Management Accounting Report: Techniques for Organisational Objectives

VerifiedAdded on 2020/07/23

|20

|4798

|287

Report

AI Summary

This report, prepared for the General Manager of Unicorn Grocery, comprehensively explores management accounting. It begins with an introduction to management accounting systems, including inventory management, price optimization, job costing, and cost accounting systems. The report then delves into various management accounting reporting methods such as accounts receivable, accounts payable, budget, inventory control, and performance reporting. The core of the report analyzes different management accounting techniques, specifically focusing on marginal and absorption costing and their impact on income statements. Furthermore, the report examines the advantages and disadvantages of planning tools used for budgetary control. Finally, it discusses how management accounting can be used to address and resolve financial problems within an organization. The report concludes with a summary of the key findings and recommendations for the company.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Report

From: Management Accounting Officer

To: General Manager

Subject: To write a report to GM covering management accounting reporting and its various

systems together with various cost accounting techniques and planning tools. Their

implementation can assist in attaining organisational objectivities.

From: Management Accounting Officer

To: General Manager

Subject: To write a report to GM covering management accounting reporting and its various

systems together with various cost accounting techniques and planning tools. Their

implementation can assist in attaining organisational objectivities.

Table of Contents

INTRODUCTION ..........................................................................................................................1

LO1 Demonstrate an understanding of management accounting systems......................................2

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems to the chosen scenario giving examples............................2

P2 Explain different methods used for management accounting reporting that can also be used

for the chosen scenario...........................................................................................................5

LO 2 Apply a range of management accounting techniques...........................................................7

P3 Difference between income statement made through marginal and absorption costing...7

LO 3 Explain the use of planning tools used in management accounting....................................11

P4 Explain the advantages and disadvantages of different types of planning tools that can be

used for budgetary control for the chosen scenario. ............................................................11

LO 4 Compare ways in which organisations could use management accounting to respond to

financial problems..........................................................................................................................13

P5 Use of management accounting system for resolving financial problems......................13

CONCLUSION ...........................................................................................................................15

REFERENCES..............................................................................................................................16

2

INTRODUCTION ..........................................................................................................................1

LO1 Demonstrate an understanding of management accounting systems......................................2

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems to the chosen scenario giving examples............................2

P2 Explain different methods used for management accounting reporting that can also be used

for the chosen scenario...........................................................................................................5

LO 2 Apply a range of management accounting techniques...........................................................7

P3 Difference between income statement made through marginal and absorption costing...7

LO 3 Explain the use of planning tools used in management accounting....................................11

P4 Explain the advantages and disadvantages of different types of planning tools that can be

used for budgetary control for the chosen scenario. ............................................................11

LO 4 Compare ways in which organisations could use management accounting to respond to

financial problems..........................................................................................................................13

P5 Use of management accounting system for resolving financial problems......................13

CONCLUSION ...........................................................................................................................15

REFERENCES..............................................................................................................................16

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The process of making managerial report and analysing various kind of data ,that is

present in the company, is knows management accounting. It is basically use for both long and

short term decision making (Ahmad and Mohamed Zabri, 2012). Earlier enterprises could solve

most of their problems by concentrating on their financial performance but now they consider

different elements like competition in the market, globalisation etc., in order to cope up with

various type of troubles. Management accounting help in forecasting the future, it play

significant role in making judgement relating to buying or selling. By using its tools, manager

can determine the rate of return on any investment. Unicorn grocery is a small firm who is

operating in retail industry. They have a store in Manchester. This project will talk about various

kind management accounting systems like Job costing, price optimisation etc. Some methods of

reporting will also become part of this assignment. Reports shows the past performance and

current position of a company. In this file, net profit will be calculation by making income

statement. Both, marginal and absorption costing will be used for ascertain this figure. The

advantages and demerits of the planning tools will be explained under this project.

