Management Accounting Report: Osbarr Web Group Financial Analysis

VerifiedAdded on 2022/12/26

|11

|2227

|47

Report

AI Summary

This report delves into the core concepts of management accounting, providing a comprehensive overview of budgeting, variance analysis, and financial performance evaluation. It begins by defining the purpose of budgeting, including cash collection and disbursement schedules, and illustrates these concepts with examples. The report then explores flexible budgeting and its applications. Furthermore, it examines how organizations adopt management accounting systems, using key financial metrics like Return on Capital Employed (ROCE), asset turnover, and operating profit margin to assess divisional performance. The report also discusses the importance of improving financial performance through cost management and quality management. Planning tools in management accounting, such as revenue budgeting and variance analysis, are also discussed. The report concludes by emphasizing the importance of variance analysis in maintaining better corporate control and decision-making. The report provides valuable insights into financial planning and analysis techniques.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

3.1 Purpose of budget......................................................................................................................3

1. Schedule of expected cash collections.....................................................................................4

2. Schedule of expected cash disbursement.................................................................................4

3. Cash budget for September......................................................................................................4

3.2 Flexible budget..........................................................................................................................5

4.1 How organizations are adopting management accounting systems..........................................5

i. Return on capital employed (ROCE)........................................................................................5

ii. Asset turnover..........................................................................................................................6

iii. Operating profit margin..........................................................................................................6

4.2 Improvement of financial performance.....................................................................................6

4.3 Planning tools in management accounting................................................................................8

4.4 Importance of variance analysis................................................................................................8

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Introduction......................................................................................................................................3

3.1 Purpose of budget......................................................................................................................3

1. Schedule of expected cash collections.....................................................................................4

2. Schedule of expected cash disbursement.................................................................................4

3. Cash budget for September......................................................................................................4

3.2 Flexible budget..........................................................................................................................5

4.1 How organizations are adopting management accounting systems..........................................5

i. Return on capital employed (ROCE)........................................................................................5

ii. Asset turnover..........................................................................................................................6

iii. Operating profit margin..........................................................................................................6

4.2 Improvement of financial performance.....................................................................................6

4.3 Planning tools in management accounting................................................................................8

4.4 Importance of variance analysis................................................................................................8

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Part 2

Introduction

Osbarr, a web group that buys in distributed computer systems. The monthly rental costs for the

cloud have been extended. Web group leaders can use financial plans to ensure cost increases are

too expensive and have chosen to reduce and increase operating costs. Maintaining management

books examines the gradual benefit of extended creation: this is called margin analysis. This

results in fair review, which involves creating the business mix margin of effort to determine the

size of the unit that has a total transaction. An administrative custodian will use this data to

determine the point of value for objects and administrations.

3.1 Purpose of budget

Definition

Design is the way to organize the payment of your money. This spending plan is called a

financial plan. Making this spending plan will allow you to decide in advance whether you will

have enough money for the things you need to do or want to do. An expense plan is an

assessment of income and expenses for a predetermined period in the future and is generally

prepared and reconsidered from time to time. Financial plans can be made for an individual, a

group of individuals, a company, an administration, or just about anything else that makes and

goes through money.

Purpose of the budget

2. Anticipate the future financial position of the company and the future need to use the assets in

the business with the ultimate goal of keeping the company dispersed.

3. Select the piece of capitalism to ensure that assets are affordable at a reasonable cost.

4. Organize the efforts of the different departments of the company towards the usual objectives.

Introduction

Osbarr, a web group that buys in distributed computer systems. The monthly rental costs for the

cloud have been extended. Web group leaders can use financial plans to ensure cost increases are

too expensive and have chosen to reduce and increase operating costs. Maintaining management

books examines the gradual benefit of extended creation: this is called margin analysis. This

results in fair review, which involves creating the business mix margin of effort to determine the

size of the unit that has a total transaction. An administrative custodian will use this data to

determine the point of value for objects and administrations.

3.1 Purpose of budget

Definition

Design is the way to organize the payment of your money. This spending plan is called a

financial plan. Making this spending plan will allow you to decide in advance whether you will

have enough money for the things you need to do or want to do. An expense plan is an

assessment of income and expenses for a predetermined period in the future and is generally

prepared and reconsidered from time to time. Financial plans can be made for an individual, a

group of individuals, a company, an administration, or just about anything else that makes and

goes through money.

