Applied Management Accounting: Evolution, Functions, and Applications

VerifiedAdded on 2023/06/16

|14

|3873

|477

Essay

AI Summary

This essay provides a comprehensive overview of applied management accounting, tracing its evolution from basic cost tracking to a strategic function involving planning, controlling, and performance measurement. It discusses the key functions of management accounting, including planning and forecasting, organizing, coordination, and financial management. The evolution of management accounting is examined through four stages, highlighting the shift from a technical discipline focused on cost reduction to a value-generating function driven by technology and strategic focus. Key aspects such as performance measurement, balanced scorecards, and activity-based costing are explored, with practical examples illustrating their application in both service and production sectors. The essay emphasizes the role of management accounting in controlling business performance through techniques like marginal and absorption costing, ultimately supporting informed decision-making and enhanced organizational efficiency.

Applied Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting aims to prepare various financial and non – financial reports

concerning a business and its operations in an attempt to facilitate the task of management that

is, taking managerial decisions for both long term and short term perspectives. It is the process

aims to pursue business goals through identification, measurement, analysis, interpretation and

communication of financial and non – financial information to the managers, so that they can

make decisions accordingly (Taipaleenmäki, 2017). The two words that is, management

accounting itself is sufficient in making clear the meaning of what MA is, that is, accounting

meant for the management in order to enhance their efficiency by providing them with all the

required information that is necessary for carrying out their managerial tasks such as planning,

controlling and formulating policy for the business concerned. In the present essay, the

discussion will be done with regards to the evolution of MA, its functions within the organisation

and various aspects of MA such as performance measurement, activity based costing, balanced

scorecard, etc. Also, a practical example will be quoted with reference to both service and

production sector to reflect how MA can be applied within the context of business to establish

control and enhance efficiency.

MAIN BODY

Management accounting too has its development stages like other disciplines of economics.

The stages represent the economic conditions, societal conditions of the time and their reactions

to such situations. In this essay, the discussion pertaining to the evolution and development of

management accounting over the time and its interaction with other functions within the

organisations.

Management accounting can be defined as the process that identifies, measures, interprets

and communicates information that the management team can use to plan, evaluate and control

their actions in an organization (Amara and Benelifa, 2017).

In other words, the job of people in the management accounting department of an

organisation is to provide the management team with the most accurate and useful information

which would help them in decision making and evaluation. Some of the strategic functions of

management accounting are as:

Management accounting aims to prepare various financial and non – financial reports

concerning a business and its operations in an attempt to facilitate the task of management that

is, taking managerial decisions for both long term and short term perspectives. It is the process

aims to pursue business goals through identification, measurement, analysis, interpretation and

communication of financial and non – financial information to the managers, so that they can

make decisions accordingly (Taipaleenmäki, 2017). The two words that is, management

accounting itself is sufficient in making clear the meaning of what MA is, that is, accounting

meant for the management in order to enhance their efficiency by providing them with all the

required information that is necessary for carrying out their managerial tasks such as planning,

controlling and formulating policy for the business concerned. In the present essay, the

discussion will be done with regards to the evolution of MA, its functions within the organisation

and various aspects of MA such as performance measurement, activity based costing, balanced

scorecard, etc. Also, a practical example will be quoted with reference to both service and

production sector to reflect how MA can be applied within the context of business to establish

control and enhance efficiency.

MAIN BODY

Management accounting too has its development stages like other disciplines of economics.

The stages represent the economic conditions, societal conditions of the time and their reactions

to such situations. In this essay, the discussion pertaining to the evolution and development of

management accounting over the time and its interaction with other functions within the

organisations.

Management accounting can be defined as the process that identifies, measures, interprets

and communicates information that the management team can use to plan, evaluate and control

their actions in an organization (Amara and Benelifa, 2017).

In other words, the job of people in the management accounting department of an

organisation is to provide the management team with the most accurate and useful information

which would help them in decision making and evaluation. Some of the strategic functions of

management accounting are as:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Planning and forecasting: to provide data and information for short term as well as

long term planning and forecast about the operations of the business, using tools such as trend

analysis through correlation and regression, capital budgeting, marginal and standard costing etc.

Organising: The management accountant helps in organising financial as well as non-

financial functions on the modern lines by assigning specific responsibilities. For e.g. specific

divisions for accounting and finance (Wren and Bedeian, 2020).

Coordination: Various tools such as reconciliation of cost and financial accounts,

budgets and standard costing are used to facilitate coordination among various departments.

Controlling: Tools such as ratio analysis, cash and fund flow analysis and or the

comparison of the actual with the standard or desired help in controlling the performance of the

organisation.

Financial Management: The management accountant presents the financial analysis and

interpretations along with his comments and suggestions so that the leadership is helped in taking

decisions easily.

Last but most importantly, management accounting is also concerned with evaluation of

decisions and performances and improving internal as well as external communication.

An example of management accounting is the decision by Marks and Spencer plc to adopt new

currency Euro. It called for planning future course of action and strategies (Lyly-Yrjänäinen,

and et.al., 2017). To deal with the use of Euro as the currency for financial reporting, the

company took some time until the government’s decision on the Euro embark.

