Management Accounting for Costs and Control

VerifiedAdded on 2021/05/31

|26

|2430

|29

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

Management accounting for costs and control

Subject code

Student name and ID number

Assignment task number

Author note

Management accounting for costs and control

Subject code

Student name and ID number

Assignment task number

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

Table of Contents

Question 1..................................................................................................................................2

Question 2..................................................................................................................................9

Question 3................................................................................................................................12

Question 4................................................................................................................................16

Question 5................................................................................................................................21

Reference..................................................................................................................................24

Name

Student ID Page 1

Table of Contents

Question 1..................................................................................................................................2

Question 2..................................................................................................................................9

Question 3................................................................................................................................12

Question 4................................................................................................................................16

Question 5................................................................................................................................21

Reference..................................................................................................................................24

Name

Student ID Page 1

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

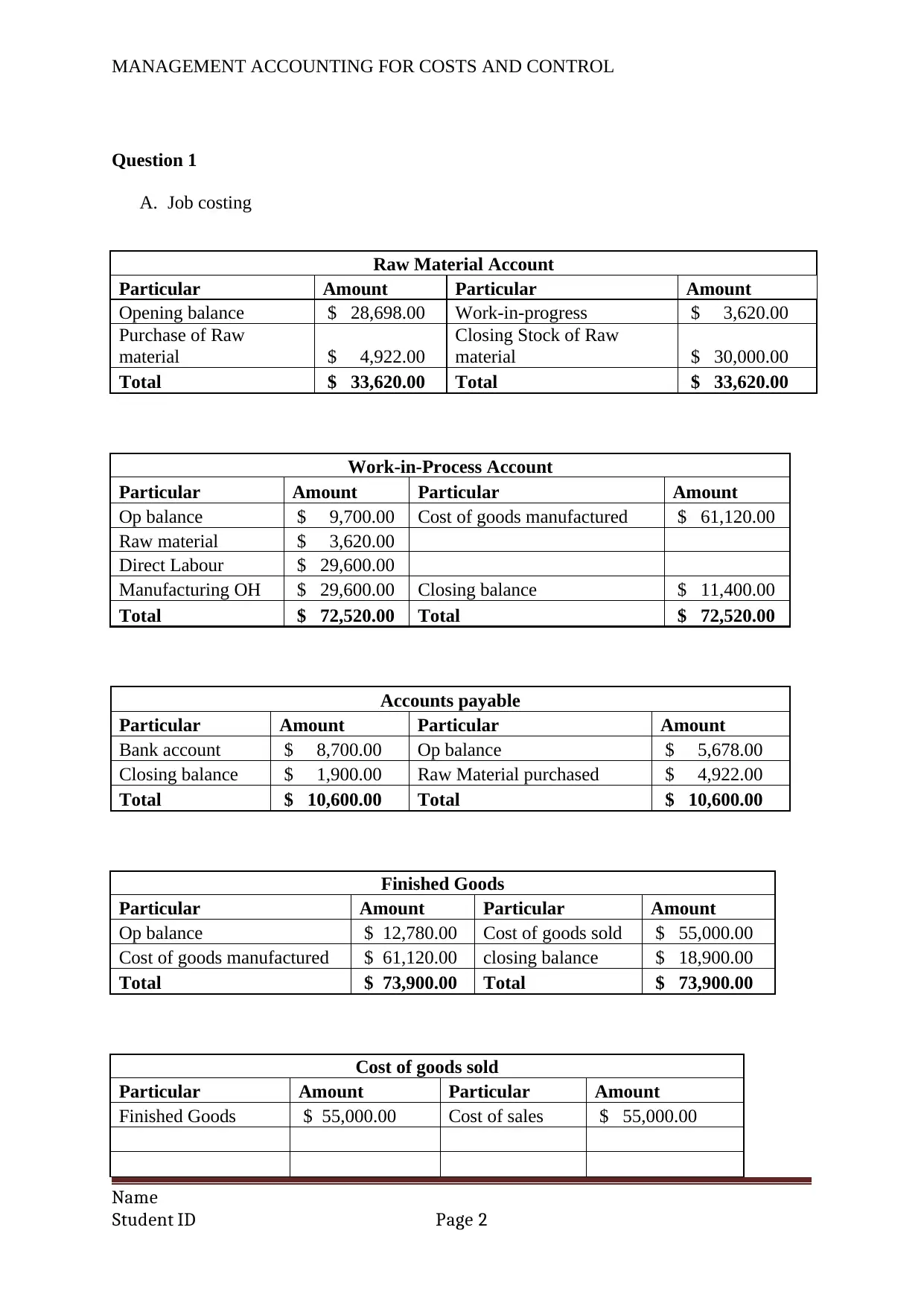

Question 1

A. Job costing

Raw Material Account

Particular Amount Particular Amount

Opening balance $ 28,698.00 Work-in-progress $ 3,620.00

Purchase of Raw

material $ 4,922.00

Closing Stock of Raw

material $ 30,000.00

Total $ 33,620.00 Total $ 33,620.00

Work-in-Process Account

Particular Amount Particular Amount

Op balance $ 9,700.00 Cost of goods manufactured $ 61,120.00

Raw material $ 3,620.00

Direct Labour $ 29,600.00

Manufacturing OH $ 29,600.00 Closing balance $ 11,400.00

Total $ 72,520.00 Total $ 72,520.00

Accounts payable

Particular Amount Particular Amount

Bank account $ 8,700.00 Op balance $ 5,678.00

Closing balance $ 1,900.00 Raw Material purchased $ 4,922.00

Total $ 10,600.00 Total $ 10,600.00

Finished Goods

Particular Amount Particular Amount

Op balance $ 12,780.00 Cost of goods sold $ 55,000.00

Cost of goods manufactured $ 61,120.00 closing balance $ 18,900.00

Total $ 73,900.00 Total $ 73,900.00

Cost of goods sold

Particular Amount Particular Amount

Finished Goods $ 55,000.00 Cost of sales $ 55,000.00

Name

Student ID Page 2

Question 1

A. Job costing

Raw Material Account

Particular Amount Particular Amount

Opening balance $ 28,698.00 Work-in-progress $ 3,620.00

Purchase of Raw

material $ 4,922.00

Closing Stock of Raw

material $ 30,000.00

Total $ 33,620.00 Total $ 33,620.00

Work-in-Process Account

Particular Amount Particular Amount

Op balance $ 9,700.00 Cost of goods manufactured $ 61,120.00

Raw material $ 3,620.00

Direct Labour $ 29,600.00

Manufacturing OH $ 29,600.00 Closing balance $ 11,400.00

Total $ 72,520.00 Total $ 72,520.00

Accounts payable