1

The process of making managerial report and analysing various kind of data ,that is

present in the company, is knows management accounting. It is basically use for both long and

short term decision making (Ahmad and Mohamed Zabri, 2012). Earlier enterprises could solve

most of their problems by concentrating on their financial performance but now they consider

different elements like competition in the market, globalisation etc., in order to cope up with

various type of troubles. Management accounting help in forecasting the future, it play

significant role in making judgement relating to buying or selling. By using its tools, manager

can determine the rate of return on any investment. Unicorn grocery is a small firm who is

operating in retail industry. They have a store in Manchester. This project will talk about various

kind management accounting systems like Job costing, price optimisation etc. Some methods of

reporting will also become part of this assignment. Reports shows the past performance and

current position of a company. In this file, net profit will be calculation by making income

statement. Both, marginal and absorption costing will be used for ascertain this figure. The

advantages and demerits of the planning tools will be explained under this project.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LO1 Demonstrate an understanding of management accounting systems

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems to the chosen scenario giving examples

Most of the enterprises face trouble at the time of making significant decision like the

right areas to invest money of the organisation. By using financial accounting, they cannot find

profitability of an investment (Aminbakhsh, Gunduz and Sonmez, 2013). This form of accounts

mainly aim at communicating the current position of the company. Management accounting help

in various significant organisational function, they identity the most suitable source of finance so

a firm can reduce the burden of debt. Their also support manager at the time of taking tuff calls

like where raise funds from public or from any financial institution. The importance of

management accounting is increasing because it do not only solve issues relating to finance, it

also help in improving overall performance of a company.

Every enterprise make some strategies so they can attain organisational objectives, the

role management accounting is significant in the whole process. It provide great assistance to a

corporation in formulation and implementing plans. Many managers argue the most of the issues

in a company happen because of miscommunication managerial accounts remove the confusion

by speeding up the process of communication. If also minimise the wastage of information. The

modern tools and techniques of management accounting are capable of fighting the challenges

that is present by swifty changing business environment (Burritt, Schaltegger and Zvezdov,

2011). Some systems of management accounting are as follows:

2

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems to the chosen scenario giving examples

Most of the enterprises face trouble at the time of making significant decision like the

right areas to invest money of the organisation. By using financial accounting, they cannot find

profitability of an investment (Aminbakhsh, Gunduz and Sonmez, 2013). This form of accounts

mainly aim at communicating the current position of the company. Management accounting help

in various significant organisational function, they identity the most suitable source of finance so

a firm can reduce the burden of debt. Their also support manager at the time of taking tuff calls

like where raise funds from public or from any financial institution. The importance of

management accounting is increasing because it do not only solve issues relating to finance, it

also help in improving overall performance of a company.

Every enterprise make some strategies so they can attain organisational objectives, the

role management accounting is significant in the whole process. It provide great assistance to a

corporation in formulation and implementing plans. Many managers argue the most of the issues

in a company happen because of miscommunication managerial accounts remove the confusion

by speeding up the process of communication. If also minimise the wastage of information. The

modern tools and techniques of management accounting are capable of fighting the challenges

that is present by swifty changing business environment (Burritt, Schaltegger and Zvezdov,

2011). Some systems of management accounting are as follows:

