Significance and Essentials of Management Accounting Systems

VerifiedAdded on 2023/01/19

|18

|4601

|63

AI Summary

This report discusses the significance and essentials of different management accounting systems, such as cost accounting system, price optimization system, job costing system, and inventory management system. It also describes the different methods used for reporting, including budget reports, receivable reports, cost accounting reports, and performance reports. Additionally, it evaluates the benefits and applications of these systems and discusses different planning tools used under budgetary control.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

LO1. ................................................................................................................................................3

Explaining the significance of MA and essentials of different MA systems...............................3

Describing different methods that are been used for reporting....................................................4

Evaluating benefits and the application of the various MA systems ..........................................6

LO2..................................................................................................................................................7

LO3..................................................................................................................................................9

Evaluating different planning tools that are been used under budgetary control........................9

Analysing uses of different budgetary tools .............................................................................12

LO4................................................................................................................................................13

Comparing the use of different MA systems by the firm in order to respond the financial

problems ....................................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

LO1. ................................................................................................................................................3

Explaining the significance of MA and essentials of different MA systems...............................3

Describing different methods that are been used for reporting....................................................4

Evaluating benefits and the application of the various MA systems ..........................................6

LO2..................................................................................................................................................7

LO3..................................................................................................................................................9

Evaluating different planning tools that are been used under budgetary control........................9

Analysing uses of different budgetary tools .............................................................................12

LO4................................................................................................................................................13

Comparing the use of different MA systems by the firm in order to respond the financial

problems ....................................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting refers to the process of facilitating financial information and the

resources to managers in respect of making suitable decisions. It is been used by the internal

team of an enterprise which reflects the information regarding the performance, budget,

receivable, cost etc. that helps in smooth running of the business operations in an overall market.

MA is the practice that assesses the cost of business in preparing of its internal financial reports

and helps the managers in setting financial and the costing data, thereafter converting such data

into the useful information for the manager in an enterprise. The present report is based on

Agmet Ltd which is a medium sized manufacturer of UK that deals in chemical products.

Furthermore the study involves role of management accounting and highlights relating to the

different MA systems and various reports that are been prepared for the purpose of reporting.

Moreover, the study also includes the evaluation of the different planning tools under the

budgetary control with the systems that are used by the firm in order to respond with the

financial problems.

LO1.

Explaining the significance of MA and essentials of different MA systems

Management accounting is considered as the most valuable tool because it helps in

analysing the real and the value cost that incurred within the operations of a manufacturing firm.

This type of information is been used internally by the managers in order run the company in a

better way. Management accounting to a large extent differs from the financial accounting as

under MA an Agment Ltd need not have to follow the accounting standards and the principles

while under financial accounting, at the time of preparing the financial statements all the

accounting standards need to be follow (Rasyid, Sugiarto and Kosasih, 2017). MA includes the

decision making regarding monetary as well as non-monetary aspects of the business. MA helps

the Agment Ltd in making for an effective plan and ensuring adequate controlling over the

activities so that if there any deviation, corrective measures could be adopted. However,

Financial accounting enables the company in recording financial performance for a particular

accounting period and presenting the financial information to the users. There are various MA

systems that plays a crucial role in the smooth functioning of an Agment Ltd are as follows-

Cost accounting system- It is the system that includes recording of the production

activities of an Agment Ltd by using a perpetual system of an inventory. In other words, this

Management accounting refers to the process of facilitating financial information and the

resources to managers in respect of making suitable decisions. It is been used by the internal

team of an enterprise which reflects the information regarding the performance, budget,

receivable, cost etc. that helps in smooth running of the business operations in an overall market.

MA is the practice that assesses the cost of business in preparing of its internal financial reports

and helps the managers in setting financial and the costing data, thereafter converting such data

into the useful information for the manager in an enterprise. The present report is based on

Agmet Ltd which is a medium sized manufacturer of UK that deals in chemical products.

Furthermore the study involves role of management accounting and highlights relating to the

different MA systems and various reports that are been prepared for the purpose of reporting.

Moreover, the study also includes the evaluation of the different planning tools under the

budgetary control with the systems that are used by the firm in order to respond with the

financial problems.

LO1.

Explaining the significance of MA and essentials of different MA systems

Management accounting is considered as the most valuable tool because it helps in

analysing the real and the value cost that incurred within the operations of a manufacturing firm.

This type of information is been used internally by the managers in order run the company in a

better way. Management accounting to a large extent differs from the financial accounting as

under MA an Agment Ltd need not have to follow the accounting standards and the principles

while under financial accounting, at the time of preparing the financial statements all the

accounting standards need to be follow (Rasyid, Sugiarto and Kosasih, 2017). MA includes the

decision making regarding monetary as well as non-monetary aspects of the business. MA helps

the Agment Ltd in making for an effective plan and ensuring adequate controlling over the

activities so that if there any deviation, corrective measures could be adopted. However,

Financial accounting enables the company in recording financial performance for a particular

accounting period and presenting the financial information to the users. There are various MA

systems that plays a crucial role in the smooth functioning of an Agment Ltd are as follows-

Cost accounting system- It is the system that includes recording of the production

activities of an Agment Ltd by using a perpetual system of an inventory. In other words, this

system is been designed for tracking the cost incurred at different level of the production stages.

It acts as the most important system for an entity in estimating their product cost which in turn

helps in making the profitability analysis, cost control and an inventory valuation. It helps in

evaluating the accurate cost of the product in order to achieve profitable operations as through

this system a firm can find out the products that are not profitable.

Price optimization system- It reflects utilization of the mathematical procedure by an

enterprise for the purpose of finding out the reaction of the buyers towards different prices set for

the product or the services through the use of diverse channels (Kurniawan and Azmi, 2019).

This system of MA is the model that helps an Agment Ltd in calculating varying demand of the

customer at different level of price and thereafter combining data with the information regarding

the cost and the inventory levels fro recommending best prices that leads to improvement in the

profits. This allows the company in using the pricing as the powerful tool of profit lever that

often is been underdeveloped. This system could be used by an Agment Ltd for tailoring the

pricing in respect of the customer segments through stimulating the way in which the targeted

customer will be responding to the changes in prices with the data driven areas.

Job costing system- It includes practice of accumulating the information regarding the

costs attached with the particular service or the production job. This information is required for

submitting cost information to the customer under the contract where the costs are been

reimbursed (Bempah, 2015). This system plays a vital role within an Agment Ltd that provides

for the products or the services in varying cost that depends upon the customer specifications.

Inventory management system- This system reflects a combination of the technology

and the procedures that oversees maintenance and monitoring of the stocked products in order to

assess that whether those goods are the assets, supplies, raw material or finished product of an

organization (Lawrence, Karlsson and Thollander, 2018). This system helps an enterprise in

managing their inventory, keeping track over the items so that inventory needs could be analysed

and in turn automate the ordering process of the firm which results in quick delivery of the

product.

Describing different methods that are been used for reporting

Under MA, an Agment Ltd prepares for different reports that is been used for planning,

decision making, measuring and regulating the performance of the firm. Such reports are

continuously been generated for an entire period as per the requirements. Most of the critical

It acts as the most important system for an entity in estimating their product cost which in turn

helps in making the profitability analysis, cost control and an inventory valuation. It helps in

evaluating the accurate cost of the product in order to achieve profitable operations as through

this system a firm can find out the products that are not profitable.

Price optimization system- It reflects utilization of the mathematical procedure by an

enterprise for the purpose of finding out the reaction of the buyers towards different prices set for

the product or the services through the use of diverse channels (Kurniawan and Azmi, 2019).

This system of MA is the model that helps an Agment Ltd in calculating varying demand of the

customer at different level of price and thereafter combining data with the information regarding

the cost and the inventory levels fro recommending best prices that leads to improvement in the

profits. This allows the company in using the pricing as the powerful tool of profit lever that

often is been underdeveloped. This system could be used by an Agment Ltd for tailoring the

pricing in respect of the customer segments through stimulating the way in which the targeted

customer will be responding to the changes in prices with the data driven areas.

Job costing system- It includes practice of accumulating the information regarding the

costs attached with the particular service or the production job. This information is required for

submitting cost information to the customer under the contract where the costs are been

reimbursed (Bempah, 2015). This system plays a vital role within an Agment Ltd that provides

for the products or the services in varying cost that depends upon the customer specifications.

Inventory management system- This system reflects a combination of the technology

and the procedures that oversees maintenance and monitoring of the stocked products in order to

assess that whether those goods are the assets, supplies, raw material or finished product of an

organization (Lawrence, Karlsson and Thollander, 2018). This system helps an enterprise in

managing their inventory, keeping track over the items so that inventory needs could be analysed

and in turn automate the ordering process of the firm which results in quick delivery of the

product.

