusses the benefits and limitations of ABC costing, offering insights into why an overseas buyer might prefer the Advance model. The analysis aims to assist Sewing Easy Ltd in understanding its costing structure and making informed business decisions. Desklib provides similar solved assignments and past papers for students.

Running head: MANAGEMENT ACCOUNTING

Management accounting

Name of the student

Name of the university

Student ID

Author note

Management accounting

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2MANAGEMENT ACCOUNTING

Table of Contents

Answer 1....................................................................................................................................3

Answer 2....................................................................................................................................3

Answer 3....................................................................................................................................4

Answer 4....................................................................................................................................5

Answer 5....................................................................................................................................6

Reference....................................................................................................................................9

Table of Contents

Answer 1....................................................................................................................................3

Answer 2....................................................................................................................................3

Answer 3....................................................................................................................................4

Answer 4....................................................................................................................................5

Answer 5....................................................................................................................................6

Reference....................................................................................................................................9

3MANAGEMENT ACCOUNTING

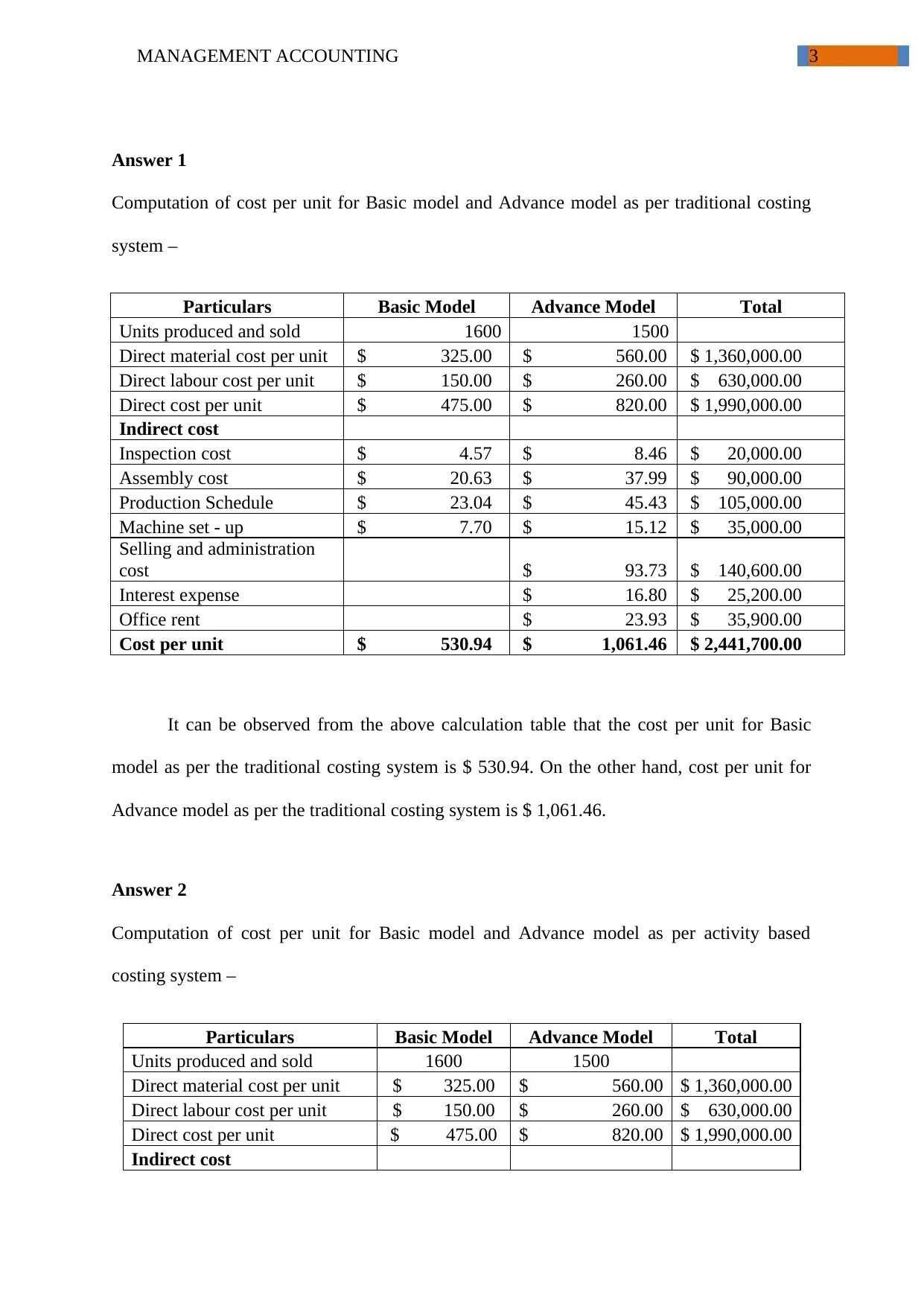

Answer 1

Computation of cost per unit for Basic model and Advance model as per traditional costing

