AFM020 Management Accounting: Investment Appraisal and Cost Analysis

VerifiedAdded on 2023/06/15

|13

|3572

|446

Report

AI Summary

This report provides a comprehensive analysis of management accounting frameworks, focusing on profit calculation and investment appraisal for MAF Associates in Loland. It includes calculations of profit for four years, a schedule of annual cash flows, and an investment appraisal using Net Present Value (NPV) and payback period methods to assess a potential retail outlet project. The report advises against the project due to a negative NPV and a payback period nearly equal to the project's duration, suggesting potential liquidity issues. Additionally, it critically examines the varying definitions of cost, such as opportunity cost, explicit and implicit costs, accounting and economic costs, business and full costs, fixed and variable costs, and incremental costs, highlighting their importance in margin calculation and cost classification. The report concludes by emphasizing the significance of accurate cost management for effective budgeting and financial decision-making.

AFM020 Management

Accounting

Frameworks

Accounting

Frameworks

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

SCENARIO 1...................................................................................................................................3

(a) Show the calculation of profit for the for years. ...................................................................3

b) Prepare a schedule for annual cash flows and investment appraisal for determining the

efficiency of project....................................................................................................................4

c) Provide insights into the CAPEX appraisal of the project and suggest whether to accept the

proposal or not.............................................................................................................................6

SCENARIO 2...................................................................................................................................7

Critically comment on the statement made by the manager. Provide illustrations for critique

and also gives comments.............................................................................................................7

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION ..........................................................................................................................3

SCENARIO 1...................................................................................................................................3

(a) Show the calculation of profit for the for years. ...................................................................3

b) Prepare a schedule for annual cash flows and investment appraisal for determining the

efficiency of project....................................................................................................................4

c) Provide insights into the CAPEX appraisal of the project and suggest whether to accept the

proposal or not.............................................................................................................................6

SCENARIO 2...................................................................................................................................7

Critically comment on the statement made by the manager. Provide illustrations for critique

and also gives comments.............................................................................................................7

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting can be defined as a process of preparation of reports related to

the operations of the business. This helps them in the continuing its target by recognising,

measuring, evaluating and interpreting the data which is to be communicated to the mangers.

Through this companies makes their long as well as short term decisions (Nielsen, 2018). The

company chosen in this report is MAF Associates. In the report the country chosen is Loland a

fictitious one. Firm deals in the buying and selling of computer equipments. The report is divided

into two sections. The first part deals in the calculation of profits and analysis of the investment

proposal. The second part discusses about the differentiation in the meaning of cost and the

problems created by it for the mangers along with illustrating it with the help of examples.