Describing different methods that are been used for reporting

Under MA, an Agment Ltd prepares for different reports that is been used for planning,

decision making, measuring and regulating the performance of the firm. Such reports are

continuously been generated for an entire period as per the requirements. Most of the critical

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

decisions depends upon the authenticity of MA reports and the managers of an entity analyses

these reports in highlighting particular patterns and converting it into the useful information

(Altukhova, Vasileva and Yemelyanov, 2018). Such reports are as follows-

Budget report- In order to measure the performance of an organization, budget reports is

of great importance as it provides for creating an entire budget for understanding grand scheme

of the business. While preparing this report, an estimation is been made on the basis of the

previous experiences for meeting an unforeseen events which may arise. Budget involves

information relating to all the sources of the expenditure and the earnings (Method of reporting,

2018). An Agment Ltd seeks for achieving its mission, goals, objectives in the budgeted amount

by performing the task as per the set standards and the strategies. This report guides the

managers in offering better incentives to their employees, renegotiating the terms with their

suppliers and the vendors, cutting down the cost etc.

Receivable report- In case if an Agment Ltd relies on extending credit then framing of

this report is very essential as it indicates the details regarding the remaining balances of the

clients into the particular period of time that allows the managers in determining the defaulters

and in finding the issues that are been faced by an entity in respect of its collection process. In

case of large number of defaulters, company needs to transform its credit policies as the cash

flow is very critical for running the operations of the business in an effective and efficient

manner (Broucker, De Wit and Leisyte, 2015). Receivable report helps the firm in recovering the

amount that is due on part of the debtors in timely manner so that it needs not face any uncertain

circumstances like insolvency, bad debts etc.

Cost accounting report- This report computes cost of the items that are been produced

such as cost of raw material, labour, overhead and other. Cost report provides for the summary of

all the information which the managers uses for realizing cost price of the goods against its

selling price. Through this, profit are been estimated or monitored as it offers a clear picture

regarding all the costs which went into procurement or the production of the articles (Agyeman,

2017). Therefore, cost accounting report facilitates exact understanding of overall expenses that

is important for making optimum use of the resources within all the departments.

Performance report- It is the MA report that is been created for reviewing performance

of an Agment Ltd and also its employees at end of an accounting period. Under this departmental

reports are been framed by the managers that states the efficiency of each department in

these reports in highlighting particular patterns and converting it into the useful information

(Altukhova, Vasileva and Yemelyanov, 2018). Such reports are as follows-

Budget report- In order to measure the performance of an organization, budget reports is

of great importance as it provides for creating an entire budget for understanding grand scheme

of the business. While preparing this report, an estimation is been made on the basis of the

previous experiences for meeting an unforeseen events which may arise. Budget involves

information relating to all the sources of the expenditure and the earnings (Method of reporting,

2018). An Agment Ltd seeks for achieving its mission, goals, objectives in the budgeted amount

by performing the task as per the set standards and the strategies. This report guides the

managers in offering better incentives to their employees, renegotiating the terms with their

suppliers and the vendors, cutting down the cost etc.

Receivable report- In case if an Agment Ltd relies on extending credit then framing of

this report is very essential as it indicates the details regarding the remaining balances of the

clients into the particular period of time that allows the managers in determining the defaulters

and in finding the issues that are been faced by an entity in respect of its collection process. In

case of large number of defaulters, company needs to transform its credit policies as the cash

flow is very critical for running the operations of the business in an effective and efficient

manner (Broucker, De Wit and Leisyte, 2015). Receivable report helps the firm in recovering the

amount that is due on part of the debtors in timely manner so that it needs not face any uncertain

circumstances like insolvency, bad debts etc.

Cost accounting report- This report computes cost of the items that are been produced

such as cost of raw material, labour, overhead and other. Cost report provides for the summary of

all the information which the managers uses for realizing cost price of the goods against its

selling price. Through this, profit are been estimated or monitored as it offers a clear picture

regarding all the costs which went into procurement or the production of the articles (Agyeman,

2017). Therefore, cost accounting report facilitates exact understanding of overall expenses that

is important for making optimum use of the resources within all the departments.

Performance report- It is the MA report that is been created for reviewing performance

of an Agment Ltd and also its employees at end of an accounting period. Under this departmental

reports are been framed by the managers that states the efficiency of each department in

performing the task. Managers make use of this report for making important strategic decisions

in relation to the future of an entity. It plays crucial role for an Agment Ltd in keeping an

accurate measure relating to their strategy towards attaining their vision efficiently and as per the

standards of performance.

other reports- It includes framing of the order information reports, competitors analysis,

project reports. Other similar kind of reports that are very vital for an entity. Such reports are

either been generated within or outside through the professionals. Selection of the most suitable

action course depends highly on the capabilities of the company in context of handling reporting

needs (Bedford, 2018). For attaining maximum out of the decisions, managers must access for

credible and the authentic MA reports.

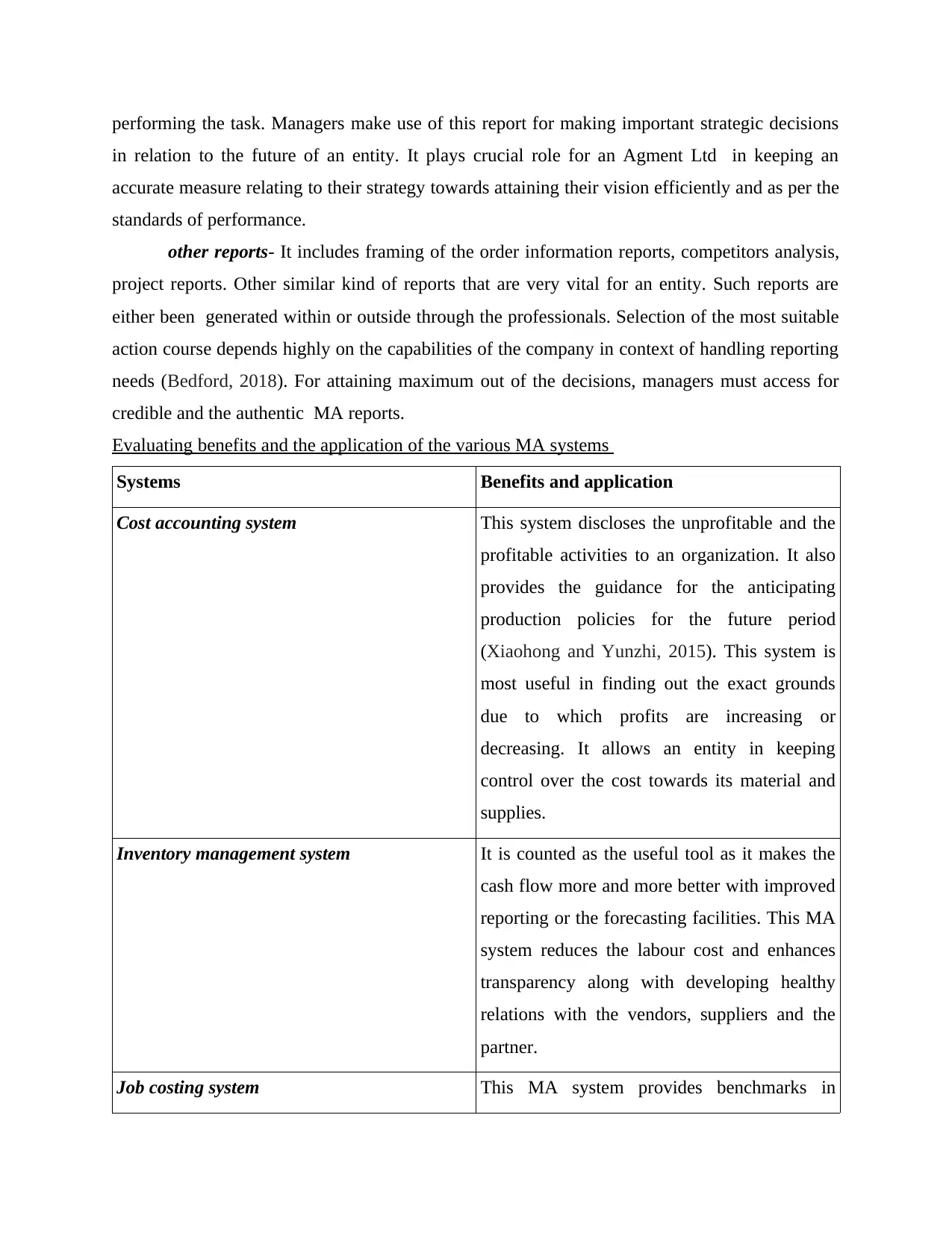

Evaluating benefits and the application of the various MA systems

Systems Benefits and application

Cost accounting system This system discloses the unprofitable and the

profitable activities to an organization. It also

provides the guidance for the anticipating

production policies for the future period

(Xiaohong and Yunzhi, 2015). This system is

most useful in finding out the exact grounds

due to which profits are increasing or

decreasing. It allows an entity in keeping

control over the cost towards its material and

supplies.

