Management Accounting Report: Financial Problem Solving and Analysis

VerifiedAdded on 2021/02/17

|12

|3121

|37

Report

AI Summary

This report delves into the core concepts of management accounting, focusing on costing techniques, budgetary controls, and variance analysis. It begins by defining management accounting and its various systems, then explores different reporting methods used in managerial accounting. The report includes calculations of costing techniques like marginal and absorption costing, along with the preparation of profit and loss accounts. It also examines the merits and demerits of different budgetary control methods, and concludes by applying management accounting techniques to address financial problems. The report provides detailed calculations of labor and material variances, offering a practical understanding of financial analysis and decision-making in a business context. The analysis is based on a case study of TSR Pvt. Ltd., demonstrating the practical application of these concepts.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION..............................................................................................................1

TASK 1 ........................................................................................................................... 1

P1: Define management accounting and various types of management accounting

systems....................................................................................................................1

P2: Discuss various methods utilised in managerial accounting reporting .............2

TASK 2.............................................................................................................................4

P3: Calculating cost of techniques and preparation of profit and loss account........4

TASK 3.............................................................................................................................7

P4: Merits and Demerits of different types of Budgetary controls............................7

TASK 4.............................................................................................................................8

P5: Using management accounting techniques in responding to financial problems8

REFERENCES...............................................................................................................10

INTRODUCTION..............................................................................................................1

TASK 1 ........................................................................................................................... 1

P1: Define management accounting and various types of management accounting

systems....................................................................................................................1

P2: Discuss various methods utilised in managerial accounting reporting .............2

TASK 2.............................................................................................................................4

P3: Calculating cost of techniques and preparation of profit and loss account........4

TASK 3.............................................................................................................................7

P4: Merits and Demerits of different types of Budgetary controls............................7

TASK 4.............................................................................................................................8

P5: Using management accounting techniques in responding to financial problems8

REFERENCES...............................................................................................................10

INTRODUCTION

Management accounting is one of the branch of accounting is related with the

process of preparation of the accounting reports which is prepared so that the internal

management of company can make decision regarding the Objectives of the company

and determine the policies according to the future trends of the market. Managerial

accounting reports are prepared by the accountants of company by utilising financial

statements of the company such as Balance sheet, Statement of profit and loss account

and cash flow statement. These reports also consider the future economic and Non

economic activities of market that will be prevalent in future.

This report is prepared on TSR pvt. Ltd. and discusses about the significance of

management accounting and techniques. Various planning tools used in management

accounting process and the use of accounting tools that assists in responding to

financial problem.

TASK 1

P1: Define management accounting and various types of management accounting

systems

Management accounting is the process of accounting which deals with the

preparation of managerial accounting reports so that the internal management of the

company can determine the objectives and formulate policies for the company by

utilising those reports. Managerial accounting reports make use of the financial

statements of the company and also considers the future economic and non economic

activities of the market that will be prevalent in future so that the managers can make

decision effectively and it does not impact the operations of the company in future.

Types of management accounting system and their need in organisation:

The system of management accounting are formulated in such a manner that

help the managers to prepare the accounts and reports so that the managers can take

effective decisions for the company.

Product Costing: This process of costing is utilised to make the estimation

about the all over cost that is used in the production of a specific product. This

assist the managers in making estimation about the expenses that is incurred in

1

Management accounting is one of the branch of accounting is related with the

process of preparation of the accounting reports which is prepared so that the internal

management of company can make decision regarding the Objectives of the company

and determine the policies according to the future trends of the market. Managerial

accounting reports are prepared by the accountants of company by utilising financial

statements of the company such as Balance sheet, Statement of profit and loss account

and cash flow statement. These reports also consider the future economic and Non

economic activities of market that will be prevalent in future.

This report is prepared on TSR pvt. Ltd. and discusses about the significance of

management accounting and techniques. Various planning tools used in management

accounting process and the use of accounting tools that assists in responding to

financial problem.

TASK 1

P1: Define management accounting and various types of management accounting

systems

Management accounting is the process of accounting which deals with the

preparation of managerial accounting reports so that the internal management of the

company can determine the objectives and formulate policies for the company by

utilising those reports. Managerial accounting reports make use of the financial

statements of the company and also considers the future economic and non economic

activities of the market that will be prevalent in future so that the managers can make

decision effectively and it does not impact the operations of the company in future.

Types of management accounting system and their need in organisation:

The system of management accounting are formulated in such a manner that

help the managers to prepare the accounts and reports so that the managers can take

effective decisions for the company.

Product Costing: This process of costing is utilised to make the estimation

about the all over cost that is used in the production of a specific product. This

assist the managers in making estimation about the expenses that is incurred in

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the process and allocating those overheads. This system can be implemented in

the small business organisation which have simple business operations.

Cost accounting system: This system of accounting is used to estimate the

overall cost and expenses that will be incurred in the operation of business. This

system assists the managers in making an estimation about the expenses that

will incurred in future, which makes the easy in allocating the funds accordingly

and in turn also helps the company in determining the profitability of the

business.

