Management Accounting: Principles, Techniques, and Applications in Diageo

VerifiedAdded on 2023/06/18

|15

|3887

|178

AI Summary

This article discusses the principles, techniques, and applications of management accounting in Diageo, a UK-based manufacturing company. It covers topics such as financial planning, variance analysis, investment appraisal techniques, and key performance indicators. The article also explores different planning tools and their effectiveness in dealing with financial problems.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENT

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

PART 1............................................................................................................................................3

Principles of management accounting.........................................................................................3

Management accounting and management accounting system roles..........................................4

Utilization of techniques and methods for the management accounting.....................................5

Integration of management accounting in the organization.........................................................6

Benefits of management accounting functions............................................................................7

CONCLUSION................................................................................................................................7

PART 2............................................................................................................................................9

INTRODUCTION...........................................................................................................................9

Utilization of planning tools in management accounting and differences between them...........9

Comparison of ways for management accounting for its application and effectiveness for

dealing with financial problems.................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

PART 1............................................................................................................................................3

Principles of management accounting.........................................................................................3

Management accounting and management accounting system roles..........................................4

Utilization of techniques and methods for the management accounting.....................................5

Integration of management accounting in the organization.........................................................6

Benefits of management accounting functions............................................................................7

CONCLUSION................................................................................................................................7

PART 2............................................................................................................................................9

INTRODUCTION...........................................................................................................................9

Utilization of planning tools in management accounting and differences between them...........9

Comparison of ways for management accounting for its application and effectiveness for

dealing with financial problems.................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting is the presentation of the financial information which shows the

internal purpose of the management that allows the business in making the key decision. The

managerial accounting is the one which encompasses the many facets of the accounting allowing

the company in making decision (Abdusalomova, 2020). Diageo is the UK company which is a

manufacturing company that manufactures many alcoholic beverages. It is a multinational

company and is the largest producer of Scotch whiskey in the world. This project demonstrates

the understanding of the management accounting system in the organization. With the help of

this project different application of the management accounting techniques is going to be used.

MAIN BODY

PART 1

Principles of management accounting

The principles of the management accounting are as follows,

Designing and compiling:

Management accounting helps the Diageo to design the accounting information, records,

statements and also other evidence which allows the business in the future to meet the

requirements which are particular to the relevancy of the business.

Management by exception:

Management accounting follows the budgetary control system and also the standard

costing techniques. This allows the management accounting in making comparison of the actual

performance of the company to the findings in management accounting.

Management accounting is the presentation of the financial information which shows the

internal purpose of the management that allows the business in making the key decision. The

managerial accounting is the one which encompasses the many facets of the accounting allowing

the company in making decision (Abdusalomova, 2020). Diageo is the UK company which is a

manufacturing company that manufactures many alcoholic beverages. It is a multinational

company and is the largest producer of Scotch whiskey in the world. This project demonstrates

the understanding of the management accounting system in the organization. With the help of

this project different application of the management accounting techniques is going to be used.

MAIN BODY

PART 1

Principles of management accounting

The principles of the management accounting are as follows,

Designing and compiling:

Management accounting helps the Diageo to design the accounting information, records,

statements and also other evidence which allows the business in the future to meet the

requirements which are particular to the relevancy of the business.

Management by exception:

Management accounting follows the budgetary control system and also the standard

costing techniques. This allows the management accounting in making comparison of the actual

performance of the company to the findings in management accounting.

Control at source accounting :

The best way of controlling the cost is by controlling at the point at which it is incurred.

Management accounting enables the business to understand the utilization and usage of the

services to be understood and employed (Charifzadeh and Taschner, 2017).

Accounting for inflation:

For an enterprise earning profit is essential and due to the change in the value of money

the profit which the business is not the same as it contributes towards the business with the help

of real value and money. The rate of inflation is calculated and understood by the management

accounting.

Use of Return on Investment:

The rate of return shows the efficiency of the business. Management accounting helps the

business to analyse how much return it has made out of its investments with the calculation of

return on investment.

Management accounting and management accounting system roles

The roles of management accounting systems is to advise the managers to for the

financial implications of the business which helps in the business decision-making for aiding the

business to growth and development of profit. Management accounting helps in the preparation

of the reports, budget, commentaries and also financial statements. Management accounting

system is the system which provides critical informations to the management about the

utilization of the operations of the business for its decision-making. A manufacturing company

like the Diageo utilizes these systems for management of its costs and process. The management

accounting systems vary from industry to industry about what they are utilized for. Some roles of

management accounting systems is to collect the data which is required in the field of accounting

which informs the management of the business operations (Englund and Gerdin, 2018)

Management accounting systems utilizes the budget for the planning of the business operations.

These systems utilize the performance reports for noting the deviation of the actual results in

comparison to the budget analysation.

Utilization of techniques and methods for the management accounting

Some important tool and techniques which are used in the management accounting are,

Financial planning :

The best way of controlling the cost is by controlling at the point at which it is incurred.

Management accounting enables the business to understand the utilization and usage of the

services to be understood and employed (Charifzadeh and Taschner, 2017).

Accounting for inflation:

For an enterprise earning profit is essential and due to the change in the value of money

the profit which the business is not the same as it contributes towards the business with the help

of real value and money. The rate of inflation is calculated and understood by the management

accounting.