system –

Particulars Basic Model Advance Model Total

Units produced and sold 1600 1500

Direct material cost per unit $ 325.00 $ 560.00 $ 1,360,000.00

Direct labour cost per unit $ 150.00 $ 260.00 $ 630,000.00

Direct cost per unit $ 475.00 $ 820.00 $ 1,990,000.00

Indirect cost

Inspection cost $ 4.57 $ 8.46 $ 20,000.00

Assembly cost $ 20.63 $ 37.99 $ 90,000.00

Production Schedule $ 23.04 $ 45.43 $ 105,000.00

Machine set - up $ 7.70 $ 15.12 $ 35,000.00

Selling and administration

cost $ 93.73 $ 140,600.00

Interest expense $ 16.80 $ 25,200.00

Office rent $ 23.93 $ 35,900.00

Cost per unit $ 530.94 $ 1,061.46 $ 2,441,700.00

It can be observed from the above calculation table that the cost per unit for Basic

model as per the traditional costing system is $ 530.94. On the other hand, cost per unit for

Advance model as per the traditional costing system is $ 1,061.46.

Answer 2

Computation of cost per unit for Basic model and Advance model as per activity based

costing system –

Particulars Basic Model Advance Model Total

Units produced and sold 1600 1500

Direct material cost per unit $ 325.00 $ 560.00 $ 1,360,000.00

Direct labour cost per unit $ 150.00 $ 260.00 $ 630,000.00

Direct cost per unit $ 475.00 $ 820.00 $ 1,990,000.00

Indirect cost

Answer 1

Computation of cost per unit for Basic model and Advance model as per traditional costing

system –

Particulars Basic Model Advance Model Total

Units produced and sold 1600 1500

Direct material cost per unit $ 325.00 $ 560.00 $ 1,360,000.00

Direct labour cost per unit $ 150.00 $ 260.00 $ 630,000.00

Direct cost per unit $ 475.00 $ 820.00 $ 1,990,000.00

Indirect cost

Inspection cost $ 4.57 $ 8.46 $ 20,000.00

Assembly cost $ 20.63 $ 37.99 $ 90,000.00

Production Schedule $ 23.04 $ 45.43 $ 105,000.00

Machine set - up $ 7.70 $ 15.12 $ 35,000.00

Selling and administration

cost $ 93.73 $ 140,600.00

Interest expense $ 16.80 $ 25,200.00

Office rent $ 23.93 $ 35,900.00

Cost per unit $ 530.94 $ 1,061.46 $ 2,441,700.00

It can be observed from the above calculation table that the cost per unit for Basic

model as per the traditional costing system is $ 530.94. On the other hand, cost per unit for

Advance model as per the traditional costing system is $ 1,061.46.

Answer 2

Computation of cost per unit for Basic model and Advance model as per activity based