Particular Amount Particular Amount

Bank account $ 8,700.00 Op balance $ 5,678.00

Closing balance $ 1,900.00 Raw Material purchased $ 4,922.00

Total $ 10,600.00 Total $ 10,600.00

Finished Goods

Particular Amount Particular Amount

Op balance $ 12,780.00 Cost of goods sold $ 55,000.00

Cost of goods manufactured $ 61,120.00 closing balance $ 18,900.00

Total $ 73,900.00 Total $ 73,900.00

Cost of goods sold

Particular Amount Particular Amount

Finished Goods $ 55,000.00 Cost of sales $ 55,000.00

Name

Student ID Page 2

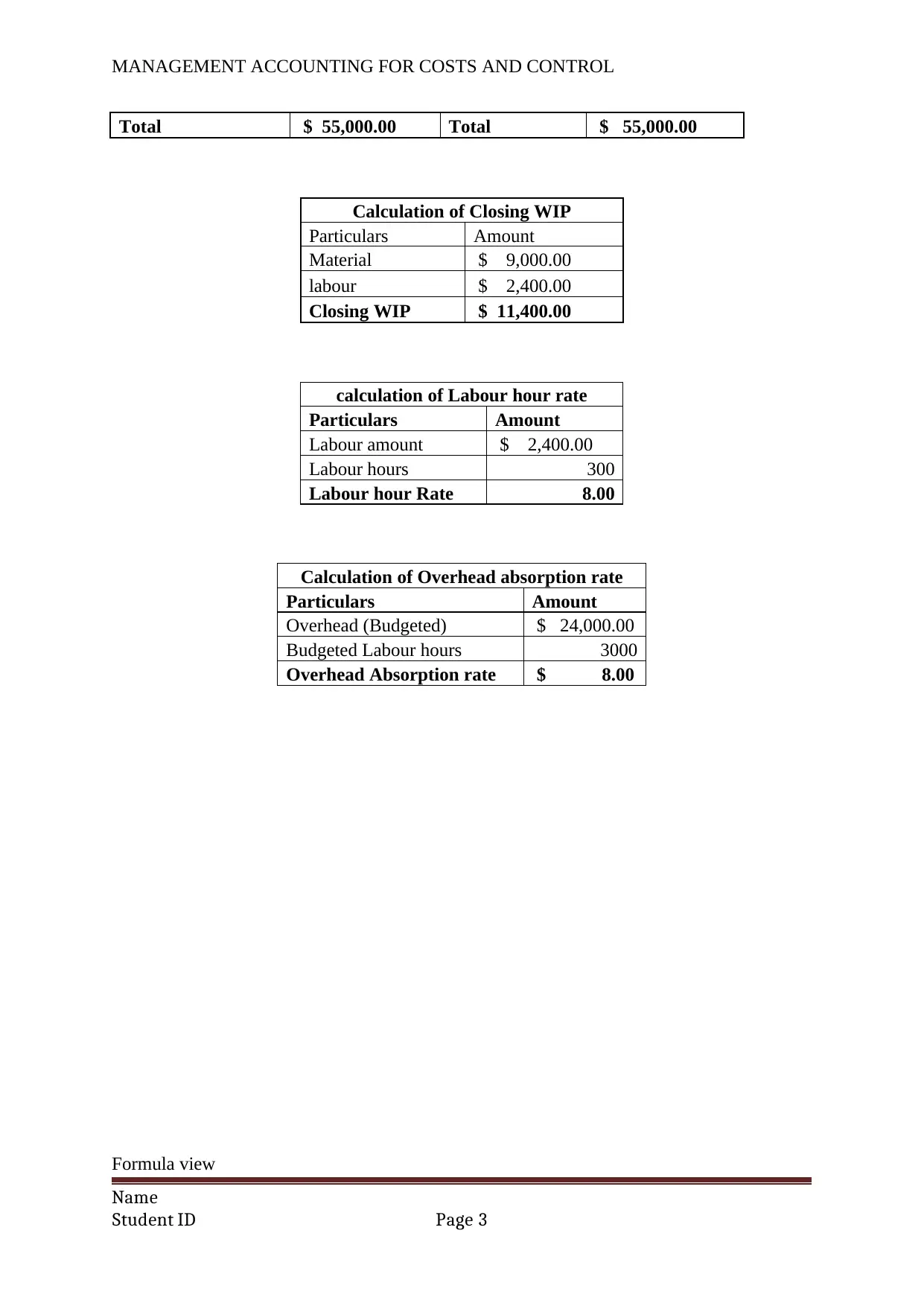

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

Total $ 55,000.00 Total $ 55,000.00

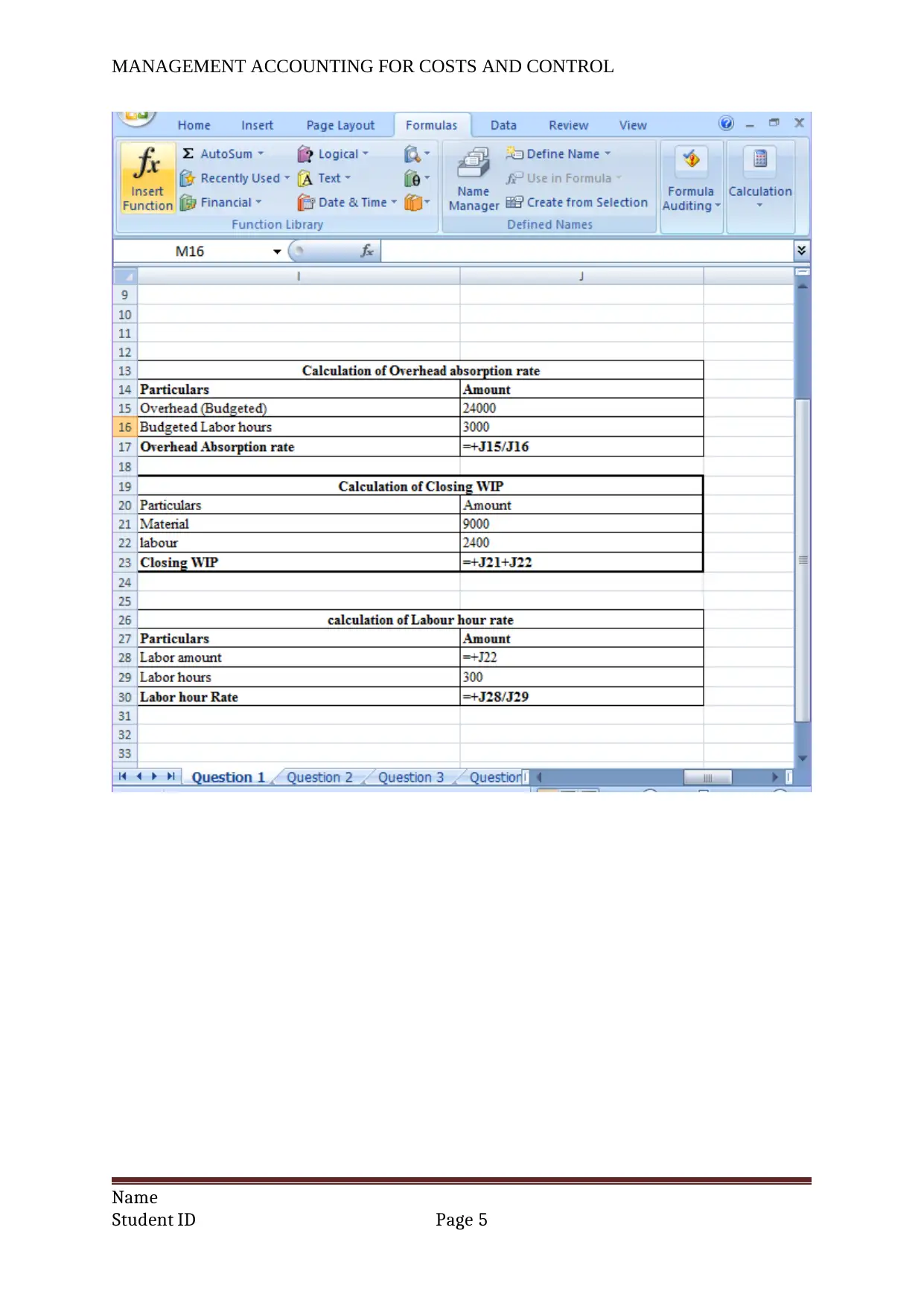

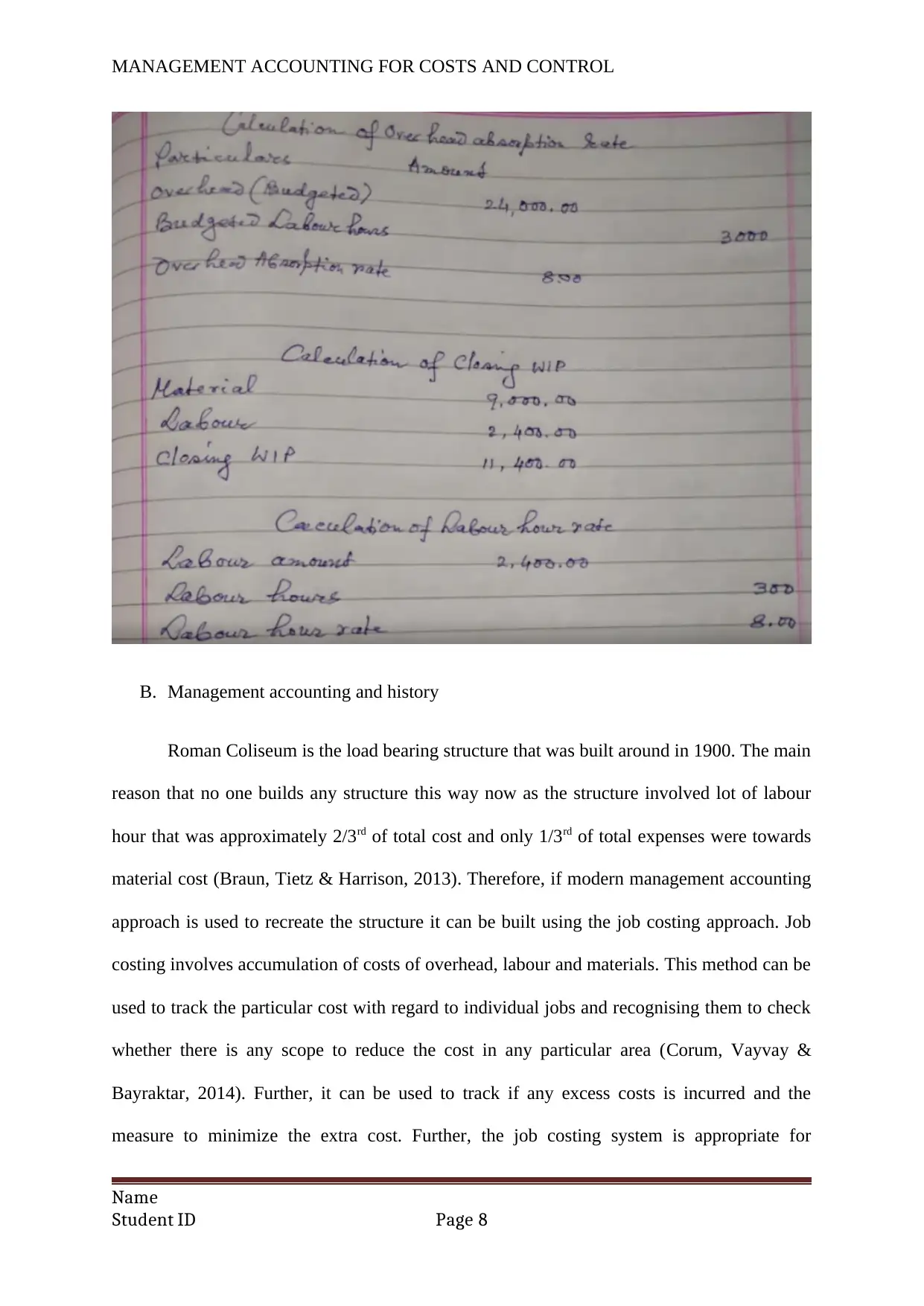

Calculation of Closing WIP

Particulars Amount

Material $ 9,000.00

labour $ 2,400.00

Closing WIP $ 11,400.00

calculation of Labour hour rate

Particulars Amount

Labour amount $ 2,400.00

Labour hours 300

Labour hour Rate 8.00

Calculation of Overhead absorption rate

Particulars Amount

Overhead (Budgeted) $ 24,000.00

Budgeted Labour hours 3000

Overhead Absorption rate $ 8.00

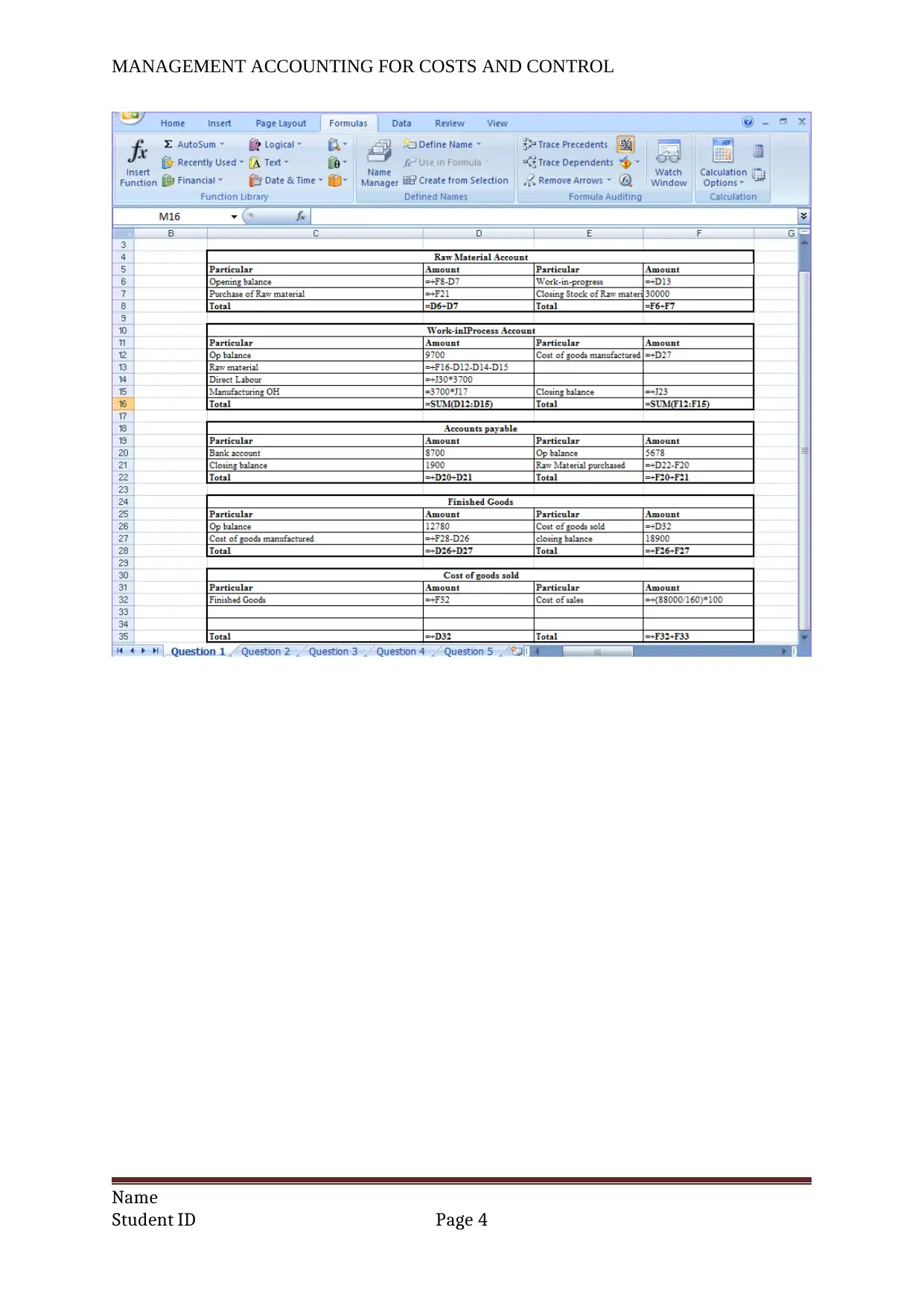

Formula view

Name

Student ID Page 3

Total $ 55,000.00 Total $ 55,000.00

Calculation of Closing WIP

Particulars Amount

Material $ 9,000.00

labour $ 2,400.00

Closing WIP $ 11,400.00

calculation of Labour hour rate

Particulars Amount

Labour amount $ 2,400.00

Labour hours 300

Labour hour Rate 8.00

Calculation of Overhead absorption rate

Particulars Amount

Overhead (Budgeted) $ 24,000.00

Budgeted Labour hours 3000

Overhead Absorption rate $ 8.00

Formula view

Name

Student ID Page 3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

Name

Student ID Page 4

Name

Student ID Page 4

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

Name

Student ID Page 5

Name

Student ID Page 5

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

Name

Student ID Page 6

Name

Student ID Page 6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

Manual solution –

Name

Student ID Page 7

Manual solution –

Name

Student ID Page 7

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

B. Management accounting and history

Roman Coliseum is the load bearing structure that was built around in 1900. The main

reason that no one builds any structure this way now as the structure involved lot of labour

hour that was approximately 2/3rd of total cost and only 1/3rd of total expenses were towards

material cost (Braun, Tietz & Harrison, 2013). Therefore, if modern management accounting

approach is used to recreate the structure it can be built using the job costing approach. Job

costing involves accumulation of costs of overhead, labour and materials. This method can be

used to track the particular cost with regard to individual jobs and recognising them to check

whether there is any scope to reduce the cost in any particular area (Corum, Vayvay &

Bayraktar, 2014). Further, it can be used to track if any excess costs is incurred and the

measure to minimize the extra cost. Further, the job costing system is appropriate for

Name

Student ID Page 8

B. Management accounting and history

Roman Coliseum is the load bearing structure that was built around in 1900. The main

reason that no one builds any structure this way now as the structure involved lot of labour

hour that was approximately 2/3rd of total cost and only 1/3rd of total expenses were towards

material cost (Braun, Tietz & Harrison, 2013). Therefore, if modern management accounting

approach is used to recreate the structure it can be built using the job costing approach. Job

costing involves accumulation of costs of overhead, labour and materials. This method can be

used to track the particular cost with regard to individual jobs and recognising them to check

whether there is any scope to reduce the cost in any particular area (Corum, Vayvay &