Use of Return on Investment:

The rate of return shows the efficiency of the business. Management accounting helps the

business to analyse how much return it has made out of its investments with the calculation of

return on investment.

Management accounting and management accounting system roles

The roles of management accounting systems is to advise the managers to for the

financial implications of the business which helps in the business decision-making for aiding the

business to growth and development of profit. Management accounting helps in the preparation

of the reports, budget, commentaries and also financial statements. Management accounting

system is the system which provides critical informations to the management about the

utilization of the operations of the business for its decision-making. A manufacturing company

like the Diageo utilizes these systems for management of its costs and process. The management

accounting systems vary from industry to industry about what they are utilized for. Some roles of

management accounting systems is to collect the data which is required in the field of accounting

which informs the management of the business operations (Englund and Gerdin, 2018)

Management accounting systems utilizes the budget for the planning of the business operations.

These systems utilize the performance reports for noting the deviation of the actual results in

comparison to the budget analysation.

Utilization of techniques and methods for the management accounting

Some important tool and techniques which are used in the management accounting are,

Financial planning :

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Main objective of Diageo is to maximize its profit with the help of management

accounting. Management accounting does this by the help of proper financial planning which is

the most important tool of business objectives achievements.

Financial statement's analysis:

Both profit and loss account and balance sheet are very important financial statements

which are considered to be very important tool for the analysation of the different period. It helps

the management accounting to understand the rate of growth of which the business is concerned

with.

Cost accounting ;

The cost accounting is the presentation of the cost data which product wise or even the

process wise helps the department of the branch. The determination of the cost of the data helps

the business to compare with the predetermined ones (Agustia, Sawarjuwono and Dianawati,

2019). Comparison between the two costs enables the management to decide the reasons for

which its is responsible. For example Diageo has the raw materials of £50000 as the opening

stock and a closing stock of £40000. This organization purchases £145000. There fore the

calculation of Cost of material consumed would be, (50000+145000)- 40000

155000.

Fund flow analysis :

This analysis of the organization allows the business with the movement of fund from

one period to the another. This analysis is considered to be very important for the comparison of

the use of funds of two different years of the organization. Fund flow analysis is also useful for

the finding the working capital changes and funds.

Cash flow analysis :

This analysis is that tool of management accounting which helps the business to find out

the movement of cash from one period to the another. It shows the changes in the cash balance

between two periods. With the help of this tool the operations of cash and its movement in a

period can be understood.

Standard Costing :

It is the predetermined cost which helps the business to provide the measurement of the

actual performance of the business operations. This technique of management accounting is

accounting. Management accounting does this by the help of proper financial planning which is

the most important tool of business objectives achievements.

Financial statement's analysis:

Both profit and loss account and balance sheet are very important financial statements

which are considered to be very important tool for the analysation of the different period. It helps

the management accounting to understand the rate of growth of which the business is concerned

with.

Cost accounting ;

The cost accounting is the presentation of the cost data which product wise or even the

process wise helps the department of the branch. The determination of the cost of the data helps

the business to compare with the predetermined ones (Agustia, Sawarjuwono and Dianawati,

2019). Comparison between the two costs enables the management to decide the reasons for

which its is responsible. For example Diageo has the raw materials of £50000 as the opening

stock and a closing stock of £40000. This organization purchases £145000. There fore the

calculation of Cost of material consumed would be, (50000+145000)- 40000

155000.

Fund flow analysis :

This analysis of the organization allows the business with the movement of fund from

one period to the another. This analysis is considered to be very important for the comparison of

the use of funds of two different years of the organization. Fund flow analysis is also useful for

the finding the working capital changes and funds.

Cash flow analysis :

This analysis is that tool of management accounting which helps the business to find out

the movement of cash from one period to the another. It shows the changes in the cash balance

between two periods. With the help of this tool the operations of cash and its movement in a

period can be understood.

Standard Costing :

It is the predetermined cost which helps the business to provide the measurement of the

actual performance of the business operations. This technique of management accounting is

considered to be very useful for recognizing the deviations found in the operations along with its

reason.

Marginal Costing :

The technique of marginal costing is used for fixing the selling price for the business and

its product with the help of some best strategies, raw materials or resources, production decision-

making and analysation of the decision-making based on the fixed cost, variable cost and

contribution.

Integration of management accounting in the organization

The integration of management accounting in the business operation of Diageo are,

Reviewing products :

As a manufacturing company Diageo brings different range of products for its customers.

The review of the current product range, the management accounting provides the financial and

business statistical analysis which help in the deciding which products are profitable and which

are not (NGUYEN and LE, 2020).

Launching new products:

The launch of the new products of the management accounting is considered to be very

important as it can support the business in every stage. Management accounting breaks down the

details on the products which helps in understanding the accurate picture of the market for that

product. It allows the business to understand the quality and quantity of the products which is

needed to be changed.

Staffing:

Management accounting is also very important for understanding the importance of the

decision-making that allows the business to understand and evaluate the decision of hiring of

new staff (Boyd, 2019). Management accounting is important in making the right decisions as its

allows the business to understand how much is needed for the business to spend on the staffing

and also how much return it gets and can get from the staff the business own (Charifzadeh and

Taschner, 2017).