costing system –

Particulars Basic Model Advance Model Total

Units produced and sold 1600 1500

Direct material cost per unit $ 325.00 $ 560.00 $ 1,360,000.00

Direct labour cost per unit $ 150.00 $ 260.00 $ 630,000.00

Direct cost per unit $ 475.00 $ 820.00 $ 1,990,000.00

Indirect cost

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4MANAGEMENT ACCOUNTING

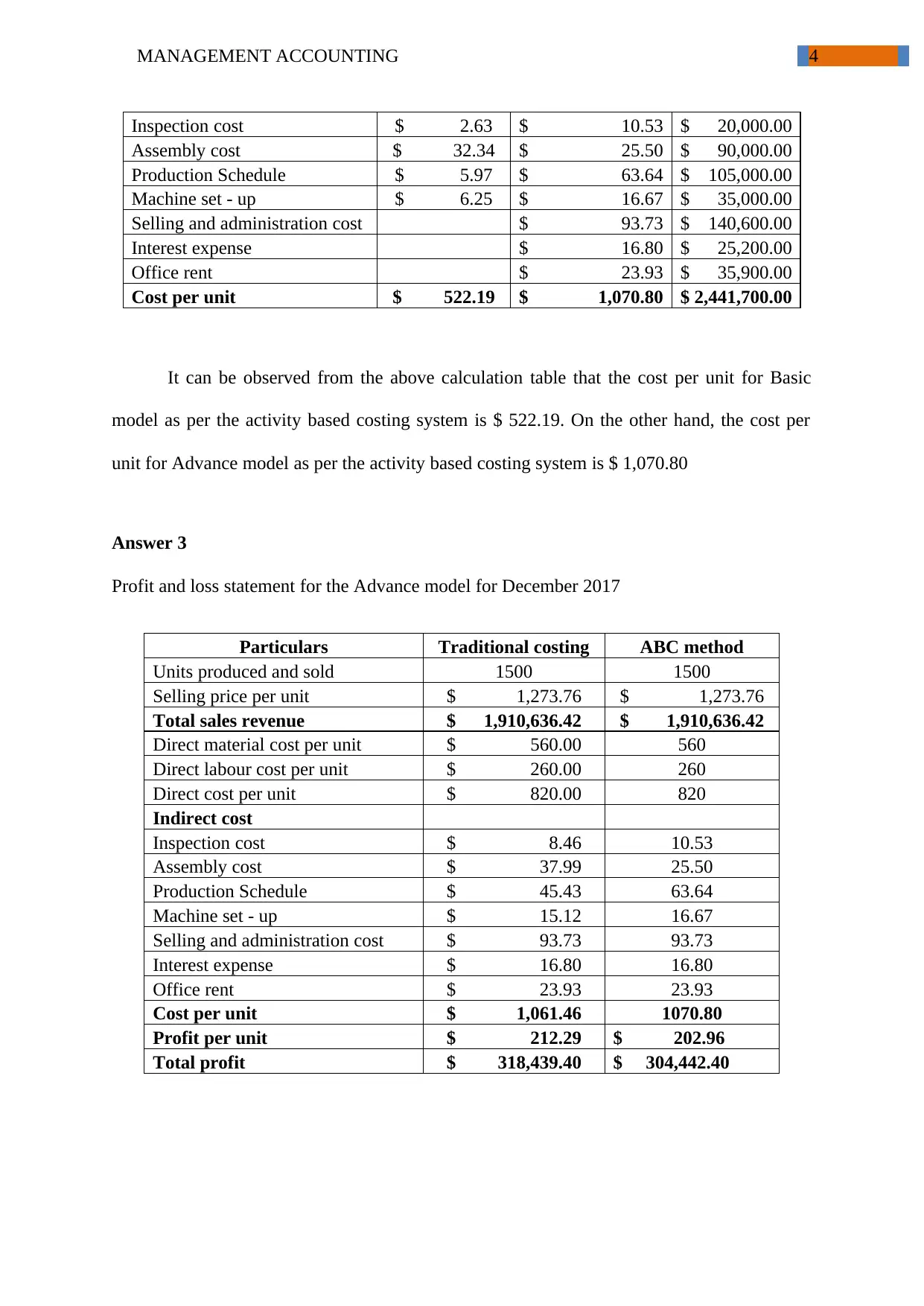

Inspection cost $ 2.63 $ 10.53 $ 20,000.00

Assembly cost $ 32.34 $ 25.50 $ 90,000.00

Production Schedule $ 5.97 $ 63.64 $ 105,000.00

Machine set - up $ 6.25 $ 16.67 $ 35,000.00

Selling and administration cost $ 93.73 $ 140,600.00

Interest expense $ 16.80 $ 25,200.00

Office rent $ 23.93 $ 35,900.00

Cost per unit $ 522.19 $ 1,070.80 $ 2,441,700.00

It can be observed from the above calculation table that the cost per unit for Basic

model as per the activity based costing system is $ 522.19. On the other hand, the cost per

