Management Accounting for David Jones: Features of Activity Based Budgeting and its Suitability

VerifiedAdded on 2023/06/04

|15

|4006

|247

AI Summary

This report discusses the use of activity based costing and its features in an organization. The organization that has been selected for pursuing this report is David Jones, which is an upmarket department store in Australia, deals in different products and altering its operations with time. The report highlights the features of activity based budgeting, the difference between traditional budgeting and activity based budgeting, and checks the suitability of activity based costing for David Jones.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

David Jones

Management Accounting

David Jones

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT ACCOUNTING 1

Table of Contents

Introduction................................................................................................................................2

Overview of David Jones.......................................................................................................2

The vision of David Jones Limited....................................................................................3

The mission of David Jones Limited.................................................................................4

Values of David Jones Limited..........................................................................................4

Overview of Activity Based Budgeting and Features............................................................4

Features of Activity based budgeting.................................................................................6

Difference between traditional budgeting system and activity based budgeting...................7

Checking the Suitability of Activity Based Costing for David Jones....................................9

Conclusion................................................................................................................................11

References................................................................................................................................12

Table of Contents

Introduction................................................................................................................................2

Overview of David Jones.......................................................................................................2

The vision of David Jones Limited....................................................................................3

The mission of David Jones Limited.................................................................................4

Values of David Jones Limited..........................................................................................4

Overview of Activity Based Budgeting and Features............................................................4

Features of Activity based budgeting.................................................................................6

Difference between traditional budgeting system and activity based budgeting...................7

Checking the Suitability of Activity Based Costing for David Jones....................................9

Conclusion................................................................................................................................11

References................................................................................................................................12

MANAGEMENT ACCOUNTING 2

Introduction

Management is the procedure of recognizing, evaluating, analyzing, understanding, and

communicating info to the administration that is focused towards attaining the goals of the

organization (Nørreklit, 2017). Management accounting is also called cost accounting. The

main dissimilarity between financial accounting and managerial accounting is that financial

accounting is attentive towards offering data to the external parties of the company, and

management accounting information is supporting the executives in the business in taking

proper decisions. There are various tools available that support management accounting

determines and handle their resources, costs, and strategies of the organization (CGMA,

2013). One of the significant tools of management accounting that support organizations in

planning their budgets and managing resources of every activity of the business is Activity

based budgeting. The purpose of this report is to highlight the use of activity based costing

and its features in an organization. The organization that has been selected for pursuing this

report is David Jones, which is an upmarket department store in Australia, deals in different

products and altering its operations with time. After discussing this report will review

whether Activity based costing will be suitable for David Jones or not. In the end, an

argument will be presented that will highlight the dissimilarity between traditional budgeting

and activity based budgeting.

Overview of David Jones

David Jones is the upmarket department store of Australia, which is owned by the retail

group of South Africa i.e. Woolworths Holdings Limited. David Jones established this firm in

1838, a Welsh trader, and forthcoming politician after he settled to Australia, and is the eldest

unceasingly functioning department store in the whole world still operating under its original

name. Presently, David Jones Limited has 45 stores placed in most of the states and territories

Introduction

Management is the procedure of recognizing, evaluating, analyzing, understanding, and

communicating info to the administration that is focused towards attaining the goals of the

organization (Nørreklit, 2017). Management accounting is also called cost accounting. The

main dissimilarity between financial accounting and managerial accounting is that financial

accounting is attentive towards offering data to the external parties of the company, and

management accounting information is supporting the executives in the business in taking

proper decisions. There are various tools available that support management accounting

determines and handle their resources, costs, and strategies of the organization (CGMA,

2013). One of the significant tools of management accounting that support organizations in

planning their budgets and managing resources of every activity of the business is Activity

based budgeting. The purpose of this report is to highlight the use of activity based costing

and its features in an organization. The organization that has been selected for pursuing this

report is David Jones, which is an upmarket department store in Australia, deals in different

products and altering its operations with time. After discussing this report will review

whether Activity based costing will be suitable for David Jones or not. In the end, an

argument will be presented that will highlight the dissimilarity between traditional budgeting

and activity based budgeting.

Overview of David Jones

David Jones is the upmarket department store of Australia, which is owned by the retail

group of South Africa i.e. Woolworths Holdings Limited. David Jones established this firm in

1838, a Welsh trader, and forthcoming politician after he settled to Australia, and is the eldest

unceasingly functioning department store in the whole world still operating under its original

name. Presently, David Jones Limited has 45 stores placed in most of the states and territories

MANAGEMENT ACCOUNTING 3

of Australia (except in the Northern Territory and Tasmania) (IBIS World, 2013). The main

rivals of David Jones are the big, high-class subdivision chin of store i.e., Myer. In 2016, the

company opened its first store in New Zealand market after purchasing Kirkcaldie & Stains.

In the same year, the parent company of David Jones i.e. Woolworths Holdings Limited

proclaimed that headquarter of the company is shifted from Sydney, New South Wales to

Richmond, Victoria (David Jones, 2018).

