Comprehensive Management Accounting Report: Techniques and Analysis

VerifiedAdded on 2022/12/26

|26

|4956

|78

Report

AI Summary

This report provides a detailed overview of management accounting principles and techniques. It explores various aspects, including managerial accounting, inventory management systems, job costing, and price optimization. The report delves into the application of absorption costing and marginal costing, along with the preparation of income statements and financial reporting documents. Budgeting, including flexible budget preparation, is also discussed. Furthermore, the report analyzes the integration of management accounting systems and their significance for organizational success, emphasizing the importance of variance analysis and its types. The report uses financial reporting documents to evaluate data for business activities and the formulation of marginal costing techniques. It also discusses the purpose of a budget, budget preparation, and the comparison of organizations in response to financial problems using management accounting.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART 1............................................................................................................................................3

Section 1.................................................................................................................................3

1.1 Managerial Accounting including necessity of various management accounting forms 3

1.2 Application of various methods of management accounting reporting ...........................4

1.3 Benefits and application of management accounting systems in an organisation............5

1.4 Analysis of how management accounting system and Management accounting are

integrated as well as significance of various methods of reporting for organisational success . 6

Section 2.................................................................................................................................7

2.1 Preparation of income statements using absorption costing and marginal costing..........7

2.2 Application of various management accounting techniques and financial reporting

documents...............................................................................................................................8

2.3 Financial reporting which apply and evaluate data for business activities....................10

2.4 Formulation of Marginal costing techniques..................................................................12

PART 2..........................................................................................................................................13

3.1 Purpose of a Budget........................................................................................................13

Budget preparation...............................................................................................................13

3.2 Preparation of Flexible budget.......................................................................................16

4.1 Comparison of organisations in respond to financial problems by adapting to management

accounting ............................................................................................................................16

4.2 Analysis of financial performance of respective companies in regard to management

accounting.............................................................................................................................18

4.3 Evaluation of planning used in Management accounting to reduce financial issues.....19

4.4 Importance of variance analysis and its various types...................................................19

CONCLUSION .............................................................................................................................21

REFERENCES..............................................................................................................................22

INTRODUCTION...........................................................................................................................3

PART 1............................................................................................................................................3

Section 1.................................................................................................................................3

1.1 Managerial Accounting including necessity of various management accounting forms 3

1.2 Application of various methods of management accounting reporting ...........................4

1.3 Benefits and application of management accounting systems in an organisation............5

1.4 Analysis of how management accounting system and Management accounting are

integrated as well as significance of various methods of reporting for organisational success . 6

Section 2.................................................................................................................................7

2.1 Preparation of income statements using absorption costing and marginal costing..........7

2.2 Application of various management accounting techniques and financial reporting

documents...............................................................................................................................8

2.3 Financial reporting which apply and evaluate data for business activities....................10

2.4 Formulation of Marginal costing techniques..................................................................12

PART 2..........................................................................................................................................13

3.1 Purpose of a Budget........................................................................................................13

Budget preparation...............................................................................................................13

3.2 Preparation of Flexible budget.......................................................................................16

4.1 Comparison of organisations in respond to financial problems by adapting to management

accounting ............................................................................................................................16

4.2 Analysis of financial performance of respective companies in regard to management

accounting.............................................................................................................................18

4.3 Evaluation of planning used in Management accounting to reduce financial issues.....19

4.4 Importance of variance analysis and its various types...................................................19

CONCLUSION .............................................................................................................................21

REFERENCES..............................................................................................................................22

INTRODUCTION

Management accounting is a wide concept which covers preparation of different forms of

statements in relevance to managerial decision-making. It is usually utilised by internal staff in

order to evaluate financial information for preparation of reports which will ultimately help in

decision making. In this report, several factors of management accounting will be used in order

to evaluate financial position of company. These factors will include inventory management

system, marginal costing, absorption costing, fixed and variable costs, etc. Such statements will

ultimately help manager in decision-making which is significant for organisational growth and

success in the long term.

PART 1

Section 1

1.1 Managerial Accounting including necessity of various management accounting forms

Management accounting is defined as procedure where financial data is being provided to

the managers so that optimum decision-making can be made for respective organisation. It is

ultimate determination, measurement, aggregation, analysis, formulation and communication of

financial data which will assist in satisfaction of organisational objectives. Managerial

accounting has various aspects of finance which intent to improve quality of data which is being

delivered to management in regard to business operations (Kyriakopoulos and et. al., 2020). This

is mainly centralized at internal management reporting in context to produce decisions by

managers.

Managerial management mostly concerned with budgeting of weekly or monthly data in

order to analyse actual efficiency and effectiveness of company's respective operations which

will aid managers in decision-making. In case of high competitive environment, usually business

entity is required to cope with its competitors in order to sustain in the market for long period.

Therefore it emphasises over future aspects of a business which needs to be pre-determined

through preparation of strategic plans so that company's position and finances stays unaffected in

the market.

Management accounting is a wide concept which covers preparation of different forms of

statements in relevance to managerial decision-making. It is usually utilised by internal staff in

order to evaluate financial information for preparation of reports which will ultimately help in

decision making. In this report, several factors of management accounting will be used in order

to evaluate financial position of company. These factors will include inventory management

system, marginal costing, absorption costing, fixed and variable costs, etc. Such statements will

ultimately help manager in decision-making which is significant for organisational growth and

success in the long term.

PART 1

Section 1

1.1 Managerial Accounting including necessity of various management accounting forms

Management accounting is defined as procedure where financial data is being provided to

the managers so that optimum decision-making can be made for respective organisation. It is

ultimate determination, measurement, aggregation, analysis, formulation and communication of

financial data which will assist in satisfaction of organisational objectives. Managerial

accounting has various aspects of finance which intent to improve quality of data which is being

delivered to management in regard to business operations (Kyriakopoulos and et. al., 2020). This

is mainly centralized at internal management reporting in context to produce decisions by

managers.

Managerial management mostly concerned with budgeting of weekly or monthly data in

order to analyse actual efficiency and effectiveness of company's respective operations which

will aid managers in decision-making. In case of high competitive environment, usually business

entity is required to cope with its competitors in order to sustain in the market for long period.

