Management Accounting Report: Sollatek Ltd. Fiscal Analysis

VerifiedAdded on 2023/06/18

|17

|5235

|135

Report

AI Summary

This report provides an analysis of management accounting technologies and their application within Sollatek Ltd., a UK-based manufacturer of electromagnetic and digital equipment. It examines various management accounting techniques, including cost optimization, asset administration, cost accounting, and job pricing, highlighting their importance in maintaining fiscal competitiveness. The report also discusses the necessity of management accounting reporting, detailing different types of statements such as performance reports, accounts receivables documents, job cost documents, and stock administration statements. Furthermore, it explores the advantages and disadvantages of different accounting systems and forecasting methods, emphasizing their role in addressing fiscal challenges and supporting strategic decision-making within the organization. The analysis includes a discussion of cost estimation methods and the involvement of managerial accounting in the fiscal analysis phase, concluding with an assessment of planning strategies for dealing with fiscal concerns.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

P1: The various sorts of managerial accountancy technologies and their criteria.................1

P2: The necessity of managing accountancy reporting and the many sorts of managing

accountancy statements..........................................................................................................4

M1: Managerial accountancy solutions' advantages and applications...................................5

D1: Analyze the pros and cons of alternative compliance with accountancy systems..........6

P3: Cost estimation utilizing the most relevant methods.......................................................6

M2: Accountancy procedures come in a variety of shapes and sizes.....................................8

D2: Evaluation of the information..........................................................................................9

PART 2............................................................................................................................................9

P4: The advantages and disadvantages of employing financial management instruments....9

P4. Various sorts of forecasting methods have benefits and drawbacks................................9

M3: The usage of various organizing technologies, as well as their applicability...............11

P5: In order to address fiscal challenges, we compared ourselves to other organizations...11

M4: Managerial accounting's involvement in fiscal analysis phase.....................................12

D3: Assessment of planning strategies for dealing with fiscal concerns.............................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

P1: The various sorts of managerial accountancy technologies and their criteria.................1

P2: The necessity of managing accountancy reporting and the many sorts of managing

accountancy statements..........................................................................................................4

M1: Managerial accountancy solutions' advantages and applications...................................5

D1: Analyze the pros and cons of alternative compliance with accountancy systems..........6

P3: Cost estimation utilizing the most relevant methods.......................................................6

M2: Accountancy procedures come in a variety of shapes and sizes.....................................8

D2: Evaluation of the information..........................................................................................9

PART 2............................................................................................................................................9

P4: The advantages and disadvantages of employing financial management instruments....9

P4. Various sorts of forecasting methods have benefits and drawbacks................................9

M3: The usage of various organizing technologies, as well as their applicability...............11

P5: In order to address fiscal challenges, we compared ourselves to other organizations...11

M4: Managerial accounting's involvement in fiscal analysis phase.....................................12

D3: Assessment of planning strategies for dealing with fiscal concerns.............................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Managerial accountancy is the method of creating yearly fiscal statements to assist a

company in preserving its fiscal competitiveness in the global marketplace (Altukhov, Predeus

and Predeus, 2019). Profit and loss a/c, Balance sheet, Cash Flow report, and other fiscal

instruments fall into this category. It is advantageous to investors who assist a company in

conducting company's activities in a comprehensive and timely way. Accountancy executives

have the responsibility of converting fiscal information into meaningful knowledge so that they

may make efficient judgments and lucrative strategies for the company. It strengthens the brand

visibility amongst competitors in a more effective manner. For the task of introducing this study,

Sollatak Ltd., a corporation that manufactures and sells electromagnetic and digital gear to the

citizens of the United Kingdom with the goal of protecting other employees and consumers from

energy outages, was chosen. The study illustrates the distinct accountancy technologies and their

critical importance in a company. In moreover, this study discusses several distinct

methodologies that aid management in the decision-making processes. In addition, this study

covers various methods of pricing that are employed in the computation of net viability. Aside

from that, this study primarily discusses organizational techniques for budgetary management

and finance instruments for resolving fiscal concerns.

PART 1

P1: The various sorts of managerial accountancy technologies and their criteria

MA's criteria include:

Institute of Management Accountants (IMA): The Institute of Management Accountants

(IMA) is a vocation that entails a variety of positions and obligations, including decision-

making, developing programs and strategies, and preparing financial statements, among others,

to help an institution accomplish pre-determined aims and outcomes within a provided time

frame.