In 2013, Myer management approached David Jones with a provisional, non-binding,

revealing offer for a possible union of the two businesses. Myer thought that the combined

group would have produced highest earnings and sales before tax and interest in 2013 of

around $5.0 billion and $364 million, correspondingly. Moreover, Myer estimated that a

union of both the companies could have helped in attaining around $85 million of continuing

yearly cost collaborations within three years, mainly determined by organizational

competences. The David Jones board disallowed the proposal in November 2013 (David

Jones, 2018). In 2014, again Myer went to David Jones offering to purchase the business at

market value, with David Jones possess a market capitalization of around $1.7 billion. Myer

also specified that its CEO Bernie Brookes would be competent in handling both the entities

if the merger will take place. David Jones recognized the letter affirming it would think about

any offer that will be in the best interest of the company’s shareholders (David Jones, 2018).

The vision of David Jones Limited

The vision of David Jones Limited is to be the most responsible retailer in the world that

could reflect their passion and commitment to be involved in a good trade, for their people,

planet, and customers (Woolworths Holding, 2018).

of Australia (except in the Northern Territory and Tasmania) (IBIS World, 2013). The main

rivals of David Jones are the big, high-class subdivision chin of store i.e., Myer. In 2016, the

company opened its first store in New Zealand market after purchasing Kirkcaldie & Stains.

In the same year, the parent company of David Jones i.e. Woolworths Holdings Limited

proclaimed that headquarter of the company is shifted from Sydney, New South Wales to

Richmond, Victoria (David Jones, 2018).

In 2013, Myer management approached David Jones with a provisional, non-binding,

revealing offer for a possible union of the two businesses. Myer thought that the combined

group would have produced highest earnings and sales before tax and interest in 2013 of

around $5.0 billion and $364 million, correspondingly. Moreover, Myer estimated that a

union of both the companies could have helped in attaining around $85 million of continuing

yearly cost collaborations within three years, mainly determined by organizational

competences. The David Jones board disallowed the proposal in November 2013 (David

Jones, 2018). In 2014, again Myer went to David Jones offering to purchase the business at

market value, with David Jones possess a market capitalization of around $1.7 billion. Myer

also specified that its CEO Bernie Brookes would be competent in handling both the entities

if the merger will take place. David Jones recognized the letter affirming it would think about

any offer that will be in the best interest of the company’s shareholders (David Jones, 2018).

The vision of David Jones Limited

The vision of David Jones Limited is to be the most responsible retailer in the world that

could reflect their passion and commitment to be involved in a good trade, for their people,

planet, and customers (Woolworths Holding, 2018).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT ACCOUNTING 4

The mission of David Jones Limited

The mission of David Jones Limited is to add value to the life of people by offering good

quality products and enhance the experience of their people and customers (Woolworths

Holding, 2018).

Values of David Jones Limited

The values of David Jones notify and reinforce the manner they do the business across their

group. From the value-centric leadership to passionate brand support, they look to implant

their values in all the extents of their business. The values reflect that they are consumer

obsesses, stimulating, accountable, combined, and dedicated towards the quality

(Woolworths Holding, 2018).

Overview of Activity Based Budgeting and Features

Budgets are generally planned for the areas in an organization and for different activities.

System of budgeting i.e. Activity based budgeting offer the inclusive financial plan to the

business as a whole and offers a business various advantages such as it enforces executives to

plan, and it offers information of the resources that could be used to enhance the procedure of

decision making (CGMA, 2013). Besides this, it assists in the utilization of employees,

resources by placing a standard that could be used for the succeeding performance

assessment, and it enhances coordination and communication among customers, organization,

and employees. Budgeting forces administration to do planning for the upcoming period to

frame direction for the business, predict issues, and improve future strategies. When

executives spend their time in planning, the understanding of the capabilities of the business

increases and the understanding of where the key resources of the company must be used

increases. Budgets allow executives to make improved decisions. They support executives to

predict their potential variances, particularly in shortfalls (Huynh and Huynh, 2013). By

evaluating differences to discover the cause, support managers develop activities of the

The mission of David Jones Limited

The mission of David Jones Limited is to add value to the life of people by offering good

quality products and enhance the experience of their people and customers (Woolworths

Holding, 2018).

Values of David Jones Limited

The values of David Jones notify and reinforce the manner they do the business across their

group. From the value-centric leadership to passionate brand support, they look to implant

their values in all the extents of their business. The values reflect that they are consumer

obsesses, stimulating, accountable, combined, and dedicated towards the quality

(Woolworths Holding, 2018).

Overview of Activity Based Budgeting and Features

Budgets are generally planned for the areas in an organization and for different activities.

System of budgeting i.e. Activity based budgeting offer the inclusive financial plan to the

business as a whole and offers a business various advantages such as it enforces executives to

plan, and it offers information of the resources that could be used to enhance the procedure of

decision making (CGMA, 2013). Besides this, it assists in the utilization of employees,

resources by placing a standard that could be used for the succeeding performance

assessment, and it enhances coordination and communication among customers, organization,

and employees. Budgeting forces administration to do planning for the upcoming period to

frame direction for the business, predict issues, and improve future strategies. When

executives spend their time in planning, the understanding of the capabilities of the business

increases and the understanding of where the key resources of the company must be used

increases. Budgets allow executives to make improved decisions. They support executives to

predict their potential variances, particularly in shortfalls (Huynh and Huynh, 2013). By

evaluating differences to discover the cause, support managers develop activities of the

