Management Accounting Systems and Techniques for Oshodi Plc

VerifiedAdded on 2021/02/20

|17

|5461

|17

Report

AI Summary

This report provides a detailed analysis of management accounting systems and their application within Oshodi Plc, a manufacturing company specializing in JOJO fruit juice. The report covers various aspects of management accounting, including the essential requirements of management accounting systems, the benefits of these systems, and the integration of management accounting within organizational processes. It explores different methods of management accounting reports, such as budgeting reports, accounts receivable aging reports, inventory and manufacturing reports, and performance reports. Furthermore, the report delves into cost analysis techniques, specifically marginal and absorption costing, and their role in preparing income statements. It also examines the advantages of various planning tools used for budgetary control and their application in preparing and forecasting budgets. Finally, the report addresses the adoption of management accounting systems to respond to financial problems and the contribution of management accounting in ensuring the sustainable success of the organization.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential requirements of management accounting systems...1

M1 Benefits of management Accounting systems......................................................................3

D1 Integration of management accounting system and report within organisational process....4

P2 Different methods of management accounting reports .........................................................4

TASK 2............................................................................................................................................6

P3 Usage of the techniques of cost analysis to prepare income statement by using marginal

and absorption costing.................................................................................................................6

M2 Applying range of management accounting techniques.......................................................8

D2 Interpretation of above data...................................................................................................8

TASK 3............................................................................................................................................9

P4 Advantages of different planning tools used for budgetary control......................................9

M3 Analyse the use of different planning tools and their application for preparing and

forecasting budgets ..................................................................................................................10

TASK 4..........................................................................................................................................11

P5 Adoption of management accounting systems to respond financial problems ...................11

Contribution of management accounting in sustainable success of the organisation while

responding financial problems..................................................................................................12

D3 Application of planning tools to respond financial issue along with attainment of

sustainable success ...................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES.............................................................................................................................14

INTRODUCTION

Management accounting introduces as an useful process of preparing management

reports as well as accounts also. As it give timely and accurate statistical and financial

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential requirements of management accounting systems...1

M1 Benefits of management Accounting systems......................................................................3

D1 Integration of management accounting system and report within organisational process....4

P2 Different methods of management accounting reports .........................................................4

TASK 2............................................................................................................................................6

P3 Usage of the techniques of cost analysis to prepare income statement by using marginal

and absorption costing.................................................................................................................6

M2 Applying range of management accounting techniques.......................................................8

D2 Interpretation of above data...................................................................................................8

TASK 3............................................................................................................................................9

P4 Advantages of different planning tools used for budgetary control......................................9

M3 Analyse the use of different planning tools and their application for preparing and

forecasting budgets ..................................................................................................................10

TASK 4..........................................................................................................................................11

P5 Adoption of management accounting systems to respond financial problems ...................11

Contribution of management accounting in sustainable success of the organisation while

responding financial problems..................................................................................................12

D3 Application of planning tools to respond financial issue along with attainment of

sustainable success ...................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES.............................................................................................................................14

INTRODUCTION

Management accounting introduces as an useful process of preparing management

reports as well as accounts also. As it give timely and accurate statistical and financial

information which is required by business managers to make short-term or day-to-day decisions.

This type of accounting only followed by the internal team within an enterprise, and this is only

thing which creates it dissimilar from financial accounting. There are different benefits of

management accounting for an organisation such as decision making, planning, controlling

business operations, organising, understanding financial data, identifying business problem

areas, strategic management and so on. All these are main advantages of management accounting

which will help an organisation in its success and growth at marketplace. For this project Oshodi

Plc is chosen manufacturing organisation which mainly specialise in manufacturing of JOJO fruit

juice in all age bracket. The main purpose about conducting this this project is to give accurate

data to the internal stakeholders within an organisation. This information mainly related with the

functioning of the internal departments for effective decision making.

This report divided into different parts which covers understanding of management

accounting systems and different techniques of management accounting. This report will also

include effective techniques of cost analysis which will help an organisation in preparation of its

income statement with the use of marginal and absorption costing. Along with this, advantages

and disadvantages of different types of planning tools for budgetary control will be cover in this

report. At last, importance of management accounting in solving of financial problems will be

include in this assignment.

TASK 1

P1 Management accounting and essential requirements of management accounting systems

Management Accounting: It is the concept which includes usage of different accounting

systems behind the preparation of various accounts which depicts information related to different

departments of the organisation. All such information is further used by the manager of the

organisation to build decision making for effective operation of day to day functions(Zoni, Dossi

and Morelli, 2012). These systems further used in the process of making reports which aid to

gain the information to analyse the results. Afterwards, organisation is able to made changes in

their strategies in accordance to the deviations noticed after comparison of actual result with

standard. This will further aid in attainment of results in accordance to standard set by the

management.

This type of accounting only followed by the internal team within an enterprise, and this is only

thing which creates it dissimilar from financial accounting. There are different benefits of

management accounting for an organisation such as decision making, planning, controlling

business operations, organising, understanding financial data, identifying business problem

areas, strategic management and so on. All these are main advantages of management accounting

which will help an organisation in its success and growth at marketplace. For this project Oshodi

Plc is chosen manufacturing organisation which mainly specialise in manufacturing of JOJO fruit

juice in all age bracket. The main purpose about conducting this this project is to give accurate

data to the internal stakeholders within an organisation. This information mainly related with the

functioning of the internal departments for effective decision making.

This report divided into different parts which covers understanding of management

accounting systems and different techniques of management accounting. This report will also

include effective techniques of cost analysis which will help an organisation in preparation of its

income statement with the use of marginal and absorption costing. Along with this, advantages

and disadvantages of different types of planning tools for budgetary control will be cover in this

report. At last, importance of management accounting in solving of financial problems will be

include in this assignment.

TASK 1

P1 Management accounting and essential requirements of management accounting systems

Management Accounting: It is the concept which includes usage of different accounting

systems behind the preparation of various accounts which depicts information related to different

departments of the organisation. All such information is further used by the manager of the

organisation to build decision making for effective operation of day to day functions(Zoni, Dossi

and Morelli, 2012). These systems further used in the process of making reports which aid to

gain the information to analyse the results. Afterwards, organisation is able to made changes in

their strategies in accordance to the deviations noticed after comparison of actual result with

standard. This will further aid in attainment of results in accordance to standard set by the

management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting system: These systems are different type of accounts prepared

by the accountant to grab the information about the strength of internal departments working and

their contribution behind accomplishment of desired results. The different type of systems which

are prepared by Oshodi includes cost accounting, job costing. Inventory management and price

optimisation system. All these systems are different in nature and having their own contribution

within the organisation. Through proper study of all the information, manager able to get insight

into the departmental functioning(Bryer, 2013). The functioning of different accounting system

has their own contribution in the development of the organisation and accomplishment of the

objectives that can be ascertained from the description presented below:

Cost accounting system: This system is used for the purpose of analysing total cost of

the product. The same system is used by Oshodi to analyse the cost they incurred in the process

of preparing JOJO fruit juice. The main advantage that can gathered by the organisation with the

help of this method is about ascertainment of the financial performance by input results with the

actual. Also, this will help the management is ascertaining the contribution made by the JOJO

fruit juice in process of creating profit.

Inventory management system: The main function of this system is about effective

management of stock within the organisation by tracking the level of inventories they have at

warehouse. For the same purpose, Oshodi use this system and further use the results in creation

of work order, bill of materials in respect of the inventories which are used in preparation of

JOJO fruit juice. It improves the inventory management of the organisation and allows to track

the whole supply chain which is used to handle the whole process from production to retail.

Another benefit which is associated with this is about maintaining the inventory and focus on

continuous production of JOJO fruit juice without any disruption. The methods that can be used

very frequently in management of inventory are named as LIFO, FIFO and AVCO. To manage

the inventories in warehouse the method which is used is FIFO. For the purpose of ascertaining

the time period for re order of the raw material EOQ method is used(Grabner and Moers, 2013).

This will help to grab the information about the time period under which organisation has re

order their inventories.

Price optimisation system: The main function of this system is about ascertain the

behaviour of consumers on the different price of the fruit juice. The main advantage is that it

by the accountant to grab the information about the strength of internal departments working and

their contribution behind accomplishment of desired results. The different type of systems which

are prepared by Oshodi includes cost accounting, job costing. Inventory management and price

optimisation system. All these systems are different in nature and having their own contribution

within the organisation. Through proper study of all the information, manager able to get insight

into the departmental functioning(Bryer, 2013). The functioning of different accounting system

has their own contribution in the development of the organisation and accomplishment of the

objectives that can be ascertained from the description presented below:

Cost accounting system: This system is used for the purpose of analysing total cost of

the product. The same system is used by Oshodi to analyse the cost they incurred in the process

of preparing JOJO fruit juice. The main advantage that can gathered by the organisation with the

help of this method is about ascertainment of the financial performance by input results with the

actual. Also, this will help the management is ascertaining the contribution made by the JOJO

fruit juice in process of creating profit.

Inventory management system: The main function of this system is about effective

management of stock within the organisation by tracking the level of inventories they have at

warehouse. For the same purpose, Oshodi use this system and further use the results in creation

of work order, bill of materials in respect of the inventories which are used in preparation of

JOJO fruit juice. It improves the inventory management of the organisation and allows to track

the whole supply chain which is used to handle the whole process from production to retail.

Another benefit which is associated with this is about maintaining the inventory and focus on

continuous production of JOJO fruit juice without any disruption. The methods that can be used

very frequently in management of inventory are named as LIFO, FIFO and AVCO. To manage

the inventories in warehouse the method which is used is FIFO. For the purpose of ascertaining

the time period for re order of the raw material EOQ method is used(Grabner and Moers, 2013).

This will help to grab the information about the time period under which organisation has re

order their inventories.