SCENARIO 1

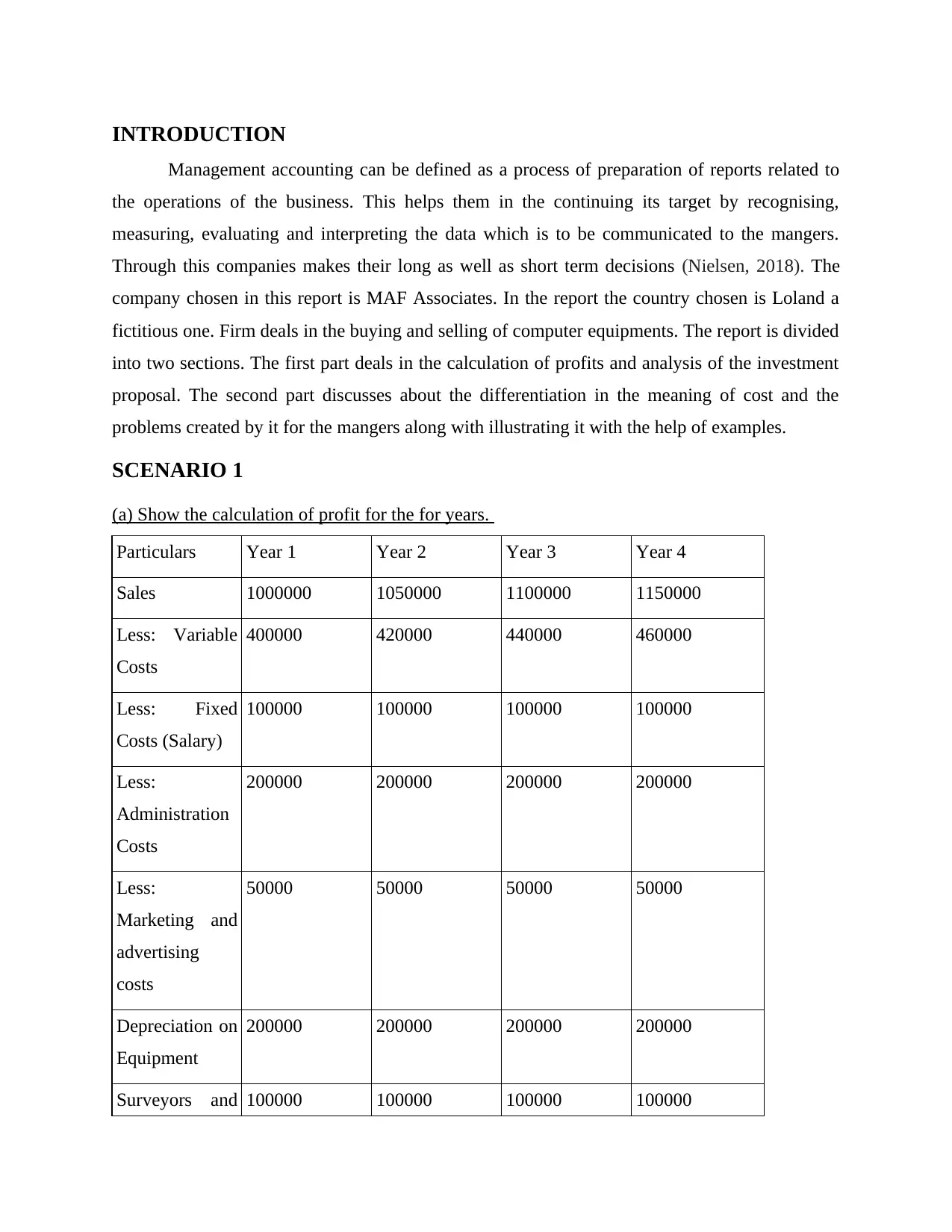

(a) Show the calculation of profit for the for years.

Particulars Year 1 Year 2 Year 3 Year 4

Sales 1000000 1050000 1100000 1150000

Less: Variable

Costs

400000 420000 440000 460000

Less: Fixed

Costs (Salary)

100000 100000 100000 100000

Less:

Administration

Costs

200000 200000 200000 200000

Less:

Marketing and

advertising

costs

50000 50000 50000 50000

Depreciation on

Equipment

200000 200000 200000 200000

Surveyors and 100000 100000 100000 100000

Management accounting can be defined as a process of preparation of reports related to

the operations of the business. This helps them in the continuing its target by recognising,

measuring, evaluating and interpreting the data which is to be communicated to the mangers.

Through this companies makes their long as well as short term decisions (Nielsen, 2018). The

company chosen in this report is MAF Associates. In the report the country chosen is Loland a

fictitious one. Firm deals in the buying and selling of computer equipments. The report is divided

into two sections. The first part deals in the calculation of profits and analysis of the investment

proposal. The second part discusses about the differentiation in the meaning of cost and the

problems created by it for the mangers along with illustrating it with the help of examples.

SCENARIO 1

(a) Show the calculation of profit for the for years.

Particulars Year 1 Year 2 Year 3 Year 4

Sales 1000000 1050000 1100000 1150000

Less: Variable

Costs

400000 420000 440000 460000

Less: Fixed

Costs (Salary)

100000 100000 100000 100000

Less:

Administration

Costs

200000 200000 200000 200000

Less:

Marketing and

advertising

costs

50000 50000 50000 50000

Depreciation on

Equipment

200000 200000 200000 200000

Surveyors and 100000 100000 100000 100000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

legal fees

Profit before

tax

-50000 -20000 10000 40000

Corporation tax 2000 8000

Profit after tax 8000 32000

Calculation of depreciation of equipment

Cost of equipment = $ 1000000

Residual value = $ 200000

Number of years = 4

Value of depreciation = (1000000 – 200000) / 4

= 800000 / 4

= $ 200000

b) Prepare a schedule for annual cash flows and investment appraisal for determining the

efficiency of project.

Particulars Year 0 Year 1 Year 2 Year 3 Year 4

Sales 1000000 1050000 1100000 1150000

Less:

Variable

Costs

400000 420000 440000 460000

Less: Fixed

Costs

(Salary)

100000 100000 100000 100000

Less:

Administrati

on Costs

200000 200000 200000 200000

Less: 50000 50000 50000 50000

Profit before

tax

-50000 -20000 10000 40000

Corporation tax 2000 8000

Profit after tax 8000 32000

Calculation of depreciation of equipment

Cost of equipment = $ 1000000

Residual value = $ 200000

Number of years = 4

Value of depreciation = (1000000 – 200000) / 4

= 800000 / 4

= $ 200000

b) Prepare a schedule for annual cash flows and investment appraisal for determining the

efficiency of project.