unit for Advance model as per the activity based costing system is $ 1,070.80

Answer 3

Profit and loss statement for the Advance model for December 2017

Particulars Traditional costing ABC method

Units produced and sold 1500 1500

Selling price per unit $ 1,273.76 $ 1,273.76

Total sales revenue $ 1,910,636.42 $ 1,910,636.42

Direct material cost per unit $ 560.00 560

Direct labour cost per unit $ 260.00 260

Direct cost per unit $ 820.00 820

Indirect cost

Inspection cost $ 8.46 10.53

Assembly cost $ 37.99 25.50

Production Schedule $ 45.43 63.64

Machine set - up $ 15.12 16.67

Selling and administration cost $ 93.73 93.73

Interest expense $ 16.80 16.80

Office rent $ 23.93 23.93

Cost per unit $ 1,061.46 1070.80

Profit per unit $ 212.29 $ 202.96

Total profit $ 318,439.40 $ 304,442.40

Inspection cost $ 2.63 $ 10.53 $ 20,000.00

Assembly cost $ 32.34 $ 25.50 $ 90,000.00

Production Schedule $ 5.97 $ 63.64 $ 105,000.00

Machine set - up $ 6.25 $ 16.67 $ 35,000.00

Selling and administration cost $ 93.73 $ 140,600.00

Interest expense $ 16.80 $ 25,200.00

Office rent $ 23.93 $ 35,900.00

Cost per unit $ 522.19 $ 1,070.80 $ 2,441,700.00

It can be observed from the above calculation table that the cost per unit for Basic

model as per the activity based costing system is $ 522.19. On the other hand, the cost per

unit for Advance model as per the activity based costing system is $ 1,070.80

Answer 3

Profit and loss statement for the Advance model for December 2017

Particulars Traditional costing ABC method

Units produced and sold 1500 1500

Selling price per unit $ 1,273.76 $ 1,273.76

Total sales revenue $ 1,910,636.42 $ 1,910,636.42

Direct material cost per unit $ 560.00 560

Direct labour cost per unit $ 260.00 260

Direct cost per unit $ 820.00 820

Indirect cost

Inspection cost $ 8.46 10.53

Assembly cost $ 37.99 25.50

Production Schedule $ 45.43 63.64

Machine set - up $ 15.12 16.67

Selling and administration cost $ 93.73 93.73

Interest expense $ 16.80 16.80

Office rent $ 23.93 23.93

Cost per unit $ 1,061.46 1070.80

Profit per unit $ 212.29 $ 202.96

Total profit $ 318,439.40 $ 304,442.40

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5MANAGEMENT ACCOUNTING

The selling price of advance model as per the traditional costing system is $ 1061.46

and as per the activity based costing system is $ 1070.80. However, the selling price for the

advance model under both the system of costing is 20% above the cost as per traditional

system that is $ 1,273.76 per unit. Therefore, the resultant profit for the month of December

for Advance model under traditional costing system is $ 318,439.40 and under activity based

costing system is $ 304,442.40.

The overseas buyer is interested to purchase the Advance model only due to various

reasons. Generally the ABC costing system is more appropriate basis of allocating overheads

as compared to the traditional costing system of allocation. It can be seen from the above

calculation that the cost per unit for Basic model as per the traditional method is $ 530.94

whereas the same under ABC system is $ 522.19. Therefore, using the traditional system the

company is showing the higher cost per unit as compared to ABC. Therefore, if the company

add profit percentage on cost the cost of the product will be higher than actual as the

company is using traditional system (Dale and Plunkett 2017). On the other hand, cost per

unit for Advance model as per the traditional method is $ 1061.46 whereas the same under

ABC system is $ 1070.80. Therefore, using the traditional system the company is showing

the lower cost per unit as compared to ABC. Therefore, if the company add profit percentage

on cost the cost of the product will be lower than actual as the company is using traditional

system. Hence, the buyers will be in profitable position if they buy the Advance model and

will be in a losing position if they buy the Basic model (Dong, Liu and Lin 2014).

Answer 4

From the above calculation it can be seen that the actual overhead using the ABC

system for Basic model is $ 47.19 per unit and for Advance model it is $ 116.33 per unit. On

the other hand, the applied overhead per unit as per the traditional system for Basic model is

The selling price of advance model as per the traditional costing system is $ 1061.46

and as per the activity based costing system is $ 1070.80. However, the selling price for the

advance model under both the system of costing is 20% above the cost as per traditional

system that is $ 1,273.76 per unit. Therefore, the resultant profit for the month of December

for Advance model under traditional costing system is $ 318,439.40 and under activity based

costing system is $ 304,442.40.

The overseas buyer is interested to purchase the Advance model only due to various

reasons. Generally the ABC costing system is more appropriate basis of allocating overheads

as compared to the traditional costing system of allocation. It can be seen from the above

calculation that the cost per unit for Basic model as per the traditional method is $ 530.94

whereas the same under ABC system is $ 522.19. Therefore, using the traditional system the

company is showing the higher cost per unit as compared to ABC. Therefore, if the company

add profit percentage on cost the cost of the product will be higher than actual as the

company is using traditional system (Dale and Plunkett 2017). On the other hand, cost per

unit for Advance model as per the traditional method is $ 1061.46 whereas the same under

ABC system is $ 1070.80. Therefore, using the traditional system the company is showing

the lower cost per unit as compared to ABC. Therefore, if the company add profit percentage

on cost the cost of the product will be lower than actual as the company is using traditional

system. Hence, the buyers will be in profitable position if they buy the Advance model and

will be in a losing position if they buy the Basic model (Dong, Liu and Lin 2014).

