Management Accounting - Desklib

VerifiedAdded on 2023/06/18

|13

|1906

|101

AI Summary

This report covers various topics related to Management Accounting such as cost formula, income statement, variance analysis, and contribution margin ratio. It includes questions and answers related to financial activities recorded by a company in a financial year.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

INTRODUCTION...........................................................................................................................................4

QUESTION 1.................................................................................................................................................4

QUESTION 3.................................................................................................................................................5

QUESTION 4.................................................................................................................................................7

(b) Possible causes of variances...............................................................................................................9

(c) Explain how you would determine which variance to examine further in relation to a work

performance?..........................................................................................................................................9

QUESTION 6...............................................................................................................................................10

6. What is meant by a product’s contribution margin (CM) ratio? How is this ratio useful in planning

business operations? ............................................................................................................................11

REFERENCES..............................................................................................................................................12

INTRODUCTION...........................................................................................................................................4

QUESTION 1.................................................................................................................................................4

QUESTION 3.................................................................................................................................................5

QUESTION 4.................................................................................................................................................7

(b) Possible causes of variances...............................................................................................................9

(c) Explain how you would determine which variance to examine further in relation to a work

performance?..........................................................................................................................................9

QUESTION 6...............................................................................................................................................10

6. What is meant by a product’s contribution margin (CM) ratio? How is this ratio useful in planning

business operations? ............................................................................................................................11

REFERENCES..............................................................................................................................................12

INTRODUCTION

Management accounting, often defined as managerial accounting, is the process of giving

financial data and knowledge to executives in order to assist them in solving problems. This

activity is performed by an important core teams, but this is what distinguishes managerial

accounting from accrual analysis. Effective internal accounting exchanges analyses and

information (such as balanced sheets and payments) with corporate governance as part of this

procedure. Those documentations are used by leadership to determine knowledgeable and

methods to assess on business operations, organization, and management consulting. In this

report consist of different questions which are based on the financial activities that are recorded

by company in a financial year.

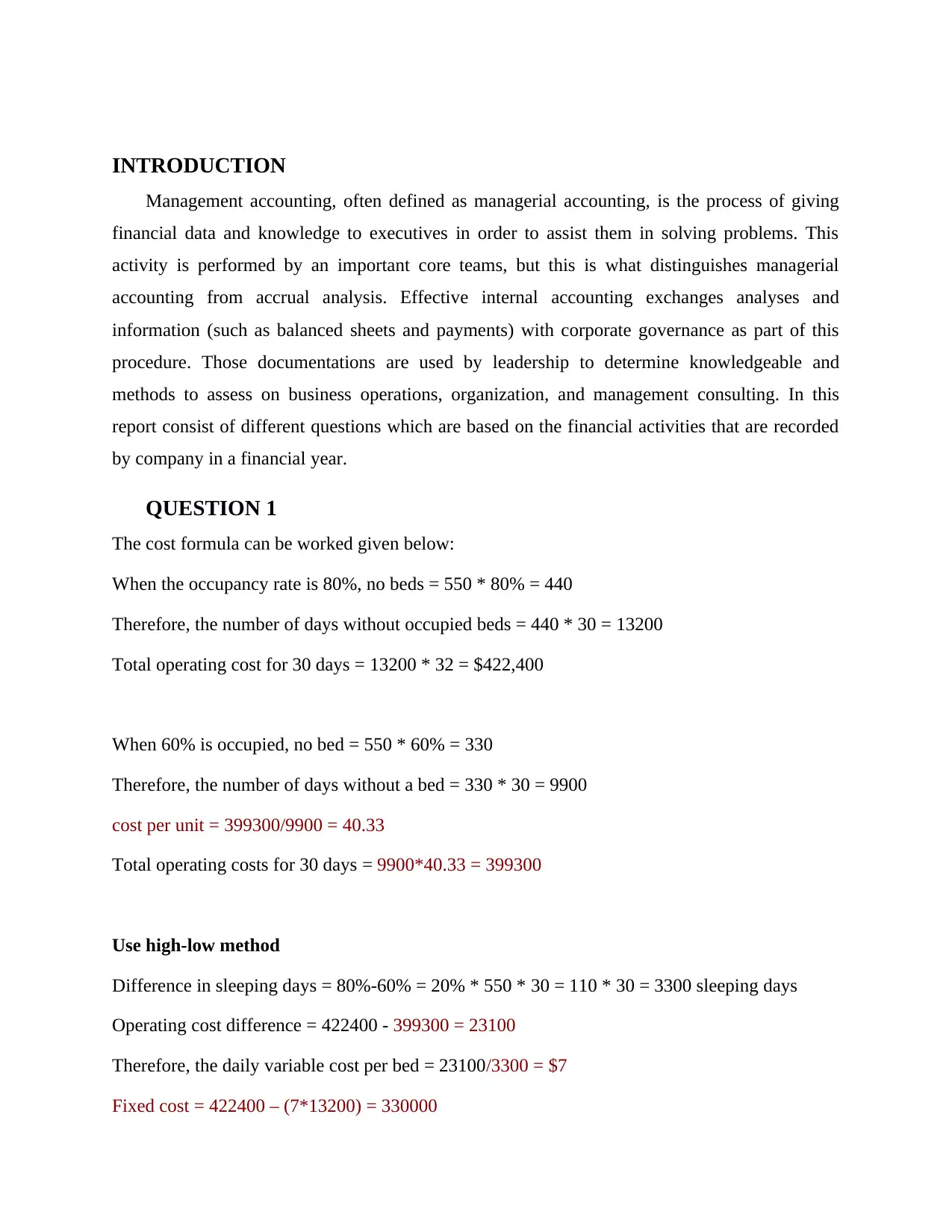

QUESTION 1

The cost formula can be worked given below:

When the occupancy rate is 80%, no beds = 550 * 80% = 440

Therefore, the number of days without occupied beds = 440 * 30 = 13200

Total operating cost for 30 days = 13200 * 32 = $422,400

When 60% is occupied, no bed = 550 * 60% = 330

Therefore, the number of days without a bed = 330 * 30 = 9900

cost per unit = 399300/9900 = 40.33

Total operating costs for 30 days = 9900*40.33 = 399300

Use high-low method

Difference in sleeping days = 80%-60% = 20% * 550 * 30 = 110 * 30 = 3300 sleeping days

Operating cost difference = 422400 - 399300 = 23100

Therefore, the daily variable cost per bed = 23100/3300 = $7

Fixed cost = 422400 – (7*13200) = 330000

Management accounting, often defined as managerial accounting, is the process of giving

financial data and knowledge to executives in order to assist them in solving problems. This

activity is performed by an important core teams, but this is what distinguishes managerial

accounting from accrual analysis. Effective internal accounting exchanges analyses and

information (such as balanced sheets and payments) with corporate governance as part of this

procedure. Those documentations are used by leadership to determine knowledgeable and

methods to assess on business operations, organization, and management consulting. In this

report consist of different questions which are based on the financial activities that are recorded

by company in a financial year.

QUESTION 1

The cost formula can be worked given below:

When the occupancy rate is 80%, no beds = 550 * 80% = 440

Therefore, the number of days without occupied beds = 440 * 30 = 13200

Total operating cost for 30 days = 13200 * 32 = $422,400

When 60% is occupied, no bed = 550 * 60% = 330

Therefore, the number of days without a bed = 330 * 30 = 9900

cost per unit = 399300/9900 = 40.33

Total operating costs for 30 days = 9900*40.33 = 399300

Use high-low method

Difference in sleeping days = 80%-60% = 20% * 550 * 30 = 110 * 30 = 3300 sleeping days

Operating cost difference = 422400 - 399300 = 23100

Therefore, the daily variable cost per bed = 23100/3300 = $7

Fixed cost = 422400 – (7*13200) = 330000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

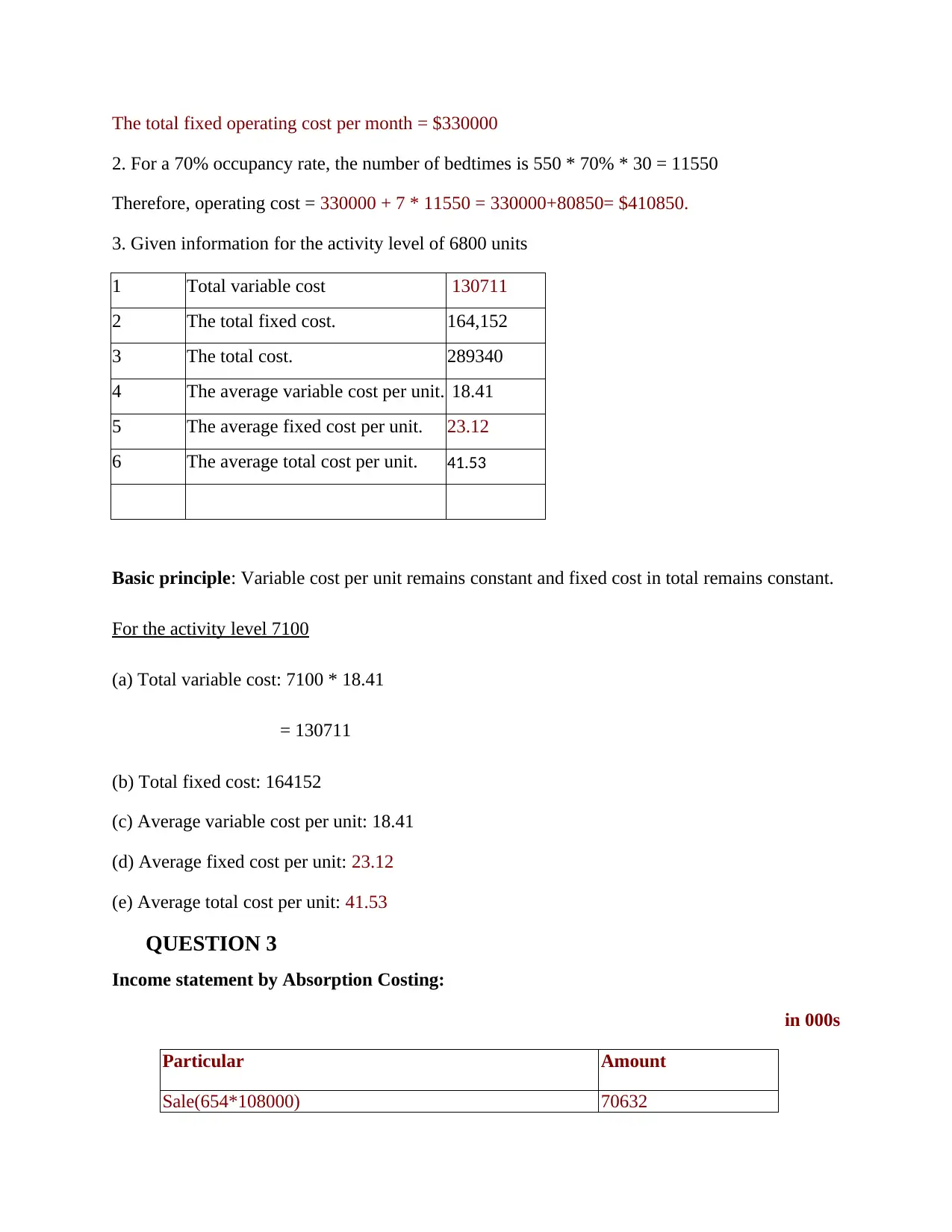

The total fixed operating cost per month = $330000

2. For a 70% occupancy rate, the number of bedtimes is 550 * 70% * 30 = 11550

Therefore, operating cost = 330000 + 7 * 11550 = 330000+80850= $410850.