Paul Smith, Euro project manager for the company stated that significant training of the staff and

expenditure of about 2 million pounds went into the preparation for adopting new currency.

Evolution of Management Accounting

Management accounting is very liquid and subjective in nature. The academicians and

practitioners of the discipline too never expected such development like what is practised in

today’s real world. Many a time, educational institutions receive enormous amount of pressure

that they update their curriculum so that it matches with the existing practice of the discipline

(Loft, 2020). For a general example to show the growth of management accounting, basic

differences between traditional and modern management accounting can be described. Whereas

the field was dominated by principle techniques of analysis of variances traditionally, it has

developed to include concepts like activity based costing, life cycle costs etc.

long term planning and forecast about the operations of the business, using tools such as trend

analysis through correlation and regression, capital budgeting, marginal and standard costing etc.

Organising: The management accountant helps in organising financial as well as non-

financial functions on the modern lines by assigning specific responsibilities. For e.g. specific

divisions for accounting and finance (Wren and Bedeian, 2020).

Coordination: Various tools such as reconciliation of cost and financial accounts,

budgets and standard costing are used to facilitate coordination among various departments.

Controlling: Tools such as ratio analysis, cash and fund flow analysis and or the

comparison of the actual with the standard or desired help in controlling the performance of the

organisation.

Financial Management: The management accountant presents the financial analysis and

interpretations along with his comments and suggestions so that the leadership is helped in taking

decisions easily.

Last but most importantly, management accounting is also concerned with evaluation of

decisions and performances and improving internal as well as external communication.

An example of management accounting is the decision by Marks and Spencer plc to adopt new

currency Euro. It called for planning future course of action and strategies (Lyly-Yrjänäinen,

and et.al., 2017). To deal with the use of Euro as the currency for financial reporting, the

company took some time until the government’s decision on the Euro embark.

Paul Smith, Euro project manager for the company stated that significant training of the staff and

expenditure of about 2 million pounds went into the preparation for adopting new currency.

Evolution of Management Accounting

Management accounting is very liquid and subjective in nature. The academicians and

practitioners of the discipline too never expected such development like what is practised in

today’s real world. Many a time, educational institutions receive enormous amount of pressure

that they update their curriculum so that it matches with the existing practice of the discipline

(Loft, 2020). For a general example to show the growth of management accounting, basic

differences between traditional and modern management accounting can be described. Whereas

the field was dominated by principle techniques of analysis of variances traditionally, it has

developed to include concepts like activity based costing, life cycle costs etc.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Stage I – Before 1950

In this stage, the discipline was considered in its original form, where the only

components of management accounting were the technical activities in requirement to keep track

of business. So the discipline was simply concerned with activities that determined product costs.

Due to relatively simple production technology at the time, this was quite easy (Kehoe, P. J.,

Midrigan and Pastorino, 2018). After the material and labour costs were defined, overheads

could be determined simply based on direct labour hrs.

At this stage, there were few regulatory challenges and less competition. The focus was

more on cost effectiveness and productivity than innovation. The use of cost accounting and

budgetary control was popular, still the information distribution for the purpose of managerial

decision making was poor. Managers were still allowed decision making on the basis of

intuition, experiences etc.

Stage II – 1950-1965

In the second stage of the evolution of the discipline, the concept developed to include

more than just the technical activities of costing. By this time, planning and controlling activities

have been included (Oldman and Tomkins, 2018). Experts believe that the discipline shifted to

more of the managerial work than the technical work by this time but, remaining at the staff

level. In other words, controls were restricted to manufacturing and operations rather than

strategic decision making. Therefore, management accounting was more or less reactive; actions

are only taken when problems are discovered through analysis of deviations.

Stage III – 1965-1985

This stage is noteworthy representing a significant change in the practice of the

discipline. Corporate leadership and the management team have joined hands in their common

interest to reduce waste in processes by efficient and effective decision making. This has

increased the need for better management accounting practices significantly.

The department of management accounting can no longer afford to be passive and

reactive in its job. Aggressive plans of cost cutting and efficiency have driven the management

accountant to be much more skilled and creative in providing information to support decision

making by the managers.

In this stage, the discipline was considered in its original form, where the only

components of management accounting were the technical activities in requirement to keep track

of business. So the discipline was simply concerned with activities that determined product costs.

Due to relatively simple production technology at the time, this was quite easy (Kehoe, P. J.,

Midrigan and Pastorino, 2018). After the material and labour costs were defined, overheads

could be determined simply based on direct labour hrs.

At this stage, there were few regulatory challenges and less competition. The focus was

more on cost effectiveness and productivity than innovation. The use of cost accounting and

budgetary control was popular, still the information distribution for the purpose of managerial

decision making was poor. Managers were still allowed decision making on the basis of

intuition, experiences etc.

Stage II – 1950-1965

In the second stage of the evolution of the discipline, the concept developed to include

more than just the technical activities of costing. By this time, planning and controlling activities

have been included (Oldman and Tomkins, 2018). Experts believe that the discipline shifted to

more of the managerial work than the technical work by this time but, remaining at the staff

level. In other words, controls were restricted to manufacturing and operations rather than

strategic decision making. Therefore, management accounting was more or less reactive; actions

are only taken when problems are discovered through analysis of deviations.