Answer 4

From the above calculation it can be seen that the actual overhead using the ABC

system for Basic model is $ 47.19 per unit and for Advance model it is $ 116.33 per unit. On

the other hand, the applied overhead per unit as per the traditional system for Basic model is

6MANAGEMENT ACCOUNTING

$ 55.94 per unit and for Advance model it is $ 107.00 per unit. Therefore, the applied

overhead differs from the actual overhead due to changes in the method.

Dealing with over / under applied overhead cost

As per the given scenario over applied overhead cost per unit for basic model is ($

55.94 - $ 47.19) = $ 8.75 per unit. On the other hand, the under applied overhead cost per unit

for Advance model is ($ 116.33 - $ 107.00) = $ 9.33. Over application or under application of

overhead cost can be dealt in the following ways –

1. Adjustment in the cost of sales – the under absorbed or over absorbed overhead is

closed and thereafter it is transferred to the account of cost of sales. This is performed

by cost accountant at closing of each month or at the close of each accounting period.

However, if transfer is made at closing of accounting period the amount of under

absorption or over absorption is carried forward to the next period and it is treated as

deferred income if it is over applied and as deferred charges if it is under applied

(Lakmal 2014.).

2. Carry forward to the subsequent year – the over absorption or under absorption can

be carried forward to next accounting period. This can be transferred to overhead

reserve account and the overhead reserve account is shown under the balance sheet.

3. Writing off to the costing profit and loss account – if the amount of over absorption

or under absorption is small, it can be written off through transferring it to costing

account of profit and loss. If it is treated in this way, the valuation of the closing

stock will be under stated or over stated (Novak et al. 2017).

Answer 5

Benefits and limitations of ABC system

$ 55.94 per unit and for Advance model it is $ 107.00 per unit. Therefore, the applied

overhead differs from the actual overhead due to changes in the method.

Dealing with over / under applied overhead cost

As per the given scenario over applied overhead cost per unit for basic model is ($

55.94 - $ 47.19) = $ 8.75 per unit. On the other hand, the under applied overhead cost per unit

for Advance model is ($ 116.33 - $ 107.00) = $ 9.33. Over application or under application of

overhead cost can be dealt in the following ways –

1. Adjustment in the cost of sales – the under absorbed or over absorbed overhead is

closed and thereafter it is transferred to the account of cost of sales. This is performed

by cost accountant at closing of each month or at the close of each accounting period.

However, if transfer is made at closing of accounting period the amount of under

absorption or over absorption is carried forward to the next period and it is treated as

deferred income if it is over applied and as deferred charges if it is under applied

(Lakmal 2014.).

2. Carry forward to the subsequent year – the over absorption or under absorption can

be carried forward to next accounting period. This can be transferred to overhead

reserve account and the overhead reserve account is shown under the balance sheet.

3. Writing off to the costing profit and loss account – if the amount of over absorption

or under absorption is small, it can be written off through transferring it to costing

account of profit and loss. If it is treated in this way, the valuation of the closing

stock will be under stated or over stated (Novak et al. 2017).

Answer 5

Benefits and limitations of ABC system

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7MANAGEMENT ACCOUNTING

Various benefits of ABC system are as follows –

Accurate cost of product – ABC helps in determining the cost of the product in

reliable and accurate manner through focussing on the relationship of cause and

impact that takes place while cost is incurred. It identifies the activities that involve

cost and the product to which the cost is incurred (Hilton and Platt 2013).

Details information regarding cost behaviour – it recognizes the cost behaviour nature

and assists in reducing the costs and recognising the activities that does not add any

value to product. With the ABC system, the managers will be able to have control on

various fixed overheads through applying more control on the activities that caused

the fixed overhead. This is possible as the fixed overhead cost will be more clear and

visible (Özkan and Karaibrahimoğlu 2013).

Better decision making – ABC system significantly improves the decision of the

managers as they are able to use more reliable data with regard to the cost of product.

It assists in fixing the selling price of the product as more accurate data can be

available readily.