Particulars Year 0 Year 1 Year 2 Year 3 Year 4

Sales 1000000 1050000 1100000 1150000

Less:

Variable

Costs

400000 420000 440000 460000

Less: Fixed

Costs

(Salary)

100000 100000 100000 100000

Less:

Administrati

on Costs

200000 200000 200000 200000

Less: 50000 50000 50000 50000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Marketing

and

advertising

costs

Purchase of

Equipment

1000000

Residual

value of

equipment

200000

Land and

building

purchased

1000000

Residual

value of

Land and

building

1200000

Working

capital

430000

Corporation

tax

2000 8000

Net cash

flows

-2000000 250000 280000 308000 1302000

Calculation of working capital

Year 1

10 % of sales = 10 % * 1000000 = $ 100000

Year 2

= 10 % * 1050000 = $ 105000

Year 3

and

advertising

costs

Purchase of

Equipment

1000000

Residual

value of

equipment

200000

Land and

building

purchased

1000000

Residual

value of

Land and

building

1200000

Working

capital

430000

Corporation

tax

2000 8000

Net cash

flows

-2000000 250000 280000 308000 1302000

Calculation of working capital

Year 1

10 % of sales = 10 % * 1000000 = $ 100000

Year 2

= 10 % * 1050000 = $ 105000

Year 3

= 10 % * 1100000 = $ 110000

Year 4

= 10 % * 1150000 = $ 115000

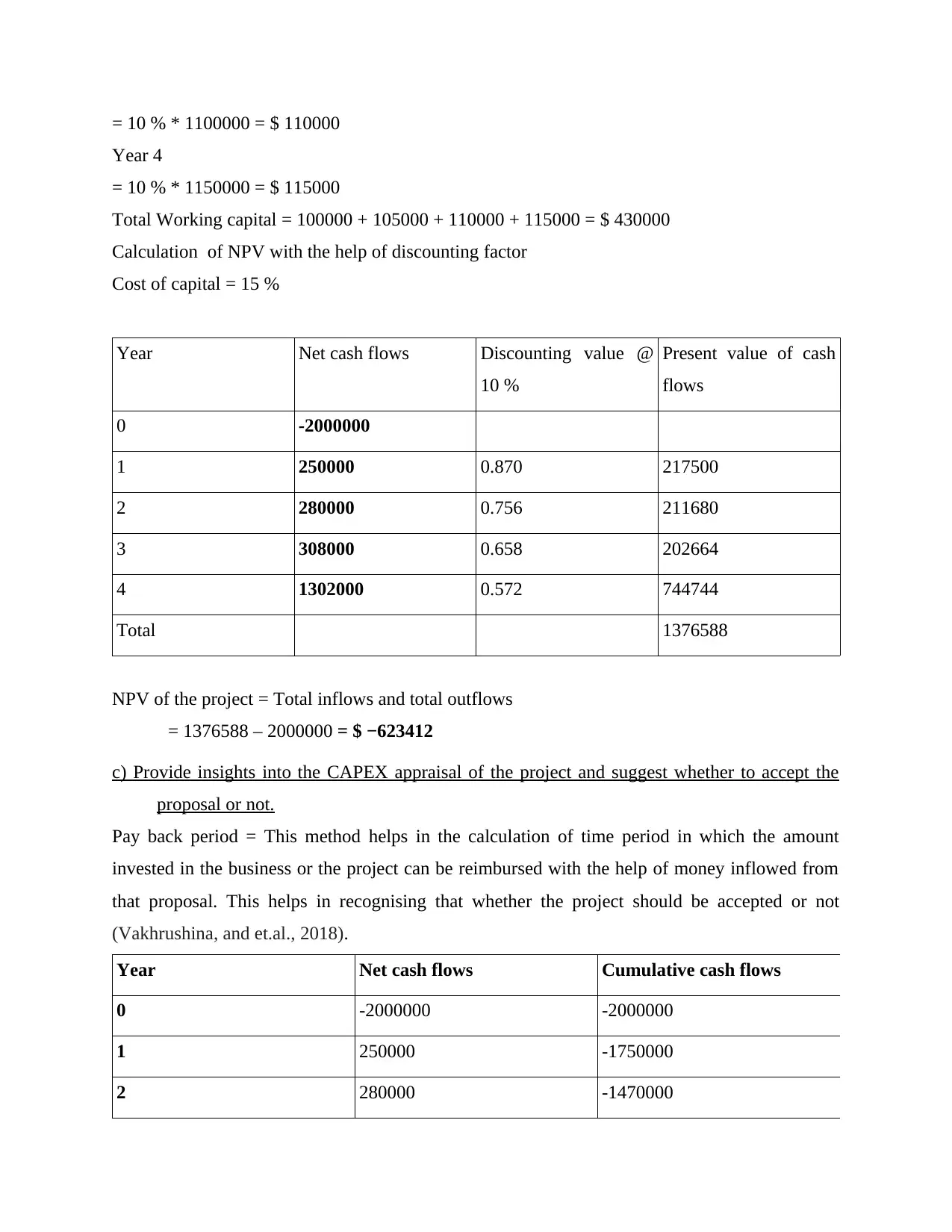

Total Working capital = 100000 + 105000 + 110000 + 115000 = $ 430000

Calculation of NPV with the help of discounting factor

Cost of capital = 15 %

Year Net cash flows Discounting value @

10 %

Present value of cash

flows

0 -2000000

1 250000 0.870 217500

2 280000 0.756 211680

3 308000 0.658 202664

4 1302000 0.572 744744

Total 1376588

NPV of the project = Total inflows and total outflows

= 1376588 – 2000000 = $ −623412

c) Provide insights into the CAPEX appraisal of the project and suggest whether to accept the

proposal or not.