Stage III – 1965-1985

This stage is noteworthy representing a significant change in the practice of the

discipline. Corporate leadership and the management team have joined hands in their common

interest to reduce waste in processes by efficient and effective decision making. This has

increased the need for better management accounting practices significantly.

The department of management accounting can no longer afford to be passive and

reactive in its job. Aggressive plans of cost cutting and efficiency have driven the management

accountant to be much more skilled and creative in providing information to support decision

making by the managers.

Researchers believe the cause behind such a change to be the oil crisis in the 1970s. The

world went into a recession and even threatened stable economies. Competition gave rise to

better strategies for financial management (Jansen, 2018). However, others believe the cause

behind the change to be the rapid advances in the production technologies that enhanced

competitiveness in production and operations, leading to improved management accounting

practices and informed managerial decisions.

Stage IV – 1985-1995

In this stage, the development of the discipline got a boost mainly by the advent of new

information and communication technologies such as World Wide Web. Now the game is no

longer about reducing waste and cost cutting, but rather generating value through better and

better use of available resources. Since then, professionals in the management accounting

department have been struggling to enhance value generation by the information provided to

leadership having already clearer strategic focus.

Aspects of management accounting revolves around the company’s financial results such as

sales, cost control and operating expenses of the company (Nielsen, 2018). There are various

aspects of MA which indicates the scope and characteristics of management accounting. Here

three of such aspects will be discussed that is, performance measurement, balanced scorecard

and activity based costing.

Performance measurement refers to the monitoring of targets or budgets against the results

actually achieved to determine the functioning of company’s employees in terms of their ability

as a whole or individually, in other words how well a company’s employees are performing

individually or as a whole. Performance measurement is useful for both short term and long term

objectives that is, by controlling cost and satisfying customers (Bititci and et.al., 20180. It

facilitates numeric outcome of an analysis in order to indicate how well a business is achieving

its objectives both in short and long run. Some of the examples of what management accounting

measures in terms of performance of the company are efficiency in controlling cost, ability to

attain sales targets, effectiveness that is, the speed with which the sales targets are being met by

the business.

There are various tools and techniques that is being used vastly in modern business

scenario such as balanced scorecard which is considered to be best known technique of

performance measurement based on four different perspectives that is, customer, learning &

world went into a recession and even threatened stable economies. Competition gave rise to

better strategies for financial management (Jansen, 2018). However, others believe the cause

behind the change to be the rapid advances in the production technologies that enhanced

competitiveness in production and operations, leading to improved management accounting

practices and informed managerial decisions.

Stage IV – 1985-1995

In this stage, the development of the discipline got a boost mainly by the advent of new

information and communication technologies such as World Wide Web. Now the game is no

longer about reducing waste and cost cutting, but rather generating value through better and

better use of available resources. Since then, professionals in the management accounting

department have been struggling to enhance value generation by the information provided to

leadership having already clearer strategic focus.

Aspects of management accounting revolves around the company’s financial results such as

sales, cost control and operating expenses of the company (Nielsen, 2018). There are various

aspects of MA which indicates the scope and characteristics of management accounting. Here

three of such aspects will be discussed that is, performance measurement, balanced scorecard

and activity based costing.

Performance measurement refers to the monitoring of targets or budgets against the results

actually achieved to determine the functioning of company’s employees in terms of their ability

as a whole or individually, in other words how well a company’s employees are performing

individually or as a whole. Performance measurement is useful for both short term and long term

objectives that is, by controlling cost and satisfying customers (Bititci and et.al., 20180. It

facilitates numeric outcome of an analysis in order to indicate how well a business is achieving

its objectives both in short and long run. Some of the examples of what management accounting

measures in terms of performance of the company are efficiency in controlling cost, ability to

attain sales targets, effectiveness that is, the speed with which the sales targets are being met by

the business.

There are various tools and techniques that is being used vastly in modern business

scenario such as balanced scorecard which is considered to be best known technique of

performance measurement based on four different perspectives that is, customer, learning &

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

growth, financial and internal process. These four perspectives are designed in such a way

covering all the activities of the organization whether it is external or internal and future or

current. Therefore, performance management is also known as a tool meant for strategic analysis.

Also, this aspect of MA is useful for organization disregarding the industry in which it operates

and the size or type it has (Rikhardsson and Yigitbasioglu, 2018). With the help of various tools

and techniques of management accounting such as budgets, costing reports, etc. are very useful

in providing information to carry out the performance measurement activities and also suggests

various systems for efficiently and effectively carrying out of related tasks. The other

performance measurement techniques are financial, non – financial and benchmarking. In

financial performance measurement, various ratios are calculated to determine the performance

trends of business for various years and can also be compared with that the competitor's average.

Accordingly, areas which needs improvement are determined and managerial actions are taken

for correcting figures in future periods. Non-financial techniques takes into consideration the

measurement of customer satisfaction, resource utilization and quality measurement. At last,

benchmarking is being useful in setting standards in advance which the business aims to achieve

within the given period of time and in this way the organization become efficient and effective in

getting up to the best practices across the industry.