MANAGEMENT ACCOUNTING 5

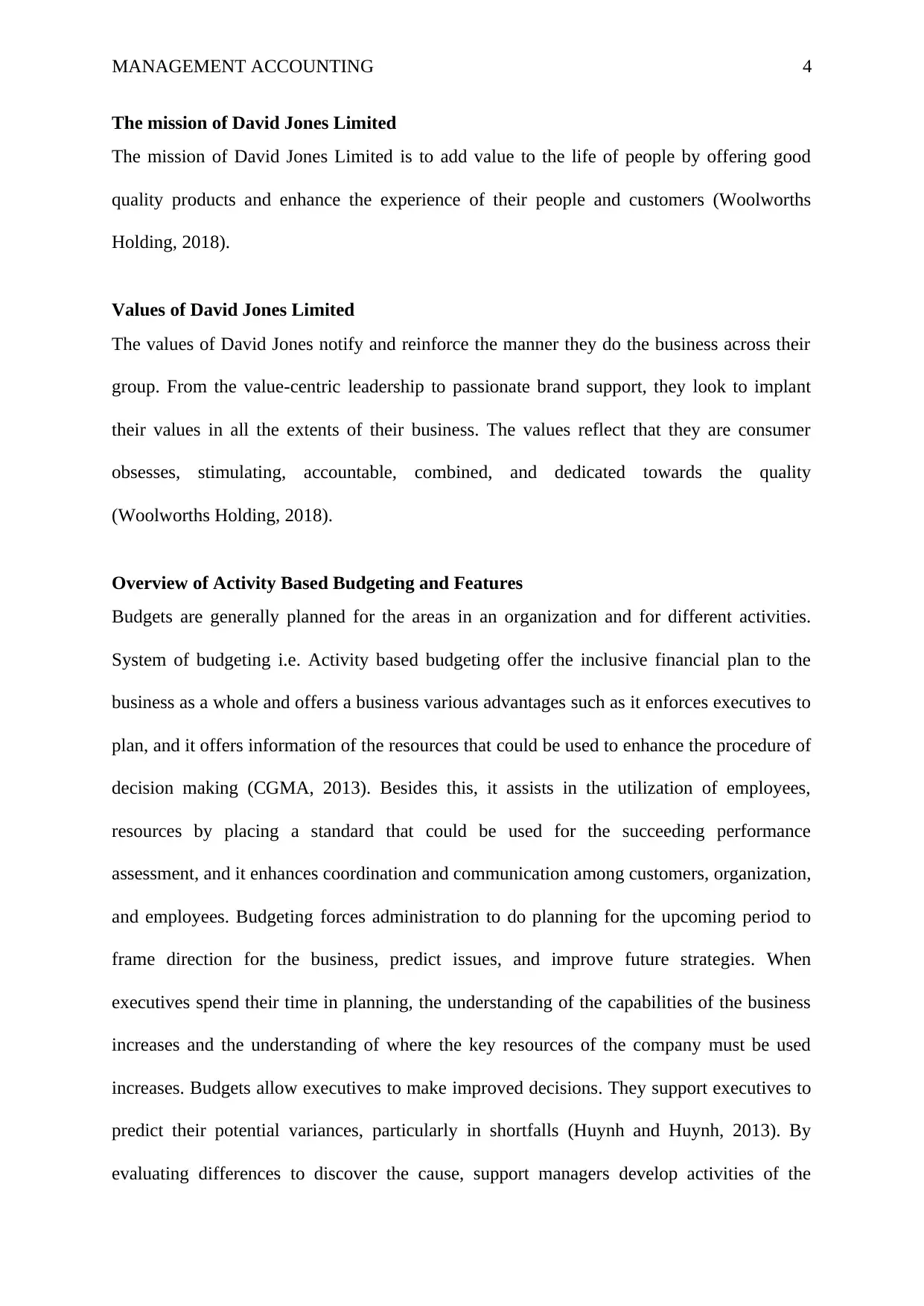

organization to attain the planned goals. Budgets set the criteria that can regulate the use of

resources of the company and employee’s motivation.

Source [(Pietrzak, 2013)]

Activity based budgeting is the technique that researches, analyze, and records activities that

are valuable for the business. Activity based budgets are just regulating preceding budgets to

check the inflation or development of the business (Oneshko and Boiko, 2016). In its place,

ABB identifies efficiencies in the operations of the business and creates budgets based on

different activities involved. The two fundamental and basic notions that motivate the usage

of ABB are Activity Based Costing and Activity Based Analysis. The first is the set of

processes and rules utilized in evaluating, assigning, and tracking cost to objects, whereas,

the second concept is the heat of valuation all the function in the fundamental detailed

elements. In order to adopt activity based budgeting, business must have sufficient funds that

can support business in bearing the expenditures that are incurred at the time of conducting

research and preparing budgets under this system (Moustafa, 2005). This method is a time

consuming which comprises detailed analysis and research to prepare the budgets of the

business. However, activity based budgeting helps in getting detailed and precise information

about the cost that can be incurred while planning changes in the future.

organization to attain the planned goals. Budgets set the criteria that can regulate the use of

resources of the company and employee’s motivation.