Purpose of the budget

2. Anticipate the future financial position of the company and the future need to use the assets in

the business with the ultimate goal of keeping the company dispersed.

3. Select the piece of capitalism to ensure that assets are affordable at a reasonable cost.

4. Organize the efforts of the different departments of the company towards the usual objectives.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5. Accelerate the productivity of operations of various offices, departments and the cost of the

company.

6. Determine the responsibilities of the various department heads.

7. To bind an executive command regarding the finances, shares and contracts of the company, e

8. Promote the integrated management of the company through the budget framework.

Design work usually begins with contract evaluation because a company's overall function

depends on contracts. Negotiating the contract requires an assessment of the current market

situation and a forecast of a person's thoughts about what the future market situation for which

the financial plan is proposed might be. A little bit inside just like the external variables.

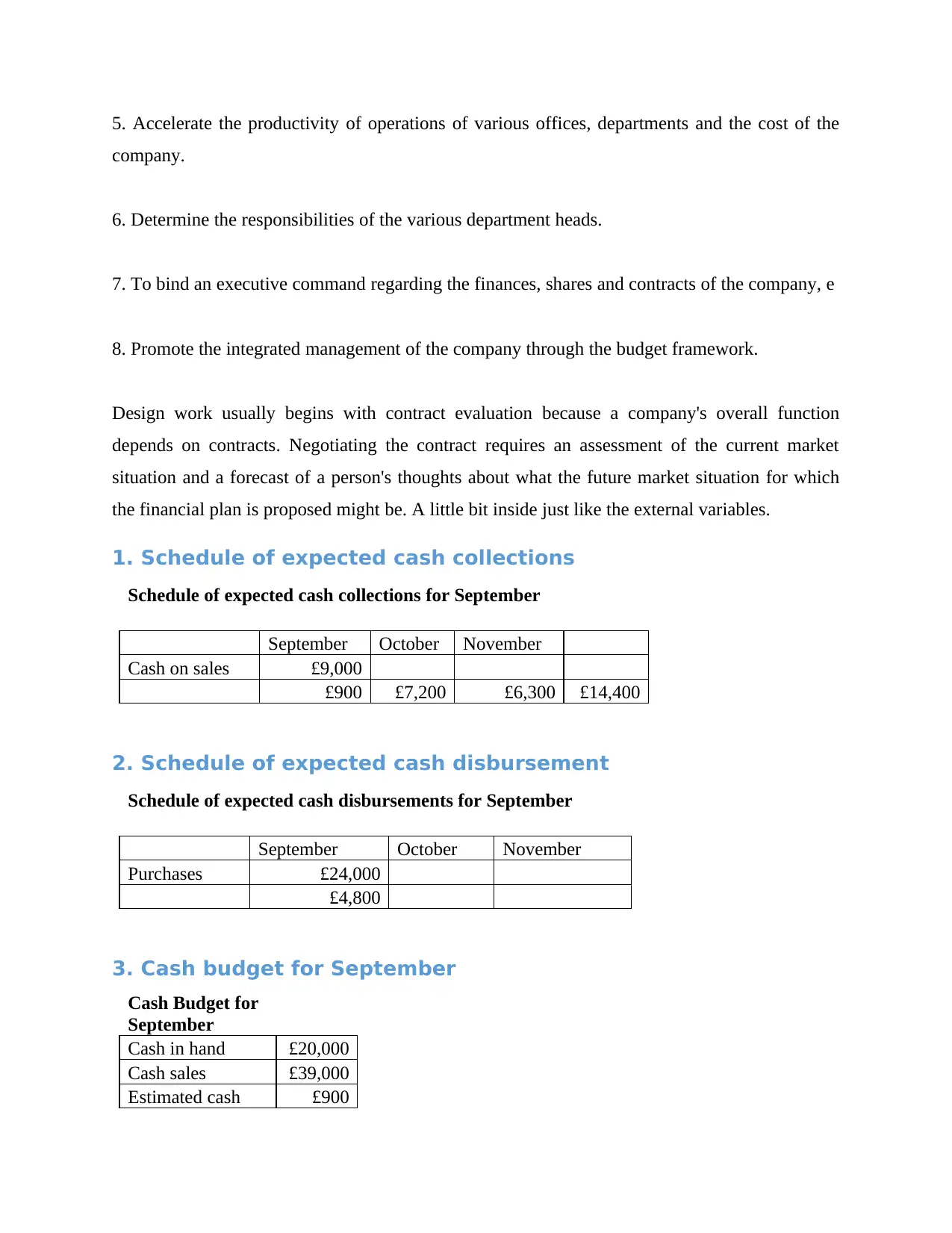

1. Schedule of expected cash collections

Schedule of expected cash collections for September

September October November

Cash on sales £9,000

£900 £7,200 £6,300 £14,400

2. Schedule of expected cash disbursement

Schedule of expected cash disbursements for September

September October November

Purchases £24,000

£4,800

3. Cash budget for September

Cash Budget for

September

Cash in hand £20,000

Cash sales £39,000

Estimated cash £900

company.

6. Determine the responsibilities of the various department heads.

7. To bind an executive command regarding the finances, shares and contracts of the company, e

8. Promote the integrated management of the company through the budget framework.

Design work usually begins with contract evaluation because a company's overall function

depends on contracts. Negotiating the contract requires an assessment of the current market

situation and a forecast of a person's thoughts about what the future market situation for which

the financial plan is proposed might be. A little bit inside just like the external variables.