Institute of Certified Management Accountants (CMA): The Association of Certified

Management Accountants (CMA) is a professional association of professional accounting

professionals. Managerial accountancy necessitates managing accountancy training and expertise

abilities in order to generate accountancy information that assist managers in formulating

Managerial accountancy is the method of creating yearly fiscal statements to assist a

company in preserving its fiscal competitiveness in the global marketplace (Altukhov, Predeus

and Predeus, 2019). Profit and loss a/c, Balance sheet, Cash Flow report, and other fiscal

instruments fall into this category. It is advantageous to investors who assist a company in

conducting company's activities in a comprehensive and timely way. Accountancy executives

have the responsibility of converting fiscal information into meaningful knowledge so that they

may make efficient judgments and lucrative strategies for the company. It strengthens the brand

visibility amongst competitors in a more effective manner. For the task of introducing this study,

Sollatak Ltd., a corporation that manufactures and sells electromagnetic and digital gear to the

citizens of the United Kingdom with the goal of protecting other employees and consumers from

energy outages, was chosen. The study illustrates the distinct accountancy technologies and their

critical importance in a company. In moreover, this study discusses several distinct

methodologies that aid management in the decision-making processes. In addition, this study

covers various methods of pricing that are employed in the computation of net viability. Aside

from that, this study primarily discusses organizational techniques for budgetary management

and finance instruments for resolving fiscal concerns.

PART 1

P1: The various sorts of managerial accountancy technologies and their criteria

MA's criteria include:

Institute of Management Accountants (IMA): The Institute of Management Accountants

(IMA) is a vocation that entails a variety of positions and obligations, including decision-

making, developing programs and strategies, and preparing financial statements, among others,

to help an institution accomplish pre-determined aims and outcomes within a provided time

frame.

Institute of Certified Management Accountants (CMA): The Association of Certified

Management Accountants (CMA) is a professional association of professional accounting

professionals. Managerial accountancy necessitates managing accountancy training and expertise

abilities in order to generate accountancy information that assist managers in formulating

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

lucrative decisions and appropriate regulations for the development of a company (Amidu, Effah

and Abor, 2011).

Meaning: Managerial accountancy allows a company to compete with its competitors by

preserving its fiscal place in the industry. It could be achieved by utilizing yearly fiscal records

such as profit and loss accounts, balance sheets, and cash flow statements.

As a result, managerial accountancy is critical to a firm's productivity and expansion.

Developing fiscal reporting, adopting resources effectively and efficiently, selecting the

appropriate pricing approach, producing a budgets, and using planned instruments to oversee are

just a few of the responsibilities that an accountants supervisor is expected to undertake. Sollatek

Ltd. is a manufacturer of electromagnetic technology that helps businesses and consumers use

less power and save even more money. As a result, in order to extend its company activities on a

big extent, its administration must hold a consistent fiscal circumstances. It could be

accomplished by incorporating various accountancy methods, such as a pricing efficiency

platform, a costing accountancy framework, a task pricing framework, and so on, in addition to

create successful strategies and judgments in terms of achieving an economy's productivity. It

provides a number of benefits to the businesses, which also are listed below:

Increased client commitment: Sollatek Ltd. can detect the perspective of prospective

consumers regarding the pricing imposed on their goods and solutions through utilizing multiple

accountancy methods, such as a pricing management platform. It allows managers to make

optimal marketing strategies that enhance customer happiness (Arroyo, 2012).

Productivity evaluation: Managerial accountancy assists divisions in improving their

entire results by evaluating real and planned performances. It makes the greatest contribution to

accomplishing a firm's targeted aims and ambitions. For instance, employing a price accountancy

platform to create a budgeting allows you to allocate costs to multiple divisions based on their

wants and objectives.

Effective management control: Sollatek Ltd. is competent to lower corporate costs and

operations with the help of the managing accountancy process to develop efficient programs and

strategies after evaluating the valuable information received from the managing accountancy

platform.

Various accountancy techniques for administration:

and Abor, 2011).

Meaning: Managerial accountancy allows a company to compete with its competitors by

preserving its fiscal place in the industry. It could be achieved by utilizing yearly fiscal records

such as profit and loss accounts, balance sheets, and cash flow statements.

As a result, managerial accountancy is critical to a firm's productivity and expansion.

Developing fiscal reporting, adopting resources effectively and efficiently, selecting the

appropriate pricing approach, producing a budgets, and using planned instruments to oversee are

just a few of the responsibilities that an accountants supervisor is expected to undertake. Sollatek

Ltd. is a manufacturer of electromagnetic technology that helps businesses and consumers use

less power and save even more money. As a result, in order to extend its company activities on a

big extent, its administration must hold a consistent fiscal circumstances. It could be

accomplished by incorporating various accountancy methods, such as a pricing efficiency

platform, a costing accountancy framework, a task pricing framework, and so on, in addition to

create successful strategies and judgments in terms of achieving an economy's productivity. It

provides a number of benefits to the businesses, which also are listed below:

Increased client commitment: Sollatek Ltd. can detect the perspective of prospective

consumers regarding the pricing imposed on their goods and solutions through utilizing multiple

accountancy methods, such as a pricing management platform. It allows managers to make

optimal marketing strategies that enhance customer happiness (Arroyo, 2012).