Source [(Pietrzak, 2013)]

Activity based budgeting is the technique that researches, analyze, and records activities that

are valuable for the business. Activity based budgets are just regulating preceding budgets to

check the inflation or development of the business (Oneshko and Boiko, 2016). In its place,

ABB identifies efficiencies in the operations of the business and creates budgets based on

different activities involved. The two fundamental and basic notions that motivate the usage

of ABB are Activity Based Costing and Activity Based Analysis. The first is the set of

processes and rules utilized in evaluating, assigning, and tracking cost to objects, whereas,

the second concept is the heat of valuation all the function in the fundamental detailed

elements. In order to adopt activity based budgeting, business must have sufficient funds that

can support business in bearing the expenditures that are incurred at the time of conducting

research and preparing budgets under this system (Moustafa, 2005). This method is a time

consuming which comprises detailed analysis and research to prepare the budgets of the

business. However, activity based budgeting helps in getting detailed and precise information

about the cost that can be incurred while planning changes in the future.

MANAGEMENT ACCOUNTING 6

Features of Activity based budgeting

Costlier

Activity based budgeting is a costly method of budgeting as it requires the involvement of

executives and experts that possess the detailed knowledge of the business as well as the

market. Moreover, it is comprised of detailed analysis and research that could not be

conducted without the support of management and funds (Bragg, 2016).

Time Consuming

It takes a lot of time to arrange the data and perform the research to identify the relevant

activities as well as resources required to attain the goals. Therefore, it is a very time

consuming procedure (Bragg, 2016).

Reliable information

Traditional budgeting systems only check the previous year results to prepare the current year

budget that does not provide a company reliable as well as precise information about the

expenditures that are going to incur in the future. However, activity-based budgeting is one of

the reliable systems because it performs a detailed analysis of the activities and the cost

associated with them (Drury, 2008).

Competitive Advantage

The system of activity based budgeting removes all kind of needless activities that support

the company in saving its costs. The saved cost is the utilized in the goods production at less

cost (Drury, 2008). Besides this, it, help the business to attain a competitive edge over its

competitors.

Improve Customer and Company’s Relationship

The system of Activity based budgeting support in enhancing the company's relationship with

its stakeholders particularly with the consumers. The key objective of this system is to

Features of Activity based budgeting

Costlier

Activity based budgeting is a costly method of budgeting as it requires the involvement of

executives and experts that possess the detailed knowledge of the business as well as the

market. Moreover, it is comprised of detailed analysis and research that could not be

conducted without the support of management and funds (Bragg, 2016).

Time Consuming

It takes a lot of time to arrange the data and perform the research to identify the relevant

activities as well as resources required to attain the goals. Therefore, it is a very time

consuming procedure (Bragg, 2016).

Reliable information

Traditional budgeting systems only check the previous year results to prepare the current year

budget that does not provide a company reliable as well as precise information about the

expenditures that are going to incur in the future. However, activity-based budgeting is one of

the reliable systems because it performs a detailed analysis of the activities and the cost

associated with them (Drury, 2008).

Competitive Advantage

The system of activity based budgeting removes all kind of needless activities that support

the company in saving its costs. The saved cost is the utilized in the goods production at less

cost (Drury, 2008). Besides this, it, help the business to attain a competitive edge over its

competitors.

Improve Customer and Company’s Relationship

The system of Activity based budgeting support in enhancing the company's relationship with

its stakeholders particularly with the consumers. The key objective of this system is to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 7

exclude the excessive activities and offer the consumer the best quality at a reasonable price.

This makes compulsory for the workforce of the business to assist customers in the best

possible way and ensure their increased satisfaction (Bragg, 2016).

Assessment

Method of activity based budgeting measures every cost driver in the business. It considers

all the possible phases included in an activity. The immaterial activities are eradicated and

only the required activities are included to generate value for the business (Drury, 2008).

Short term

The focus of activity based budgeting is towards the short-term objectives of the company. It

does not consider the long-term situation of the company as it focuses more on the short term

goals that could be proved to be very incurable for the organization (Bragg, 2016).

Resource consumption

The process of budgeting makes use of various resources of the business that need the

requirement of the top administration of the company for conducting the analysis (Drury,

2008).

Difference between traditional budgeting system and activity based budgeting

Traditional budgeting is a technique of preparing budgets in which the previous year's budget

is considered as a base. The budget for the current year is prepared by doing some alterations

to the budget of the previous year by amending the overheads depending on the customer

demand, the situation of the market, and inflation rate, etc. Whereas, Activity based is a

system of planning in which cost is linked with the activities and budgeting expenditure is

then compiled based on the expected activity level. Unlike other methods of budgeting,

activity based budgeting adjust cost levels for inflation and changes in the revenue to derive

the yearly budget (E-Finance, 2018). The key objective of budgeting is enhancing and

exclude the excessive activities and offer the consumer the best quality at a reasonable price.

This makes compulsory for the workforce of the business to assist customers in the best

possible way and ensure their increased satisfaction (Bragg, 2016).

Assessment

Method of activity based budgeting measures every cost driver in the business. It considers

all the possible phases included in an activity. The immaterial activities are eradicated and

only the required activities are included to generate value for the business (Drury, 2008).

Short term

The focus of activity based budgeting is towards the short-term objectives of the company. It

does not consider the long-term situation of the company as it focuses more on the short term

goals that could be proved to be very incurable for the organization (Bragg, 2016).

Resource consumption

The process of budgeting makes use of various resources of the business that need the

requirement of the top administration of the company for conducting the analysis (Drury,

2008).