1. Schedule of expected cash collections

Schedule of expected cash collections for September

September October November

Cash on sales £9,000

£900 £7,200 £6,300 £14,400

2. Schedule of expected cash disbursement

Schedule of expected cash disbursements for September

September October November

Purchases £24,000

£4,800

3. Cash budget for September

Cash Budget for

September

Cash in hand £20,000

Cash sales £39,000

Estimated cash £900

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

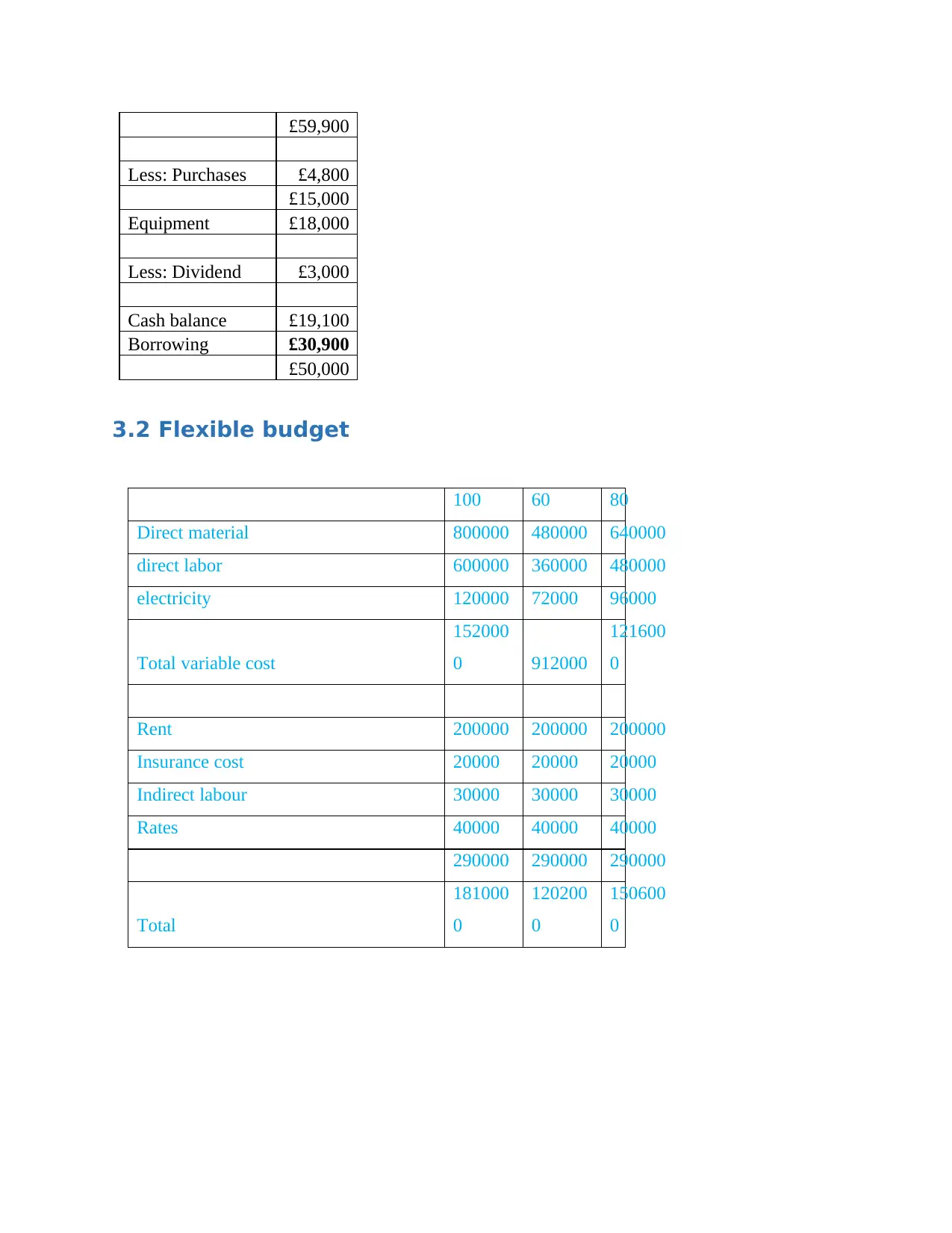

£59,900

Less: Purchases £4,800

£15,000

Equipment £18,000

Less: Dividend £3,000

Cash balance £19,100

Borrowing £30,900

£50,000

3.2 Flexible budget

100 60 80

Direct material 800000 480000 640000

direct labor 600000 360000 480000

electricity 120000 72000 96000

Total variable cost

152000

0 912000

121600

0

Rent 200000 200000 200000

Insurance cost 20000 20000 20000

Indirect labour 30000 30000 30000

Rates 40000 40000 40000

290000 290000 290000

Total

181000

0

120200

0

150600

0

Less: Purchases £4,800

£15,000

Equipment £18,000

Less: Dividend £3,000

Cash balance £19,100

Borrowing £30,900

£50,000

3.2 Flexible budget

100 60 80

Direct material 800000 480000 640000

direct labor 600000 360000 480000

electricity 120000 72000 96000

Total variable cost

