Management Accounting Report: Analyzing Corporate Holiday Packages

VerifiedAdded on 2023/06/14

|15

|2507

|335

Report

AI Summary

This management accounting report analyzes the profitability of corporate holiday packages offered by Asian Adventure Holidays. It evaluates the Bali Adventure, Thailand Discovery, and Malaysian Orienteering packages, examining sales revenue, direct costs, and overhead expenses. The report critiques the current method of profitability calculation and suggests improvements, focusing on individual package characteristics. It also addresses economic order quantity (EOQ) calculations, supply chain management (SCM), customer relationship management (CRM), and quality control costs, providing recommendations for optimizing operations and enhancing profitability. The document also explores different air filtration systems for a new laboratory, recommending the HEPA filtered system based on cost and waste considerations. Desklib provides this document and many more solved assignments for students.

Running head: MANAGEMENT ACCOUNT

Management Accounting

Name of Student:

Name of University:

Author’s Note:

Management Accounting

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING

Table of Contents

Question One...................................................................................................................................3

Answer to Part A i...........................................................................................................................3

Answer to Part A ii..........................................................................................................................4

Answer to Part A iii.........................................................................................................................4

Answer to Part A iv.........................................................................................................................5

Question Two...................................................................................................................................5

Answer to Part A i...........................................................................................................................5

Answer to Part A ii..........................................................................................................................5

Answer to Part A iii.........................................................................................................................6

Answer to Part A iv.........................................................................................................................6

Answer to Part A v..........................................................................................................................6

Answer to Part A vi.........................................................................................................................7

Answer to Part A vii........................................................................................................................7

Answer to Part A viii a and viii b....................................................................................................8

Answer to Part A ix.........................................................................................................................8

Part B i.............................................................................................................................................9

Part B ii............................................................................................................................................9

Part B iii...........................................................................................................................................9

Part C i...........................................................................................................................................10

Part C ii..........................................................................................................................................10

Part C iii.........................................................................................................................................10

Question Three...............................................................................................................................10

Table of Contents

Question One...................................................................................................................................3

Answer to Part A i...........................................................................................................................3

Answer to Part A ii..........................................................................................................................4

Answer to Part A iii.........................................................................................................................4

Answer to Part A iv.........................................................................................................................5

Question Two...................................................................................................................................5

Answer to Part A i...........................................................................................................................5

Answer to Part A ii..........................................................................................................................5

Answer to Part A iii.........................................................................................................................6

Answer to Part A iv.........................................................................................................................6

Answer to Part A v..........................................................................................................................6

Answer to Part A vi.........................................................................................................................7

Answer to Part A vii........................................................................................................................7

Answer to Part A viii a and viii b....................................................................................................8

Answer to Part A ix.........................................................................................................................8

Part B i.............................................................................................................................................9

Part B ii............................................................................................................................................9

Part B iii...........................................................................................................................................9

Part C i...........................................................................................................................................10

Part C ii..........................................................................................................................................10

Part C iii.........................................................................................................................................10

Question Three...............................................................................................................................10

2MANAGEMENT ACCOUNTING

Part A i...........................................................................................................................................10

Part A ii..........................................................................................................................................11

Part A iii.........................................................................................................................................11

Part Bi............................................................................................................................................12

Part B ii..........................................................................................................................................12

References......................................................................................................................................13

Part A i...........................................................................................................................................10

Part A ii..........................................................................................................................................11

Part A iii.........................................................................................................................................11

Part Bi............................................................................................................................................12

Part B ii..........................................................................................................................................12

References......................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING

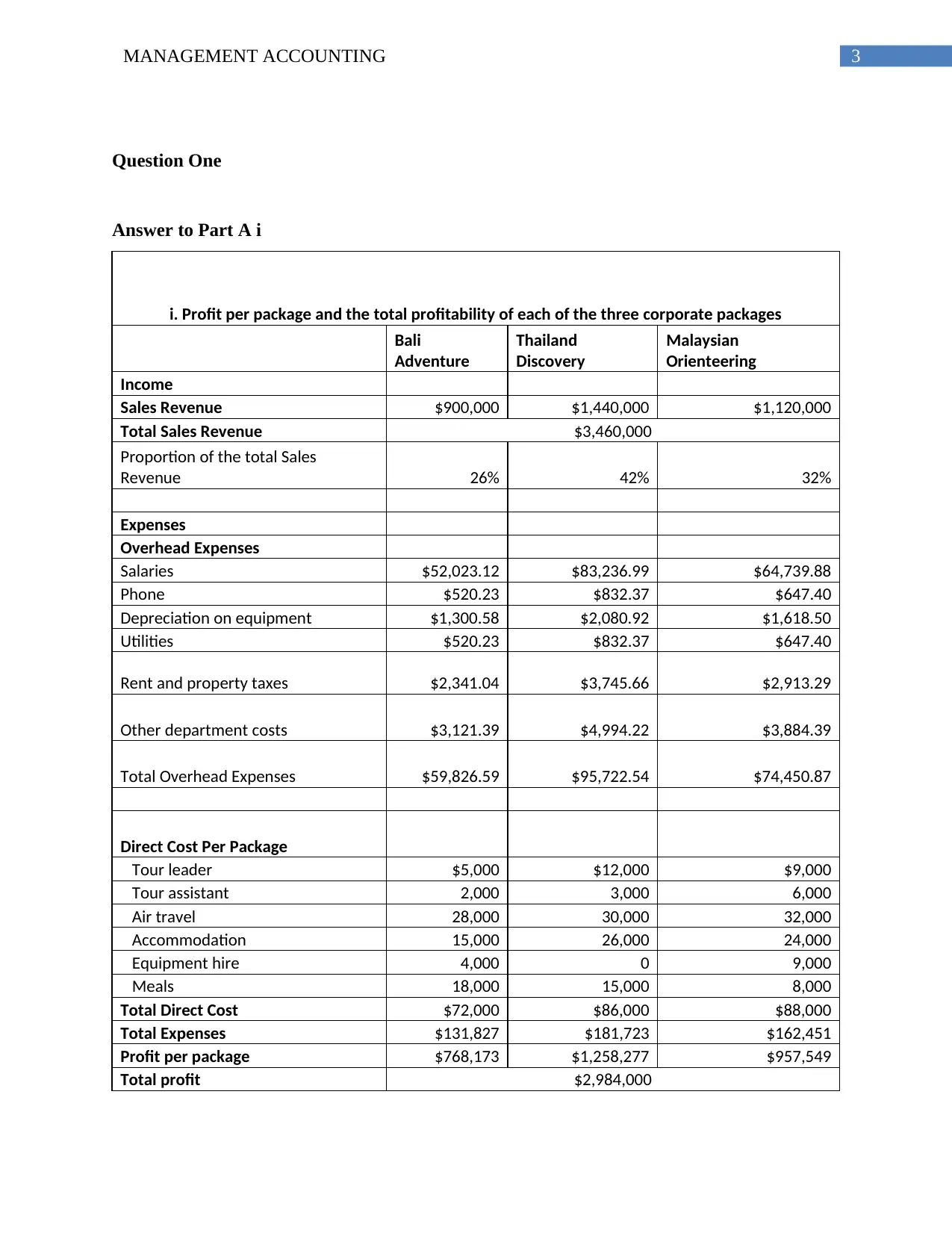

Question One

Answer to Part A i

i. Profit per package and the total profitability of each of the three corporate packages