Inventory management system It is counted as the useful tool as it makes the

cash flow more and more better with improved

reporting or the forecasting facilities. This MA

system reduces the labour cost and enhances

transparency along with developing healthy

relations with the vendors, suppliers and the

partner.

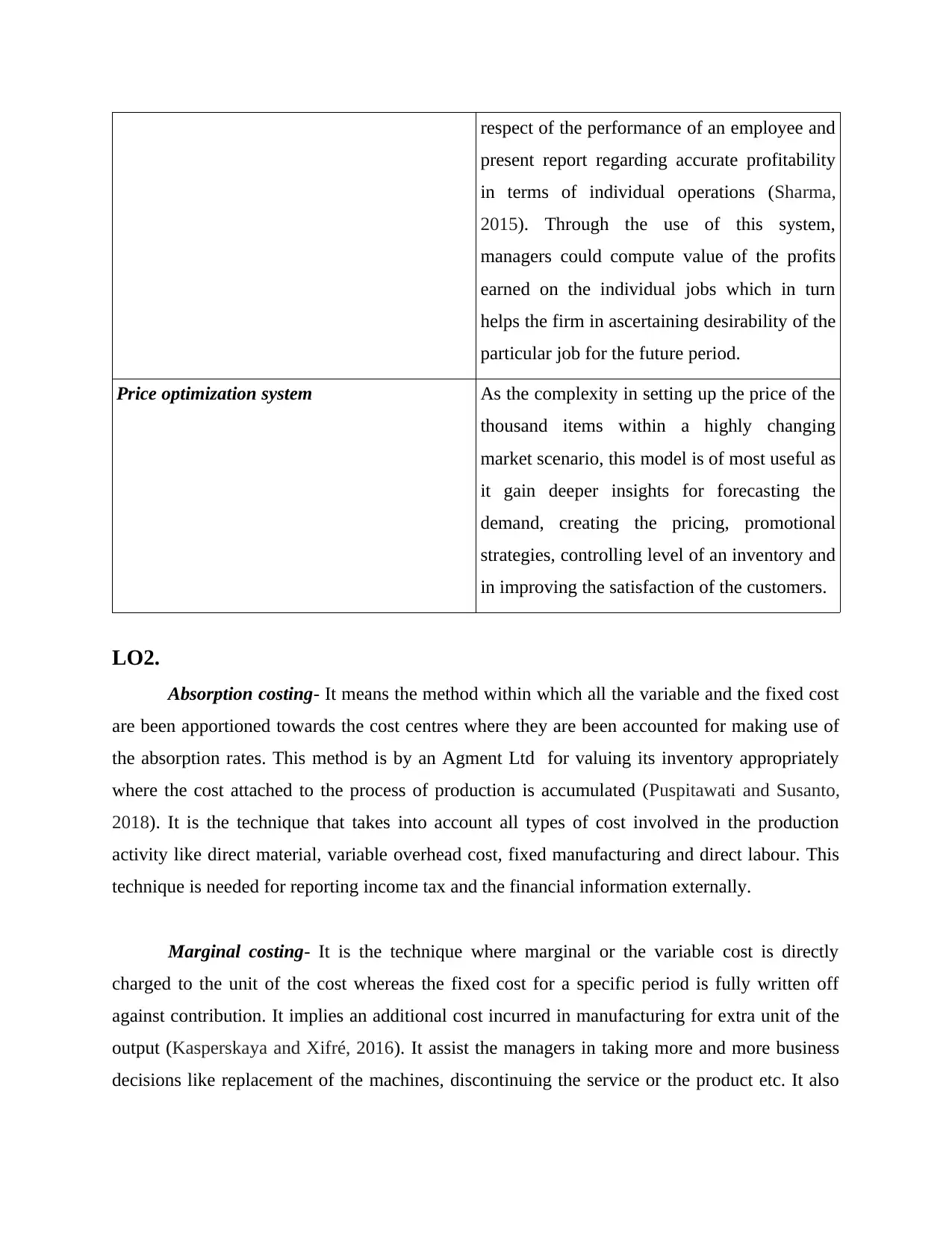

Job costing system This MA system provides benchmarks in

in relation to the future of an entity. It plays crucial role for an Agment Ltd in keeping an

accurate measure relating to their strategy towards attaining their vision efficiently and as per the

standards of performance.

other reports- It includes framing of the order information reports, competitors analysis,

project reports. Other similar kind of reports that are very vital for an entity. Such reports are

either been generated within or outside through the professionals. Selection of the most suitable

action course depends highly on the capabilities of the company in context of handling reporting

needs (Bedford, 2018). For attaining maximum out of the decisions, managers must access for

credible and the authentic MA reports.

Evaluating benefits and the application of the various MA systems

Systems Benefits and application

Cost accounting system This system discloses the unprofitable and the

profitable activities to an organization. It also

provides the guidance for the anticipating

production policies for the future period

(Xiaohong and Yunzhi, 2015). This system is

most useful in finding out the exact grounds

due to which profits are increasing or

decreasing. It allows an entity in keeping

control over the cost towards its material and

supplies.

Inventory management system It is counted as the useful tool as it makes the

cash flow more and more better with improved

reporting or the forecasting facilities. This MA

system reduces the labour cost and enhances

transparency along with developing healthy

relations with the vendors, suppliers and the

partner.

Job costing system This MA system provides benchmarks in

respect of the performance of an employee and

present report regarding accurate profitability

in terms of individual operations (Sharma,

2015). Through the use of this system,

managers could compute value of the profits

earned on the individual jobs which in turn

helps the firm in ascertaining desirability of the

particular job for the future period.

Price optimization system As the complexity in setting up the price of the

thousand items within a highly changing

market scenario, this model is of most useful as

it gain deeper insights for forecasting the

demand, creating the pricing, promotional

strategies, controlling level of an inventory and

in improving the satisfaction of the customers.

LO2.