Therefore it emphasises over future aspects of a business which needs to be pre-determined

through preparation of strategic plans so that company's position and finances stays unaffected in

the market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.2 Application of various methods of management accounting reporting

Management accounting is an effective branch of finance which include flow of decisions

on basis identification, evaluation and communication of produced financial information by

management (Ardiansah and Anisykurlillah, 2020). This financial data is being prepared through

implementation of various management accounting techniques which can be stated as follows:

Inventory management system: It is considered as significant part of management

accounting which is used to keep track of inventory in entire supply chain system. It starts from

purchases of raw material, manufacturing, production of finished goods and ultimately sale of

feasible products. It is convenient approach which helps in overall management of goods from

initial stage till its ultimate sale. This system is helpful for business organisation in order to

achieve its pre-determined profitability in a systematic manner. In this approach various sub

factors are included such as First in first out(FIFO), Last in first out(LIFO) and average cost

method. These methods can be described as follows:

FIFO: This is relevant flow of inventory from initial stage till its final delivery. In this

process, product which is produced first will be first one to be delivered or sold out.

LIFO: This system is connected with the current rate of particular product. It considers

current purchase unit to be sold first which is vice versa of LIFO method.

AVCO: This is unique system of inventory management where average of all inventories

are being calculated in order to reach average cost of per unit of inventory.

Job costing System: This is unit of management accounting where costing method is

used to ascertain cost of specific job or unit in an organisation which is being performed for

ultimate satisfaction of consumers. Through this procedure, value of each individual unit is being

measured so that their respective profits and losses are identified in order to modify effectiveness

and efficiency of operations as per the requirement. It is used to record individual cost to its

particular head in order to reveal relevant profitability so that it could be compared with

budgeted estimates. This way accuracy of jobs can be maintained and necessary modification

could be made in regard to future requirements. Timely records, internal controls, detection of

frauds and errors are also its relevant outcomes which plays significant role in organisational

growth (Schaltegger, 2020). Several documents being in job order costing are manufacturing

order, cost sheet, payrolls, etc. Also it provides detailed structure of material, labour and

overheads costs for each individual job.

Management accounting is an effective branch of finance which include flow of decisions

on basis identification, evaluation and communication of produced financial information by

management (Ardiansah and Anisykurlillah, 2020). This financial data is being prepared through

implementation of various management accounting techniques which can be stated as follows:

Inventory management system: It is considered as significant part of management

accounting which is used to keep track of inventory in entire supply chain system. It starts from

purchases of raw material, manufacturing, production of finished goods and ultimately sale of

feasible products. It is convenient approach which helps in overall management of goods from

initial stage till its ultimate sale. This system is helpful for business organisation in order to

achieve its pre-determined profitability in a systematic manner. In this approach various sub

factors are included such as First in first out(FIFO), Last in first out(LIFO) and average cost

method. These methods can be described as follows:

FIFO: This is relevant flow of inventory from initial stage till its final delivery. In this

process, product which is produced first will be first one to be delivered or sold out.

LIFO: This system is connected with the current rate of particular product. It considers

current purchase unit to be sold first which is vice versa of LIFO method.

AVCO: This is unique system of inventory management where average of all inventories

are being calculated in order to reach average cost of per unit of inventory.

Job costing System: This is unit of management accounting where costing method is

used to ascertain cost of specific job or unit in an organisation which is being performed for

ultimate satisfaction of consumers. Through this procedure, value of each individual unit is being

measured so that their respective profits and losses are identified in order to modify effectiveness

and efficiency of operations as per the requirement. It is used to record individual cost to its

particular head in order to reveal relevant profitability so that it could be compared with

budgeted estimates. This way accuracy of jobs can be maintained and necessary modification

could be made in regard to future requirements. Timely records, internal controls, detection of

frauds and errors are also its relevant outcomes which plays significant role in organisational

growth (Schaltegger, 2020). Several documents being in job order costing are manufacturing

order, cost sheet, payrolls, etc. Also it provides detailed structure of material, labour and

overheads costs for each individual job.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Though it has various advantages, it is expensive approach which mandate elaborated

clerical job which may reflect certain errors due to increased and detailed work. This system

required effective operating structure without which its formulation is of no use. Also it uses

historical approach of cost determination which may not reflect actual costs.

Price optimization System: It refers to a mathematical tool which is used to identify

customer's response in regard to differing prices for receptive goods and services by various

channels (Tirkolaee and et. al., 2020). By analysing market trends, it becomes easier for a

company to conclude best suitable price for their respective products and services that will

enhance their profitability and to meet organisational objectives in the long term. Useful data in

such system is collected through market surveys, related inventories, sales, operating costs and

so on. Such data is used to analyse behaviour of customer base in regard to various goods &

services. Price-optimization technique is helpful in the long term for increasing company's

overall profitability. It includes various data such as raw data, leveraged data, etc. It signifies

relevant variables which actually affect price of a particular product and service which could lead

to affected sales, production and profitability.

1.3 Benefits and application of management accounting systems in an organisation

Inventory management System: This process is helpful by reducing inaccuracies in its

relevant operations which will result in enhanced productivity. Through adoption of such

approach, more emphasis is given over the cost of a product in order to promote cost effective

procedures (Alam and et. al., 2019). By reduction of inaccuracies and cost, company will be able

to earn maximum profits in the long term.

Such system is being adopted by production, retail, warehouses based companies in order

to maintain their respective goods in more effective manner. This procedure helps organisations

to implement systematic approach towards management of their inventories in order to avoid any

deviations, errors and frauds which could result in intense losses.

Job costing System: This system assists in producing adequate level of profits through

allotment of respective cost to their jobs. This way performance could be modified as per the

requirement of company. It is also considered as flexible approach and accuracy if maintained

through screening each task appropriately (Chamberlin and et. al., 2018).

clerical job which may reflect certain errors due to increased and detailed work. This system

required effective operating structure without which its formulation is of no use. Also it uses

historical approach of cost determination which may not reflect actual costs.