Benefits of management accounting functions

Some benefits of management accounting functions are,

Decision-making :

reason.

Marginal Costing :

The technique of marginal costing is used for fixing the selling price for the business and

its product with the help of some best strategies, raw materials or resources, production decision-

making and analysation of the decision-making based on the fixed cost, variable cost and

contribution.

Integration of management accounting in the organization

The integration of management accounting in the business operation of Diageo are,

Reviewing products :

As a manufacturing company Diageo brings different range of products for its customers.

The review of the current product range, the management accounting provides the financial and

business statistical analysis which help in the deciding which products are profitable and which

are not (NGUYEN and LE, 2020).

Launching new products:

The launch of the new products of the management accounting is considered to be very

important as it can support the business in every stage. Management accounting breaks down the

details on the products which helps in understanding the accurate picture of the market for that

product. It allows the business to understand the quality and quantity of the products which is

needed to be changed.

Staffing:

Management accounting is also very important for understanding the importance of the

decision-making that allows the business to understand and evaluate the decision of hiring of

new staff (Boyd, 2019). Management accounting is important in making the right decisions as its

allows the business to understand how much is needed for the business to spend on the staffing

and also how much return it gets and can get from the staff the business own (Charifzadeh and

Taschner, 2017).

Benefits of management accounting functions

Some benefits of management accounting functions are,

Decision-making :

The management accounting functions allows the business to make important decision-

making on the basis of costing, economics and statistics. The decision-making is very important

for a business it helps its plan its operations.

Planning :

Management accounting's one of the function is that it is not fixed to a time line, it is a

continuous process. Due to this function the business is allowed to plan its activities on the basis

of the data analysed in the management accounting.

Identification of Business Problems :

The management accounting has the function of maintaining the records and data of all

the products, services, department, assets etc. of the business. Due to which any area of the

business that is having a problem management accounting is able to identify that error

(Massicotte and Henri, 2020).

Strategic Management :

The concept of the management accounting is not considered to be mandatory by any

law. Due to which the business can have its own management accounting structure as per the

requirements of the business. In case the company requires in depth analysis the or investigation

of its operations. With the help of this the business can strategically manage some core areas

which holds high importance for a business.

CONCLUSION

From the above evaluation it can be concluded that management accounting is very

important for providing some framework for the financial decision-making of the business of

Diageo. The application of the management accounting techniques includes the utilization of

some traditional methods such as the standard costing, budgeting and cost volume profit. For its

application some integrated approaches like the Just-in-Time, Activity Based-costing,

Benchmarking and target costing is utilized. The management accounting process is very

essential for a manufacturing organization as it helps the manager in making decisions which in

regard to the given scenario can understand the areas of improvements. Its importance in the

application of cost implications helps in making better and efficient decisions for the

organization.

making on the basis of costing, economics and statistics. The decision-making is very important

for a business it helps its plan its operations.

Planning :

Management accounting's one of the function is that it is not fixed to a time line, it is a

continuous process. Due to this function the business is allowed to plan its activities on the basis

of the data analysed in the management accounting.

Identification of Business Problems :

The management accounting has the function of maintaining the records and data of all

the products, services, department, assets etc. of the business. Due to which any area of the

business that is having a problem management accounting is able to identify that error

(Massicotte and Henri, 2020).

Strategic Management :

The concept of the management accounting is not considered to be mandatory by any

law. Due to which the business can have its own management accounting structure as per the

requirements of the business. In case the company requires in depth analysis the or investigation

of its operations. With the help of this the business can strategically manage some core areas

which holds high importance for a business.

CONCLUSION

From the above evaluation it can be concluded that management accounting is very

important for providing some framework for the financial decision-making of the business of

Diageo. The application of the management accounting techniques includes the utilization of

some traditional methods such as the standard costing, budgeting and cost volume profit. For its

application some integrated approaches like the Just-in-Time, Activity Based-costing,

Benchmarking and target costing is utilized. The management accounting process is very

essential for a manufacturing organization as it helps the manager in making decisions which in

regard to the given scenario can understand the areas of improvements. Its importance in the

application of cost implications helps in making better and efficient decisions for the

organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART 2

INTRODUCTION

Management accounting is the presentation of the financial information which serves as

the internal purpose of the management for its key decision-making in the business (Saeidi and

et.al.,2018). The role of assistance financial accountant in management accounting is helping the

organization choose and manage the investments made, planning, budgeting, strategizing and

also decision-making. The chosen organization is Diageo. This UK company is a manufacturing

company that manufactures many alcoholic beverages.

Utilization of planning tools in management accounting and differences between them

There are many tools of planning in the management accounting. The tools which can be

applied in the business organization for improvements in the forecasting, systematic planning

and also the elimination of the threats. Some planning tools in management accounting are,

Cash flow budget :

Cash is a very critical issue for the business as it is related to the working capital

requirements. The activities which are present in the cash flow budget are the one which are

utilized for evaluation of the future figures of the financial factors (Vakhrushina and et.al.2018).

The advantages and disadvantages of this planning tool in management accounting are,

Advantages Disadvantages

The cash flow budget allows advanced and

diversified strategy which can be used for

making up for the future shortages of cash.