Price optimisation system: The main function of this system is about ascertain the

behaviour of consumers on the different price of the fruit juice. The main advantage is that it

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

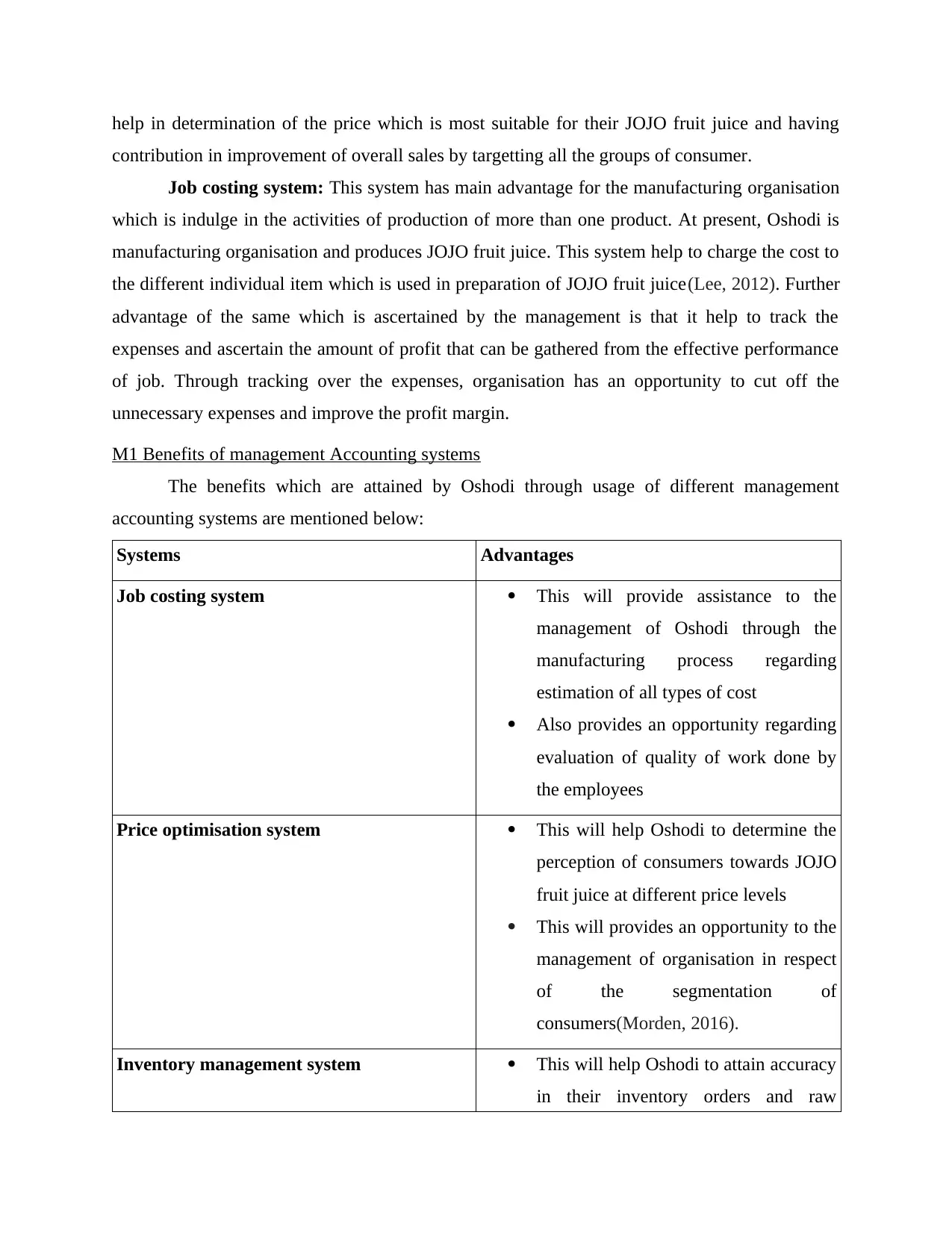

help in determination of the price which is most suitable for their JOJO fruit juice and having

contribution in improvement of overall sales by targetting all the groups of consumer.

Job costing system: This system has main advantage for the manufacturing organisation

which is indulge in the activities of production of more than one product. At present, Oshodi is

manufacturing organisation and produces JOJO fruit juice. This system help to charge the cost to

the different individual item which is used in preparation of JOJO fruit juice(Lee, 2012). Further

advantage of the same which is ascertained by the management is that it help to track the

expenses and ascertain the amount of profit that can be gathered from the effective performance

of job. Through tracking over the expenses, organisation has an opportunity to cut off the

unnecessary expenses and improve the profit margin.

M1 Benefits of management Accounting systems

The benefits which are attained by Oshodi through usage of different management

accounting systems are mentioned below:

Systems Advantages

Job costing system This will provide assistance to the

management of Oshodi through the

manufacturing process regarding

estimation of all types of cost

Also provides an opportunity regarding

evaluation of quality of work done by

the employees

Price optimisation system This will help Oshodi to determine the

perception of consumers towards JOJO

fruit juice at different price levels

This will provides an opportunity to the

management of organisation in respect

of the segmentation of

consumers(Morden, 2016).

Inventory management system This will help Oshodi to attain accuracy

in their inventory orders and raw

contribution in improvement of overall sales by targetting all the groups of consumer.

Job costing system: This system has main advantage for the manufacturing organisation

which is indulge in the activities of production of more than one product. At present, Oshodi is

manufacturing organisation and produces JOJO fruit juice. This system help to charge the cost to

the different individual item which is used in preparation of JOJO fruit juice(Lee, 2012). Further

advantage of the same which is ascertained by the management is that it help to track the

expenses and ascertain the amount of profit that can be gathered from the effective performance

of job. Through tracking over the expenses, organisation has an opportunity to cut off the

unnecessary expenses and improve the profit margin.

M1 Benefits of management Accounting systems

The benefits which are attained by Oshodi through usage of different management

accounting systems are mentioned below:

Systems Advantages

Job costing system This will provide assistance to the

management of Oshodi through the

manufacturing process regarding

estimation of all types of cost

Also provides an opportunity regarding

evaluation of quality of work done by

the employees

Price optimisation system This will help Oshodi to determine the

perception of consumers towards JOJO

fruit juice at different price levels

This will provides an opportunity to the

management of organisation in respect

of the segmentation of

consumers(Morden, 2016).

Inventory management system This will help Oshodi to attain accuracy

in their inventory orders and raw

material in respect of JOJO fruit juice

with the assistance of this system

The main emphasis of this system is

upon increment of effectiveness and

efficiency which in turn help to save

time and money

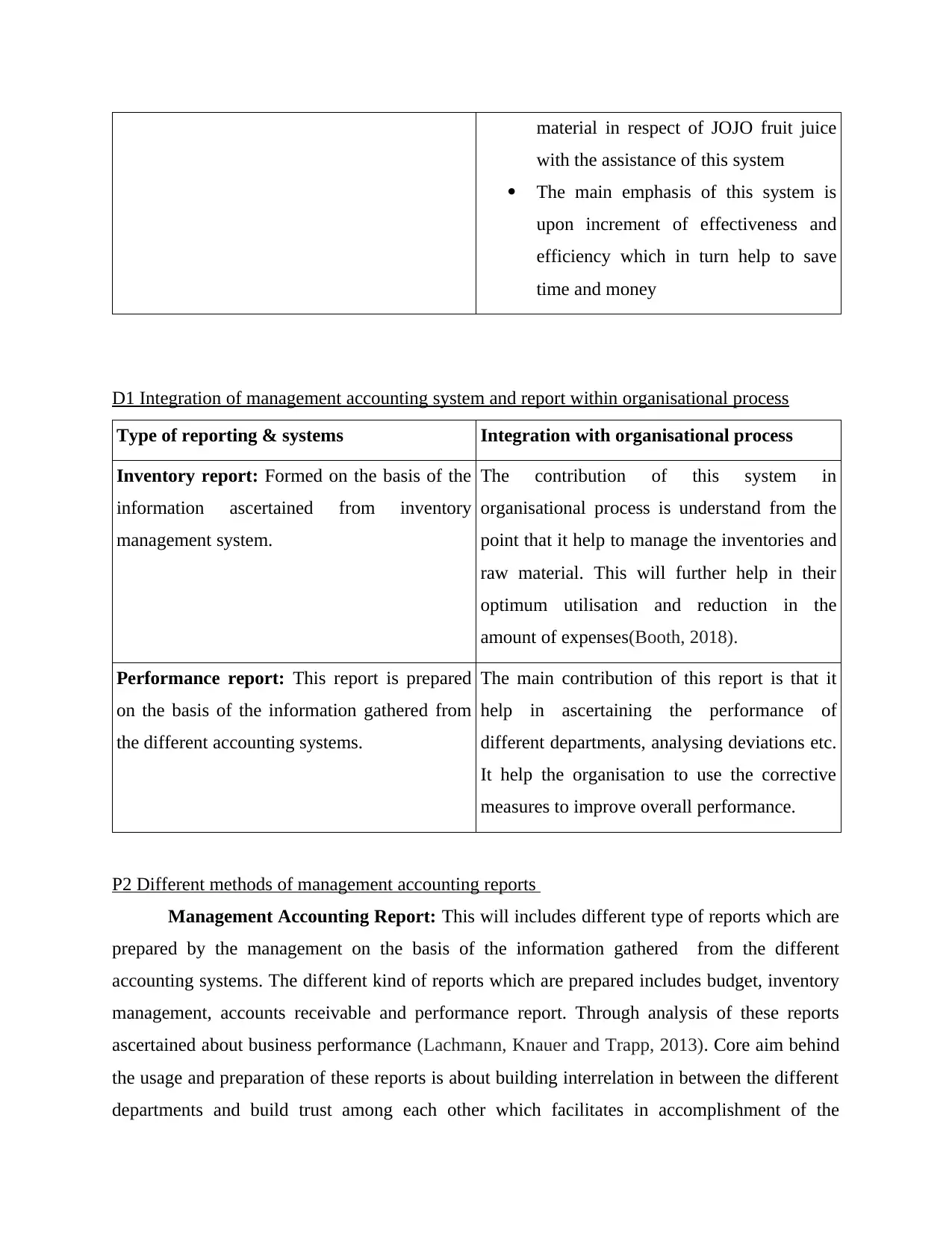

D1 Integration of management accounting system and report within organisational process

Type of reporting & systems Integration with organisational process

Inventory report: Formed on the basis of the

information ascertained from inventory

management system.

The contribution of this system in

organisational process is understand from the

point that it help to manage the inventories and

raw material. This will further help in their

optimum utilisation and reduction in the

amount of expenses(Booth, 2018).

Performance report: This report is prepared

on the basis of the information gathered from

the different accounting systems.

The main contribution of this report is that it

help in ascertaining the performance of

different departments, analysing deviations etc.

It help the organisation to use the corrective

measures to improve overall performance.