Productivity evaluation: Managerial accountancy assists divisions in improving their

entire results by evaluating real and planned performances. It makes the greatest contribution to

accomplishing a firm's targeted aims and ambitions. For instance, employing a price accountancy

platform to create a budgeting allows you to allocate costs to multiple divisions based on their

wants and objectives.

Effective management control: Sollatek Ltd. is competent to lower corporate costs and

operations with the help of the managing accountancy process to develop efficient programs and

strategies after evaluating the valuable information received from the managing accountancy

platform.

Various accountancy techniques for administration:

Price Optimization technique: This accountancy technology enable managers in creating

efficient marketing strategies by understanding potential customers' perceptions as well as how

much customers are inclined to purchase for Sollatek Ltd's offerings. This should increase the

degree of pleasure of prospective customer while also making it easier to gain their commitment.

For example, increasing the cost of electronics appliances on a constant schedule could raise the

likelihood of committed customers defecting to competitors, which is not really a promising

indicator for Sollatek Ltd. As a result, employing such a method aids in determining what level

of price the consumers were pleased with at the date of acquisition (Bedford, Malmi and

Sandelin, 2016).

Asset administration technique: This is yet another excellent accountancy method that

instructs organizations to keep enough products in the organization in order to satisfy

marketplace expectations and demands. Sollatek Ltd. should use such a strategy in order to take

advantage of the circumstances of expanding product growth over the coming years by ensuring

the accessibility of raw resources in their facilities. Improvements in number of power

commodities, for instance, in the nearest term will necessitate the business possesses buffer

supply to fulfill consumption, which could be facilitated by such a network.

Cost accountancy technique: This is an accountancy framework which assists managers

in formulating the overall expense that will be spent in the implementation of various company

operations such as manufacturing or advertising. Since Sollatek Ltd. is a small business with

scarce funds, it is critical for leadership to make the best use of those assets in order to reduce

waste. It is feasible via the use of a price accountancy framework that limits and guides a firm's

expenditures after considering prospective risks and associated efficacy.

Job pricing technique: This is an accountancy method that assists in determining the

total expense of creating a single commodity or a collection of items, allows companies to

construct a performance characteristics. Sollatek Ltd.'s administration must evaluate all of the

actions involved in creating items, as well as the costs associated with them, in attempt to

accomplish beneficial results in the coming years. Batch costing, procedure costing, and

contractual costing are some of the methodologies used in such a framework. Owing to the fact

that Sollatek Ltd. deals with power gear, batching pricing could be a possibility (Borthick and

Pennington, 2017).

efficient marketing strategies by understanding potential customers' perceptions as well as how

much customers are inclined to purchase for Sollatek Ltd's offerings. This should increase the

degree of pleasure of prospective customer while also making it easier to gain their commitment.

For example, increasing the cost of electronics appliances on a constant schedule could raise the

likelihood of committed customers defecting to competitors, which is not really a promising

indicator for Sollatek Ltd. As a result, employing such a method aids in determining what level

of price the consumers were pleased with at the date of acquisition (Bedford, Malmi and

Sandelin, 2016).

Asset administration technique: This is yet another excellent accountancy method that

instructs organizations to keep enough products in the organization in order to satisfy

marketplace expectations and demands. Sollatek Ltd. should use such a strategy in order to take

advantage of the circumstances of expanding product growth over the coming years by ensuring

the accessibility of raw resources in their facilities. Improvements in number of power

commodities, for instance, in the nearest term will necessitate the business possesses buffer

supply to fulfill consumption, which could be facilitated by such a network.

Cost accountancy technique: This is an accountancy framework which assists managers

in formulating the overall expense that will be spent in the implementation of various company

operations such as manufacturing or advertising. Since Sollatek Ltd. is a small business with

scarce funds, it is critical for leadership to make the best use of those assets in order to reduce

waste. It is feasible via the use of a price accountancy framework that limits and guides a firm's

expenditures after considering prospective risks and associated efficacy.

Job pricing technique: This is an accountancy method that assists in determining the

total expense of creating a single commodity or a collection of items, allows companies to

construct a performance characteristics. Sollatek Ltd.'s administration must evaluate all of the

actions involved in creating items, as well as the costs associated with them, in attempt to

accomplish beneficial results in the coming years. Batch costing, procedure costing, and

contractual costing are some of the methodologies used in such a framework. Owing to the fact

that Sollatek Ltd. deals with power gear, batching pricing could be a possibility (Borthick and

Pennington, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P2: The necessity of managing accountancy reporting and the many sorts of managing

accountancy statements

Sollatek Ltd. is a modest firm that manufactures and sells electronic goods to other

organizations and consumers. The administration has constantly attempted to develop the

company's operations, which could be accomplished by keeping weekly, bimonthly, fortnightly,

or annual accountancy statements. Profit and loss a/c, Balance sheet, Cash flow statement, and

other documents reveal the firm's existing and precise fiscal reputation in the industry. This

instructs managers to adopt sound judgments and develop appropriate programs in order to get a

comparative benefit. As a result, it is critical for Sollatek Ltd. to preserve several sorts of records,

like annual reviews, accounts receivables findings, and work expense findings, among others,

that would offer helpful material on which appropriate strategies and regulations may be created.