Due to the number of estimation present in this

tool it lacks accuracy of cash.

This allows the management accounting to

plan better utilization of resources in different

department.

The adoption of this tool in management

accounting sometimes can be problematic due

to lack of coordination in the employees.

Variance Analysis :

This tool of management accounting is the set of some analytical arrangements which are

available to the pre-budgeted standards which provides outcomes which can be utilized in both

financial and non-financial aspects (Ax and Greve, 2017). This is a very popular tool of

INTRODUCTION

Management accounting is the presentation of the financial information which serves as

the internal purpose of the management for its key decision-making in the business (Saeidi and

et.al.,2018). The role of assistance financial accountant in management accounting is helping the

organization choose and manage the investments made, planning, budgeting, strategizing and

also decision-making. The chosen organization is Diageo. This UK company is a manufacturing

company that manufactures many alcoholic beverages.

Utilization of planning tools in management accounting and differences between them

There are many tools of planning in the management accounting. The tools which can be

applied in the business organization for improvements in the forecasting, systematic planning

and also the elimination of the threats. Some planning tools in management accounting are,

Cash flow budget :

Cash is a very critical issue for the business as it is related to the working capital

requirements. The activities which are present in the cash flow budget are the one which are

utilized for evaluation of the future figures of the financial factors (Vakhrushina and et.al.2018).

The advantages and disadvantages of this planning tool in management accounting are,

Advantages Disadvantages

The cash flow budget allows advanced and

diversified strategy which can be used for

making up for the future shortages of cash.

Due to the number of estimation present in this

tool it lacks accuracy of cash.

This allows the management accounting to

plan better utilization of resources in different

department.

The adoption of this tool in management

accounting sometimes can be problematic due

to lack of coordination in the employees.

Variance Analysis :

This tool of management accounting is the set of some analytical arrangements which are

available to the pre-budgeted standards which provides outcomes which can be utilized in both

financial and non-financial aspects (Ax and Greve, 2017). This is a very popular tool of

determination of efficiency of the business operations. The advantages and disadvantages of