Inventory management system: The Inventory management systems is

adopted by every organisation no matter what is its size, as every company has

the responsibility to efficiently manage the stocks of the company. This system

deals with the management of inventory level of the company in such a manner

that manufacturing department and final consumers get the goods as and when

required. Different companies use the different systems of Inventory

management for efficiently managing their stock levels. The different types of

inventory management systems that are adopted by the companies include

LIFO, FIFO, weighted average system etc. as per the nature of the products of

organisation.

Job costing: Under this costing methods the managers of the company get an

estimation about the cost of the similar units of the product or regarding the

particular job function. This helps the internal management in estimating the

profitability from the specific job function, so that they can invest the funds of the

company in those job function which are most profitable.

P2: Discuss various methods utilised in managerial accounting reporting

The reports that are made under managerial accounting are formulated for the

purpose of supporting internal management in the decision making process and making

policies for the company. These reports include financial as well as non financial

transactions that has been adoptedtaken in the companies. This is the reason why it is

so significant to prepare these reports. The various reports prepared under managerial

accounting are as under:

2

the small business organisation which have simple business operations.

Cost accounting system: This system of accounting is used to estimate the

overall cost and expenses that will be incurred in the operation of business. This

system assists the managers in making an estimation about the expenses that

will incurred in future, which makes the easy in allocating the funds accordingly

and in turn also helps the company in determining the profitability of the

business.

Inventory management system: The Inventory management systems is

adopted by every organisation no matter what is its size, as every company has

the responsibility to efficiently manage the stocks of the company. This system

deals with the management of inventory level of the company in such a manner

that manufacturing department and final consumers get the goods as and when

required. Different companies use the different systems of Inventory

management for efficiently managing their stock levels. The different types of

inventory management systems that are adopted by the companies include

LIFO, FIFO, weighted average system etc. as per the nature of the products of

organisation.

Job costing: Under this costing methods the managers of the company get an

estimation about the cost of the similar units of the product or regarding the

particular job function. This helps the internal management in estimating the

profitability from the specific job function, so that they can invest the funds of the

company in those job function which are most profitable.

P2: Discuss various methods utilised in managerial accounting reporting

The reports that are made under managerial accounting are formulated for the

purpose of supporting internal management in the decision making process and making

policies for the company. These reports include financial as well as non financial

transactions that has been adoptedtaken in the companies. This is the reason why it is

so significant to prepare these reports. The various reports prepared under managerial

accounting are as under:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Budget reports: The budgets are preparedin process . The budgets are

prepared for the purpose of estimating the expenses that will be incurred in the process,

the amount of funds that will be utilised in the process and the profitability that will be

generated from the operation. The budgets that are prepared in the companies include

Sales Budget, Purchases Budget, Production Budget etc. The preparation of budgets

also helps managers in setting the performance standards for the company and then

taking corrective actions if there are any variations.

Accounts receivable reports: This report is prepared to manage the Accounts

receivable of the company. Under this report the estimation is made regarding the

debtors that the company currently have and when the payment is to be received from

them. This report also identifies those debtors from which the company have not

received the payments on time and debtors have gone bad or are doubtful. This assists

the managers in tightening or loosening the credit policy of the company as per the

results.

Job cost reports: These reports make an estimation regarding the total

revenues and cost that is being generated from undertaking or manufacturing a batch of

product or a specific product. This assists the internal management of the company in

making the estimation regarding the profitability that is generated from the production of

those products, so that managers can allocate the funds in the process accordingly.

Significance of information collected from managerial accounting reports:

Decision making: The reports that are made under managerial accounting helps

the managers of the company in making efficient decision for the company. These

reports make use of financial statements as well as economic and non economic

activities of market so that it provides the complete information to the mangers of TSR

Pvt Ltd. essential for decision making .

Cost reduction: The managerial accounting reports helps the company in

determining objectives and Formulating policies for the company. This helps the

managers in the managing the operations effectively and thus reduces the cost of

operations by identifying and eliminating the problems in advance.

3

prepared for the purpose of estimating the expenses that will be incurred in the process,

the amount of funds that will be utilised in the process and the profitability that will be

generated from the operation. The budgets that are prepared in the companies include

Sales Budget, Purchases Budget, Production Budget etc. The preparation of budgets

also helps managers in setting the performance standards for the company and then

taking corrective actions if there are any variations.

Accounts receivable reports: This report is prepared to manage the Accounts

receivable of the company. Under this report the estimation is made regarding the

debtors that the company currently have and when the payment is to be received from

them. This report also identifies those debtors from which the company have not

received the payments on time and debtors have gone bad or are doubtful. This assists

the managers in tightening or loosening the credit policy of the company as per the

results.

Job cost reports: These reports make an estimation regarding the total

revenues and cost that is being generated from undertaking or manufacturing a batch of

product or a specific product. This assists the internal management of the company in

making the estimation regarding the profitability that is generated from the production of

those products, so that managers can allocate the funds in the process accordingly.