P2 Different methods of management accounting reports

Management Accounting Report: This will includes different type of reports which are

prepared by the management on the basis of the information gathered from the different

accounting systems. The different kind of reports which are prepared includes budget, inventory

management, accounts receivable and performance report. Through analysis of these reports

ascertained about business performance (Lachmann, Knauer and Trapp, 2013). Core aim behind

the usage and preparation of these reports is about building interrelation in between the different

departments and build trust among each other which facilitates in accomplishment of the

with the assistance of this system

The main emphasis of this system is

upon increment of effectiveness and

efficiency which in turn help to save

time and money

D1 Integration of management accounting system and report within organisational process

Type of reporting & systems Integration with organisational process

Inventory report: Formed on the basis of the

information ascertained from inventory

management system.

The contribution of this system in

organisational process is understand from the

point that it help to manage the inventories and

raw material. This will further help in their

optimum utilisation and reduction in the

amount of expenses(Booth, 2018).

Performance report: This report is prepared

on the basis of the information gathered from

the different accounting systems.

The main contribution of this report is that it

help in ascertaining the performance of

different departments, analysing deviations etc.

It help the organisation to use the corrective

measures to improve overall performance.

P2 Different methods of management accounting reports

Management Accounting Report: This will includes different type of reports which are

prepared by the management on the basis of the information gathered from the different

accounting systems. The different kind of reports which are prepared includes budget, inventory

management, accounts receivable and performance report. Through analysis of these reports

ascertained about business performance (Lachmann, Knauer and Trapp, 2013). Core aim behind

the usage and preparation of these reports is about building interrelation in between the different

departments and build trust among each other which facilitates in accomplishment of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

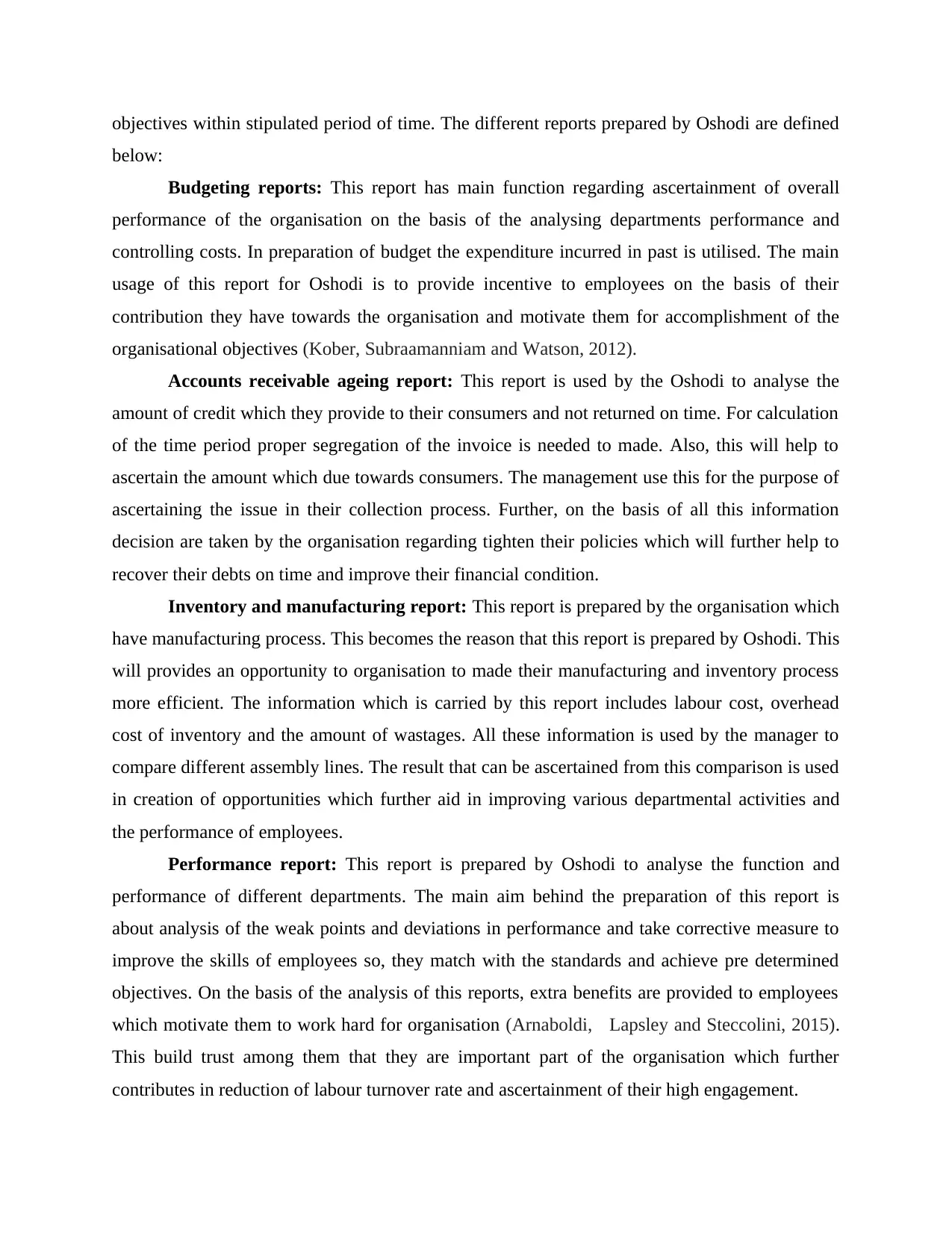

objectives within stipulated period of time. The different reports prepared by Oshodi are defined

below:

Budgeting reports: This report has main function regarding ascertainment of overall

performance of the organisation on the basis of the analysing departments performance and

controlling costs. In preparation of budget the expenditure incurred in past is utilised. The main

usage of this report for Oshodi is to provide incentive to employees on the basis of their

contribution they have towards the organisation and motivate them for accomplishment of the

organisational objectives (Kober, Subraamanniam and Watson, 2012).

Accounts receivable ageing report: This report is used by the Oshodi to analyse the

amount of credit which they provide to their consumers and not returned on time. For calculation

of the time period proper segregation of the invoice is needed to made. Also, this will help to

ascertain the amount which due towards consumers. The management use this for the purpose of

ascertaining the issue in their collection process. Further, on the basis of all this information

decision are taken by the organisation regarding tighten their policies which will further help to

recover their debts on time and improve their financial condition.

Inventory and manufacturing report: This report is prepared by the organisation which

have manufacturing process. This becomes the reason that this report is prepared by Oshodi. This

will provides an opportunity to organisation to made their manufacturing and inventory process

more efficient. The information which is carried by this report includes labour cost, overhead

cost of inventory and the amount of wastages. All these information is used by the manager to

compare different assembly lines. The result that can be ascertained from this comparison is used

in creation of opportunities which further aid in improving various departmental activities and

the performance of employees.

Performance report: This report is prepared by Oshodi to analyse the function and

performance of different departments. The main aim behind the preparation of this report is

about analysis of the weak points and deviations in performance and take corrective measure to

improve the skills of employees so, they match with the standards and achieve pre determined

objectives. On the basis of the analysis of this reports, extra benefits are provided to employees

which motivate them to work hard for organisation (Arnaboldi, Lapsley and Steccolini, 2015).

This build trust among them that they are important part of the organisation which further

contributes in reduction of labour turnover rate and ascertainment of their high engagement.

below:

Budgeting reports: This report has main function regarding ascertainment of overall

performance of the organisation on the basis of the analysing departments performance and

controlling costs. In preparation of budget the expenditure incurred in past is utilised. The main

usage of this report for Oshodi is to provide incentive to employees on the basis of their

contribution they have towards the organisation and motivate them for accomplishment of the

organisational objectives (Kober, Subraamanniam and Watson, 2012).

Accounts receivable ageing report: This report is used by the Oshodi to analyse the

amount of credit which they provide to their consumers and not returned on time. For calculation

of the time period proper segregation of the invoice is needed to made. Also, this will help to

ascertain the amount which due towards consumers. The management use this for the purpose of

ascertaining the issue in their collection process. Further, on the basis of all this information

decision are taken by the organisation regarding tighten their policies which will further help to

recover their debts on time and improve their financial condition.

Inventory and manufacturing report: This report is prepared by the organisation which

have manufacturing process. This becomes the reason that this report is prepared by Oshodi. This

will provides an opportunity to organisation to made their manufacturing and inventory process

more efficient. The information which is carried by this report includes labour cost, overhead

cost of inventory and the amount of wastages. All these information is used by the manager to

compare different assembly lines. The result that can be ascertained from this comparison is used

in creation of opportunities which further aid in improving various departmental activities and

the performance of employees.

Performance report: This report is prepared by Oshodi to analyse the function and

performance of different departments. The main aim behind the preparation of this report is

about analysis of the weak points and deviations in performance and take corrective measure to

improve the skills of employees so, they match with the standards and achieve pre determined

objectives. On the basis of the analysis of this reports, extra benefits are provided to employees

which motivate them to work hard for organisation (Arnaboldi, Lapsley and Steccolini, 2015).

This build trust among them that they are important part of the organisation which further

contributes in reduction of labour turnover rate and ascertainment of their high engagement.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