variance analysis are,

variance analysis are,

Advantages Disadvantages

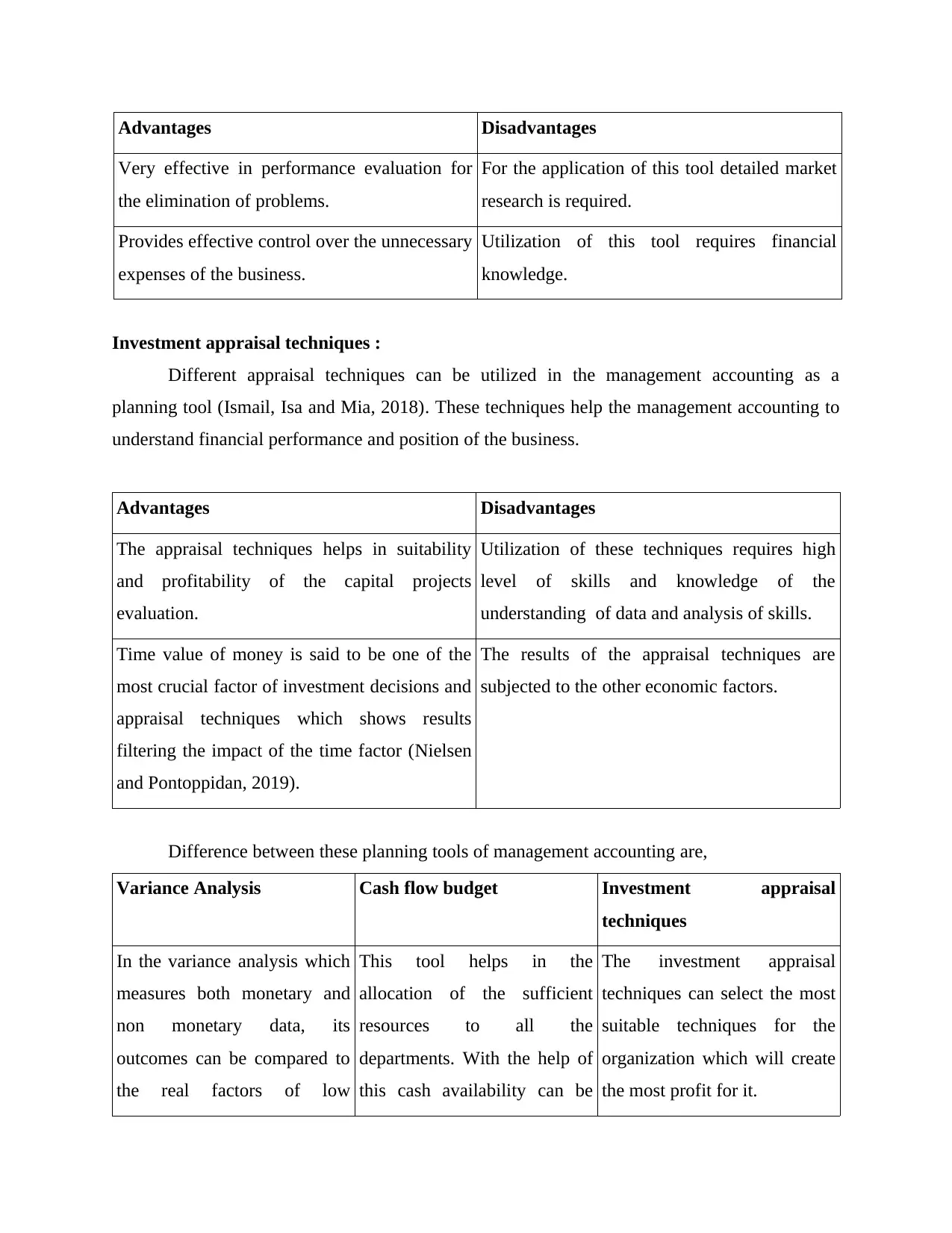

Very effective in performance evaluation for

the elimination of problems.

For the application of this tool detailed market

research is required.

Provides effective control over the unnecessary

expenses of the business.

Utilization of this tool requires financial

knowledge.

Investment appraisal techniques :

Different appraisal techniques can be utilized in the management accounting as a

planning tool (Ismail, Isa and Mia, 2018). These techniques help the management accounting to

understand financial performance and position of the business.

Advantages Disadvantages

The appraisal techniques helps in suitability

and profitability of the capital projects

evaluation.

Utilization of these techniques requires high

level of skills and knowledge of the

understanding of data and analysis of skills.

Time value of money is said to be one of the

most crucial factor of investment decisions and

appraisal techniques which shows results

filtering the impact of the time factor (Nielsen

and Pontoppidan, 2019).

The results of the appraisal techniques are

subjected to the other economic factors.

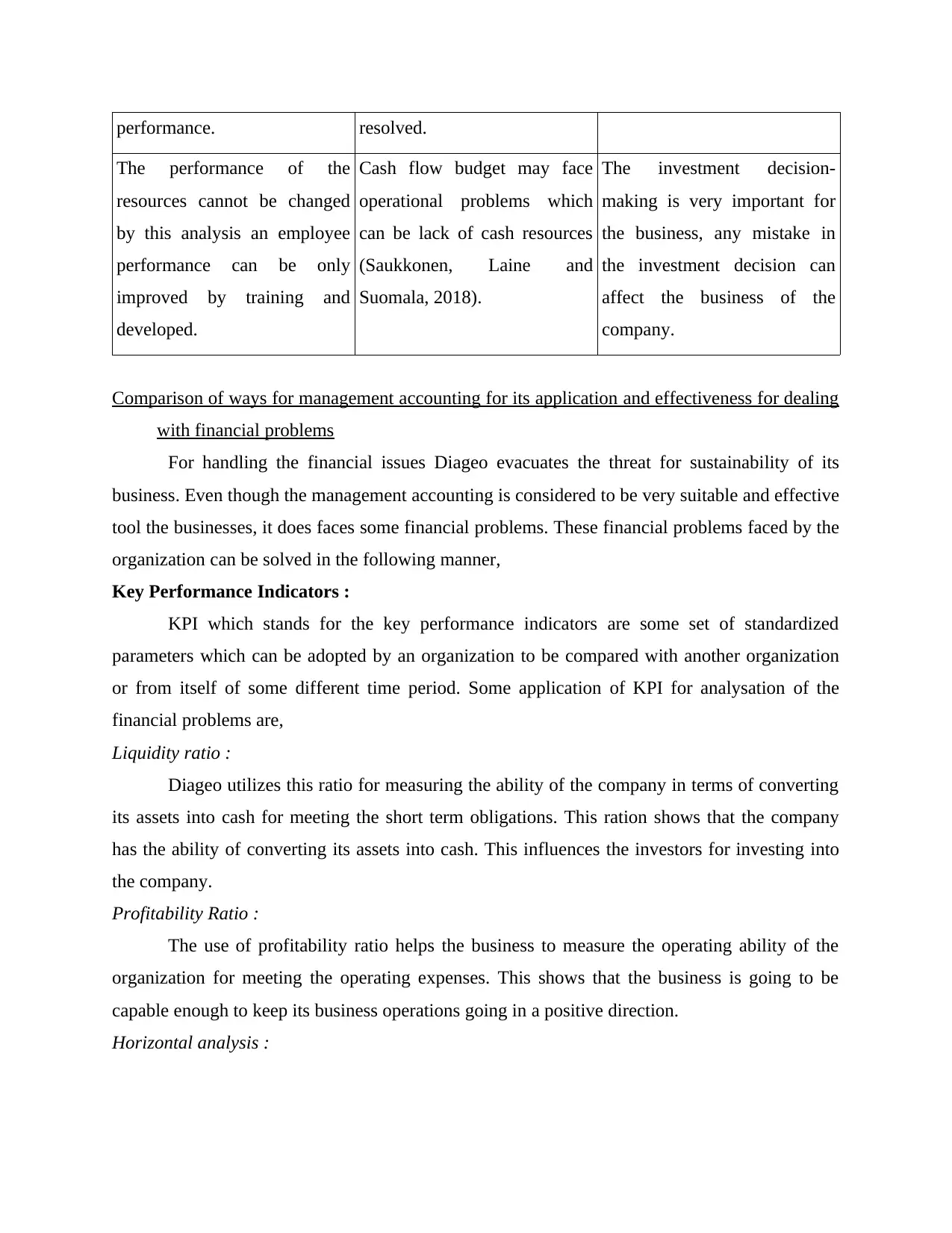

Difference between these planning tools of management accounting are,

Variance Analysis Cash flow budget Investment appraisal

techniques

In the variance analysis which

measures both monetary and

non monetary data, its

outcomes can be compared to

the real factors of low

This tool helps in the

allocation of the sufficient

resources to all the

departments. With the help of

this cash availability can be

The investment appraisal

techniques can select the most

suitable techniques for the

organization which will create

the most profit for it.