Bayraktar, 2014). Further, it can be used to track if any excess costs is incurred and the

measure to minimize the extra cost. Further, the job costing system is appropriate for

Name

Student ID Page 8

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

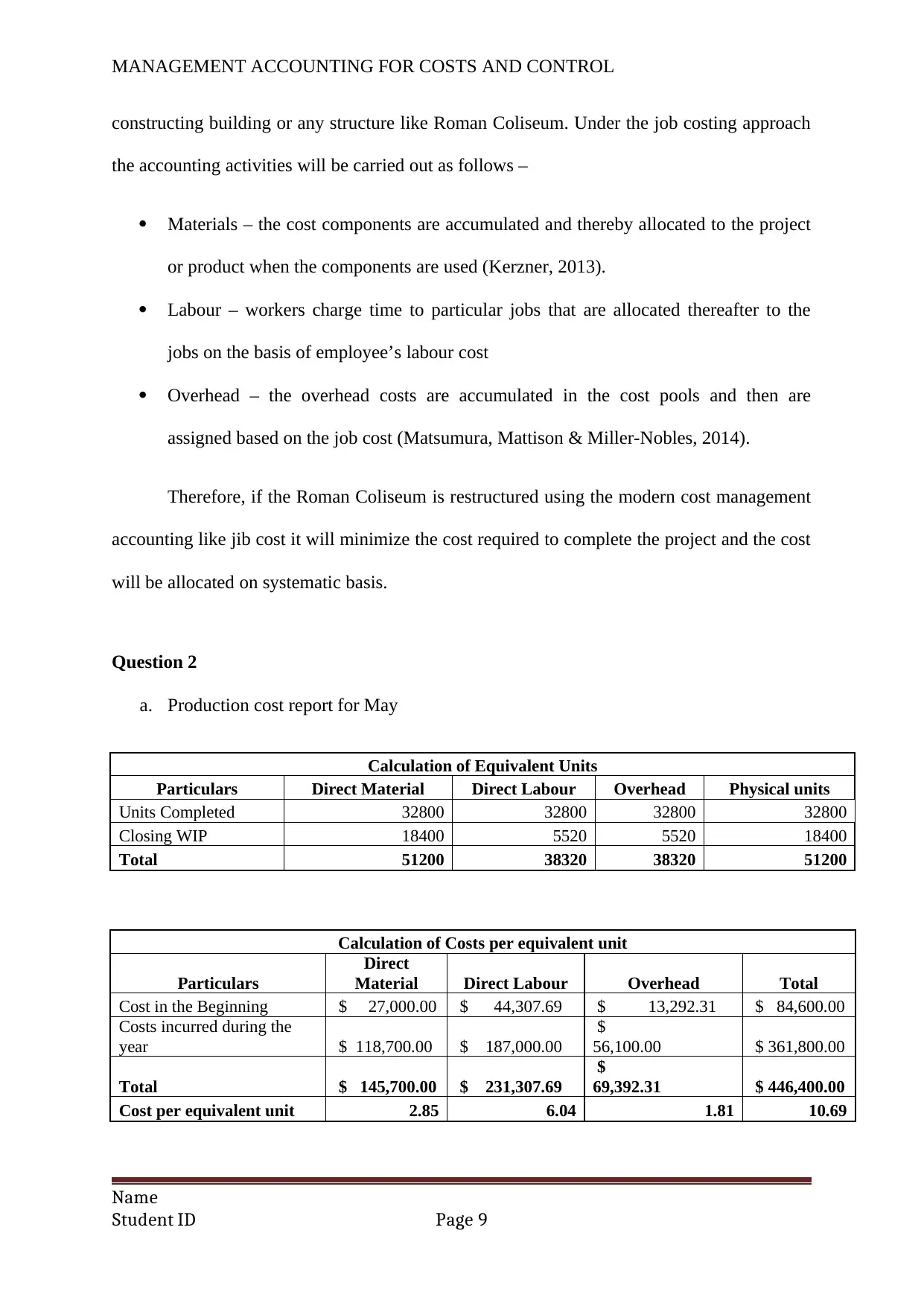

constructing building or any structure like Roman Coliseum. Under the job costing approach

the accounting activities will be carried out as follows –

Materials – the cost components are accumulated and thereby allocated to the project

or product when the components are used (Kerzner, 2013).

Labour – workers charge time to particular jobs that are allocated thereafter to the

jobs on the basis of employee’s labour cost

Overhead – the overhead costs are accumulated in the cost pools and then are

assigned based on the job cost (Matsumura, Mattison & Miller-Nobles, 2014).

Therefore, if the Roman Coliseum is restructured using the modern cost management

accounting like jib cost it will minimize the cost required to complete the project and the cost

will be allocated on systematic basis.

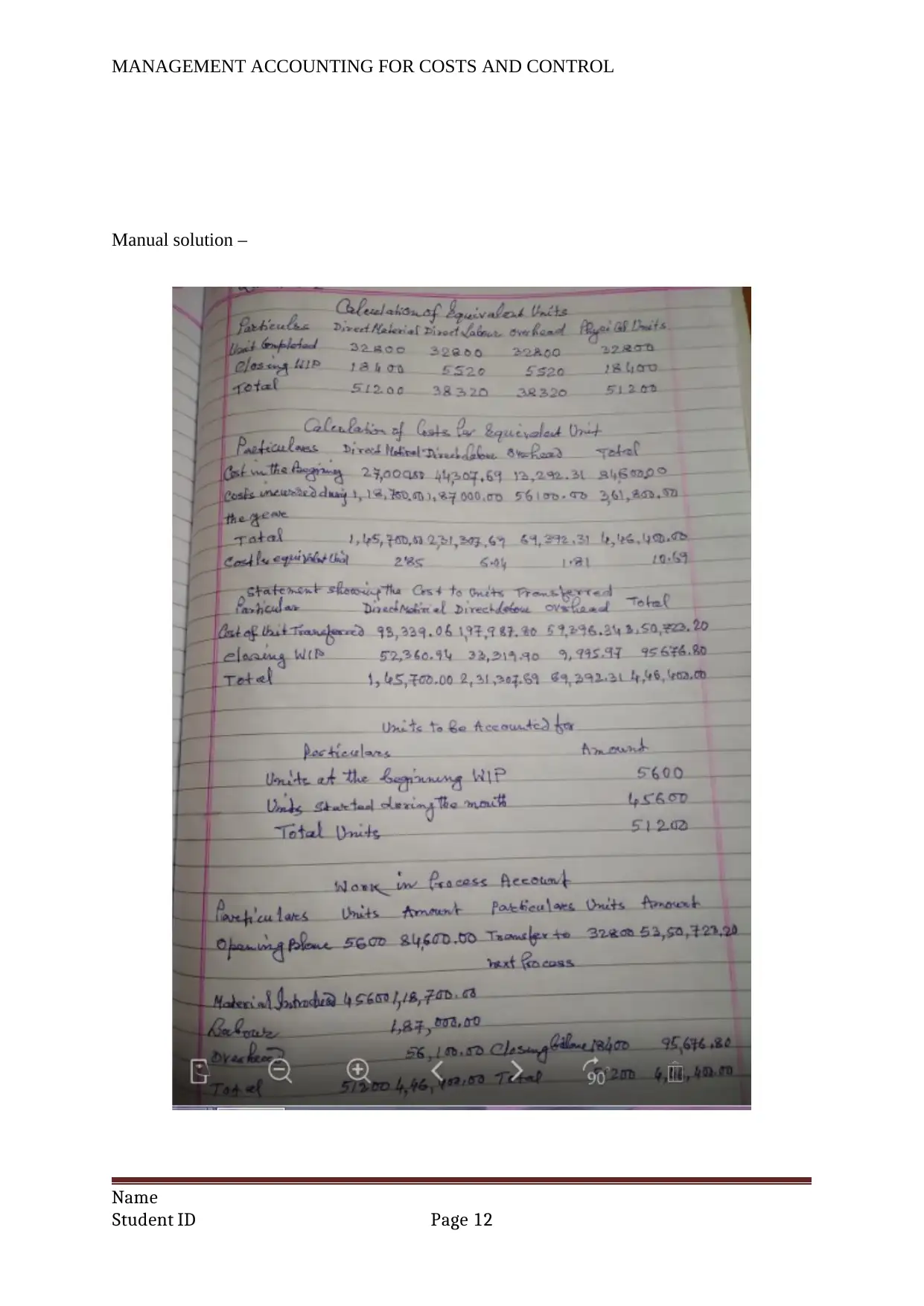

Question 2

a. Production cost report for May

Calculation of Equivalent Units

Particulars Direct Material Direct Labour Overhead Physical units

Units Completed 32800 32800 32800 32800

Closing WIP 18400 5520 5520 18400

Total 51200 38320 38320 51200

Calculation of Costs per equivalent unit

Particulars

Direct

Material Direct Labour Overhead Total

Cost in the Beginning $ 27,000.00 $ 44,307.69 $ 13,292.31 $ 84,600.00

Costs incurred during the

year $ 118,700.00 $ 187,000.00

$

56,100.00 $ 361,800.00

Total $ 145,700.00 $ 231,307.69

$

69,392.31 $ 446,400.00

Cost per equivalent unit 2.85 6.04 1.81 10.69

Name

Student ID Page 9

constructing building or any structure like Roman Coliseum. Under the job costing approach

the accounting activities will be carried out as follows –

Materials – the cost components are accumulated and thereby allocated to the project

or product when the components are used (Kerzner, 2013).

Labour – workers charge time to particular jobs that are allocated thereafter to the

jobs on the basis of employee’s labour cost

Overhead – the overhead costs are accumulated in the cost pools and then are

assigned based on the job cost (Matsumura, Mattison & Miller-Nobles, 2014).

Therefore, if the Roman Coliseum is restructured using the modern cost management

accounting like jib cost it will minimize the cost required to complete the project and the cost

will be allocated on systematic basis.