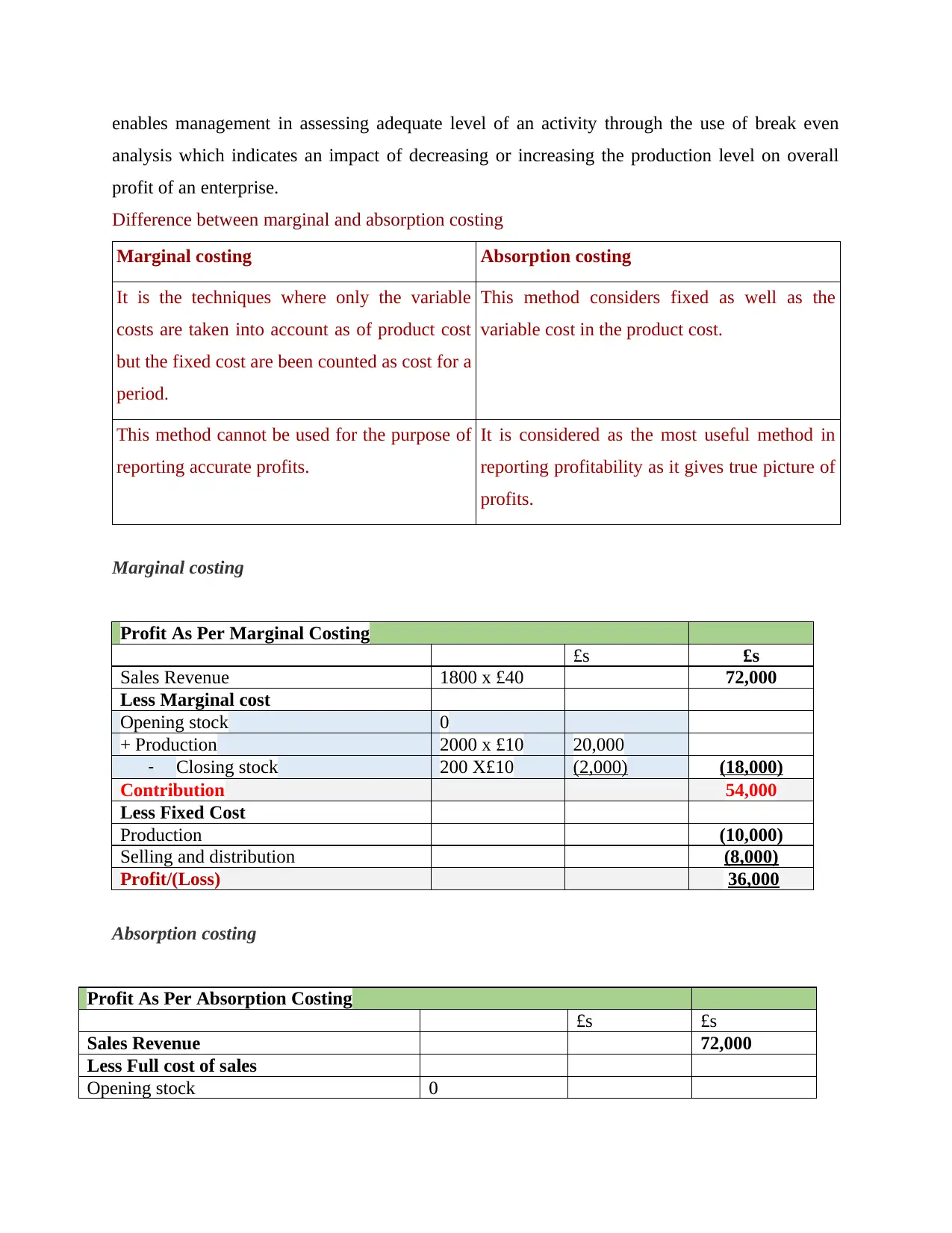

Absorption costing- It means the method within which all the variable and the fixed cost

are been apportioned towards the cost centres where they are been accounted for making use of

the absorption rates. This method is by an Agment Ltd for valuing its inventory appropriately

where the cost attached to the process of production is accumulated (Puspitawati and Susanto,

2018). It is the technique that takes into account all types of cost involved in the production

activity like direct material, variable overhead cost, fixed manufacturing and direct labour. This

technique is needed for reporting income tax and the financial information externally.

Marginal costing- It is the technique where marginal or the variable cost is directly

charged to the unit of the cost whereas the fixed cost for a specific period is fully written off

against contribution. It implies an additional cost incurred in manufacturing for extra unit of the

output (Kasperskaya and Xifré, 2016). It assist the managers in taking more and more business

decisions like replacement of the machines, discontinuing the service or the product etc. It also

present report regarding accurate profitability

in terms of individual operations (Sharma,

2015). Through the use of this system,

managers could compute value of the profits

earned on the individual jobs which in turn

helps the firm in ascertaining desirability of the

particular job for the future period.

Price optimization system As the complexity in setting up the price of the

thousand items within a highly changing

market scenario, this model is of most useful as

it gain deeper insights for forecasting the

demand, creating the pricing, promotional

strategies, controlling level of an inventory and

in improving the satisfaction of the customers.

LO2.

Absorption costing- It means the method within which all the variable and the fixed cost

are been apportioned towards the cost centres where they are been accounted for making use of

the absorption rates. This method is by an Agment Ltd for valuing its inventory appropriately

where the cost attached to the process of production is accumulated (Puspitawati and Susanto,

2018). It is the technique that takes into account all types of cost involved in the production

activity like direct material, variable overhead cost, fixed manufacturing and direct labour. This

technique is needed for reporting income tax and the financial information externally.

Marginal costing- It is the technique where marginal or the variable cost is directly

charged to the unit of the cost whereas the fixed cost for a specific period is fully written off

against contribution. It implies an additional cost incurred in manufacturing for extra unit of the

output (Kasperskaya and Xifré, 2016). It assist the managers in taking more and more business

decisions like replacement of the machines, discontinuing the service or the product etc. It also

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

enables management in assessing adequate level of an activity through the use of break even

analysis which indicates an impact of decreasing or increasing the production level on overall

profit of an enterprise.

Difference between marginal and absorption costing

Marginal costing Absorption costing

It is the techniques where only the variable

costs are taken into account as of product cost

but the fixed cost are been counted as cost for a

period.

This method considers fixed as well as the

variable cost in the product cost.

This method cannot be used for the purpose of

reporting accurate profits.

It is considered as the most useful method in

reporting profitability as it gives true picture of

profits.

Marginal costing

Profit As Per Marginal Costing

£s £s

Sales Revenue 1800 x £40 72,000

Less Marginal cost

Opening stock 0

+ Production 2000 x £10 20,000

- Closing stock 200 X£10 (2,000) (18,000)

Contribution 54,000

Less Fixed Cost

Production (10,000)

Selling and distribution (8,000)

Profit/(Loss) 36,000

Absorption costing

Profit As Per Absorption Costing

£s £s

Sales Revenue 72,000

Less Full cost of sales

Opening stock 0

analysis which indicates an impact of decreasing or increasing the production level on overall

profit of an enterprise.

Difference between marginal and absorption costing

Marginal costing Absorption costing

It is the techniques where only the variable

costs are taken into account as of product cost

but the fixed cost are been counted as cost for a

period.

This method considers fixed as well as the

variable cost in the product cost.

This method cannot be used for the purpose of

reporting accurate profits.

It is considered as the most useful method in

reporting profitability as it gives true picture of

profits.

Marginal costing

Profit As Per Marginal Costing

£s £s

Sales Revenue 1800 x £40 72,000

Less Marginal cost

Opening stock 0

+ Production 2000 x £10 20,000

- Closing stock 200 X£10 (2,000) (18,000)

Contribution 54,000

Less Fixed Cost

Production (10,000)

Selling and distribution (8,000)

Profit/(Loss) 36,000

Absorption costing

Profit As Per Absorption Costing

£s £s

Sales Revenue 72,000

Less Full cost of sales

Opening stock 0

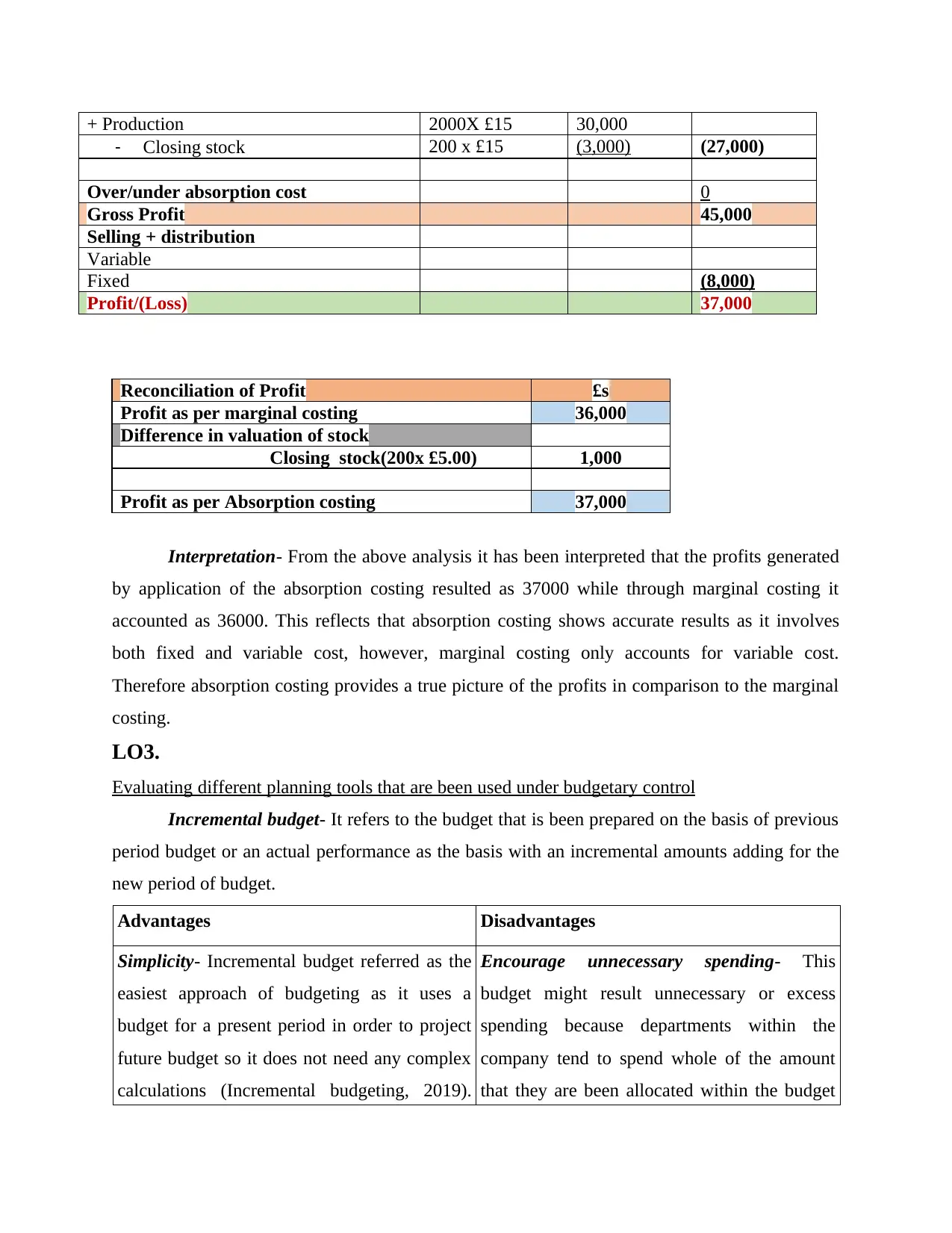

+ Production 2000X £15 30,000

- Closing stock 200 x £15 (3,000) (27,000)

Over/under absorption cost 0

Gross Profit 45,000

Selling + distribution

Variable

Fixed (8,000)

Profit/(Loss) 37,000

Reconciliation of Profit £s

Profit as per marginal costing 36,000

Difference in valuation of stock

Closing stock(200x £5.00) 1,000

Profit as per Absorption costing 37,000

Interpretation- From the above analysis it has been interpreted that the profits generated

by application of the absorption costing resulted as 37000 while through marginal costing it

accounted as 36000. This reflects that absorption costing shows accurate results as it involves

both fixed and variable cost, however, marginal costing only accounts for variable cost.