Bali

Adventure

Thailand

Discovery

Malaysian

Orienteering

Income

Sales Revenue $900,000 $1,440,000 $1,120,000

Total Sales Revenue $3,460,000

Proportion of the total Sales

Revenue 26% 42% 32%

Expenses

Overhead Expenses

Salaries $52,023.12 $83,236.99 $64,739.88

Phone $520.23 $832.37 $647.40

Depreciation on equipment $1,300.58 $2,080.92 $1,618.50

Utilities $520.23 $832.37 $647.40

Rent and property taxes $2,341.04 $3,745.66 $2,913.29

Other department costs $3,121.39 $4,994.22 $3,884.39

Total Overhead Expenses $59,826.59 $95,722.54 $74,450.87

Direct Cost Per Package

Tour leader $5,000 $12,000 $9,000

Tour assistant 2,000 3,000 6,000

Air travel 28,000 30,000 32,000

Accommodation 15,000 26,000 24,000

Equipment hire 4,000 0 9,000

Meals 18,000 15,000 8,000

Total Direct Cost $72,000 $86,000 $88,000

Total Expenses $131,827 $181,723 $162,451

Profit per package $768,173 $1,258,277 $957,549

Total profit $2,984,000

Question One

Answer to Part A i

i. Profit per package and the total profitability of each of the three corporate packages

