Management Accounting in Flying Airlines Company

Added on 2020-05-16

8 Pages1727 Words81 Views

MANAGEMENT ACCOUNTING

Situation 1.The flying airlines company has two options- either it can replace the loader truck with the conveyor belt now or it can wait for an year to replace the same.The airlines can take the decision based on two things. The first option is to look on the cash flows of the company ignoring the depreciation tax shield and the other is to take a decision keeping in mind the depreciation tax shield. (Chandra, 2014)Option 1: Cash flows in both the cases ignoring the depreciation tax shieldIf the Airlines company takes the decision to replace the loader now then it will have a net cash outflow of $75000. As we know that the total cash outflow ( annual variable operating cost) will be $80000 whereas the cash inflow i.e. the amount received on selling the loader is $5000. So, we can conclude that the net cash outflow if the company takes the decision of replacing the loader by conveyor belt now will be $75000. In the second case, the operations manager is thinking of replacing the loader next year. His decision will be finalised only after comparing it with the other option. So, he calculates the total cash outslow for this situation as well. The total amount of money spent will include the cost of purchasing the conveyor belt i.e., $20000 along with the annual variable operating cost i.e., $50000. Therefore, total cash outflow will be $70000.The airline company should buy the conveyor belt now itself rather than to wait for one more year because this will help them to save $(75000-70000) = $ 5000 this year.Option 2 : Cash flows assuming that there is a depreciation tax shieldWe all know that depreciation is a non cash item that is reflected as an expense in the profit and loss account. However, depreciation also provides as a tax shield. We consider money saved to be money earned and so it will affect the cash flows of the company. Let us see the impact of this tax shield on both the situations. (Shah, 2009)In the first situation, the annual depreciation is $25000. Assuming the tax rate to be 30%, we can say that the tax saving is $25000*30*= $7500. Therefore, the net cash flow in the first situation is $(80000-5000-7500) =$ 67500.In the second situation, tax saved = $(20000*30%) =$6000. Therefore the total cash outflow of the Airlines company would be $(20000+50000-6000) = $64000.Therefore, the cash outflow is less when the company chooses to purchase a new conveyor belt without waiting for one year based on both the options.

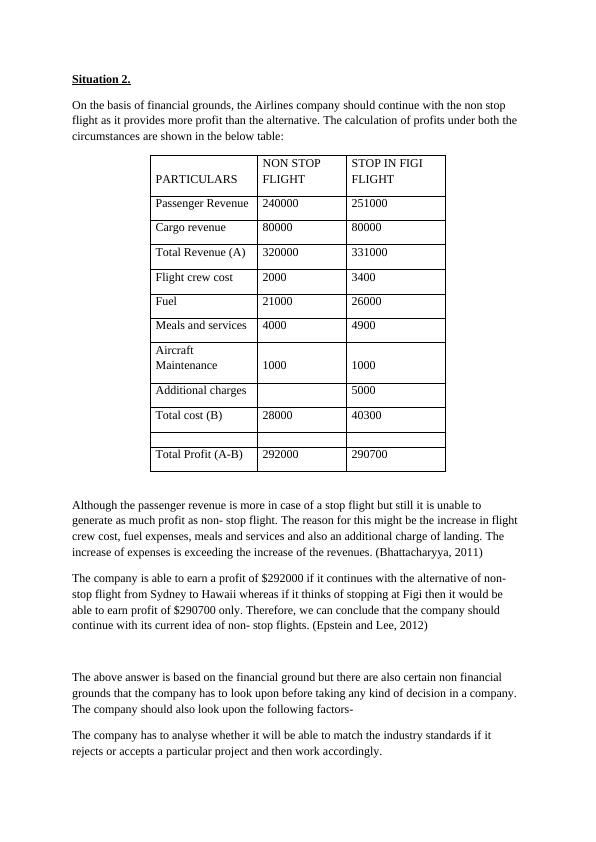

Situation 2.On the basis of financial grounds, the Airlines company should continue with the non stop flight as it provides more profit than the alternative. The calculation of profits under both the circumstances are shown in the below table:PARTICULARSNON STOP FLIGHTSTOP IN FIGI FLIGHTPassenger Revenue240000251000Cargo revenue8000080000Total Revenue (A)320000331000Flight crew cost20003400Fuel2100026000Meals and services40004900Aircraft Maintenance10001000Additional charges5000Total cost (B)2800040300Total Profit (A-B)292000290700Although the passenger revenue is more in case of a stop flight but still it is unable to generate as much profit as non- stop flight. The reason for this might be the increase in flight crew cost, fuel expenses, meals and services and also an additional charge of landing. The increase of expenses is exceeding the increase of the revenues. (Bhattacharyya, 2011)The company is able to earn a profit of $292000 if it continues with the alternative of non- stop flight from Sydney to Hawaii whereas if it thinks of stopping at Figi then it would be able to earn profit of $290700 only. Therefore, we can conclude that the company should continue with its current idea of non- stop flights. (Epstein and Lee, 2012)The above answer is based on the financial ground but there are also certain non financial grounds that the company has to look upon before taking any kind of decision in a company. The company should also look upon the following factors-The company has to analyse whether it will be able to match the industry standards if it rejects or accepts a particular project and then work accordingly.

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Management Accounting Assignment | Airline Companylg...

|8

|1160

|84

(solution) Management Accounting : Doclg...

|11

|1883

|68

Management Accounting Assignment( MA )lg...

|9

|1321

|151

Assignment on Management Accounting Samplelg...

|7

|1218

|45

Managerial Finance Assignment 2022lg...

|10

|1671

|21