Question 2

a. Production cost report for May

Calculation of Equivalent Units

Particulars Direct Material Direct Labour Overhead Physical units

Units Completed 32800 32800 32800 32800

Closing WIP 18400 5520 5520 18400

Total 51200 38320 38320 51200

Calculation of Costs per equivalent unit

Particulars

Direct

Material Direct Labour Overhead Total

Cost in the Beginning $ 27,000.00 $ 44,307.69 $ 13,292.31 $ 84,600.00

Costs incurred during the

year $ 118,700.00 $ 187,000.00

$

56,100.00 $ 361,800.00

Total $ 145,700.00 $ 231,307.69

$

69,392.31 $ 446,400.00

Cost per equivalent unit 2.85 6.04 1.81 10.69

Name

Student ID Page 9

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

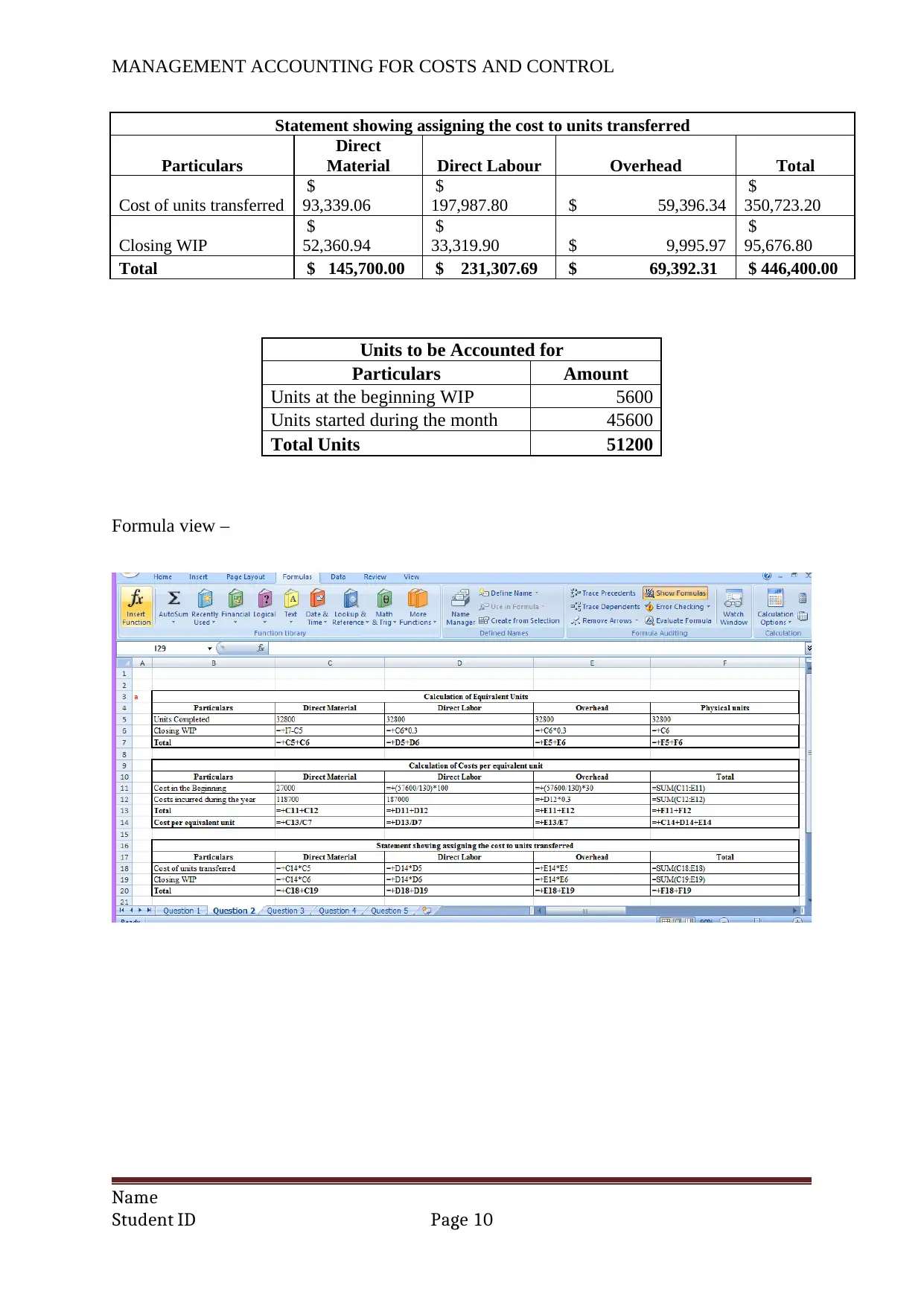

Statement showing assigning the cost to units transferred

Particulars

Direct

Material Direct Labour Overhead Total

Cost of units transferred

$

93,339.06

$

197,987.80 $ 59,396.34

$

350,723.20

Closing WIP

$

52,360.94

$

33,319.90 $ 9,995.97

$

95,676.80

Total $ 145,700.00 $ 231,307.69 $ 69,392.31 $ 446,400.00

Units to be Accounted for

Particulars Amount

Units at the beginning WIP 5600

Units started during the month 45600

Total Units 51200

Formula view –

Name

Student ID Page 10

Statement showing assigning the cost to units transferred

Particulars

Direct

Material Direct Labour Overhead Total

Cost of units transferred

$

93,339.06

$

197,987.80 $ 59,396.34

$

350,723.20

Closing WIP

$

52,360.94

$

33,319.90 $ 9,995.97

$

95,676.80

Total $ 145,700.00 $ 231,307.69 $ 69,392.31 $ 446,400.00

Units to be Accounted for

Particulars Amount

Units at the beginning WIP 5600

Units started during the month 45600

Total Units 51200

Formula view –

Name

Student ID Page 10

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

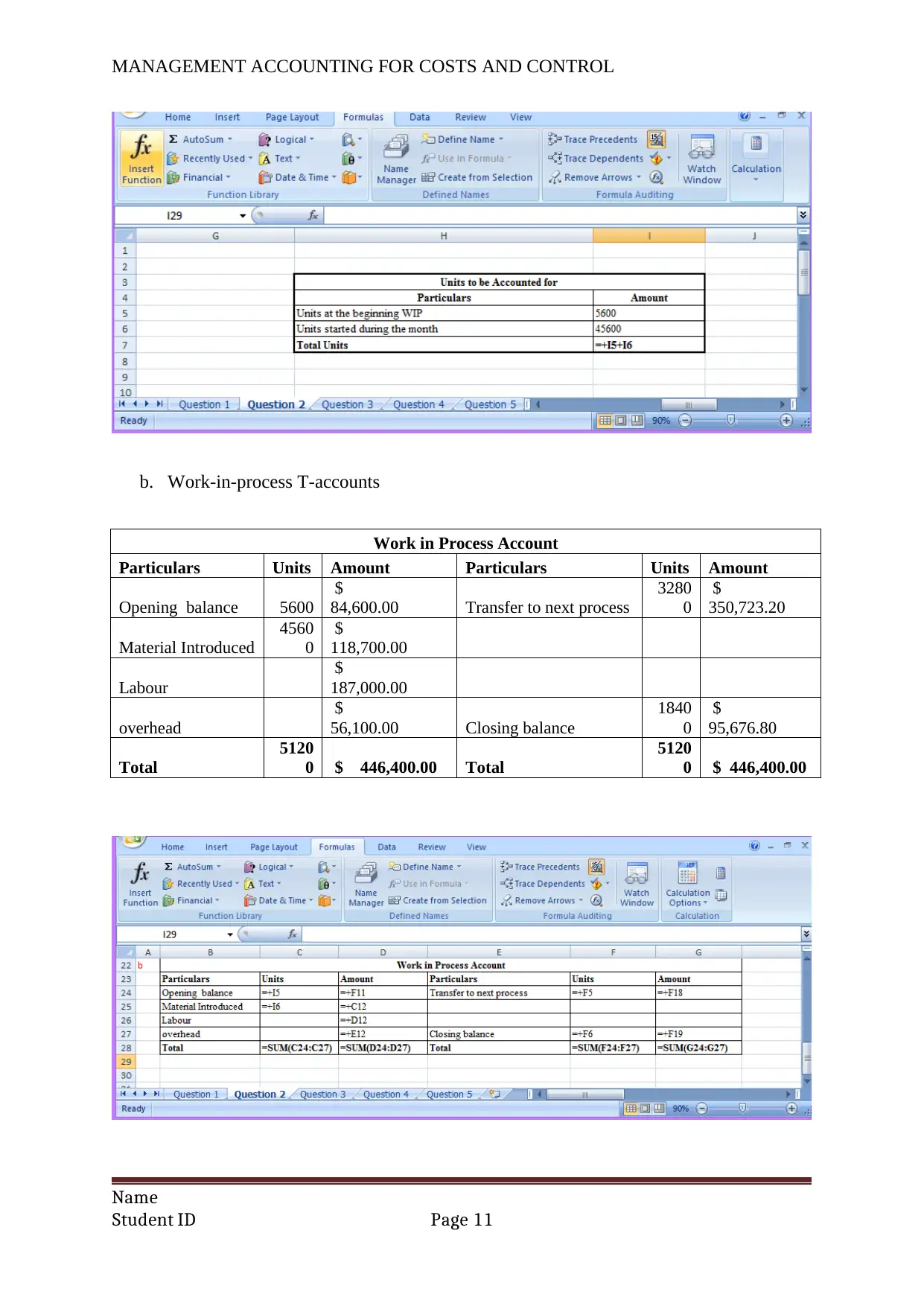

b. Work-in-process T-accounts

Work in Process Account

Particulars Units Amount Particulars Units Amount

Opening balance 5600

$

84,600.00 Transfer to next process

3280

0

$

350,723.20

Material Introduced

4560

0

$

118,700.00

Labour

$

187,000.00

overhead

$

56,100.00 Closing balance

1840

0

$

95,676.80

Total

5120

0 $ 446,400.00 Total

5120

0 $ 446,400.00

Name

Student ID Page 11

b. Work-in-process T-accounts

Work in Process Account

Particulars Units Amount Particulars Units Amount

Opening balance 5600

$

84,600.00 Transfer to next process

3280

0

$

350,723.20

Material Introduced

4560

0

$

118,700.00

Labour

$

187,000.00

overhead

$

56,100.00 Closing balance

1840

0

$

95,676.80

Total

5120

0 $ 446,400.00 Total

5120

0 $ 446,400.00

Name

Student ID Page 11

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

Manual solution –

Name

Student ID Page 12

Manual solution –

Name

Student ID Page 12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

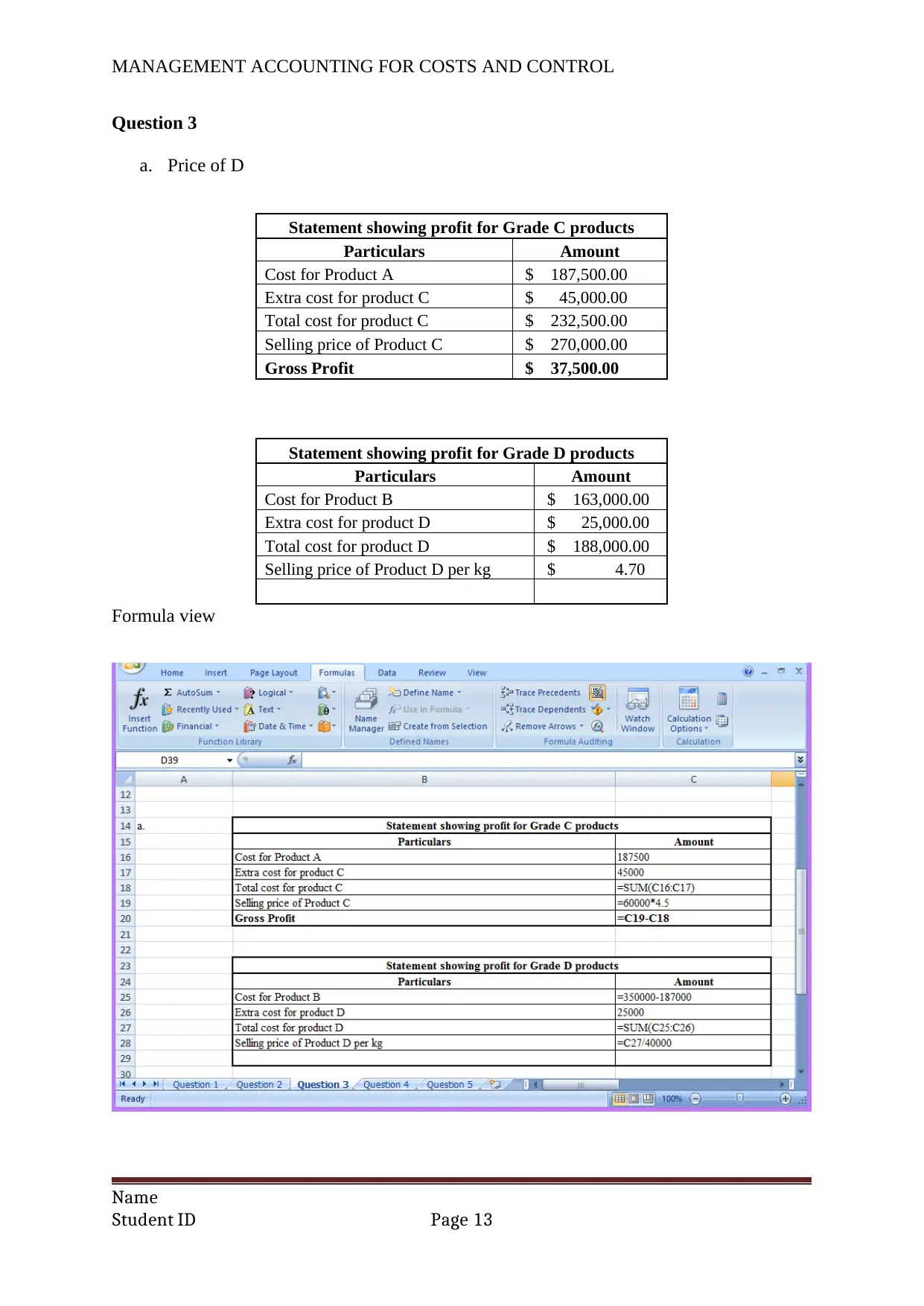

Question 3

a. Price of D

Statement showing profit for Grade C products

Particulars Amount

Cost for Product A $ 187,500.00

Extra cost for product C $ 45,000.00

Total cost for product C $ 232,500.00