Another aspect of MA is balanced scorecard, a performance metric used by management

to help in the identification and improvement in the company's internal operations that are seems

to be useful in increasing external outcomes (Loft, 20200. Here, past data indicating the

performance are measured to provide feedback to the managers on how they are need to make

better decisions in future. For example, increase in revenue per customer is a mission forming

part of financial perspective of balanced scorecard.

The last one is the activity based costing which is based on principles that are meant for

controlling the resource consuming activities of the organization to ensure that the costs are

controlled at the source itself. Time driven ABC in the recent time helps in overcoming various

issues pertaining to traditional system of cost management. With the use of activity based

costing, all the indirect and overhead costs are assigned to the organizational products and

services. The cost are assigned to products on the basis of activities performed for producing it.

For example if the total electricity bill for production house comes to 35000 as against the usage

of electricity for 700 hours, then the overhead rate of this cost comes to 35000 / 700 = 50 per

covering all the activities of the organization whether it is external or internal and future or

current. Therefore, performance management is also known as a tool meant for strategic analysis.

Also, this aspect of MA is useful for organization disregarding the industry in which it operates

and the size or type it has (Rikhardsson and Yigitbasioglu, 2018). With the help of various tools

and techniques of management accounting such as budgets, costing reports, etc. are very useful

in providing information to carry out the performance measurement activities and also suggests

various systems for efficiently and effectively carrying out of related tasks. The other

performance measurement techniques are financial, non – financial and benchmarking. In

financial performance measurement, various ratios are calculated to determine the performance

trends of business for various years and can also be compared with that the competitor's average.

Accordingly, areas which needs improvement are determined and managerial actions are taken

for correcting figures in future periods. Non-financial techniques takes into consideration the

measurement of customer satisfaction, resource utilization and quality measurement. At last,

benchmarking is being useful in setting standards in advance which the business aims to achieve

within the given period of time and in this way the organization become efficient and effective in

getting up to the best practices across the industry.

Another aspect of MA is balanced scorecard, a performance metric used by management

to help in the identification and improvement in the company's internal operations that are seems

to be useful in increasing external outcomes (Loft, 20200. Here, past data indicating the

performance are measured to provide feedback to the managers on how they are need to make

better decisions in future. For example, increase in revenue per customer is a mission forming

part of financial perspective of balanced scorecard.

The last one is the activity based costing which is based on principles that are meant for

controlling the resource consuming activities of the organization to ensure that the costs are

controlled at the source itself. Time driven ABC in the recent time helps in overcoming various

issues pertaining to traditional system of cost management. With the use of activity based

costing, all the indirect and overhead costs are assigned to the organizational products and

services. The cost are assigned to products on the basis of activities performed for producing it.

For example if the total electricity bill for production house comes to 35000 as against the usage

of electricity for 700 hours, then the overhead rate of this cost comes to 35000 / 700 = 50 per

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

hour. If a product say, XYZ consumes 30 hours for its production, then the cost allocated to this

activity would be 30 * 50 = 1500.

Controlling

The other and most important function of the management accounting is controlling the

performance of the business by using the various aspects and tools. The purpose behind the

company for controlling the business expenses and performance is achieving the targets and

goals of the enterprises (Hayes, 2019). Two most important and main aspects of the management

accounting which help the businesses in controlling is Marginal Costing and Absorption Costing.

Marginal Costing is one of the technique and aspects of management accounting which

state that profits earned by the company where fixed cost taken into account by the company. In

simple term, in marginal costing aspects the company need to exclude the fixed cost of

manufacturing and admin expenses from the product cost so that the management of the

company can manage marginal cost effectively. With the help of marginal costing the degree of

the treatment of over and under overheads get reduces. Not only that, the management of the

company with the use of these aspects can start the new line of the production because they help

in making the decision regarding the buy and manufacture of products along with decision

regarding pricing and tendering. However, the marginal costing does not provide the real profit

as it does not consider the semi-variable and semi-fixed cost in their decision-making (Johnsson,

Normann and Svensson, 2020). Along with that, the most important issue attach with this aspect

is that it basically ignores the time element while classifying the total cost into the variable and

fixed category. Another issue found out under the marginal costing aspect is that the assumption

regrading the constant selling price of the product is unrealistic.

Absorption costing is also another and most significant aspect and technique of

management accounting which helps in controlling and decision-making function. In this aspect,

the company get the real profit of the products as it seize the fixed cost of the product in the

closing stock itself. The benefit of absorption costing is that it comply with the GAAPs

principles such as accrual and matching concept. With the application of the absorption costing

technique, the company match the cost with the revenue of the same period. It is one of the best

aspects of management accounting for the purpose of preparing external reports. In this costing

method, the company need not separate the total cost of manufacturing of product in the fixed

and variable cost as it cover whole cost of manufacturing in direct cost. It is because these

activity would be 30 * 50 = 1500.