Difference between traditional budgeting system and activity based budgeting

Traditional budgeting is a technique of preparing budgets in which the previous year's budget

is considered as a base. The budget for the current year is prepared by doing some alterations

to the budget of the previous year by amending the overheads depending on the customer

demand, the situation of the market, and inflation rate, etc. Whereas, Activity based is a

system of planning in which cost is linked with the activities and budgeting expenditure is

then compiled based on the expected activity level. Unlike other methods of budgeting,

activity based budgeting adjust cost levels for inflation and changes in the revenue to derive

the yearly budget (E-Finance, 2018). The key objective of budgeting is enhancing and

MANAGEMENT ACCOUNTING 8

controlling the efficiency. From the analysis, it could be said that Activity based budgeting

has several advantages as compared to traditional budgeting. ABB creates a target and

motivates managers to operate towards attaining the goals of the organization. The company

makes use of activity based budgeting to assess its competence and success. Competence is

attained when the process of the business is performed effectively, with zero percentage

waste. The ABB offer a valuation of the competence of an executive. This is because it helps

in comparing the definite outcomes with the pre-planned budgeting activity. Success means

that an executive attains or surpasses the described goals (Pietrzak, 2013).

Activity based budgeting upkeep some potential as an answer to the errors and hindrances of

methods of traditional. Traditional budgets do not recognize any type of waste whereas

activity based budgeting disclose non-value costs. Traditional budgeting concentrate on the

employees and activity based budgeting concentrate on the workload on the employees

(Smith, 2018). Besides this traditional budget, concentrates on the cost of divisions and

activity based budgeting talks about the cost of the process. Traditional budgets talk about the

fixed versus variable costs and activity based costing talks about used capacity versus

unemployed capacity. Traditional budgets evaluate effect whereas activity based budgeting

evaluates root cause (Shane, 2018).

Activity based budgeting is said to be a substitute to the government traditional budgets, the

line item might be essential according to the law, but there is nothing stopping a company

from accepting the activity based budgeting to resolve the internal business issues. ABB

system is useful for the businesses experiencing changes in terms of material, like new

subsidiaries, locations of the business, products of the business, significant consumers, etc.

Because traditional method just adjusts a budget of the previous year. Traditional budgeting

is a system that lacks in offering consistent and detailed information whereas today

organizations adopt activity based budgeting just because it provides them more consistent as

controlling the efficiency. From the analysis, it could be said that Activity based budgeting

has several advantages as compared to traditional budgeting. ABB creates a target and

motivates managers to operate towards attaining the goals of the organization. The company

makes use of activity based budgeting to assess its competence and success. Competence is

attained when the process of the business is performed effectively, with zero percentage

waste. The ABB offer a valuation of the competence of an executive. This is because it helps

in comparing the definite outcomes with the pre-planned budgeting activity. Success means

that an executive attains or surpasses the described goals (Pietrzak, 2013).

Activity based budgeting upkeep some potential as an answer to the errors and hindrances of

methods of traditional. Traditional budgets do not recognize any type of waste whereas

activity based budgeting disclose non-value costs. Traditional budgeting concentrate on the

employees and activity based budgeting concentrate on the workload on the employees

(Smith, 2018). Besides this traditional budget, concentrates on the cost of divisions and

activity based budgeting talks about the cost of the process. Traditional budgets talk about the

fixed versus variable costs and activity based costing talks about used capacity versus

unemployed capacity. Traditional budgets evaluate effect whereas activity based budgeting

evaluates root cause (Shane, 2018).

Activity based budgeting is said to be a substitute to the government traditional budgets, the

line item might be essential according to the law, but there is nothing stopping a company

from accepting the activity based budgeting to resolve the internal business issues. ABB

system is useful for the businesses experiencing changes in terms of material, like new

subsidiaries, locations of the business, products of the business, significant consumers, etc.

Because traditional method just adjusts a budget of the previous year. Traditional budgeting

is a system that lacks in offering consistent and detailed information whereas today

organizations adopt activity based budgeting just because it provides them more consistent as

MANAGEMENT ACCOUNTING 9

well as detailed information to manage the expenditures that take place to complete different

business activities (Surbhi, 2017). Moreover, ABB also provides detailed information that

offers various opportunities and data cross-analysis to the company. Unlike traditional

budgeting method, the ABB method analyses the present opportunities and assign resources

precisely to every activity. Businesses select activities or task depending on the goals of the

company, like enticing new consumers or involved in a new business line, then assign

spending by arranging activities as per priorities. This procedure is very beneficial for the

companies with huge history from scratch.

Checking the Suitability of Activity Based Costing for David Jones

From the above analysis, it has been identified that activity based budgeting is beneficial for

those organization that has a long history and regular make changes in its processes as well as

activities. David Jones is one of the well-known chains of an upmarket department store in

Australia comprised of different departments and activities. David Jones is regularly

experiencing the changes in its business such as the addition of different types of products in

its offering, material change, expansion in the different market, etc. Moreover, it has a very

long list of future planning and one of them is to open its second store in the New Zealand

market with different as well as quality offerings (Inside Retail, 2018). This reflects that the

company is regularly gets affected by altering the cost of material, infrastructure, the rate of

land, etc. that disturbs the budget of the company. Therefore, it can be suggested that in order

to operate effectively with the frequent changes in the market as well as in the business

operations David Jones need to avoid its traditional budgeting system and must adopt activity

based budgeting.