Price optimization System: It refers to a mathematical tool which is used to identify

customer's response in regard to differing prices for receptive goods and services by various

channels (Tirkolaee and et. al., 2020). By analysing market trends, it becomes easier for a

company to conclude best suitable price for their respective products and services that will

enhance their profitability and to meet organisational objectives in the long term. Useful data in

such system is collected through market surveys, related inventories, sales, operating costs and

so on. Such data is used to analyse behaviour of customer base in regard to various goods &

services. Price-optimization technique is helpful in the long term for increasing company's

overall profitability. It includes various data such as raw data, leveraged data, etc. It signifies

relevant variables which actually affect price of a particular product and service which could lead

to affected sales, production and profitability.

1.3 Benefits and application of management accounting systems in an organisation

Inventory management System: This process is helpful by reducing inaccuracies in its

relevant operations which will result in enhanced productivity. Through adoption of such

approach, more emphasis is given over the cost of a product in order to promote cost effective

procedures (Alam and et. al., 2019). By reduction of inaccuracies and cost, company will be able

to earn maximum profits in the long term.

Such system is being adopted by production, retail, warehouses based companies in order

to maintain their respective goods in more effective manner. This procedure helps organisations

to implement systematic approach towards management of their inventories in order to avoid any

deviations, errors and frauds which could result in intense losses.

Job costing System: This system assists in producing adequate level of profits through

allotment of respective cost to their jobs. This way performance could be modified as per the

requirement of company. It is also considered as flexible approach and accuracy if maintained

through screening each task appropriately (Chamberlin and et. al., 2018).

This system is used by various organisations in order to know that respective profits and

losses being reflected by different heads so that required modifications could be made in such

respect by the company.

Price optimization System: This is a beneficial system which helps to understand

customer's behaviour in reference to various products and services in the marketplace (Pagel and

Westerfelhaus, 2019). It helps in price regulation and controlling price based decisions in regard

to each product category. In sort of approach, company's are required to conduct market survey

in order to understand customer's needs and preferences in order to deliver potential results.

This approach is adopted by each company being operating in market in order to identify

impact of prices over consumer behaviour. Companies needs to formulate such policies

effectively in order to generate maximum profits and sustainability in the market (Muller, 2019).

1.4 Analysis of how management accounting system and Management accounting are integrated

as well as significance of various methods of reporting for organisational success

Management accounting comprises of significant systems which is a base of effective

managerial decision-making (Bakhodirovna, 2019). Such techniques are used in various

operations of an organisation in order to produce effective outcomes. Management accounting

systems is an integral part of management accounting which provides detailed structure of

manner in which operations of a company is being carried away in order to produce effective

decisions. Manager of an organisation plays key role decision-making by evaluating respective

various reports in this concern. These reports can be discussed as follows:

Budget report: Budget is an intrinsic report which is used by management in order to

compare estimated projections with actual performance of a company. It is significant practice

being formulated by companies in order to measure company's overall financial and non-

financial performance (Selvakumar and et. al., 2019). Its is key element in managerial decisions

which are being guided through budgets in regard to cost- effectiveness, optimum incentives,

cope with contingencies, modification in policies related to supply and purchase and so on.

Various forms of budgets such as production budget, master budget, operating budget are used

considering company's relevant activities in this regard. This reflects summary of each

department related costing to make better evaluation of individual performance in order to

produce optimum profits.

losses being reflected by different heads so that required modifications could be made in such

respect by the company.

Price optimization System: This is a beneficial system which helps to understand

customer's behaviour in reference to various products and services in the marketplace (Pagel and

Westerfelhaus, 2019). It helps in price regulation and controlling price based decisions in regard

to each product category. In sort of approach, company's are required to conduct market survey

in order to understand customer's needs and preferences in order to deliver potential results.

This approach is adopted by each company being operating in market in order to identify

impact of prices over consumer behaviour. Companies needs to formulate such policies

effectively in order to generate maximum profits and sustainability in the market (Muller, 2019).

1.4 Analysis of how management accounting system and Management accounting are integrated

as well as significance of various methods of reporting for organisational success

Management accounting comprises of significant systems which is a base of effective

managerial decision-making (Bakhodirovna, 2019). Such techniques are used in various

operations of an organisation in order to produce effective outcomes. Management accounting

systems is an integral part of management accounting which provides detailed structure of

manner in which operations of a company is being carried away in order to produce effective

decisions. Manager of an organisation plays key role decision-making by evaluating respective

various reports in this concern. These reports can be discussed as follows:

Budget report: Budget is an intrinsic report which is used by management in order to

compare estimated projections with actual performance of a company. It is significant practice

being formulated by companies in order to measure company's overall financial and non-

financial performance (Selvakumar and et. al., 2019). Its is key element in managerial decisions

which are being guided through budgets in regard to cost- effectiveness, optimum incentives,

cope with contingencies, modification in policies related to supply and purchase and so on.

Various forms of budgets such as production budget, master budget, operating budget are used

considering company's relevant activities in this regard. This reflects summary of each

department related costing to make better evaluation of individual performance in order to

produce optimum profits.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Performance report: Performance is an ultimate factor at which company looks up to.

Performance evaluation must be given adequate preference in order to promote overall

sustainability of a company. The performance of a company is been evaluated to conclude a

report in this regard. This report is used by managers of a company to provide required decisions

in overall growth or modification in performance segment. Employees are usually encouraged or

compensated for their respective contribution in company's overall success. It suggests

formulation of accuracy measure in an organisation in order to maintain standard of performance

in an organisation over long period (Brown and et. al., 2017).