Bali

Adventure

Thailand

Discovery

Malaysian

Orienteering

Income

Sales Revenue $900,000 $1,440,000 $1,120,000

Total Sales Revenue $3,460,000

Proportion of the total Sales

Revenue 26% 42% 32%

Expenses

Overhead Expenses

Salaries $52,023.12 $83,236.99 $64,739.88

Phone $520.23 $832.37 $647.40

Depreciation on equipment $1,300.58 $2,080.92 $1,618.50

Utilities $520.23 $832.37 $647.40

Rent and property taxes $2,341.04 $3,745.66 $2,913.29

Other department costs $3,121.39 $4,994.22 $3,884.39

Total Overhead Expenses $59,826.59 $95,722.54 $74,450.87

Direct Cost Per Package

Tour leader $5,000 $12,000 $9,000

Tour assistant 2,000 3,000 6,000

Air travel 28,000 30,000 32,000

Accommodation 15,000 26,000 24,000

Equipment hire 4,000 0 9,000

Meals 18,000 15,000 8,000

Total Direct Cost $72,000 $86,000 $88,000

Total Expenses $131,827 $181,723 $162,451

Profit per package $768,173 $1,258,277 $957,549

Total profit $2,984,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING

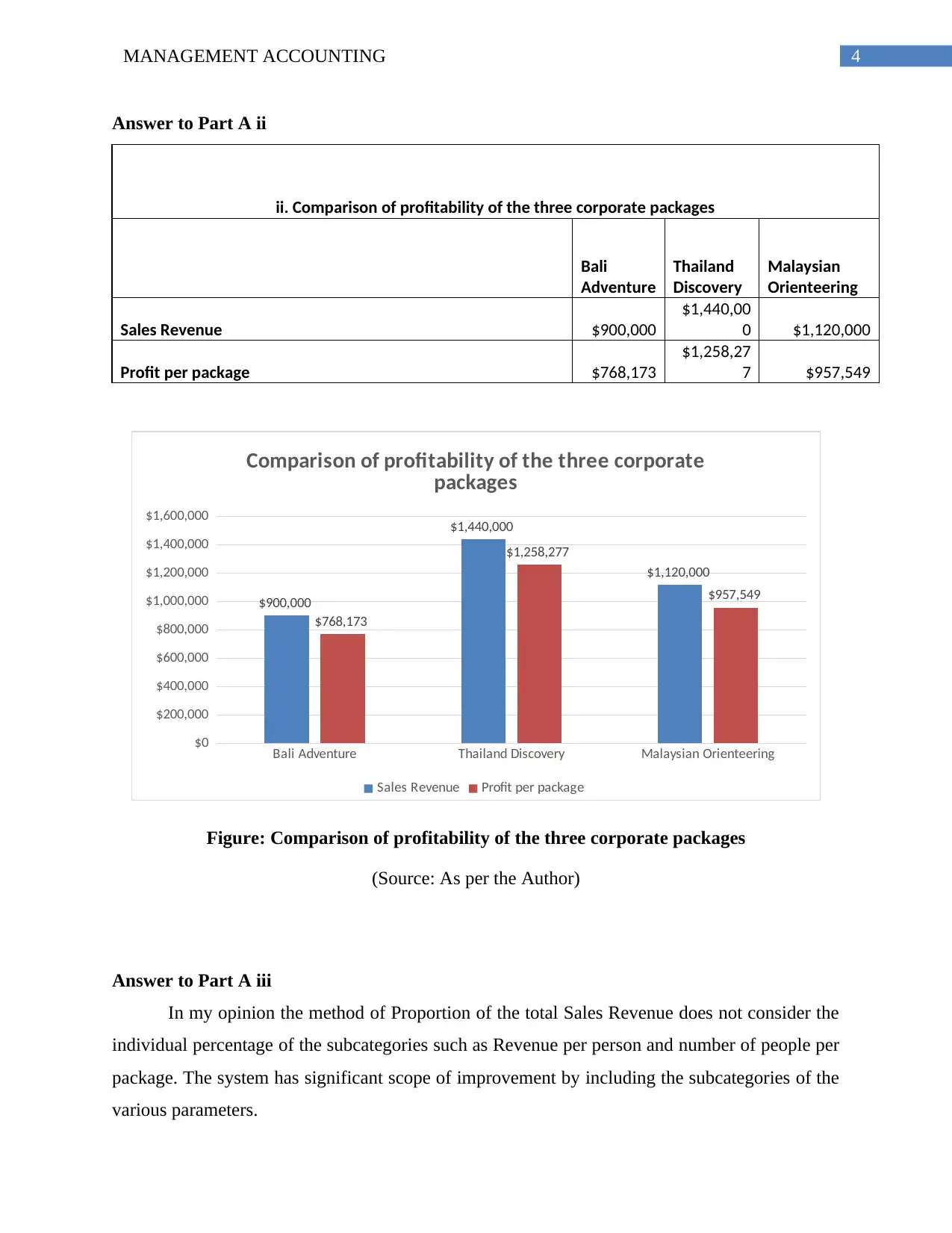

Answer to Part A ii

ii. Comparison of profitability of the three corporate packages

Bali

Adventure

Thailand

Discovery

Malaysian

Orienteering

Sales Revenue $900,000

$1,440,00

0 $1,120,000

Profit per package $768,173

$1,258,27

7 $957,549

Bali Adventure Thailand Discovery Malaysian Orienteering

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

$1,600,000

$900,000

$1,440,000

$1,120,000

$768,173

$1,258,277

$957,549

Comparison of profitability of the three corporate

packages

Sales Revenue Profit per package

Figure: Comparison of profitability of the three corporate packages

(Source: As per the Author)

Answer to Part A iii

In my opinion the method of Proportion of the total Sales Revenue does not consider the

individual percentage of the subcategories such as Revenue per person and number of people per

package. The system has significant scope of improvement by including the subcategories of the

various parameters.

Answer to Part A ii

ii. Comparison of profitability of the three corporate packages

Bali

Adventure

Thailand

Discovery

Malaysian

Orienteering

Sales Revenue $900,000

$1,440,00

0 $1,120,000

Profit per package $768,173

$1,258,27

7 $957,549

Bali Adventure Thailand Discovery Malaysian Orienteering

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

$1,600,000

$900,000

$1,440,000

$1,120,000

$768,173

$1,258,277

$957,549

Comparison of profitability of the three corporate

packages

Sales Revenue Profit per package

Figure: Comparison of profitability of the three corporate packages

(Source: As per the Author)

Answer to Part A iii

In my opinion the method of Proportion of the total Sales Revenue does not consider the

individual percentage of the subcategories such as Revenue per person and number of people per

package. The system has significant scope of improvement by including the subcategories of the

various parameters.

5MANAGEMENT ACCOUNTING

Answer to Part A iv

The main suggestion to the company has been seen with focusing more on improving the

sales of Bali Adventure package. This may be done by making changes in the target customer

and follow a competitive price strategy.

Question Two

Answer to Part A i

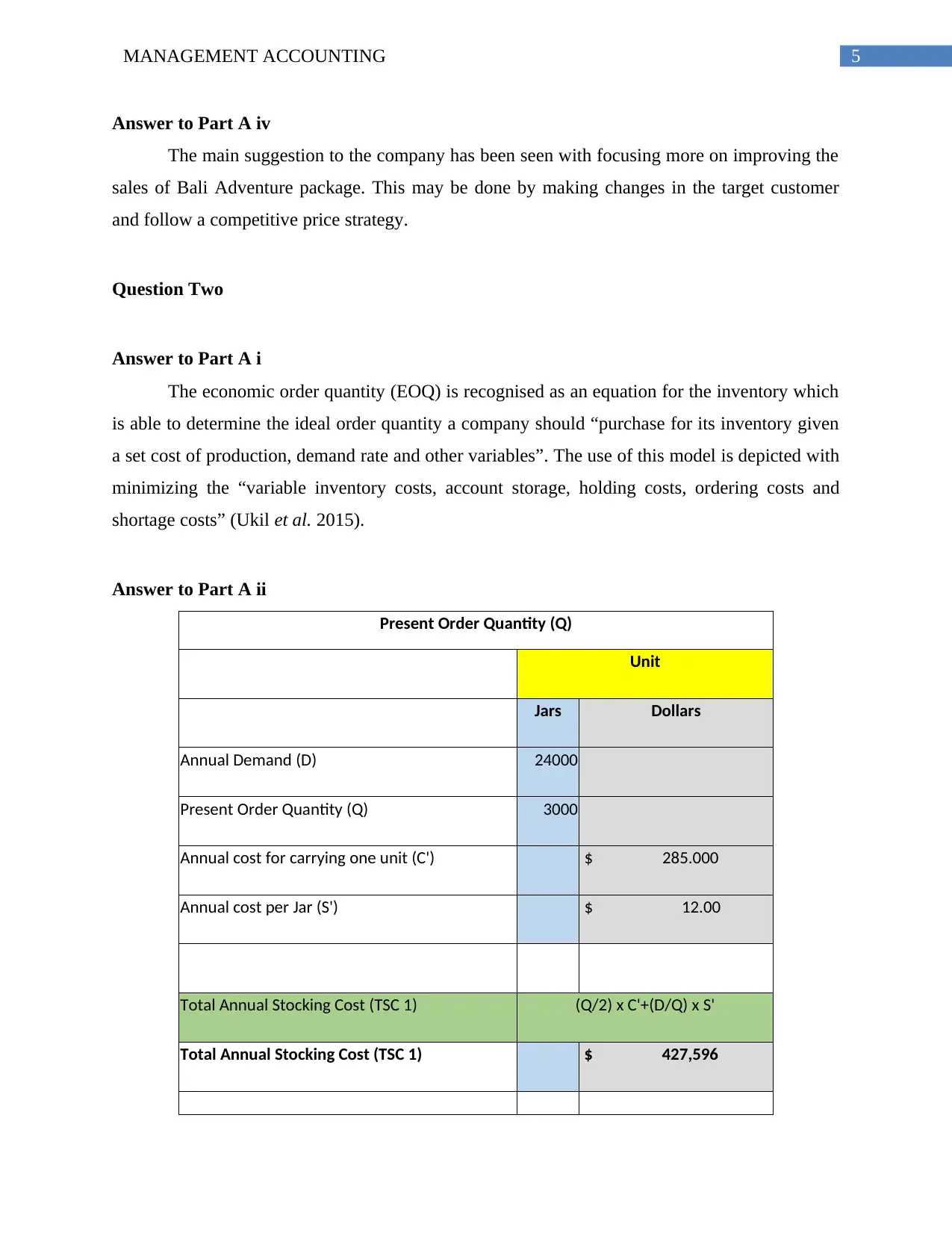

The economic order quantity (EOQ) is recognised as an equation for the inventory which

is able to determine the ideal order quantity a company should “purchase for its inventory given

a set cost of production, demand rate and other variables”. The use of this model is depicted with

minimizing the “variable inventory costs, account storage, holding costs, ordering costs and

shortage costs” (Ukil et al. 2015).