Selling price of Product C $ 270,000.00

Gross Profit $ 37,500.00

Statement showing profit for Grade D products

Particulars Amount

Cost for Product B $ 163,000.00

Extra cost for product D $ 25,000.00

Total cost for product D $ 188,000.00

Selling price of Product D per kg $ 4.70

Formula view

Name

Student ID Page 13

Question 3

a. Price of D

Statement showing profit for Grade C products

Particulars Amount

Cost for Product A $ 187,500.00

Extra cost for product C $ 45,000.00

Total cost for product C $ 232,500.00

Selling price of Product C $ 270,000.00

Gross Profit $ 37,500.00

Statement showing profit for Grade D products

Particulars Amount

Cost for Product B $ 163,000.00

Extra cost for product D $ 25,000.00

Total cost for product D $ 188,000.00

Selling price of Product D per kg $ 4.70

Formula view

Name

Student ID Page 13

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

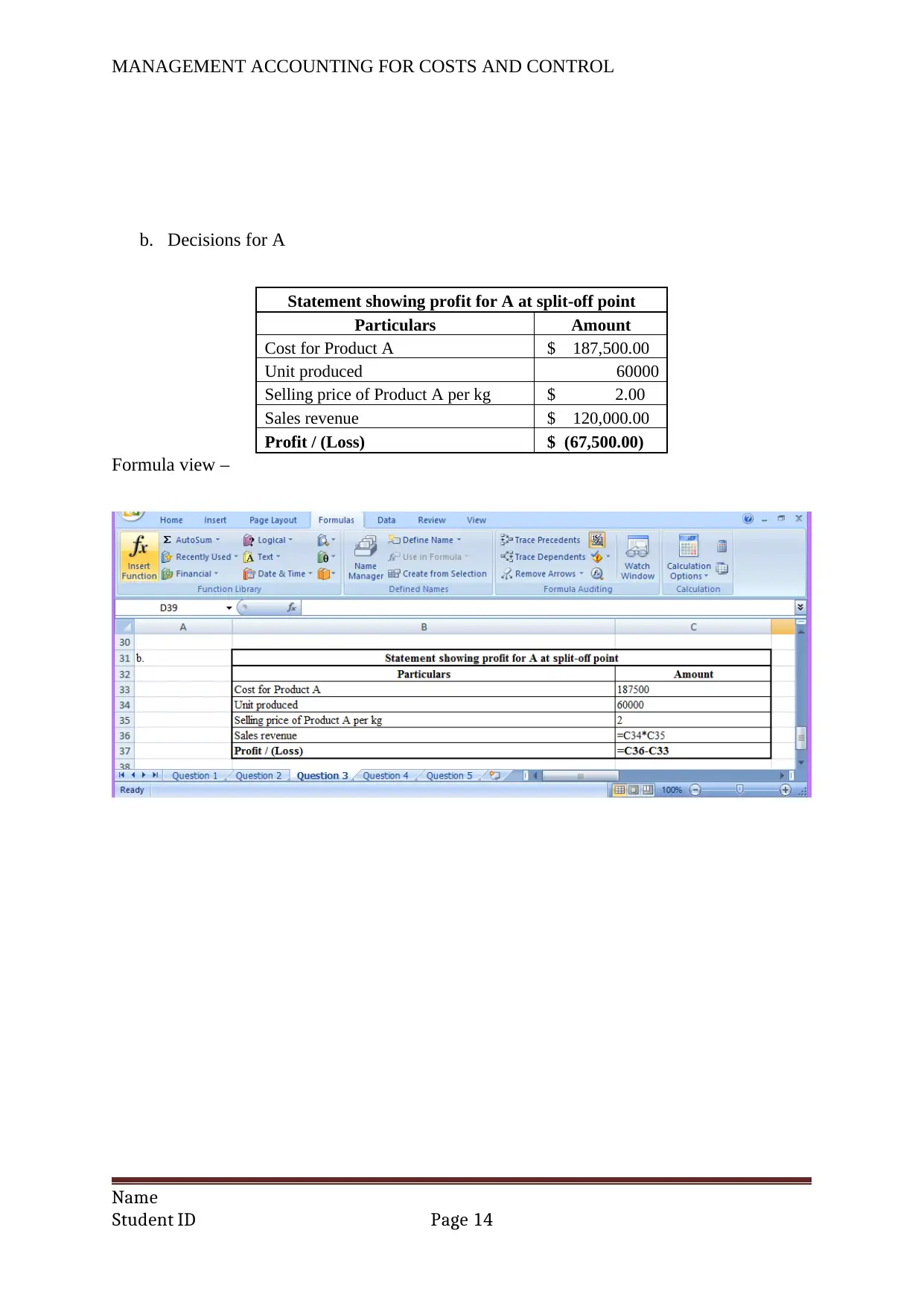

b. Decisions for A

Statement showing profit for A at split-off point

Particulars Amount

Cost for Product A $ 187,500.00

Unit produced 60000

Selling price of Product A per kg $ 2.00

Sales revenue $ 120,000.00

Profit / (Loss) $ (67,500.00)

Formula view –

Name

Student ID Page 14

b. Decisions for A

Statement showing profit for A at split-off point

Particulars Amount

Cost for Product A $ 187,500.00

Unit produced 60000

Selling price of Product A per kg $ 2.00

Sales revenue $ 120,000.00

Profit / (Loss) $ (67,500.00)

Formula view –

Name

Student ID Page 14

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

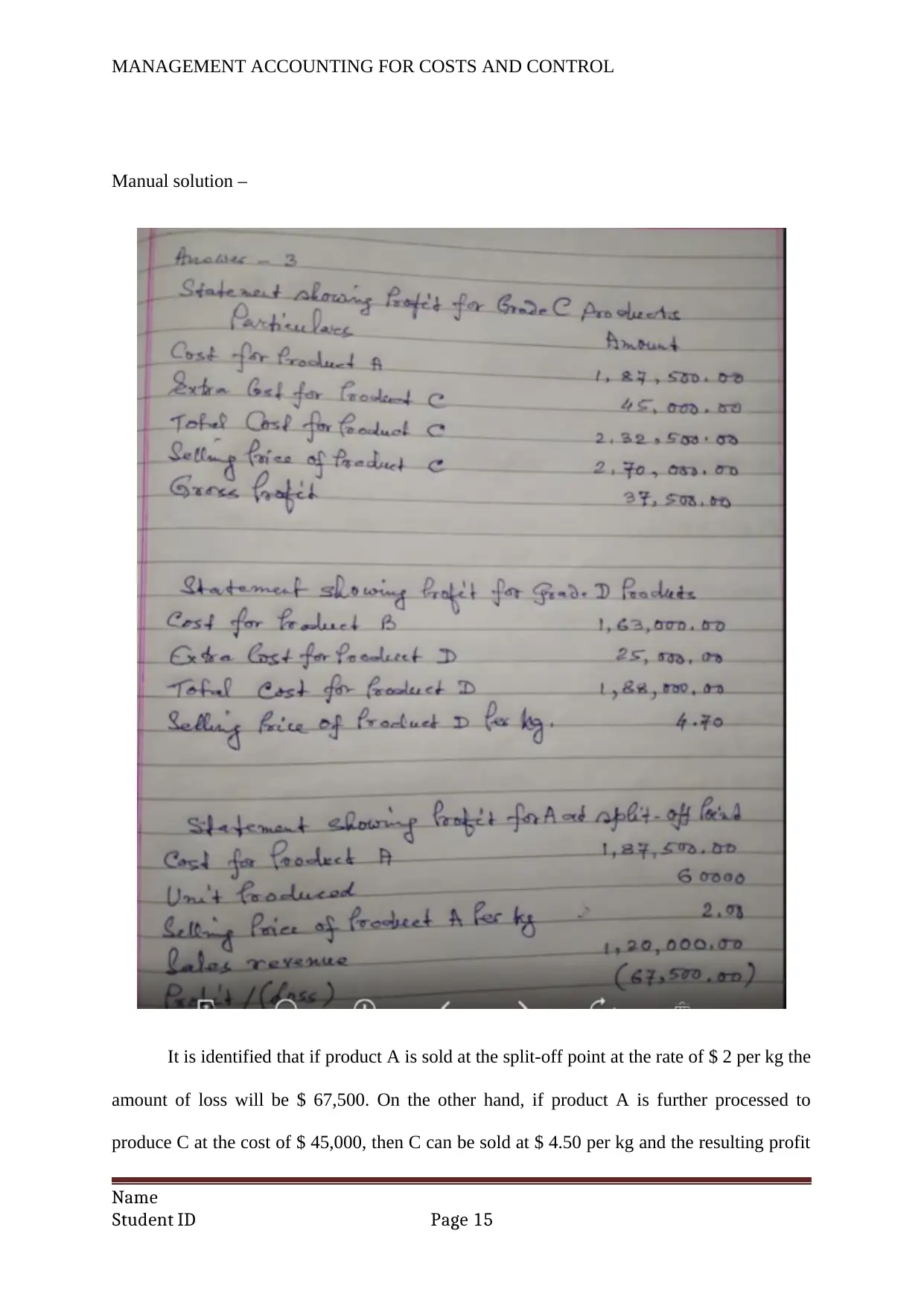

Manual solution –

It is identified that if product A is sold at the split-off point at the rate of $ 2 per kg the

amount of loss will be $ 67,500. On the other hand, if product A is further processed to

produce C at the cost of $ 45,000, then C can be sold at $ 4.50 per kg and the resulting profit

Name

Student ID Page 15

Manual solution –

It is identified that if product A is sold at the split-off point at the rate of $ 2 per kg the

amount of loss will be $ 67,500. On the other hand, if product A is further processed to

produce C at the cost of $ 45,000, then C can be sold at $ 4.50 per kg and the resulting profit

Name

Student ID Page 15

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

will be $ 37,500. Therefore, the difference in profit will be = 37,500 – (- 67,500) = $ 105,000.

Hence, product A shall be further processed to produce product C and shall not be sold at

split-off point.

Question 4

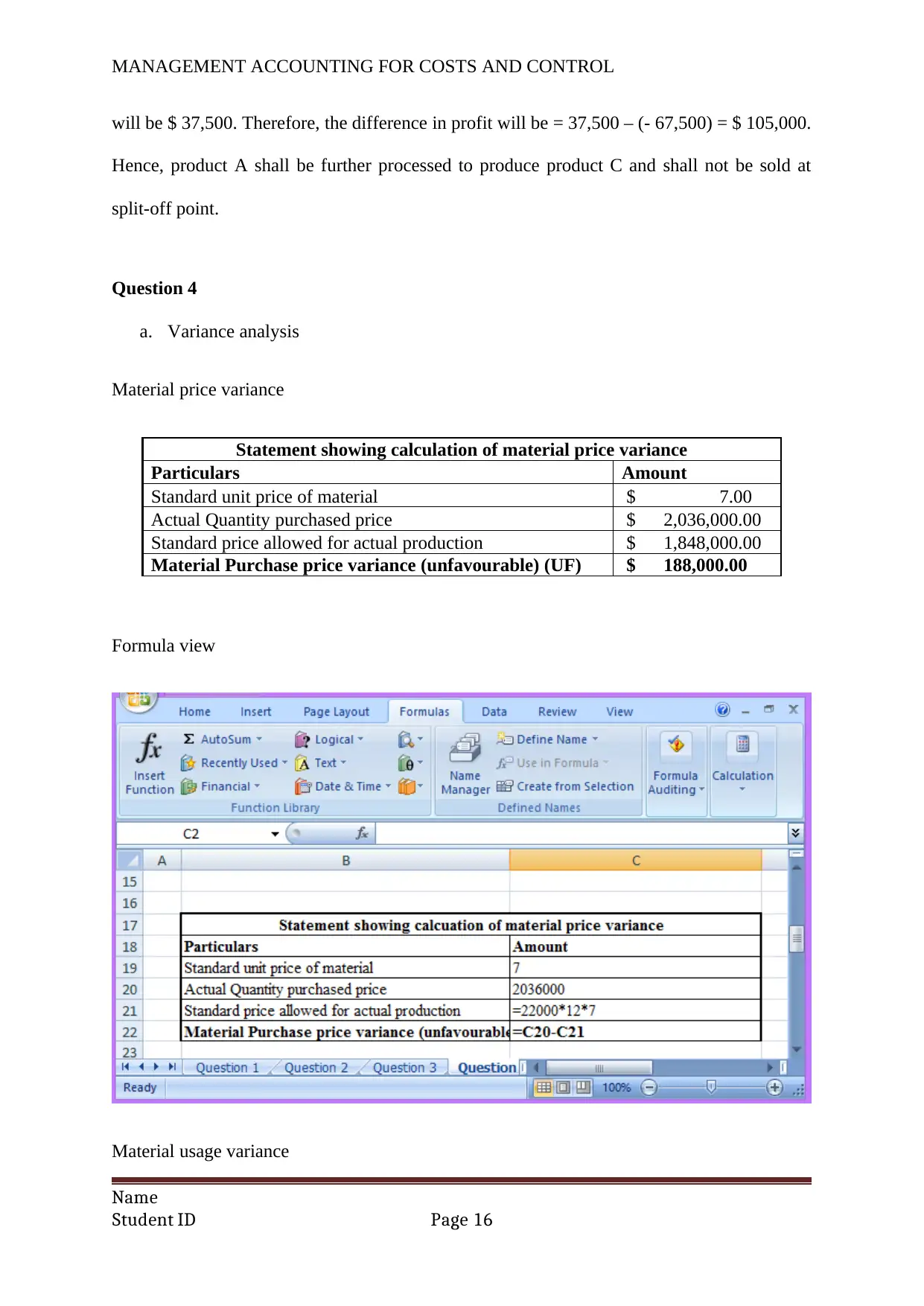

a. Variance analysis

Material price variance

Statement showing calculation of material price variance

Particulars Amount

Standard unit price of material $ 7.00

Actual Quantity purchased price $ 2,036,000.00

Standard price allowed for actual production $ 1,848,000.00

Material Purchase price variance (unfavourable) (UF) $ 188,000.00

Formula view

Material usage variance

Name

Student ID Page 16

will be $ 37,500. Therefore, the difference in profit will be = 37,500 – (- 67,500) = $ 105,000.