Significance of information collected from managerial accounting reports:

Decision making: The reports that are made under managerial accounting helps

the managers of the company in making efficient decision for the company. These

reports make use of financial statements as well as economic and non economic

activities of market so that it provides the complete information to the mangers of TSR

Pvt Ltd. essential for decision making .

Cost reduction: The managerial accounting reports helps the company in

determining objectives and Formulating policies for the company. This helps the

managers in the managing the operations effectively and thus reduces the cost of

operations by identifying and eliminating the problems in advance.

3

TASK 2

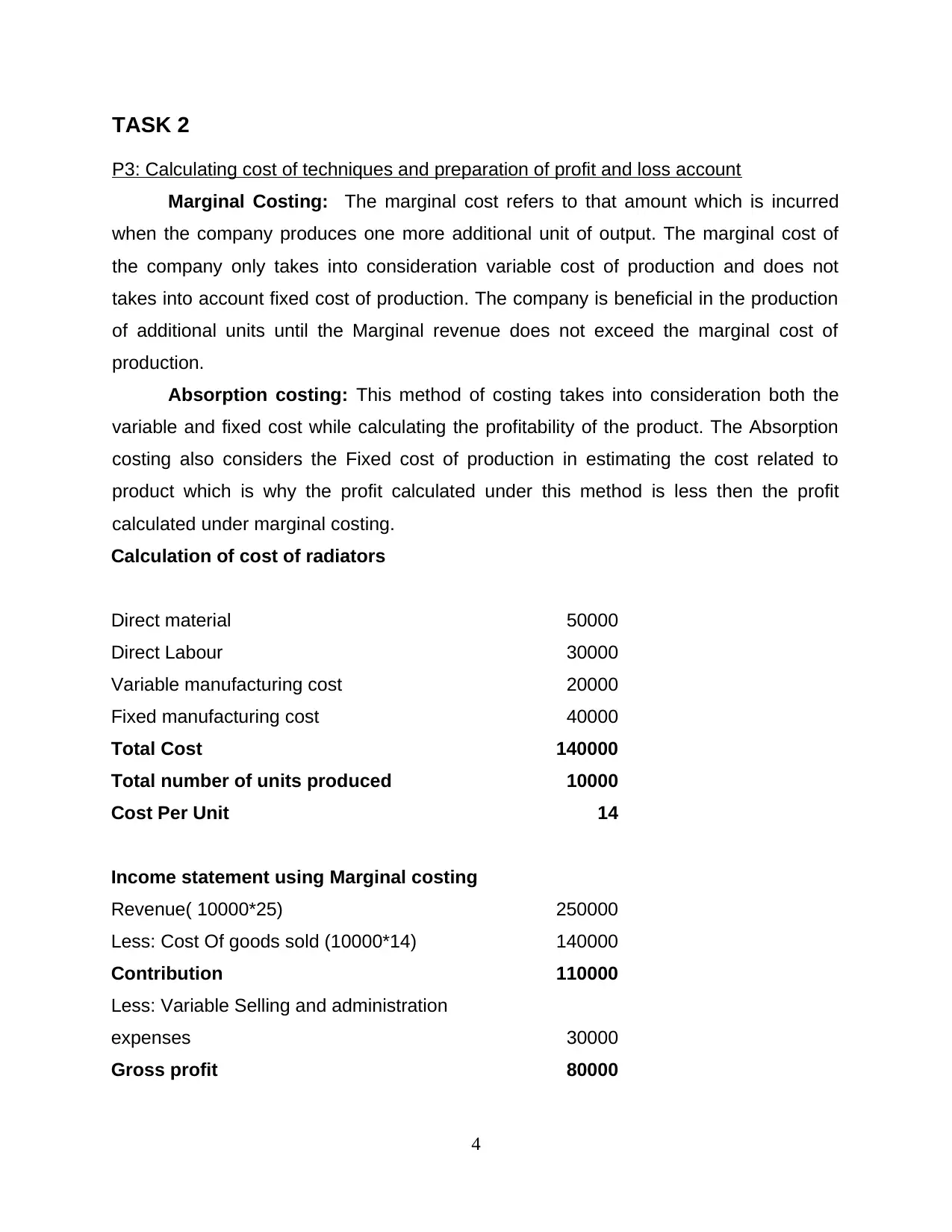

P3: Calculating cost of techniques and preparation of profit and loss account

Marginal Costing: The marginal cost refers to that amount which is incurred

when the company produces one more additional unit of output. The marginal cost of

the company only takes into consideration variable cost of production and does not

takes into account fixed cost of production. The company is beneficial in the production

of additional units until the Marginal revenue does not exceed the marginal cost of

production.

Absorption costing: This method of costing takes into consideration both the

variable and fixed cost while calculating the profitability of the product. The Absorption

costing also considers the Fixed cost of production in estimating the cost related to

product which is why the profit calculated under this method is less then the profit

calculated under marginal costing.