Therefore absorption costing provides a true picture of the profits in comparison to the marginal

costing.

LO3.

Evaluating different planning tools that are been used under budgetary control

Incremental budget- It refers to the budget that is been prepared on the basis of previous

period budget or an actual performance as the basis with an incremental amounts adding for the

new period of budget.

Advantages Disadvantages

Simplicity- Incremental budget referred as the

easiest approach of budgeting as it uses a

budget for a present period in order to project

future budget so it does not need any complex

calculations (Incremental budgeting, 2019).

Encourage unnecessary spending- This

budget might result unnecessary or excess

spending because departments within the

company tend to spend whole of the amount

that they are been allocated within the budget

- Closing stock 200 x £15 (3,000) (27,000)

Over/under absorption cost 0

Gross Profit 45,000

Selling + distribution

Variable

Fixed (8,000)

Profit/(Loss) 37,000

Reconciliation of Profit £s

Profit as per marginal costing 36,000

Difference in valuation of stock

Closing stock(200x £5.00) 1,000

Profit as per Absorption costing 37,000

Interpretation- From the above analysis it has been interpreted that the profits generated

by application of the absorption costing resulted as 37000 while through marginal costing it

accounted as 36000. This reflects that absorption costing shows accurate results as it involves

both fixed and variable cost, however, marginal costing only accounts for variable cost.

Therefore absorption costing provides a true picture of the profits in comparison to the marginal

costing.

LO3.

Evaluating different planning tools that are been used under budgetary control

Incremental budget- It refers to the budget that is been prepared on the basis of previous

period budget or an actual performance as the basis with an incremental amounts adding for the

new period of budget.

Advantages Disadvantages

Simplicity- Incremental budget referred as the

easiest approach of budgeting as it uses a

budget for a present period in order to project

future budget so it does not need any complex

calculations (Incremental budgeting, 2019).

Encourage unnecessary spending- This

budget might result unnecessary or excess

spending because departments within the

company tend to spend whole of the amount

that they are been allocated within the budget

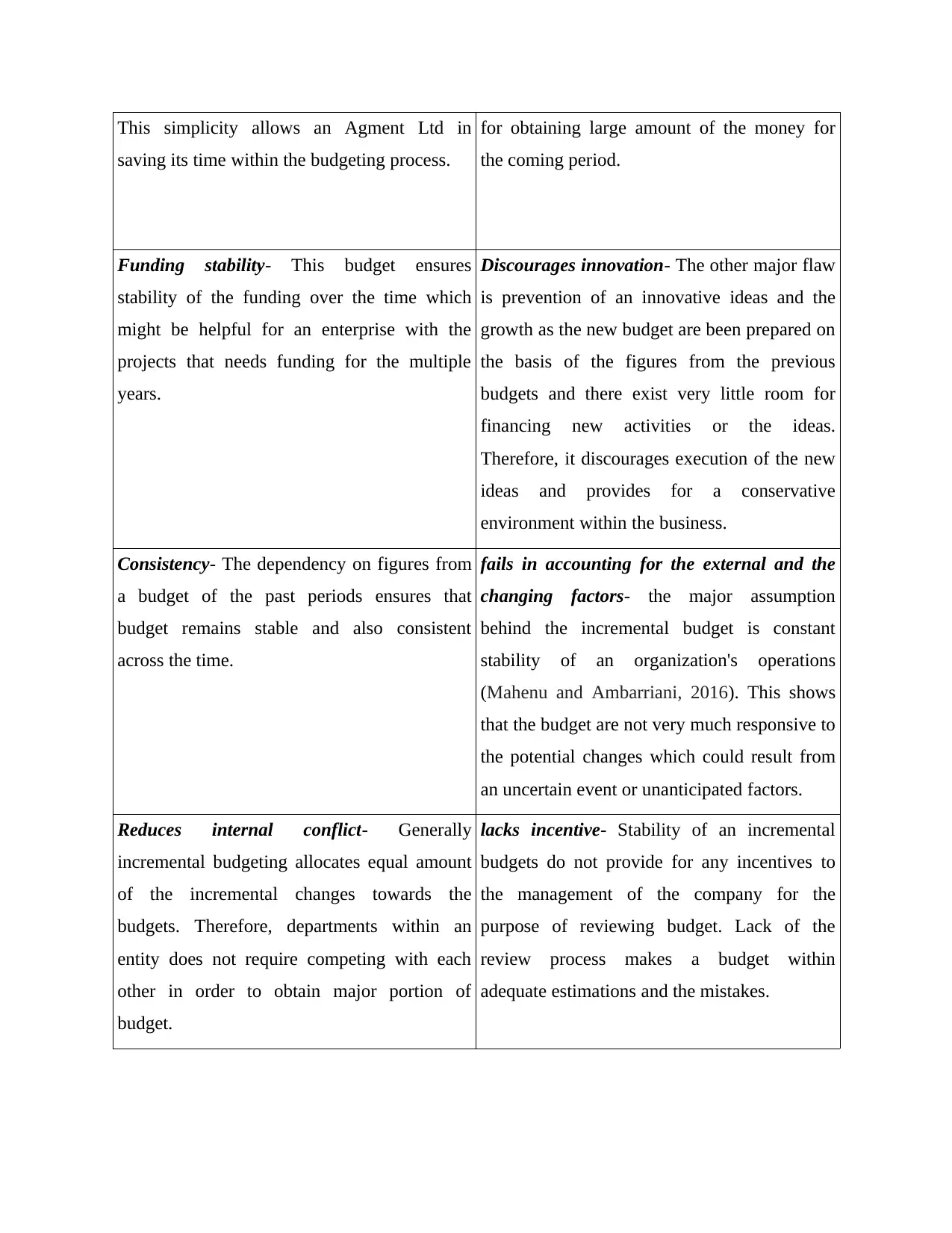

This simplicity allows an Agment Ltd in

saving its time within the budgeting process.

for obtaining large amount of the money for

the coming period.

Funding stability- This budget ensures

stability of the funding over the time which

might be helpful for an enterprise with the

projects that needs funding for the multiple

years.

Discourages innovation- The other major flaw

is prevention of an innovative ideas and the

growth as the new budget are been prepared on

the basis of the figures from the previous

budgets and there exist very little room for

financing new activities or the ideas.

Therefore, it discourages execution of the new

ideas and provides for a conservative

environment within the business.

Consistency- The dependency on figures from

a budget of the past periods ensures that

budget remains stable and also consistent

across the time.

fails in accounting for the external and the

changing factors- the major assumption

behind the incremental budget is constant

stability of an organization's operations

(Mahenu and Ambarriani, 2016). This shows

that the budget are not very much responsive to

the potential changes which could result from

an uncertain event or unanticipated factors.

Reduces internal conflict- Generally

incremental budgeting allocates equal amount

of the incremental changes towards the

budgets. Therefore, departments within an

entity does not require competing with each

other in order to obtain major portion of

budget.

lacks incentive- Stability of an incremental

budgets do not provide for any incentives to

the management of the company for the

purpose of reviewing budget. Lack of the

review process makes a budget within

adequate estimations and the mistakes.

saving its time within the budgeting process.

for obtaining large amount of the money for

the coming period.

Funding stability- This budget ensures

stability of the funding over the time which

might be helpful for an enterprise with the

projects that needs funding for the multiple

years.

Discourages innovation- The other major flaw

is prevention of an innovative ideas and the

growth as the new budget are been prepared on

the basis of the figures from the previous

budgets and there exist very little room for

financing new activities or the ideas.