Hence, product A shall be further processed to produce product C and shall not be sold at

split-off point.

Question 4

a. Variance analysis

Material price variance

Statement showing calculation of material price variance

Particulars Amount

Standard unit price of material $ 7.00

Actual Quantity purchased price $ 2,036,000.00

Standard price allowed for actual production $ 1,848,000.00

Material Purchase price variance (unfavourable) (UF) $ 188,000.00

Formula view

Material usage variance

Name

Student ID Page 16

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

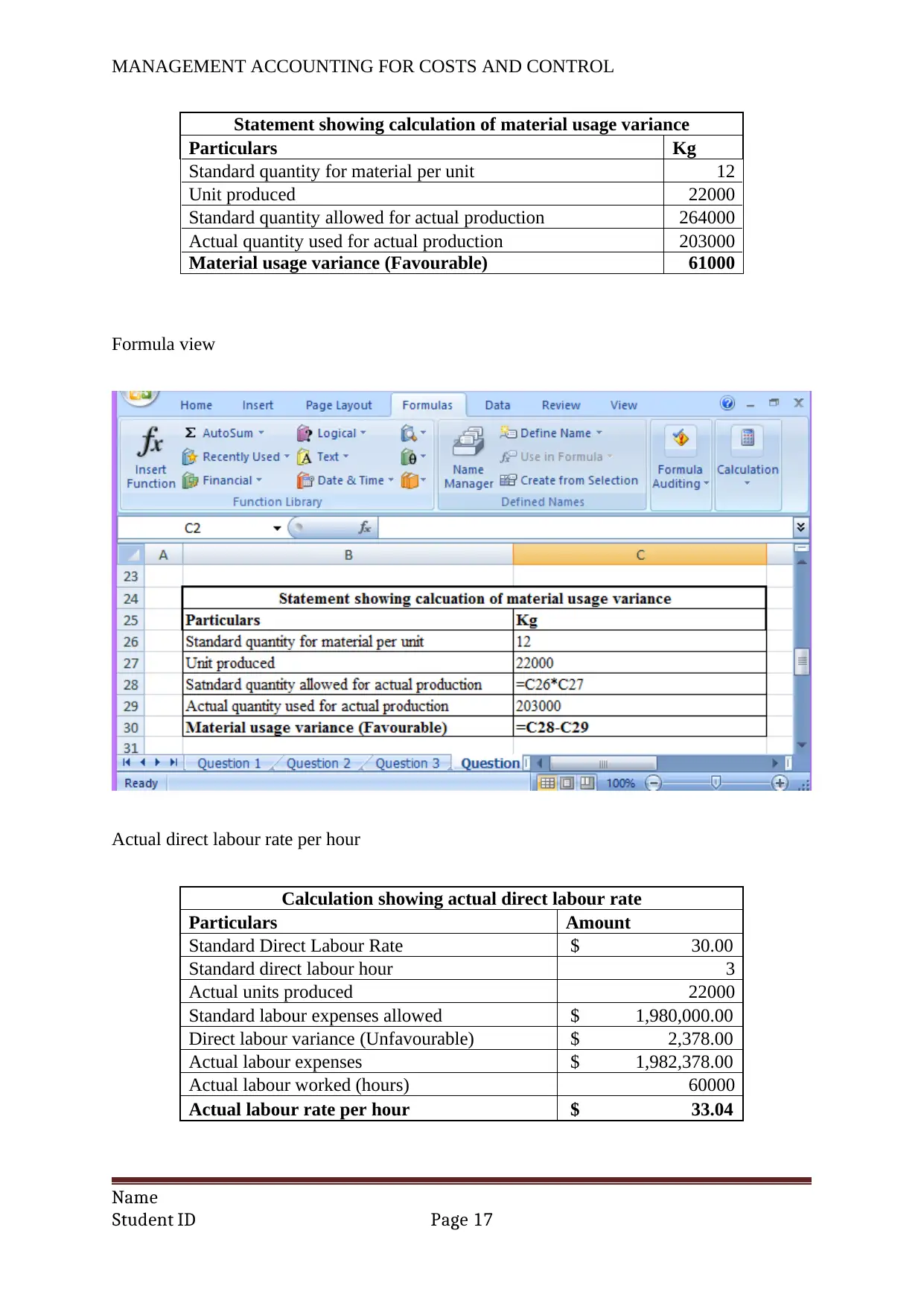

Statement showing calculation of material usage variance

Particulars Kg

Standard quantity for material per unit 12

Unit produced 22000

Standard quantity allowed for actual production 264000

Actual quantity used for actual production 203000

Material usage variance (Favourable) 61000

Formula view

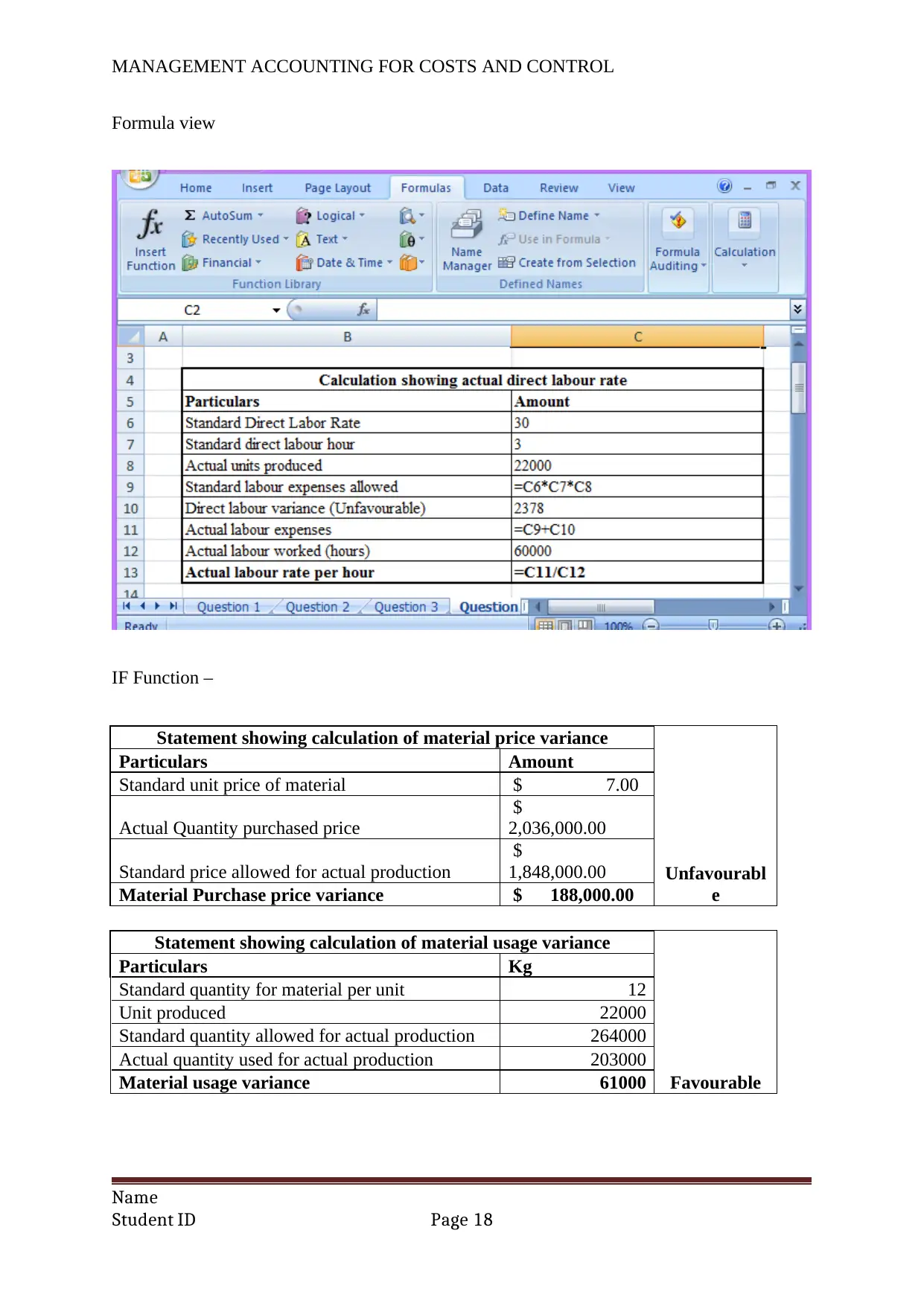

Actual direct labour rate per hour

Calculation showing actual direct labour rate

Particulars Amount

Standard Direct Labour Rate $ 30.00

Standard direct labour hour 3

Actual units produced 22000

Standard labour expenses allowed $ 1,980,000.00

Direct labour variance (Unfavourable) $ 2,378.00

Actual labour expenses $ 1,982,378.00

Actual labour worked (hours) 60000

Actual labour rate per hour $ 33.04

Name

Student ID Page 17

Statement showing calculation of material usage variance

Particulars Kg

Standard quantity for material per unit 12

Unit produced 22000

Standard quantity allowed for actual production 264000

Actual quantity used for actual production 203000

Material usage variance (Favourable) 61000

Formula view

Actual direct labour rate per hour

Calculation showing actual direct labour rate

Particulars Amount

Standard Direct Labour Rate $ 30.00

Standard direct labour hour 3

Actual units produced 22000

Standard labour expenses allowed $ 1,980,000.00

Direct labour variance (Unfavourable) $ 2,378.00

Actual labour expenses $ 1,982,378.00

Actual labour worked (hours) 60000

Actual labour rate per hour $ 33.04

Name

Student ID Page 17

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

Formula view

IF Function –

Statement showing calculation of material price variance

Unfavourabl

e

Particulars Amount

Standard unit price of material $ 7.00

Actual Quantity purchased price

$

2,036,000.00

Standard price allowed for actual production

$

1,848,000.00

Material Purchase price variance $ 188,000.00

Statement showing calculation of material usage variance

Favourable

Particulars Kg

Standard quantity for material per unit 12

Unit produced 22000

Standard quantity allowed for actual production 264000

Actual quantity used for actual production 203000

Material usage variance 61000

Name

Student ID Page 18

Formula view

IF Function –

Statement showing calculation of material price variance

Unfavourabl

e

Particulars Amount

Standard unit price of material $ 7.00

Actual Quantity purchased price

$

2,036,000.00

Standard price allowed for actual production

$

1,848,000.00

Material Purchase price variance $ 188,000.00

Statement showing calculation of material usage variance

Favourable

Particulars Kg

Standard quantity for material per unit 12

Unit produced 22000

Standard quantity allowed for actual production 264000

Actual quantity used for actual production 203000

Material usage variance 61000

Name

Student ID Page 18

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

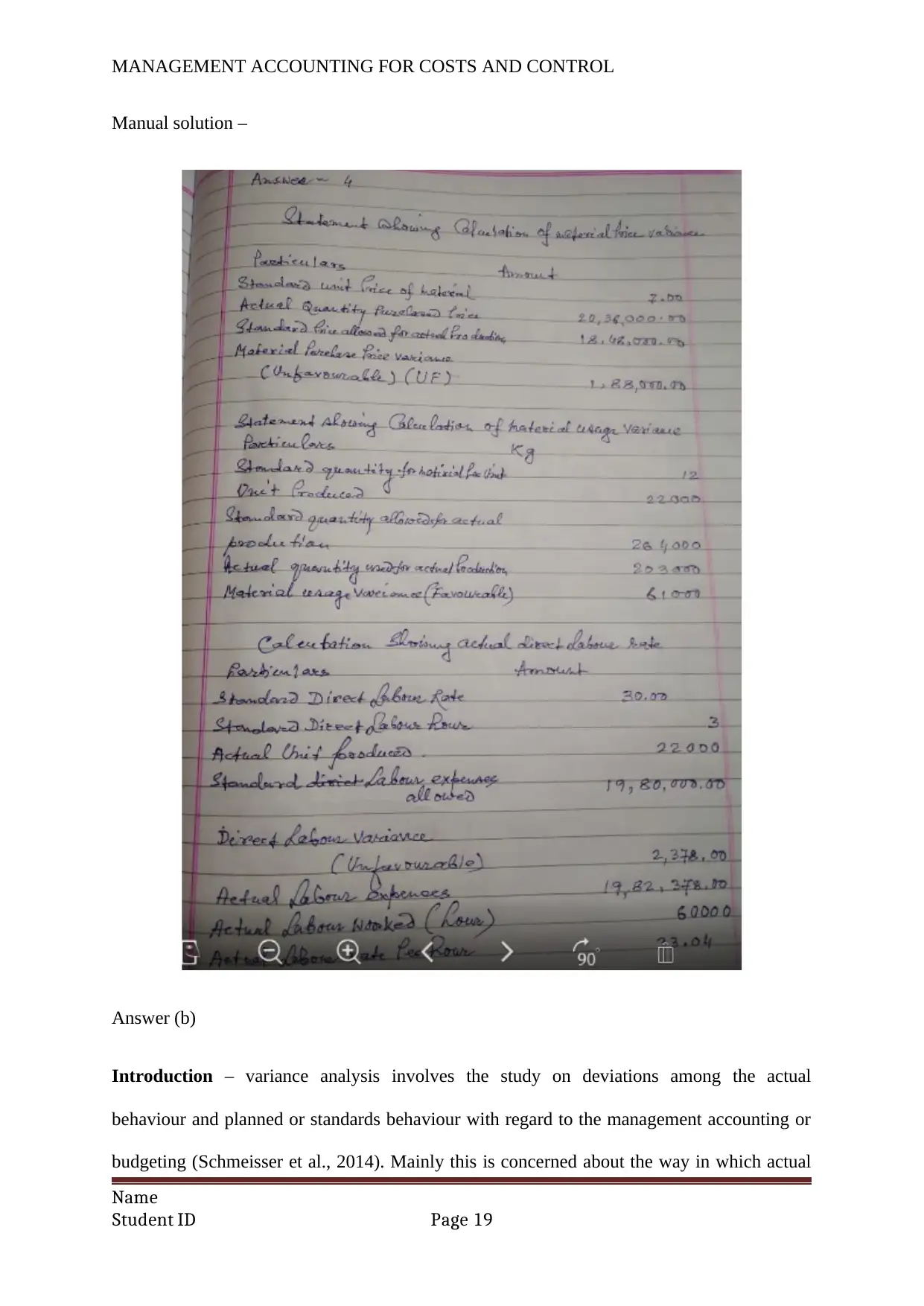

Manual solution –

Answer (b)

Introduction – variance analysis involves the study on deviations among the actual

behaviour and planned or standards behaviour with regard to the management accounting or

budgeting (Schmeisser et al., 2014). Mainly this is concerned about the way in which actual

Name

Student ID Page 19

Manual solution –

Answer (b)

Introduction – variance analysis involves the study on deviations among the actual

behaviour and planned or standards behaviour with regard to the management accounting or

budgeting (Schmeisser et al., 2014). Mainly this is concerned about the way in which actual

Name

Student ID Page 19

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

and standard behaviour signifies the impact on the performance of the business. The main

objective of variance analysis is to calculate and record individual variances and

understanding the reason behind every variance.

