Management Accounting for Cost & Control

VerifiedAdded on 2023/06/14

|18

|3573

|330

AI Summary

This article discusses the concept of Panopticism, major functions of management accounting, the use of checklist in control activities, and more. It also includes manufacturing and income statements, journal entries, and calculations for payroll accrual. Subject: Management Accounting, Course Code: N/A, Course Name: N/A, College/University: N/A

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGEMENT ACCOUNTING FOR COST & CONTROL

Management Accounting for Cost & Control

Name of the Student:

Name of the University:

Author’s Note:

Management Accounting for Cost & Control

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Table of Contents

Answer to Question No 1................................................................................................................3

Answer to Question No 2................................................................................................................3

Answer to Question No 3................................................................................................................4

Answer to Question No 4:...............................................................................................................6

Normal View:..............................................................................................................................6

Manufacturing Statement:.......................................................................................................6

Income Statement:...................................................................................................................7

Formula View:.............................................................................................................................8

Manufacturing Statement:.......................................................................................................8

Income Statement:...................................................................................................................9

Answer to Question No 5..............................................................................................................10

Answer to Question No 6:.............................................................................................................10

Answer to Question No 7:.............................................................................................................11

Answer to Question No 8:.............................................................................................................11

Requirement a:...........................................................................................................................11

Requirement b:...........................................................................................................................11

Requirement c:...........................................................................................................................12

Answer to Question No 9:.............................................................................................................13

Answer to Question 10:.................................................................................................................15

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Table of Contents

Answer to Question No 1................................................................................................................3

Answer to Question No 2................................................................................................................3

Answer to Question No 3................................................................................................................4

Answer to Question No 4:...............................................................................................................6

Normal View:..............................................................................................................................6

Manufacturing Statement:.......................................................................................................6

Income Statement:...................................................................................................................7

Formula View:.............................................................................................................................8

Manufacturing Statement:.......................................................................................................8

Income Statement:...................................................................................................................9

Answer to Question No 5..............................................................................................................10

Answer to Question No 6:.............................................................................................................10

Answer to Question No 7:.............................................................................................................11

Answer to Question No 8:.............................................................................................................11

Requirement a:...........................................................................................................................11

Requirement b:...........................................................................................................................11

Requirement c:...........................................................................................................................12

Answer to Question No 9:.............................................................................................................13

Answer to Question 10:.................................................................................................................15

2

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Direct Method:...........................................................................................................................15

Step Method:..............................................................................................................................15

Reciprocal Method:...................................................................................................................15

Reference List................................................................................................................................17

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Direct Method:...........................................................................................................................15

Step Method:..............................................................................................................................15

Reciprocal Method:...................................................................................................................15

Reference List................................................................................................................................17

3

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Answer to Question No 1

Panopticism is a socio-theoretical and communal framework which was introduced by

Michel Foucault, a French philosopher. The framework was named after Panopticon which is a

model for external surveillance (Gane, 2012). Panopticon refers to the external laboratory of

power with the application of which attitude and behaviour of individuals can be modified for

the better and is considered to be a disciplinary course of action which involves surveillance. It is

a course of disciplinary action which is used in case of prisons in order to implement discipline

as a tool of authority. It is used for observation of prisoners and it is used as a source of data.

For example, the concept of panopticon can be used effectively for the purpose of

surveillance which is a very much significant with the introduction and overall development of

technology. The observable data which can be collected with the various data mining techniques

and such data can be made available to the individuals and companies for the purpose of

surveillance of data.

The use of Panopticism is very useful in management accounting as it can be used to

keep track of every transactions and at the same time ensure that there are no mistakes or errors

in such transactions (King, 2012). Even if there are certain mistakes in the process of accounting

the same can be rectified and ensure that the accounting process remains authentic.

Answer to Question No 2

The major functions of management accounting are given below in details:

1. Planning: The method of planning is sued by the management to make short term and

long-term plans for attaining a particular goal or objective of business. The management

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Answer to Question No 1

Panopticism is a socio-theoretical and communal framework which was introduced by

Michel Foucault, a French philosopher. The framework was named after Panopticon which is a

model for external surveillance (Gane, 2012). Panopticon refers to the external laboratory of

power with the application of which attitude and behaviour of individuals can be modified for

the better and is considered to be a disciplinary course of action which involves surveillance. It is

a course of disciplinary action which is used in case of prisons in order to implement discipline

as a tool of authority. It is used for observation of prisoners and it is used as a source of data.

For example, the concept of panopticon can be used effectively for the purpose of

surveillance which is a very much significant with the introduction and overall development of

technology. The observable data which can be collected with the various data mining techniques

and such data can be made available to the individuals and companies for the purpose of

surveillance of data.

The use of Panopticism is very useful in management accounting as it can be used to

keep track of every transactions and at the same time ensure that there are no mistakes or errors

in such transactions (King, 2012). Even if there are certain mistakes in the process of accounting

the same can be rectified and ensure that the accounting process remains authentic.

Answer to Question No 2

The major functions of management accounting are given below in details:

1. Planning: The method of planning is sued by the management to make short term and

long-term plans for attaining a particular goal or objective of business. The management

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

MANAGEMENT ACCOUNTING FOR COST & CONTROL

of the company is responsible for the planning process and also for the various important

decisions which are to be taken by the business regarding various aspects such as

allocation of funds, financing decision and other similar decisions. Generally, the most

important tool which is used for the purpose of planning is budgeting (Chadwick, 2013).

For example, the management accounting method employs the use of budget for planning

process which is useful for deciding the targets and also measure the performance of the

company. in addition to this, the budget is useful for planning for allocation of resources.

2. Organising: The method is used to establish the business model of the company as well

assigning the different part of the plans to the various departments in pursuance of the

objectives and goals of the business (Biege, Lay & Buschak, 2012). The managers of the

companies are responsible to organise the process with the use of management

accounting so that different departmental performance can be measured effectively. For

example, the statements which are prepared by the management with the application of

management accounting can be used to make decisions regarding operations, product and

similar other decisions.

3. Controlling: This is one of the functions of management accounting which is used for

evaluation, reviewing and correcting the results of the business. The process of

controlling is executed with the use of various performance reports which is used to

measure the performance of the business on the basis of standards set by the business

(Zubakov & Mustafin, 2015).

Answer to Question No 3

Rock band Van Halen has used the checklist in the process of control. In the case of

rocker David Lee Roth who made an agreement with the rock band Van Halen. The application

MANAGEMENT ACCOUNTING FOR COST & CONTROL

of the company is responsible for the planning process and also for the various important

decisions which are to be taken by the business regarding various aspects such as

allocation of funds, financing decision and other similar decisions. Generally, the most

important tool which is used for the purpose of planning is budgeting (Chadwick, 2013).

For example, the management accounting method employs the use of budget for planning

process which is useful for deciding the targets and also measure the performance of the

company. in addition to this, the budget is useful for planning for allocation of resources.

2. Organising: The method is used to establish the business model of the company as well

assigning the different part of the plans to the various departments in pursuance of the

objectives and goals of the business (Biege, Lay & Buschak, 2012). The managers of the

companies are responsible to organise the process with the use of management

accounting so that different departmental performance can be measured effectively. For

example, the statements which are prepared by the management with the application of

management accounting can be used to make decisions regarding operations, product and

similar other decisions.

3. Controlling: This is one of the functions of management accounting which is used for

evaluation, reviewing and correcting the results of the business. The process of

controlling is executed with the use of various performance reports which is used to

measure the performance of the business on the basis of standards set by the business

(Zubakov & Mustafin, 2015).

Answer to Question No 3

Rock band Van Halen has used the checklist in the process of control. In the case of

rocker David Lee Roth who made an agreement with the rock band Van Halen. The application

5

MANAGEMENT ACCOUNTING FOR COST & CONTROL

of checklist by the business is an effective measure for the control activities of the business. The

application of checklist allowed the band to properly plan and implement the plans of the band.

Moreover, it is useful in the effective maintenance of the resources. The rock band needs to carry

the checklist in order to ensure that every resource such as instruments which are used for the

performance is carried from one place to another. A checklist can also be used by the band to

prepare a schedule for the performance of the band in different destination. In this way the band

can make use of the checklist for the effective performance measurement and scheduling of the

band.

MANAGEMENT ACCOUNTING FOR COST & CONTROL

of checklist by the business is an effective measure for the control activities of the business. The

application of checklist allowed the band to properly plan and implement the plans of the band.

Moreover, it is useful in the effective maintenance of the resources. The rock band needs to carry

the checklist in order to ensure that every resource such as instruments which are used for the

performance is carried from one place to another. A checklist can also be used by the band to

prepare a schedule for the performance of the band in different destination. In this way the band

can make use of the checklist for the effective performance measurement and scheduling of the

band.