Very effective in performance evaluation for

the elimination of problems.

For the application of this tool detailed market

research is required.

Provides effective control over the unnecessary

expenses of the business.

Utilization of this tool requires financial

knowledge.

Investment appraisal techniques :

Different appraisal techniques can be utilized in the management accounting as a

planning tool (Ismail, Isa and Mia, 2018). These techniques help the management accounting to

understand financial performance and position of the business.

Advantages Disadvantages

The appraisal techniques helps in suitability

and profitability of the capital projects

evaluation.

Utilization of these techniques requires high

level of skills and knowledge of the

understanding of data and analysis of skills.

Time value of money is said to be one of the

most crucial factor of investment decisions and

appraisal techniques which shows results

filtering the impact of the time factor (Nielsen

and Pontoppidan, 2019).

The results of the appraisal techniques are

subjected to the other economic factors.

Difference between these planning tools of management accounting are,

Variance Analysis Cash flow budget Investment appraisal

techniques

In the variance analysis which

measures both monetary and

non monetary data, its

outcomes can be compared to

the real factors of low

This tool helps in the

allocation of the sufficient

resources to all the

departments. With the help of

this cash availability can be

The investment appraisal

techniques can select the most

suitable techniques for the

organization which will create

the most profit for it.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

performance. resolved.

The performance of the

resources cannot be changed

by this analysis an employee

performance can be only

improved by training and

developed.

Cash flow budget may face

operational problems which

can be lack of cash resources

(Saukkonen, Laine and

Suomala, 2018).

The investment decision-

making is very important for

the business, any mistake in

the investment decision can

affect the business of the

company.

Comparison of ways for management accounting for its application and effectiveness for dealing

with financial problems

For handling the financial issues Diageo evacuates the threat for sustainability of its

business. Even though the management accounting is considered to be very suitable and effective

tool the businesses, it does faces some financial problems. These financial problems faced by the

organization can be solved in the following manner,

Key Performance Indicators :

KPI which stands for the key performance indicators are some set of standardized

parameters which can be adopted by an organization to be compared with another organization

or from itself of some different time period. Some application of KPI for analysation of the

financial problems are,

Liquidity ratio :

Diageo utilizes this ratio for measuring the ability of the company in terms of converting

its assets into cash for meeting the short term obligations. This ration shows that the company

has the ability of converting its assets into cash. This influences the investors for investing into

the company.

Profitability Ratio :

The use of profitability ratio helps the business to measure the operating ability of the

organization for meeting the operating expenses. This shows that the business is going to be

capable enough to keep its business operations going in a positive direction.

Horizontal analysis :

The performance of the

resources cannot be changed

by this analysis an employee

performance can be only

improved by training and

developed.

Cash flow budget may face

operational problems which

can be lack of cash resources

(Saukkonen, Laine and

Suomala, 2018).

The investment decision-

making is very important for

the business, any mistake in

the investment decision can

affect the business of the

company.

Comparison of ways for management accounting for its application and effectiveness for dealing

with financial problems

For handling the financial issues Diageo evacuates the threat for sustainability of its

business. Even though the management accounting is considered to be very suitable and effective

tool the businesses, it does faces some financial problems. These financial problems faced by the

organization can be solved in the following manner,

Key Performance Indicators :

KPI which stands for the key performance indicators are some set of standardized

parameters which can be adopted by an organization to be compared with another organization

or from itself of some different time period. Some application of KPI for analysation of the

financial problems are,

Liquidity ratio :

Diageo utilizes this ratio for measuring the ability of the company in terms of converting

its assets into cash for meeting the short term obligations. This ration shows that the company

has the ability of converting its assets into cash. This influences the investors for investing into

the company.

Profitability Ratio :

The use of profitability ratio helps the business to measure the operating ability of the

organization for meeting the operating expenses. This shows that the business is going to be

capable enough to keep its business operations going in a positive direction.

Horizontal analysis :

This analysis is considered to be very useful for evaluating the financial performance of

the company over a given time horizon, this analysis in the KPI shows that the business has

maintained financial stability (Christine, 2019).

Segment reporting:

The segment reporting shows that the business has the operating ability of specified

segment which can have segment margin for earning the segmented profit of the organization.

Benchmarking :

This term of benchmarking suggests the process which can be used for making

comparison between two companies showing the after-effect of the business operations.

Benchmarking is known to be the most essential tool of systematic management of the business

operations. The application of benchmarking can help the business to improve and also over

come the financial problems. The improvements of this level can insure the profits and

expansion of the organization making major impacts on the internal performance.