Therefore, it discourages execution of the new

ideas and provides for a conservative

environment within the business.

Consistency- The dependency on figures from

a budget of the past periods ensures that

budget remains stable and also consistent

across the time.

fails in accounting for the external and the

changing factors- the major assumption

behind the incremental budget is constant

stability of an organization's operations

(Mahenu and Ambarriani, 2016). This shows

that the budget are not very much responsive to

the potential changes which could result from

an uncertain event or unanticipated factors.

Reduces internal conflict- Generally

incremental budgeting allocates equal amount

of the incremental changes towards the

budgets. Therefore, departments within an

entity does not require competing with each

other in order to obtain major portion of

budget.

lacks incentive- Stability of an incremental

budgets do not provide for any incentives to

the management of the company for the

purpose of reviewing budget. Lack of the

review process makes a budget within

adequate estimations and the mistakes.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

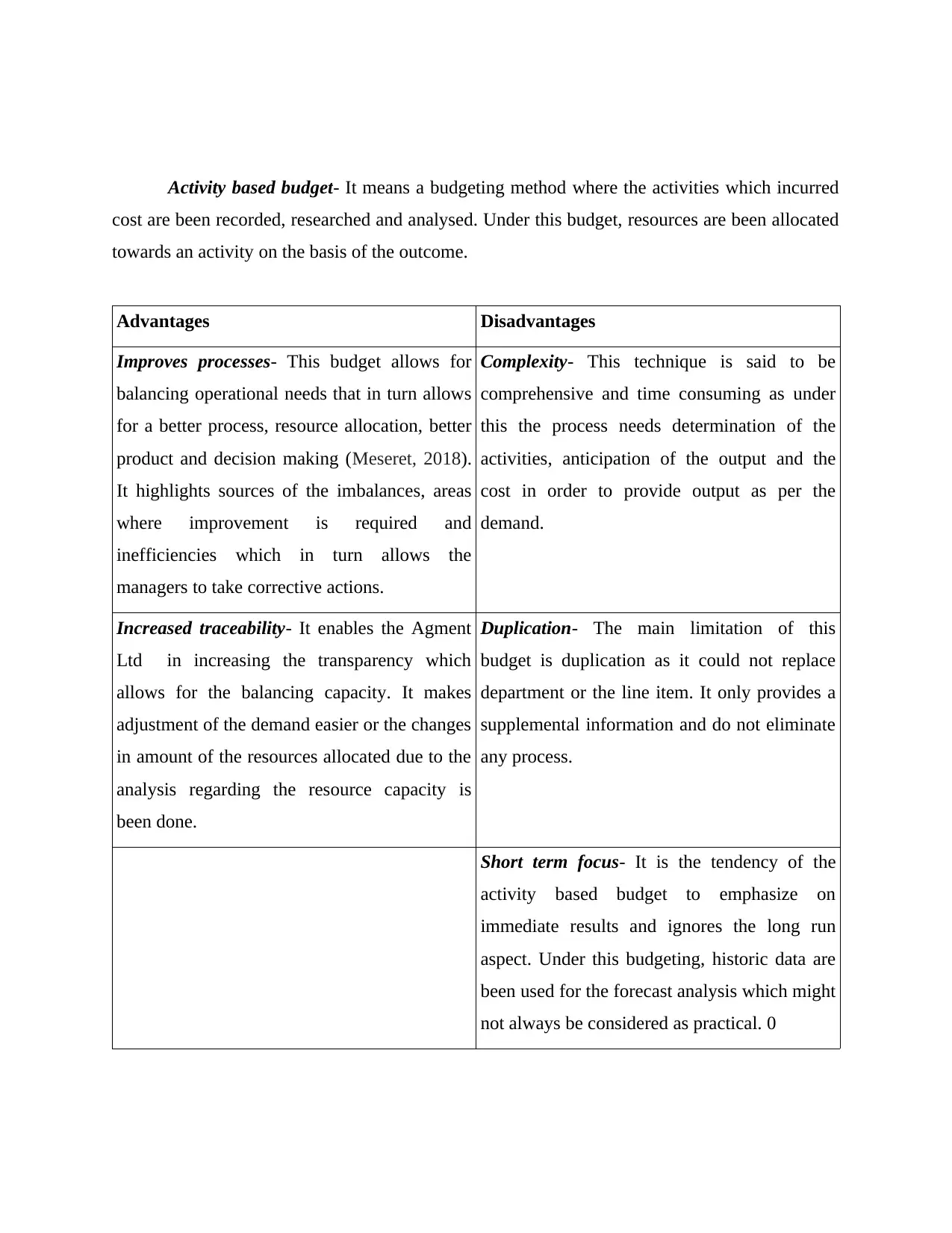

Activity based budget- It means a budgeting method where the activities which incurred

cost are been recorded, researched and analysed. Under this budget, resources are been allocated

towards an activity on the basis of the outcome.

Advantages Disadvantages

Improves processes- This budget allows for

balancing operational needs that in turn allows

for a better process, resource allocation, better

product and decision making (Meseret, 2018).

It highlights sources of the imbalances, areas

where improvement is required and

inefficiencies which in turn allows the

managers to take corrective actions.

Complexity- This technique is said to be

comprehensive and time consuming as under

this the process needs determination of the

activities, anticipation of the output and the

cost in order to provide output as per the

demand.

Increased traceability- It enables the Agment

Ltd in increasing the transparency which

allows for the balancing capacity. It makes

adjustment of the demand easier or the changes

in amount of the resources allocated due to the

analysis regarding the resource capacity is

been done.

Duplication- The main limitation of this

budget is duplication as it could not replace

department or the line item. It only provides a

supplemental information and do not eliminate

any process.

Short term focus- It is the tendency of the

activity based budget to emphasize on

immediate results and ignores the long run

aspect. Under this budgeting, historic data are

been used for the forecast analysis which might

not always be considered as practical. 0

cost are been recorded, researched and analysed. Under this budget, resources are been allocated

towards an activity on the basis of the outcome.

Advantages Disadvantages

Improves processes- This budget allows for

balancing operational needs that in turn allows

for a better process, resource allocation, better

product and decision making (Meseret, 2018).

It highlights sources of the imbalances, areas

where improvement is required and

inefficiencies which in turn allows the

managers to take corrective actions.

Complexity- This technique is said to be

comprehensive and time consuming as under

this the process needs determination of the

activities, anticipation of the output and the

cost in order to provide output as per the

demand.

Increased traceability- It enables the Agment

Ltd in increasing the transparency which

allows for the balancing capacity. It makes

adjustment of the demand easier or the changes

in amount of the resources allocated due to the

analysis regarding the resource capacity is

been done.

Duplication- The main limitation of this

budget is duplication as it could not replace

department or the line item. It only provides a

supplemental information and do not eliminate

any process.