6

MANAGEMENT ACCOUNTING FOR COST & CONTROL

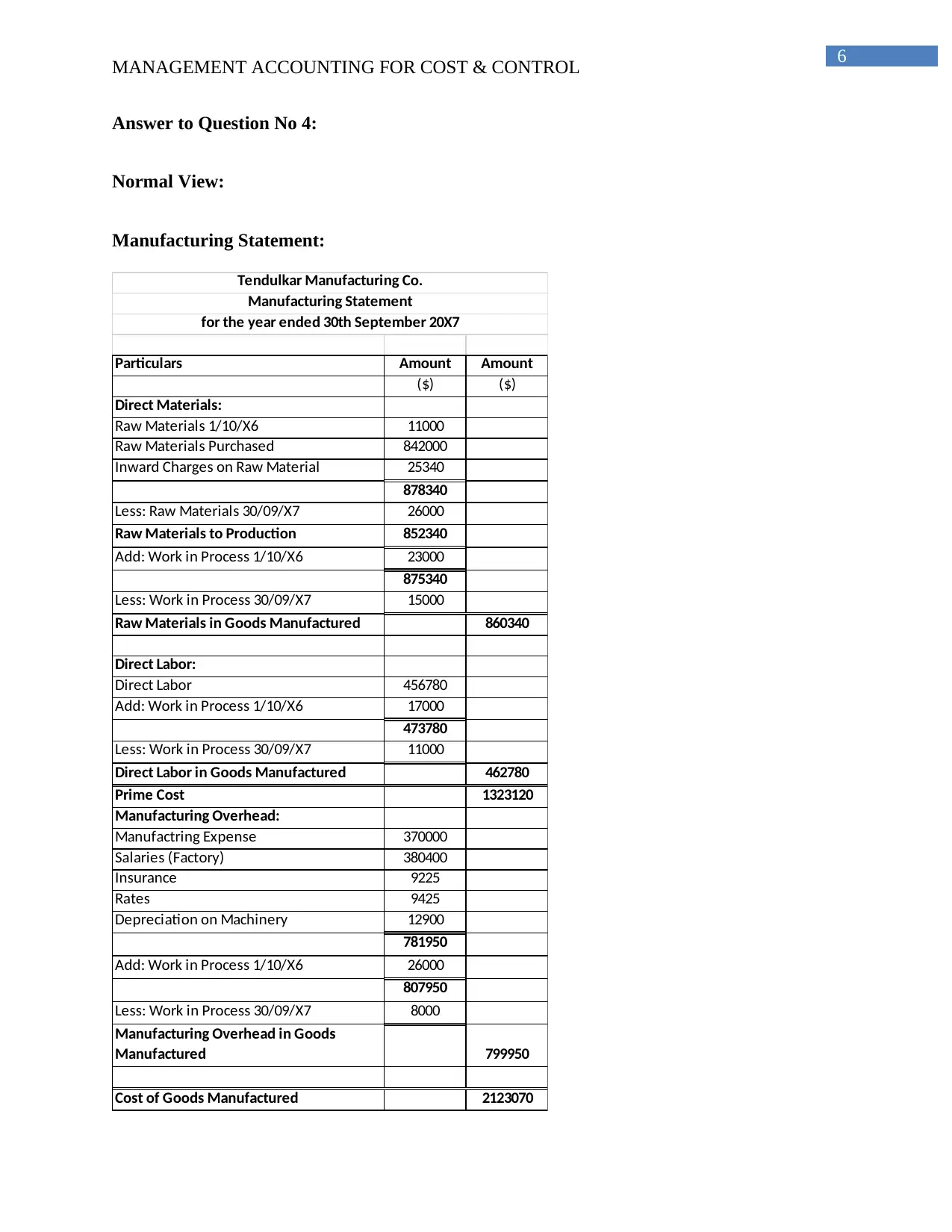

Answer to Question No 4:

Normal View:

Manufacturing Statement:

Particulars Amount Amount

($) ($)

Direct Materials:

Raw Materials 1/10/X6 11000

Raw Materials Purchased 842000

Inward Charges on Raw Material 25340

878340

Less: Raw Materials 30/09/X7 26000

Raw Materials to Production 852340

Add: Work in Process 1/10/X6 23000

875340

Less: Work in Process 30/09/X7 15000

Raw Materials in Goods Manufactured 860340

Direct Labor:

Direct Labor 456780

Add: Work in Process 1/10/X6 17000

473780

Less: Work in Process 30/09/X7 11000

Direct Labor in Goods Manufactured 462780

Prime Cost 1323120

Manufacturing Overhead:

Manufactring Expense 370000

Salaries (Factory) 380400

Insurance 9225

Rates 9425

Depreciation on Machinery 12900

781950

Add: Work in Process 1/10/X6 26000

807950

Less: Work in Process 30/09/X7 8000

Manufacturing Overhead in Goods

Manufactured 799950

Cost of Goods Manufactured 2123070

Tendulkar Manufacturing Co.

Manufacturing Statement

for the year ended 30th September 20X7

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Answer to Question No 4:

Normal View:

Manufacturing Statement:

Particulars Amount Amount

($) ($)

Direct Materials:

Raw Materials 1/10/X6 11000

Raw Materials Purchased 842000

Inward Charges on Raw Material 25340

878340

Less: Raw Materials 30/09/X7 26000

Raw Materials to Production 852340

Add: Work in Process 1/10/X6 23000

875340

Less: Work in Process 30/09/X7 15000

Raw Materials in Goods Manufactured 860340

Direct Labor:

Direct Labor 456780

Add: Work in Process 1/10/X6 17000

473780

Less: Work in Process 30/09/X7 11000

Direct Labor in Goods Manufactured 462780

Prime Cost 1323120

Manufacturing Overhead:

Manufactring Expense 370000

Salaries (Factory) 380400

Insurance 9225

Rates 9425

Depreciation on Machinery 12900

781950

Add: Work in Process 1/10/X6 26000

807950

Less: Work in Process 30/09/X7 8000

Manufacturing Overhead in Goods

Manufactured 799950

Cost of Goods Manufactured 2123070

Tendulkar Manufacturing Co.

Manufacturing Statement

for the year ended 30th September 20X7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGEMENT ACCOUNTING FOR COST & CONTROL

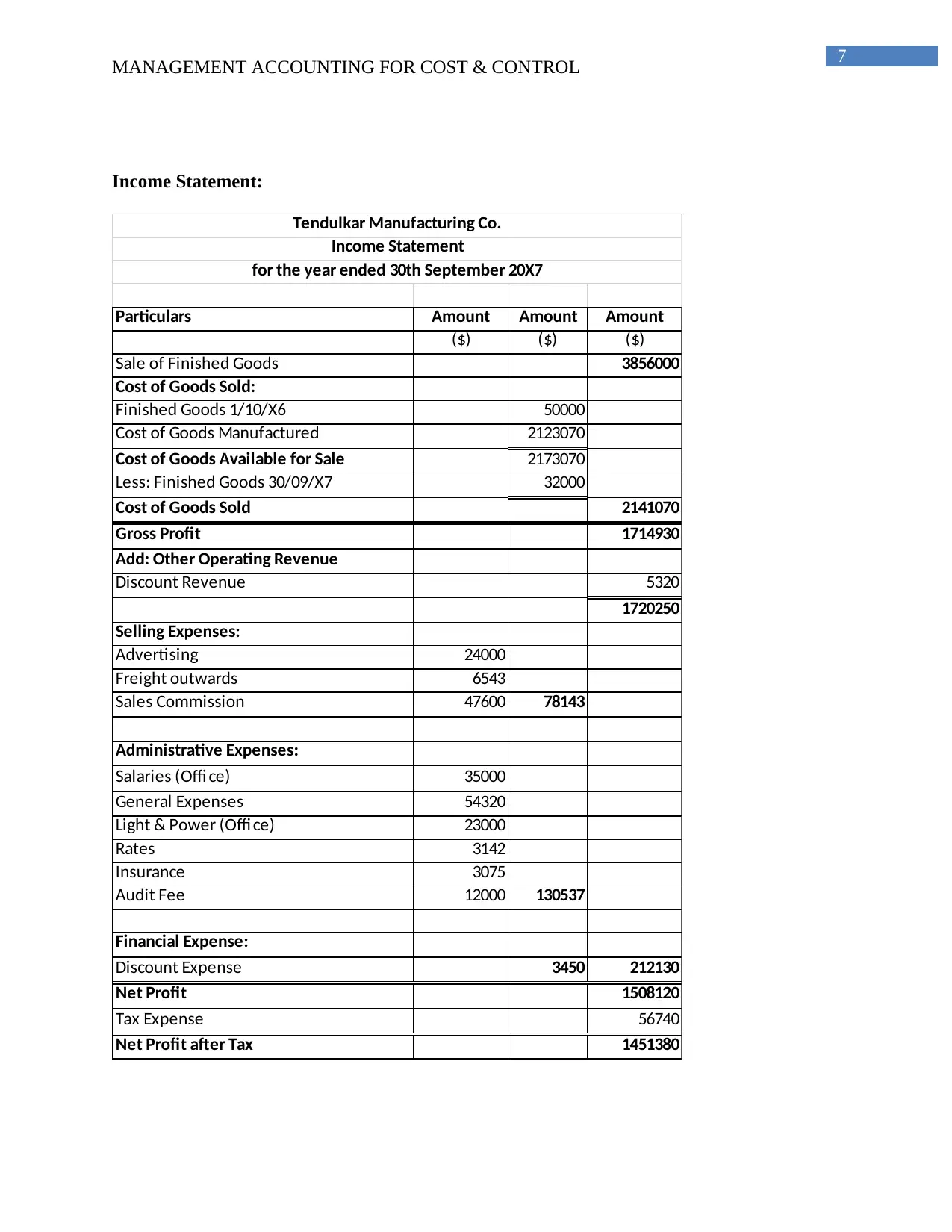

Income Statement:

Particulars Amount Amount Amount

($) ($) ($)

Sale of Finished Goods 3856000

Cost of Goods Sold:

Finished Goods 1/10/X6 50000

Cost of Goods Manufactured 2123070

Cost of Goods Available for Sale 2173070

Less: Finished Goods 30/09/X7 32000

Cost of Goods Sold 2141070

Gross Profit 1714930

Add: Other Operating Revenue

Discount Revenue 5320

1720250

Selling Expenses:

Advertising 24000

Freight outwards 6543

Sales Commission 47600 78143

Administrative Expenses:

Salaries (Offi ce) 35000

General Expenses 54320

Light & Power (Offi ce) 23000

Rates 3142

Insurance 3075

Audit Fee 12000 130537

Financial Expense:

Discount Expense 3450 212130

Net Profit 1508120

Tax Expense 56740

Net Profit after Tax 1451380

Tendulkar Manufacturing Co.