3. Given information for the activity level of 6800 units

1 Total variable cost 130711

2 The total fixed cost. 164,152

3 The total cost. 289340

4 The average variable cost per unit. 18.41

5 The average fixed cost per unit. 23.12

6 The average total cost per unit. 41.53

Basic principle: Variable cost per unit remains constant and fixed cost in total remains constant.

For the activity level 7100

(a) Total variable cost: 7100 * 18.41

= 130711

(b) Total fixed cost: 164152

(c) Average variable cost per unit: 18.41

(d) Average fixed cost per unit: 23.12

(e) Average total cost per unit: 41.53

QUESTION 3

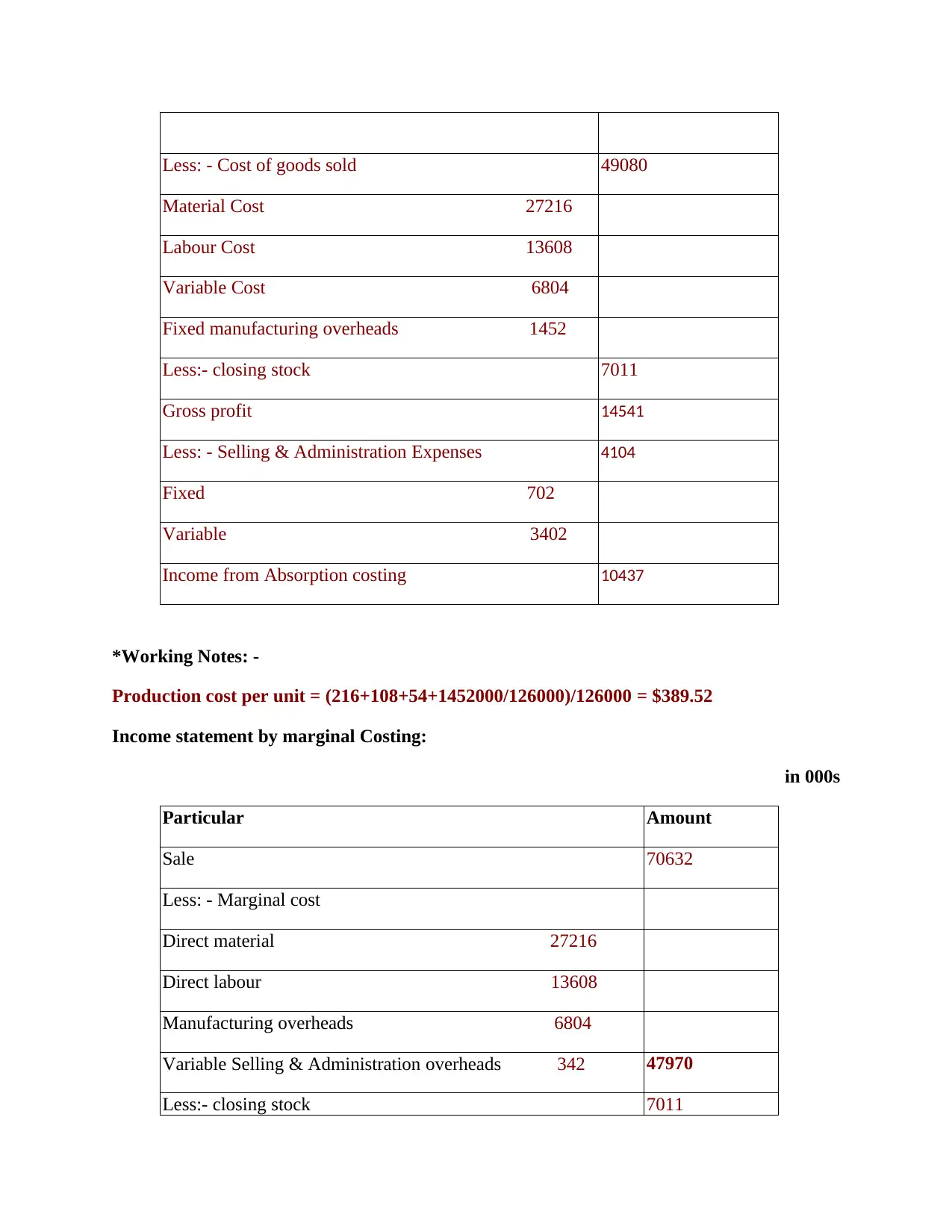

Income statement by Absorption Costing:

in 000s

Particular Amount

Sale(654*108000) 70632

2. For a 70% occupancy rate, the number of bedtimes is 550 * 70% * 30 = 11550

Therefore, operating cost = 330000 + 7 * 11550 = 330000+80850= $410850.

3. Given information for the activity level of 6800 units

1 Total variable cost 130711

2 The total fixed cost. 164,152

3 The total cost. 289340

4 The average variable cost per unit. 18.41

5 The average fixed cost per unit. 23.12

6 The average total cost per unit. 41.53

Basic principle: Variable cost per unit remains constant and fixed cost in total remains constant.