Section 2

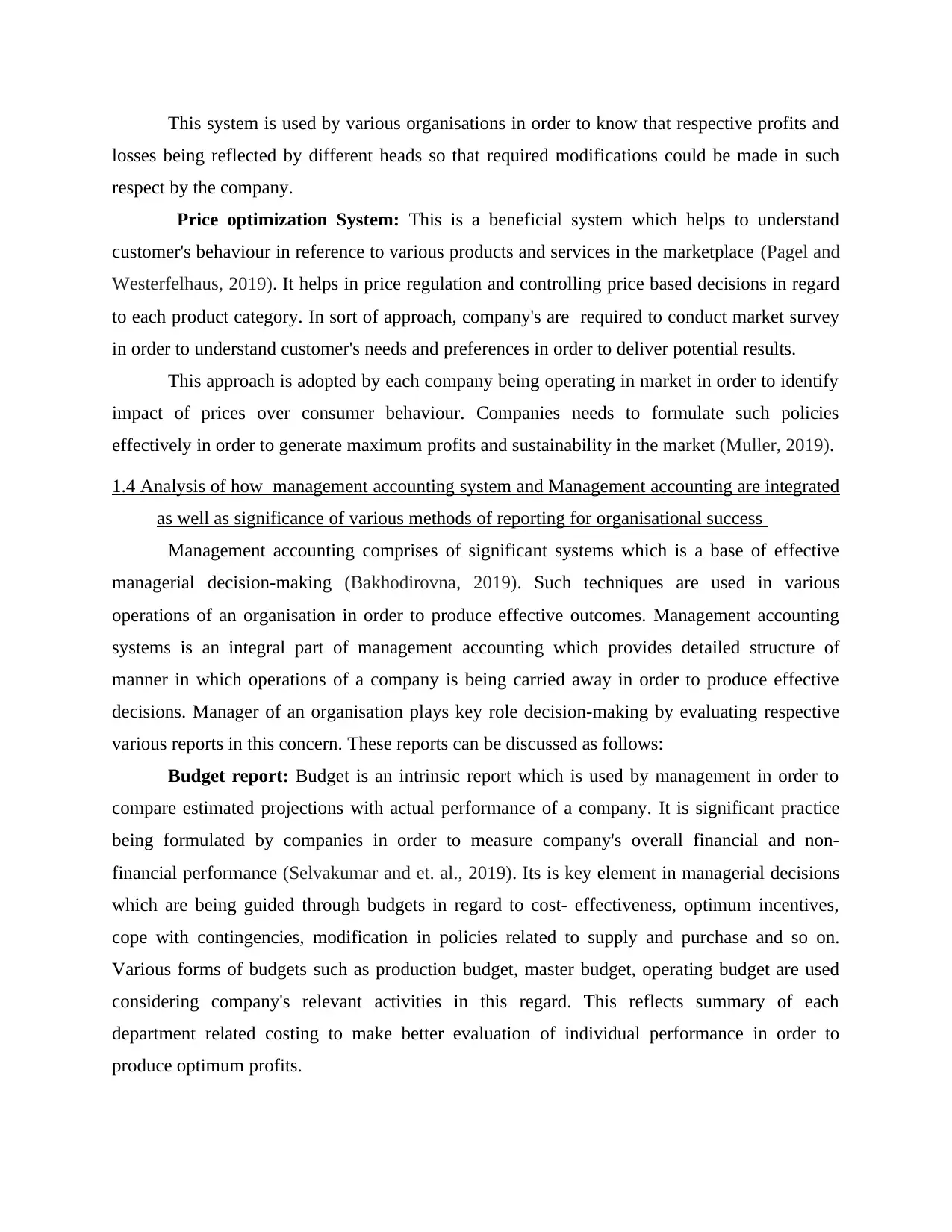

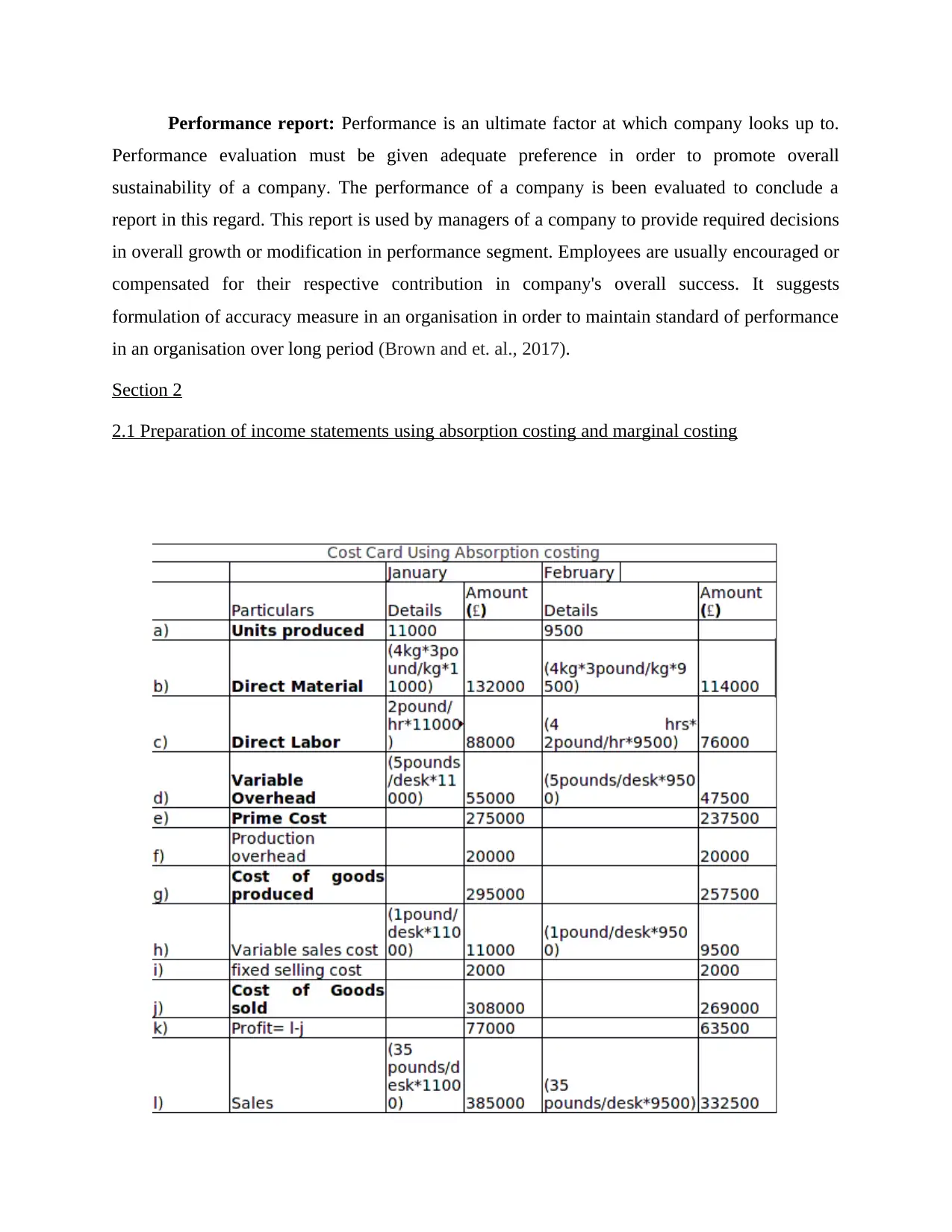

2.1 Preparation of income statements using absorption costing and marginal costing

Performance evaluation must be given adequate preference in order to promote overall