Income Statement

for the year ended 30th September 20X7

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Income Statement:

Particulars Amount Amount Amount

($) ($) ($)

Sale of Finished Goods 3856000

Cost of Goods Sold:

Finished Goods 1/10/X6 50000

Cost of Goods Manufactured 2123070

Cost of Goods Available for Sale 2173070

Less: Finished Goods 30/09/X7 32000

Cost of Goods Sold 2141070

Gross Profit 1714930

Add: Other Operating Revenue

Discount Revenue 5320

1720250

Selling Expenses:

Advertising 24000

Freight outwards 6543

Sales Commission 47600 78143

Administrative Expenses:

Salaries (Offi ce) 35000

General Expenses 54320

Light & Power (Offi ce) 23000

Rates 3142

Insurance 3075

Audit Fee 12000 130537

Financial Expense:

Discount Expense 3450 212130

Net Profit 1508120

Tax Expense 56740

Net Profit after Tax 1451380

Tendulkar Manufacturing Co.

Income Statement

for the year ended 30th September 20X7

8

MANAGEMENT ACCOUNTING FOR COST & CONTROL

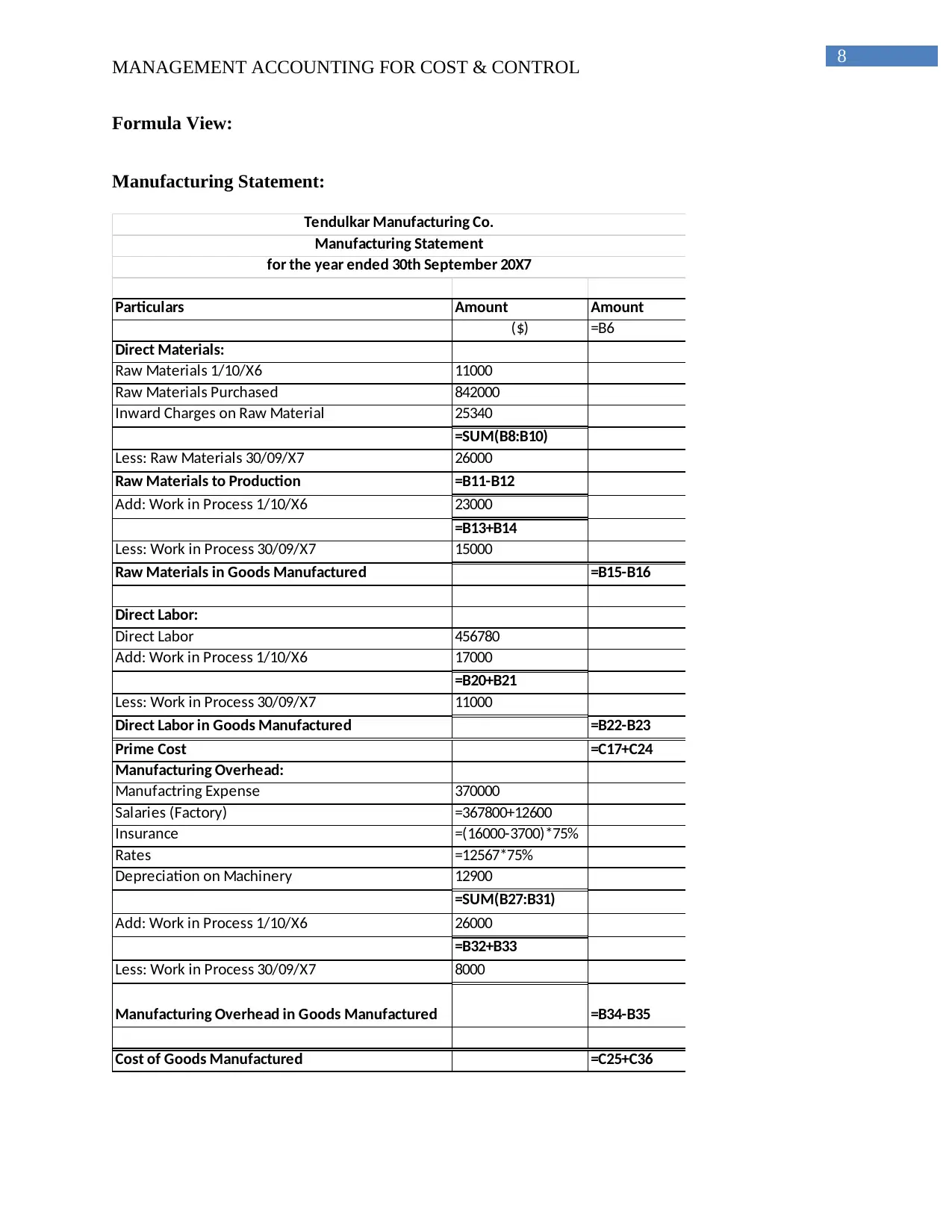

Formula View:

Manufacturing Statement:

Particulars Amount Amount

($) =B6

Direct Materials:

Raw Materials 1/10/X6 11000

Raw Materials Purchased 842000

Inward Charges on Raw Material 25340

=SUM(B8:B10)

Less: Raw Materials 30/09/X7 26000

Raw Materials to Production =B11-B12

Add: Work in Process 1/10/X6 23000

=B13+B14

Less: Work in Process 30/09/X7 15000

Raw Materials in Goods Manufactured =B15-B16

Direct Labor:

Direct Labor 456780

Add: Work in Process 1/10/X6 17000

=B20+B21

Less: Work in Process 30/09/X7 11000

Direct Labor in Goods Manufactured =B22-B23

Prime Cost =C17+C24

Manufacturing Overhead:

Manufactring Expense 370000

Salaries (Factory) =367800+12600

Insurance =(16000-3700)*75%

Rates =12567*75%

Depreciation on Machinery 12900

=SUM(B27:B31)

Add: Work in Process 1/10/X6 26000

=B32+B33

Less: Work in Process 30/09/X7 8000

Manufacturing Overhead in Goods Manufactured =B34-B35

Cost of Goods Manufactured =C25+C36

Tendulkar Manufacturing Co.

Manufacturing Statement

for the year ended 30th September 20X7

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Formula View:

Manufacturing Statement:

Particulars Amount Amount

($) =B6

Direct Materials:

Raw Materials 1/10/X6 11000

Raw Materials Purchased 842000

Inward Charges on Raw Material 25340

=SUM(B8:B10)

Less: Raw Materials 30/09/X7 26000

Raw Materials to Production =B11-B12

Add: Work in Process 1/10/X6 23000

=B13+B14

Less: Work in Process 30/09/X7 15000

Raw Materials in Goods Manufactured =B15-B16

Direct Labor:

Direct Labor 456780

Add: Work in Process 1/10/X6 17000

=B20+B21

Less: Work in Process 30/09/X7 11000

Direct Labor in Goods Manufactured =B22-B23

Prime Cost =C17+C24

Manufacturing Overhead:

Manufactring Expense 370000

Salaries (Factory) =367800+12600

Insurance =(16000-3700)*75%

Rates =12567*75%

Depreciation on Machinery 12900

=SUM(B27:B31)

Add: Work in Process 1/10/X6 26000

=B32+B33

Less: Work in Process 30/09/X7 8000

Manufacturing Overhead in Goods Manufactured =B34-B35

Cost of Goods Manufactured =C25+C36

Tendulkar Manufacturing Co.