Discussion – variance can be favourable that is the actual costs are lower as compared to

standard costs as well as unfavourable that is the actual costs are higher as compared to the

standard costs (Whitecotton, Libby & Phillips, 2013). Positive as well as negative both the

variances have negative impact on the budget unless it is caused by the extreme events. The

main purposes of variance analysis are as follows –

It helps in preparing efficient budget as the management will prefer to experience

lower level of deviation with the budget (Xia & Walker, 2015). Preferring the lower

deviations will lead the managers to prepare more accurate budgets and take

decisions based on the budget

The variance analysis act as the control mechanism. Analysing the large difference

based on major items will assist in evaluating the causes and it will eventually help

the management to search for the possible methods to minimize the differences

The analysis of variances assists in allocating the responsibility and establishing the

control mechanism on various departments, wherever required. For instance, if it is

found out that the labour efficiency variable is not favourable or the raw material

procurement cost variance is not favourable, the management can improve the control

system to enhance efficiency.

Variance analysis can be used in the financial and operational areas of the business. It

can be used to analyse the variance among the standard and actual budget, forecasting,

materiality and the business planning.

Name

Student ID Page 20

and standard behaviour signifies the impact on the performance of the business. The main

objective of variance analysis is to calculate and record individual variances and

understanding the reason behind every variance.

Discussion – variance can be favourable that is the actual costs are lower as compared to

standard costs as well as unfavourable that is the actual costs are higher as compared to the

standard costs (Whitecotton, Libby & Phillips, 2013). Positive as well as negative both the

variances have negative impact on the budget unless it is caused by the extreme events. The

main purposes of variance analysis are as follows –

It helps in preparing efficient budget as the management will prefer to experience

lower level of deviation with the budget (Xia & Walker, 2015). Preferring the lower

deviations will lead the managers to prepare more accurate budgets and take

decisions based on the budget

The variance analysis act as the control mechanism. Analysing the large difference

based on major items will assist in evaluating the causes and it will eventually help

the management to search for the possible methods to minimize the differences

The analysis of variances assists in allocating the responsibility and establishing the

control mechanism on various departments, wherever required. For instance, if it is

found out that the labour efficiency variable is not favourable or the raw material

procurement cost variance is not favourable, the management can improve the control

system to enhance efficiency.

Variance analysis can be used in the financial and operational areas of the business. It

can be used to analyse the variance among the standard and actual budget, forecasting,

materiality and the business planning.

Name

Student ID Page 20

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

The difference among the incurred overhead and absorbed overhead is known as the

overhead variance. The overhead variance helps in analysing the cost incurred as compared to

the plan. However, it does not provide any scope to pinpoint the reason for the variance and

thus corrective actions are taken as far as possible. It is not possible to recognize whether the

reason behind the overhead variance is the inefficiency of the labours or expenses has been

incurred more or less. Therefore, total variance in overhead cost further analysed into parts to

get an idea regarding the overhead variance from various angles (Maas, Schaltegger &

Crutzen, 2016).

Conclusion – it is identified from the above analysis that the variance analysis under cost

accounting indicates gain or loss. However, it is the loss or gain owing to the actual activity

that is actually planned. It pays important role in analysing the actual expenses as compared

to the plan or budget and thereby makes to management more efficient in controlling costs

and plan the expenses in more efficient and exact way. It further helps in forecasting the costs

and profits for the future years.