Calculation of cost of radiators

Direct material 50000

Direct Labour 30000

Variable manufacturing cost 20000

Fixed manufacturing cost 40000

Total Cost 140000

Total number of units produced 10000

Cost Per Unit 14

Income statement using Marginal costing

Revenue( 10000*25) 250000

Less: Cost Of goods sold (10000*14) 140000

Contribution 110000

Less: Variable Selling and administration

expenses 30000

Gross profit 80000

4

P3: Calculating cost of techniques and preparation of profit and loss account

Marginal Costing: The marginal cost refers to that amount which is incurred

when the company produces one more additional unit of output. The marginal cost of

the company only takes into consideration variable cost of production and does not

takes into account fixed cost of production. The company is beneficial in the production

of additional units until the Marginal revenue does not exceed the marginal cost of

production.

Absorption costing: This method of costing takes into consideration both the

variable and fixed cost while calculating the profitability of the product. The Absorption

costing also considers the Fixed cost of production in estimating the cost related to

product which is why the profit calculated under this method is less then the profit

calculated under marginal costing.

Calculation of cost of radiators

Direct material 50000

Direct Labour 30000

Variable manufacturing cost 20000

Fixed manufacturing cost 40000

Total Cost 140000

Total number of units produced 10000

Cost Per Unit 14

Income statement using Marginal costing

Revenue( 10000*25) 250000

Less: Cost Of goods sold (10000*14) 140000

Contribution 110000

Less: Variable Selling and administration

expenses 30000

Gross profit 80000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

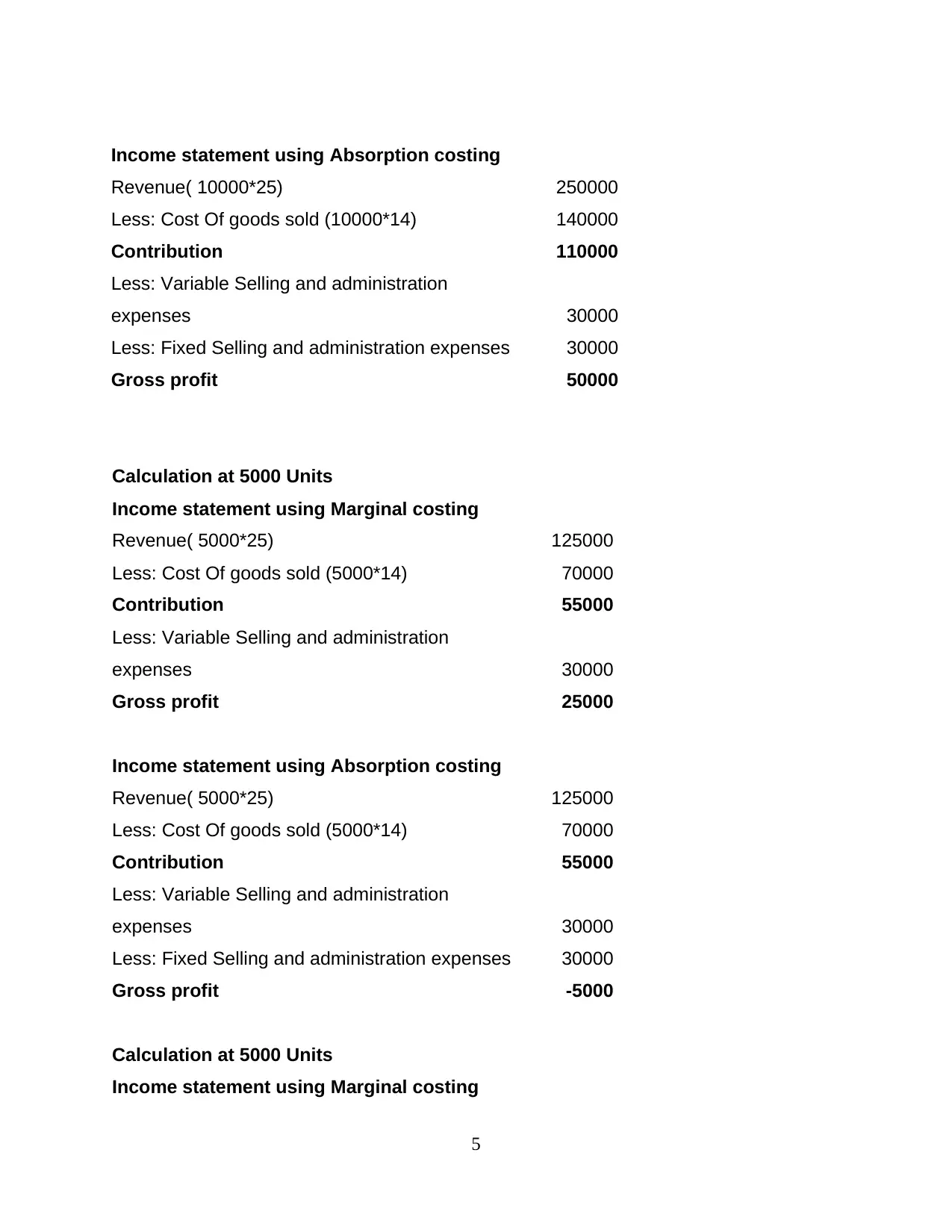

Income statement using Absorption costing

Revenue( 10000*25) 250000

Less: Cost Of goods sold (10000*14) 140000

Contribution 110000

Less: Variable Selling and administration

expenses 30000

Less: Fixed Selling and administration expenses 30000

Gross profit 50000

Calculation at 5000 Units

Income statement using Marginal costing

Revenue( 5000*25) 125000

Less: Cost Of goods sold (5000*14) 70000

Contribution 55000

Less: Variable Selling and administration

expenses 30000

Gross profit 25000

Income statement using Absorption costing

Revenue( 5000*25) 125000

Less: Cost Of goods sold (5000*14) 70000

Contribution 55000

Less: Variable Selling and administration

expenses 30000

Less: Fixed Selling and administration expenses 30000

Gross profit -5000

Calculation at 5000 Units

Income statement using Marginal costing

5

Revenue( 10000*25) 250000