Manufacturing Statement

for the year ended 30th September 20X7

9

MANAGEMENT ACCOUNTING FOR COST & CONTROL

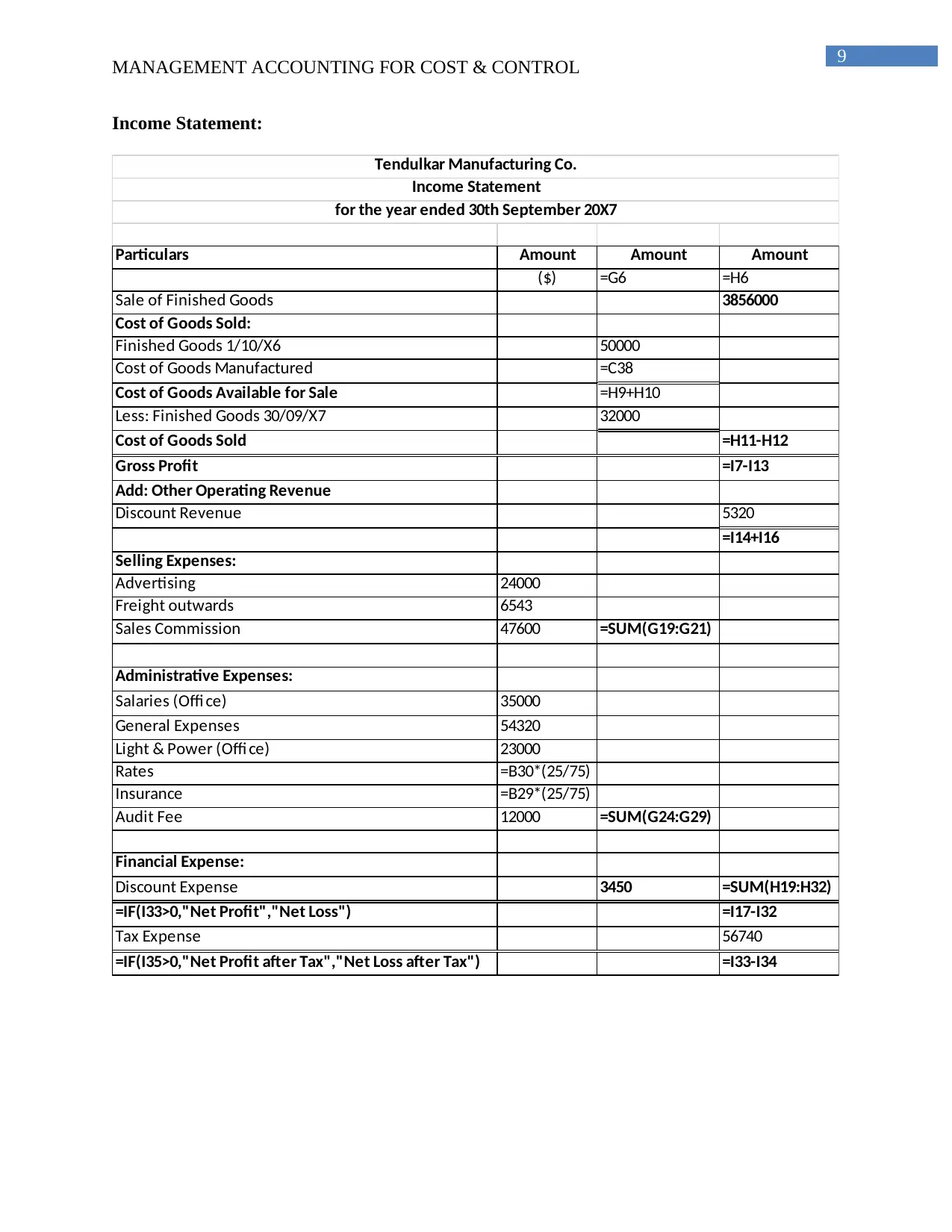

Income Statement:

Particulars Amount Amount Amount

($) =G6 =H6

Sale of Finished Goods 3856000

Cost of Goods Sold:

Finished Goods 1/10/X6 50000

Cost of Goods Manufactured =C38

Cost of Goods Available for Sale =H9+H10

Less: Finished Goods 30/09/X7 32000

Cost of Goods Sold =H11-H12

Gross Profit =I7-I13

Add: Other Operating Revenue

Discount Revenue 5320

=I14+I16

Selling Expenses:

Advertising 24000

Freight outwards 6543

Sales Commission 47600 =SUM(G19:G21)

Administrative Expenses:

Salaries (Offi ce) 35000

General Expenses 54320

Light & Power (Offi ce) 23000

Rates =B30*(25/75)

Insurance =B29*(25/75)

Audit Fee 12000 =SUM(G24:G29)

Financial Expense:

Discount Expense 3450 =SUM(H19:H32)

=IF(I33>0,"Net Profit","Net Loss") =I17-I32

Tax Expense 56740

=IF(I35>0,"Net Profit after Tax","Net Loss after Tax") =I33-I34

Tendulkar Manufacturing Co.

Income Statement

for the year ended 30th September 20X7

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Income Statement:

Particulars Amount Amount Amount

($) =G6 =H6

Sale of Finished Goods 3856000

Cost of Goods Sold:

Finished Goods 1/10/X6 50000

Cost of Goods Manufactured =C38

Cost of Goods Available for Sale =H9+H10

Less: Finished Goods 30/09/X7 32000

Cost of Goods Sold =H11-H12

Gross Profit =I7-I13

Add: Other Operating Revenue

Discount Revenue 5320

=I14+I16

Selling Expenses:

Advertising 24000

Freight outwards 6543

Sales Commission 47600 =SUM(G19:G21)

Administrative Expenses:

Salaries (Offi ce) 35000

General Expenses 54320

Light & Power (Offi ce) 23000

Rates =B30*(25/75)

Insurance =B29*(25/75)

Audit Fee 12000 =SUM(G24:G29)

Financial Expense:

Discount Expense 3450 =SUM(H19:H32)

=IF(I33>0,"Net Profit","Net Loss") =I17-I32

Tax Expense 56740

=IF(I35>0,"Net Profit after Tax","Net Loss after Tax") =I33-I34

Tendulkar Manufacturing Co.

Income Statement

for the year ended 30th September 20X7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

MANAGEMENT ACCOUNTING FOR COST & CONTROL

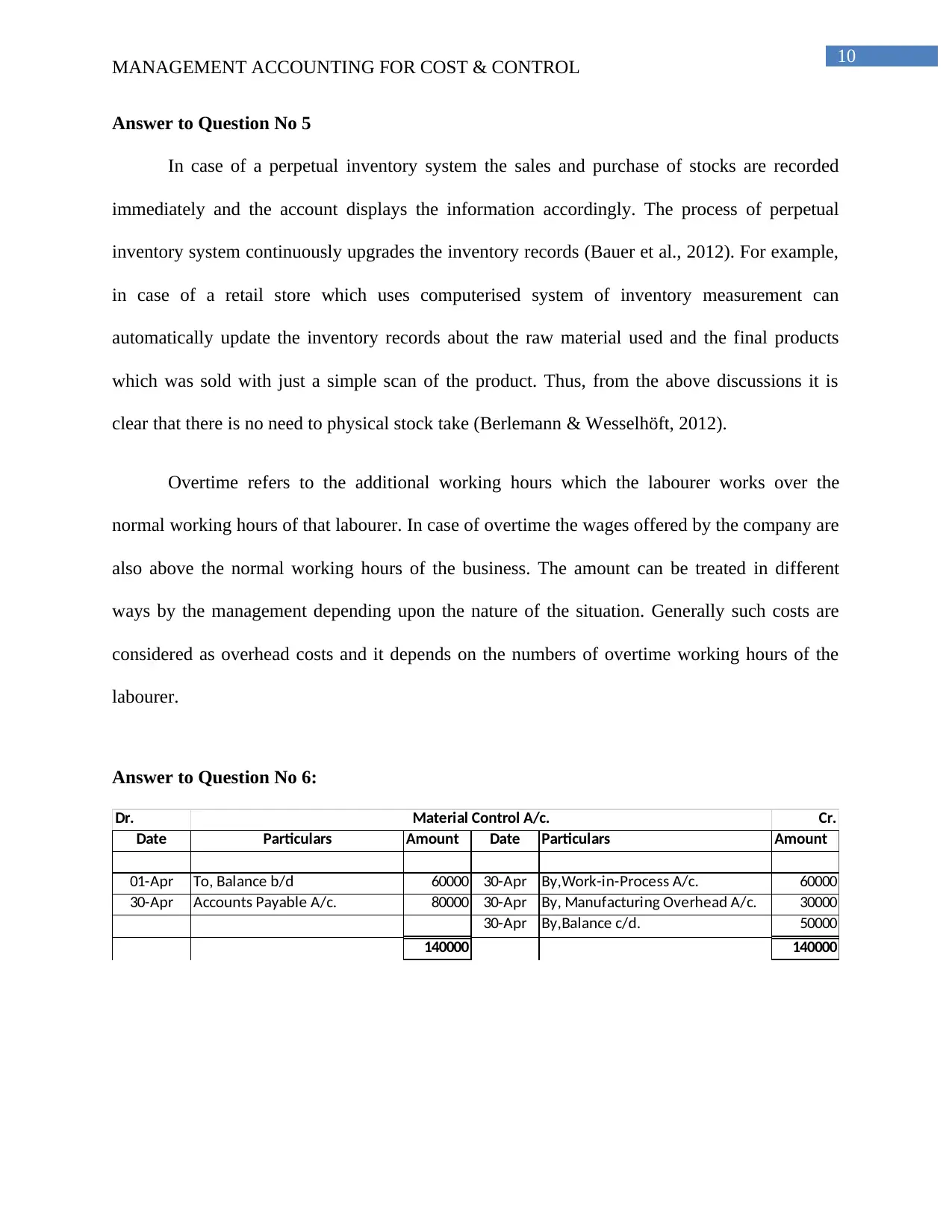

Answer to Question No 5

In case of a perpetual inventory system the sales and purchase of stocks are recorded

immediately and the account displays the information accordingly. The process of perpetual

inventory system continuously upgrades the inventory records (Bauer et al., 2012). For example,

in case of a retail store which uses computerised system of inventory measurement can

automatically update the inventory records about the raw material used and the final products

which was sold with just a simple scan of the product. Thus, from the above discussions it is

clear that there is no need to physical stock take (Berlemann & Wesselhöft, 2012).

Overtime refers to the additional working hours which the labourer works over the

normal working hours of that labourer. In case of overtime the wages offered by the company are

also above the normal working hours of the business. The amount can be treated in different

ways by the management depending upon the nature of the situation. Generally such costs are

considered as overhead costs and it depends on the numbers of overtime working hours of the

labourer.

Answer to Question No 6:

Dr. Cr.

Date Particulars Amount Date Particulars Amount

01-Apr To, Balance b/d 60000 30-Apr By,Work-in-Process A/c. 60000

30-Apr Accounts Payable A/c. 80000 30-Apr By, Manufacturing Overhead A/c. 30000

30-Apr By,Balance c/d. 50000

140000 140000

Material Control A/c.

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Answer to Question No 5

In case of a perpetual inventory system the sales and purchase of stocks are recorded

immediately and the account displays the information accordingly. The process of perpetual

inventory system continuously upgrades the inventory records (Bauer et al., 2012). For example,

in case of a retail store which uses computerised system of inventory measurement can

automatically update the inventory records about the raw material used and the final products

which was sold with just a simple scan of the product. Thus, from the above discussions it is

clear that there is no need to physical stock take (Berlemann & Wesselhöft, 2012).