Question 5

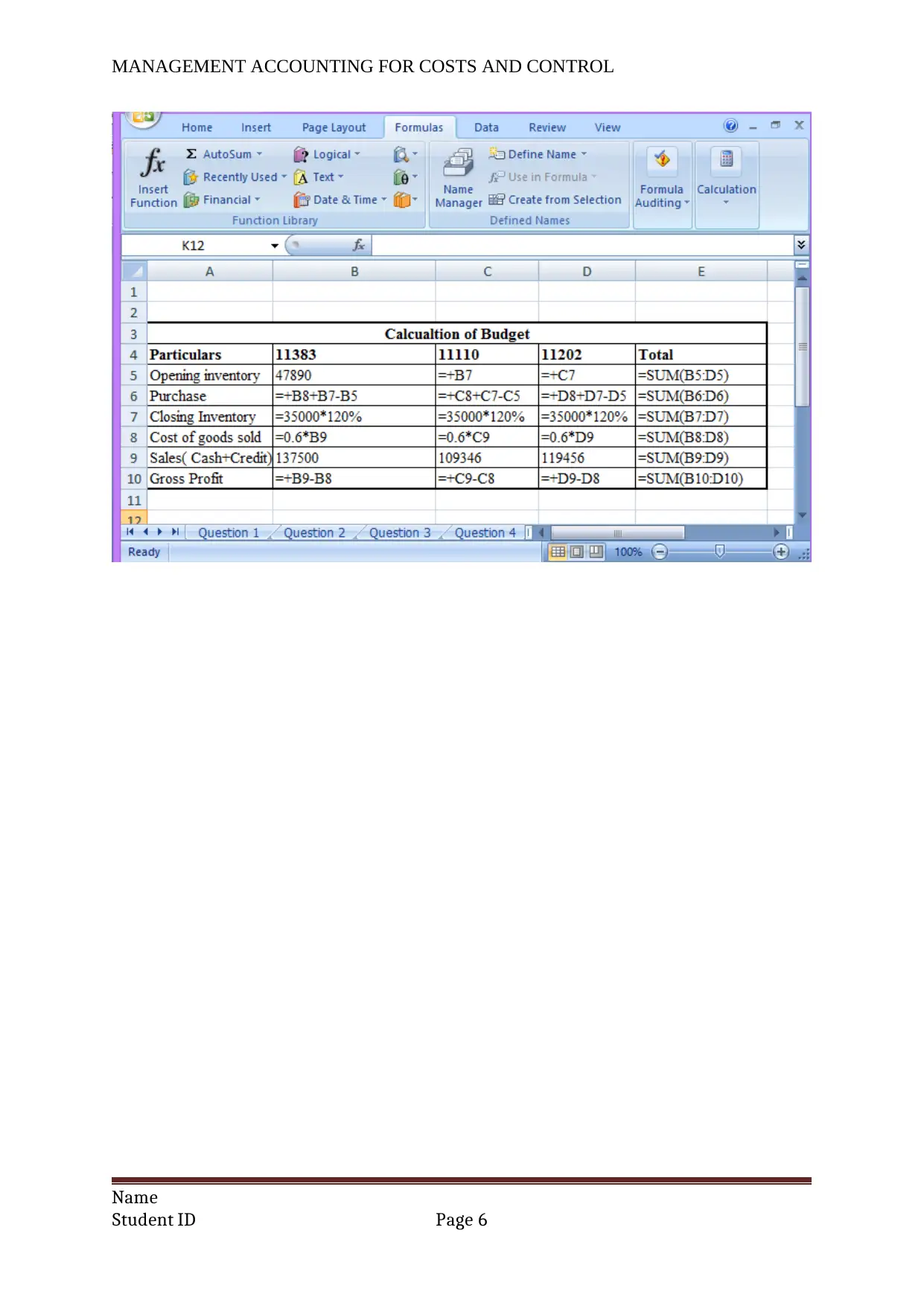

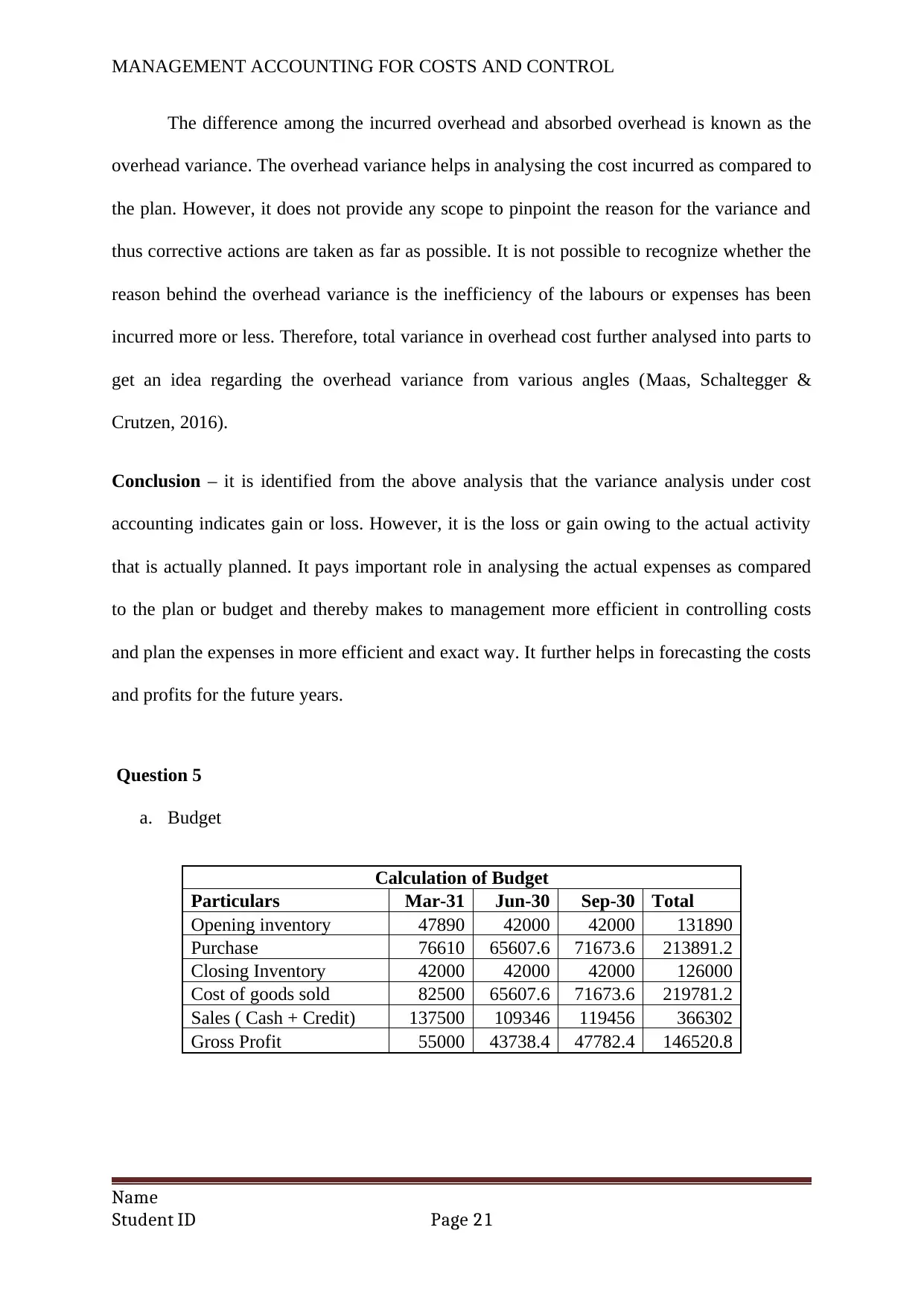

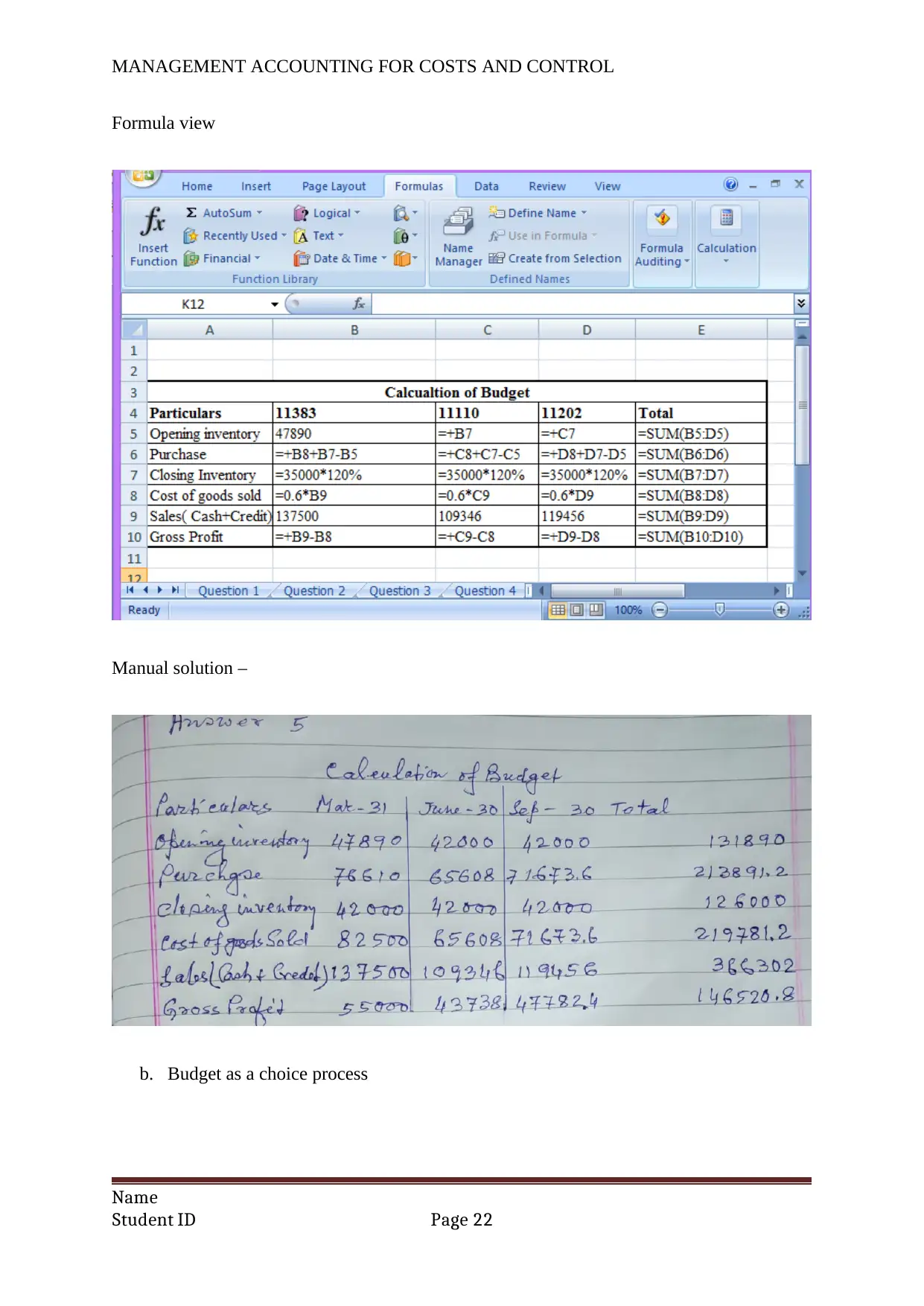

a. Budget

Calculation of Budget

Particulars Mar-31 Jun-30 Sep-30 Total

Opening inventory 47890 42000 42000 131890

Purchase 76610 65607.6 71673.6 213891.2

Closing Inventory 42000 42000 42000 126000

Cost of goods sold 82500 65607.6 71673.6 219781.2

Sales ( Cash + Credit) 137500 109346 119456 366302

Gross Profit 55000 43738.4 47782.4 146520.8

Name

Student ID Page 21

The difference among the incurred overhead and absorbed overhead is known as the

overhead variance. The overhead variance helps in analysing the cost incurred as compared to

the plan. However, it does not provide any scope to pinpoint the reason for the variance and

thus corrective actions are taken as far as possible. It is not possible to recognize whether the

reason behind the overhead variance is the inefficiency of the labours or expenses has been

incurred more or less. Therefore, total variance in overhead cost further analysed into parts to

get an idea regarding the overhead variance from various angles (Maas, Schaltegger &

Crutzen, 2016).

Conclusion – it is identified from the above analysis that the variance analysis under cost

accounting indicates gain or loss. However, it is the loss or gain owing to the actual activity

that is actually planned. It pays important role in analysing the actual expenses as compared

to the plan or budget and thereby makes to management more efficient in controlling costs

and plan the expenses in more efficient and exact way. It further helps in forecasting the costs

and profits for the future years.

Question 5

a. Budget

Calculation of Budget

Particulars Mar-31 Jun-30 Sep-30 Total

Opening inventory 47890 42000 42000 131890

Purchase 76610 65607.6 71673.6 213891.2

Closing Inventory 42000 42000 42000 126000

Cost of goods sold 82500 65607.6 71673.6 219781.2

Sales ( Cash + Credit) 137500 109346 119456 366302

Gross Profit 55000 43738.4 47782.4 146520.8

Name

Student ID Page 21

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

Formula view

Manual solution –

b. Budget as a choice process

Name

Student ID Page 22

Formula view

Manual solution –

b. Budget as a choice process

Name

Student ID Page 22

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

Budget in the various businesses are used to analyse the cost actually incurred with

the plan made in advance. Different aspects are taken into consideration while preparing the

budget (Klychova, Faskhutdinova & Sadrieva, 2014). Though the views of different

companies are different, it is mainly influenced by the past records and various preference

and plans of the company (Drury, 2013). Further, while preparing the budget, the interest of

various group of people like employees, management and stakeholders are taken into

consideration (Hilton & Platt, 2013).

In the above shown cartoon image one person is telling his boss that he has completed

the project on time and within the amount allocated for the project. The other person is

replaying that he will get less amount and time next time for the same project (Williams,

2014). Therefore, the 2nd person is challenging the 1st person to complete the next project in

less time and money.

Name

Student ID Page 23

Budget in the various businesses are used to analyse the cost actually incurred with

the plan made in advance. Different aspects are taken into consideration while preparing the

budget (Klychova, Faskhutdinova & Sadrieva, 2014). Though the views of different

companies are different, it is mainly influenced by the past records and various preference

and plans of the company (Drury, 2013). Further, while preparing the budget, the interest of

various group of people like employees, management and stakeholders are taken into

consideration (Hilton & Platt, 2013).

In the above shown cartoon image one person is telling his boss that he has completed

the project on time and within the amount allocated for the project. The other person is

replaying that he will get less amount and time next time for the same project (Williams,

2014). Therefore, the 2nd person is challenging the 1st person to complete the next project in

less time and money.

Name

Student ID Page 23

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

Reference

Braun, K. W., Tietz, W. M., & Harrison, W. T. (2013). Managerial accounting. Pearson.

Corum, A., Vayvay, Ö., & Bayraktar, E. (2014). The impact of remanufacturing on total

inventory cost and order variance. Journal of Cleaner Production, 85, 442-452.

DRURY, C. M. (2013). Management and cost accounting. Springer.

Hilton, R. W., & Platt, D. E. (2013). Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Kerzner, H. (2013). Project management: a systems approach to planning, scheduling, and

controlling. John Wiley & Sons.

Klychova, G. S., Faskhutdinova, М. S., & Sadrieva, E. R. (2014). Budget efficiency for cost

control purposes in management accounting system. Mediterranean journal of social

sciences, 5(24), 79.

Maas, K., Schaltegger, S., & Crutzen, N. (2016). Integrating corporate sustainability

assessment, management accounting, control, and reporting. Journal of Cleaner

Production, 136, 237-248.

Matsumura, E. M., Mattison, B. L., & Miller-Nobles, T. L. (2014). Horngren's Financial &

Managerial Accounting. Pearson Education Limited.

Schmeisser, W., Mohnkopf, H., Hartmann, M., & Metze, G. (2014). Innovation Performance

Accounting. Springer.

Whitecotton, S., Libby, R., & Phillips, F. (2013). Managerial accounting. McGraw-Hill

Higher Education.

Name

Student ID Page 24

Reference

Braun, K. W., Tietz, W. M., & Harrison, W. T. (2013). Managerial accounting. Pearson.

Corum, A., Vayvay, Ö., & Bayraktar, E. (2014). The impact of remanufacturing on total

inventory cost and order variance. Journal of Cleaner Production, 85, 442-452.

DRURY, C. M. (2013). Management and cost accounting. Springer.

Hilton, R. W., & Platt, D. E. (2013). Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Kerzner, H. (2013). Project management: a systems approach to planning, scheduling, and

controlling. John Wiley & Sons.

Klychova, G. S., Faskhutdinova, М. S., & Sadrieva, E. R. (2014). Budget efficiency for cost

control purposes in management accounting system. Mediterranean journal of social

sciences, 5(24), 79.

Maas, K., Schaltegger, S., & Crutzen, N. (2016). Integrating corporate sustainability

assessment, management accounting, control, and reporting. Journal of Cleaner

Production, 136, 237-248.

Matsumura, E. M., Mattison, B. L., & Miller-Nobles, T. L. (2014). Horngren's Financial &

Managerial Accounting. Pearson Education Limited.

Schmeisser, W., Mohnkopf, H., Hartmann, M., & Metze, G. (2014). Innovation Performance

Accounting. Springer.

Whitecotton, S., Libby, R., & Phillips, F. (2013). Managerial accounting. McGraw-Hill

Higher Education.

Name

Student ID Page 24

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING FOR COSTS AND CONTROL

Williams, J. (2014). Financial accounting. McGraw-Hill Higher Education.

Xia, F., & Walker, G. (2015). How much does owner type matter for firm performance?

Manufacturing firms in China 1998–2007. Strategic Management Journal, 36(4),

576-585.

Name

Student ID Page 25

Williams, J. (2014). Financial accounting. McGraw-Hill Higher Education.

Xia, F., & Walker, G. (2015). How much does owner type matter for firm performance?

Manufacturing firms in China 1998–2007. Strategic Management Journal, 36(4),

576-585.

Name

Student ID Page 25

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.