Answer to Part A ii

Present Order Quantity (Q)

Unit

Jars Dollars

Annual Demand (D) 24000

Present Order Quantity (Q) 3000

Annual cost for carrying one unit (C') $ 285.000

Annual cost per Jar (S') $ 12.00

Total Annual Stocking Cost (TSC 1) (Q/2) x C'+(D/Q) x S'

Total Annual Stocking Cost (TSC 1) $ 427,596

Answer to Part A iv

The main suggestion to the company has been seen with focusing more on improving the

sales of Bali Adventure package. This may be done by making changes in the target customer

and follow a competitive price strategy.

Question Two

Answer to Part A i

The economic order quantity (EOQ) is recognised as an equation for the inventory which

is able to determine the ideal order quantity a company should “purchase for its inventory given

a set cost of production, demand rate and other variables”. The use of this model is depicted with

minimizing the “variable inventory costs, account storage, holding costs, ordering costs and

shortage costs” (Ukil et al. 2015).

Answer to Part A ii

Present Order Quantity (Q)

Unit

Jars Dollars

Annual Demand (D) 24000

Present Order Quantity (Q) 3000

Annual cost for carrying one unit (C') $ 285.000

Annual cost per Jar (S') $ 12.00

Total Annual Stocking Cost (TSC 1) (Q/2) x C'+(D/Q) x S'

Total Annual Stocking Cost (TSC 1) $ 427,596

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING

Economic Order Quantity (EOQ) SQRT(2xDxS')/C

Economic Order Quantity (EOQ) 44.96

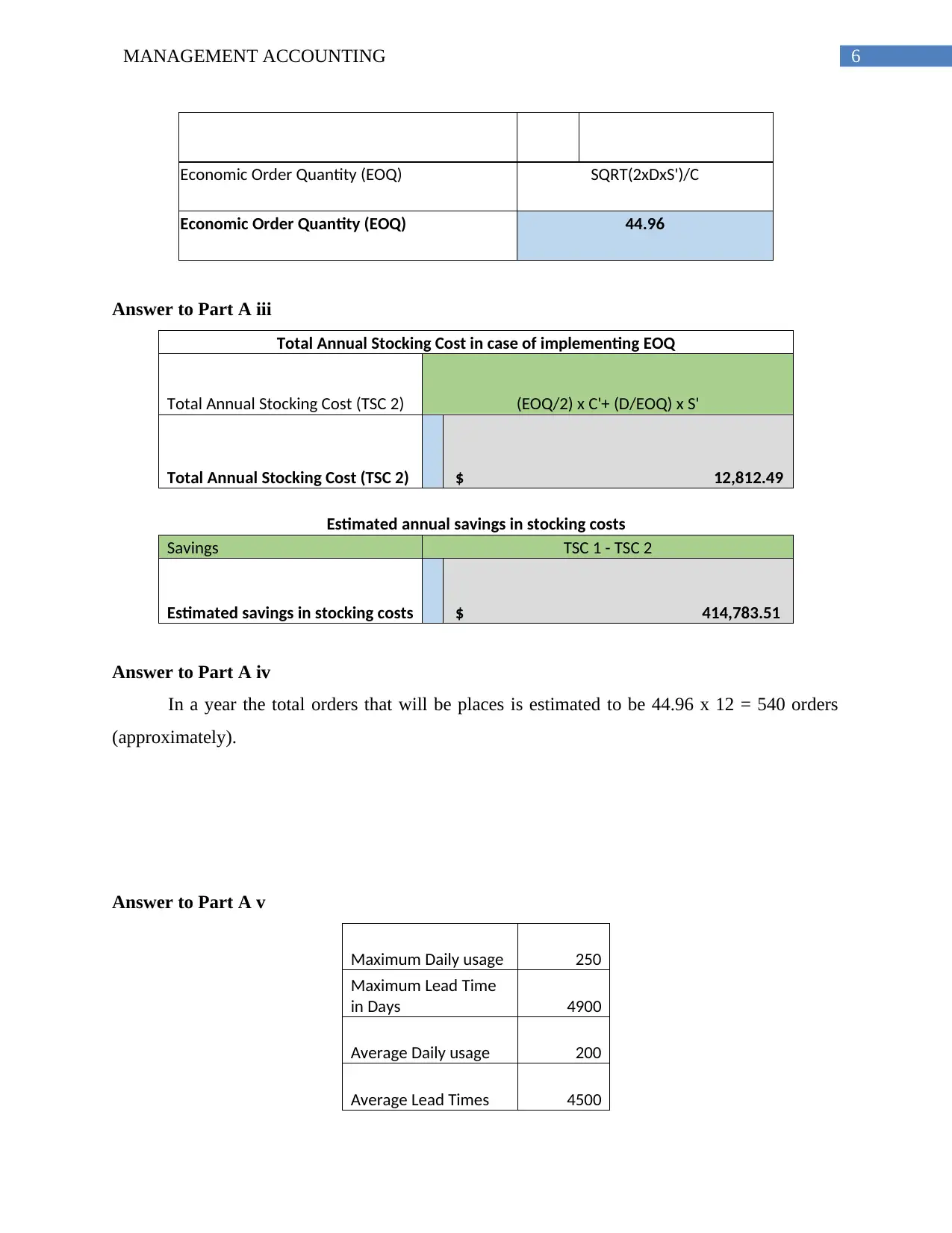

Answer to Part A iii

Total Annual Stocking Cost in case of implementing EOQ

Total Annual Stocking Cost (TSC 2) (EOQ/2) x C'+ (D/EOQ) x S'

Total Annual Stocking Cost (TSC 2) $ 12,812.49

Estimated annual savings in stocking costs

Savings TSC 1 - TSC 2

Estimated savings in stocking costs $ 414,783.51

Answer to Part A iv

In a year the total orders that will be places is estimated to be 44.96 x 12 = 540 orders

(approximately).