For the activity level 7100

(a) Total variable cost: 7100 * 18.41

= 130711

(b) Total fixed cost: 164152

(c) Average variable cost per unit: 18.41

(d) Average fixed cost per unit: 23.12

(e) Average total cost per unit: 41.53

QUESTION 3

Income statement by Absorption Costing:

in 000s

Particular Amount

Sale(654*108000) 70632

Less: - Cost of goods sold 49080

Material Cost 27216

Labour Cost 13608

Variable Cost 6804

Fixed manufacturing overheads 1452

Less:- closing stock 7011

Gross profit 14541

Less: - Selling & Administration Expenses 4104

Fixed 702

Variable 3402

Income from Absorption costing 10437

*Working Notes: -

Production cost per unit = (216+108+54+1452000/126000)/126000 = $389.52

Income statement by marginal Costing:

in 000s

Particular Amount

Sale 70632

Less: - Marginal cost

Direct material 27216

Direct labour 13608

Manufacturing overheads 6804

Variable Selling & Administration overheads 342 47970

Less:- closing stock 7011

Material Cost 27216

Labour Cost 13608

Variable Cost 6804

Fixed manufacturing overheads 1452

Less:- closing stock 7011

Gross profit 14541

Less: - Selling & Administration Expenses 4104

Fixed 702

Variable 3402

Income from Absorption costing 10437

*Working Notes: -

Production cost per unit = (216+108+54+1452000/126000)/126000 = $389.52

Income statement by marginal Costing:

in 000s

Particular Amount

Sale 70632

Less: - Marginal cost

Direct material 27216

Direct labour 13608

Manufacturing overheads 6804

Variable Selling & Administration overheads 342 47970

Less:- closing stock 7011

Contribution 15651

Less: - Fixed Cost 2154

Fixed manufacturing overheads 1452

Fixed selling & administrative Expenses 702

Income from Marginal costing 13497

QUESTION 4

(a) Material Price Variance:

Formula:

Material Price Variance = (Standard price – Actual price) * Actual quantity

= (10 - 9) * 63,000

= 63000 (F)

Material Usage Variance:

Formula:

Material Usage Variance = (Standard quantity – Actual quantity) * Standard Price

= (54675 – 63,000)* 10

= -83250 (U)

Labour Rate Variance:

Formula:

Labour Rate Variance = (Standard Rate - Actual Rate) * Actual Hours

= (7 – 9.6)* 45000

Less: - Fixed Cost 2154

Fixed manufacturing overheads 1452

Fixed selling & administrative Expenses 702

Income from Marginal costing 13497

QUESTION 4

(a) Material Price Variance:

Formula:

Material Price Variance = (Standard price – Actual price) * Actual quantity

= (10 - 9) * 63,000

= 63000 (F)

Material Usage Variance:

Formula:

Material Usage Variance = (Standard quantity – Actual quantity) * Standard Price

= (54675 – 63,000)* 10

= -83250 (U)

Labour Rate Variance:

Formula:

Labour Rate Variance = (Standard Rate - Actual Rate) * Actual Hours

= (7 – 9.6)* 45000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

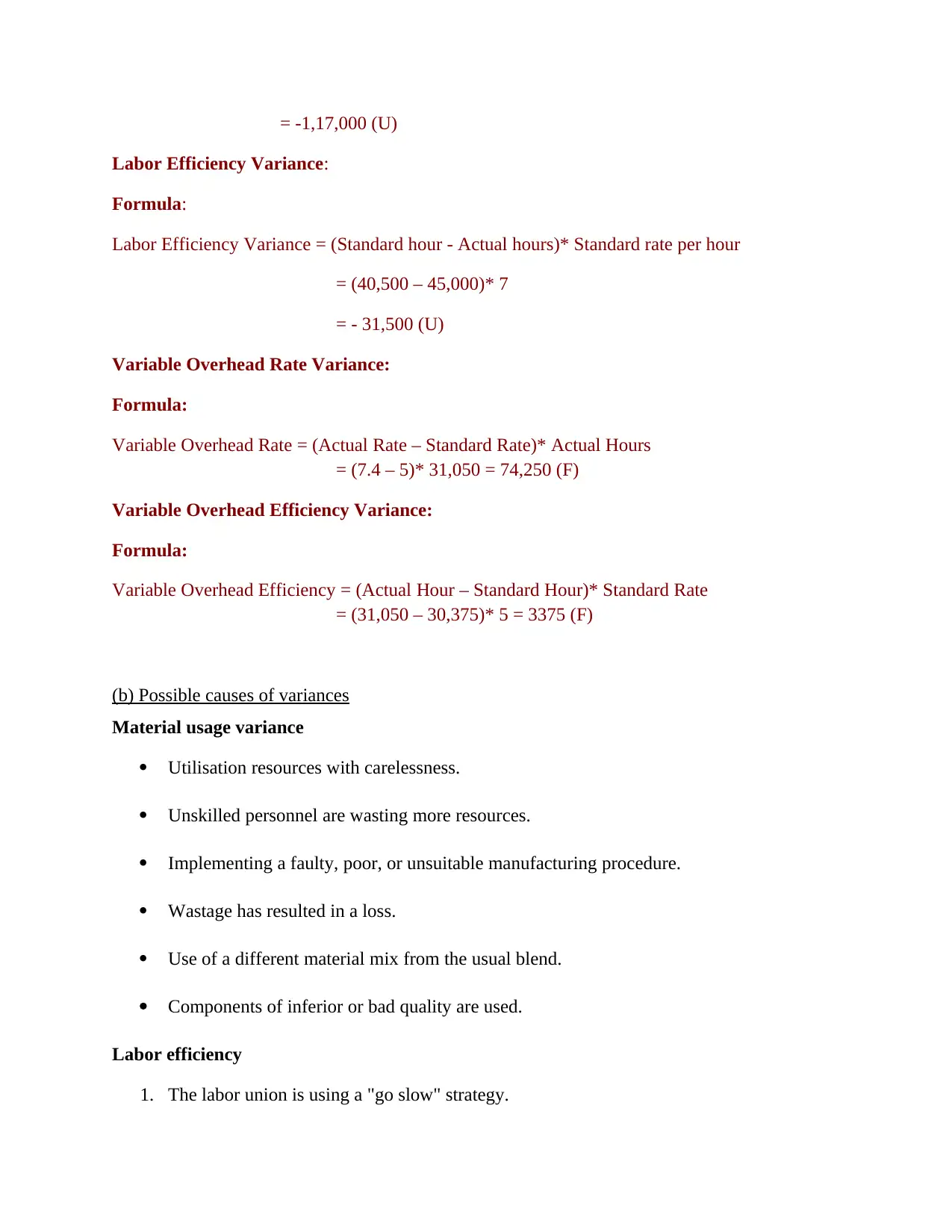

= -1,17,000 (U)