Pay back period = This method helps in the calculation of time period in which the amount

invested in the business or the project can be reimbursed with the help of money inflowed from

that proposal. This helps in recognising that whether the project should be accepted or not

(Vakhrushina, and et.al., 2018).

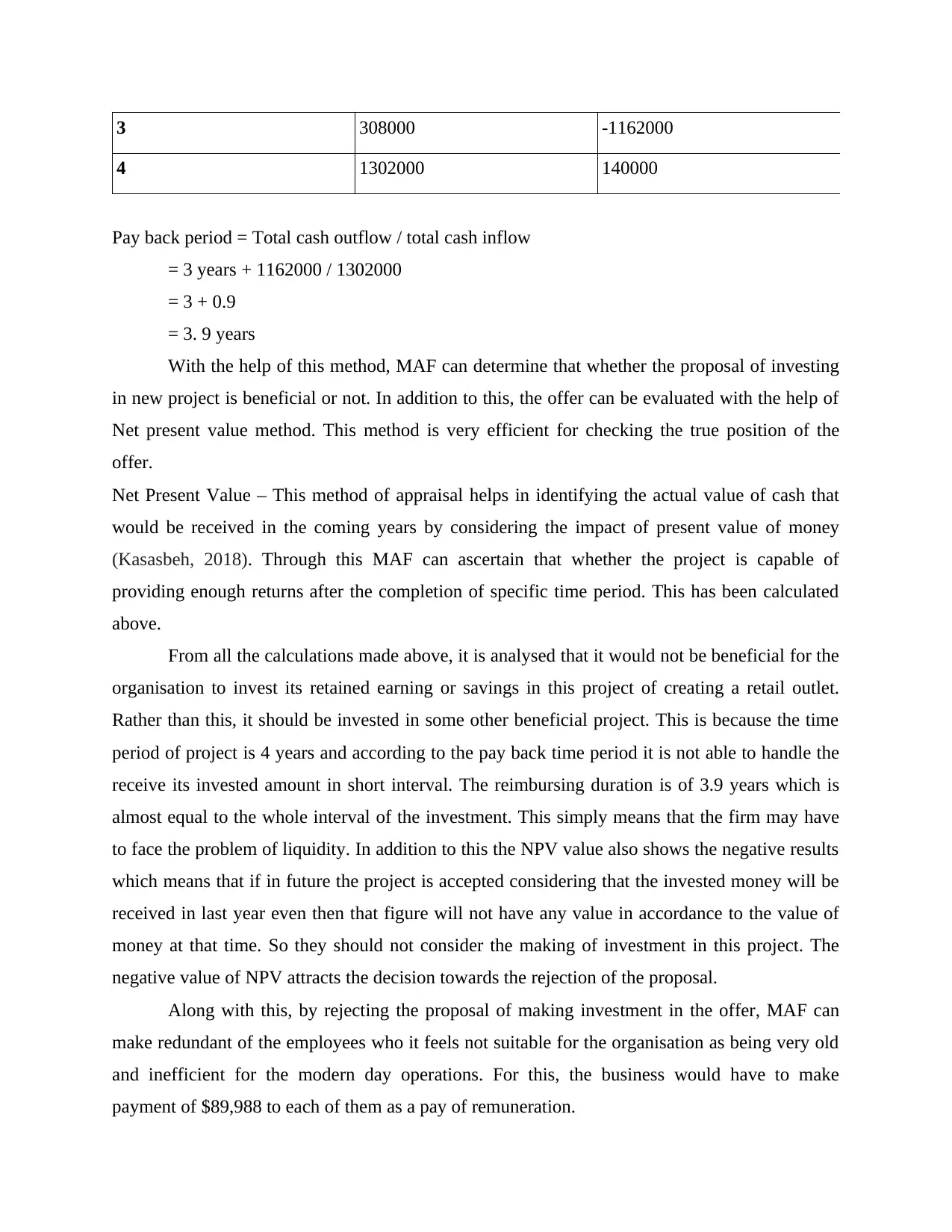

Year Net cash flows Cumulative cash flows

0 -2000000 -2000000

1 250000 -1750000

2 280000 -1470000

Year 4

= 10 % * 1150000 = $ 115000

Total Working capital = 100000 + 105000 + 110000 + 115000 = $ 430000

Calculation of NPV with the help of discounting factor

Cost of capital = 15 %

Year Net cash flows Discounting value @

10 %

Present value of cash

flows

0 -2000000

1 250000 0.870 217500

2 280000 0.756 211680

3 308000 0.658 202664

4 1302000 0.572 744744

Total 1376588

NPV of the project = Total inflows and total outflows

= 1376588 – 2000000 = $ −623412

c) Provide insights into the CAPEX appraisal of the project and suggest whether to accept the

proposal or not.