2

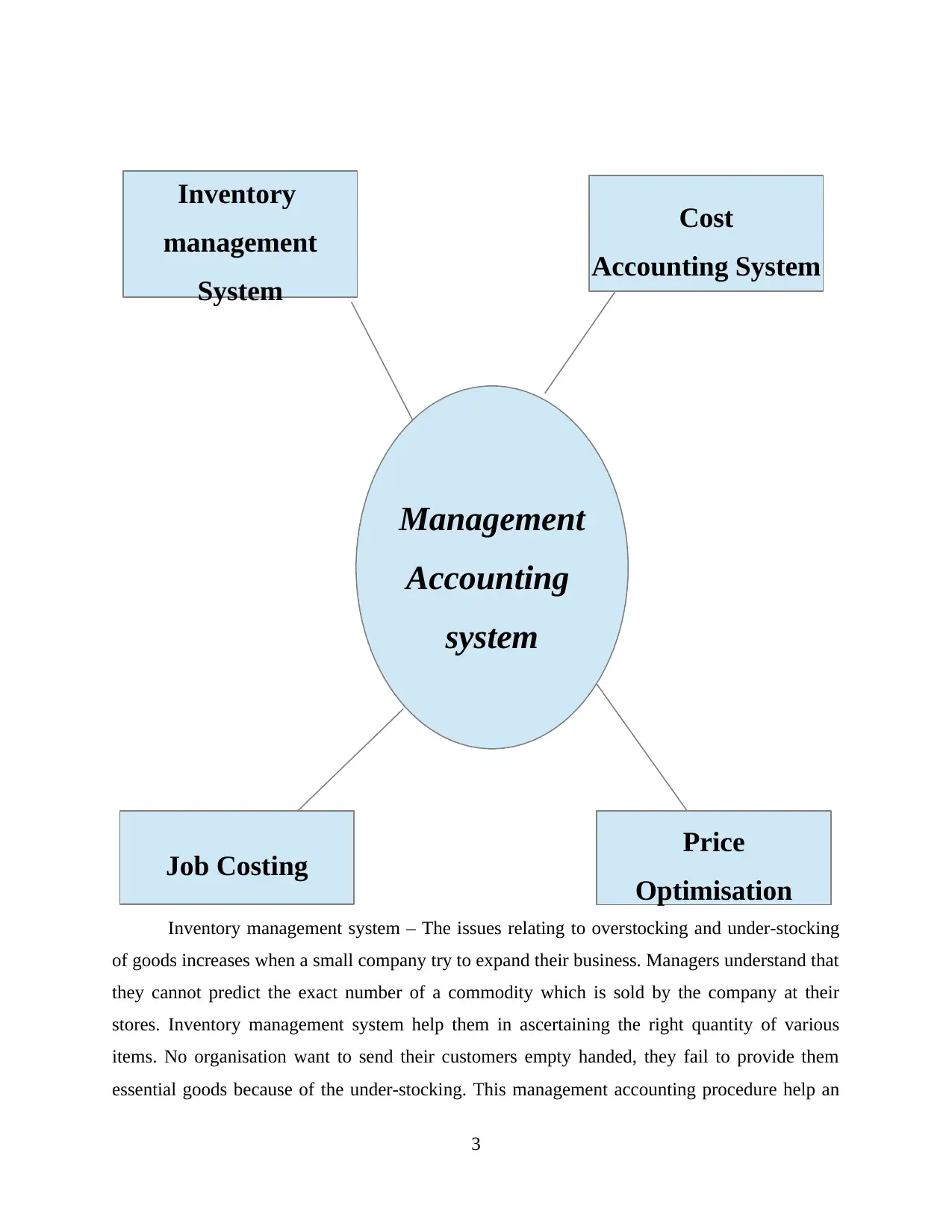

Inventory management system – The issues relating to overstocking and under-stocking

of goods increases when a small company try to expand their business. Managers understand that

they cannot predict the exact number of a commodity which is sold by the company at their

stores. Inventory management system help them in ascertaining the right quantity of various

items. No organisation want to send their customers empty handed, they fail to provide them

essential goods because of the under-stocking. This management accounting procedure help an

3

Management

Accounting

system

Inventory

management

System

Cost

Accounting System

Price

Optimisation

Job Costing

of goods increases when a small company try to expand their business. Managers understand that

they cannot predict the exact number of a commodity which is sold by the company at their

stores. Inventory management system help them in ascertaining the right quantity of various

items. No organisation want to send their customers empty handed, they fail to provide them

essential goods because of the under-stocking. This management accounting procedure help an

3

Management

Accounting

system

Inventory

management

System

Cost

Accounting System

Price

Optimisation

Job Costing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

enterprises in creating a proper balance between demand and supply different products. If also

minimises the wastages and reduce carrying and ordering cost. Earlier managers has to do this

work manually but now can use sofa-tares for accomplishing this task in an effective way.

Price optimisation – Decision a price which is suitable for both an enterprise and their

customers is very difficult. Sometime buyer refuse the buy a product on the ground that it is too

expensive. But at the same time, in the views of company, the rates are economical (Chen,

Weikart and Williams, 2014). A reverse situation can also take place where consumer are ready

to pay more money for an item but corporation did not understand the buying patter of

customers. This basically result in huge and unnecessary loss. Price optimisation play key role at

the time of making call regarding ''what should be the price of a product''. This system assist in

increasing the number of permanent buyers.