Labor Efficiency Variance:

Formula:

Labor Efficiency Variance = (Standard hour - Actual hours)* Standard rate per hour

= (40,500 – 45,000)* 7

= - 31,500 (U)

Variable Overhead Rate Variance:

Formula:

Variable Overhead Rate = (Actual Rate – Standard Rate)* Actual Hours

= (7.4 – 5)* 31,050 = 74,250 (F)

Variable Overhead Efficiency Variance:

Formula:

Variable Overhead Efficiency = (Actual Hour – Standard Hour)* Standard Rate

= (31,050 – 30,375)* 5 = 3375 (F)

(b) Possible causes of variances

Material usage variance

Utilisation resources with carelessness.

Unskilled personnel are wasting more resources.

Implementing a faulty, poor, or unsuitable manufacturing procedure.

Wastage has resulted in a loss.

Use of a different material mix from the usual blend.

Components of inferior or bad quality are used.

Labor efficiency

1. The labor union is using a "go slow" strategy.

Labor Efficiency Variance:

Formula:

Labor Efficiency Variance = (Standard hour - Actual hours)* Standard rate per hour

= (40,500 – 45,000)* 7

= - 31,500 (U)

Variable Overhead Rate Variance:

Formula:

Variable Overhead Rate = (Actual Rate – Standard Rate)* Actual Hours

= (7.4 – 5)* 31,050 = 74,250 (F)

Variable Overhead Efficiency Variance:

Formula:

Variable Overhead Efficiency = (Actual Hour – Standard Hour)* Standard Rate

= (31,050 – 30,375)* 5 = 3375 (F)

(b) Possible causes of variances

Material usage variance

Utilisation resources with carelessness.

Unskilled personnel are wasting more resources.

Implementing a faulty, poor, or unsuitable manufacturing procedure.

Wastage has resulted in a loss.

Use of a different material mix from the usual blend.

Components of inferior or bad quality are used.

Labor efficiency

1. The labor union is using a "go slow" strategy.

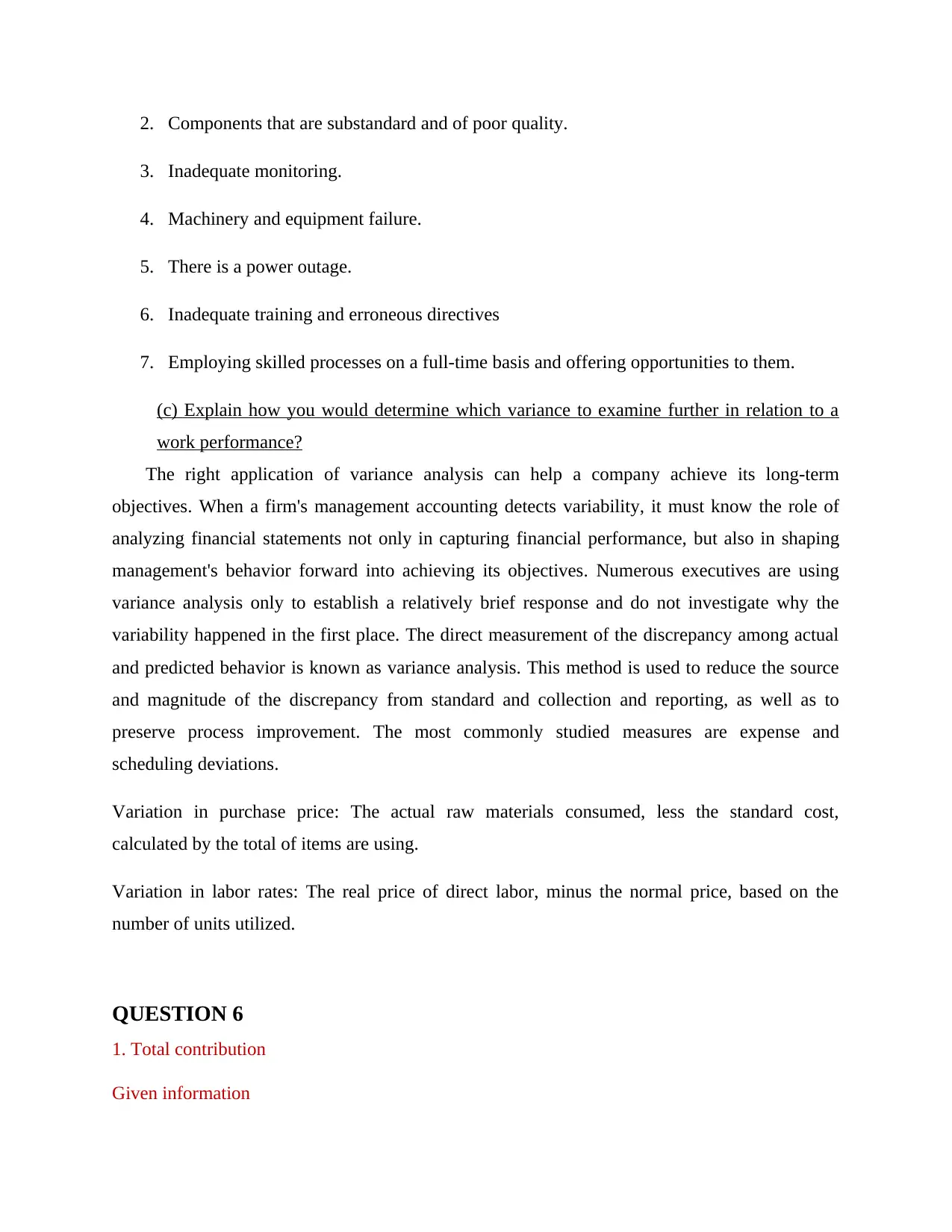

2. Components that are substandard and of poor quality.

3. Inadequate monitoring.

4. Machinery and equipment failure.

5. There is a power outage.

6. Inadequate training and erroneous directives

7. Employing skilled processes on a full-time basis and offering opportunities to them.

(c) Explain how you would determine which variance to examine further in relation to a

work performance?