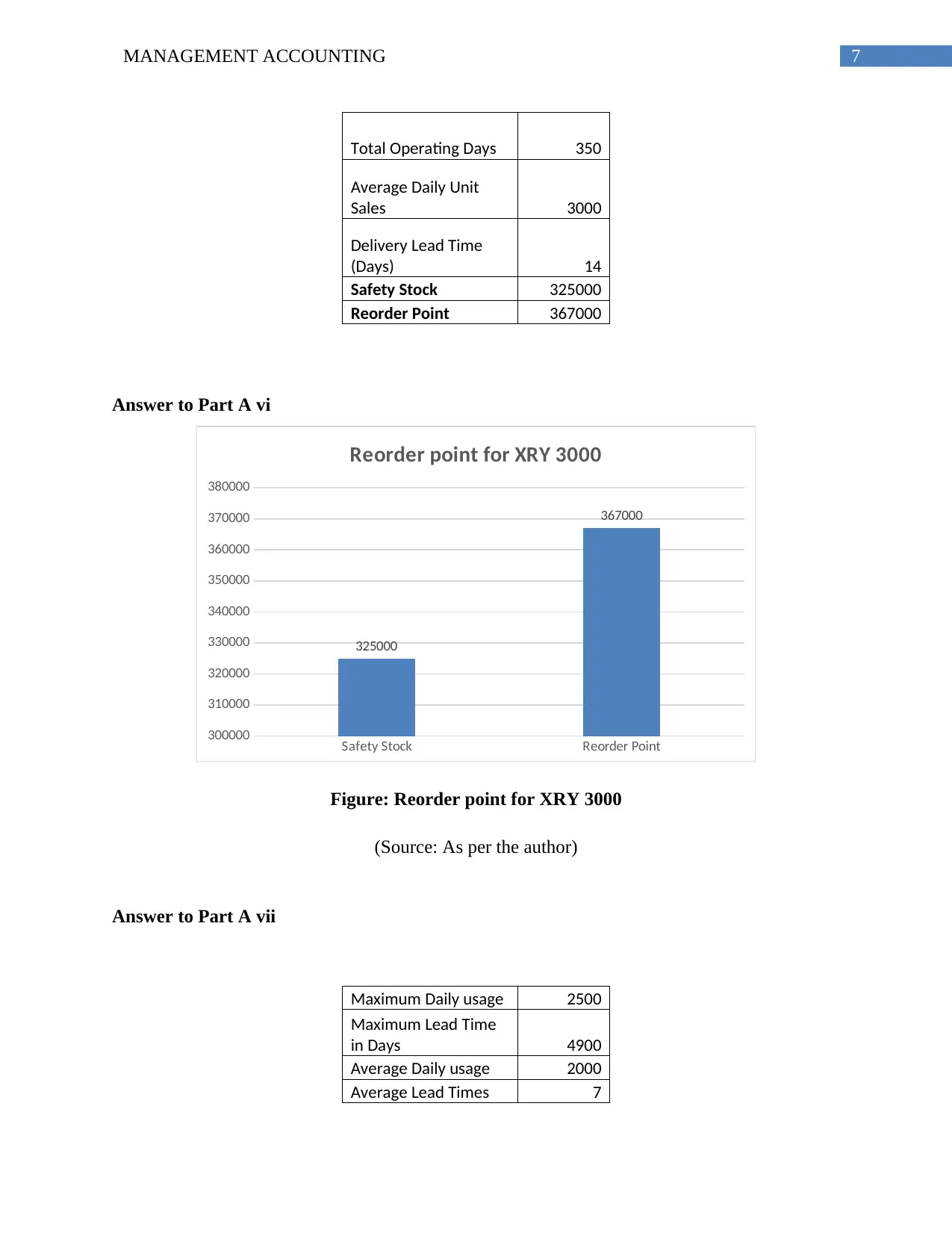

Answer to Part A v

Maximum Daily usage 250

Maximum Lead Time

in Days 4900

Average Daily usage 200

Average Lead Times 4500

Economic Order Quantity (EOQ) SQRT(2xDxS')/C

Economic Order Quantity (EOQ) 44.96

Answer to Part A iii

Total Annual Stocking Cost in case of implementing EOQ

Total Annual Stocking Cost (TSC 2) (EOQ/2) x C'+ (D/EOQ) x S'

Total Annual Stocking Cost (TSC 2) $ 12,812.49

Estimated annual savings in stocking costs

Savings TSC 1 - TSC 2

Estimated savings in stocking costs $ 414,783.51

Answer to Part A iv

In a year the total orders that will be places is estimated to be 44.96 x 12 = 540 orders

(approximately).

Answer to Part A v

Maximum Daily usage 250

Maximum Lead Time

in Days 4900

Average Daily usage 200

Average Lead Times 4500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING

Total Operating Days 350

Average Daily Unit

Sales 3000

Delivery Lead Time

(Days) 14

Safety Stock 325000

Reorder Point 367000

Answer to Part A vi

Safety Stock Reorder Point

300000

310000

320000

330000

340000

350000

360000

370000

380000

325000

367000

Reorder point for XRY 3000

Figure: Reorder point for XRY 3000

(Source: As per the author)

Answer to Part A vii

Maximum Daily usage 2500

Maximum Lead Time

in Days 4900

Average Daily usage 2000

Average Lead Times 7

Total Operating Days 350

Average Daily Unit

Sales 3000

Delivery Lead Time

(Days) 14

Safety Stock 325000

Reorder Point 367000

Answer to Part A vi

Safety Stock Reorder Point

300000

310000

320000

330000

340000

350000

360000

370000

380000

325000

367000

Reorder point for XRY 3000

Figure: Reorder point for XRY 3000

(Source: As per the author)