Job costing – Some jobs in a company has high significance, because they generate more

revenue, while other are not very important for an enterprise. Every job is analysed on the

individual basis, this help an organisation in reducing their cost and it also support managers in

easily focusing on the work which is generate more profit for the corporation. Material, labour

and overhead are three types of cost that is involved in this management accounting system.

Cost accounting system – This is general approach and it has wide reach. It concentrate in

reducing the expenses by identifying the areas in the production system where company is doing

unnecessary expenditure. Profit can be increased by either enhancing sale or reducing total cost

of operation.

4

minimises the wastages and reduce carrying and ordering cost. Earlier managers has to do this

work manually but now can use sofa-tares for accomplishing this task in an effective way.

Price optimisation – Decision a price which is suitable for both an enterprise and their

customers is very difficult. Sometime buyer refuse the buy a product on the ground that it is too

expensive. But at the same time, in the views of company, the rates are economical (Chen,

Weikart and Williams, 2014). A reverse situation can also take place where consumer are ready

to pay more money for an item but corporation did not understand the buying patter of

customers. This basically result in huge and unnecessary loss. Price optimisation play key role at

the time of making call regarding ''what should be the price of a product''. This system assist in

increasing the number of permanent buyers.

Job costing – Some jobs in a company has high significance, because they generate more

revenue, while other are not very important for an enterprise. Every job is analysed on the

individual basis, this help an organisation in reducing their cost and it also support managers in

easily focusing on the work which is generate more profit for the corporation. Material, labour

and overhead are three types of cost that is involved in this management accounting system.

Cost accounting system – This is general approach and it has wide reach. It concentrate in

reducing the expenses by identifying the areas in the production system where company is doing

unnecessary expenditure. Profit can be increased by either enhancing sale or reducing total cost

of operation.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2 Explain different methods used for management accounting reporting that can also be used

for the chosen scenario

Report is basically the observation and investigation of company's performance.

Reporting tell the top level; management about the set targets and and actual results. It also

shows the areas where an enterprise can improve their performance. Some methods of

management accounting reporting are as follows:

Account receivable reporting – This report is made for maintaining a good relation with

debtors. Unicorn grocery is operating at small level and they understand that in order to make

permanent customer they have to provide credit facility to their customers. It provide them

competitive advantages on their competitors (Cokins, 2013). A/C receivable report contain the

details about people who owe money to the company. It also reveal the time period for which

they are holding the sum. Some organisation like to keep the records on the basis of time while

other prefer the amount that is due on the customers. This report assist in decreasing the amount

of bad debts. This can be considered as one of the prime reason behind formation of this report.

By taking assistance from this report, cited firm can tighten the rules for the debtors who are not

paying their debts in allotted time.

Account payable reporting – Keeping good connection with suppliers is crucial for the

success of the business because they are significant shareholder of the enterprise. Account

payable report is made for determining the amounts which company has paid to their suppliers.

Maintaining a record help an organisation in minimising their expenses. Manager can found the

extra amount which they have to pay to their supplier, in the name of interest, because they fail

to make payment in time (Delafrooz and Paim, 2011).

Budget reporting – Every firm make budget so they can invest their resources in proper

way. Budget report is made by using previous year data. It shows all the planned and actual

expenses & income. If a company is running their business at a large level then they has to focus

on performance of different departments but a small firm like Unicorn grocery can make this

budget for determining the performance of their employees. This importance of budget report has

increase in past several years because it shows the right the direction to a company. If a company

has clear plans in their budget then they can remove the issues of conflicts. Budget report of past

year can be used for making next years budget, it will increase the accuracy of the budget.

5

for the chosen scenario

Report is basically the observation and investigation of company's performance.

Reporting tell the top level; management about the set targets and and actual results. It also

shows the areas where an enterprise can improve their performance. Some methods of

management accounting reporting are as follows:

Account receivable reporting – This report is made for maintaining a good relation with

debtors. Unicorn grocery is operating at small level and they understand that in order to make

permanent customer they have to provide credit facility to their customers. It provide them

competitive advantages on their competitors (Cokins, 2013). A/C receivable report contain the

details about people who owe money to the company. It also reveal the time period for which

they are holding the sum. Some organisation like to keep the records on the basis of time while

other prefer the amount that is due on the customers. This report assist in decreasing the amount

of bad debts. This can be considered as one of the prime reason behind formation of this report.