The right application of variance analysis can help a company achieve its long-term

objectives. When a firm's management accounting detects variability, it must know the role of

analyzing financial statements not only in capturing financial performance, but also in shaping

management's behavior forward into achieving its objectives. Numerous executives are using

variance analysis only to establish a relatively brief response and do not investigate why the

variability happened in the first place. The direct measurement of the discrepancy among actual

and predicted behavior is known as variance analysis. This method is used to reduce the source

and magnitude of the discrepancy from standard and collection and reporting, as well as to

preserve process improvement. The most commonly studied measures are expense and

scheduling deviations.

Variation in purchase price: The actual raw materials consumed, less the standard cost,

calculated by the total of items are using.

Variation in labor rates: The real price of direct labor, minus the normal price, based on the

number of units utilized.

QUESTION 6

1. Total contribution

Given information

3. Inadequate monitoring.

4. Machinery and equipment failure.

5. There is a power outage.

6. Inadequate training and erroneous directives

7. Employing skilled processes on a full-time basis and offering opportunities to them.

(c) Explain how you would determine which variance to examine further in relation to a

work performance?

The right application of variance analysis can help a company achieve its long-term

objectives. When a firm's management accounting detects variability, it must know the role of

analyzing financial statements not only in capturing financial performance, but also in shaping

management's behavior forward into achieving its objectives. Numerous executives are using

variance analysis only to establish a relatively brief response and do not investigate why the

variability happened in the first place. The direct measurement of the discrepancy among actual

and predicted behavior is known as variance analysis. This method is used to reduce the source

and magnitude of the discrepancy from standard and collection and reporting, as well as to

preserve process improvement. The most commonly studied measures are expense and

scheduling deviations.

Variation in purchase price: The actual raw materials consumed, less the standard cost,

calculated by the total of items are using.

Variation in labor rates: The real price of direct labor, minus the normal price, based on the

number of units utilized.