Overtime refers to the additional working hours which the labourer works over the

normal working hours of that labourer. In case of overtime the wages offered by the company are

also above the normal working hours of the business. The amount can be treated in different

ways by the management depending upon the nature of the situation. Generally such costs are

considered as overhead costs and it depends on the numbers of overtime working hours of the

labourer.

Answer to Question No 6:

Dr. Cr.

Date Particulars Amount Date Particulars Amount

01-Apr To, Balance b/d 60000 30-Apr By,Work-in-Process A/c. 60000

30-Apr Accounts Payable A/c. 80000 30-Apr By, Manufacturing Overhead A/c. 30000

30-Apr By,Balance c/d. 50000

140000 140000

Material Control A/c.

11

MANAGEMENT ACCOUNTING FOR COST & CONTROL

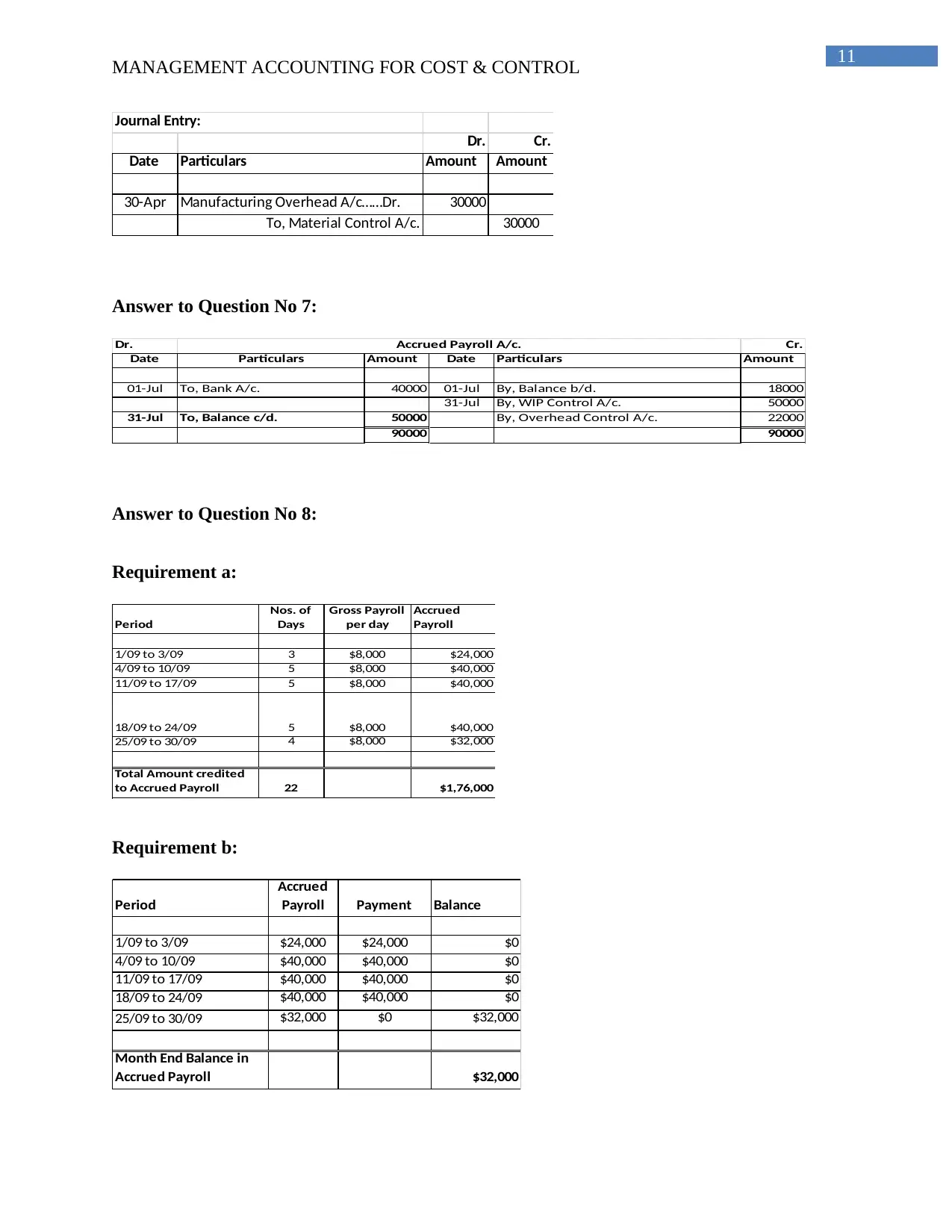

Journal Entry:

Dr. Cr.

Date Particulars Amount Amount

30-Apr Manufacturing Overhead A/c……Dr. 30000

To, Material Control A/c. 30000

Answer to Question No 7:

Dr. Cr.

Date Particulars Amount Date Particulars Amount

01-Jul To, Bank A/c. 40000 01-Jul By, Balance b/d. 18000

31-Jul By, WIP Control A/c. 50000

31-Jul To, Balance c/d. 50000 By, Overhead Control A/c. 22000

90000 90000

Accrued Payroll A/c.

Answer to Question No 8:

Requirement a:

Period

Nos. of

Days

Gross Payroll

per day

Accrued

Payroll

1/09 to 3/09 3 $8,000 $24,000

4/09 to 10/09 5 $8,000 $40,000

11/09 to 17/09 5 $8,000 $40,000

18/09 to 24/09 5 $8,000 $40,000

25/09 to 30/09 4 $8,000 $32,000

Total Amount credited

to Accrued Payroll 22 $1,76,000

Requirement b:

Period

Accrued

Payroll Payment Balance

1/09 to 3/09 $24,000 $24,000 $0

4/09 to 10/09 $40,000 $40,000 $0

11/09 to 17/09 $40,000 $40,000 $0

18/09 to 24/09 $40,000 $40,000 $0

25/09 to 30/09 $32,000 $0 $32,000

Month End Balance in

Accrued Payroll $32,000

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Journal Entry:

Dr. Cr.

Date Particulars Amount Amount

30-Apr Manufacturing Overhead A/c……Dr. 30000

To, Material Control A/c. 30000

Answer to Question No 7:

Dr. Cr.

Date Particulars Amount Date Particulars Amount

01-Jul To, Bank A/c. 40000 01-Jul By, Balance b/d. 18000

31-Jul By, WIP Control A/c. 50000

31-Jul To, Balance c/d. 50000 By, Overhead Control A/c. 22000

90000 90000

Accrued Payroll A/c.

Answer to Question No 8:

Requirement a:

Period

Nos. of

Days

Gross Payroll

per day

Accrued

Payroll

1/09 to 3/09 3 $8,000 $24,000

4/09 to 10/09 5 $8,000 $40,000

11/09 to 17/09 5 $8,000 $40,000

18/09 to 24/09 5 $8,000 $40,000

25/09 to 30/09 4 $8,000 $32,000

Total Amount credited

to Accrued Payroll 22 $1,76,000

Requirement b:

Period

Accrued

Payroll Payment Balance

1/09 to 3/09 $24,000 $24,000 $0

4/09 to 10/09 $40,000 $40,000 $0

11/09 to 17/09 $40,000 $40,000 $0

18/09 to 24/09 $40,000 $40,000 $0

25/09 to 30/09 $32,000 $0 $32,000

Month End Balance in

Accrued Payroll $32,000

12

MANAGEMENT ACCOUNTING FOR COST & CONTROL

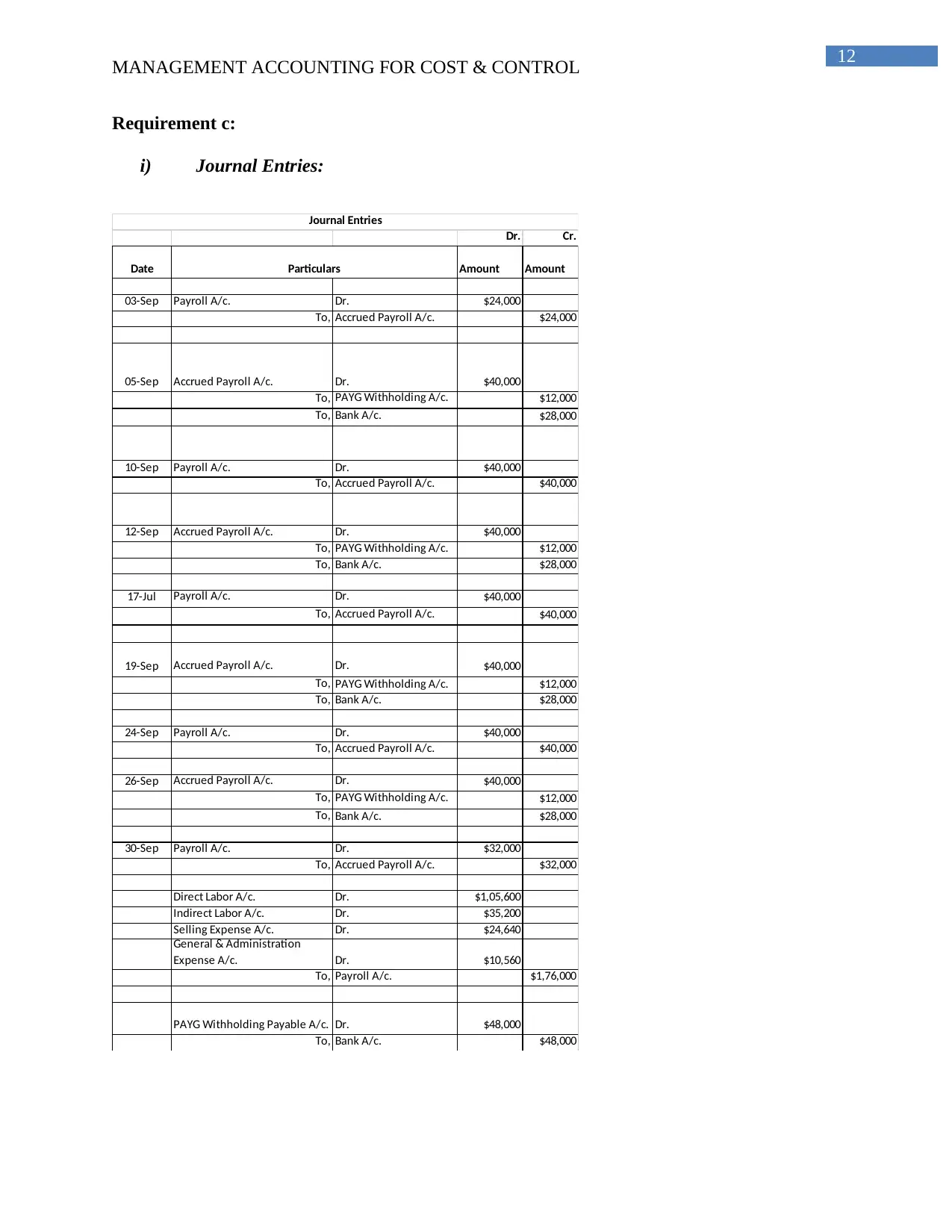

Requirement c:

i) Journal Entries:

Dr. Cr.

Date Amount Amount

03-Sep Payroll A/c. Dr. $24,000

To, Accrued Payroll A/c. $24,000

05-Sep Accrued Payroll A/c. Dr. $40,000

To, PAYG Withholding A/c. $12,000

To, Bank A/c. $28,000

10-Sep Payroll A/c. Dr. $40,000

To, Accrued Payroll A/c. $40,000

12-Sep Accrued Payroll A/c. Dr. $40,000

To, PAYG Withholding A/c. $12,000

To, Bank A/c. $28,000

17-Jul Payroll A/c. Dr. $40,000

To, Accrued Payroll A/c. $40,000

19-Sep Accrued Payroll A/c. Dr. $40,000

To, PAYG Withholding A/c. $12,000

To, Bank A/c. $28,000

24-Sep Payroll A/c. Dr. $40,000

To, Accrued Payroll A/c. $40,000

26-Sep Accrued Payroll A/c. Dr. $40,000

To, PAYG Withholding A/c. $12,000

To, Bank A/c. $28,000

30-Sep Payroll A/c. Dr. $32,000

To, Accrued Payroll A/c. $32,000

Direct Labor A/c. Dr. $1,05,600

Indirect Labor A/c. Dr. $35,200

Selling Expense A/c. Dr. $24,640

General & Administration

Expense A/c. Dr. $10,560

To, Payroll A/c. $1,76,000

PAYG Withholding Payable A/c. Dr. $48,000

To, Bank A/c. $48,000

Particulars

Journal Entries

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Requirement c:

i) Journal Entries:

Dr. Cr.

Date Amount Amount

03-Sep Payroll A/c. Dr. $24,000

To, Accrued Payroll A/c. $24,000

05-Sep Accrued Payroll A/c. Dr. $40,000

To, PAYG Withholding A/c. $12,000

To, Bank A/c. $28,000

10-Sep Payroll A/c. Dr. $40,000

To, Accrued Payroll A/c. $40,000

12-Sep Accrued Payroll A/c. Dr. $40,000

To, PAYG Withholding A/c. $12,000

To, Bank A/c. $28,000

17-Jul Payroll A/c. Dr. $40,000

To, Accrued Payroll A/c. $40,000

19-Sep Accrued Payroll A/c. Dr. $40,000

To, PAYG Withholding A/c. $12,000

To, Bank A/c. $28,000

24-Sep Payroll A/c. Dr. $40,000

To, Accrued Payroll A/c. $40,000

26-Sep Accrued Payroll A/c. Dr. $40,000

To, PAYG Withholding A/c. $12,000

To, Bank A/c. $28,000

30-Sep Payroll A/c. Dr. $32,000

To, Accrued Payroll A/c. $32,000

Direct Labor A/c. Dr. $1,05,600

Indirect Labor A/c. Dr. $35,200

Selling Expense A/c. Dr. $24,640

General & Administration

Expense A/c. Dr. $10,560

To, Payroll A/c. $1,76,000

PAYG Withholding Payable A/c. Dr. $48,000

To, Bank A/c. $48,000

Particulars

Journal Entries

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

MANAGEMENT ACCOUNTING FOR COST & CONTROL

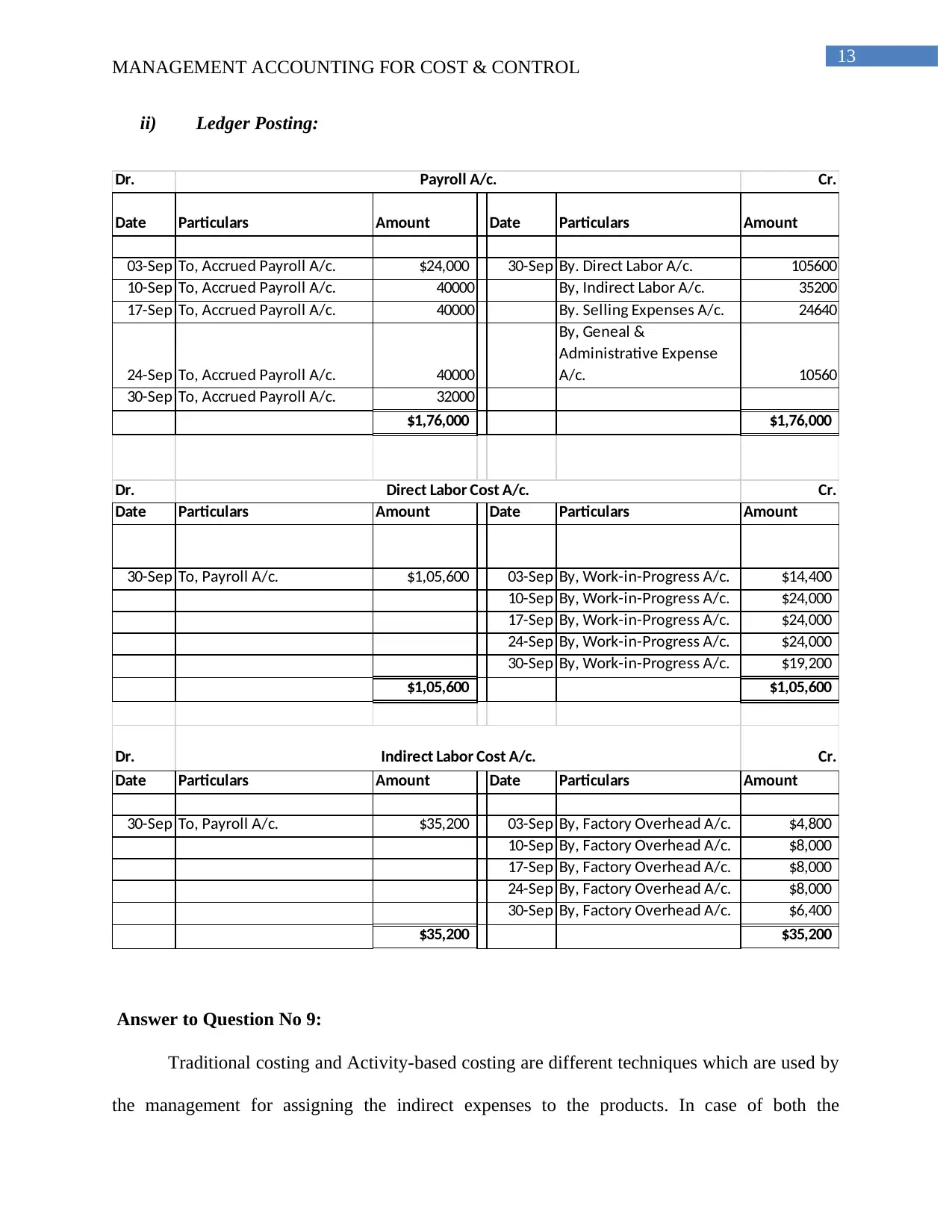

ii) Ledger Posting:

Dr. Cr.

Date Particulars Amount Date Particulars Amount

03-Sep To, Accrued Payroll A/c. $24,000 30-Sep By. Direct Labor A/c. 105600

10-Sep To, Accrued Payroll A/c. 40000 By, Indirect Labor A/c. 35200

17-Sep To, Accrued Payroll A/c. 40000 By. Selling Expenses A/c. 24640

24-Sep To, Accrued Payroll A/c. 40000

By, Geneal &

Administrative Expense

A/c. 10560

30-Sep To, Accrued Payroll A/c. 32000

$1,76,000 $1,76,000

Dr. Cr.

Date Particulars Amount Date Particulars Amount

30-Sep To, Payroll A/c. $1,05,600 03-Sep By, Work-in-Progress A/c. $14,400

10-Sep By, Work-in-Progress A/c. $24,000

17-Sep By, Work-in-Progress A/c. $24,000

24-Sep By, Work-in-Progress A/c. $24,000

30-Sep By, Work-in-Progress A/c. $19,200

$1,05,600 $1,05,600

Dr. Cr.