sustainability of a company. The performance of a company is been evaluated to conclude a

report in this regard. This report is used by managers of a company to provide required decisions

in overall growth or modification in performance segment. Employees are usually encouraged or

compensated for their respective contribution in company's overall success. It suggests

formulation of accuracy measure in an organisation in order to maintain standard of performance

in an organisation over long period (Brown and et. al., 2017).

Section 2

2.1 Preparation of income statements using absorption costing and marginal costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Note: Here, Productions overhead is considered as average productions per month: 10000

units. Therefore, for the month of Jan. overheads = (20000/10000)* 11000 whereas for month of

Feb. overhead= (20000/ 10000) * 9500

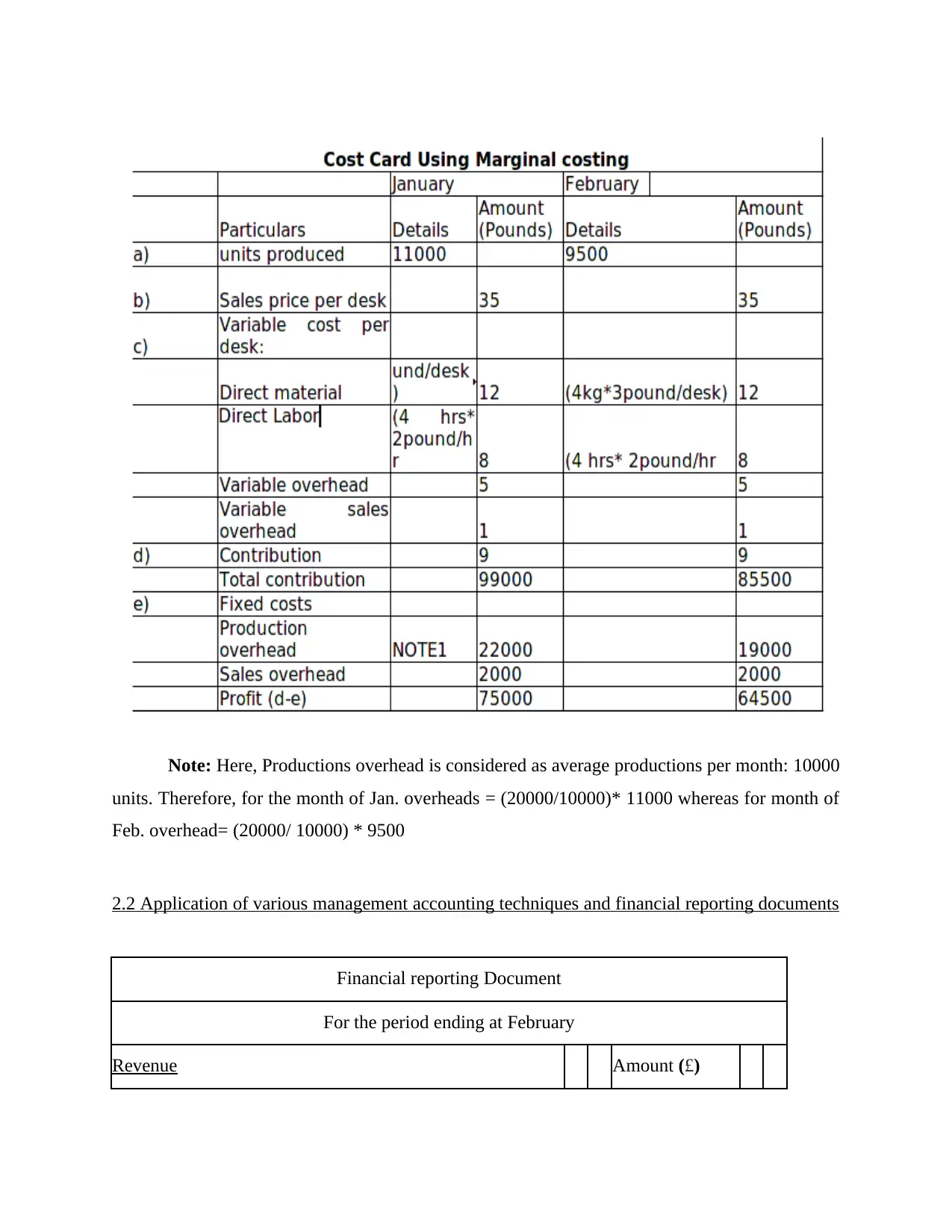

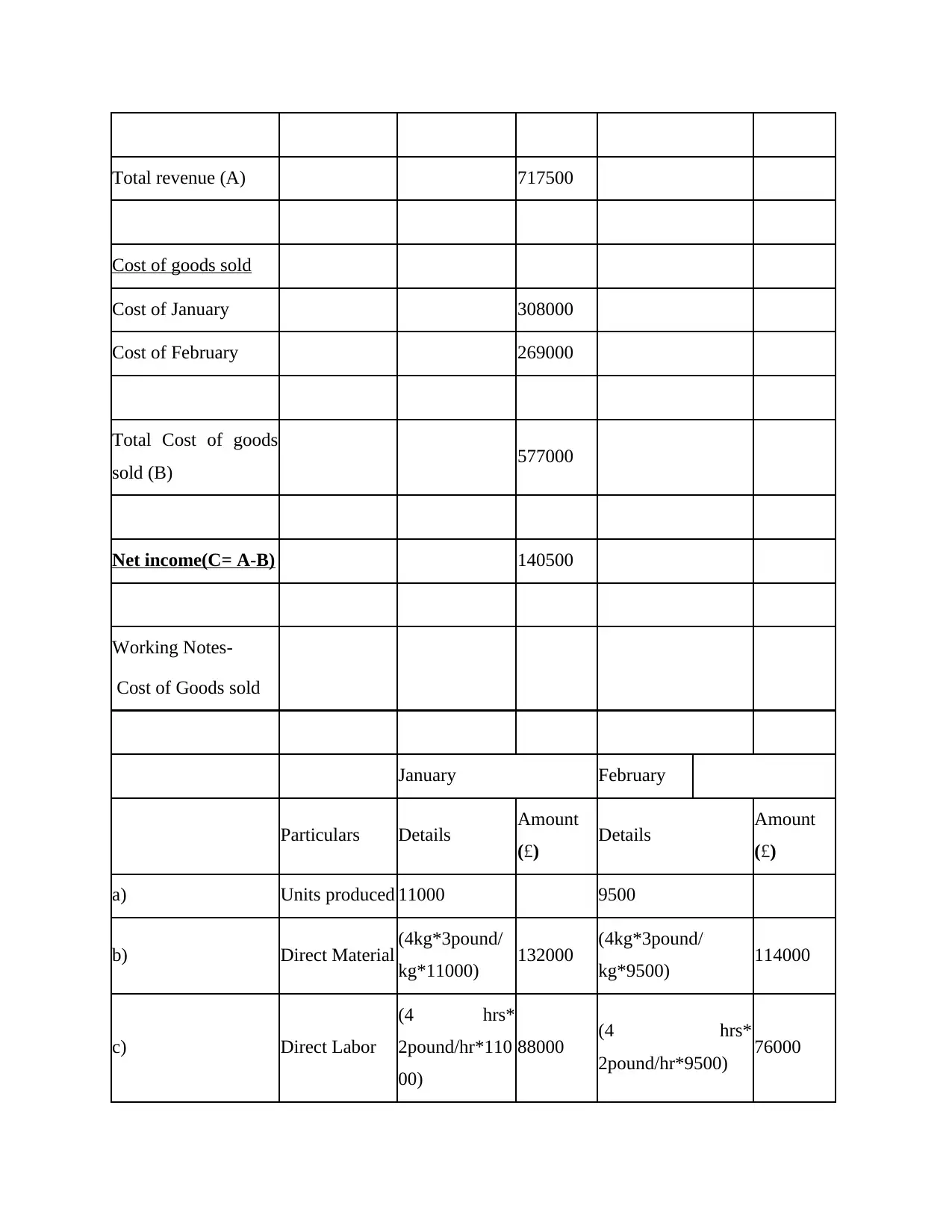

2.2 Application of various management accounting techniques and financial reporting documents

Financial reporting Document

For the period ending at February

Revenue Amount (£)

units. Therefore, for the month of Jan. overheads = (20000/10000)* 11000 whereas for month of

Feb. overhead= (20000/ 10000) * 9500

2.2 Application of various management accounting techniques and financial reporting documents

Financial reporting Document

For the period ending at February

Revenue Amount (£)