Controlling

The other and most important function of the management accounting is controlling the

performance of the business by using the various aspects and tools. The purpose behind the

company for controlling the business expenses and performance is achieving the targets and

goals of the enterprises (Hayes, 2019). Two most important and main aspects of the management

accounting which help the businesses in controlling is Marginal Costing and Absorption Costing.

Marginal Costing is one of the technique and aspects of management accounting which

state that profits earned by the company where fixed cost taken into account by the company. In

simple term, in marginal costing aspects the company need to exclude the fixed cost of

manufacturing and admin expenses from the product cost so that the management of the

company can manage marginal cost effectively. With the help of marginal costing the degree of

the treatment of over and under overheads get reduces. Not only that, the management of the

company with the use of these aspects can start the new line of the production because they help

in making the decision regarding the buy and manufacture of products along with decision

regarding pricing and tendering. However, the marginal costing does not provide the real profit

as it does not consider the semi-variable and semi-fixed cost in their decision-making (Johnsson,

Normann and Svensson, 2020). Along with that, the most important issue attach with this aspect

is that it basically ignores the time element while classifying the total cost into the variable and

fixed category. Another issue found out under the marginal costing aspect is that the assumption

regrading the constant selling price of the product is unrealistic.

Absorption costing is also another and most significant aspect and technique of

management accounting which helps in controlling and decision-making function. In this aspect,

the company get the real profit of the products as it seize the fixed cost of the product in the

closing stock itself. The benefit of absorption costing is that it comply with the GAAPs

principles such as accrual and matching concept. With the application of the absorption costing

technique, the company match the cost with the revenue of the same period. It is one of the best

aspects of management accounting for the purpose of preparing external reports. In this costing

method, the company need not separate the total cost of manufacturing of product in the fixed

and variable cost as it cover whole cost of manufacturing in direct cost. It is because these

aspects is highly recognized the importance of including the fixed production cost (Xu and et.al.,

2017). This techniques are the best for determining the suitable pricing policy for their products

of the company.

However, on the other hand, absorption costing is also had various disadvantage. Many

authors have argued that the fixed cost are period cost not the product cost and thus it should be

eliminated from the product revenue. One of the biggest issue arises in this management

accounting aspects is that it skewed profit and loss. It means that it reduces the level of the profit

of the company which further causes the issue of poor decision-making of the company (Hojna

and Stryckova, 2018). Any wrong decision may result into the heavy loss to the company thus it

is advisable to the company that before adopting any technique and aspects the company have to

do though analysis of it.