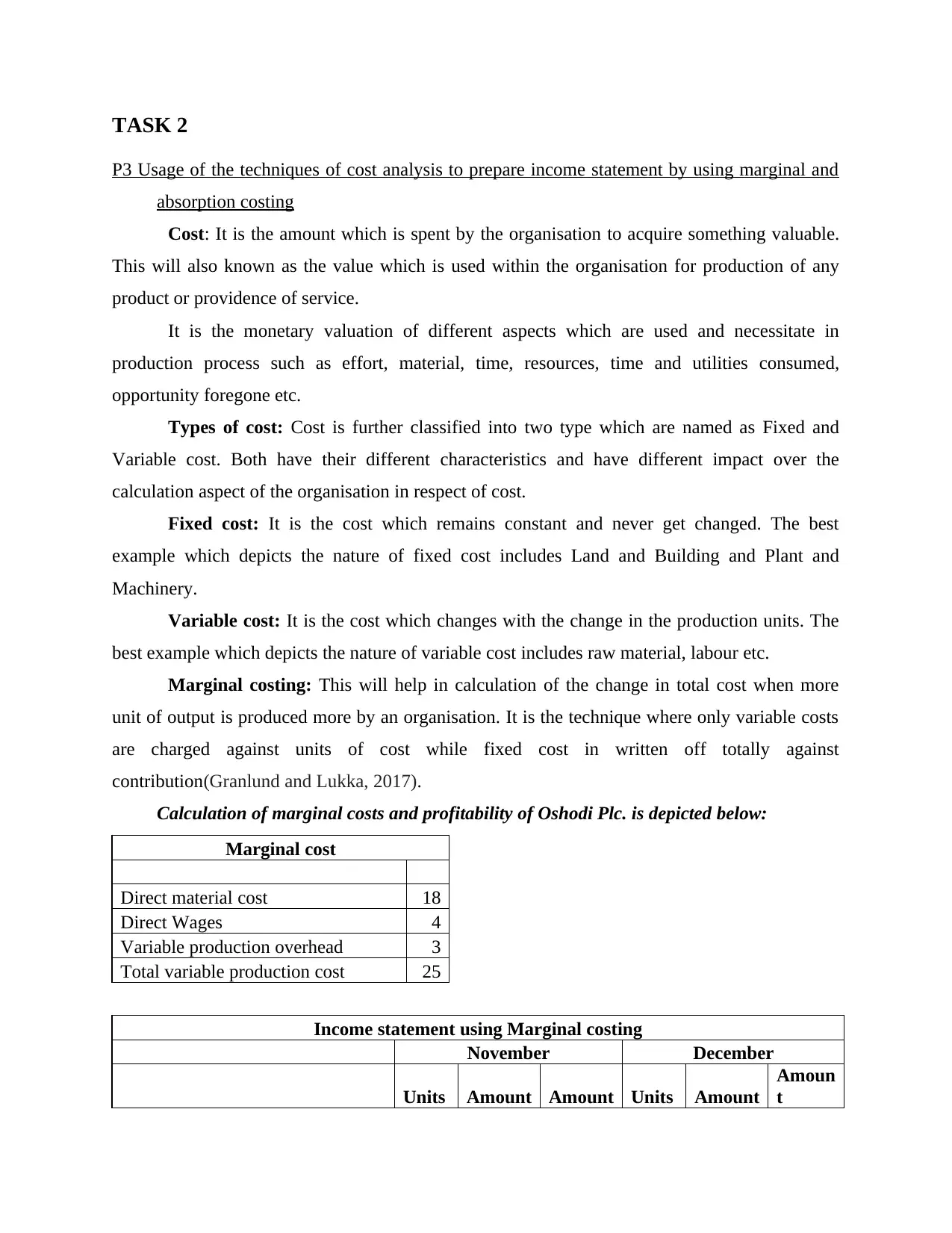

TASK 2

P3 Usage of the techniques of cost analysis to prepare income statement by using marginal and

absorption costing

Cost: It is the amount which is spent by the organisation to acquire something valuable.

This will also known as the value which is used within the organisation for production of any

product or providence of service.

It is the monetary valuation of different aspects which are used and necessitate in

production process such as effort, material, time, resources, time and utilities consumed,

opportunity foregone etc.

Types of cost: Cost is further classified into two type which are named as Fixed and

Variable cost. Both have their different characteristics and have different impact over the

calculation aspect of the organisation in respect of cost.

Fixed cost: It is the cost which remains constant and never get changed. The best

example which depicts the nature of fixed cost includes Land and Building and Plant and

Machinery.

Variable cost: It is the cost which changes with the change in the production units. The

best example which depicts the nature of variable cost includes raw material, labour etc.

Marginal costing: This will help in calculation of the change in total cost when more

unit of output is produced more by an organisation. It is the technique where only variable costs

are charged against units of cost while fixed cost in written off totally against

contribution(Granlund and Lukka, 2017).

Calculation of marginal costs and profitability of Oshodi Plc. is depicted below:

Marginal cost

Direct material cost 18

Direct Wages 4

Variable production overhead 3

Total variable production cost 25

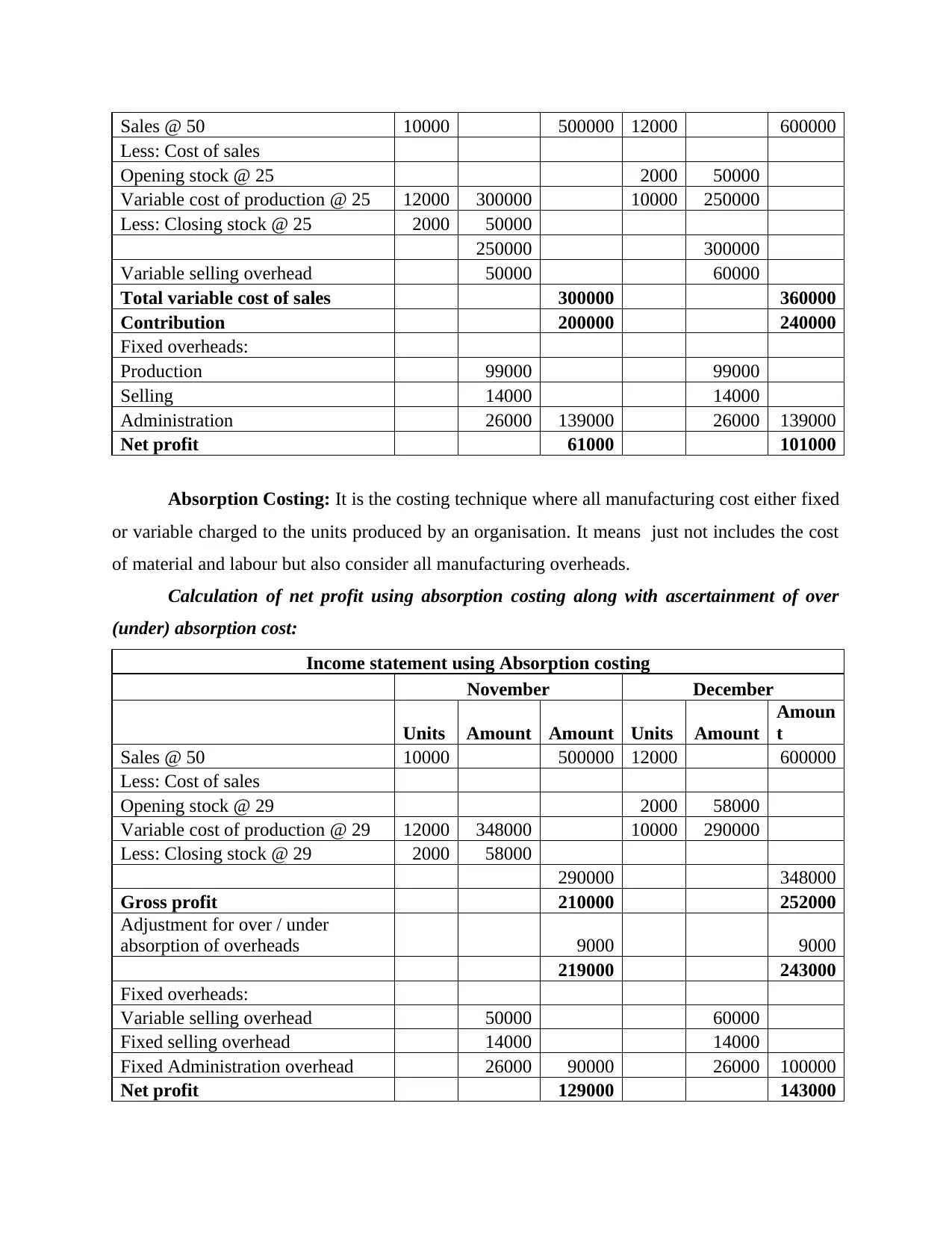

Income statement using Marginal costing

November December

Units Amount Amount Units Amount

Amoun

t

P3 Usage of the techniques of cost analysis to prepare income statement by using marginal and

absorption costing

Cost: It is the amount which is spent by the organisation to acquire something valuable.

This will also known as the value which is used within the organisation for production of any

product or providence of service.

It is the monetary valuation of different aspects which are used and necessitate in

production process such as effort, material, time, resources, time and utilities consumed,

opportunity foregone etc.

Types of cost: Cost is further classified into two type which are named as Fixed and

Variable cost. Both have their different characteristics and have different impact over the

calculation aspect of the organisation in respect of cost.

Fixed cost: It is the cost which remains constant and never get changed. The best

example which depicts the nature of fixed cost includes Land and Building and Plant and

Machinery.

Variable cost: It is the cost which changes with the change in the production units. The

best example which depicts the nature of variable cost includes raw material, labour etc.

Marginal costing: This will help in calculation of the change in total cost when more

unit of output is produced more by an organisation. It is the technique where only variable costs

are charged against units of cost while fixed cost in written off totally against

contribution(Granlund and Lukka, 2017).

Calculation of marginal costs and profitability of Oshodi Plc. is depicted below:

Marginal cost

Direct material cost 18

Direct Wages 4

Variable production overhead 3

Total variable production cost 25

Income statement using Marginal costing

November December

Units Amount Amount Units Amount

Amoun

t

Sales @ 50 10000 500000 12000 600000

Less: Cost of sales

Opening stock @ 25 2000 50000

Variable cost of production @ 25 12000 300000 10000 250000

Less: Closing stock @ 25 2000 50000

250000 300000

Variable selling overhead 50000 60000

Total variable cost of sales 300000 360000

Contribution 200000 240000

Fixed overheads:

Production 99000 99000

Selling 14000 14000

Administration 26000 139000 26000 139000

Net profit 61000 101000

Absorption Costing: It is the costing technique where all manufacturing cost either fixed

or variable charged to the units produced by an organisation. It means just not includes the cost

of material and labour but also consider all manufacturing overheads.

Calculation of net profit using absorption costing along with ascertainment of over

(under) absorption cost:

Income statement using Absorption costing

November December

Units Amount Amount Units Amount

Amoun

t

Sales @ 50 10000 500000 12000 600000

Less: Cost of sales

Opening stock @ 29 2000 58000

Variable cost of production @ 29 12000 348000 10000 290000

Less: Closing stock @ 29 2000 58000

290000 348000

Gross profit 210000 252000

Adjustment for over / under

absorption of overheads 9000 9000

219000 243000

Fixed overheads:

Variable selling overhead 50000 60000

Fixed selling overhead 14000 14000

Fixed Administration overhead 26000 90000 26000 100000

Net profit 129000 143000

Less: Cost of sales

Opening stock @ 25 2000 50000

Variable cost of production @ 25 12000 300000 10000 250000

Less: Closing stock @ 25 2000 50000

250000 300000

Variable selling overhead 50000 60000

Total variable cost of sales 300000 360000

Contribution 200000 240000

Fixed overheads:

Production 99000 99000

Selling 14000 14000

Administration 26000 139000 26000 139000

Net profit 61000 101000

Absorption Costing: It is the costing technique where all manufacturing cost either fixed

or variable charged to the units produced by an organisation. It means just not includes the cost

of material and labour but also consider all manufacturing overheads.

