ACC 203 Managerial Accounting

VerifiedAdded on 2021/12/08

|7

|1251

|26

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT ACCOUNTING

STUDENT ID:

[Pick the date]

STUDENT ID:

[Pick the date]

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Question 1

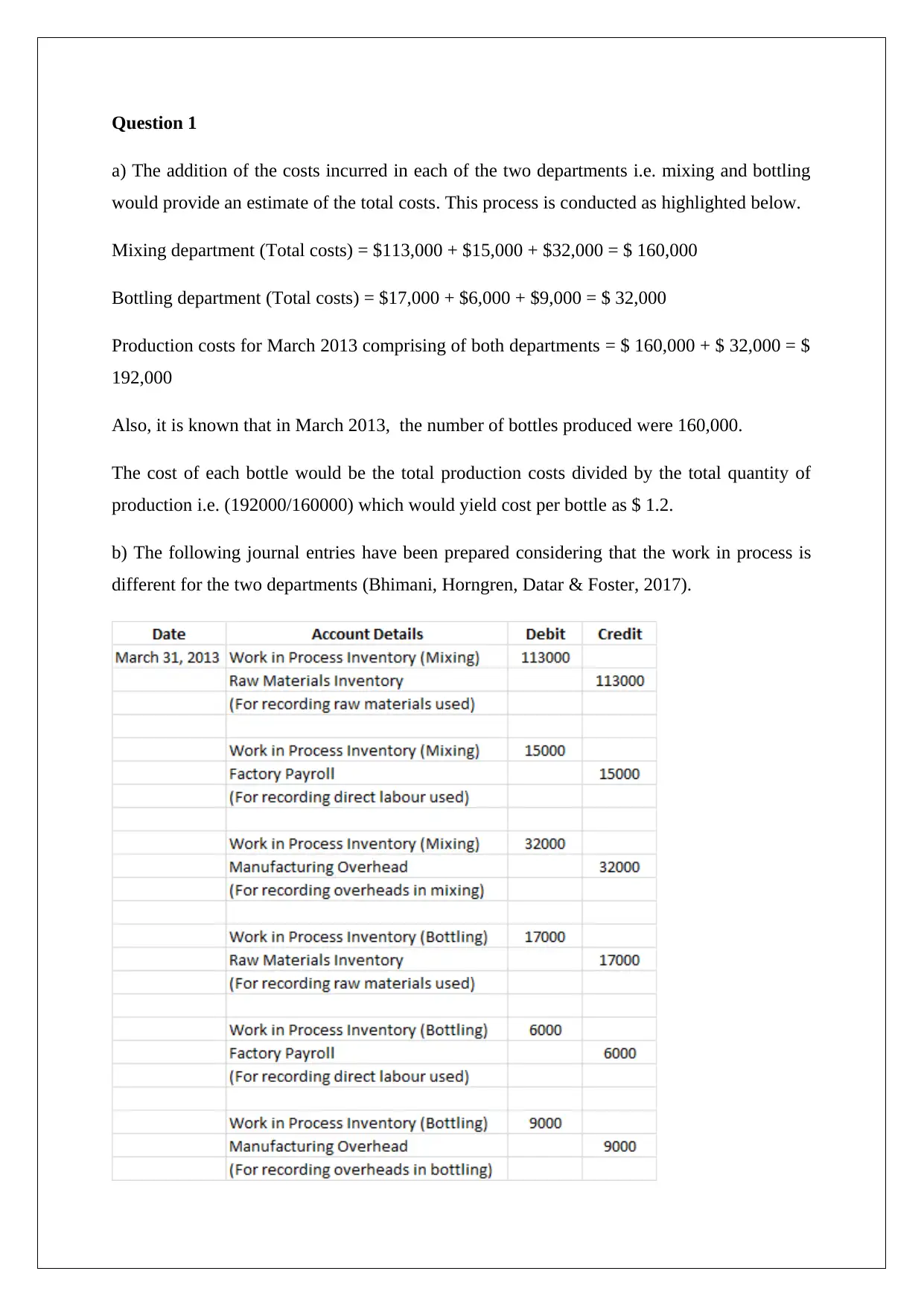

a) The addition of the costs incurred in each of the two departments i.e. mixing and bottling

would provide an estimate of the total costs. This process is conducted as highlighted below.

Mixing department (Total costs) = $113,000 + $15,000 + $32,000 = $ 160,000

Bottling department (Total costs) = $17,000 + $6,000 + $9,000 = $ 32,000

Production costs for March 2013 comprising of both departments = $ 160,000 + $ 32,000 = $

192,000

Also, it is known that in March 2013, the number of bottles produced were 160,000.