Pay back period = This method helps in the calculation of time period in which the amount

invested in the business or the project can be reimbursed with the help of money inflowed from

that proposal. This helps in recognising that whether the project should be accepted or not

(Vakhrushina, and et.al., 2018).

Year Net cash flows Cumulative cash flows

0 -2000000 -2000000

1 250000 -1750000

2 280000 -1470000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3 308000 -1162000

4 1302000 140000

Pay back period = Total cash outflow / total cash inflow

= 3 years + 1162000 / 1302000

= 3 + 0.9

= 3. 9 years

With the help of this method, MAF can determine that whether the proposal of investing

in new project is beneficial or not. In addition to this, the offer can be evaluated with the help of

Net present value method. This method is very efficient for checking the true position of the

offer.

Net Present Value – This method of appraisal helps in identifying the actual value of cash that

would be received in the coming years by considering the impact of present value of money

(Kasasbeh, 2018). Through this MAF can ascertain that whether the project is capable of

providing enough returns after the completion of specific time period. This has been calculated

above.

From all the calculations made above, it is analysed that it would not be beneficial for the

organisation to invest its retained earning or savings in this project of creating a retail outlet.

Rather than this, it should be invested in some other beneficial project. This is because the time

period of project is 4 years and according to the pay back time period it is not able to handle the

receive its invested amount in short interval. The reimbursing duration is of 3.9 years which is

almost equal to the whole interval of the investment. This simply means that the firm may have

to face the problem of liquidity. In addition to this the NPV value also shows the negative results

which means that if in future the project is accepted considering that the invested money will be

received in last year even then that figure will not have any value in accordance to the value of

money at that time. So they should not consider the making of investment in this project. The

negative value of NPV attracts the decision towards the rejection of the proposal.

Along with this, by rejecting the proposal of making investment in the offer, MAF can

make redundant of the employees who it feels not suitable for the organisation as being very old

and inefficient for the modern day operations. For this, the business would have to make

payment of $89,988 to each of them as a pay of remuneration.

4 1302000 140000

Pay back period = Total cash outflow / total cash inflow

= 3 years + 1162000 / 1302000

= 3 + 0.9

= 3. 9 years

With the help of this method, MAF can determine that whether the proposal of investing

in new project is beneficial or not. In addition to this, the offer can be evaluated with the help of

Net present value method. This method is very efficient for checking the true position of the

offer.

Net Present Value – This method of appraisal helps in identifying the actual value of cash that

would be received in the coming years by considering the impact of present value of money

(Kasasbeh, 2018). Through this MAF can ascertain that whether the project is capable of

providing enough returns after the completion of specific time period. This has been calculated

above.

From all the calculations made above, it is analysed that it would not be beneficial for the

organisation to invest its retained earning or savings in this project of creating a retail outlet.

Rather than this, it should be invested in some other beneficial project. This is because the time

period of project is 4 years and according to the pay back time period it is not able to handle the

receive its invested amount in short interval. The reimbursing duration is of 3.9 years which is

almost equal to the whole interval of the investment. This simply means that the firm may have

to face the problem of liquidity. In addition to this the NPV value also shows the negative results

which means that if in future the project is accepted considering that the invested money will be

received in last year even then that figure will not have any value in accordance to the value of

money at that time. So they should not consider the making of investment in this project. The

negative value of NPV attracts the decision towards the rejection of the proposal.

Along with this, by rejecting the proposal of making investment in the offer, MAF can

make redundant of the employees who it feels not suitable for the organisation as being very old

and inefficient for the modern day operations. For this, the business would have to make

payment of $89,988 to each of them as a pay of remuneration.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SCENARIO 2

Critically comment on the statement made by the manager. Provide illustrations for critique and

also gives comments.

According to the managers in the meeting, there is a difference between the definition of

cost for different persons and variant situations. This creates problems in management of costs,

preparation of budgets and taking financial decisions and understanding the true situation of the

cost. Here is the discussion related to the difference in costs and its related issues (Bulgakova,

and et.al., 2018).

Cost can be defined as a value that is incurred in the production of any goods or service

and once consumed it is of no more use. The amount invested on the acquisition of goods or

machinery or any plant is also a part of this cost. Here, money is the mode which is used for

acquiring the goods and thus the cost is always measured in monetary forms. Their are different

types of costs that are been incurred by the organisations at the time of handling any process.

Below are the different kinds of costs related to the companies (Jarwal, 2018).