Answer to Part A vii

Maximum Daily usage 2500

Maximum Lead Time

in Days 4900

Average Daily usage 2000

Average Lead Times 7

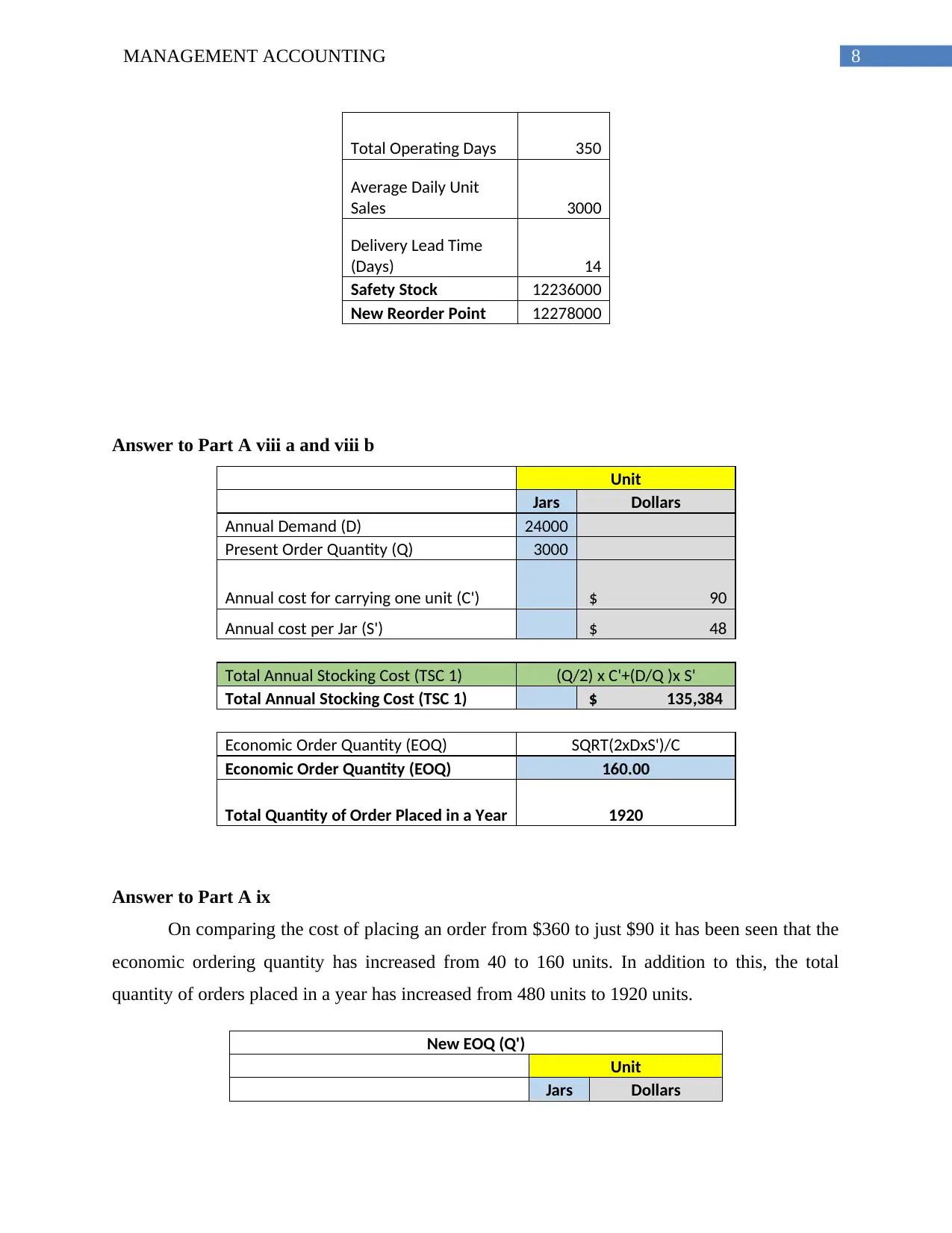

8MANAGEMENT ACCOUNTING

Total Operating Days 350

Average Daily Unit

Sales 3000

Delivery Lead Time

(Days) 14

Safety Stock 12236000

New Reorder Point 12278000

Answer to Part A viii a and viii b

Unit

Jars Dollars

Annual Demand (D) 24000

Present Order Quantity (Q) 3000

Annual cost for carrying one unit (C') $ 90

Annual cost per Jar (S') $ 48

Total Annual Stocking Cost (TSC 1) (Q/2) x C'+(D/Q )x S'

Total Annual Stocking Cost (TSC 1) $ 135,384

Economic Order Quantity (EOQ) SQRT(2xDxS')/C

Economic Order Quantity (EOQ) 160.00

Total Quantity of Order Placed in a Year 1920

Answer to Part A ix

On comparing the cost of placing an order from $360 to just $90 it has been seen that the

economic ordering quantity has increased from 40 to 160 units. In addition to this, the total

quantity of orders placed in a year has increased from 480 units to 1920 units.

New EOQ (Q')

Unit

Jars Dollars

Total Operating Days 350

Average Daily Unit

Sales 3000

Delivery Lead Time

(Days) 14

Safety Stock 12236000

New Reorder Point 12278000

Answer to Part A viii a and viii b

Unit

Jars Dollars

Annual Demand (D) 24000

Present Order Quantity (Q) 3000

Annual cost for carrying one unit (C') $ 90

Annual cost per Jar (S') $ 48

Total Annual Stocking Cost (TSC 1) (Q/2) x C'+(D/Q )x S'

Total Annual Stocking Cost (TSC 1) $ 135,384

Economic Order Quantity (EOQ) SQRT(2xDxS')/C

Economic Order Quantity (EOQ) 160.00

Total Quantity of Order Placed in a Year 1920

Answer to Part A ix

On comparing the cost of placing an order from $360 to just $90 it has been seen that the

economic ordering quantity has increased from 40 to 160 units. In addition to this, the total

quantity of orders placed in a year has increased from 480 units to 1920 units.

New EOQ (Q')

Unit

Jars Dollars

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING

Annual Demand (D) 24000

Present Order Quantity (Q) 3000

Annual cost for carrying one unit (C') $ 360

Annual cost per Jar (S') $ 12

Total Annual Stocking Cost (TSC 1) (Q/2) x C'+(D/Q) x S'