Various limitations of ABC system are as follows

Complex and expensive – ABC system has various cost drivers and numerous cost

pools. Thus, installation of the system can be more complex and costlier as compared

to the traditional system.

Driver selection – various issues arises while the ABC system is implemented. The

issues involve may be allocation of common cost, cost drivers and variations in the

rates of cost driver (Weygandt, Kimmel and Kieso 2015).

Difficulties in measurements – another major difficulty associated with the ABC

system is the requirement measurement for implementing the ABC system. It requires

Various benefits of ABC system are as follows –

Accurate cost of product – ABC helps in determining the cost of the product in

reliable and accurate manner through focussing on the relationship of cause and

impact that takes place while cost is incurred. It identifies the activities that involve

cost and the product to which the cost is incurred (Hilton and Platt 2013).

Details information regarding cost behaviour – it recognizes the cost behaviour nature

and assists in reducing the costs and recognising the activities that does not add any

value to product. With the ABC system, the managers will be able to have control on

various fixed overheads through applying more control on the activities that caused

the fixed overhead. This is possible as the fixed overhead cost will be more clear and

visible (Özkan and Karaibrahimoğlu 2013).

Better decision making – ABC system significantly improves the decision of the

managers as they are able to use more reliable data with regard to the cost of product.

It assists in fixing the selling price of the product as more accurate data can be

available readily.

Various limitations of ABC system are as follows

Complex and expensive – ABC system has various cost drivers and numerous cost

pools. Thus, installation of the system can be more complex and costlier as compared

to the traditional system.

Driver selection – various issues arises while the ABC system is implemented. The

issues involve may be allocation of common cost, cost drivers and variations in the

rates of cost driver (Weygandt, Kimmel and Kieso 2015).

Difficulties in measurements – another major difficulty associated with the ABC

system is the requirement measurement for implementing the ABC system. It requires

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8MANAGEMENT ACCOUNTING

the management to project the costs for activity pool and recognise and measure the

cost drivers for serving the method of cost allocation. Further, even the basic systems

of ABC need various calculations for determining the cost of the services and

products (Drury, 2013).

Therefore, irrespective of various limitations ABC can produce more accurate result if

is used in proper way and the people who are using the system are trained properly.

the management to project the costs for activity pool and recognise and measure the

cost drivers for serving the method of cost allocation. Further, even the basic systems

of ABC need various calculations for determining the cost of the services and

products (Drury, 2013).

Therefore, irrespective of various limitations ABC can produce more accurate result if

is used in proper way and the people who are using the system are trained properly.

9MANAGEMENT ACCOUNTING

Reference

Dale, B.G. and Plunkett, J.J., 2017. Quality costing. Routledge.

Dong, J., Liu, C. and Lin, Z., 2014. Charging infrastructure planning for promoting battery

electric vehicles: An activity-based approach using multiday travel data. Transportation

Research Part C: Emerging Technologies, 38, pp.44-55.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Hilton, R.W. and Platt, D.E., 2013. Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Lakmal, D., 2014. Cost Analysis for Decision Making and Control: Marginal Costing versus

Absorption Costing.

Novak, R., Fong, M.H., Zhang, H. and Vrzic, S., Apple Inc, 2017. Methods and systems for

resource allocation. U.S. Patent 9,614,650.

Özkan, S. and Karaibrahimoğlu, Y.Z., 2013. Activity-based costing approach in the

measurement of cost of quality in SMEs: a case study. Total Quality Management & Business

Excellence, 24(3-4), pp.420-431.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & managerial accounting.

John Wiley & Sons.

Reference

Dale, B.G. and Plunkett, J.J., 2017. Quality costing. Routledge.

Dong, J., Liu, C. and Lin, Z., 2014. Charging infrastructure planning for promoting battery

electric vehicles: An activity-based approach using multiday travel data. Transportation

Research Part C: Emerging Technologies, 38, pp.44-55.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Hilton, R.W. and Platt, D.E., 2013. Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Lakmal, D., 2014. Cost Analysis for Decision Making and Control: Marginal Costing versus

Absorption Costing.

Novak, R., Fong, M.H., Zhang, H. and Vrzic, S., Apple Inc, 2017. Methods and systems for

resource allocation. U.S. Patent 9,614,650.

Özkan, S. and Karaibrahimoğlu, Y.Z., 2013. Activity-based costing approach in the

measurement of cost of quality in SMEs: a case study. Total Quality Management & Business

Excellence, 24(3-4), pp.420-431.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & managerial accounting.

John Wiley & Sons.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.