Date Particulars Amount Date Particulars Amount

30-Sep To, Payroll A/c. $35,200 03-Sep By, Factory Overhead A/c. $4,800

10-Sep By, Factory Overhead A/c. $8,000

17-Sep By, Factory Overhead A/c. $8,000

24-Sep By, Factory Overhead A/c. $8,000

30-Sep By, Factory Overhead A/c. $6,400

$35,200 $35,200

Indirect Labor Cost A/c.

Payroll A/c.

Direct Labor Cost A/c.

Answer to Question No 9:

Traditional costing and Activity-based costing are different techniques which are used by

the management for assigning the indirect expenses to the products. In case of both the

MANAGEMENT ACCOUNTING FOR COST & CONTROL

ii) Ledger Posting:

Dr. Cr.

Date Particulars Amount Date Particulars Amount

03-Sep To, Accrued Payroll A/c. $24,000 30-Sep By. Direct Labor A/c. 105600

10-Sep To, Accrued Payroll A/c. 40000 By, Indirect Labor A/c. 35200

17-Sep To, Accrued Payroll A/c. 40000 By. Selling Expenses A/c. 24640

24-Sep To, Accrued Payroll A/c. 40000

By, Geneal &

Administrative Expense

A/c. 10560

30-Sep To, Accrued Payroll A/c. 32000

$1,76,000 $1,76,000

Dr. Cr.

Date Particulars Amount Date Particulars Amount

30-Sep To, Payroll A/c. $1,05,600 03-Sep By, Work-in-Progress A/c. $14,400

10-Sep By, Work-in-Progress A/c. $24,000

17-Sep By, Work-in-Progress A/c. $24,000

24-Sep By, Work-in-Progress A/c. $24,000

30-Sep By, Work-in-Progress A/c. $19,200

$1,05,600 $1,05,600

Dr. Cr.

Date Particulars Amount Date Particulars Amount

30-Sep To, Payroll A/c. $35,200 03-Sep By, Factory Overhead A/c. $4,800

10-Sep By, Factory Overhead A/c. $8,000

17-Sep By, Factory Overhead A/c. $8,000

24-Sep By, Factory Overhead A/c. $8,000

30-Sep By, Factory Overhead A/c. $6,400

$35,200 $35,200

Indirect Labor Cost A/c.

Payroll A/c.

Direct Labor Cost A/c.

Answer to Question No 9:

Traditional costing and Activity-based costing are different techniques which are used by

the management for assigning the indirect expenses to the products. In case of both the

14

MANAGEMENT ACCOUNTING FOR COST & CONTROL

processes, the indirect costs are projected and the same are allocated on the basis of the cost

drivers which are most appropriate (Ray, 2012). The basic differences between the two

processes are on the points of complexity and accuracy which exists between the two processes.

In case of traditional costing method costs are allocated on the basis of random aggregate rate

and is less precise. These factors are covered up by activity-based costing techniques, however it

is a bit on the complex side.

The benefits which are associated with ABC Costing techniques are:

1. The method improves the processes of organization

2. The products which are not productive are recognized by the business by the use of this

method.

3. The method of ABC costing is easy to understand

4. It is good for business

The disadvantages of ABC costing are as follows:

1. The implementation process of ABC Costing techniques is quite costly.

2. The chances of data misinterpretation are also there in case of ABC Techniques.

MANAGEMENT ACCOUNTING FOR COST & CONTROL

processes, the indirect costs are projected and the same are allocated on the basis of the cost

drivers which are most appropriate (Ray, 2012). The basic differences between the two

processes are on the points of complexity and accuracy which exists between the two processes.

In case of traditional costing method costs are allocated on the basis of random aggregate rate

and is less precise. These factors are covered up by activity-based costing techniques, however it

is a bit on the complex side.

The benefits which are associated with ABC Costing techniques are:

1. The method improves the processes of organization

2. The products which are not productive are recognized by the business by the use of this

method.

3. The method of ABC costing is easy to understand

4. It is good for business

The disadvantages of ABC costing are as follows:

1. The implementation process of ABC Costing techniques is quite costly.

2. The chances of data misinterpretation are also there in case of ABC Techniques.

15

MANAGEMENT ACCOUNTING FOR COST & CONTROL

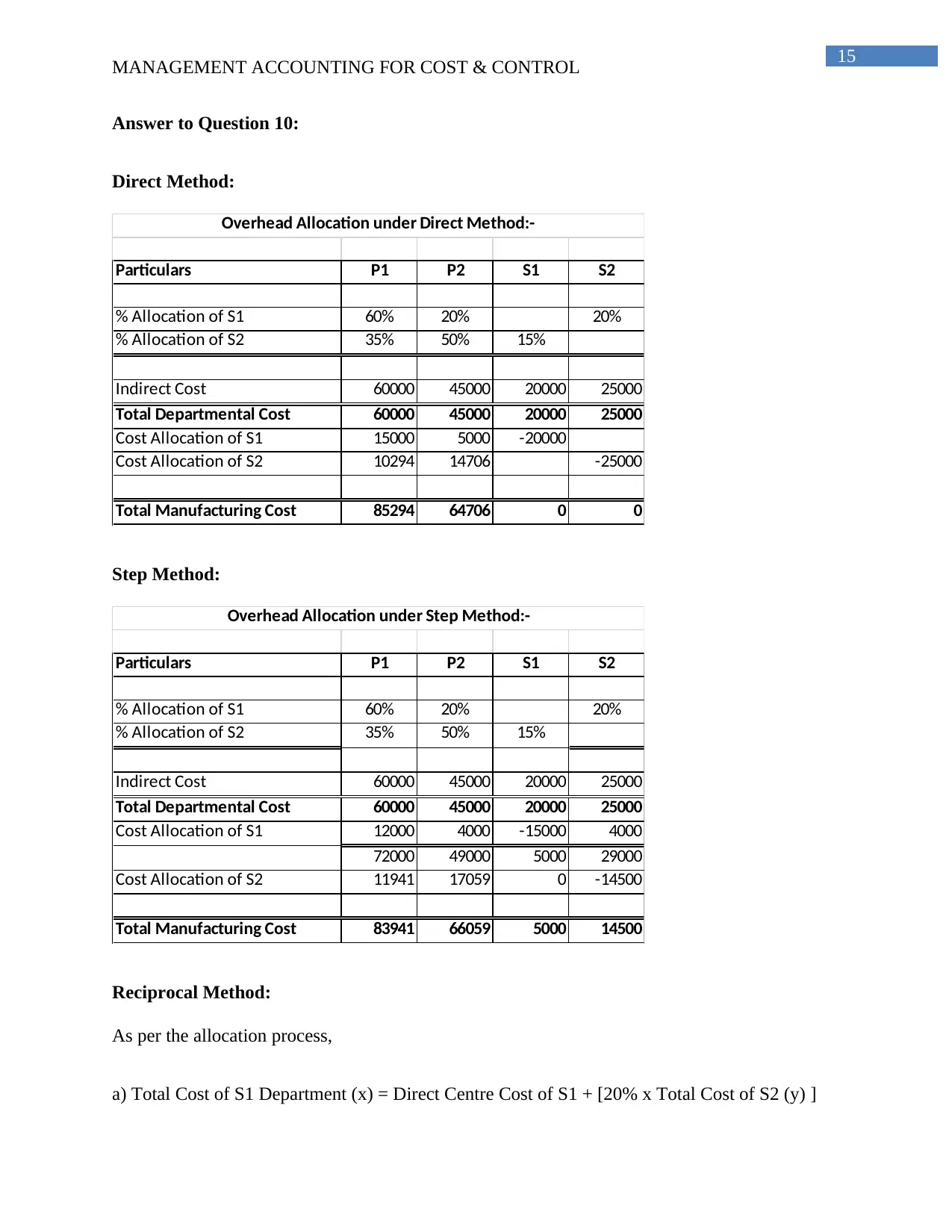

Answer to Question 10:

Direct Method:

Particulars P1 P2 S1 S2

% Allocation of S1 60% 20% 20%

% Allocation of S2 35% 50% 15%

Indirect Cost 60000 45000 20000 25000

Total Departmental Cost 60000 45000 20000 25000

Cost Allocation of S1 15000 5000 -20000

Cost Allocation of S2 10294 14706 -25000

Total Manufacturing Cost 85294 64706 0 0

Overhead Allocation under Direct Method:-

Step Method:

Particulars P1 P2 S1 S2

% Allocation of S1 60% 20% 20%

% Allocation of S2 35% 50% 15%

Indirect Cost 60000 45000 20000 25000

Total Departmental Cost 60000 45000 20000 25000

Cost Allocation of S1 12000 4000 -15000 4000

72000 49000 5000 29000

Cost Allocation of S2 11941 17059 0 -14500

Total Manufacturing Cost 83941 66059 5000 14500

Overhead Allocation under Step Method:-

Reciprocal Method:

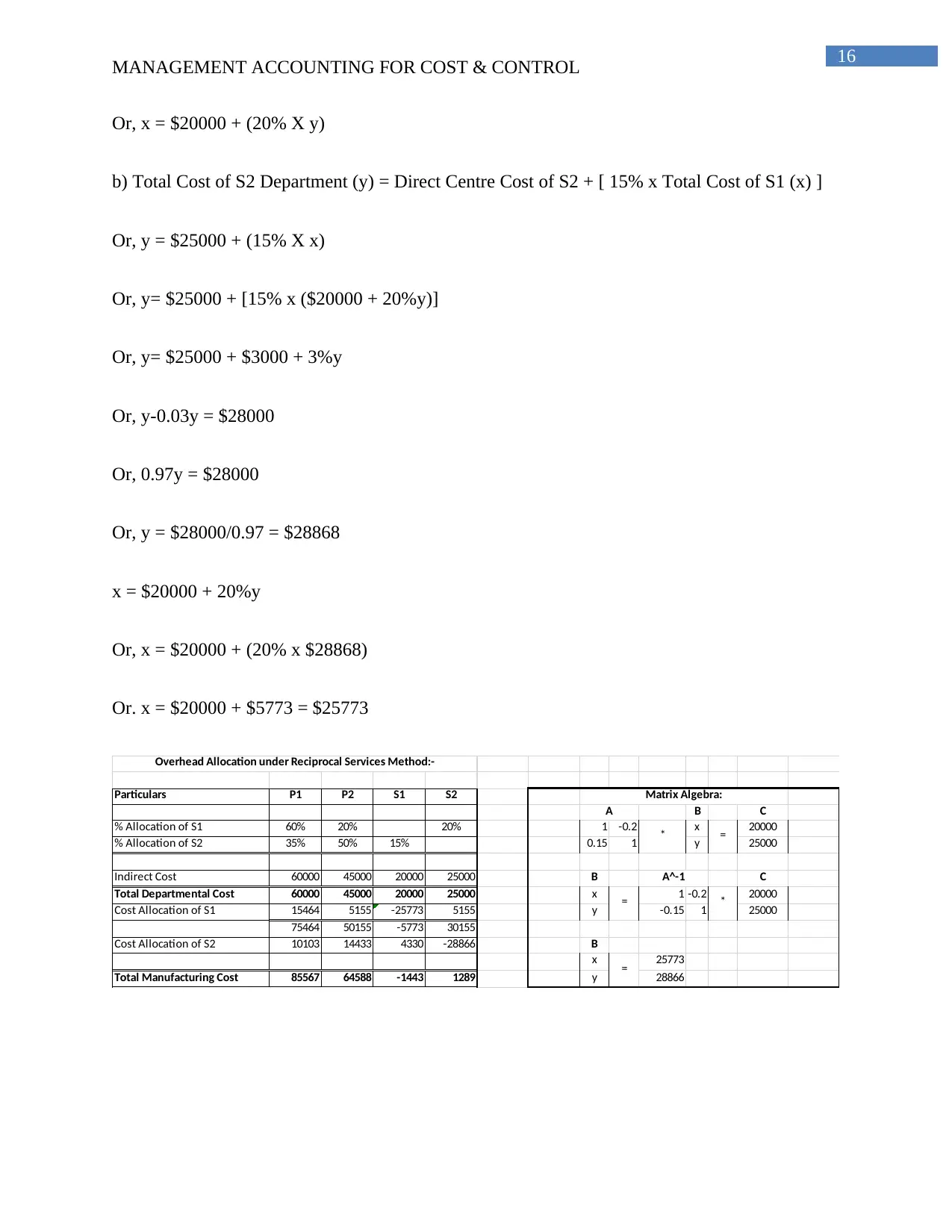

As per the allocation process,

a) Total Cost of S1 Department (x) = Direct Centre Cost of S1 + [20% x Total Cost of S2 (y) ]

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Answer to Question 10:

Direct Method:

Particulars P1 P2 S1 S2

% Allocation of S1 60% 20% 20%

% Allocation of S2 35% 50% 15%

Indirect Cost 60000 45000 20000 25000

Total Departmental Cost 60000 45000 20000 25000

Cost Allocation of S1 15000 5000 -20000

Cost Allocation of S2 10294 14706 -25000

Total Manufacturing Cost 85294 64706 0 0

Overhead Allocation under Direct Method:-

Step Method:

Particulars P1 P2 S1 S2

% Allocation of S1 60% 20% 20%

% Allocation of S2 35% 50% 15%

Indirect Cost 60000 45000 20000 25000

Total Departmental Cost 60000 45000 20000 25000

Cost Allocation of S1 12000 4000 -15000 4000

72000 49000 5000 29000

Cost Allocation of S2 11941 17059 0 -14500

Total Manufacturing Cost 83941 66059 5000 14500

Overhead Allocation under Step Method:-

Reciprocal Method:

As per the allocation process,

a) Total Cost of S1 Department (x) = Direct Centre Cost of S1 + [20% x Total Cost of S2 (y) ]

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Or, x = $20000 + (20% X y)

b) Total Cost of S2 Department (y) = Direct Centre Cost of S2 + [ 15% x Total Cost of S1 (x) ]

Or, y = $25000 + (15% X x)

Or, y= $25000 + [15% x ($20000 + 20%y)]

Or, y= $25000 + $3000 + 3%y

Or, y-0.03y = $28000

Or, 0.97y = $28000

Or, y = $28000/0.97 = $28868

x = $20000 + 20%y

Or, x = $20000 + (20% x $28868)

Or. x = $20000 + $5773 = $25773

Particulars P1 P2 S1 S2

B C

% Allocation of S1 60% 20% 20% 1 -0.2 x 20000

% Allocation of S2 35% 50% 15% 0.15 1 y 25000

Indirect Cost 60000 45000 20000 25000 B C

Total Departmental Cost 60000 45000 20000 25000 x 1 -0.2 20000

Cost Allocation of S1 15464 5155 -25773 5155 y -0.15 1 25000

75464 50155 -5773 30155

Cost Allocation of S2 10103 14433 4330 -28866 B

x 25773

Total Manufacturing Cost 85567 64588 -1443 1289 y 28866

=

A^-1

*

=

Overhead Allocation under Reciprocal Services Method:-

A

*

Matrix Algebra:

=

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Or, x = $20000 + (20% X y)

b) Total Cost of S2 Department (y) = Direct Centre Cost of S2 + [ 15% x Total Cost of S1 (x) ]

Or, y = $25000 + (15% X x)

Or, y= $25000 + [15% x ($20000 + 20%y)]

Or, y= $25000 + $3000 + 3%y

Or, y-0.03y = $28000

Or, 0.97y = $28000

Or, y = $28000/0.97 = $28868

x = $20000 + 20%y

Or, x = $20000 + (20% x $28868)

Or. x = $20000 + $5773 = $25773

Particulars P1 P2 S1 S2

B C

% Allocation of S1 60% 20% 20% 1 -0.2 x 20000

% Allocation of S2 35% 50% 15% 0.15 1 y 25000

Indirect Cost 60000 45000 20000 25000 B C

Total Departmental Cost 60000 45000 20000 25000 x 1 -0.2 20000

Cost Allocation of S1 15464 5155 -25773 5155 y -0.15 1 25000

75464 50155 -5773 30155

Cost Allocation of S2 10103 14433 4330 -28866 B

x 25773

Total Manufacturing Cost 85567 64588 -1443 1289 y 28866

=

A^-1

*

=

Overhead Allocation under Reciprocal Services Method:-

A

*

Matrix Algebra:

=

17

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Reference List

Bauer, D. G., Campero, R. J., Rasband, P. B., & Weel, M. D. (2012). U.S. Patent No. 8,321,302.

Washington, DC: U.S. Patent and Trademark Office.

Berlemann, M., & Wesselhöft, J. E. (2012). Estimating aggregate capital stocks using the

perpetual inventory method: New empirical evidence for 103 countries (No. 125).

Diskussionspapier, Helmut-Schmidt-Universität, Fächergruppe Volkswirtschaftslehre.

Biege, S., Lay, G., & Buschak, D. (2012). Mapping service processes in manufacturing

companies: industrial service blueprinting. International Journal of Operations & Production

Management, 32(8), 932-957.

Chadwick, G. (2013). A systems view of planning: towards a theory of the urban and regional

planning process. Elsevier.

Gane, N. (2012). The governmentalities of neoliberalism: panopticism, post-panopticism and

beyond. The Sociological Review, 60(4), 611-634.

King, R. D. (2012). Imprisonment: some international comparisons and the need to revisit

panopticism. In Handbook on prisons (pp. 125-152). Routledge.

Ray, S. (2012). Relevance and applicability of activity based costing: An appraisal. Journal of

Expert Systems (JES), 1(3), 7.

Zubakov, V. M., & Mustafin, A. N. (2015). The Controlling Process of the Human Capital

through the Effective Redistribution of the General Welfare. Mediterranean Journal of Social

Sciences, 6(1 S3), 270.

MANAGEMENT ACCOUNTING FOR COST & CONTROL

Reference List

Bauer, D. G., Campero, R. J., Rasband, P. B., & Weel, M. D. (2012). U.S. Patent No. 8,321,302.

Washington, DC: U.S. Patent and Trademark Office.

Berlemann, M., & Wesselhöft, J. E. (2012). Estimating aggregate capital stocks using the

perpetual inventory method: New empirical evidence for 103 countries (No. 125).

Diskussionspapier, Helmut-Schmidt-Universität, Fächergruppe Volkswirtschaftslehre.

Biege, S., Lay, G., & Buschak, D. (2012). Mapping service processes in manufacturing

companies: industrial service blueprinting. International Journal of Operations & Production

Management, 32(8), 932-957.

Chadwick, G. (2013). A systems view of planning: towards a theory of the urban and regional

planning process. Elsevier.

Gane, N. (2012). The governmentalities of neoliberalism: panopticism, post-panopticism and

beyond. The Sociological Review, 60(4), 611-634.

King, R. D. (2012). Imprisonment: some international comparisons and the need to revisit

panopticism. In Handbook on prisons (pp. 125-152). Routledge.

Ray, S. (2012). Relevance and applicability of activity based costing: An appraisal. Journal of

Expert Systems (JES), 1(3), 7.

Zubakov, V. M., & Mustafin, A. N. (2015). The Controlling Process of the Human Capital

through the Effective Redistribution of the General Welfare. Mediterranean Journal of Social

Sciences, 6(1 S3), 270.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.