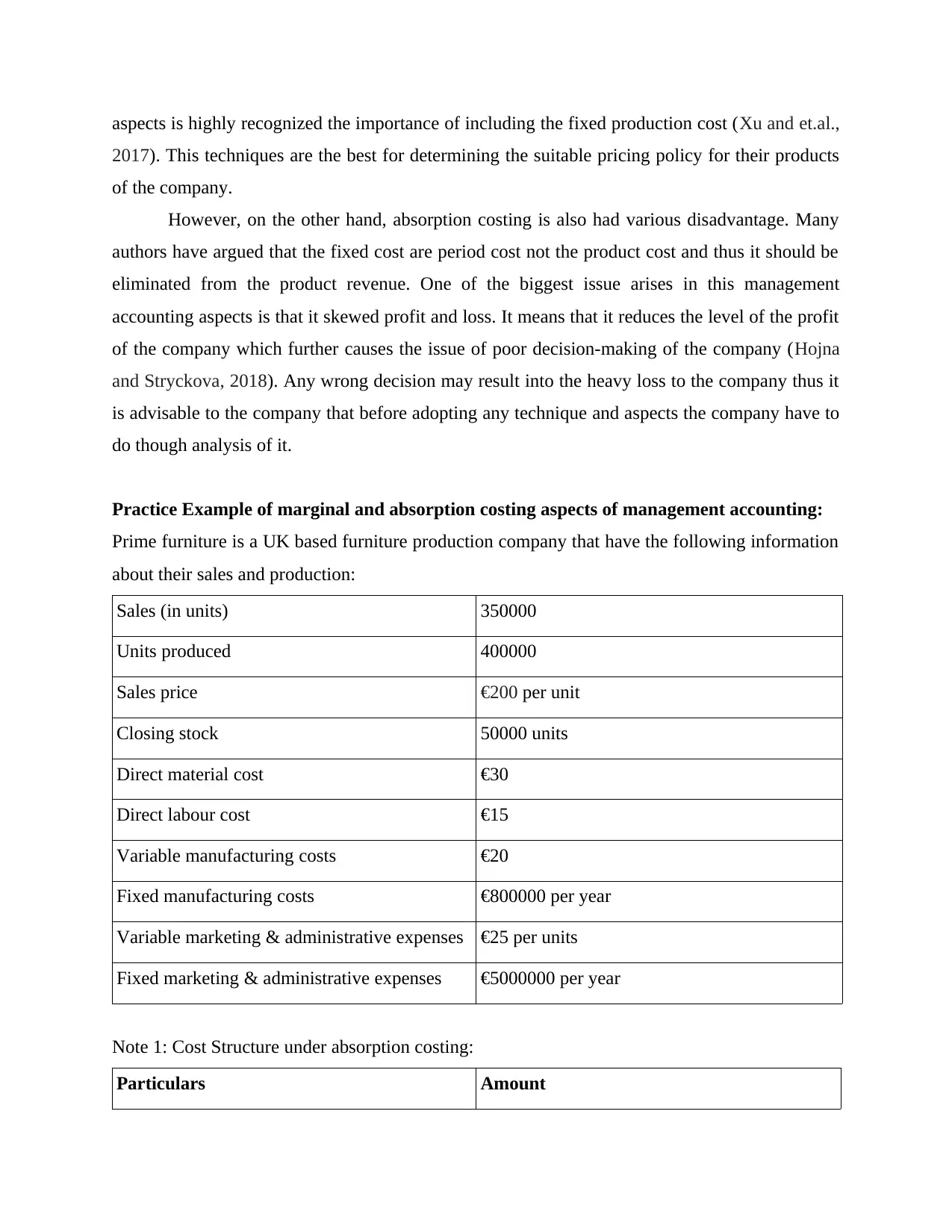

Practice Example of marginal and absorption costing aspects of management accounting:

Prime furniture is a UK based furniture production company that have the following information

about their sales and production:

Sales (in units) 350000

Units produced 400000

Sales price €200 per unit

Closing stock 50000 units

Direct material cost €30

Direct labour cost €15

Variable manufacturing costs €20

Fixed manufacturing costs €800000 per year

Variable marketing & administrative expenses €25 per units

Fixed marketing & administrative expenses €5000000 per year

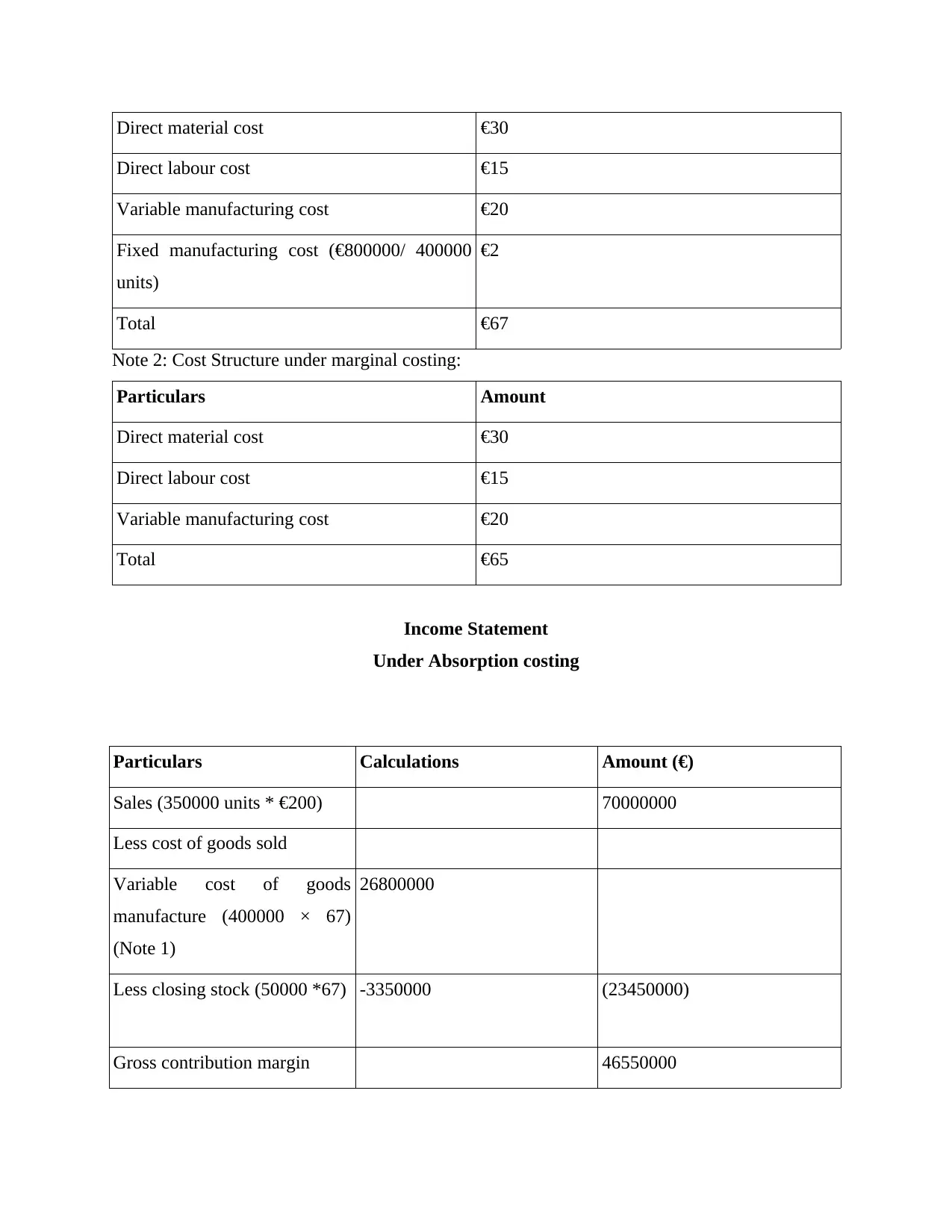

Note 1: Cost Structure under absorption costing:

Particulars Amount

2017). This techniques are the best for determining the suitable pricing policy for their products

of the company.