ABB budgeting will offer reliable and detailed information of the changing resources price to

the business. Moreover, before creating the budget this system perform proper analysis and

investigation of all the activities involved in the business to identify the actual cost that could

well as detailed information to manage the expenditures that take place to complete different

business activities (Surbhi, 2017). Moreover, ABB also provides detailed information that

offers various opportunities and data cross-analysis to the company. Unlike traditional

budgeting method, the ABB method analyses the present opportunities and assign resources

precisely to every activity. Businesses select activities or task depending on the goals of the

company, like enticing new consumers or involved in a new business line, then assign

spending by arranging activities as per priorities. This procedure is very beneficial for the

companies with huge history from scratch.

Checking the Suitability of Activity Based Costing for David Jones

From the above analysis, it has been identified that activity based budgeting is beneficial for

those organization that has a long history and regular make changes in its processes as well as

activities. David Jones is one of the well-known chains of an upmarket department store in

Australia comprised of different departments and activities. David Jones is regularly

experiencing the changes in its business such as the addition of different types of products in

its offering, material change, expansion in the different market, etc. Moreover, it has a very

long list of future planning and one of them is to open its second store in the New Zealand

market with different as well as quality offerings (Inside Retail, 2018). This reflects that the

company is regularly gets affected by altering the cost of material, infrastructure, the rate of

land, etc. that disturbs the budget of the company. Therefore, it can be suggested that in order

to operate effectively with the frequent changes in the market as well as in the business

operations David Jones need to avoid its traditional budgeting system and must adopt activity

based budgeting.

ABB budgeting will offer reliable and detailed information of the changing resources price to

the business. Moreover, before creating the budget this system perform proper analysis and

investigation of all the activities involved in the business to identify the actual cost that could

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT ACCOUNTING 10

be incurred and irrelevant activities that can be eliminated from the process. Elimination of

irrelevant activities also supports in saving the cost that eventually could be used in the

business for the production of the service or product. Besides this, activity based budgeting

delivers genuine data in terms of a number of cost declines defined by the cost upgrading

initiatives, thus offering auditors another standpoint to the costs (Hansen, Mowen and Guan,

2007). This reflects that the Activity-Based Budgeting can add something to the growth and

performance of the business in different industries. Moreover, if activities based budgeting

will be adopted within the financial system of the David Jones then the managers of the

business could look at the business as one single system from the initial stage to the last

stage, in place of individual departments. As the aim of the company is to offer quality to its

customers due to its customer-centric approach activity based budgeting will help in

maintaining the consumer focus culture. This system of budgeting will also make the

strategic planning easier when there will be the only motive to satisfy the customer (Julyan,

2018).

One of the major advantages that could be observed after adopting activity based budgeting

in the business is it encourages team spirit among employees of the company (Căpuşneanu,

Topor and Rof, 2013). David Jones Limited is experiencing huge competition from its strong

rival i.e. Myer because it frames different strategies to attract customers and increase its

customer base. In order to deal with this and gain the competitive advantage against its rival

activity based costing will help the company in planning a precise budget with the help of

detailed research and involvement of top management. David Jones is one of the strongest

players of the Australian market with maximum funds and huge investments that reflect that

company can afford this budgeting system because it is a bit costly due to detailed procedure

of the system.

be incurred and irrelevant activities that can be eliminated from the process. Elimination of

irrelevant activities also supports in saving the cost that eventually could be used in the

business for the production of the service or product. Besides this, activity based budgeting

delivers genuine data in terms of a number of cost declines defined by the cost upgrading

initiatives, thus offering auditors another standpoint to the costs (Hansen, Mowen and Guan,

2007). This reflects that the Activity-Based Budgeting can add something to the growth and

performance of the business in different industries. Moreover, if activities based budgeting

will be adopted within the financial system of the David Jones then the managers of the

business could look at the business as one single system from the initial stage to the last

stage, in place of individual departments. As the aim of the company is to offer quality to its

customers due to its customer-centric approach activity based budgeting will help in

maintaining the consumer focus culture. This system of budgeting will also make the

strategic planning easier when there will be the only motive to satisfy the customer (Julyan,

2018).

One of the major advantages that could be observed after adopting activity based budgeting

in the business is it encourages team spirit among employees of the company (Căpuşneanu,

Topor and Rof, 2013). David Jones Limited is experiencing huge competition from its strong

rival i.e. Myer because it frames different strategies to attract customers and increase its

customer base. In order to deal with this and gain the competitive advantage against its rival

activity based costing will help the company in planning a precise budget with the help of

detailed research and involvement of top management. David Jones is one of the strongest

players of the Australian market with maximum funds and huge investments that reflect that

company can afford this budgeting system because it is a bit costly due to detailed procedure

of the system.