This organization uses benchmarking for the identification of the opportunities of

improvement in the organization and also understanding the effects it has on the business.

Benchmarking allows the business to note down the performance areas of improvement

by the company.

With the help of benchmarking Diageo is successful in developing an improvement plan.

The results which are developed after its identification are used for further more

improvements can be noticed.

Variance analysis :

Variance analysis is the summarization of the analysis which can be differentiated

between the planned and the actual numbers. The sum of the variances given in the picture helps

the business in achieving the overall performance or underperformance of the particular

reporting period. Diageo utilizes the Variance analysis for the comparison of the actual

performance numbers with the predicted one. This shows what the business is doing wrong and

helps the organization in planning future of the price, quantity of materials and labour.

According to the analysis of an organization usually there are two types of variances. Variable

and Fixed. The organization generally makes changes over the results of the variable variances

as they have the tendency of changing. The changes in these variances of the management

accounting generally occurs due to the certain financial problems (Nguyen, 2018).

the company over a given time horizon, this analysis in the KPI shows that the business has

maintained financial stability (Christine, 2019).

Segment reporting:

The segment reporting shows that the business has the operating ability of specified

segment which can have segment margin for earning the segmented profit of the organization.

Benchmarking :

This term of benchmarking suggests the process which can be used for making

comparison between two companies showing the after-effect of the business operations.

Benchmarking is known to be the most essential tool of systematic management of the business

operations. The application of benchmarking can help the business to improve and also over

come the financial problems. The improvements of this level can insure the profits and

expansion of the organization making major impacts on the internal performance.

This organization uses benchmarking for the identification of the opportunities of

improvement in the organization and also understanding the effects it has on the business.

Benchmarking allows the business to note down the performance areas of improvement

by the company.

With the help of benchmarking Diageo is successful in developing an improvement plan.

The results which are developed after its identification are used for further more

improvements can be noticed.

Variance analysis :

Variance analysis is the summarization of the analysis which can be differentiated

between the planned and the actual numbers. The sum of the variances given in the picture helps

the business in achieving the overall performance or underperformance of the particular

reporting period. Diageo utilizes the Variance analysis for the comparison of the actual

performance numbers with the predicted one. This shows what the business is doing wrong and

helps the organization in planning future of the price, quantity of materials and labour.

According to the analysis of an organization usually there are two types of variances. Variable

and Fixed. The organization generally makes changes over the results of the variable variances

as they have the tendency of changing. The changes in these variances of the management

accounting generally occurs due to the certain financial problems (Nguyen, 2018).

One of the competitors of Diageo which in itself is very established is Bacardi. This

business is very similar to that of Diageo and has also been very successful in the operations. The

KPI of this organization shows the following,

Earning per share :

This shows that the earning business has on every share. It allows the company to show

the net earning for every common stock holder. This shows that the business is earning from

every investment which is made in it by the investors.

Solvency ratio :

This ratio is considered to be very important in measurement of the capability of the

factors which have a survival importance. The focus of the ratio of debt and its total asset and the

assessment of the amount provided to the creditors is also done with the help of solvency ratio.

The Benchmarking analysis of the two organization shows that the Diageo should utilize

continuous improvement for resolving the financial issues it faces. However, the Bacardi is

doing very well as per this analysis but can improve its productivity and efficiency by

analysation of the market.

CONCLUSION

With the help of this project it can be concluded that management accounting system is

interrelated with information of the business and the accuracy of the decision-making based on

the accurate information. It can be recommended to the Diageo company to utilize the budgetary

control tools for being successful in the business. Also, for the achieving the organizational

targets the business can adopt this method for achieving accuracy in the business performance.

The cash flow analysis method can be also very essential planning tool for the organization as it

will help the business to improve its daily operational cost management that is very important for

the management accounting of the business.

business is very similar to that of Diageo and has also been very successful in the operations. The

KPI of this organization shows the following,

Earning per share :

This shows that the earning business has on every share. It allows the company to show

the net earning for every common stock holder. This shows that the business is earning from

every investment which is made in it by the investors.

Solvency ratio :

This ratio is considered to be very important in measurement of the capability of the

factors which have a survival importance. The focus of the ratio of debt and its total asset and the

assessment of the amount provided to the creditors is also done with the help of solvency ratio.

The Benchmarking analysis of the two organization shows that the Diageo should utilize

continuous improvement for resolving the financial issues it faces. However, the Bacardi is

doing very well as per this analysis but can improve its productivity and efficiency by

analysation of the market.

CONCLUSION

With the help of this project it can be concluded that management accounting system is

interrelated with information of the business and the accuracy of the decision-making based on

the accurate information. It can be recommended to the Diageo company to utilize the budgetary

control tools for being successful in the business. Also, for the achieving the organizational

targets the business can adopt this method for achieving accuracy in the business performance.

The cash flow analysis method can be also very essential planning tool for the organization as it

will help the business to improve its daily operational cost management that is very important for

the management accounting of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Abdusalomova, N., 2020. Principles of ties of internal control and management accounting

systems at the enterprises of black metallurgy. Архив научных исследований. (2).

Agustia, D., Sawarjuwono, T. and Dianawati, W., 2019. The mediating effect of environmental

management accounting on green innovation-Firm value relationship. International

Journal of Energy Economics and Policy. 9(2). pp.299-306.