However, on the other hand, absorption costing is also had various disadvantage. Many

authors have argued that the fixed cost are period cost not the product cost and thus it should be

eliminated from the product revenue. One of the biggest issue arises in this management

accounting aspects is that it skewed profit and loss. It means that it reduces the level of the profit

of the company which further causes the issue of poor decision-making of the company (Hojna

and Stryckova, 2018). Any wrong decision may result into the heavy loss to the company thus it

is advisable to the company that before adopting any technique and aspects the company have to

do though analysis of it.

Practice Example of marginal and absorption costing aspects of management accounting:

Prime furniture is a UK based furniture production company that have the following information

about their sales and production:

Sales (in units) 350000

Units produced 400000

Sales price €200 per unit

Closing stock 50000 units

Direct material cost €30

Direct labour cost €15

Variable manufacturing costs €20

Fixed manufacturing costs €800000 per year

Variable marketing & administrative expenses €25 per units

Fixed marketing & administrative expenses €5000000 per year

Note 1: Cost Structure under absorption costing:

Particulars Amount

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Direct material cost €30

Direct labour cost €15

Variable manufacturing cost €20

Fixed manufacturing cost (€800000/ 400000

units)

€2

Total €67

Note 2: Cost Structure under marginal costing:

Particulars Amount

Direct material cost €30

Direct labour cost €15

Variable manufacturing cost €20

Total €65

Income Statement

Under Absorption costing

Particulars Calculations Amount (€)

Sales (350000 units * €200) 70000000

Less cost of goods sold

Variable cost of goods

manufacture (400000 × 67)

(Note 1)

26800000

Less closing stock (50000 *67) -3350000 (23450000)

Gross contribution margin 46550000

Direct labour cost €15

Variable manufacturing cost €20

Fixed manufacturing cost (€800000/ 400000

units)

€2

Total €67

Note 2: Cost Structure under marginal costing:

Particulars Amount

Direct material cost €30

Direct labour cost €15

Variable manufacturing cost €20

Total €65

Income Statement

Under Absorption costing

Particulars Calculations Amount (€)

Sales (350000 units * €200) 70000000

Less cost of goods sold

Variable cost of goods

manufacture (400000 × 67)

(Note 1)

26800000

Less closing stock (50000 *67) -3350000 (23450000)

Gross contribution margin 46550000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