Total Annual Stocking Cost (TSC 1) $ 540,096

Economic Order Quantity (EOQ) SQRT(2xDxS')/C

Economic Order Quantity (EOQ) 40.00

Total Quantity of Order Placed in a Year 480

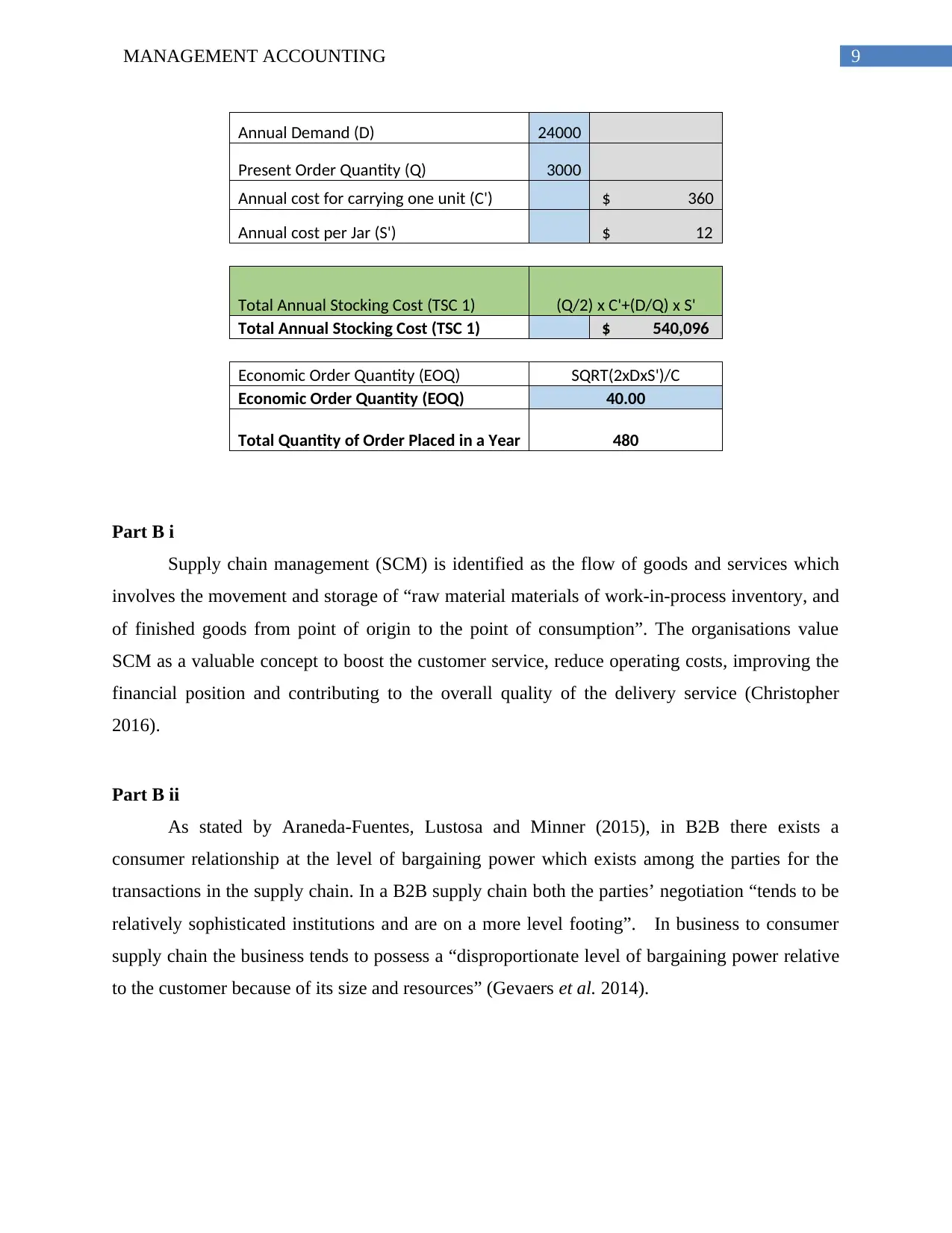

Part B i

Supply chain management (SCM) is identified as the flow of goods and services which

involves the movement and storage of “raw material materials of work-in-process inventory, and

of finished goods from point of origin to the point of consumption”. The organisations value

SCM as a valuable concept to boost the customer service, reduce operating costs, improving the

financial position and contributing to the overall quality of the delivery service (Christopher

2016).

Part B ii

As stated by Araneda-Fuentes, Lustosa and Minner (2015), in B2B there exists a

consumer relationship at the level of bargaining power which exists among the parties for the

transactions in the supply chain. In a B2B supply chain both the parties’ negotiation “tends to be

relatively sophisticated institutions and are on a more level footing”. In business to consumer

supply chain the business tends to possess a “disproportionate level of bargaining power relative

to the customer because of its size and resources” (Gevaers et al. 2014).

Annual Demand (D) 24000

Present Order Quantity (Q) 3000

Annual cost for carrying one unit (C') $ 360

Annual cost per Jar (S') $ 12

Total Annual Stocking Cost (TSC 1) (Q/2) x C'+(D/Q) x S'

Total Annual Stocking Cost (TSC 1) $ 540,096

Economic Order Quantity (EOQ) SQRT(2xDxS')/C

Economic Order Quantity (EOQ) 40.00

Total Quantity of Order Placed in a Year 480

Part B i

Supply chain management (SCM) is identified as the flow of goods and services which

involves the movement and storage of “raw material materials of work-in-process inventory, and

of finished goods from point of origin to the point of consumption”. The organisations value

SCM as a valuable concept to boost the customer service, reduce operating costs, improving the

financial position and contributing to the overall quality of the delivery service (Christopher

2016).

Part B ii

As stated by Araneda-Fuentes, Lustosa and Minner (2015), in B2B there exists a

consumer relationship at the level of bargaining power which exists among the parties for the

transactions in the supply chain. In a B2B supply chain both the parties’ negotiation “tends to be

relatively sophisticated institutions and are on a more level footing”. In business to consumer

supply chain the business tends to possess a “disproportionate level of bargaining power relative

to the customer because of its size and resources” (Gevaers et al. 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING

Part B iii

It is important for organisations to create collaborative relationships with suppliers to link

the network in the right way. The “placing relationships at the centre of supply chain

management allows for a more collaborative and effective dynamic performance for the

companies”. The best supply chains relationships are based on value and consistent adherence to

the same. These values are based on factors such as “services, quality, on-time deliveries, returns

management, or some combination of these”. Moreover, “long-term supply chain collaboration”

are the cost savings that result from routinized procedures and reduction in the indirect costs

(Fawcett et al. 2015).

Part C i

Customer Relationship Management is identified as a practice to analyse and manage

customer interactions and data in the entire customer lifecycle, with the aim of improving

customer service relationship, retaining the customers and achieve sales growth (Khodakarami

and Chan 2014).

Part C ii

The application of the CRM will be conducive in understanding the technical drawbacks

in the system and will provide Mitty Pty Ltd to take a step forward in increasing the sales

growth.

Part C iii

The use of e-commerce will be conducive in sourcing the products at a much cheaper

price in compared to the conventional methods. This will also allow the company to source the

vendors of the raw materials who will provide the best value (Qureshi et al. 2016.)

Part B iii

It is important for organisations to create collaborative relationships with suppliers to link

the network in the right way. The “placing relationships at the centre of supply chain

management allows for a more collaborative and effective dynamic performance for the

companies”. The best supply chains relationships are based on value and consistent adherence to

the same. These values are based on factors such as “services, quality, on-time deliveries, returns

management, or some combination of these”. Moreover, “long-term supply chain collaboration”

are the cost savings that result from routinized procedures and reduction in the indirect costs

(Fawcett et al. 2015).