Less: Cost Of goods sold (10000*14) 140000

Contribution 110000

Less: Variable Selling and administration

expenses 30000

Less: Fixed Selling and administration expenses 30000

Gross profit 50000

Calculation at 5000 Units

Income statement using Marginal costing

Revenue( 5000*25) 125000

Less: Cost Of goods sold (5000*14) 70000

Contribution 55000

Less: Variable Selling and administration

expenses 30000

Gross profit 25000

Income statement using Absorption costing

Revenue( 5000*25) 125000

Less: Cost Of goods sold (5000*14) 70000

Contribution 55000

Less: Variable Selling and administration

expenses 30000

Less: Fixed Selling and administration expenses 30000

Gross profit -5000

Calculation at 5000 Units

Income statement using Marginal costing

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Revenue( 5000*25) 125000

Less: Cost Of goods sold (5000*14) 70000

Contribution 55000

Less: Variable Selling and administration

expenses 30000

Gross profit 25000

Income statement using Absorption costing

Revenue( 5000*25) 125000

Less: Cost Of goods sold (5000*14) 70000

Contribution 55000

Less: Variable Selling and administration

expenses 30000

Less: Fixed Selling and administration expenses 30000

Gross profit -5000

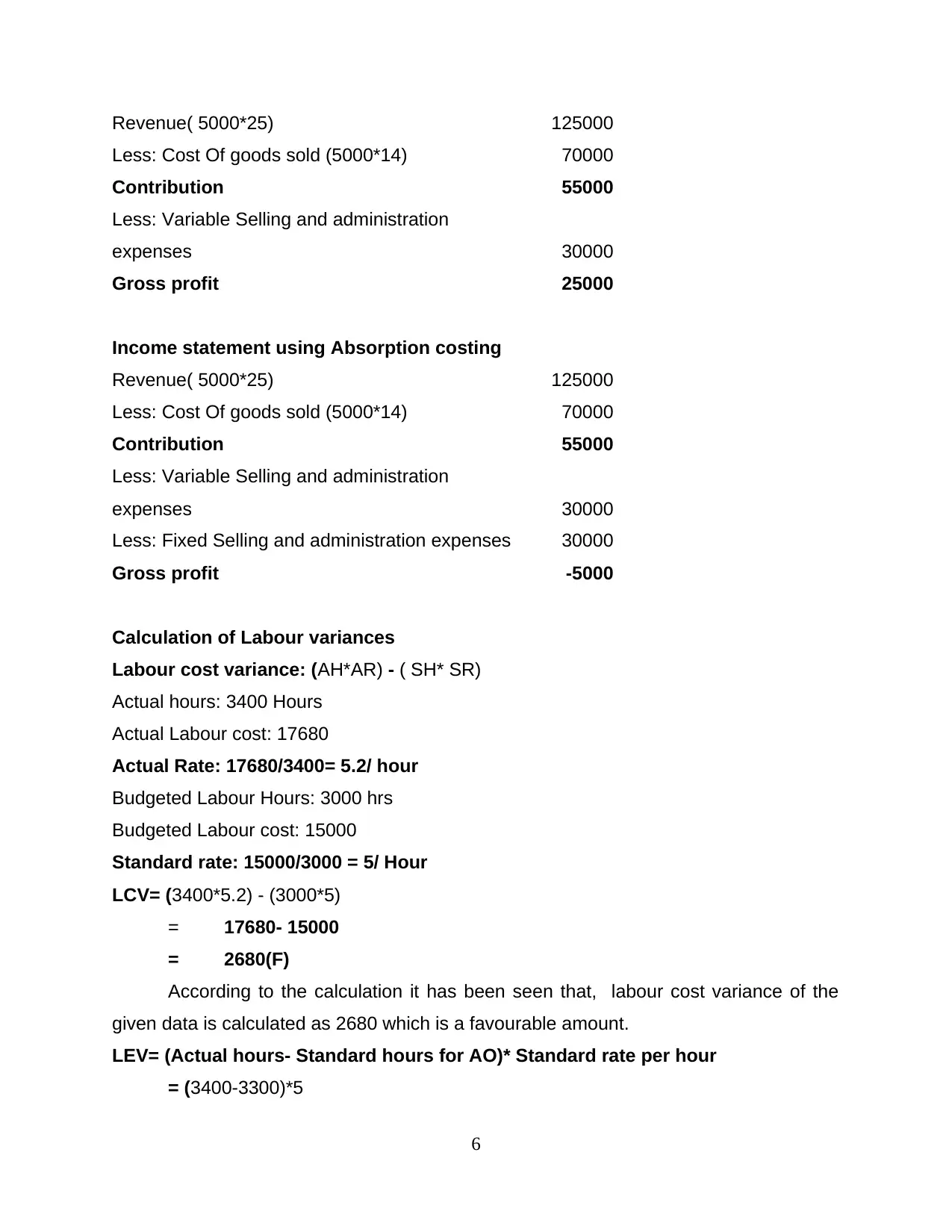

Calculation of Labour variances

Labour cost variance: (AH*AR) - ( SH* SR)

Actual hours: 3400 Hours

Actual Labour cost: 17680

Actual Rate: 17680/3400= 5.2/ hour

Budgeted Labour Hours: 3000 hrs

Budgeted Labour cost: 15000

Standard rate: 15000/3000 = 5/ Hour

LCV= (3400*5.2) - (3000*5)

= 17680- 15000

= 2680(F)

According to the calculation it has been seen that, labour cost variance of the

given data is calculated as 2680 which is a favourable amount.

LEV= (Actual hours- Standard hours for AO)* Standard rate per hour

= (3400-3300)*5

6

Less: Cost Of goods sold (5000*14) 70000

Contribution 55000

Less: Variable Selling and administration

expenses 30000

Gross profit 25000

Income statement using Absorption costing

Revenue( 5000*25) 125000

Less: Cost Of goods sold (5000*14) 70000

Contribution 55000

Less: Variable Selling and administration

expenses 30000

Less: Fixed Selling and administration expenses 30000

Gross profit -5000

Calculation of Labour variances

Labour cost variance: (AH*AR) - ( SH* SR)

Actual hours: 3400 Hours

Actual Labour cost: 17680

Actual Rate: 17680/3400= 5.2/ hour

Budgeted Labour Hours: 3000 hrs

Budgeted Labour cost: 15000

Standard rate: 15000/3000 = 5/ Hour

LCV= (3400*5.2) - (3000*5)

= 17680- 15000

= 2680(F)

According to the calculation it has been seen that, labour cost variance of the

given data is calculated as 2680 which is a favourable amount.