These studies are also important for presenting such studies to investors in order to obtain

additional fiscal assistance in plan to enlarge the company's operations to new nations. Traders,

lenders, and vendors are examples of these kinds of owners. As a result, Sollatek Ltd. should

produce a variety of documents in ability to remain above of their competitors and stay in the

marketplace for a prolonged amount of duration. The following sections go over comparable

report standards in more detail:

Performance report: A productivity statement is a summary that contains pertinent data

on the functioning of different divisions inside a company. Supervisors within every division

should indeed be expected to keep all documents relevant to their efforts in attaining the intended

goal. Sollatek Ltd.'s administration and leadership tasks a strategy and assigns activities and

duties based on this information. Since each division's participation maximizes a company's core

success, financiers are increasingly drawn to them for investing (Christ, Burritt and Varsei,

2016).

Accounts receivables document: This document is necessary to keep in order for the

organization to retain a healthy fiscal circumstance. This type of data collection informs the

business about a database of borrowers who have not yet reimbursed the business for activities

they conducted with the firm previously. This will instruct administration to approach

individuals in order to retrieve the restoration payment. It also encourages businesses to

reconsider their lending procedures in order to prevent outstanding debt or non-payment by

customers.

accountancy statements

Sollatek Ltd. is a modest firm that manufactures and sells electronic goods to other

organizations and consumers. The administration has constantly attempted to develop the

company's operations, which could be accomplished by keeping weekly, bimonthly, fortnightly,

or annual accountancy statements. Profit and loss a/c, Balance sheet, Cash flow statement, and

other documents reveal the firm's existing and precise fiscal reputation in the industry. This

instructs managers to adopt sound judgments and develop appropriate programs in order to get a

comparative benefit. As a result, it is critical for Sollatek Ltd. to preserve several sorts of records,

like annual reviews, accounts receivables findings, and work expense findings, among others,

that would offer helpful material on which appropriate strategies and regulations may be created.

These studies are also important for presenting such studies to investors in order to obtain

additional fiscal assistance in plan to enlarge the company's operations to new nations. Traders,

lenders, and vendors are examples of these kinds of owners. As a result, Sollatek Ltd. should

produce a variety of documents in ability to remain above of their competitors and stay in the

marketplace for a prolonged amount of duration. The following sections go over comparable

report standards in more detail:

Performance report: A productivity statement is a summary that contains pertinent data

on the functioning of different divisions inside a company. Supervisors within every division

should indeed be expected to keep all documents relevant to their efforts in attaining the intended

goal. Sollatek Ltd.'s administration and leadership tasks a strategy and assigns activities and

duties based on this information. Since each division's participation maximizes a company's core

success, financiers are increasingly drawn to them for investing (Christ, Burritt and Varsei,

2016).

Accounts receivables document: This document is necessary to keep in order for the

organization to retain a healthy fiscal circumstance. This type of data collection informs the

business about a database of borrowers who have not yet reimbursed the business for activities

they conducted with the firm previously. This will instruct administration to approach

individuals in order to retrieve the restoration payment. It also encourages businesses to

reconsider their lending procedures in order to prevent outstanding debt or non-payment by

customers.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job price document: This is a critical accountancy summary that Sollatek Ltd. must keep

track of in order to establish the accrued in manufacturing a specific commodity or collection of

similar products. An institution's administration must determine if the money spent in a specific

commodity would be recovered in the coming years. The major goal of generating such a

document is to determine the costs associated with various work order. It would have a

significant and positive effect on the firm's financial performance.

Stock administration statement: This is an accountancy document that puts the

organization in a condition to satisfy marketplace expectations and demands by keeping enough

stock on hand. Since Sollatek Ltd.'s clientele include employees and consumers, desire for their

electronic goods would be considerable at any moment, necessitating the firm's maintaining an

adequate quantity of inventory. This could be accomplished by gathering knowledge from

certain data so that management could execute an allocation for merchandise at the appropriate

time and location, allowing the manufacturing operation to function more efficiently. The EOQ,

ABC costing methodology, and stock governance methodology are all important techniques for

preparing accounting reports (Cleve, 2017).

M1: Managerial accountancy solutions' advantages and applications

Sollatek Ltd. could gain a number of advantages by implementing various managerial

accountancy solutions. The following are some of the advantages:

Accountancy tools for administration Advantages

Accountancy methods for costs It aids in reducing cost waste by allocating

costs after evaluating the information gained in

the upcoming.

Stock control mechanism It aids Sollatek Ltd. in maintaining an

acceptable inventory levels in addition to fulfil

industry demands.