152000

0 912000

121600

0

Rent 200000 200000 200000

Insurance cost 20000 20000 20000

Indirect labour 30000 30000 30000

Rates 40000 40000 40000

290000 290000 290000

Total

181000

0

120200

0

150600

0

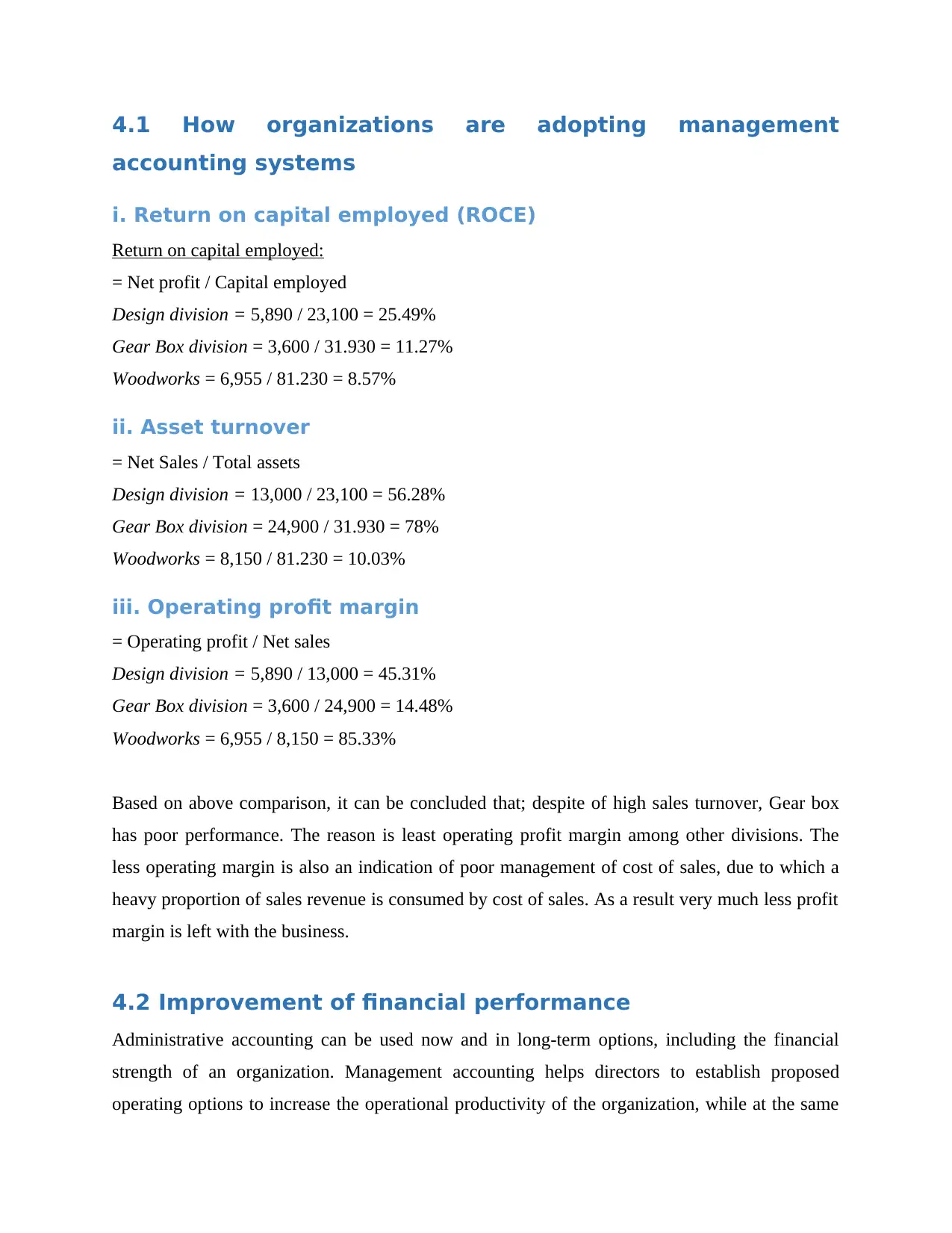

4.1 How organizations are adopting management

accounting systems

i. Return on capital employed (ROCE)

Return on capital employed:

= Net profit / Capital employed

Design division = 5,890 / 23,100 = 25.49%

Gear Box division = 3,600 / 31.930 = 11.27%

Woodworks = 6,955 / 81.230 = 8.57%

ii. Asset turnover

= Net Sales / Total assets

Design division = 13,000 / 23,100 = 56.28%

Gear Box division = 24,900 / 31.930 = 78%

Woodworks = 8,150 / 81.230 = 10.03%

iii. Operating profit margin

= Operating profit / Net sales

Design division = 5,890 / 13,000 = 45.31%

Gear Box division = 3,600 / 24,900 = 14.48%

Woodworks = 6,955 / 8,150 = 85.33%

Based on above comparison, it can be concluded that; despite of high sales turnover, Gear box

has poor performance. The reason is least operating profit margin among other divisions. The

less operating margin is also an indication of poor management of cost of sales, due to which a

heavy proportion of sales revenue is consumed by cost of sales. As a result very much less profit

margin is left with the business.

4.2 Improvement of financial performance

Administrative accounting can be used now and in long-term options, including the financial

strength of an organization. Management accounting helps directors to establish proposed

operating options to increase the operational productivity of the organization, while at the same

accounting systems

i. Return on capital employed (ROCE)

Return on capital employed:

= Net profit / Capital employed

Design division = 5,890 / 23,100 = 25.49%

Gear Box division = 3,600 / 31.930 = 11.27%

Woodworks = 6,955 / 81.230 = 8.57%

ii. Asset turnover

= Net Sales / Total assets

Design division = 13,000 / 23,100 = 56.28%

Gear Box division = 24,900 / 31.930 = 78%

Woodworks = 8,150 / 81.230 = 10.03%

iii. Operating profit margin

= Operating profit / Net sales

Design division = 5,890 / 13,000 = 45.31%

Gear Box division = 3,600 / 24,900 = 14.48%

Woodworks = 6,955 / 8,150 = 85.33%

Based on above comparison, it can be concluded that; despite of high sales turnover, Gear box

has poor performance. The reason is least operating profit margin among other divisions. The

less operating margin is also an indication of poor management of cost of sales, due to which a

heavy proportion of sales revenue is consumed by cost of sales. As a result very much less profit

margin is left with the business.