LEV= (Actual hours- Standard hours for AO)* Standard rate per hour

= (3400-3300)*5

6

= 100*5

= 500(F)

Calculation of Material variances:

Material cost variance = (AQ*AP) – (SQ*SP)

Actual Quantity= 2200

Actual Price= 9.5

Standard Quantity= 2000

Standard price= 10/ Kg

MCV= (2200*9.5) - (2000*10)

= 20,900-20000

= 900(F)

Material Usage variance= (Actual Quantity- Standard Quantity) * Standard Price

Actual Quantity= 2200

Standard Quantity= 2000

Standard price= 10/ Kg

MUV= (AQ – SQ) * SP

= (2200-2000)* 10

= 2000(F)

TASK 3

P4: Merits and Demerits of different types of Budgetary controls

There internal management of the company prepares various budgets to

increase the overall efficiency of the organisation. The budget that the company

prepares under this system include Forecasting tools, Contingency Tools, and scenario

Planning. The detailed discussion about these budgets are as under:

Forecasting Tools: This is considered as an efficient technique which is

adopted by the company for the purpose of analysing future trends of the market. This

tool is considered as accurate and reliable by the managers of the company as the

data is collected from both internal and external sources.

7

= 500(F)

Calculation of Material variances:

Material cost variance = (AQ*AP) – (SQ*SP)

Actual Quantity= 2200

Actual Price= 9.5

Standard Quantity= 2000

Standard price= 10/ Kg

MCV= (2200*9.5) - (2000*10)

= 20,900-20000

= 900(F)

Material Usage variance= (Actual Quantity- Standard Quantity) * Standard Price

Actual Quantity= 2200

Standard Quantity= 2000

Standard price= 10/ Kg

MUV= (AQ – SQ) * SP

= (2200-2000)* 10

= 2000(F)

TASK 3

P4: Merits and Demerits of different types of Budgetary controls

There internal management of the company prepares various budgets to

increase the overall efficiency of the organisation. The budget that the company

prepares under this system include Forecasting tools, Contingency Tools, and scenario

Planning. The detailed discussion about these budgets are as under:

Forecasting Tools: This is considered as an efficient technique which is

adopted by the company for the purpose of analysing future trends of the market. This

tool is considered as accurate and reliable by the managers of the company as the

data is collected from both internal and external sources.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advantages: The major benefit of the preparation of this tools is that it creates

value for which every person (Budgetary Control, 2017).

Disadvantages: Under this tool, it is very difficult to properly and accurately

predict the future. Because the nature of information is qualitative.