QUESTION 6

1. Total contribution

Given information

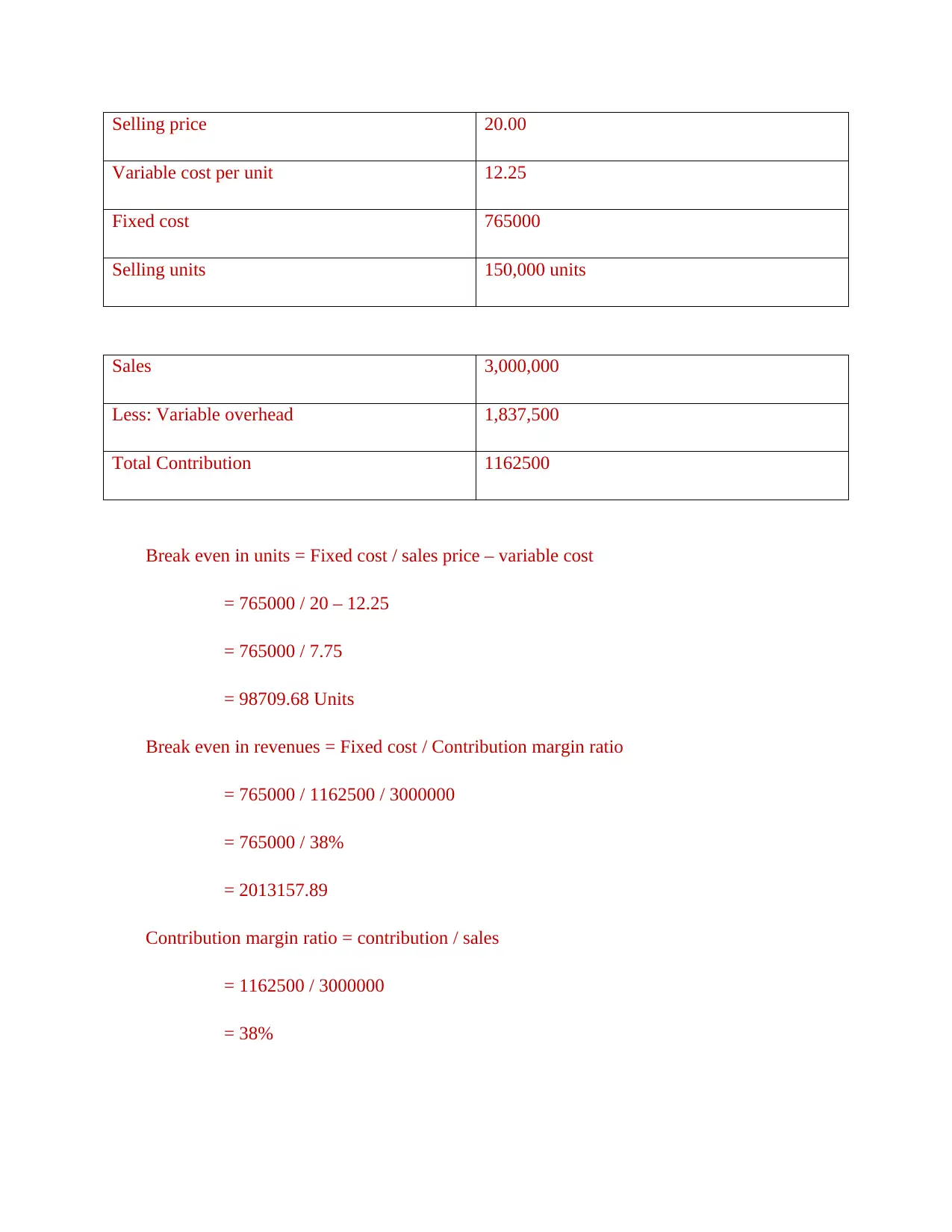

Selling price 20.00

Variable cost per unit 12.25

Fixed cost 765000

Selling units 150,000 units

Sales 3,000,000

Less: Variable overhead 1,837,500

Total Contribution 1162500

Break even in units = Fixed cost / sales price – variable cost

= 765000 / 20 – 12.25

= 765000 / 7.75

= 98709.68 Units

Break even in revenues = Fixed cost / Contribution margin ratio

= 765000 / 1162500 / 3000000

= 765000 / 38%

= 2013157.89

Contribution margin ratio = contribution / sales

= 1162500 / 3000000

= 38%

Variable cost per unit 12.25

Fixed cost 765000

Selling units 150,000 units

Sales 3,000,000

Less: Variable overhead 1,837,500

Total Contribution 1162500

Break even in units = Fixed cost / sales price – variable cost

= 765000 / 20 – 12.25

= 765000 / 7.75

= 98709.68 Units

Break even in revenues = Fixed cost / Contribution margin ratio

= 765000 / 1162500 / 3000000

= 765000 / 38%

= 2013157.89

Contribution margin ratio = contribution / sales

= 1162500 / 3000000

= 38%

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

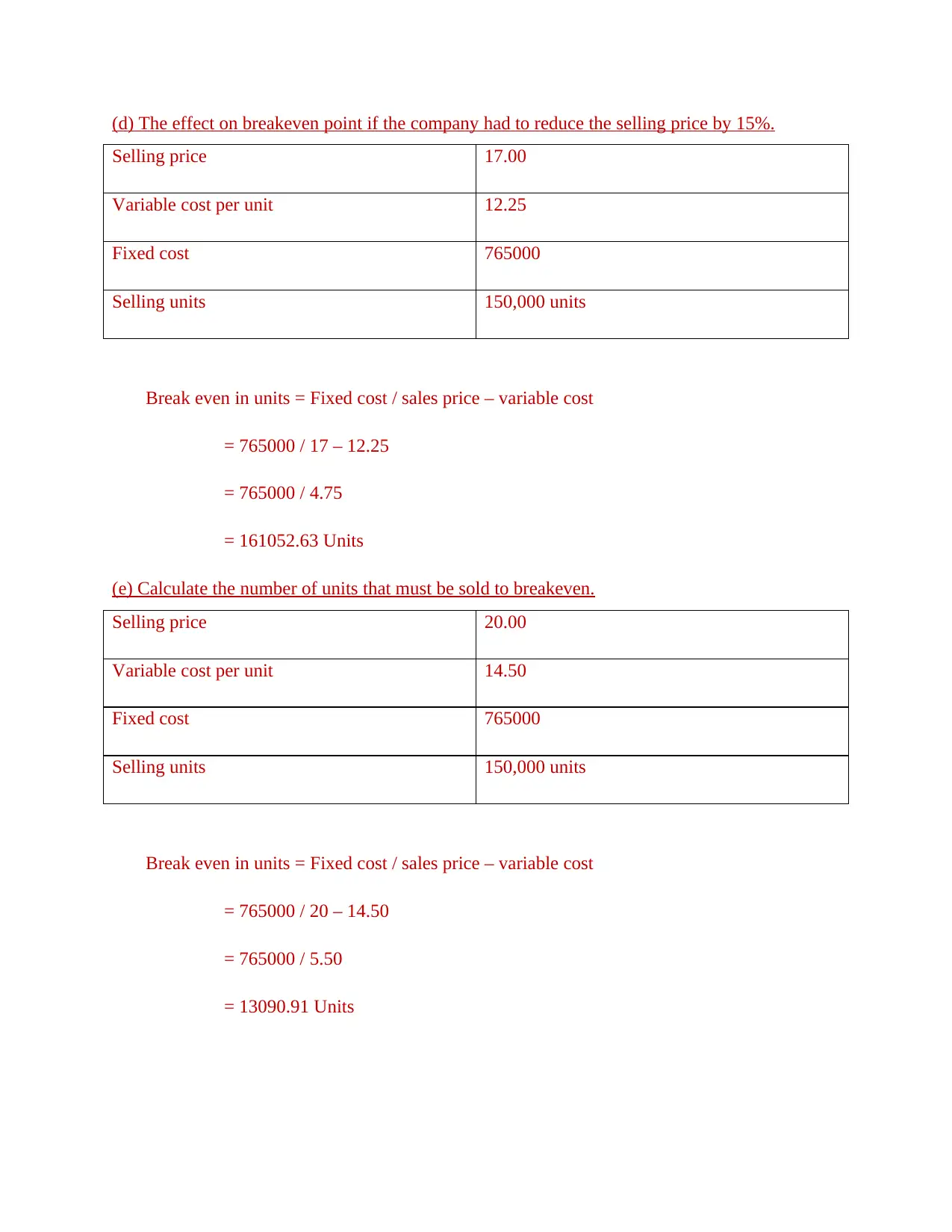

(d) The effect on breakeven point if the company had to reduce the selling price by 15%.

Selling price 17.00

Variable cost per unit 12.25

Fixed cost 765000

Selling units 150,000 units

Break even in units = Fixed cost / sales price – variable cost

= 765000 / 17 – 12.25

= 765000 / 4.75

= 161052.63 Units

(e) Calculate the number of units that must be sold to breakeven.