4.2 Improvement of financial performance

Administrative accounting can be used now and in long-term options, including the financial

strength of an organization. Management accounting helps directors to establish proposed

operating options to increase the operational productivity of the organization, while at the same

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

time helping to establish long-term speculative options. Determining, monitoring and tracking

execution is an integral part of administrative accounting to ensure that the actual results meet

the cost plans and figures established at first of all.

Administrative accounting provides organizations with quantitative and thematic data on

performance and financial performance. While cash accounting focuses on the external use of

this data by banks and others to review performance and decision making, administrative

accounting is used internally by owners, bosses and others. representatives. The organizational

management accounting framework covers the cycles that organizations have introduced to

control and plan activities and maintain success dynamics.

Cost management

One of the main ways in which administrative accounting officers contribute to the continuous

improvement of society is through turning events and coordinating the expenses of board

officers. Instead of planning and controlling it directly at the office or at a practical level,

organizations do so at a mobile stage, such as buying shares or measuring receipts or disposals.

Organizations measure the costs of data repositories and reduce or eliminate those costs that add

almost zero value. They also measure and evaluate the potential of their important exercises,

demonstrating new exercises that will improve performance where possible.

Template

An organization’s accounting administrator takes out the flow of stock purchase measures and

compares it to its costs. In doing so, it recognizes that some investment and effort is required to

buy from certain suppliers compared to others, although the costs of materials are comparable.

The supervisor chooses to reduce the size of the demand and what is happening with these

providers. The boss goes back to this stream of bike and cost verification and points out that

some purchase orders last tight days for a complicated agreement if the owner is traveling. He

recommends purchasing programs that provide a tool for interaction and allow the owner to

support a purchase request via email.

Quality Management

execution is an integral part of administrative accounting to ensure that the actual results meet

the cost plans and figures established at first of all.

Administrative accounting provides organizations with quantitative and thematic data on

performance and financial performance. While cash accounting focuses on the external use of

this data by banks and others to review performance and decision making, administrative

accounting is used internally by owners, bosses and others. representatives. The organizational

management accounting framework covers the cycles that organizations have introduced to

control and plan activities and maintain success dynamics.

Cost management

One of the main ways in which administrative accounting officers contribute to the continuous

improvement of society is through turning events and coordinating the expenses of board

officers. Instead of planning and controlling it directly at the office or at a practical level,

organizations do so at a mobile stage, such as buying shares or measuring receipts or disposals.

Organizations measure the costs of data repositories and reduce or eliminate those costs that add

almost zero value. They also measure and evaluate the potential of their important exercises,

demonstrating new exercises that will improve performance where possible.

Template

An organization’s accounting administrator takes out the flow of stock purchase measures and

compares it to its costs. In doing so, it recognizes that some investment and effort is required to

buy from certain suppliers compared to others, although the costs of materials are comparable.

The supervisor chooses to reduce the size of the demand and what is happening with these

providers. The boss goes back to this stream of bike and cost verification and points out that

some purchase orders last tight days for a complicated agreement if the owner is traveling. He

recommends purchasing programs that provide a tool for interaction and allow the owner to

support a purchase request via email.

Quality Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Administrative bookkeeping frameworks measures and screen quality-related expenses

additionally add to ceaseless improvement. By estimating quality-related expenses and binds

them to item or administration quality, a decent framework continually distinguishes where little

changes can be had to emphatically effect quality. This emphasis on improving quality at the

littlest level by those not straightforwardly engaged with creation or conveyance assists

organizations with centering building incredible items and conveying excellent help.

4.3 Planning tools in management accounting

Financial plan of revenue:

Money is perhaps the most important issue for a company because it is characterized by working

capital resources and a lack of money can affect the ability to manage the product. A revenue

spending plan is essential for the planning exercises that are performed to estimate future cash

factor data by examining ongoing models (Pinheiro, 2014).