Contingency Tools: This is considered as an normal process for the analysis of

business performance. This is undertaken in order to determine the risk that is

associated with the overall profitability of the company. In order to deal with these types

of issues the managers are needed to formulate these contingent strategies for making

an analysis of the risk (Maher, Stickney and Weil, 2012).

Advantages: The benefit of this Tool is that it helps the small sized organisations

in measuring growth and profitability.

Disadvantages: The main drawback of this tool is that it is rigid and very costly

as well as time consuming.

Scenario Planning: This is considered as a technique which is systematic and

faced by many organisations so that flexibility can be achieved at the time of the long

term planning. The scenario planning is the process of the company which deals with

the adoption of techniques that are much helpful in generating better outcomes.

Merits: This is the most important tools which is used by the company for the

analysis of uncertainties that are affecting the company's profitability.

Demerits: By using this method it is very difficult to efficiently predict the future.

The alternatives cause many issues in this.

TASK 4

P5: Using management accounting techniques in responding to financial problems

The company should various management accounting tools because these tools

helps the internal management of the company in responding and resolving the financial

issues that are faced by the company during the course of the operations. The tools that

the company can adopt to solve the issues include benchmarking , key performance

indicators , corporate government etc. These will be discussed in brief as under:

8

value for which every person (Budgetary Control, 2017).

Disadvantages: Under this tool, it is very difficult to properly and accurately

predict the future. Because the nature of information is qualitative.

Contingency Tools: This is considered as an normal process for the analysis of

business performance. This is undertaken in order to determine the risk that is

associated with the overall profitability of the company. In order to deal with these types

of issues the managers are needed to formulate these contingent strategies for making

an analysis of the risk (Maher, Stickney and Weil, 2012).

Advantages: The benefit of this Tool is that it helps the small sized organisations

in measuring growth and profitability.

Disadvantages: The main drawback of this tool is that it is rigid and very costly

as well as time consuming.

Scenario Planning: This is considered as a technique which is systematic and

faced by many organisations so that flexibility can be achieved at the time of the long

term planning. The scenario planning is the process of the company which deals with

the adoption of techniques that are much helpful in generating better outcomes.

Merits: This is the most important tools which is used by the company for the

analysis of uncertainties that are affecting the company's profitability.

Demerits: By using this method it is very difficult to efficiently predict the future.

The alternatives cause many issues in this.

TASK 4

P5: Using management accounting techniques in responding to financial problems

The company should various management accounting tools because these tools

helps the internal management of the company in responding and resolving the financial

issues that are faced by the company during the course of the operations. The tools that

the company can adopt to solve the issues include benchmarking , key performance

indicators , corporate government etc. These will be discussed in brief as under:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