MANAGEMENT ACCOUNTING 11

Conclusion

The technique of management accounting i.e. Activity based budgeting is not a new concept

but it is an effective technique that could change the image of the company in the market. It

supports business in getting proper data and information of the capabilities it possesses to

compete in the market. The above report has highlighted all the significant information that is

required to understand the benefits of the budgeting system and attract businesses to adopt it

for their growth. From the analysis, it has been suggested that David Jones Limited must

adopt this system of budgeting in order to survive in the market for a longer time and manage

the cost of changing resources and activities in the business. In comparison to traditional

budgeting, activity based budgeting is much more reliable and valuable for the company to

increase the revenue and eliminate the unnecessary cost incurred in the business. Moreover,

activity based costing will not just analyze the future funds required for performing the

activities but it will also help the company in understanding the importance of each and every

activity involved in the business along with resources required to complete those activities.

However, ABB is a costly system of budgeting that cannot be afforded by any business

because it is long as well as costlier procedure. The report has also discussed the features of

this system that shows that ABB budgeting enhances the relationship between the company

and its stakeholders by eliminating the additional cost involved in the product that results in

lower cost of production as well as increased disposable income of the customers. Traditional

budgeting is different from activity based costing in terms of cost and time involved in

preparing the budget, assignment of cost to the activities, reliability, etc. In the end, the

suitability of activity based budgeting for David Jones Limited has been proofed by this

report with the help of relevant data.

Conclusion

The technique of management accounting i.e. Activity based budgeting is not a new concept

but it is an effective technique that could change the image of the company in the market. It

supports business in getting proper data and information of the capabilities it possesses to

compete in the market. The above report has highlighted all the significant information that is

required to understand the benefits of the budgeting system and attract businesses to adopt it

for their growth. From the analysis, it has been suggested that David Jones Limited must

adopt this system of budgeting in order to survive in the market for a longer time and manage

the cost of changing resources and activities in the business. In comparison to traditional

budgeting, activity based budgeting is much more reliable and valuable for the company to

increase the revenue and eliminate the unnecessary cost incurred in the business. Moreover,

activity based costing will not just analyze the future funds required for performing the

activities but it will also help the company in understanding the importance of each and every

activity involved in the business along with resources required to complete those activities.

However, ABB is a costly system of budgeting that cannot be afforded by any business

because it is long as well as costlier procedure. The report has also discussed the features of

this system that shows that ABB budgeting enhances the relationship between the company

and its stakeholders by eliminating the additional cost involved in the product that results in

lower cost of production as well as increased disposable income of the customers. Traditional

budgeting is different from activity based costing in terms of cost and time involved in

preparing the budget, assignment of cost to the activities, reliability, etc. In the end, the

suitability of activity based budgeting for David Jones Limited has been proofed by this

report with the help of relevant data.

MANAGEMENT ACCOUNTING 12

References

Bragg, S.M. (2016) Cost Accounting Fundamentals: Fifth Edition: Essential Concepts and

Examples 5th ed. Accounting Tools.

Căpuşneanu, S., Topor, D., and Rof, L.M. (2013) Implementation of Activity-Based

Budgeting method in the economic entities from mining industry of Romania. International

Journal of Academic Research in Accounting, Finance, and Management Sciences, 3(1), 26-

33.

CGMA (2013) Activity-Based Budgeting (ABB) [online]. Available from

https://www.cgma.org/resources/tools/essential-tools/activity-based-budgeting.html [accessed

23 September 2018]

CGMA (2013) Essential tools for management accountants [online]. Available from

https://www.cgma.org/resources/tools/essential-tools/list.html [accessed 23 September 2018]

David Jones (2018) About us [online]. Available from https://www.davidjones.com/about-us

[accessed 23 September 2018]

David Jones (2018) The Story Of David Jones [online]. Available from

https://www.davidjones.com/about-us/the-story-of-david-jones [accessed 23 September

2018]

Drury, C. (2008) Management and Cost Accounting 5th ed. U.S: Cengage Learning.

E-Finance (2018) Zero Based Vs. Activity Based Budgeting [online]. Available from

https://efinancemanagement.com/budgeting/zero-based/zero-based-vs-activity-based-

budgeting [accessed 23 September 2018]

References

Bragg, S.M. (2016) Cost Accounting Fundamentals: Fifth Edition: Essential Concepts and

Examples 5th ed. Accounting Tools.

Căpuşneanu, S., Topor, D., and Rof, L.M. (2013) Implementation of Activity-Based

Budgeting method in the economic entities from mining industry of Romania. International

Journal of Academic Research in Accounting, Finance, and Management Sciences, 3(1), 26-

33.

CGMA (2013) Activity-Based Budgeting (ABB) [online]. Available from

https://www.cgma.org/resources/tools/essential-tools/activity-based-budgeting.html [accessed

23 September 2018]

CGMA (2013) Essential tools for management accountants [online]. Available from

https://www.cgma.org/resources/tools/essential-tools/list.html [accessed 23 September 2018]

David Jones (2018) About us [online]. Available from https://www.davidjones.com/about-us

[accessed 23 September 2018]

David Jones (2018) The Story Of David Jones [online]. Available from

https://www.davidjones.com/about-us/the-story-of-david-jones [accessed 23 September

2018]

Drury, C. (2008) Management and Cost Accounting 5th ed. U.S: Cengage Learning.

E-Finance (2018) Zero Based Vs. Activity Based Budgeting [online]. Available from

https://efinancemanagement.com/budgeting/zero-based/zero-based-vs-activity-based-

budgeting [accessed 23 September 2018]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 13

Hansen, D., Mowen, M., and Guan, L. (2007) Cost Management: Accounting and Control 6th

ed. U.S: Cengage Learning.