Study of the differences:

It is sensible as an arrangement of some logical game plans that are accessible to businesses to

look at pre-planned principles versus actual outcomes. This tool is useful for both monetary and

non-monetary perspectives and is best known for determining the efficiency of business activity

and the accuracy of design forecasts (Cleartax, 2018).

Business valuation methods:

There are a number of verification methods that a business association can use to reasonably

assess the reasonableness of capital initiatives. For example, NPV (Net Present Value) teaches

the current estimate of the reliable benefits that will be generated by corporate options (Lindvall

and Larsson, 2017). In addition, the recovery time period indicates the length of time it takes for

a campaign to restore a measure of profitability.

4.4 Importance of variance analysis

The analysis of variance is a way to evaluate the difference between the evaluated financial plans

and the actual numbers. It is a measure that helps in maintaining better corporate control.

additionally add to ceaseless improvement. By estimating quality-related expenses and binds

them to item or administration quality, a decent framework continually distinguishes where little

changes can be had to emphatically effect quality. This emphasis on improving quality at the

littlest level by those not straightforwardly engaged with creation or conveyance assists

organizations with centering building incredible items and conveying excellent help.

4.3 Planning tools in management accounting

Financial plan of revenue:

Money is perhaps the most important issue for a company because it is characterized by working

capital resources and a lack of money can affect the ability to manage the product. A revenue

spending plan is essential for the planning exercises that are performed to estimate future cash

factor data by examining ongoing models (Pinheiro, 2014).

Study of the differences:

It is sensible as an arrangement of some logical game plans that are accessible to businesses to

look at pre-planned principles versus actual outcomes. This tool is useful for both monetary and

non-monetary perspectives and is best known for determining the efficiency of business activity

and the accuracy of design forecasts (Cleartax, 2018).

Business valuation methods:

There are a number of verification methods that a business association can use to reasonably

assess the reasonableness of capital initiatives. For example, NPV (Net Present Value) teaches

the current estimate of the reliable benefits that will be generated by corporate options (Lindvall

and Larsson, 2017). In addition, the recovery time period indicates the length of time it takes for

a campaign to restore a measure of profitability.

4.4 Importance of variance analysis

The analysis of variance is a way to evaluate the difference between the evaluated financial plans

and the actual numbers. It is a measure that helps in maintaining better corporate control.

Material variance: this is the difference between what you intended to use and what you used,

doubled with the cost of materials. You can equate this: (actual unit used - standard unit use) x

average cost per unit.

Variation in labor: Measure how much an organization uses work versus what you hope it

wants. The variation is determined by (actual hours - normal hours) x normal rate.

Variation in variable productivity: This is the difference between how long they worked

versus what they planned for the job. It is determined by the standard x (actual hours - normal

hours).

doubled with the cost of materials. You can equate this: (actual unit used - standard unit use) x

average cost per unit.

Variation in labor: Measure how much an organization uses work versus what you hope it

wants. The variation is determined by (actual hours - normal hours) x normal rate.

Variation in variable productivity: This is the difference between how long they worked

versus what they planned for the job. It is determined by the standard x (actual hours - normal

hours).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Conclusion

On-board accounting is the framework for collecting and storing information, so that, after the

information has been processed; the last information used has created an administrative

accounting framework.

Management accounting and hierarchy systems are closely linked. The interaction of details and

implementation of the procedures in the societies is effected by the approach and type of

language. The interaction of dynamic modes usually affects the design and use of the framework

as an image of the control system. Many scientists accept that in order to be fertile at the top, it is

necessary to have clear and authoritative methods. Therefore, we need components within the

framework to facilitate unique approaches, for example, accounting data framework and

authoritative creation / primary interaction.

On-board accounting is the framework for collecting and storing information, so that, after the

information has been processed; the last information used has created an administrative

accounting framework.

Management accounting and hierarchy systems are closely linked. The interaction of details and

implementation of the procedures in the societies is effected by the approach and type of

language. The interaction of dynamic modes usually affects the design and use of the framework

as an image of the control system. Many scientists accept that in order to be fertile at the top, it is

necessary to have clear and authoritative methods. Therefore, we need components within the

framework to facilitate unique approaches, for example, accounting data framework and

authoritative creation / primary interaction.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Cleartax, 2019. Variance Analysis – Overview, Budgeting, Benefits.