Short term focus- It is the tendency of the

activity based budget to emphasize on

immediate results and ignores the long run

aspect. Under this budgeting, historic data are

been used for the forecast analysis which might

not always be considered as practical. 0

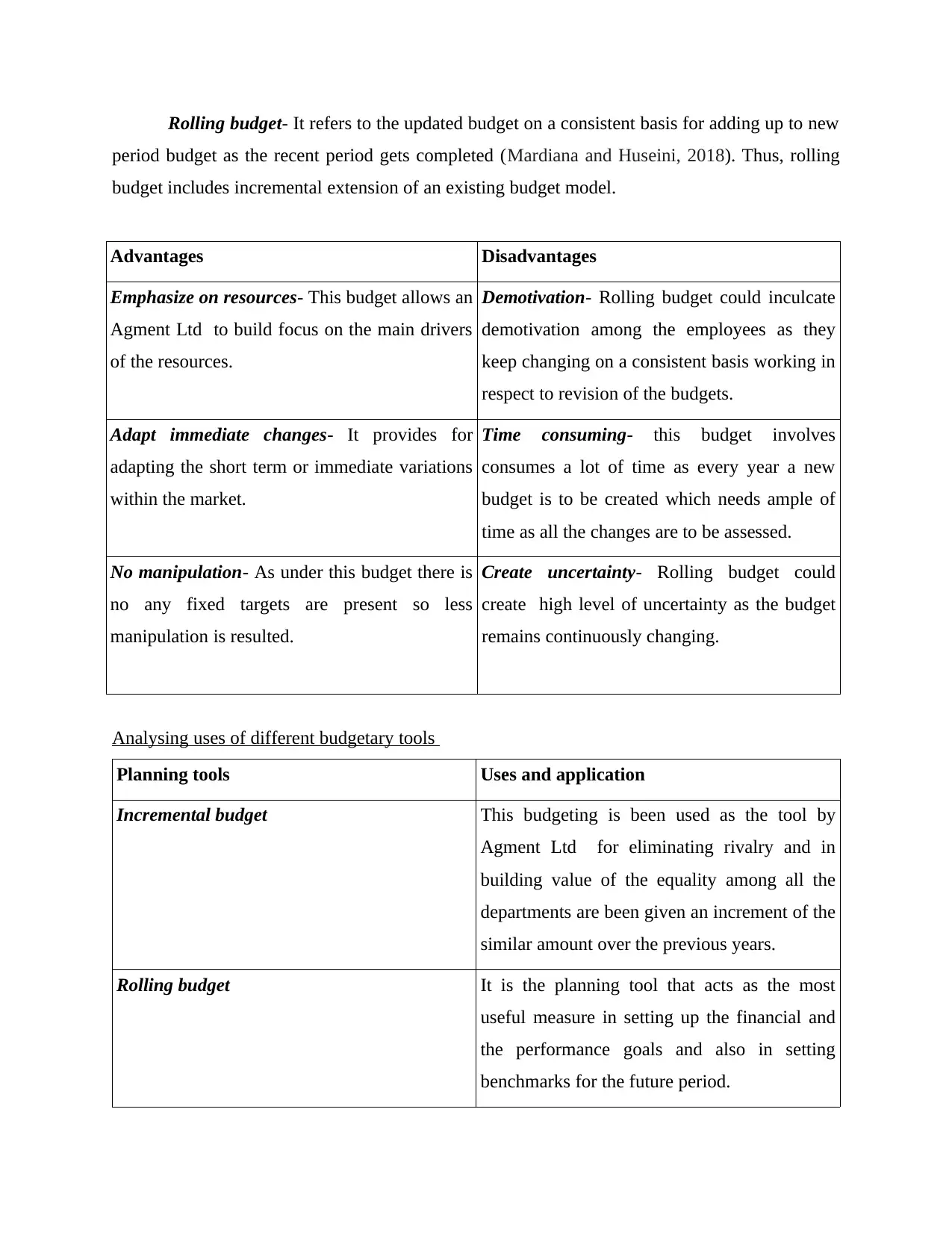

Rolling budget- It refers to the updated budget on a consistent basis for adding up to new

period budget as the recent period gets completed (Mardiana and Huseini, 2018). Thus, rolling

budget includes incremental extension of an existing budget model.

Advantages Disadvantages

Emphasize on resources- This budget allows an

Agment Ltd to build focus on the main drivers

of the resources.

Demotivation- Rolling budget could inculcate

demotivation among the employees as they

keep changing on a consistent basis working in

respect to revision of the budgets.

Adapt immediate changes- It provides for

adapting the short term or immediate variations

within the market.

Time consuming- this budget involves

consumes a lot of time as every year a new

budget is to be created which needs ample of

time as all the changes are to be assessed.

No manipulation- As under this budget there is

no any fixed targets are present so less

manipulation is resulted.

Create uncertainty- Rolling budget could

create high level of uncertainty as the budget

remains continuously changing.

Analysing uses of different budgetary tools

Planning tools Uses and application

Incremental budget This budgeting is been used as the tool by

Agment Ltd for eliminating rivalry and in

building value of the equality among all the

departments are been given an increment of the

similar amount over the previous years.

Rolling budget It is the planning tool that acts as the most

useful measure in setting up the financial and

the performance goals and also in setting

benchmarks for the future period.

period budget as the recent period gets completed (Mardiana and Huseini, 2018). Thus, rolling

budget includes incremental extension of an existing budget model.

Advantages Disadvantages

Emphasize on resources- This budget allows an

Agment Ltd to build focus on the main drivers

of the resources.

Demotivation- Rolling budget could inculcate

demotivation among the employees as they

keep changing on a consistent basis working in

respect to revision of the budgets.

Adapt immediate changes- It provides for

adapting the short term or immediate variations

within the market.

Time consuming- this budget involves

consumes a lot of time as every year a new

budget is to be created which needs ample of

time as all the changes are to be assessed.

No manipulation- As under this budget there is

no any fixed targets are present so less

manipulation is resulted.

Create uncertainty- Rolling budget could

create high level of uncertainty as the budget

remains continuously changing.

Analysing uses of different budgetary tools

Planning tools Uses and application

Incremental budget This budgeting is been used as the tool by

Agment Ltd for eliminating rivalry and in

building value of the equality among all the

departments are been given an increment of the

similar amount over the previous years.

Rolling budget It is the planning tool that acts as the most

useful measure in setting up the financial and

the performance goals and also in setting

benchmarks for the future period.

Activity based budget It is the system that is been used by an

enterprise in analysing activities that are

leading to cost within the business. This

budgetary tool works by dividing the cost in

accordance to activities that the company

requires to carry out for running its operations

smoothly.

LO4.

Comparing the use of different MA systems by the firm in order to respond the financial

problems

Balanced scorecard- It refers to the performance metric that relates to strategic

management and is used by the firm for identifying and improving several internal functions of

the business and its resulting outcome. This measure used fro measuring and facilitating the

feedback to an organization. As this approach provides a broader view of the major perspectives

such as customer, financial, internal process, growth outcome etc., an entity could be able to

resolve its financial problem in relation to raising the funds through the best sources and meeting

the demand of the customer.

Benchmarking- It is the practice of assessing performance of an entity's products,

services and the processes with that of the another business or rivalry for being the best within an

entire industry. This technique helps in identifying the internal opportunities for achieving

improvement (Kocmanova, A. and et.al., 2017). With the use of this tool Agment Ltd could be

able to attain competitive edge and overcome the financial problem regarding less profitability.

Key performance indicator- This MA tool stated as the measurable value which

demonstrates effectiveness of Agment Ltd in reaching its business objectives. For evaluating the

success, enterprise make use of KPI so that it could be able to reach its target efficiently and

effectively. It helps the company in overcoming its financial problem regarding measurement of

the success and in meeting the targets on time.

variance analysis- It means the study of the deviation that resulted in between the actual

and the standard budget. It acts as an analytical tool that helps in comparing the actual operation

of the firm with its budgeted operations. This tool enables the company in taking the appropriate

enterprise in analysing activities that are

leading to cost within the business. This

budgetary tool works by dividing the cost in

accordance to activities that the company

requires to carry out for running its operations

smoothly.

LO4.

Comparing the use of different MA systems by the firm in order to respond the financial

problems

Balanced scorecard- It refers to the performance metric that relates to strategic

management and is used by the firm for identifying and improving several internal functions of

the business and its resulting outcome. This measure used fro measuring and facilitating the

feedback to an organization. As this approach provides a broader view of the major perspectives

such as customer, financial, internal process, growth outcome etc., an entity could be able to

resolve its financial problem in relation to raising the funds through the best sources and meeting

the demand of the customer.

Benchmarking- It is the practice of assessing performance of an entity's products,

services and the processes with that of the another business or rivalry for being the best within an

entire industry. This technique helps in identifying the internal opportunities for achieving

improvement (Kocmanova, A. and et.al., 2017). With the use of this tool Agment Ltd could be

able to attain competitive edge and overcome the financial problem regarding less profitability.

Key performance indicator- This MA tool stated as the measurable value which

demonstrates effectiveness of Agment Ltd in reaching its business objectives. For evaluating the

success, enterprise make use of KPI so that it could be able to reach its target efficiently and

effectively. It helps the company in overcoming its financial problem regarding measurement of

the success and in meeting the targets on time.

variance analysis- It means the study of the deviation that resulted in between the actual

and the standard budget. It acts as an analytical tool that helps in comparing the actual operation

of the firm with its budgeted operations. This tool enables the company in taking the appropriate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

measures for resolving the financial problems regarding filling the gap between actual and the

standard estimates in order to attain goals as per the set strategies.

ABC Ltd. Agment Ltd

This entity makes use of variance analysis and

benchmarking technique which helps the firm

in achieving their set targets and in mitigating

the potential risk that eventually develops trust

among the members for delivering as per the

planned standards.

It utilizes key performance indicator and

balanced scorecard that enables in overcoming

the financial issues and provides fro strategic

insights in achieving the business goals by

keeping in view all the perspectives that could

affect the business. KPI helps the firm in

evaluating its performance in terms of numbers

so that accuracy could be attained and there are

very less chances of errors.

standard estimates in order to attain goals as per the set strategies.

ABC Ltd. Agment Ltd

This entity makes use of variance analysis and

benchmarking technique which helps the firm

in achieving their set targets and in mitigating

the potential risk that eventually develops trust

among the members for delivering as per the

planned standards.

It utilizes key performance indicator and

balanced scorecard that enables in overcoming

the financial issues and provides fro strategic

insights in achieving the business goals by

keeping in view all the perspectives that could

affect the business. KPI helps the firm in

evaluating its performance in terms of numbers

so that accuracy could be attained and there are

very less chances of errors.