Calculation of net profit using absorption costing along with ascertainment of over

(under) absorption cost:

Income statement using Absorption costing

November December

Units Amount Amount Units Amount

Amoun

t

Sales @ 50 10000 500000 12000 600000

Less: Cost of sales

Opening stock @ 29 2000 58000

Variable cost of production @ 29 12000 348000 10000 290000

Less: Closing stock @ 29 2000 58000

290000 348000

Gross profit 210000 252000

Adjustment for over / under

absorption of overheads 9000 9000

219000 243000

Fixed overheads:

Variable selling overhead 50000 60000

Fixed selling overhead 14000 14000

Fixed Administration overhead 26000 90000 26000 100000

Net profit 129000 143000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

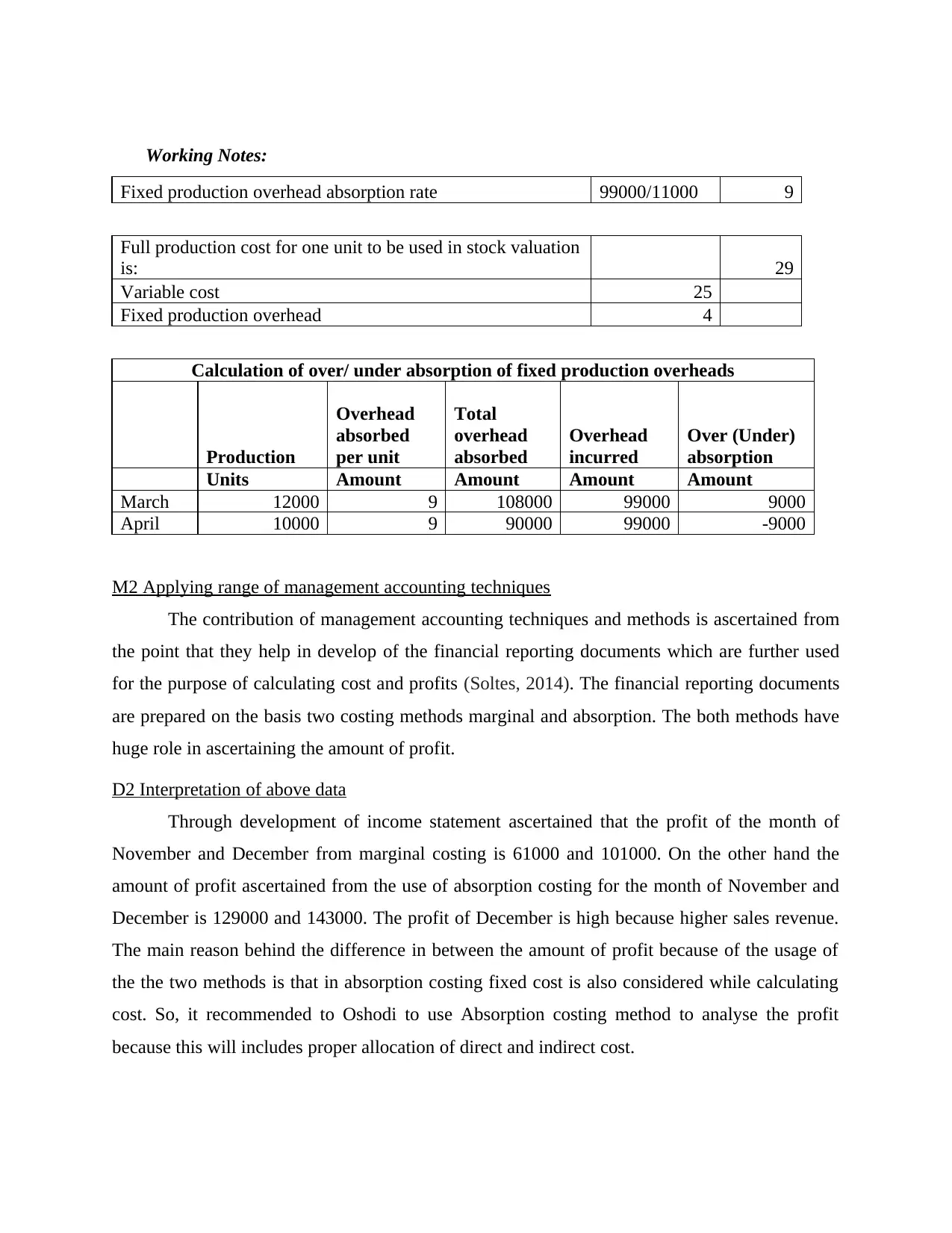

Working Notes:

Fixed production overhead absorption rate 99000/11000 9

Full production cost for one unit to be used in stock valuation

is: 29

Variable cost 25

Fixed production overhead 4

Calculation of over/ under absorption of fixed production overheads

Production

Overhead

absorbed

per unit

Total

overhead

absorbed

Overhead

incurred

Over (Under)

absorption

Units Amount Amount Amount Amount

March 12000 9 108000 99000 9000

April 10000 9 90000 99000 -9000

M2 Applying range of management accounting techniques

The contribution of management accounting techniques and methods is ascertained from

the point that they help in develop of the financial reporting documents which are further used

for the purpose of calculating cost and profits (Soltes, 2014). The financial reporting documents

are prepared on the basis two costing methods marginal and absorption. The both methods have

huge role in ascertaining the amount of profit.

D2 Interpretation of above data

Through development of income statement ascertained that the profit of the month of

November and December from marginal costing is 61000 and 101000. On the other hand the

amount of profit ascertained from the use of absorption costing for the month of November and

December is 129000 and 143000. The profit of December is high because higher sales revenue.

The main reason behind the difference in between the amount of profit because of the usage of

the the two methods is that in absorption costing fixed cost is also considered while calculating

cost. So, it recommended to Oshodi to use Absorption costing method to analyse the profit

because this will includes proper allocation of direct and indirect cost.

Fixed production overhead absorption rate 99000/11000 9

Full production cost for one unit to be used in stock valuation

is: 29

Variable cost 25

Fixed production overhead 4

Calculation of over/ under absorption of fixed production overheads

Production

Overhead

absorbed

per unit

Total

overhead

absorbed

Overhead

incurred

Over (Under)

absorption

Units Amount Amount Amount Amount

March 12000 9 108000 99000 9000

April 10000 9 90000 99000 -9000

M2 Applying range of management accounting techniques

The contribution of management accounting techniques and methods is ascertained from

the point that they help in develop of the financial reporting documents which are further used

for the purpose of calculating cost and profits (Soltes, 2014). The financial reporting documents

are prepared on the basis two costing methods marginal and absorption. The both methods have

huge role in ascertaining the amount of profit.

D2 Interpretation of above data

Through development of income statement ascertained that the profit of the month of

November and December from marginal costing is 61000 and 101000. On the other hand the

amount of profit ascertained from the use of absorption costing for the month of November and

December is 129000 and 143000. The profit of December is high because higher sales revenue.

The main reason behind the difference in between the amount of profit because of the usage of

the the two methods is that in absorption costing fixed cost is also considered while calculating

cost. So, it recommended to Oshodi to use Absorption costing method to analyse the profit

because this will includes proper allocation of direct and indirect cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

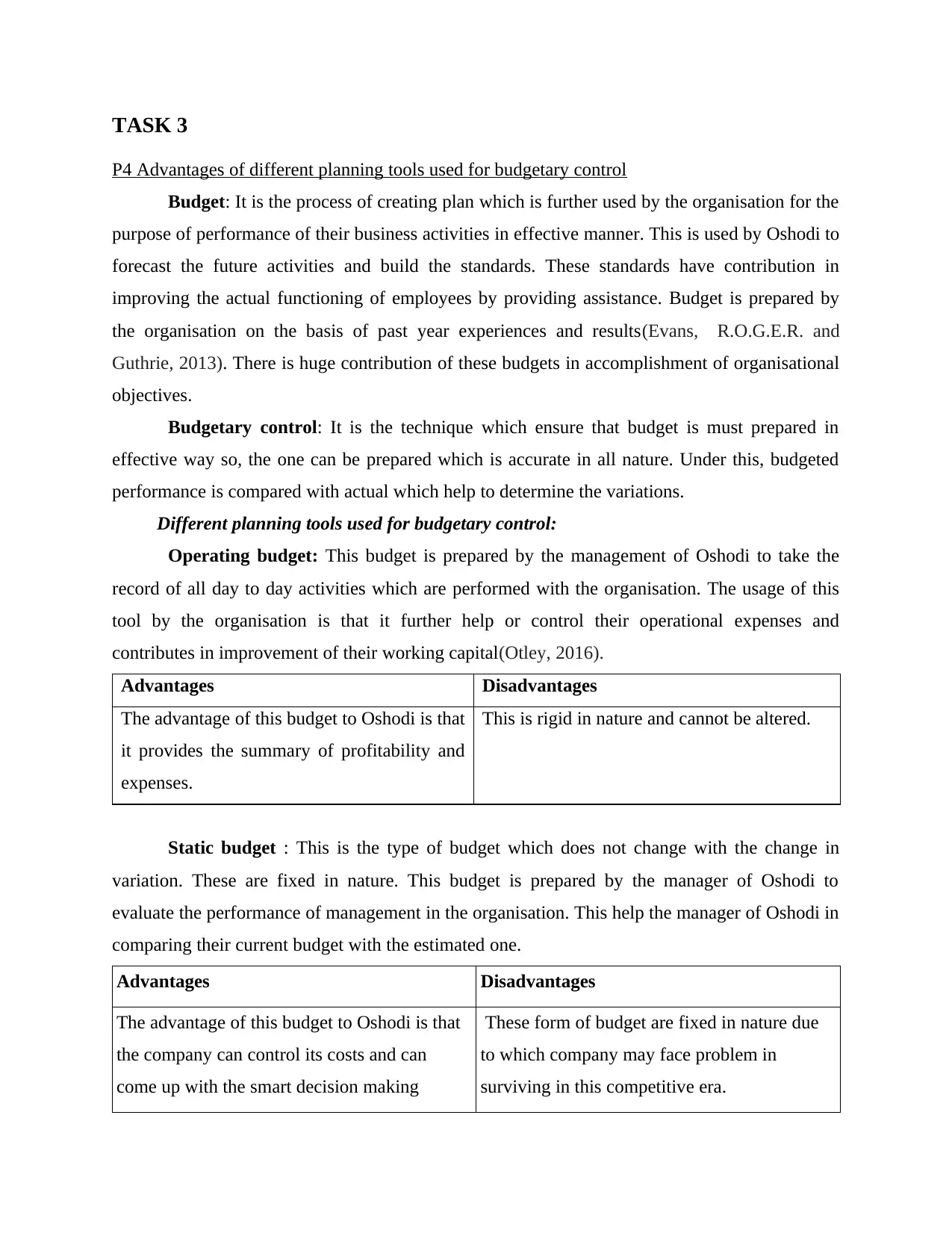

P4 Advantages of different planning tools used for budgetary control

Budget: It is the process of creating plan which is further used by the organisation for the

purpose of performance of their business activities in effective manner. This is used by Oshodi to

forecast the future activities and build the standards. These standards have contribution in

improving the actual functioning of employees by providing assistance. Budget is prepared by

the organisation on the basis of past year experiences and results(Evans, R.O.G.E.R. and

Guthrie, 2013). There is huge contribution of these budgets in accomplishment of organisational

objectives.