Mechanism for pricing optimization It assists in increasing the degree of

contentment of focused clientele by

establishing efficient price strategy (Corrigan,

2018).

Mechanism for calculating job costs It aids in calculating the entire price of

track of in order to establish the accrued in manufacturing a specific commodity or collection of

similar products. An institution's administration must determine if the money spent in a specific

commodity would be recovered in the coming years. The major goal of generating such a

document is to determine the costs associated with various work order. It would have a

significant and positive effect on the firm's financial performance.

Stock administration statement: This is an accountancy document that puts the

organization in a condition to satisfy marketplace expectations and demands by keeping enough

stock on hand. Since Sollatek Ltd.'s clientele include employees and consumers, desire for their

electronic goods would be considerable at any moment, necessitating the firm's maintaining an

adequate quantity of inventory. This could be accomplished by gathering knowledge from

certain data so that management could execute an allocation for merchandise at the appropriate

time and location, allowing the manufacturing operation to function more efficiently. The EOQ,

ABC costing methodology, and stock governance methodology are all important techniques for

preparing accounting reports (Cleve, 2017).

M1: Managerial accountancy solutions' advantages and applications

Sollatek Ltd. could gain a number of advantages by implementing various managerial

accountancy solutions. The following are some of the advantages:

Accountancy tools for administration Advantages

Accountancy methods for costs It aids in reducing cost waste by allocating

costs after evaluating the information gained in

the upcoming.

Stock control mechanism It aids Sollatek Ltd. in maintaining an

acceptable inventory levels in addition to fulfil

industry demands.

Mechanism for pricing optimization It assists in increasing the degree of

contentment of focused clientele by

establishing efficient price strategy (Corrigan,

2018).

Mechanism for calculating job costs It aids in calculating the entire price of

manufacturing a single commodity or a

collection of commodities.

D1: Analyze the pros and cons of alternative compliance with accountancy systems

There are indeed a variety of accountancy and monitoring technologies that assist

managers in formulating successful choices and appropriate strategies by providing knowledge

via these platforms and analyses. Accounts payable statements, for instance, offer data about a

list of outstanding borrowers, allowing administration to make adjustments to its reputation rules

in place to evade payments collection issues.

P3: Cost estimation utilizing the most relevant methods

Cost: It relates to the quantity of money spent to create or purchase anything in addition

to make revenue from the sale of those produced goods and solutions. To put it another way,

expense is primarily a value of the money, materials, duration and energy, hazards, and other

factors that must be engaged in the implementation of various commercial operations. These

costs are connected to the materials, personnel, running costs, and other costs involved in the

manufacturing processes. The administration has two ways for determining net efficiency in this

case (Curtis and Taylor, 2018).

Sollatek Ltd. is a production firm, therefore it must estimate the expenses associated with

various commercial operations in addition to reach high revenue and long-term viability. It

instructs administration to reduce waste as much as possible in addition to maximize revenues.

Marginal costing and absorption costing are the two most used pricing approaches. It is further

described in the following sections:

Marginal costing:

It is a technique for calculating net viability that only considers changeable expenses.

Whenever an organization produces one additional item of production in addition to the primary

production, this strategy is beneficial. It typically raises or lowers the overall expense of

manufacturing, depending on the amount of products generated. Marginal cost, sometimes

referred as variable cost, comprises personnel and commodity expenses, as well as a fraction of

the fixed cost that is projected.

Absorption costing:

collection of commodities.

D1: Analyze the pros and cons of alternative compliance with accountancy systems

There are indeed a variety of accountancy and monitoring technologies that assist

managers in formulating successful choices and appropriate strategies by providing knowledge

via these platforms and analyses. Accounts payable statements, for instance, offer data about a

list of outstanding borrowers, allowing administration to make adjustments to its reputation rules

in place to evade payments collection issues.

P3: Cost estimation utilizing the most relevant methods

Cost: It relates to the quantity of money spent to create or purchase anything in addition

to make revenue from the sale of those produced goods and solutions. To put it another way,

expense is primarily a value of the money, materials, duration and energy, hazards, and other

factors that must be engaged in the implementation of various commercial operations. These

costs are connected to the materials, personnel, running costs, and other costs involved in the

manufacturing processes. The administration has two ways for determining net efficiency in this

case (Curtis and Taylor, 2018).

Sollatek Ltd. is a production firm, therefore it must estimate the expenses associated with

various commercial operations in addition to reach high revenue and long-term viability. It

instructs administration to reduce waste as much as possible in addition to maximize revenues.

Marginal costing and absorption costing are the two most used pricing approaches. It is further

described in the following sections:

Marginal costing:

It is a technique for calculating net viability that only considers changeable expenses.

Whenever an organization produces one additional item of production in addition to the primary

production, this strategy is beneficial. It typically raises or lowers the overall expense of

manufacturing, depending on the amount of products generated. Marginal cost, sometimes

referred as variable cost, comprises personnel and commodity expenses, as well as a fraction of

the fixed cost that is projected.