Types of costs

Opportunity costs – It refers to the alternative cost of project. It is the objective of the

firms to derive maximum and best from their limited resources. This means that they

avoid the income that could be generated from the next best usage of the material.

Opportunity cost is the profit that could be generated from the second good use of

resource. For instance, there are two projects n which the same amount of $ 50000 is

required to be invested. First one would yield $150000 at last and the other one will bring

$ 100000. Here, the firm will choose first project and the amount of $ 100000 is its

opportunity cost.

Explicit cost – These are the expenses which is used by the company for the payments

that are made by the employer to buy or own the factors of production. These costs

include payments for raw materials, loan interest, rents for rented buildings or machinery,

and for the payment of taxes to the state. This amount needs to be clearly and separately

visible in the books of accounts (Rahmani, and Ghashghaei, 2018).

Implicit cost – There are many types of costs that are not regarded as cash outlays in the

records. Such as opportunity cost. In addition to this, many times, the owners of the

organisation bring their own personal asset like land and furniture in the business. This

Critically comment on the statement made by the manager. Provide illustrations for critique and

also gives comments.

According to the managers in the meeting, there is a difference between the definition of

cost for different persons and variant situations. This creates problems in management of costs,

preparation of budgets and taking financial decisions and understanding the true situation of the

cost. Here is the discussion related to the difference in costs and its related issues (Bulgakova,

and et.al., 2018).

Cost can be defined as a value that is incurred in the production of any goods or service

and once consumed it is of no more use. The amount invested on the acquisition of goods or

machinery or any plant is also a part of this cost. Here, money is the mode which is used for

acquiring the goods and thus the cost is always measured in monetary forms. Their are different

types of costs that are been incurred by the organisations at the time of handling any process.

Below are the different kinds of costs related to the companies (Jarwal, 2018).

Types of costs

Opportunity costs – It refers to the alternative cost of project. It is the objective of the

firms to derive maximum and best from their limited resources. This means that they

avoid the income that could be generated from the next best usage of the material.

Opportunity cost is the profit that could be generated from the second good use of

resource. For instance, there are two projects n which the same amount of $ 50000 is

required to be invested. First one would yield $150000 at last and the other one will bring

$ 100000. Here, the firm will choose first project and the amount of $ 100000 is its

opportunity cost.

Explicit cost – These are the expenses which is used by the company for the payments

that are made by the employer to buy or own the factors of production. These costs

include payments for raw materials, loan interest, rents for rented buildings or machinery,

and for the payment of taxes to the state. This amount needs to be clearly and separately

visible in the books of accounts (Rahmani, and Ghashghaei, 2018).

Implicit cost – There are many types of costs that are not regarded as cash outlays in the

records. Such as opportunity cost. In addition to this, many times, the owners of the

organisation bring their own personal asset like land and furniture in the business. This

amount is normally do not included in the costs but becomes a part of capital. Thus, the

companies acquire the asset without making payment for it.

Accounting costs – It is the expenditure that is used by the company for the acquisition

of the inputs for producing the goods. It involves all the administration, selling and

maintenance costs. This also includes the payment made for buying raw material,

machinery and other operational items.

Economic costs – It refers to the total amount that is incurred by the company for

acquiring one option over the another one. This involves all kinds of explicit as well as

implicit cost under it. Thus it is the sum total of all the kinds of expenses.

Business costs – It comprises of all the expenses that are consumed by the entity for

supporting its daily operations. It also consists of all the sorts of payments and the

obligations that are required by the business to be paid. These costs are further used for

the calculation of profits or losses made by it which are further used for payment of

income tax and other related procedures (Gusc, and van Veen-Dirks, 2017).

Full costs – It is the complete value of expenditure that are made by the business

including business, opportunity and other normal costs. It helps in the ascertaining of

profits generated by the company out of its sales.

Fixed Costs – It refers the amount that remains fixed through out the year or the level of

output. The business has to bear this amount even If it is not undergoing any production

and that too at the fixed amount. For instance the value of depreciation on land or interest

on loan. These values do not tend to change with the alteration in the quantity of output.

But in the long run, even this value does not remains fixed.

Variable costs – it can be defined as a cost that is incurred by the business for its

production and acquisition of the raw material and goods. This amount tends to change

with change in the number of units produced. For instance, labour, electricity and many

more. Cost of material is also variable and depends on the number of units a firm requires

for its sales.

Incremental costs – These are the costs that are additional to the other normal costs if

the business. These occur due to the change in the production level or process. This

expenses could be avoided by the business if it does not produce more than its level or

avoid possible variation in it (Habib, and Hasan, 2019).

companies acquire the asset without making payment for it.

Accounting costs – It is the expenditure that is used by the company for the acquisition

of the inputs for producing the goods. It involves all the administration, selling and

maintenance costs. This also includes the payment made for buying raw material,

machinery and other operational items.