Budgetary control: It is the technique which ensure that budget is must prepared in

effective way so, the one can be prepared which is accurate in all nature. Under this, budgeted

performance is compared with actual which help to determine the variations.

Different planning tools used for budgetary control:

Operating budget: This budget is prepared by the management of Oshodi to take the

record of all day to day activities which are performed with the organisation. The usage of this

tool by the organisation is that it further help or control their operational expenses and

contributes in improvement of their working capital(Otley, 2016).

Advantages Disadvantages

The advantage of this budget to Oshodi is that

it provides the summary of profitability and

expenses.

This is rigid in nature and cannot be altered.

Static budget : This is the type of budget which does not change with the change in

variation. These are fixed in nature. This budget is prepared by the manager of Oshodi to

evaluate the performance of management in the organisation. This help the manager of Oshodi in

comparing their current budget with the estimated one.

Advantages Disadvantages

The advantage of this budget to Oshodi is that

the company can control its costs and can

come up with the smart decision making

These form of budget are fixed in nature due

to which company may face problem in

surviving in this competitive era.

P4 Advantages of different planning tools used for budgetary control

Budget: It is the process of creating plan which is further used by the organisation for the

purpose of performance of their business activities in effective manner. This is used by Oshodi to

forecast the future activities and build the standards. These standards have contribution in

improving the actual functioning of employees by providing assistance. Budget is prepared by

the organisation on the basis of past year experiences and results(Evans, R.O.G.E.R. and

Guthrie, 2013). There is huge contribution of these budgets in accomplishment of organisational

objectives.

Budgetary control: It is the technique which ensure that budget is must prepared in

effective way so, the one can be prepared which is accurate in all nature. Under this, budgeted

performance is compared with actual which help to determine the variations.

Different planning tools used for budgetary control:

Operating budget: This budget is prepared by the management of Oshodi to take the

record of all day to day activities which are performed with the organisation. The usage of this

tool by the organisation is that it further help or control their operational expenses and

contributes in improvement of their working capital(Otley, 2016).

Advantages Disadvantages

The advantage of this budget to Oshodi is that

it provides the summary of profitability and

expenses.

This is rigid in nature and cannot be altered.

Static budget : This is the type of budget which does not change with the change in

variation. These are fixed in nature. This budget is prepared by the manager of Oshodi to

evaluate the performance of management in the organisation. This help the manager of Oshodi in

comparing their current budget with the estimated one.

Advantages Disadvantages

The advantage of this budget to Oshodi is that

the company can control its costs and can

come up with the smart decision making

These form of budget are fixed in nature due

to which company may face problem in

surviving in this competitive era.

process.

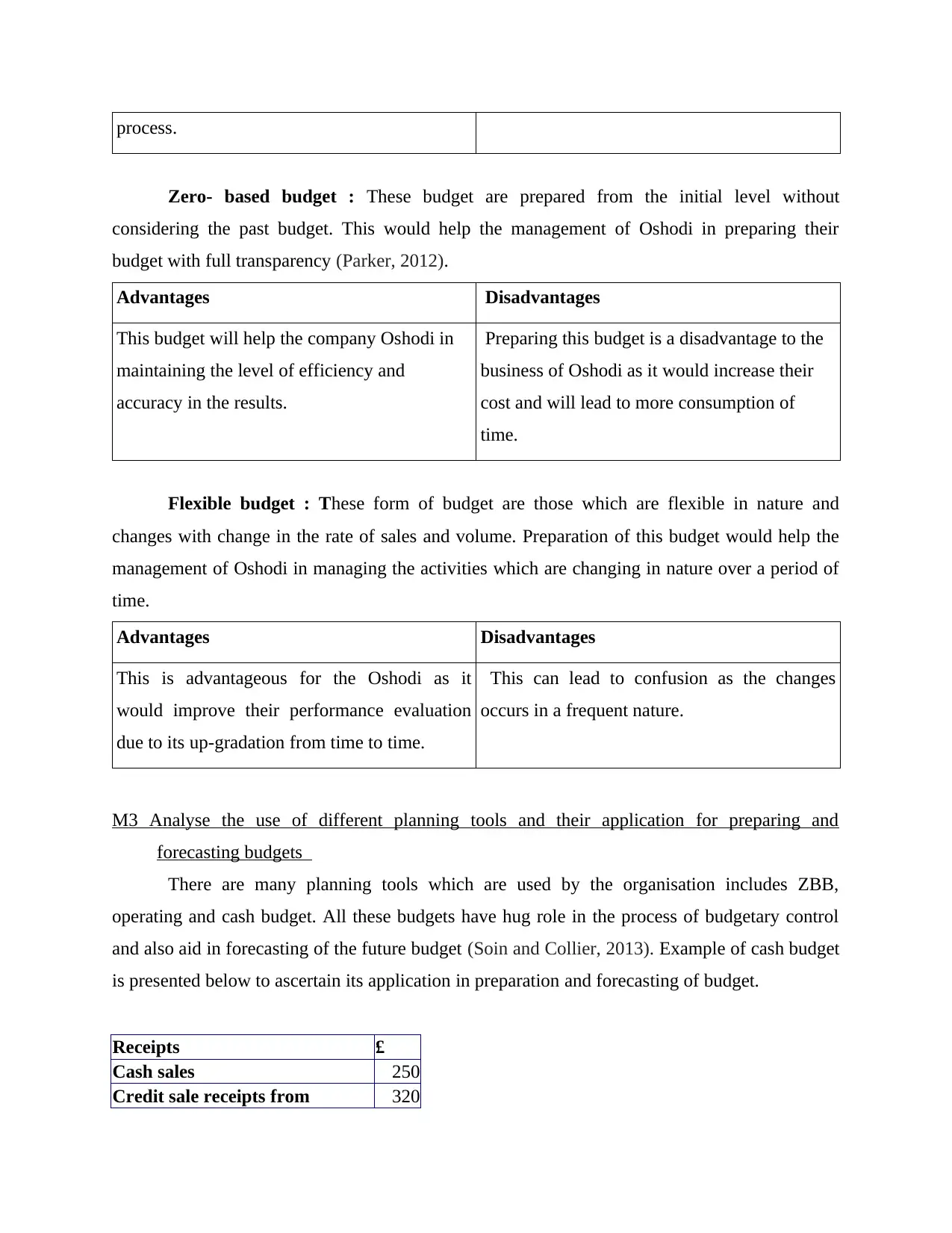

Zero- based budget : These budget are prepared from the initial level without

considering the past budget. This would help the management of Oshodi in preparing their

budget with full transparency (Parker, 2012).

Advantages Disadvantages

This budget will help the company Oshodi in

maintaining the level of efficiency and

accuracy in the results.

Preparing this budget is a disadvantage to the

business of Oshodi as it would increase their

cost and will lead to more consumption of

time.

Flexible budget : These form of budget are those which are flexible in nature and

changes with change in the rate of sales and volume. Preparation of this budget would help the

management of Oshodi in managing the activities which are changing in nature over a period of

time.

Advantages Disadvantages

This is advantageous for the Oshodi as it

would improve their performance evaluation

due to its up-gradation from time to time.

This can lead to confusion as the changes

occurs in a frequent nature.

M3 Analyse the use of different planning tools and their application for preparing and

forecasting budgets

There are many planning tools which are used by the organisation includes ZBB,

operating and cash budget. All these budgets have hug role in the process of budgetary control

and also aid in forecasting of the future budget (Soin and Collier, 2013). Example of cash budget

is presented below to ascertain its application in preparation and forecasting of budget.

Receipts £

Cash sales 250

Credit sale receipts from 320

Zero- based budget : These budget are prepared from the initial level without

considering the past budget. This would help the management of Oshodi in preparing their

budget with full transparency (Parker, 2012).

Advantages Disadvantages

This budget will help the company Oshodi in

maintaining the level of efficiency and

accuracy in the results.

Preparing this budget is a disadvantage to the

business of Oshodi as it would increase their

cost and will lead to more consumption of

time.

Flexible budget : These form of budget are those which are flexible in nature and

changes with change in the rate of sales and volume. Preparation of this budget would help the

management of Oshodi in managing the activities which are changing in nature over a period of

time.

Advantages Disadvantages

This is advantageous for the Oshodi as it

would improve their performance evaluation

due to its up-gradation from time to time.

This can lead to confusion as the changes

occurs in a frequent nature.

M3 Analyse the use of different planning tools and their application for preparing and

forecasting budgets

There are many planning tools which are used by the organisation includes ZBB,

operating and cash budget. All these budgets have hug role in the process of budgetary control

and also aid in forecasting of the future budget (Soin and Collier, 2013). Example of cash budget

is presented below to ascertain its application in preparation and forecasting of budget.