The cost of each bottle would be the total production costs divided by the total quantity of

production i.e. (192000/160000) which would yield cost per bottle as $ 1.2.

b) The following journal entries have been prepared considering that the work in process is

different for the two departments (Bhimani, Horngren, Datar & Foster, 2017).

a) The addition of the costs incurred in each of the two departments i.e. mixing and bottling

would provide an estimate of the total costs. This process is conducted as highlighted below.

Mixing department (Total costs) = $113,000 + $15,000 + $32,000 = $ 160,000

Bottling department (Total costs) = $17,000 + $6,000 + $9,000 = $ 32,000

Production costs for March 2013 comprising of both departments = $ 160,000 + $ 32,000 = $

192,000

Also, it is known that in March 2013, the number of bottles produced were 160,000.

The cost of each bottle would be the total production costs divided by the total quantity of

production i.e. (192000/160000) which would yield cost per bottle as $ 1.2.

b) The following journal entries have been prepared considering that the work in process is

different for the two departments (Bhimani, Horngren, Datar & Foster, 2017).

Question 2

a) The formula for direct material price variance is as highlighted below (Damodaran, 2015).

Direct Material Price Variance (SP-AP)*AQ

Based on the given information, SP = $7.2/kg, AP = $7.4/kg and AQ = ($31.080/7.4) = 4,200

kg

The variance computed above is unfavourable owing to the fact that the actual price per unit

material exceeded the budgeted or standard price per unit material.

b) The formula for direct material usage variance is as highlighted below (Parrino & Kidwell,

2014).

Direct Material Usage Variance = (AQ-SQ)*SP

Based on the given information, SP = $ 7.2 per kg, SQ = 2*2000 = 4,000 kg, AQ =

($31.080/7.4) = 4,200 kg

The variance computed above is unfavourable owing to the fact that the actual consumption

of quantity has exceeded the expected or budgeted quantity consumption.

c) The formula for direct labour rate variance is as highlighted below (Drury, 2016).

Direct labour rate variance = (AR-SR)*AH

Based on the given information, AR = $18.30/hr, SR =$18/hr, AH= ($118,035/18.3) = 6,450

hours

The variance computed above is unfavourable owing to the fact that the actual labour cost

exceeded the budgeted or standard labour cost per hour.

a) The formula for direct material price variance is as highlighted below (Damodaran, 2015).

Direct Material Price Variance (SP-AP)*AQ

Based on the given information, SP = $7.2/kg, AP = $7.4/kg and AQ = ($31.080/7.4) = 4,200

kg

The variance computed above is unfavourable owing to the fact that the actual price per unit

material exceeded the budgeted or standard price per unit material.

b) The formula for direct material usage variance is as highlighted below (Parrino & Kidwell,

2014).

Direct Material Usage Variance = (AQ-SQ)*SP

Based on the given information, SP = $ 7.2 per kg, SQ = 2*2000 = 4,000 kg, AQ =

($31.080/7.4) = 4,200 kg

The variance computed above is unfavourable owing to the fact that the actual consumption

of quantity has exceeded the expected or budgeted quantity consumption.

c) The formula for direct labour rate variance is as highlighted below (Drury, 2016).

Direct labour rate variance = (AR-SR)*AH

Based on the given information, AR = $18.30/hr, SR =$18/hr, AH= ($118,035/18.3) = 6,450

hours

The variance computed above is unfavourable owing to the fact that the actual labour cost

exceeded the budgeted or standard labour cost per hour.

d) The formula for direct labour efficiency variance is as highlighted below (Damodaran,

2015).

Direct labour efficiency variance = (AH-SH)*SR

Based on the given information, SR =$18 per hour, SH = 3.5*2000 = 7,000 hours, AH =

($118,035/18.3) = 6,450 hours

The variance computed above is favourable owing to the fact that the actual hours consumed

for production are lower than the standard or budgeted hours expected for the production at

the standard rate.

Question 3

a) The financial analysis that Sam has conducted in regards to the fruit juice business is not

correct as the costs considered for computing profit are not limited to only the incremental

costs that have been incurred because of the juice business. Taking into consideration the

costs which were present to the same quantum before the business was established leads to

over estimation of the costs and under estimation of the actual profitability of the business

operations which is taking place for the juice business (Brealey, Myers & Allen, 2014).

b) The appropriate financial analysis for the juice corner business is summarised below.

It is noteworthy that the above analysis does not include the following costs (Petty et. al.,

2015).

2015).

Direct labour efficiency variance = (AH-SH)*SR

Based on the given information, SR =$18 per hour, SH = 3.5*2000 = 7,000 hours, AH =

($118,035/18.3) = 6,450 hours

The variance computed above is favourable owing to the fact that the actual hours consumed

for production are lower than the standard or budgeted hours expected for the production at

the standard rate.