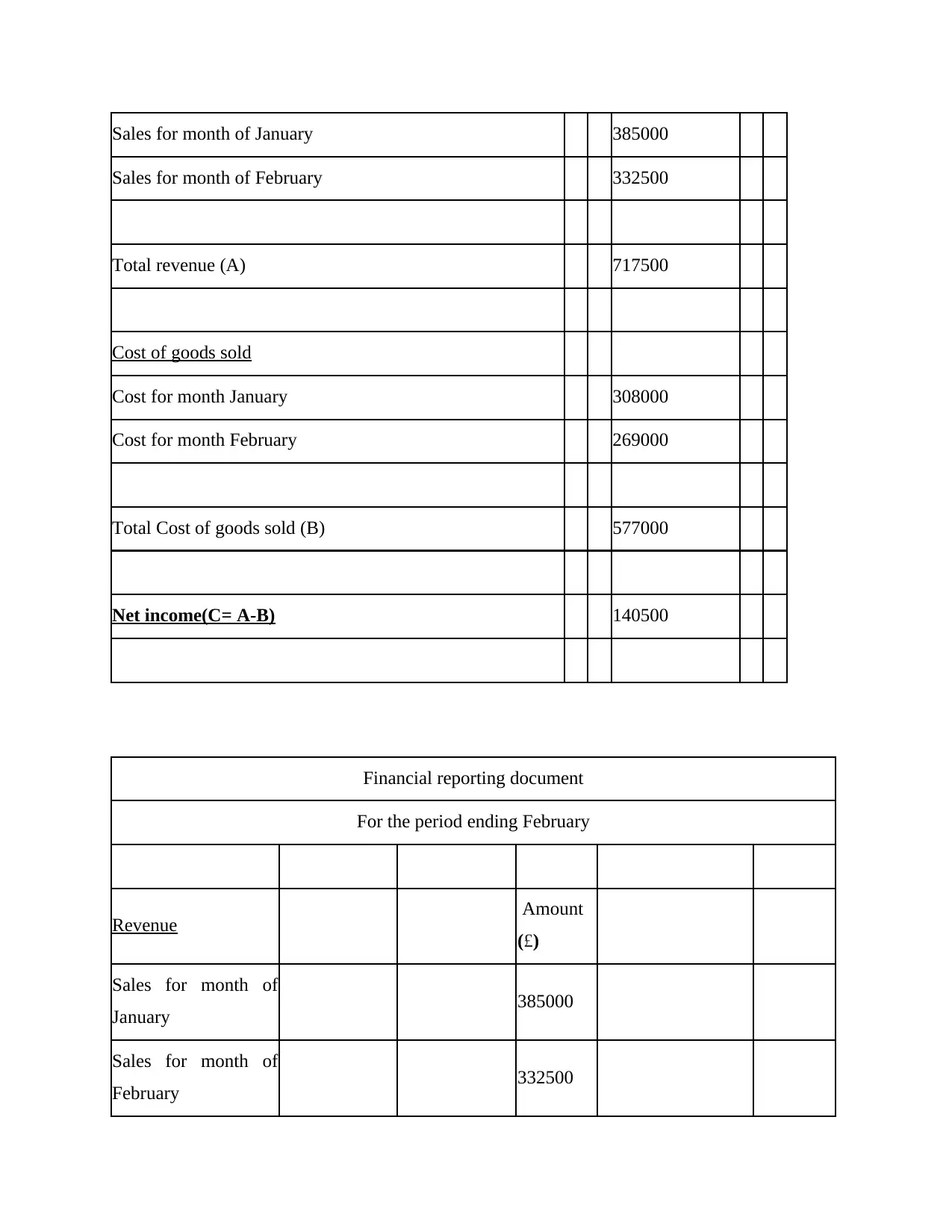

Sales for month of January 385000

Sales for month of February 332500

Total revenue (A) 717500

Cost of goods sold

Cost for month January 308000

Cost for month February 269000

Total Cost of goods sold (B) 577000

Net income(C= A-B) 140500

Financial reporting document

For the period ending February

Revenue Amount

(£)

Sales for month of

January 385000

Sales for month of

February 332500

Sales for month of February 332500

Total revenue (A) 717500

Cost of goods sold

Cost for month January 308000

Cost for month February 269000

Total Cost of goods sold (B) 577000

Net income(C= A-B) 140500

Financial reporting document

For the period ending February

Revenue Amount

(£)

Sales for month of

January 385000

Sales for month of

February 332500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total revenue (A) 717500

Cost of goods sold

Cost of January 308000

Cost of February 269000

Total Cost of goods

sold (B) 577000

Net income(C= A-B) 140500

Working Notes-

Cost of Goods sold

January February

Particulars Details Amount

(£) Details Amount

(£)