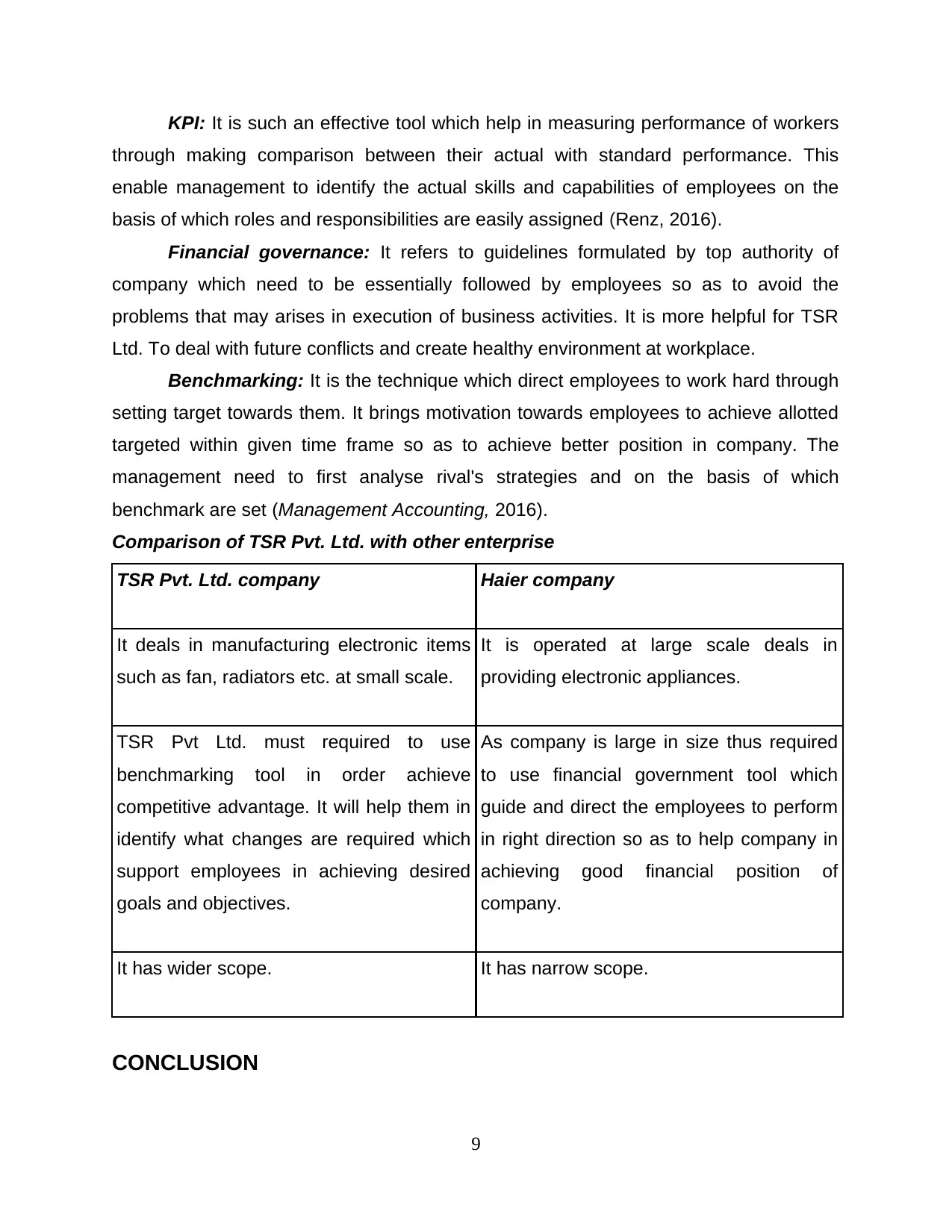

KPI: It is such an effective tool which help in measuring performance of workers

through making comparison between their actual with standard performance. This

enable management to identify the actual skills and capabilities of employees on the

basis of which roles and responsibilities are easily assigned (Renz, 2016).

Financial governance: It refers to guidelines formulated by top authority of

company which need to be essentially followed by employees so as to avoid the

problems that may arises in execution of business activities. It is more helpful for TSR

Ltd. To deal with future conflicts and create healthy environment at workplace.

Benchmarking: It is the technique which direct employees to work hard through

setting target towards them. It brings motivation towards employees to achieve allotted

targeted within given time frame so as to achieve better position in company. The

management need to first analyse rival's strategies and on the basis of which

benchmark are set (Management Accounting, 2016).

Comparison of TSR Pvt. Ltd. with other enterprise

TSR Pvt. Ltd. company Haier company

It deals in manufacturing electronic items

such as fan, radiators etc. at small scale.

It is operated at large scale deals in

providing electronic appliances.

TSR Pvt Ltd. must required to use

benchmarking tool in order achieve

competitive advantage. It will help them in

identify what changes are required which

support employees in achieving desired

goals and objectives.

As company is large in size thus required

to use financial government tool which

guide and direct the employees to perform

in right direction so as to help company in

achieving good financial position of

company.

It has wider scope. It has narrow scope.

CONCLUSION

9

through making comparison between their actual with standard performance. This

enable management to identify the actual skills and capabilities of employees on the

basis of which roles and responsibilities are easily assigned (Renz, 2016).

Financial governance: It refers to guidelines formulated by top authority of

company which need to be essentially followed by employees so as to avoid the

problems that may arises in execution of business activities. It is more helpful for TSR

Ltd. To deal with future conflicts and create healthy environment at workplace.

Benchmarking: It is the technique which direct employees to work hard through

setting target towards them. It brings motivation towards employees to achieve allotted

targeted within given time frame so as to achieve better position in company. The

management need to first analyse rival's strategies and on the basis of which

benchmark are set (Management Accounting, 2016).

Comparison of TSR Pvt. Ltd. with other enterprise

TSR Pvt. Ltd. company Haier company

It deals in manufacturing electronic items

such as fan, radiators etc. at small scale.

It is operated at large scale deals in

providing electronic appliances.

TSR Pvt Ltd. must required to use

benchmarking tool in order achieve

competitive advantage. It will help them in

identify what changes are required which

support employees in achieving desired

goals and objectives.

As company is large in size thus required

to use financial government tool which

guide and direct the employees to perform

in right direction so as to help company in

achieving good financial position of

company.

It has wider scope. It has narrow scope.

CONCLUSION

9

It has been concluded from the above project report that it is essential for an

organization to maintain financial reports and books of accounts in order to know the

actual financial position of company in market. It can be done with the help of adoption

of management accounting and reporting systems which assist management in making

an effective decision regarding achievement of growth and expansion of business.

According to the net profitability, it is must required for TSR Ltd. to use marginal costing

method as compared with absorption costing method. KPI is considered as an effective

financial tool which need to be adopted by company in order to resolve financial issues

and attain strong financial position of company in competitive market world.

10

organization to maintain financial reports and books of accounts in order to know the

actual financial position of company in market. It can be done with the help of adoption

of management accounting and reporting systems which assist management in making

an effective decision regarding achievement of growth and expansion of business.

According to the net profitability, it is must required for TSR Ltd. to use marginal costing

method as compared with absorption costing method. KPI is considered as an effective

financial tool which need to be adopted by company in order to resolve financial issues

and attain strong financial position of company in competitive market world.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.