Economic costs – It refers to the total amount that is incurred by the company for

acquiring one option over the another one. This involves all kinds of explicit as well as

implicit cost under it. Thus it is the sum total of all the kinds of expenses.

Business costs – It comprises of all the expenses that are consumed by the entity for

supporting its daily operations. It also consists of all the sorts of payments and the

obligations that are required by the business to be paid. These costs are further used for

the calculation of profits or losses made by it which are further used for payment of

income tax and other related procedures (Gusc, and van Veen-Dirks, 2017).

Full costs – It is the complete value of expenditure that are made by the business

including business, opportunity and other normal costs. It helps in the ascertaining of

profits generated by the company out of its sales.

Fixed Costs – It refers the amount that remains fixed through out the year or the level of

output. The business has to bear this amount even If it is not undergoing any production

and that too at the fixed amount. For instance the value of depreciation on land or interest

on loan. These values do not tend to change with the alteration in the quantity of output.

But in the long run, even this value does not remains fixed.

Variable costs – it can be defined as a cost that is incurred by the business for its

production and acquisition of the raw material and goods. This amount tends to change

with change in the number of units produced. For instance, labour, electricity and many

more. Cost of material is also variable and depends on the number of units a firm requires

for its sales.

Incremental costs – These are the costs that are additional to the other normal costs if

the business. These occur due to the change in the production level or process. This

expenses could be avoided by the business if it does not produce more than its level or

avoid possible variation in it (Habib, and Hasan, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Importance of Costs:

1. Calculation of the margins: The margin is the price at which The margin is simply the

price which is asked, subtracted by the cost of the product which is provided. Margin $ /

Unit, and Margin% (Margin / Selling Price) in particular, are probably the most important

analytical metrics that will help you understand a business's profitability and health.

Almost always, a negative margin business is condemned to failure.

2. Classification of various costs: It helps in classifying the different type of cost which may

incur in the business. It assists in allocating the funds and the resources appropriately and

also estimates the budget and the budgeted profit which the company may get in future.

3. Price Determination: It helps in determining and understanding the differentiation

between the costs. By this the company can take the advantage of these costs and arrange

the prices accordingly for the products and service and estimate the profit. Also it will

help in controlling the idle costs which are not necessary for the business and the venture

in incurring (Modell, 2020).

4. Timely Management: The costing helps in the management of the fiscal resources on the

timely basis so can it can manage the uncertain problems which the business may suffer

due to the certain circumstances. Through budget the company may analyse the variance

with the actual expenses and taken the decisions for the development of the organisation

for the future occurrences.

5. Costs in reduction: It might in some cases likewise be a direct result of the public

authority strategies and different elements, for example, assume assembling plant in a

remote are. Because of the climate issue, there is an inaccessibility of natural substance to

be utilized underway. Assuming the equivalent couldn't be made accessible for the

following ten days, then, at that point, the expense of work and different overheads for

such ten days will bring about additional costs that are not thought of while getting ready

spending plans.

6. Setting performance standards: The budget help in setting the standard which assist in

analysing the performance of the business with the actual data. It helps in establishing the

goals and will lead to the development of the company against the benchmark which has

been set.

Challenges faced by the managers in terms of determining the costs:

1. Calculation of the margins: The margin is the price at which The margin is simply the

price which is asked, subtracted by the cost of the product which is provided. Margin $ /

Unit, and Margin% (Margin / Selling Price) in particular, are probably the most important

analytical metrics that will help you understand a business's profitability and health.

Almost always, a negative margin business is condemned to failure.

2. Classification of various costs: It helps in classifying the different type of cost which may

incur in the business. It assists in allocating the funds and the resources appropriately and

also estimates the budget and the budgeted profit which the company may get in future.

3. Price Determination: It helps in determining and understanding the differentiation

between the costs. By this the company can take the advantage of these costs and arrange

the prices accordingly for the products and service and estimate the profit. Also it will

help in controlling the idle costs which are not necessary for the business and the venture

in incurring (Modell, 2020).

4. Timely Management: The costing helps in the management of the fiscal resources on the

timely basis so can it can manage the uncertain problems which the business may suffer

due to the certain circumstances. Through budget the company may analyse the variance

with the actual expenses and taken the decisions for the development of the organisation

for the future occurrences.

5. Costs in reduction: It might in some cases likewise be a direct result of the public

authority strategies and different elements, for example, assume assembling plant in a

remote are. Because of the climate issue, there is an inaccessibility of natural substance to

be utilized underway. Assuming the equivalent couldn't be made accessible for the

following ten days, then, at that point, the expense of work and different overheads for

such ten days will bring about additional costs that are not thought of while getting ready

spending plans.

6. Setting performance standards: The budget help in setting the standard which assist in

analysing the performance of the business with the actual data. It helps in establishing the

goals and will lead to the development of the company against the benchmark which has

been set.