By taking assistance from this report, cited firm can tighten the rules for the debtors who are not

paying their debts in allotted time.

Account payable reporting – Keeping good connection with suppliers is crucial for the

success of the business because they are significant shareholder of the enterprise. Account

payable report is made for determining the amounts which company has paid to their suppliers.

Maintaining a record help an organisation in minimising their expenses. Manager can found the

extra amount which they have to pay to their supplier, in the name of interest, because they fail

to make payment in time (Delafrooz and Paim, 2011).

Budget reporting – Every firm make budget so they can invest their resources in proper

way. Budget report is made by using previous year data. It shows all the planned and actual

expenses & income. If a company is running their business at a large level then they has to focus

on performance of different departments but a small firm like Unicorn grocery can make this

budget for determining the performance of their employees. This importance of budget report has

increase in past several years because it shows the right the direction to a company. If a company

has clear plans in their budget then they can remove the issues of conflicts. Budget report of past

year can be used for making next years budget, it will increase the accuracy of the budget.

5

Inventory control reporting – Managing inventory is a significant task for any retail

company. This report reveal the mistakes which a company has committed at the time of

ordering the good (Ekbatani and Sangeladji, 2011). An organisation can reduce cost of their

business if they order right quantity of good in right time. Significant techniques like EOQ is

used at the time of making this report. This report can help in ascertaining the right quantity of

the good which a company should keep in their stores. Unicorn grocery is small firm, facing

trouble of overstocking and low supply of some commodities can make a huge impact on their

business. By using this report, they can make effective plan for future events.

Performance reporting – This type of report focuses on performance of various divisions

of a company. But Unicorn grocery do not any major division so they can make this report for

analysing the performance of every employees who is working in this organisation. If a worker is

giving better then expected results then company can give him or her more responsibilities and

incentives in next year. Other kind of reporting only focus on a particular task but performance

reporting cover whole organisation. A report is basically the observation made by managers. If

they are used for in effective way then commit can stop committing same mistakes which they

are doing from many years.

Job costing reporting – This report is made for analysing the profitability of a job. It

shows that which job is help company in earning more revenue while which jobs are only

increasing the cost of business and does not contributing much in the profit. Most of the

companies make this report for decreasing the unwanted expenses (Foster, Hart and Lewis,

2011).

6

company. This report reveal the mistakes which a company has committed at the time of

ordering the good (Ekbatani and Sangeladji, 2011). An organisation can reduce cost of their

business if they order right quantity of good in right time. Significant techniques like EOQ is

used at the time of making this report. This report can help in ascertaining the right quantity of

the good which a company should keep in their stores. Unicorn grocery is small firm, facing

trouble of overstocking and low supply of some commodities can make a huge impact on their

business. By using this report, they can make effective plan for future events.

Performance reporting – This type of report focuses on performance of various divisions

of a company. But Unicorn grocery do not any major division so they can make this report for

analysing the performance of every employees who is working in this organisation. If a worker is

giving better then expected results then company can give him or her more responsibilities and

incentives in next year. Other kind of reporting only focus on a particular task but performance

reporting cover whole organisation. A report is basically the observation made by managers. If

they are used for in effective way then commit can stop committing same mistakes which they

are doing from many years.

Job costing reporting – This report is made for analysing the profitability of a job. It

shows that which job is help company in earning more revenue while which jobs are only

increasing the cost of business and does not contributing much in the profit. Most of the

companies make this report for decreasing the unwanted expenses (Foster, Hart and Lewis,

2011).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LO 2 Apply a range of management accounting techniques

P3 Difference between income statement made through marginal and absorption costing

Management accounting is used in improving the performance a company so they can

achieve their goals and move forward towards their mission. By reducing the expenditure done

by the corporation cited firm can enhance their net profit. Costing basically focus in finding and

minimising the wastage. Below are explanation of marginal and absorption costing along with

their difference:

Marginal costing – Every corporation want to increase their production. Whenever they

produce an extra unit, they have to spend some more money. This extra amount is known by the

name of marginal costing. This approach is completely different from tradition. The

differentiation in the fixed and variable cost is the core this form of costing. Other approaches

always include fixed cost in the cost of the product but in marginal costing, fixed cost is ignored.