Part C i

Customer Relationship Management is identified as a practice to analyse and manage

customer interactions and data in the entire customer lifecycle, with the aim of improving

customer service relationship, retaining the customers and achieve sales growth (Khodakarami

and Chan 2014).

Part C ii

The application of the CRM will be conducive in understanding the technical drawbacks

in the system and will provide Mitty Pty Ltd to take a step forward in increasing the sales

growth.

Part C iii

The use of e-commerce will be conducive in sourcing the products at a much cheaper

price in compared to the conventional methods. This will also allow the company to source the

vendors of the raw materials who will provide the best value (Qureshi et al. 2016.)

11MANAGEMENT ACCOUNTING

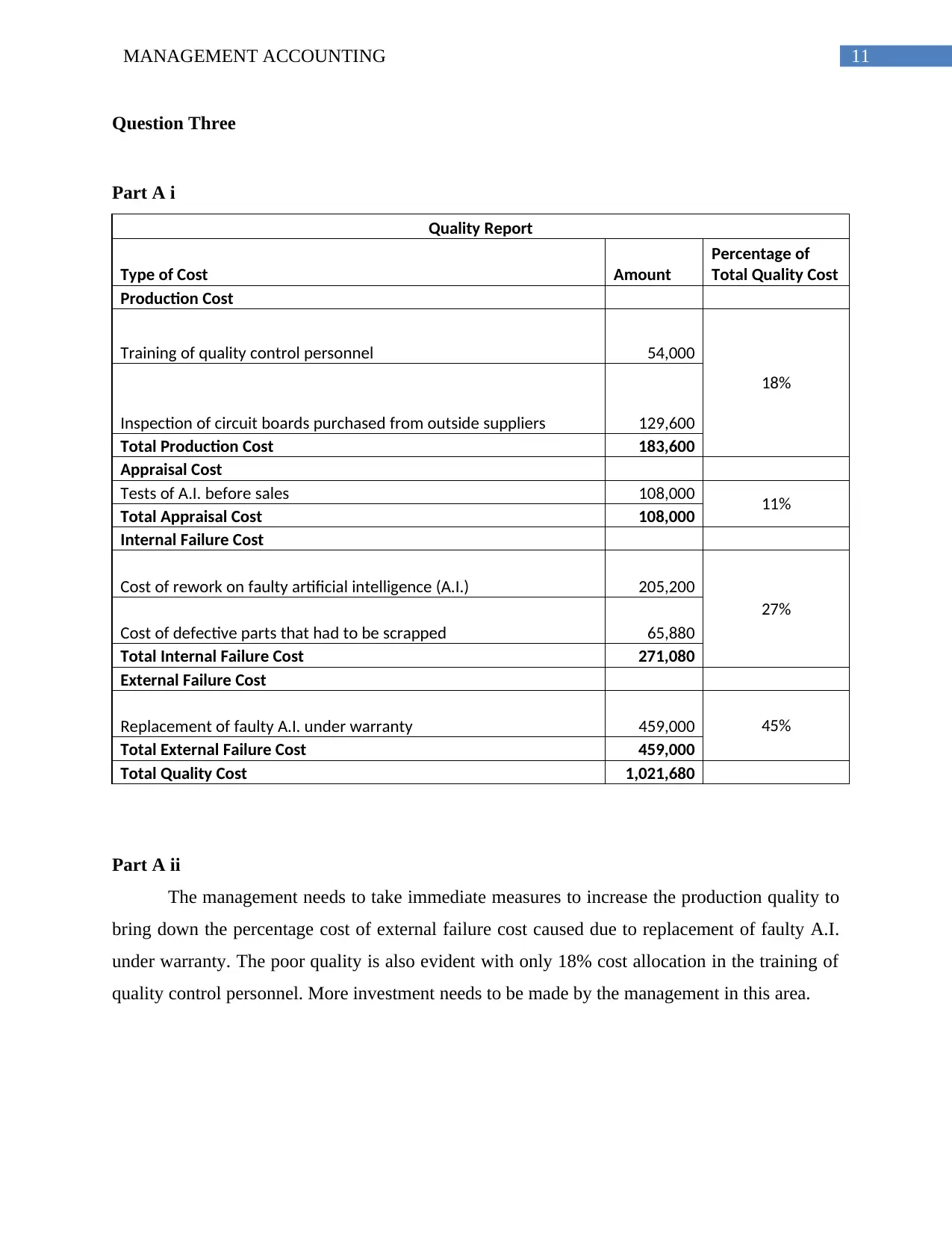

Question Three

Part A i

Quality Report

Type of Cost Amount

Percentage of

Total Quality Cost

Production Cost

Training of quality control personnel 54,000

18%

Inspection of circuit boards purchased from outside suppliers 129,600

Total Production Cost 183,600

Appraisal Cost

Tests of A.I. before sales 108,000 11%

Total Appraisal Cost 108,000

Internal Failure Cost

Cost of rework on faulty artificial intelligence (A.I.) 205,200

27%

Cost of defective parts that had to be scrapped 65,880

Total Internal Failure Cost 271,080

External Failure Cost

Replacement of faulty A.I. under warranty 459,000 45%

Total External Failure Cost 459,000

Total Quality Cost 1,021,680

Part A ii

The management needs to take immediate measures to increase the production quality to

bring down the percentage cost of external failure cost caused due to replacement of faulty A.I.

under warranty. The poor quality is also evident with only 18% cost allocation in the training of

quality control personnel. More investment needs to be made by the management in this area.

Question Three

Part A i

Quality Report

Type of Cost Amount

Percentage of

Total Quality Cost

Production Cost

Training of quality control personnel 54,000

18%

Inspection of circuit boards purchased from outside suppliers 129,600

Total Production Cost 183,600

Appraisal Cost

Tests of A.I. before sales 108,000 11%

Total Appraisal Cost 108,000

Internal Failure Cost

Cost of rework on faulty artificial intelligence (A.I.) 205,200

27%

Cost of defective parts that had to be scrapped 65,880

Total Internal Failure Cost 271,080

External Failure Cost

Replacement of faulty A.I. under warranty 459,000 45%

Total External Failure Cost 459,000

Total Quality Cost 1,021,680

Part A ii

The management needs to take immediate measures to increase the production quality to

bring down the percentage cost of external failure cost caused due to replacement of faulty A.I.

under warranty. The poor quality is also evident with only 18% cost allocation in the training of

quality control personnel. More investment needs to be made by the management in this area.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.