Question 3

a) The financial analysis that Sam has conducted in regards to the fruit juice business is not

correct as the costs considered for computing profit are not limited to only the incremental

costs that have been incurred because of the juice business. Taking into consideration the

costs which were present to the same quantum before the business was established leads to

over estimation of the costs and under estimation of the actual profitability of the business

operations which is taking place for the juice business (Brealey, Myers & Allen, 2014).

b) The appropriate financial analysis for the juice corner business is summarised below.

It is noteworthy that the above analysis does not include the following costs (Petty et. al.,

2015).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Building Depreciation – This was being incurred to the same even when juice counter

had not been established and hence no contribution from the same should be

attributed to this business.

Manager Salary – The salary of the manager existed before the establishing of the

juice counter and owing to the setting of this business, there has not been any

incremental rise in the manager’s salary. Hence, incremental effect of the juice

business on salary of manager is zero.

It is noteworthy that utility costs attributed to the business have been included owing to

incremental utility consumption by the business.

Question 4

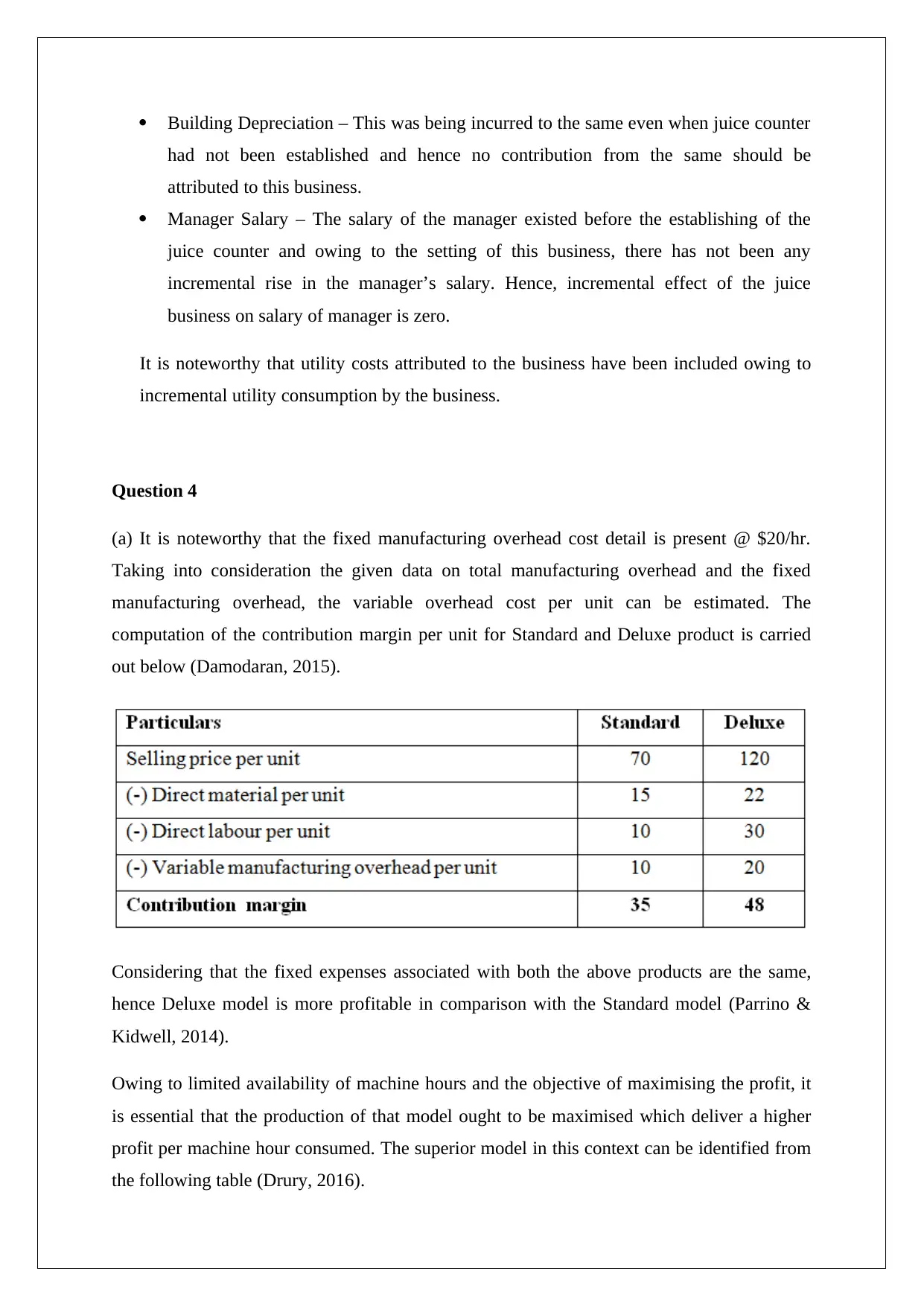

(a) It is noteworthy that the fixed manufacturing overhead cost detail is present @ $20/hr.