According to this accounting technique, fixed expenditure should be recover in a period of time

instead of allocating the burden of fixed cost on every unit produced in the factory (Fullerton,

Kennedy and Widener, 2014). One should always keep in mind the assumption which are present

in this approach. The first is that all the unit produced by the company are sold in the market,

second is that the selling price of goods remain same at all the levels of activities.

Absorption costing – It is a old method where both fixed and variable cost is considered

at the time of determining the price of a product. If some goods remain unsold then the

expenditure incurred on them in treated in next year. Direct labour, material and manufacturing

overheads are included in this form of costing. The allocation of fixed cost is done on every unit

that is made by the company. Some may find this approach an old management accounting

technique but it does not mean that it is useless. In reality, it shows correct amount of net profit

that is registered by a an enterprise.

Comparison between marginal and absorption costing

Basis Marginal costing Absorption costing

Level of Inventory Closing stock affect net profit

under marginal costing.

Closing stock does not affect

the level of profit.

Assumption It is assumed that all the

manufactured units are sold by

This of assumption is not

present under absorption

7

P3 Difference between income statement made through marginal and absorption costing

Management accounting is used in improving the performance a company so they can

achieve their goals and move forward towards their mission. By reducing the expenditure done

by the corporation cited firm can enhance their net profit. Costing basically focus in finding and

minimising the wastage. Below are explanation of marginal and absorption costing along with

their difference:

Marginal costing – Every corporation want to increase their production. Whenever they

produce an extra unit, they have to spend some more money. This extra amount is known by the

name of marginal costing. This approach is completely different from tradition. The

differentiation in the fixed and variable cost is the core this form of costing. Other approaches

always include fixed cost in the cost of the product but in marginal costing, fixed cost is ignored.

According to this accounting technique, fixed expenditure should be recover in a period of time

instead of allocating the burden of fixed cost on every unit produced in the factory (Fullerton,

Kennedy and Widener, 2014). One should always keep in mind the assumption which are present

in this approach. The first is that all the unit produced by the company are sold in the market,

second is that the selling price of goods remain same at all the levels of activities.

Absorption costing – It is a old method where both fixed and variable cost is considered

at the time of determining the price of a product. If some goods remain unsold then the

expenditure incurred on them in treated in next year. Direct labour, material and manufacturing

overheads are included in this form of costing. The allocation of fixed cost is done on every unit

that is made by the company. Some may find this approach an old management accounting

technique but it does not mean that it is useless. In reality, it shows correct amount of net profit

that is registered by a an enterprise.

Comparison between marginal and absorption costing

Basis Marginal costing Absorption costing

Level of Inventory Closing stock affect net profit

under marginal costing.

Closing stock does not affect

the level of profit.

Assumption It is assumed that all the

manufactured units are sold by

This of assumption is not

present under absorption

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the end of the year. costing.

Treatment of fixed cost Fixed cost is neglected at the

time of finding the cost of an

item.

Fixed cost become part of final

cost of the product.

Valuation of inventory The amount of inventory is

calculated by considering only

variable cost.

Both fixed and variable cost is

taken in account for

determining the value of the

inventory.