Absorption costing:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

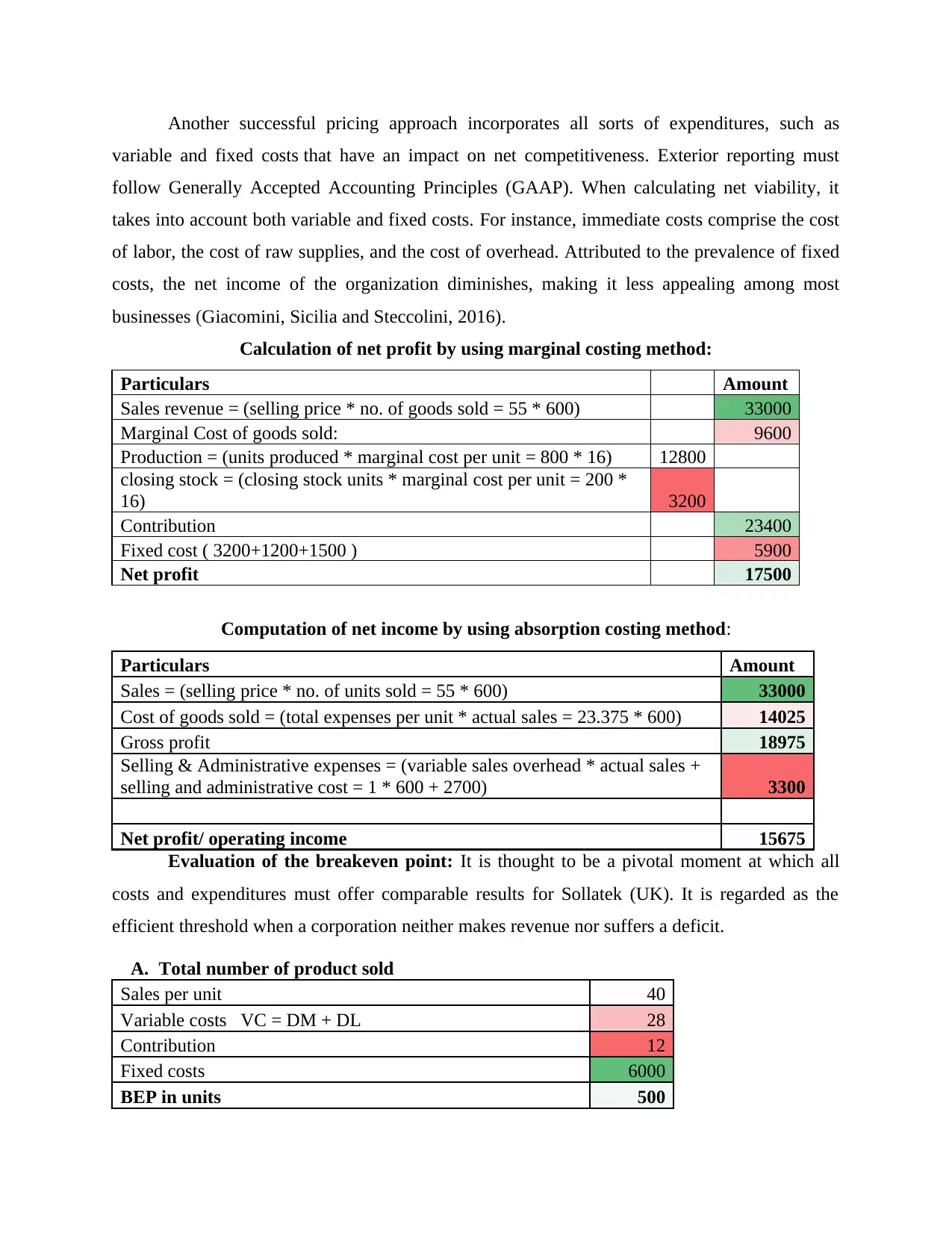

Another successful pricing approach incorporates all sorts of expenditures, such as

variable and fixed costs that have an impact on net competitiveness. Exterior reporting must

follow Generally Accepted Accounting Principles (GAAP). When calculating net viability, it

takes into account both variable and fixed costs. For instance, immediate costs comprise the cost

of labor, the cost of raw supplies, and the cost of overhead. Attributed to the prevalence of fixed

costs, the net income of the organization diminishes, making it less appealing among most

businesses (Giacomini, Sicilia and Steccolini, 2016).

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Evaluation of the breakeven point: It is thought to be a pivotal moment at which all

costs and expenditures must offer comparable results for Sollatek (UK). It is regarded as the

efficient threshold when a corporation neither makes revenue nor suffers a deficit.