Taking into consideration the given data on total manufacturing overhead and the fixed

manufacturing overhead, the variable overhead cost per unit can be estimated. The

computation of the contribution margin per unit for Standard and Deluxe product is carried

out below (Damodaran, 2015).

Considering that the fixed expenses associated with both the above products are the same,

hence Deluxe model is more profitable in comparison with the Standard model (Parrino &

Kidwell, 2014).

Owing to limited availability of machine hours and the objective of maximising the profit, it

is essential that the production of that model ought to be maximised which deliver a higher

profit per machine hour consumed. The superior model in this context can be identified from

the following table (Drury, 2016).

had not been established and hence no contribution from the same should be

attributed to this business.

Manager Salary – The salary of the manager existed before the establishing of the

juice counter and owing to the setting of this business, there has not been any

incremental rise in the manager’s salary. Hence, incremental effect of the juice

business on salary of manager is zero.

It is noteworthy that utility costs attributed to the business have been included owing to

incremental utility consumption by the business.

Question 4

(a) It is noteworthy that the fixed manufacturing overhead cost detail is present @ $20/hr.

Taking into consideration the given data on total manufacturing overhead and the fixed

manufacturing overhead, the variable overhead cost per unit can be estimated. The

computation of the contribution margin per unit for Standard and Deluxe product is carried

out below (Damodaran, 2015).

Considering that the fixed expenses associated with both the above products are the same,

hence Deluxe model is more profitable in comparison with the Standard model (Parrino &

Kidwell, 2014).

Owing to limited availability of machine hours and the objective of maximising the profit, it

is essential that the production of that model ought to be maximised which deliver a higher

profit per machine hour consumed. The superior model in this context can be identified from

the following table (Drury, 2016).

Hence, it is apparent that for the month of June, superior option is Standard model.

b) It is known that standard model monthly demand is 40,000 units which would need to b

fulfilled on priority. Since every unit of standard model consumes 1 hour of machine hour,

thus 40,000 machine hours would be consumed. Since, 60000 machine hours were available

at the beginning of June, hence 20,000 machine hours would be left which would be used for

production of the Deluxe model. As Deluxe model consumer two machine hour for producing

one unit, hence number of units produced for this model would be (20000/2) = 10,000 units

In the month of June, the company should produce 40,000 and 10,000 units of standard and

deluxe model respectively for maximising profits.

b) It is known that standard model monthly demand is 40,000 units which would need to b

fulfilled on priority. Since every unit of standard model consumes 1 hour of machine hour,

thus 40,000 machine hours would be consumed. Since, 60000 machine hours were available

at the beginning of June, hence 20,000 machine hours would be left which would be used for

production of the Deluxe model. As Deluxe model consumer two machine hour for producing

one unit, hence number of units produced for this model would be (20000/2) = 10,000 units

In the month of June, the company should produce 40,000 and 10,000 units of standard and

deluxe model respectively for maximising profits.

References

Bhimani, A., Horngren, C.T., Datar, S.M. & Foster, G. (2017), Management and Cost

Accounting 4th ed. Harlow: Prentice Hall/Financial Times

Brealey, R. A., Myers, S. C. & Allen, F. (2014) Principles of corporate finance, 6th ed. New

York: McGraw-Hill Publications

Damodaran, A. (2015). Applied corporate finance: A user’s manual 3rd ed. New York:

Wiley, John & Sons.

Drury, C. (2016) Cost and Management Accounting: An Introduction. 6th ed. New York:

Cengage Learning

Parrino, R. & Kidwell, D. (2014) Fundamentals of Corporate Finance, 3rd ed. London:

Wiley Publications

Petty, J.W., Titman, S., Keown, A., Martin, J.D., Martin, P., Burrow, M. & Nguyen, H. (2015).

Financial Management, Principles and Applications, 6th ed.. NSW: Pearson Education,

French Forest Australia

Bhimani, A., Horngren, C.T., Datar, S.M. & Foster, G. (2017), Management and Cost

Accounting 4th ed. Harlow: Prentice Hall/Financial Times

Brealey, R. A., Myers, S. C. & Allen, F. (2014) Principles of corporate finance, 6th ed. New

York: McGraw-Hill Publications

Damodaran, A. (2015). Applied corporate finance: A user’s manual 3rd ed. New York:

Wiley, John & Sons.

Drury, C. (2016) Cost and Management Accounting: An Introduction. 6th ed. New York:

Cengage Learning

Parrino, R. & Kidwell, D. (2014) Fundamentals of Corporate Finance, 3rd ed. London:

Wiley Publications

Petty, J.W., Titman, S., Keown, A., Martin, J.D., Martin, P., Burrow, M. & Nguyen, H. (2015).

Financial Management, Principles and Applications, 6th ed.. NSW: Pearson Education,

French Forest Australia

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.