[online] Cleartax.in. Available at: https://cleartax.in/s/variance-analysis [Accessed 9 Mar.

2019].

Crum, R.L. and Derkinderen, F.G., 2012. Capital budgeting under conditions of

uncertainty (Vol. 5). Springer Science & Business Media.

Gonçalves, T. and Gaio, C., 2021. The role of management accounting systems in global value

strategies. Journal of Business Research, 124, pp.603-609.

Gonçalves, T. and Gaio, C., 2021. The role of management accounting systems in global value

strategies. Journal of Business Research, 124, pp.603-609.

Hopkins, J.P., 2013. Afterlife in the cloud: Managing a digital estate. Hastings Sci. & Tech.

LJ, 5, p.209.

Lindvall, N. and Larsson, A., 2017. Investment Appraisal in the Public Sector–Incorporating

Flexibility and Environmental Impact. Journal of Advanced Management Science Vol,

5(3).

Markgraf, B., 2019. Difference among KPI and benchmarking

[online] Yourbusiness.azcentral.com. Available at:

https://yourbusiness.azcentral.com/difference-between-benchmark-indicators-key-

performance-indicators-23945.html [Accessed 9 Mar. 2019].

Massingham, P., 2014. An evaluation of knowledge management tools: Part 1–managing

knowledge resources. Journal of Knowledge Management, 18(6), pp.1075-1100.

Mutikanga, H.E., Sharma, S.K. and Vairavamoorthy, K., 2012. Methods and tools for managing

losses in water distribution systems. Journal of Water Resources Planning and

Management, 139(2), pp.166-174.

Pinheiro, J.D.O.G., 2014. Cash budget versus financial budget: advantages and disadvantages: a

case study (Doctoral dissertation).

Solovida, G.T. and Latan, H., 2021. Achieving triple bottom line performance: highlighting the

role of social capabilities and environmental management accounting. Management of

Environmental Quality: An International Journal.

Wilker, J. and Rusche, K., 2014. Economic valuation as a tool to support decision-making in

strategic green infrastructure planning. Local Environment, 19(6), pp.702-713.

Cleartax, 2019. Variance Analysis – Overview, Budgeting, Benefits.

[online] Cleartax.in. Available at: https://cleartax.in/s/variance-analysis [Accessed 9 Mar.

2019].

Crum, R.L. and Derkinderen, F.G., 2012. Capital budgeting under conditions of

uncertainty (Vol. 5). Springer Science & Business Media.

Gonçalves, T. and Gaio, C., 2021. The role of management accounting systems in global value

strategies. Journal of Business Research, 124, pp.603-609.

Gonçalves, T. and Gaio, C., 2021. The role of management accounting systems in global value

strategies. Journal of Business Research, 124, pp.603-609.

Hopkins, J.P., 2013. Afterlife in the cloud: Managing a digital estate. Hastings Sci. & Tech.

LJ, 5, p.209.

Lindvall, N. and Larsson, A., 2017. Investment Appraisal in the Public Sector–Incorporating

Flexibility and Environmental Impact. Journal of Advanced Management Science Vol,

5(3).

Markgraf, B., 2019. Difference among KPI and benchmarking

[online] Yourbusiness.azcentral.com. Available at:

https://yourbusiness.azcentral.com/difference-between-benchmark-indicators-key-

performance-indicators-23945.html [Accessed 9 Mar. 2019].

Massingham, P., 2014. An evaluation of knowledge management tools: Part 1–managing

knowledge resources. Journal of Knowledge Management, 18(6), pp.1075-1100.

Mutikanga, H.E., Sharma, S.K. and Vairavamoorthy, K., 2012. Methods and tools for managing

losses in water distribution systems. Journal of Water Resources Planning and

Management, 139(2), pp.166-174.

Pinheiro, J.D.O.G., 2014. Cash budget versus financial budget: advantages and disadvantages: a

case study (Doctoral dissertation).

Solovida, G.T. and Latan, H., 2021. Achieving triple bottom line performance: highlighting the

role of social capabilities and environmental management accounting. Management of

Environmental Quality: An International Journal.

Wilker, J. and Rusche, K., 2014. Economic valuation as a tool to support decision-making in

strategic green infrastructure planning. Local Environment, 19(6), pp.702-713.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.