Challenges faced by the managers in terms of determining the costs:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. Problem in identifying the hidden costs – It is very difficult for the organisations to detect

the hidden costs in the processes like the cost beard on training the employee at the time

of production. This results in decrease in the production of units. This cost cannot be

detected by the managers which creates difficulty in the setting of price of product. For

instance, depreciation. This amount is not paid in cash but costs the company at the time

of preparation of goods as this reduces the production capacity of company (Li, 2018).

2. At the time of preparation of budget – there are lots of situations, in which the managers

are not able to detect the amount of expenses that can actually occur at the time of real

operations. The impact of economic and external environment changes cannot be

detected by the manager with accuracy while preparing the budget. This creates a lot of

problems when the actual results are driven (Rebele, and Pierre, 2019).

3. Difference in the meaning of definition of expenses – At present, there is no proper

meanings of the costs. The people cannot determine that a particular expense is fixed or

not. There are lots of expenses whose some portion is fixed while the other is flexible.

These costs created difficulties to the managers that the while preparing the report which

portion of the cost is fixed and how much it is changing and to what extent.

4. Problem in reporting – It is difficult to communicate the report as the meaning of expense

differs from person to person. For example, many individuals do not know that the

finance cost is the amount that is been paid as an interest. So while calculating the

interest coverage ratio, such person will not be able to understand that they have to

consider the amount of finance cost under it. This will create a problem to the manager.

5. Usage of different methods for calculation of expenses – Different companies uses

various methods for the determination of the amount of expense. Such as the method of

depreciation is different in all firms which creates problems in conducting comparison

(Sjögren, and Fernler, 2019).

Thus, it is very difficult for the mangers to use the concept of cost in all their processes. It

not only creates problem in making budget but also in making various decisions like cost of

product. Thus, they should keep the facts in mind that the meaning of costs differs for all and

sometimes are hidden so they should be vigilant while dealing in them.

the hidden costs in the processes like the cost beard on training the employee at the time

of production. This results in decrease in the production of units. This cost cannot be

detected by the managers which creates difficulty in the setting of price of product. For

instance, depreciation. This amount is not paid in cash but costs the company at the time

of preparation of goods as this reduces the production capacity of company (Li, 2018).

2. At the time of preparation of budget – there are lots of situations, in which the managers

are not able to detect the amount of expenses that can actually occur at the time of real

operations. The impact of economic and external environment changes cannot be

detected by the manager with accuracy while preparing the budget. This creates a lot of

problems when the actual results are driven (Rebele, and Pierre, 2019).

3. Difference in the meaning of definition of expenses – At present, there is no proper

meanings of the costs. The people cannot determine that a particular expense is fixed or

not. There are lots of expenses whose some portion is fixed while the other is flexible.

These costs created difficulties to the managers that the while preparing the report which

portion of the cost is fixed and how much it is changing and to what extent.

4. Problem in reporting – It is difficult to communicate the report as the meaning of expense

differs from person to person. For example, many individuals do not know that the

finance cost is the amount that is been paid as an interest. So while calculating the

interest coverage ratio, such person will not be able to understand that they have to

consider the amount of finance cost under it. This will create a problem to the manager.

5. Usage of different methods for calculation of expenses – Different companies uses

various methods for the determination of the amount of expense. Such as the method of

depreciation is different in all firms which creates problems in conducting comparison

(Sjögren, and Fernler, 2019).

Thus, it is very difficult for the mangers to use the concept of cost in all their processes. It

not only creates problem in making budget but also in making various decisions like cost of

product. Thus, they should keep the facts in mind that the meaning of costs differs for all and

sometimes are hidden so they should be vigilant while dealing in them.

CONCLUSION

From the above report it can be analysed that it can be analysed that the it is necessary for

the organisations to conduct appraisal of all the available investment proposals. This helps in

recognising that whether a particular amount should be invested in the business or not. Through

this the companies can also make comparison among different projects. There are various

techniques that helps in ascertaining that whether the money that is invested today will be worth

enough in future or not. But for this it is important for the companies to make the correct

estimation of figures which is really difficult. It is a complicated process as there is not proper

definition for these cost and it differers from person to person. Also the impact of external factor

on this value is not easy. It is very much challenging to get knowledge about the hidden costs

that are not easy to detect. Thus the company should look at the all the aspects before making

any anticipation.

From the above report it can be analysed that it can be analysed that the it is necessary for

the organisations to conduct appraisal of all the available investment proposals. This helps in

recognising that whether a particular amount should be invested in the business or not. Through

this the companies can also make comparison among different projects. There are various

techniques that helps in ascertaining that whether the money that is invested today will be worth

enough in future or not. But for this it is important for the companies to make the correct

estimation of figures which is really difficult. It is a complicated process as there is not proper

definition for these cost and it differers from person to person. Also the impact of external factor

on this value is not easy. It is very much challenging to get knowledge about the hidden costs

that are not easy to detect. Thus the company should look at the all the aspects before making

any anticipation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.