Receipts £

Cash sales 250

Credit sale receipts from 320

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

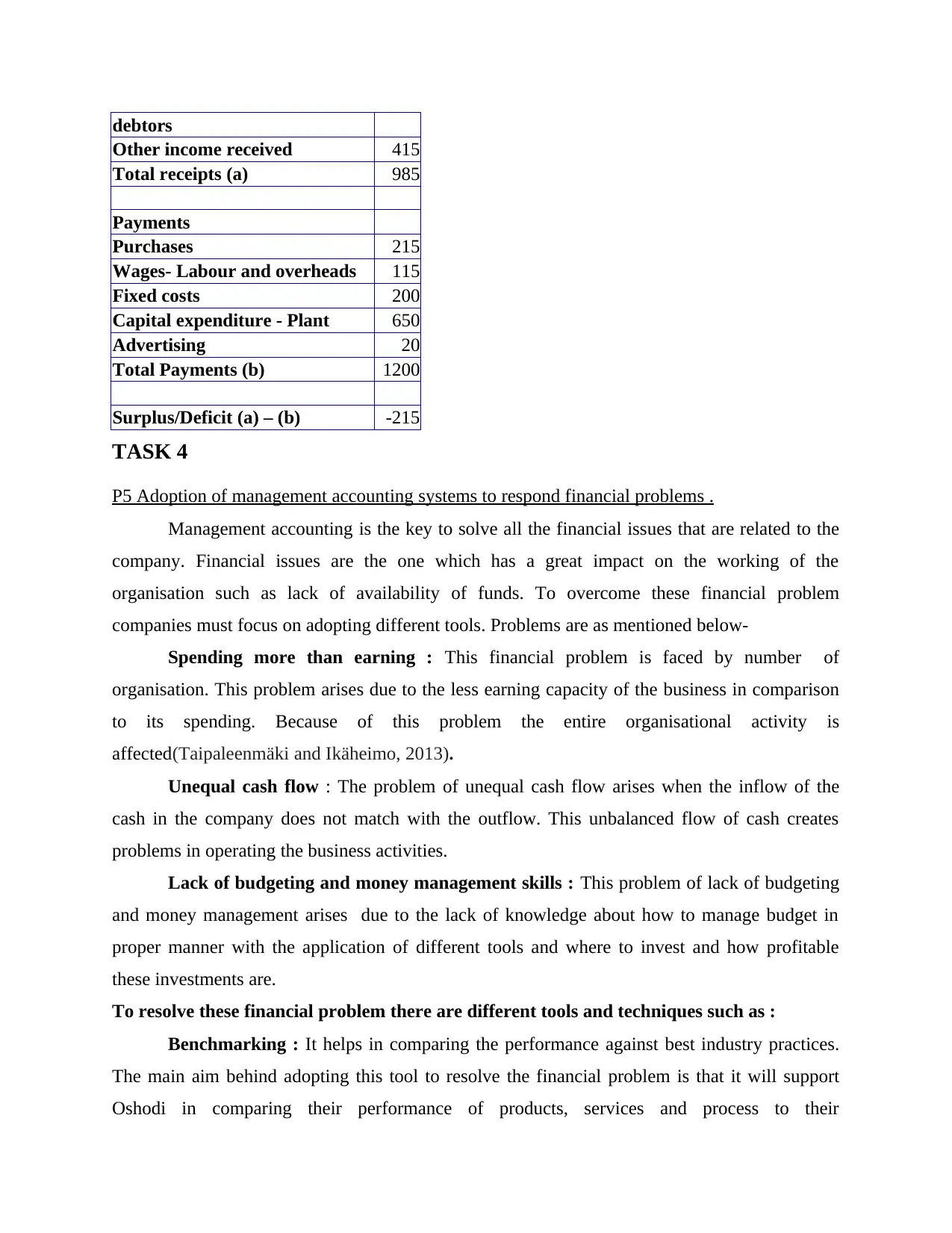

debtors

Other income received 415

Total receipts (a) 985

Payments

Purchases 215

Wages- Labour and overheads 115

Fixed costs 200

Capital expenditure - Plant 650

Advertising 20

Total Payments (b) 1200

Surplus/Deficit (a) – (b) -215

TASK 4

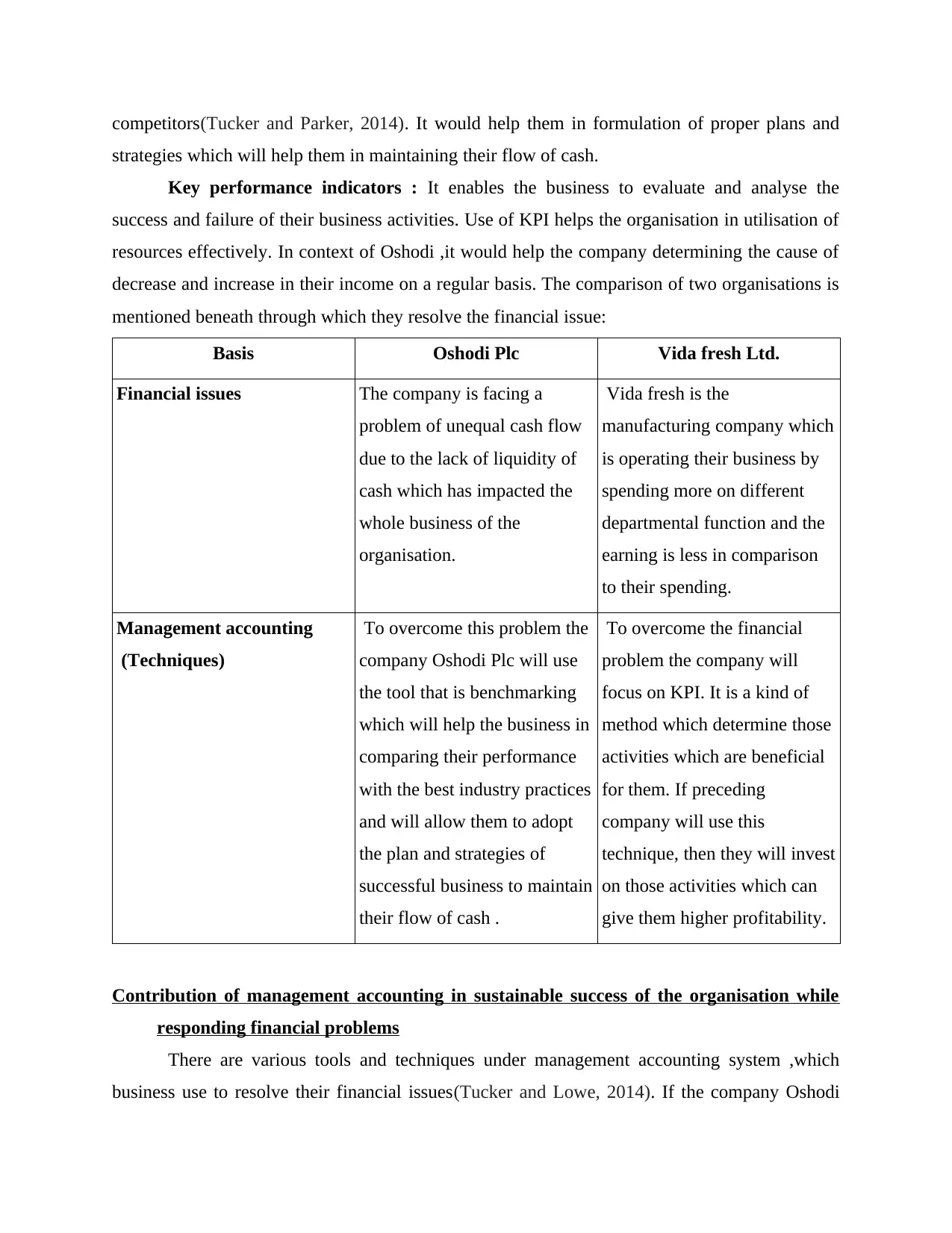

P5 Adoption of management accounting systems to respond financial problems .

Management accounting is the key to solve all the financial issues that are related to the

company. Financial issues are the one which has a great impact on the working of the

organisation such as lack of availability of funds. To overcome these financial problem

companies must focus on adopting different tools. Problems are as mentioned below-

Spending more than earning : This financial problem is faced by number of

organisation. This problem arises due to the less earning capacity of the business in comparison

to its spending. Because of this problem the entire organisational activity is

affected(Taipaleenmäki and Ikäheimo, 2013).

Unequal cash flow : The problem of unequal cash flow arises when the inflow of the

cash in the company does not match with the outflow. This unbalanced flow of cash creates

problems in operating the business activities.

Lack of budgeting and money management skills : This problem of lack of budgeting

and money management arises due to the lack of knowledge about how to manage budget in

proper manner with the application of different tools and where to invest and how profitable

these investments are.

To resolve these financial problem there are different tools and techniques such as :

Benchmarking : It helps in comparing the performance against best industry practices.

The main aim behind adopting this tool to resolve the financial problem is that it will support

Oshodi in comparing their performance of products, services and process to their

Other income received 415

Total receipts (a) 985

Payments

Purchases 215

Wages- Labour and overheads 115

Fixed costs 200

Capital expenditure - Plant 650

Advertising 20

Total Payments (b) 1200

Surplus/Deficit (a) – (b) -215

TASK 4

P5 Adoption of management accounting systems to respond financial problems .

Management accounting is the key to solve all the financial issues that are related to the

company. Financial issues are the one which has a great impact on the working of the

organisation such as lack of availability of funds. To overcome these financial problem

companies must focus on adopting different tools. Problems are as mentioned below-

Spending more than earning : This financial problem is faced by number of

organisation. This problem arises due to the less earning capacity of the business in comparison

to its spending. Because of this problem the entire organisational activity is

affected(Taipaleenmäki and Ikäheimo, 2013).

Unequal cash flow : The problem of unequal cash flow arises when the inflow of the

cash in the company does not match with the outflow. This unbalanced flow of cash creates

problems in operating the business activities.

Lack of budgeting and money management skills : This problem of lack of budgeting

and money management arises due to the lack of knowledge about how to manage budget in

proper manner with the application of different tools and where to invest and how profitable

these investments are.

To resolve these financial problem there are different tools and techniques such as :

Benchmarking : It helps in comparing the performance against best industry practices.

The main aim behind adopting this tool to resolve the financial problem is that it will support

Oshodi in comparing their performance of products, services and process to their

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

competitors(Tucker and Parker, 2014). It would help them in formulation of proper plans and

strategies which will help them in maintaining their flow of cash.

Key performance indicators : It enables the business to evaluate and analyse the

success and failure of their business activities. Use of KPI helps the organisation in utilisation of

resources effectively. In context of Oshodi ,it would help the company determining the cause of

decrease and increase in their income on a regular basis. The comparison of two organisations is

mentioned beneath through which they resolve the financial issue:

Basis Oshodi Plc Vida fresh Ltd.

Financial issues The company is facing a

problem of unequal cash flow

due to the lack of liquidity of

cash which has impacted the

whole business of the

organisation.

Vida fresh is the

manufacturing company which

is operating their business by

spending more on different

departmental function and the

earning is less in comparison

to their spending.