a) Units produced 11000 9500

b) Direct Material (4kg*3pound/

kg*11000) 132000 (4kg*3pound/

kg*9500) 114000

c) Direct Labor

(4 hrs*

2pound/hr*110

00)

88000 (4 hrs*

2pound/hr*9500) 76000

Cost of goods sold

Cost of January 308000

Cost of February 269000

Total Cost of goods

sold (B) 577000

Net income(C= A-B) 140500

Working Notes-

Cost of Goods sold

January February

Particulars Details Amount

(£) Details Amount

(£)

a) Units produced 11000 9500

b) Direct Material (4kg*3pound/

kg*11000) 132000 (4kg*3pound/

kg*9500) 114000

c) Direct Labor

(4 hrs*

2pound/hr*110

00)

88000 (4 hrs*

2pound/hr*9500) 76000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

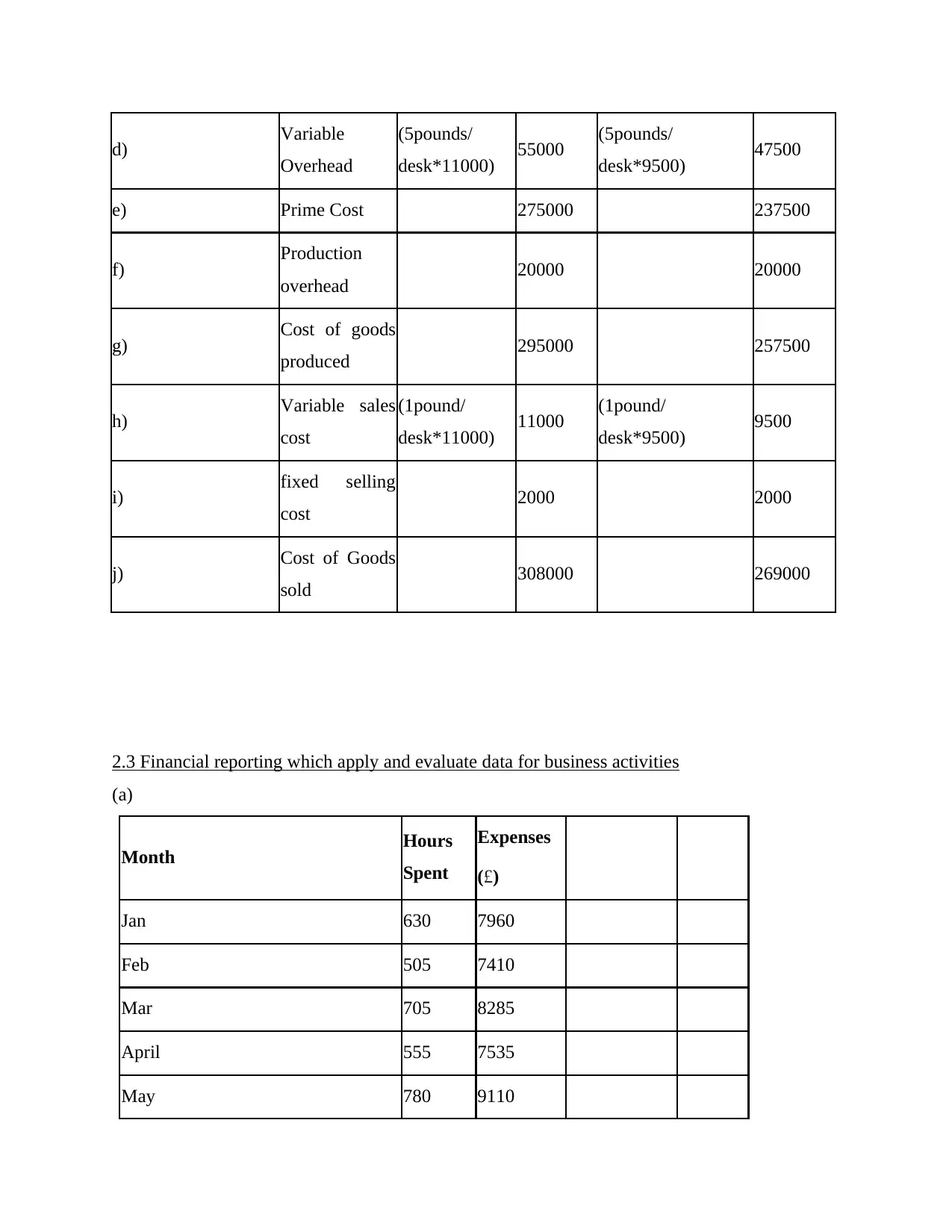

d) Variable

Overhead

(5pounds/

desk*11000) 55000 (5pounds/

desk*9500) 47500

e) Prime Cost 275000 237500

f) Production

overhead 20000 20000

g) Cost of goods

produced 295000 257500

h) Variable sales

cost

(1pound/

desk*11000) 11000 (1pound/

desk*9500) 9500

i) fixed selling

cost 2000 2000

j) Cost of Goods

sold 308000 269000

2.3 Financial reporting which apply and evaluate data for business activities

(a)