Huynh, T., and Huynh, H. (2013) Integration of activity-based budgeting and activity-based

management. International Journal of Economics, Finance and Management Sciences, 1(4),

181-185.

IBIS World (2013) James Richardson Corporation Pty Ltd - Profile Company Report

Australia [online]. Available from https://www.ibisworld.com.au/australian-company-

research-reports/retail-trade/james-richardson-corporation-pty-ltd-company.html [accessed

23 September 2018]

Inside Retail (2018) David Jones continues international expansion [online]. Available from

https://www.insideretail.com.au/news/david-jones-continues-international-expansion-201802

[accessed 23 September 2018]

Julyan (2018) Benefits of Activity Based Budgeting [online]. Available from

http://www.julyan.biz/benefits-of-activity-based-budgeting/ [accessed 23 September 2018]

Moustafa, E. (2005) An Application of Activity-Based-Budgeting in Shared Service

Departments and Its Perceived Benefits and Barriers under Low-IT Environment Conditions.

Journal of Economic & Administrative Sciences, 21(1), 42-70.

Nørreklit, H. (2017) A Philosophy of Management Accounting: A Pragmatic Constructivist

Approach 1st ed. U.K: Taylor & Francis.

Oneshko, S.V., and Boiko, M.O. (2016) Activity-Based Budgeting As A Management Tool Of

Economic Security Of Stevedoring Company [online]. Available from

https://economics.opu.ua/files/archive/2016/No3/134.pdf [accessed 23 September 2018]

Hansen, D., Mowen, M., and Guan, L. (2007) Cost Management: Accounting and Control 6th

ed. U.S: Cengage Learning.

Huynh, T., and Huynh, H. (2013) Integration of activity-based budgeting and activity-based

management. International Journal of Economics, Finance and Management Sciences, 1(4),

181-185.

IBIS World (2013) James Richardson Corporation Pty Ltd - Profile Company Report

Australia [online]. Available from https://www.ibisworld.com.au/australian-company-

research-reports/retail-trade/james-richardson-corporation-pty-ltd-company.html [accessed

23 September 2018]

Inside Retail (2018) David Jones continues international expansion [online]. Available from

https://www.insideretail.com.au/news/david-jones-continues-international-expansion-201802

[accessed 23 September 2018]

Julyan (2018) Benefits of Activity Based Budgeting [online]. Available from

http://www.julyan.biz/benefits-of-activity-based-budgeting/ [accessed 23 September 2018]

Moustafa, E. (2005) An Application of Activity-Based-Budgeting in Shared Service

Departments and Its Perceived Benefits and Barriers under Low-IT Environment Conditions.

Journal of Economic & Administrative Sciences, 21(1), 42-70.

Nørreklit, H. (2017) A Philosophy of Management Accounting: A Pragmatic Constructivist

Approach 1st ed. U.K: Taylor & Francis.

Oneshko, S.V., and Boiko, M.O. (2016) Activity-Based Budgeting As A Management Tool Of

Economic Security Of Stevedoring Company [online]. Available from

https://economics.opu.ua/files/archive/2016/No3/134.pdf [accessed 23 September 2018]

MANAGEMENT ACCOUNTING 14

Pietrzak, Z. (2013) Traditional versus Activity-based Budgeting in Non-manufacturing

Companies. Social Science Journal, 4(82), 26-32.

Shane, J.M. (2018) Activity-Based Budgeting: Creating a Nexus between Workload and Costs

[online]. Available from https://www.eccu.org/assets/general/Activity-Based-Budgeting-by-

Jon-Shane.pdf [accessed 23 September 2018]

Smith, N. (2018) Operating Budget vs. Activities Based Budget [online]. Available from

https://smallbusiness.chron.com/operating-budget-vs-activities-based-budget-72164.html

[accessed 23 September 2018]

Surbhi, S. (2017) Difference Between Traditional Budgeting and Zero-Based Budgeting

[online]. Available from https://keydifferences.com/difference-between-traditional-and-zero-

based-budgeting.html [accessed 23 September 2018]

Woolworths Holding (2018) Our Purpose, Vision And Values [online]. Available from

https://www.woolworthsholdings.co.za/overview/our-purpose-vision-and-values/ [accessed

23 September 2018]

Pietrzak, Z. (2013) Traditional versus Activity-based Budgeting in Non-manufacturing

Companies. Social Science Journal, 4(82), 26-32.

Shane, J.M. (2018) Activity-Based Budgeting: Creating a Nexus between Workload and Costs

[online]. Available from https://www.eccu.org/assets/general/Activity-Based-Budgeting-by-

Jon-Shane.pdf [accessed 23 September 2018]

Smith, N. (2018) Operating Budget vs. Activities Based Budget [online]. Available from

https://smallbusiness.chron.com/operating-budget-vs-activities-based-budget-72164.html

[accessed 23 September 2018]

Surbhi, S. (2017) Difference Between Traditional Budgeting and Zero-Based Budgeting

[online]. Available from https://keydifferences.com/difference-between-traditional-and-zero-

based-budgeting.html [accessed 23 September 2018]

Woolworths Holding (2018) Our Purpose, Vision And Values [online]. Available from

https://www.woolworthsholdings.co.za/overview/our-purpose-vision-and-values/ [accessed

23 September 2018]

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.