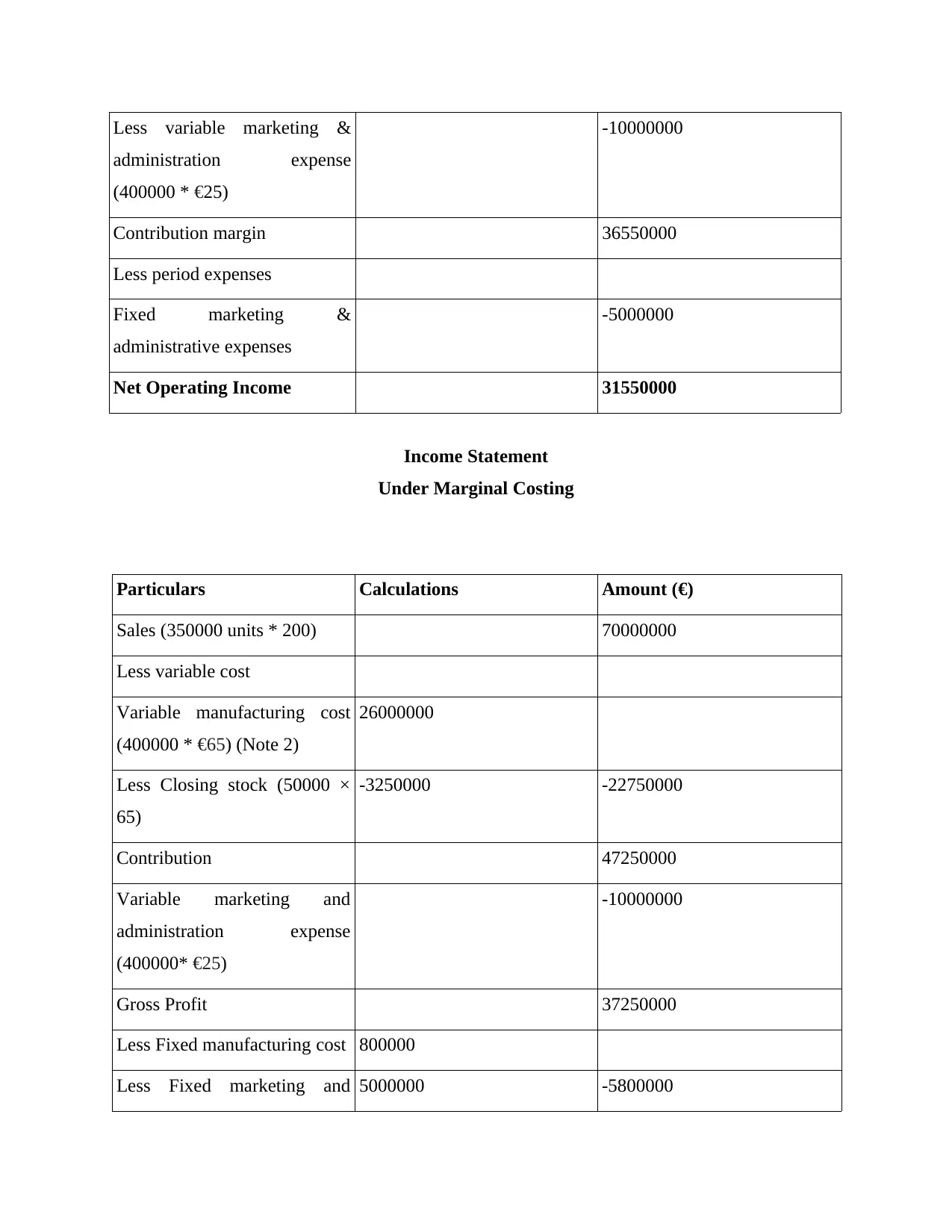

Less variable marketing &

administration expense

(400000 * €25)

-10000000

Contribution margin 36550000

Less period expenses

Fixed marketing &

administrative expenses

-5000000

Net Operating Income 31550000

Income Statement

Under Marginal Costing

Particulars Calculations Amount (€)

Sales (350000 units * 200) 70000000

Less variable cost

Variable manufacturing cost

(400000 * €65) (Note 2)

26000000

Less Closing stock (50000 ×

65)

-3250000 -22750000

Contribution 47250000

Variable marketing and

administration expense

(400000* €25)

-10000000

Gross Profit 37250000

Less Fixed manufacturing cost 800000

Less Fixed marketing and 5000000 -5800000

administration expense

(400000 * €25)

-10000000

Contribution margin 36550000

Less period expenses

Fixed marketing &

administrative expenses

-5000000

Net Operating Income 31550000

Income Statement

Under Marginal Costing

Particulars Calculations Amount (€)

Sales (350000 units * 200) 70000000

Less variable cost

Variable manufacturing cost

(400000 * €65) (Note 2)

26000000

Less Closing stock (50000 ×

65)

-3250000 -22750000

Contribution 47250000

Variable marketing and

administration expense

(400000* €25)

-10000000

Gross Profit 37250000

Less Fixed manufacturing cost 800000

Less Fixed marketing and 5000000 -5800000

administrative expenses

Net Profit 31450000

Reason of difference between absorption profit and marginal profit

The main reason behind the difference between the profit under marginal and absorption

costing aspects is the fixed cost of manufacturing the products. In the marginal costing, the fixed

cost of products is excluded while on the other hand in the absorption costing the fixed cost is

remained in the product. The impact of which the fixed cost is seized in the closing stock of the

product. At the time when the production of the product is higher than the sales of the product

than the net operating income under absorption costing is higher than marginal costing. On the

other hand, in the case when the production of product is lower than the sales of the product than

the absorption profit must be lesser than the marginal costing (Devi, Irasari and Sudibyo, 2020).

On the above practical example, it is stated that the production of units is higher while the sale is

lower which further result into the high absorption costing and low marginal costing.

CONCLUSION

From the above report it has been concluded that management accounting is one of the

most important branch of accounting concerned with the use of accounting information for

making various decisions which may be both of financial and non-financial nature. In this essay,

the various functions performed by management accountant such as planning, controlling,

decision-making and forecasting has been discussed. Also, value aspects of MA has been

evaluated such balanced scorecard and activity based costing which indicates what a great role

the MA play in an organization to ensure their sustainability on the path of success and also to

compete in market which is highly competitive and everchanging.

Net Profit 31450000

Reason of difference between absorption profit and marginal profit

The main reason behind the difference between the profit under marginal and absorption

costing aspects is the fixed cost of manufacturing the products. In the marginal costing, the fixed

cost of products is excluded while on the other hand in the absorption costing the fixed cost is

remained in the product. The impact of which the fixed cost is seized in the closing stock of the

product. At the time when the production of the product is higher than the sales of the product

than the net operating income under absorption costing is higher than marginal costing. On the

other hand, in the case when the production of product is lower than the sales of the product than

the absorption profit must be lesser than the marginal costing (Devi, Irasari and Sudibyo, 2020).

On the above practical example, it is stated that the production of units is higher while the sale is

lower which further result into the high absorption costing and low marginal costing.

CONCLUSION

From the above report it has been concluded that management accounting is one of the

most important branch of accounting concerned with the use of accounting information for

making various decisions which may be both of financial and non-financial nature. In this essay,

the various functions performed by management accountant such as planning, controlling,

decision-making and forecasting has been discussed. Also, value aspects of MA has been

evaluated such balanced scorecard and activity based costing which indicates what a great role

the MA play in an organization to ensure their sustainability on the path of success and also to

compete in market which is highly competitive and everchanging.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.