Ax, C. and Greve, J., 2017. Adoption of management accounting innovations: Organizational

culture compatibility and perceived outcomes. Management Accounting Research. 34.

pp.59-74.

Charifzadeh, M. and Taschner, A., 2017. Management accounting and control: tools and

concepts in a Central European context. John Wiley & Sons.

Charifzadeh, M. and Taschner, A., 2017. Management accounting and control: tools and

concepts in a Central European context. John Wiley & Sons.

Christine, D., 2019. The relationship of environmental management accounting, environmental

strategy and managerial commitment with environmental performance and economic

performance. 670216917.

Englund, H. and Gerdin, J., 2018. Management accounting and the paradox of embedded

agency: A framework for analyzing sources of structural change.

Ismail, K., Isa, C.R. and Mia, L., 2018. Market competition, lean manufacturing practices and

the role of management accounting systems (MAS) information. Jurnal Pengurusan

(UKM Journal of Management). 52.

Massicotte, S. and Henri, J.F., 2020. The use of management accounting information by boards

of directors to oversee strategy implementation. The British Accounting Review,

p.100953.

NGUYEN, H.Q. and LE, O.T.T., 2020. Factors affecting the intention to apply management

accounting in enterprises in Vietnam. The Journal of Asian Finance, Economics, and

Business. 7(6). pp.95-107.

Nguyen, N.P., 2018. Performance implication of market orientation and use of management

accounting systems: The moderating role of accountants’ participation in strategic

decision making. Journal of Asian Business and Economic Studies.

Nielsen, S. and Pontoppidan, I.C., 2019. Exploring the inclusion of risk in management

accounting and control. Management Research Review.

Saeidi, S.P., and et.al.,2018. The moderating role of environmental management accounting

between environmental innovation and firm financial performance. International

Journal of Business Performance Management. 19(3). pp.326-348.

Saukkonen, N., Laine, T. and Suomala, P., 2018. Utilizing management accounting information

for decision-making: Limitations stemming from the process structure and the actors

involved. Qualitative Research in Accounting & Management.

Vakhrushina, M.A., and et.al.2018. Integrated management accounting in the financial

management system. Research Journal of Pharmaceutical, Biological and Chemical

Sciences. 9(3). pp.808-813.

Online

Books and Journals

Abdusalomova, N., 2020. Principles of ties of internal control and management accounting

systems at the enterprises of black metallurgy. Архив научных исследований. (2).

Agustia, D., Sawarjuwono, T. and Dianawati, W., 2019. The mediating effect of environmental

management accounting on green innovation-Firm value relationship. International

Journal of Energy Economics and Policy. 9(2). pp.299-306.

Ax, C. and Greve, J., 2017. Adoption of management accounting innovations: Organizational

culture compatibility and perceived outcomes. Management Accounting Research. 34.

pp.59-74.

Charifzadeh, M. and Taschner, A., 2017. Management accounting and control: tools and

concepts in a Central European context. John Wiley & Sons.

Charifzadeh, M. and Taschner, A., 2017. Management accounting and control: tools and

concepts in a Central European context. John Wiley & Sons.

Christine, D., 2019. The relationship of environmental management accounting, environmental

strategy and managerial commitment with environmental performance and economic

performance. 670216917.

Englund, H. and Gerdin, J., 2018. Management accounting and the paradox of embedded

agency: A framework for analyzing sources of structural change.

Ismail, K., Isa, C.R. and Mia, L., 2018. Market competition, lean manufacturing practices and

the role of management accounting systems (MAS) information. Jurnal Pengurusan

(UKM Journal of Management). 52.

Massicotte, S. and Henri, J.F., 2020. The use of management accounting information by boards

of directors to oversee strategy implementation. The British Accounting Review,

p.100953.

NGUYEN, H.Q. and LE, O.T.T., 2020. Factors affecting the intention to apply management

accounting in enterprises in Vietnam. The Journal of Asian Finance, Economics, and

Business. 7(6). pp.95-107.

Nguyen, N.P., 2018. Performance implication of market orientation and use of management

accounting systems: The moderating role of accountants’ participation in strategic

decision making. Journal of Asian Business and Economic Studies.

Nielsen, S. and Pontoppidan, I.C., 2019. Exploring the inclusion of risk in management

accounting and control. Management Research Review.

Saeidi, S.P., and et.al.,2018. The moderating role of environmental management accounting

between environmental innovation and firm financial performance. International

Journal of Business Performance Management. 19(3). pp.326-348.

Saukkonen, N., Laine, T. and Suomala, P., 2018. Utilizing management accounting information

for decision-making: Limitations stemming from the process structure and the actors

involved. Qualitative Research in Accounting & Management.

Vakhrushina, M.A., and et.al.2018. Integrated management accounting in the financial

management system. Research Journal of Pharmaceutical, Biological and Chemical

Sciences. 9(3). pp.808-813.

Online

Boyd, K., 2019. what is management accounting and why is it important for business?[Online].

Available through: <https://www.myob.com/au/blog/management-accounting-

important-business/>

Available through: <https://www.myob.com/au/blog/management-accounting-

important-business/>

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.