Management Accounting for Costs and Control: A Comprehensive Report

VerifiedAdded on 2020/07/23

|14

|2538

|29

Report

AI Summary

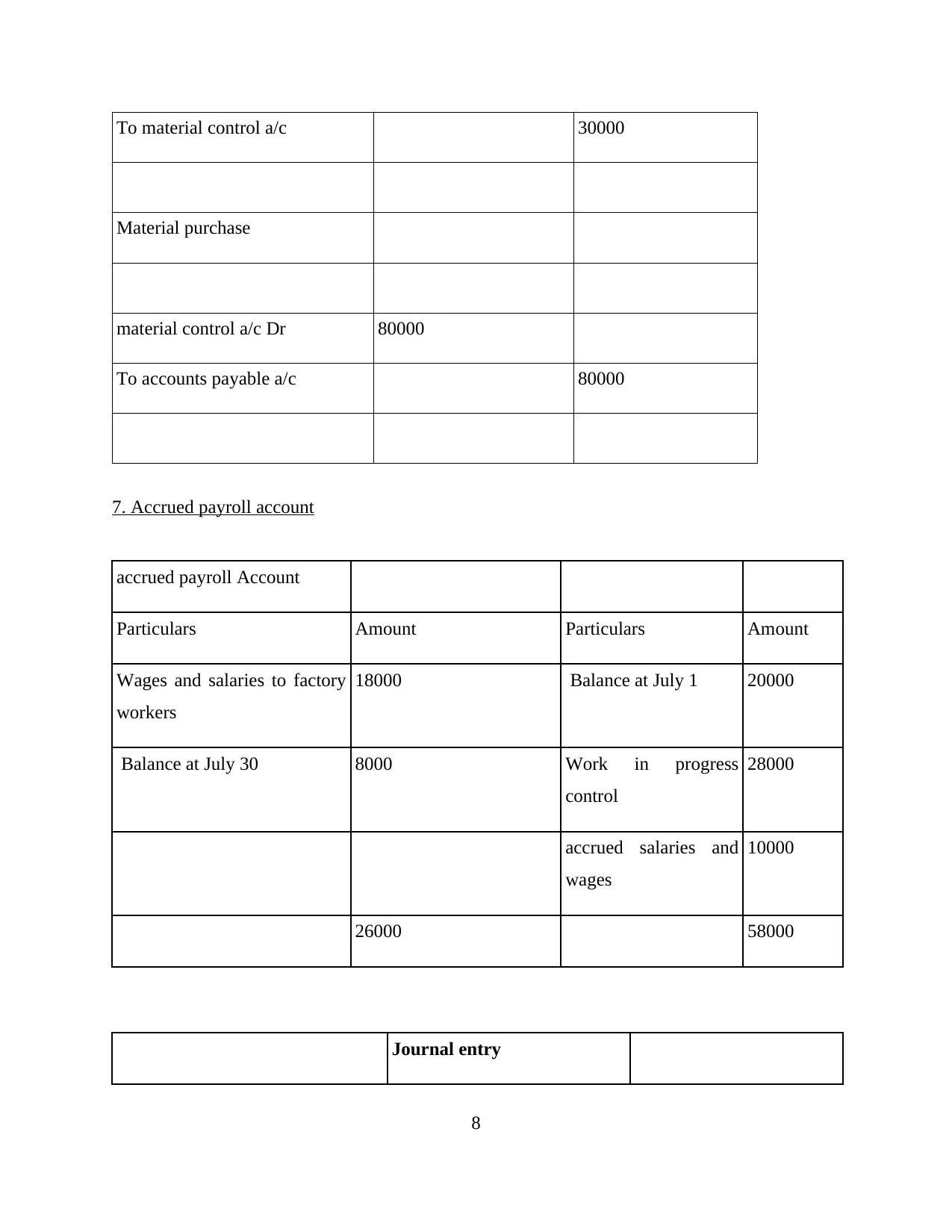

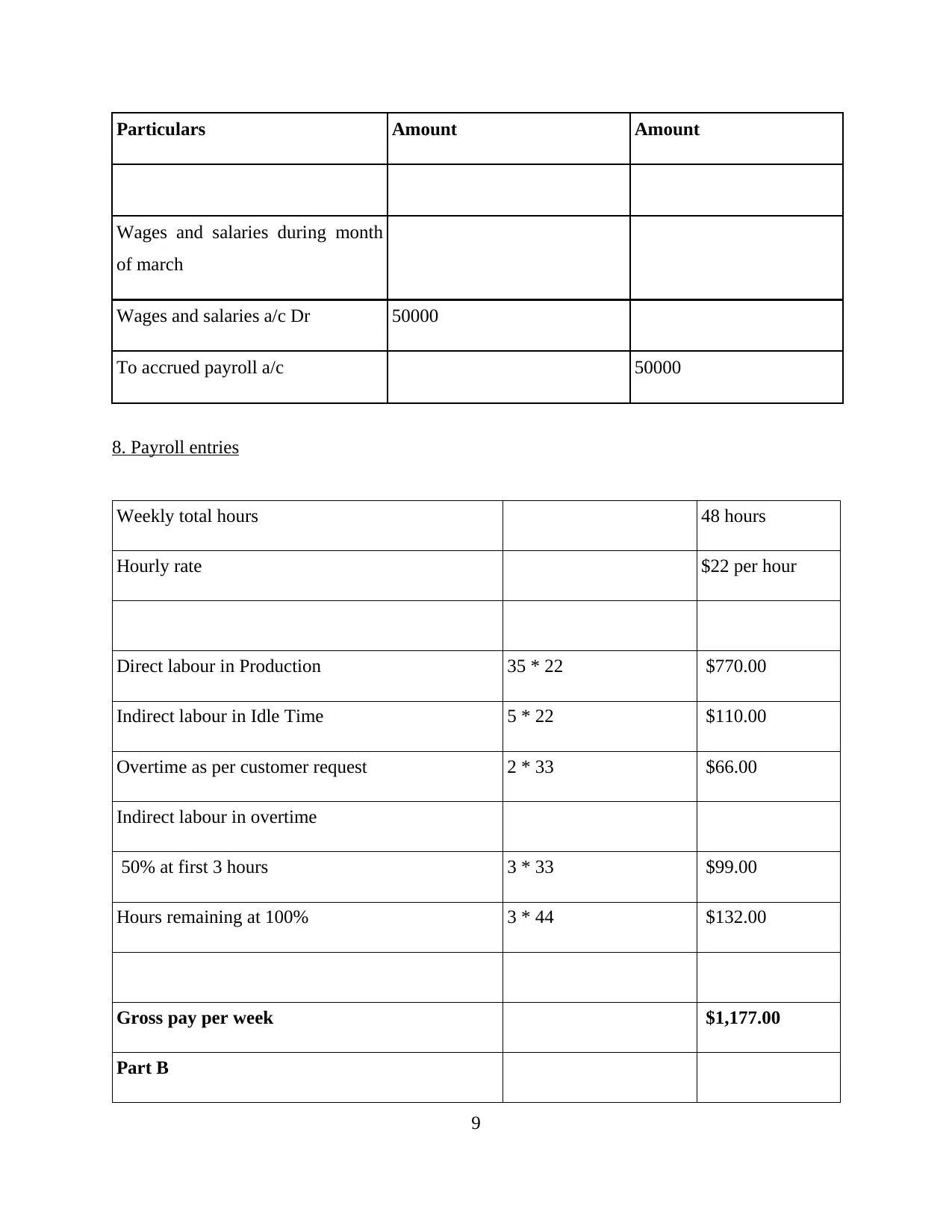

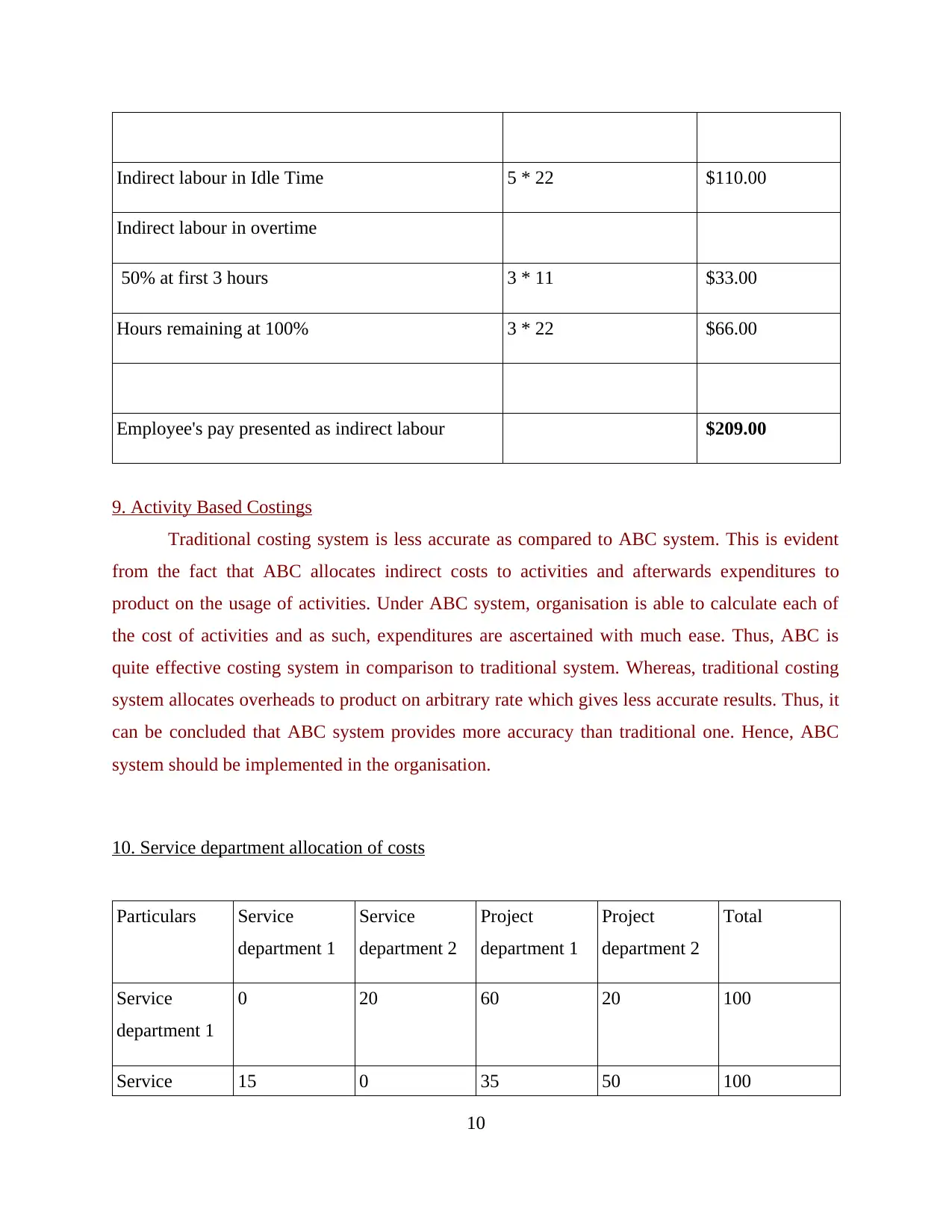

This report provides a comprehensive overview of management accounting, emphasizing cost control and its various techniques. It begins with a discussion of panopticism and its relevance to management accounting, highlighting its role in internal surveillance and decision-making. The report then explores the core functions of management accounting, including planning, decision-making, and controlling. It also delves into the usage of checklists as a control device, providing real-world examples. Furthermore, the report includes detailed manufacturing and income statements, along with discussions on labor costs, material control accounts, and accrued payroll. It also covers activity-based costing (ABC) and service department cost allocation methods, comparing traditional and ABC systems. The report offers practical insights into payroll entries, showcasing different scenarios and calculations. Overall, the report aims to provide a solid understanding of cost control and management accounting principles.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.