Month Hours

Spent

Expenses

(£)

Jan 630 7960

Feb 505 7410

Mar 705 8285

April 555 7535

May 780 9110

Overhead

(5pounds/

desk*11000) 55000 (5pounds/

desk*9500) 47500

e) Prime Cost 275000 237500

f) Production

overhead 20000 20000

g) Cost of goods

produced 295000 257500

h) Variable sales

cost

(1pound/

desk*11000) 11000 (1pound/

desk*9500) 9500

i) fixed selling

cost 2000 2000

j) Cost of Goods

sold 308000 269000

2.3 Financial reporting which apply and evaluate data for business activities

(a)

Month Hours

Spent

Expenses

(£)

Jan 630 7960

Feb 505 7410

Mar 705 8285

April 555 7535

May 780 9110

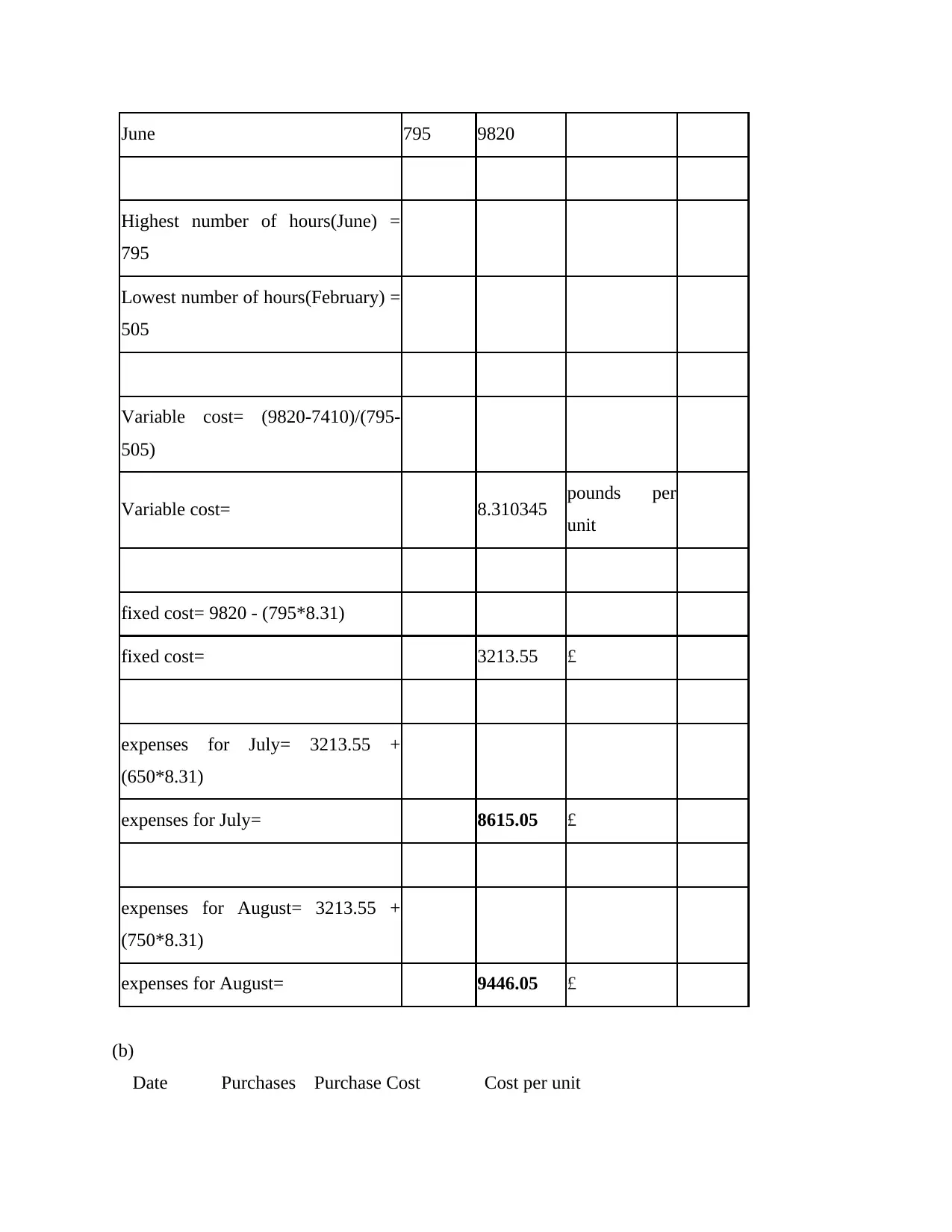

June 795 9820

Highest number of hours(June) =

795

Lowest number of hours(February) =

505

Variable cost= (9820-7410)/(795-

505)

Variable cost= 8.310345 pounds per

unit

fixed cost= 9820 - (795*8.31)

fixed cost= 3213.55 £

expenses for July= 3213.55 +

(650*8.31)

expenses for July= 8615.05 £

expenses for August= 3213.55 +

(750*8.31)

expenses for August= 9446.05 £

(b)

Date Purchases Purchase Cost Cost per unit

Highest number of hours(June) =

795

Lowest number of hours(February) =

505

Variable cost= (9820-7410)/(795-

505)

Variable cost= 8.310345 pounds per

unit

fixed cost= 9820 - (795*8.31)

fixed cost= 3213.55 £

expenses for July= 3213.55 +

(650*8.31)

expenses for July= 8615.05 £

expenses for August= 3213.55 +

(750*8.31)

expenses for August= 9446.05 £

(b)

Date Purchases Purchase Cost Cost per unit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.