Management accounting

(Techniques)

To overcome this problem the

company Oshodi Plc will use

the tool that is benchmarking

which will help the business in

comparing their performance

with the best industry practices

and will allow them to adopt

the plan and strategies of

successful business to maintain

their flow of cash .

To overcome the financial

problem the company will

focus on KPI. It is a kind of

method which determine those

activities which are beneficial

for them. If preceding

company will use this

technique, then they will invest

on those activities which can

give them higher profitability.

Contribution of management accounting in sustainable success of the organisation while

responding financial problems

There are various tools and techniques under management accounting system ,which

business use to resolve their financial issues(Tucker and Lowe, 2014). If the company Oshodi

strategies which will help them in maintaining their flow of cash.

Key performance indicators : It enables the business to evaluate and analyse the

success and failure of their business activities. Use of KPI helps the organisation in utilisation of

resources effectively. In context of Oshodi ,it would help the company determining the cause of

decrease and increase in their income on a regular basis. The comparison of two organisations is

mentioned beneath through which they resolve the financial issue:

Basis Oshodi Plc Vida fresh Ltd.

Financial issues The company is facing a

problem of unequal cash flow

due to the lack of liquidity of

cash which has impacted the

whole business of the

organisation.

Vida fresh is the

manufacturing company which

is operating their business by

spending more on different

departmental function and the

earning is less in comparison

to their spending.

Management accounting

(Techniques)

To overcome this problem the

company Oshodi Plc will use

the tool that is benchmarking

which will help the business in

comparing their performance

with the best industry practices

and will allow them to adopt

the plan and strategies of

successful business to maintain

their flow of cash .

To overcome the financial

problem the company will

focus on KPI. It is a kind of

method which determine those

activities which are beneficial

for them. If preceding

company will use this

technique, then they will invest

on those activities which can

give them higher profitability.

Contribution of management accounting in sustainable success of the organisation while

responding financial problems

There are various tools and techniques under management accounting system ,which

business use to resolve their financial issues(Tucker and Lowe, 2014). If the company Oshodi

uses the technique of benchmarking to solve their financial problem as it will help them in the

comparison of their performance with the best industry practices which will automatically lead to

the stage of sustainable success of their organisation. As benchmarking is a key tool for

sustaining of business.

D3 Application of planning tools to respond financial issue along with attainment of sustainable

success

Planning tools plays a crucial role in over coming the financial issues. In the company

like Oshodi they have considered on the use of different tools of planning such as operating

budget, zero based budget, flexible budget and static budget(Zoni, Dossi and Morelli, 2012).

These tools helps the business in overcoming the financial issues. In time, financial issues are

being solved with the coordination of planning tools and management accounting system. Like in

the above mentioned company, they use various kind of tools and accounting systems.

CONCLUSION

From the above mentioned information it has been concluded that management

accounting also called managerial accounting and can be determined as an effective process of

giving financial data and resources to the administrators in decision making. There are different

kind of management accounting such as cost accounting, inventory management system, price

optimisation system etc. all these are important for the success and growth of an organisation.

Accurate preparation of various type of reports support to circulate relevant data to internal

stakeholders as well as managers which enhances decision making and also support to acquire

desired results within given time duration. Along with this, different techniques of cost analysis

have been used by an organisation which will help them in accurate preparation of its income

statement. Cash budget and ZBB is types of planning tools which have been followed to identify

inflow and outflow of cash. KPI and Benchmarking are introduces most effective system and

tools of management which will help an organisation in solving its financial problems effectively

and systematically.

comparison of their performance with the best industry practices which will automatically lead to

the stage of sustainable success of their organisation. As benchmarking is a key tool for

sustaining of business.

D3 Application of planning tools to respond financial issue along with attainment of sustainable

success

Planning tools plays a crucial role in over coming the financial issues. In the company

like Oshodi they have considered on the use of different tools of planning such as operating

budget, zero based budget, flexible budget and static budget(Zoni, Dossi and Morelli, 2012).

These tools helps the business in overcoming the financial issues. In time, financial issues are

being solved with the coordination of planning tools and management accounting system. Like in

the above mentioned company, they use various kind of tools and accounting systems.

CONCLUSION

From the above mentioned information it has been concluded that management

accounting also called managerial accounting and can be determined as an effective process of

giving financial data and resources to the administrators in decision making. There are different

kind of management accounting such as cost accounting, inventory management system, price

optimisation system etc. all these are important for the success and growth of an organisation.

Accurate preparation of various type of reports support to circulate relevant data to internal

stakeholders as well as managers which enhances decision making and also support to acquire

desired results within given time duration. Along with this, different techniques of cost analysis

have been used by an organisation which will help them in accurate preparation of its income

statement. Cash budget and ZBB is types of planning tools which have been followed to identify

inflow and outflow of cash. KPI and Benchmarking are introduces most effective system and

tools of management which will help an organisation in solving its financial problems effectively

and systematically.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and journal:

Zoni, L., Dossi, A. and Morelli, M., 2012. Management accounting system (MAS) change: field

evidence. Asia-Pacific Journal of Accounting & Economics. 19(1). pp.119-138.

Bryer, R., 2013. Americanism and financial accounting theory–Part 2: The ‘modern business

enterprise’, America's transition to capitalism, and the genesis of management

accounting. Critical Perspectives on Accounting. 24(4-5). pp.273-318.

Grabner, I. and Moers, F., 2013. Management control as a system or a package? Conceptual and

empirical issues. Accounting, Organizations and Society. 38(6-7). pp.407-419.

Lee, B., 2012. New public management, accounting, regulators and moral panics. International

Journal of Public Sector Management. 25(3). pp.192-202.

Morden, T., 2016. Principles of strategic management. Routledge.

Booth, P., 2018. Management control in a voluntary organization: accounting and accountants

in organizational context. Routledge.

Lachmann, M., Knauer, T. and Trapp, R., 2013. Strategic management accounting practices in

hospitals: Empirical evidence on their dissemination under competitive market

environments. Journal of Accounting & Organizational Change. 9(3). pp.336-369.

Kober, R., Subraamanniam, T. and Watson, J., 2012. The impact of total quality management

adoption on small and medium enterprises’ financial performance. Accounting &

Finance. 52(2). pp.421-438.

Arnaboldi, M., Lapsley, I. and Steccolini, I., 2015. Performance management in the public

sector: The ultimate challenge. Financial Accountability & Management. 31(1). pp.1-

22.

Granlund, M. and Lukka, K., 2017. Investigating highly established research paradigms:

Reviving contextuality in contingency theory based management accounting research.

Critical Perspectives on Accounting. 45. pp.63-80.

Soltes, E., 2014. Private interaction between firm management and sell‐side analysts. Journal of

Accounting Research. 52(1). pp.245-272.

Books and journal:

Zoni, L., Dossi, A. and Morelli, M., 2012. Management accounting system (MAS) change: field

evidence. Asia-Pacific Journal of Accounting & Economics. 19(1). pp.119-138.

Bryer, R., 2013. Americanism and financial accounting theory–Part 2: The ‘modern business

enterprise’, America's transition to capitalism, and the genesis of management

accounting. Critical Perspectives on Accounting. 24(4-5). pp.273-318.

Grabner, I. and Moers, F., 2013. Management control as a system or a package? Conceptual and

empirical issues. Accounting, Organizations and Society. 38(6-7). pp.407-419.

Lee, B., 2012. New public management, accounting, regulators and moral panics. International

Journal of Public Sector Management. 25(3). pp.192-202.

Morden, T., 2016. Principles of strategic management. Routledge.

Booth, P., 2018. Management control in a voluntary organization: accounting and accountants

in organizational context. Routledge.

Lachmann, M., Knauer, T. and Trapp, R., 2013. Strategic management accounting practices in

hospitals: Empirical evidence on their dissemination under competitive market

environments. Journal of Accounting & Organizational Change. 9(3). pp.336-369.

Kober, R., Subraamanniam, T. and Watson, J., 2012. The impact of total quality management

adoption on small and medium enterprises’ financial performance. Accounting &

Finance. 52(2). pp.421-438.

Arnaboldi, M., Lapsley, I. and Steccolini, I., 2015. Performance management in the public

sector: The ultimate challenge. Financial Accountability & Management. 31(1). pp.1-

22.

Granlund, M. and Lukka, K., 2017. Investigating highly established research paradigms:

Reviving contextuality in contingency theory based management accounting research.

Critical Perspectives on Accounting. 45. pp.63-80.

Soltes, E., 2014. Private interaction between firm management and sell‐side analysts. Journal of

Accounting Research. 52(1). pp.245-272.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Evans, E .E., Burritt, R.O.G.E.R. and Guthrie, J., 2013. The virtual university: impact on

Australian accounting and business education.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–2014.

Management accounting research. 31. pp.45-62.

Parker, L. D., 2012. Qualitative management accounting research: Assessing deliverables and

relevance. Critical perspectives on accounting. 23(1). pp.54-70.

Soin, K. and Collier, P., 2013. Risk and risk management in management accounting and control.

Taipaleenmäki, J. and Ikäheimo, S., 2013. On the convergence of management accounting and

financial accounting–the role of information technology in accounting change.

International Journal of Accounting Information Systems. 14(4). pp.321-348.

Tucker, B. and Parker, L., 2014. In our ivory towers? The research-practice gap in management

accounting. Accounting and Business Research. 44(2). pp.104-143.

Tucker, B. P. and Lowe, A. D., 2014. Practitioners are from Mars; academics are from Venus?:

An investigation of the research-practice gap in management accounting. Accounting,

Auditing & Accountability Journal. 27(3). pp.394-425.

Australian accounting and business education.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–2014.

Management accounting research. 31. pp.45-62.

Parker, L. D., 2012. Qualitative management accounting research: Assessing deliverables and

relevance. Critical perspectives on accounting. 23(1). pp.54-70.

Soin, K. and Collier, P., 2013. Risk and risk management in management accounting and control.

Taipaleenmäki, J. and Ikäheimo, S., 2013. On the convergence of management accounting and

financial accounting–the role of information technology in accounting change.

International Journal of Accounting Information Systems. 14(4). pp.321-348.

Tucker, B. and Parker, L., 2014. In our ivory towers? The research-practice gap in management

accounting. Accounting and Business Research. 44(2). pp.104-143.

Tucker, B. P. and Lowe, A. D., 2014. Practitioners are from Mars; academics are from Venus?:

An investigation of the research-practice gap in management accounting. Accounting,

Auditing & Accountability Journal. 27(3). pp.394-425.

1 out of 17