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

variable and fixed costs that have an impact on net competitiveness. Exterior reporting must

follow Generally Accepted Accounting Principles (GAAP). When calculating net viability, it

takes into account both variable and fixed costs. For instance, immediate costs comprise the cost

of labor, the cost of raw supplies, and the cost of overhead. Attributed to the prevalence of fixed

costs, the net income of the organization diminishes, making it less appealing among most

businesses (Giacomini, Sicilia and Steccolini, 2016).

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Evaluation of the breakeven point: It is thought to be a pivotal moment at which all

costs and expenditures must offer comparable results for Sollatek (UK). It is regarded as the

efficient threshold when a corporation neither makes revenue nor suffers a deficit.

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

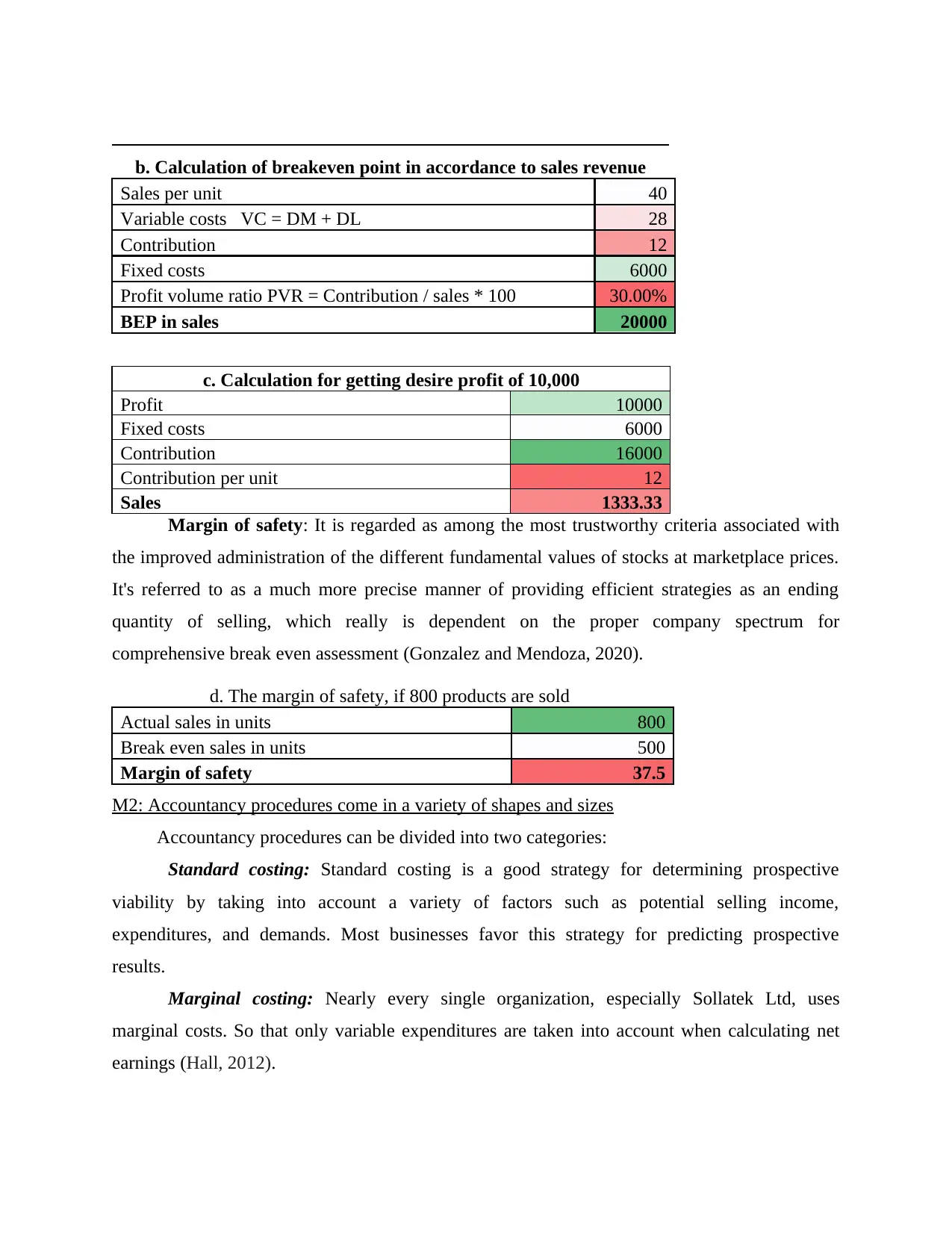

b. Calculation of breakeven point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

c. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety: It is regarded as among the most trustworthy criteria associated with

the improved administration of the different fundamental values of stocks at marketplace prices.

It's referred to as a much more precise manner of providing efficient strategies as an ending

quantity of selling, which really is dependent on the proper company spectrum for

comprehensive break even assessment (Gonzalez and Mendoza, 2020).

d. The margin of safety, if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2: Accountancy procedures come in a variety of shapes and sizes

Accountancy procedures can be divided into two categories:

Standard costing: Standard costing is a good strategy for determining prospective

viability by taking into account a variety of factors such as potential selling income,

expenditures, and demands. Most businesses favor this strategy for predicting prospective

results.