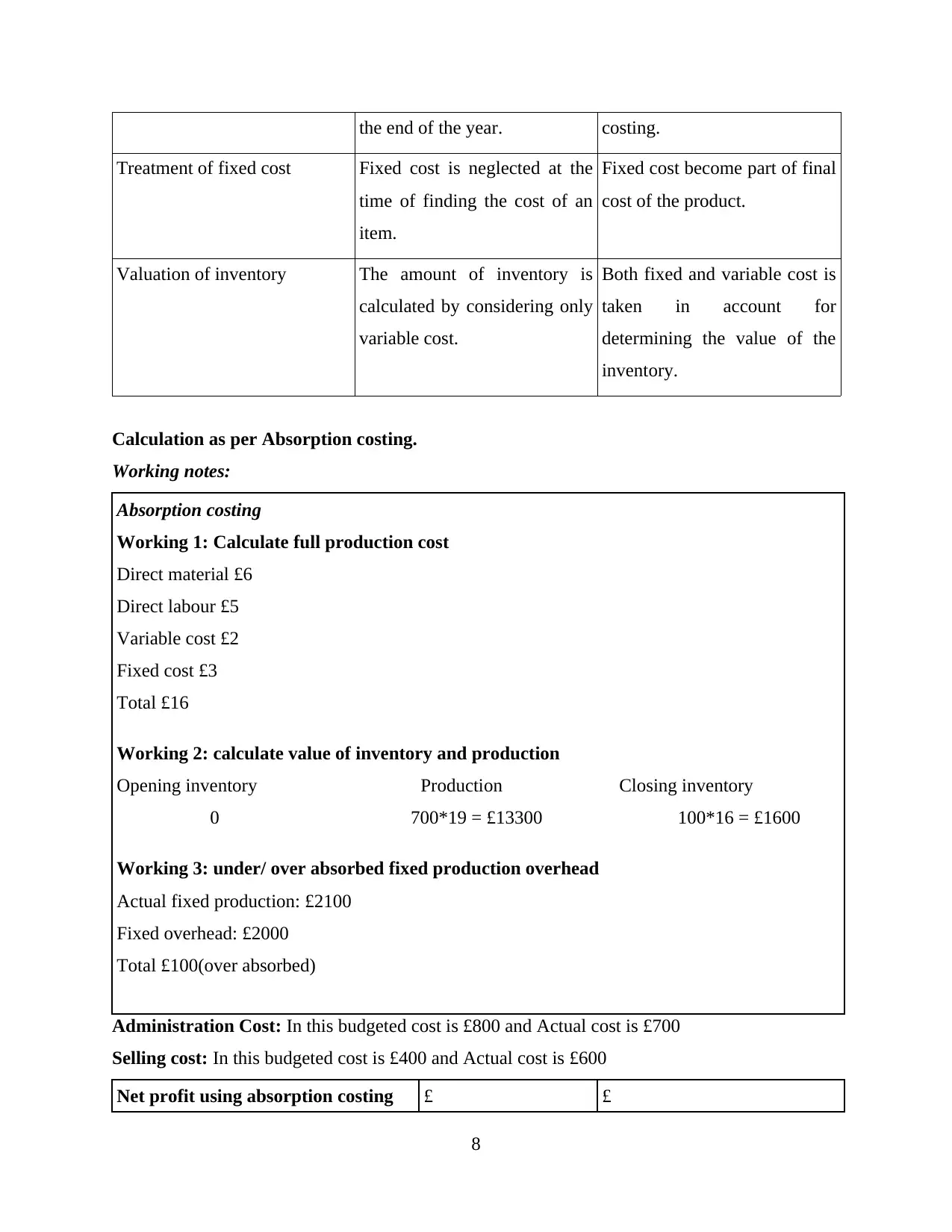

Calculation as per Absorption costing.

Working notes:

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £2

Fixed cost £3

Total £16

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*16 = £1600

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £2100

Fixed overhead: £2000

Total £100(over absorbed)

Administration Cost: In this budgeted cost is £800 and Actual cost is £700

Selling cost: In this budgeted cost is £400 and Actual cost is £600

Net profit using absorption costing £ £

8

Treatment of fixed cost Fixed cost is neglected at the

time of finding the cost of an

item.

Fixed cost become part of final

cost of the product.

Valuation of inventory The amount of inventory is

calculated by considering only

variable cost.

Both fixed and variable cost is

taken in account for

determining the value of the

inventory.

Calculation as per Absorption costing.