CONCLUSION

By summing up the above study it has been indicated that management accounting plays

a significant role in the routine activities of the business with respect to setting up the strategies,

performance, cost incurred in producing the goods of Agmet Ltd. MA systems helps the

company in attaining growing success for the future periods with ensuring prpoer control over

the cost so that higher profitability could be achieved. Similarly budgetary tools helps in

responding towards the financial problems and in enhancing the financial performance and the

position of an enterprise.

By summing up the above study it has been indicated that management accounting plays

a significant role in the routine activities of the business with respect to setting up the strategies,

performance, cost incurred in producing the goods of Agmet Ltd. MA systems helps the

company in attaining growing success for the future periods with ensuring prpoer control over

the cost so that higher profitability could be achieved. Similarly budgetary tools helps in

responding towards the financial problems and in enhancing the financial performance and the

position of an enterprise.

REFERENCES

Books and journals

Agyeman, B., 2017. BALANCED SCORECARD AS A TOOL FOR MANAGING

PERFORMANCE IN SELECTED GHANAIAN BANKS. European Journal of Research

and Reflection in Educational Sciences Vol. 5(5).

Altukhova, N., Vasileva, E. and Yemelyanov, V., 2018. How to Add Value to Business by

Employing Digital Technologies and Transforming Management Approaches.

Bedford, D.A., 2018. Sustainable Knowledge Management Strategies: Aligning Business

Capabilities and Knowledge Management Goals. In Global Practices in Knowledge

Management for Societal and Organizational Development(pp. 46-73). IGI Global.

Bempah, B.S.O., 2015. Factors affecting budgeting and financial management practices of

district health directorates in Ghana. International Journal of Arts & Sciences. 8(7). p.303.

Broucker, B., De Wit, K. and Leisyte, L., 2015. An evaluation of new public management in

higher education. Same rationale, different implementation. In EAIR, Date: 2015/08/30-

2015/09/02, Location: Krems.

Kasperskaya, Y. and Xifré, R., 2016. The Effectiveness of Reforms in Public Sector Accounting

and Financial Management: The Case of Spain, 2010-2015.

Kocmanova, A. and et.al., 2017. Corporate sustainability measurement and assessment of Czech

manufacturing companies using a composite indicator. Engineering Economics. 28(1).

pp.88-100.

Kurniawan, P.C. and Azmi, F., 2019. The Effect of Management Morality on Accounting Fraud

with Internal Control as A Moderating Variable (Study in Pemalang Regency). Riset

Akuntansi dan Keuangan Indonesia. 4(2). pp.77-85.

Lawrence, A., Karlsson, M. and Thollander, P., 2018. Effects of firm characteristics and energy

management for improving energy efficiency in the pulp and paper industry. Energy. 153.

pp.825-835.

Mahenu, N.F.P. and Ambarriani, A.S., 2016. Pengaruh Management Accounting System Dalam

Memoderasi Hubungan Antara Process Quality Management Dengan Kinerja Kualitas

Produk. Jurnal Akuntansi Fakultas Ekonomi.

Books and journals

Agyeman, B., 2017. BALANCED SCORECARD AS A TOOL FOR MANAGING

PERFORMANCE IN SELECTED GHANAIAN BANKS. European Journal of Research

and Reflection in Educational Sciences Vol. 5(5).

Altukhova, N., Vasileva, E. and Yemelyanov, V., 2018. How to Add Value to Business by

Employing Digital Technologies and Transforming Management Approaches.

Bedford, D.A., 2018. Sustainable Knowledge Management Strategies: Aligning Business

Capabilities and Knowledge Management Goals. In Global Practices in Knowledge

Management for Societal and Organizational Development(pp. 46-73). IGI Global.

Bempah, B.S.O., 2015. Factors affecting budgeting and financial management practices of

district health directorates in Ghana. International Journal of Arts & Sciences. 8(7). p.303.

Broucker, B., De Wit, K. and Leisyte, L., 2015. An evaluation of new public management in

higher education. Same rationale, different implementation. In EAIR, Date: 2015/08/30-

2015/09/02, Location: Krems.

Kasperskaya, Y. and Xifré, R., 2016. The Effectiveness of Reforms in Public Sector Accounting

and Financial Management: The Case of Spain, 2010-2015.

Kocmanova, A. and et.al., 2017. Corporate sustainability measurement and assessment of Czech

manufacturing companies using a composite indicator. Engineering Economics. 28(1).

pp.88-100.

Kurniawan, P.C. and Azmi, F., 2019. The Effect of Management Morality on Accounting Fraud

with Internal Control as A Moderating Variable (Study in Pemalang Regency). Riset

Akuntansi dan Keuangan Indonesia. 4(2). pp.77-85.

Lawrence, A., Karlsson, M. and Thollander, P., 2018. Effects of firm characteristics and energy

management for improving energy efficiency in the pulp and paper industry. Energy. 153.

pp.825-835.

Mahenu, N.F.P. and Ambarriani, A.S., 2016. Pengaruh Management Accounting System Dalam

Memoderasi Hubungan Antara Process Quality Management Dengan Kinerja Kualitas

Produk. Jurnal Akuntansi Fakultas Ekonomi.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Mardiana, S. and Huseini, M., 2018. HOW BIG DATA MANAGEMENT AND

GOVERNANCE MECHANISMS ENHANCE SUPPLY CHAIN

PERFORMANCE. ICASPGS. p.217.

Meseret, G., 2018. EFFECTIVENESS OF PROJECT MANAGEMENT TOOLS AND

TECHNIQUES FOR PROJECT PERFORMANCE IN THE CONTEXT OF WORLD

VISION ETHIOPIA (Doctoral dissertation).

Puspitawati, L. and Susanto, A., 2018, November. The Influence of Business Strategy Through

the Management Accounting Information System to the Quality of Management

Accounting Information-Evidence in Indonesia. In International Conference on Business,

Economic, Social Science and Humanities (ICOBEST 2018). Atlantis Press.

Rasyid, A., Sugiarto, E. and Kosasih, W., 2017. MANAGEMENT ACCOUNTING

TECHNIQUES AND CORPORATE PERFORMANCE OF MANUFACTURING

INDUSTRIES. RISK GOVERNANCE & CONTROL: Financial markets and institutions.

p.116.

Sharma, G., 2015. Practices of Financial and Management Accounting: Evidence fromSmall and

Medium-Sized Enterprises of Nepal. Journal of Nepalese Business Studies. 9(1). pp.77-86.

Xiaohong, H. and Yunzhi, J., 2015. The Management Equity Incentive and Real Earnings Under

the Different Company Governance Strength——The Protective Role of

Marketization. Economy and Management. (1). p.15.

Online

Method of reporting. 2018. [Online]. Available through:

<https://www.completecontroller.com/types-of-managerial-accounting-reports/>

Incremental budgeting. 2019. [Online]. Available

through:<https://corporatefinanceinstitute.com/resources/knowledge/finance/incremental-

budgeting/>

GOVERNANCE MECHANISMS ENHANCE SUPPLY CHAIN

PERFORMANCE. ICASPGS. p.217.

Meseret, G., 2018. EFFECTIVENESS OF PROJECT MANAGEMENT TOOLS AND

TECHNIQUES FOR PROJECT PERFORMANCE IN THE CONTEXT OF WORLD

VISION ETHIOPIA (Doctoral dissertation).

Puspitawati, L. and Susanto, A., 2018, November. The Influence of Business Strategy Through

the Management Accounting Information System to the Quality of Management

Accounting Information-Evidence in Indonesia. In International Conference on Business,

Economic, Social Science and Humanities (ICOBEST 2018). Atlantis Press.

Rasyid, A., Sugiarto, E. and Kosasih, W., 2017. MANAGEMENT ACCOUNTING

TECHNIQUES AND CORPORATE PERFORMANCE OF MANUFACTURING

INDUSTRIES. RISK GOVERNANCE & CONTROL: Financial markets and institutions.

p.116.

Sharma, G., 2015. Practices of Financial and Management Accounting: Evidence fromSmall and

Medium-Sized Enterprises of Nepal. Journal of Nepalese Business Studies. 9(1). pp.77-86.

Xiaohong, H. and Yunzhi, J., 2015. The Management Equity Incentive and Real Earnings Under

the Different Company Governance Strength——The Protective Role of

Marketization. Economy and Management. (1). p.15.

Online

Method of reporting. 2018. [Online]. Available through:

<https://www.completecontroller.com/types-of-managerial-accounting-reports/>

Incremental budgeting. 2019. [Online]. Available

through:<https://corporatefinanceinstitute.com/resources/knowledge/finance/incremental-

budgeting/>

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.