Marginal costing: Nearly every single organization, especially Sollatek Ltd, uses

marginal costs. So that only variable expenditures are taken into account when calculating net

earnings (Hall, 2012).

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

c. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety: It is regarded as among the most trustworthy criteria associated with

the improved administration of the different fundamental values of stocks at marketplace prices.

It's referred to as a much more precise manner of providing efficient strategies as an ending

quantity of selling, which really is dependent on the proper company spectrum for

comprehensive break even assessment (Gonzalez and Mendoza, 2020).

d. The margin of safety, if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2: Accountancy procedures come in a variety of shapes and sizes

Accountancy procedures can be divided into two categories:

Standard costing: Standard costing is a good strategy for determining prospective

viability by taking into account a variety of factors such as potential selling income,

expenditures, and demands. Most businesses favor this strategy for predicting prospective

results.

Marginal costing: Nearly every single organization, especially Sollatek Ltd, uses

marginal costs. So that only variable expenditures are taken into account when calculating net

earnings (Hall, 2012).

D2: Evaluation of the information

In addition to estimate net viability, two techniques are used, as shown in the above

computation. The profit is 17500 when utilizing the marginal pricing approach, whereas it is

15675 when utilizing the marginal pricing technique. The 9600 discrepancy is due to changes in

variable costs. The entire quantity of items produced in Breakeven is 500, and the total quantity

of sales income required to break even is $20,000. Sollatek Ltd. needs sales revenue of 1333.33

to make a profit of at least 1000. Whenever 800 goods are sold, the safety margins are 37.5.

PART 2

P4: The advantages and disadvantages of employing financial management instruments

Budgeting control: Various divisions put up their best attempts to accomplish the

intended aims and targets. They required finances to perform their tasks, therefore the

administration created a budgeted based on the demands and objectives of every sector. It is

critical to keep track of expenditures incurred in the implementation of various corporate tasks,

and administration is obligated to use various budgeting techniques to do so (Roberts and Gnan,

2017).

P4. Various sorts of forecasting methods have benefits and drawbacks

Budgeting control: This is a strategy for effectively regulating costs that comprises

integrating departments, preparing budgeting, assigning duties, and evaluating the current

performances with an acceptable quantity of funding in order to achieve greater productivity and

efficiency. The main goal of this instrument is to decrease or eradicate the company's

inefficiency and boost revenue. The financial management method involves a number of

components, which have been listed below:

Communicate with the executive: As a first stage, the supervisory or managers of

different departments must meet and discuss the corporate activities that will help the company

or its numerous businesses in the big scheme of things.

Assertions: After gathering all facts and input from multiple divisions, the management

of Sollatek Ltd. requires to convene for the goal of addressing the actions that are beneficial for

the company in terms of offering long-term disadvantages and rewards. Make concerns for

upcoming commercial activities if you want to get effective findings.

In addition to estimate net viability, two techniques are used, as shown in the above

computation. The profit is 17500 when utilizing the marginal pricing approach, whereas it is

15675 when utilizing the marginal pricing technique. The 9600 discrepancy is due to changes in

variable costs. The entire quantity of items produced in Breakeven is 500, and the total quantity

of sales income required to break even is $20,000. Sollatek Ltd. needs sales revenue of 1333.33

to make a profit of at least 1000. Whenever 800 goods are sold, the safety margins are 37.5.

PART 2

P4: The advantages and disadvantages of employing financial management instruments

Budgeting control: Various divisions put up their best attempts to accomplish the

intended aims and targets. They required finances to perform their tasks, therefore the

administration created a budgeted based on the demands and objectives of every sector. It is

critical to keep track of expenditures incurred in the implementation of various corporate tasks,

and administration is obligated to use various budgeting techniques to do so (Roberts and Gnan,

2017).

P4. Various sorts of forecasting methods have benefits and drawbacks

Budgeting control: This is a strategy for effectively regulating costs that comprises

integrating departments, preparing budgeting, assigning duties, and evaluating the current

performances with an acceptable quantity of funding in order to achieve greater productivity and

efficiency. The main goal of this instrument is to decrease or eradicate the company's

inefficiency and boost revenue. The financial management method involves a number of

components, which have been listed below:

Communicate with the executive: As a first stage, the supervisory or managers of

different departments must meet and discuss the corporate activities that will help the company

or its numerous businesses in the big scheme of things.

Assertions: After gathering all facts and input from multiple divisions, the management

of Sollatek Ltd. requires to convene for the goal of addressing the actions that are beneficial for

the company in terms of offering long-term disadvantages and rewards. Make concerns for

upcoming commercial activities if you want to get effective findings.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.