Working notes:

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £2

Fixed cost £3

Total £16

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*16 = £1600

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £2100

Fixed overhead: £2000

Total £100(over absorbed)

Administration Cost: In this budgeted cost is £800 and Actual cost is £700

Selling cost: In this budgeted cost is £400 and Actual cost is £600

Net profit using absorption costing £ £

8

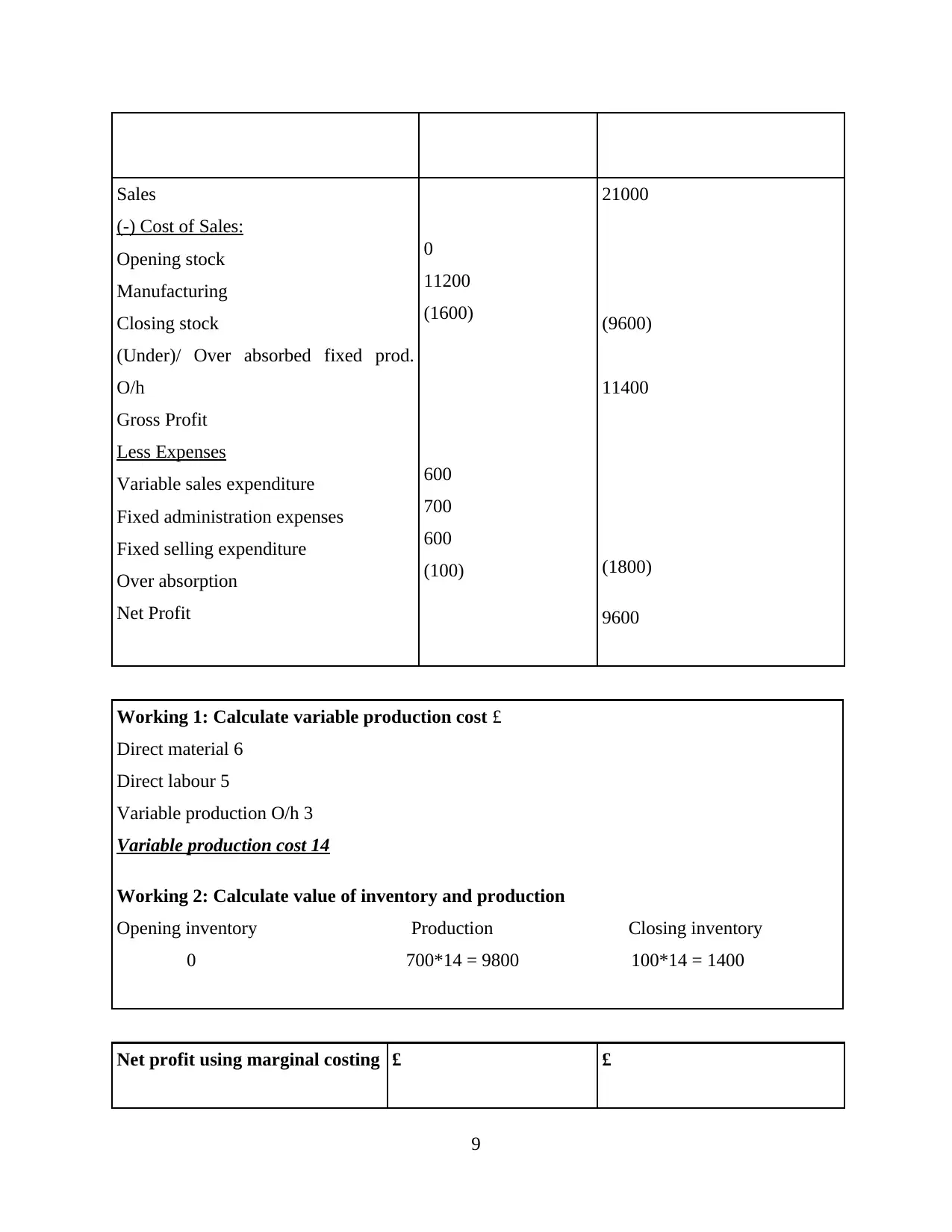

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed administration expenses

Fixed selling expenditure

Over absorption

Net Profit

0

11200

(1600)

600

700

600

(100)

21000

(9600)

11400

(1800)

9600

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Net profit using marginal costing £ £

9

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed administration expenses

Fixed selling expenditure

Over absorption

Net Profit

0

11200

(1600)

600

700

600

(100)

21000

(9600)

11400

(1800)

9600

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Net profit using marginal costing £ £

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.