Selling price 20.00

Variable cost per unit 14.50

Fixed cost 765000

Selling units 150,000 units

Break even in units = Fixed cost / sales price – variable cost

= 765000 / 20 – 14.50

= 765000 / 5.50

= 13090.91 Units

Selling price 17.00

Variable cost per unit 12.25

Fixed cost 765000

Selling units 150,000 units

Break even in units = Fixed cost / sales price – variable cost

= 765000 / 17 – 12.25

= 765000 / 4.75

= 161052.63 Units

(e) Calculate the number of units that must be sold to breakeven.

Selling price 20.00

Variable cost per unit 14.50

Fixed cost 765000

Selling units 150,000 units

Break even in units = Fixed cost / sales price – variable cost

= 765000 / 20 – 14.50

= 765000 / 5.50

= 13090.91 Units

6. What is meant by a product’s contribution margin (CM) ratio? How is this ratio useful in

planning business operations?

The contribution margin ratio is the percentile rank among a total business and indirect

cost. The ratio can also be used to calculate the earnings that will result from different sales

volumes. This ratio shows how much each dollar of sales is ready to discuss an absorption

costing includes and profit. The contribution margin (revenue less all variable costs) is divided

by sales to get the proportion. Following removing variable expenses, contribution margin is a

metric that shows how much money a company makes on every commodity it delivers.

Increasing the wholesale price by the amount sold less the marginal cost times the cost of goods

sold yields the contribution margin. The generated value is then used to offset the company'

fixed expenses and to calculate the break-even threshold.

planning business operations?

The contribution margin ratio is the percentile rank among a total business and indirect

cost. The ratio can also be used to calculate the earnings that will result from different sales

volumes. This ratio shows how much each dollar of sales is ready to discuss an absorption

costing includes and profit. The contribution margin (revenue less all variable costs) is divided

by sales to get the proportion. Following removing variable expenses, contribution margin is a

metric that shows how much money a company makes on every commodity it delivers.

Increasing the wholesale price by the amount sold less the marginal cost times the cost of goods

sold yields the contribution margin. The generated value is then used to offset the company'

fixed expenses and to calculate the break-even threshold.

REFERENCES

Books and Journal

Baños, J. and López-Manjón, J. D., 2021. Revisiting the boundaries of the sacred: guilds and

brotherhoods’ accounting in the last decade of the 16th century. De Computis-Revista

Española de Historia de la Contabilidad. 18(1). pp.55-73.

Hassan, M. K. and et.al, 2021. Bibliometric analysis of the Journal of Islamic Accounting and

Business Research: Ten years review. COLLNET Journal of Scientometrics and

Information Management. 15(1). pp.63-88.

Hur, K. S. and Hwang, I. T., 2021. The effect of bank governance on borrowers’ accounting

choices. Asia-Pacific Journal of Accounting & Economics, pp.1-27.

Callejas, D. G. and Ocampo-Salazar, C. A., 2021. Whither Environmental Accounting. The

Challenge of Ecological and Green Accounting. Environment and Innovation: Strategies

to Promote Growth and Sustainability, p.179.

Bond, D., and et.al, 2021. Research productivity of Australian accounting academics. Accounting

& Finance, 61(1), pp.1081-1104.

Kryshtal, H., and et.al, 2021. ACCOUNTING AS AN INTEGRAL PART OF FINANCIAL

AND ECONOMIC ASSESSMENT OF BUSINESS ENTITIES. Natsional'nyi Hirnychyi

Universytet. Naukovyi Visnyk, (3), pp.162-166.

Foroodi, M. and Hejazi, R., 2021. Presenting a reductive model of Earnings management based

on Multi_ grounded Theory approach. Journal of Knowledge Accounting.

Krismiaji, K., 2021. Audit Quality Characteristics and Accounting Conservatism: Empirical

Study in Indonesian Company. ATESTASI: Jurnal Ilmiah Akuntansi. 4(2). pp.132-141.

Books and Journal

Baños, J. and López-Manjón, J. D., 2021. Revisiting the boundaries of the sacred: guilds and

brotherhoods’ accounting in the last decade of the 16th century. De Computis-Revista

Española de Historia de la Contabilidad. 18(1). pp.55-73.

Hassan, M. K. and et.al, 2021. Bibliometric analysis of the Journal of Islamic Accounting and

Business Research: Ten years review. COLLNET Journal of Scientometrics and

Information Management. 15(1). pp.63-88.

Hur, K. S. and Hwang, I. T., 2021. The effect of bank governance on borrowers’ accounting

choices. Asia-Pacific Journal of Accounting & Economics, pp.1-27.

Callejas, D. G. and Ocampo-Salazar, C. A., 2021. Whither Environmental Accounting. The

Challenge of Ecological and Green Accounting. Environment and Innovation: Strategies

to Promote Growth and Sustainability, p.179.

Bond, D., and et.al, 2021. Research productivity of Australian accounting academics. Accounting

& Finance, 61(1), pp.1081-1104.

Kryshtal, H., and et.al, 2021. ACCOUNTING AS AN INTEGRAL PART OF FINANCIAL

AND ECONOMIC ASSESSMENT OF BUSINESS ENTITIES. Natsional'nyi Hirnychyi

Universytet. Naukovyi Visnyk, (3), pp.162-166.

Foroodi, M. and Hejazi, R., 2021. Presenting a reductive model of Earnings management based

on Multi_ grounded Theory approach. Journal of Knowledge Accounting.

Krismiaji, K., 2021. Audit Quality Characteristics and Accounting Conservatism: Empirical

Study in Indonesian Company. ATESTASI: Jurnal Ilmiah Akuntansi. 4(2). pp.132-141.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.