Management Accounting Report: Financial Statement Analysis and MAS

VerifiedAdded on 2023/01/11

|12

|3177

|57

Report

AI Summary

This report delves into the realm of management accounting, exploring various techniques and their applications within a business context, specifically using Prime Furniture Limited as a case study. It begins with an introduction to management accounting and its role in decision-making, followed by an in-depth analysis of cost assessment methods, including absorption and marginal costing, with calculations and comparisons. The report then examines budgetary control techniques, outlining their benefits and limitations, and discusses alternative budgeting methods like cash budgets and pricing strategies. Furthermore, it explores the use of Management Accounting Systems (MAS) in resolving financial issues, providing insights into how these systems can be leveraged to overcome challenges. The report covers product costing, inventory management, strategic planning and SWOT analysis. Overall, the report provides a comprehensive overview of management accounting principles and their practical application in financial management, offering valuable insights for students studying accounting and finance.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK 2............................................................................................................................................3

P3. Cost assessment and review of the financial statements by the method of marginal

and absorption........................................................................................................................3

TASK 3............................................................................................................................................7

P4. Limitations and drawbacks of budget management techniques in planning....................7

TASK 4............................................................................................................................................9

P5.MAS use to resolve and overcome financial issues..........................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

TASK 2............................................................................................................................................3

P3. Cost assessment and review of the financial statements by the method of marginal

and absorption........................................................................................................................3

TASK 3............................................................................................................................................7

P4. Limitations and drawbacks of budget management techniques in planning....................7

TASK 4............................................................................................................................................9

P5.MAS use to resolve and overcome financial issues..........................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

The term MA is defined as a method of actually creating records, with the support of

monetary and non - monetary details within company to make crucial decision. There is a range

of methods, including absorption, marginal for creating financial reports to describe the net

income (Arroyo, 2012). The report includes detailed information relevant to particular

accounting processes, planning techniques and MAS to address monetary issues. The company

selected for this particular project is Prime Furniture Limited.

TASK 2

P3. Cost assessment and review of the financial statements by the method of marginal

and absorption.

Micro business methods:

Cost: this might be expressed as the total amount of expenses that emerges to complete various

types of operations as well as facilities of businesses. There are specific costs to regard as fixed

costs that continue with increases in supply level while variable costs tend to adjust as per

increases in output volume. Direct rates are directly connected to the conduct of company

operations, and additional costs are conversely.

CV analysis: Cost-benefit assessment is a structured method for the definition of advantages and

disadvantages of options used to determine the right effect approach while maintaining costs,

also referred to as cost-benefit assessment.

Variability in cost: this can be regarded as a process of assessing the variability proportion

between real cost as well as expected cost throughout a particular program within business

during accounting period. This is presented in ways that are unfavourable and beneficial to the

company.

The description of some costing methods which help to prepare statement and extract net

profit is stated as follows:

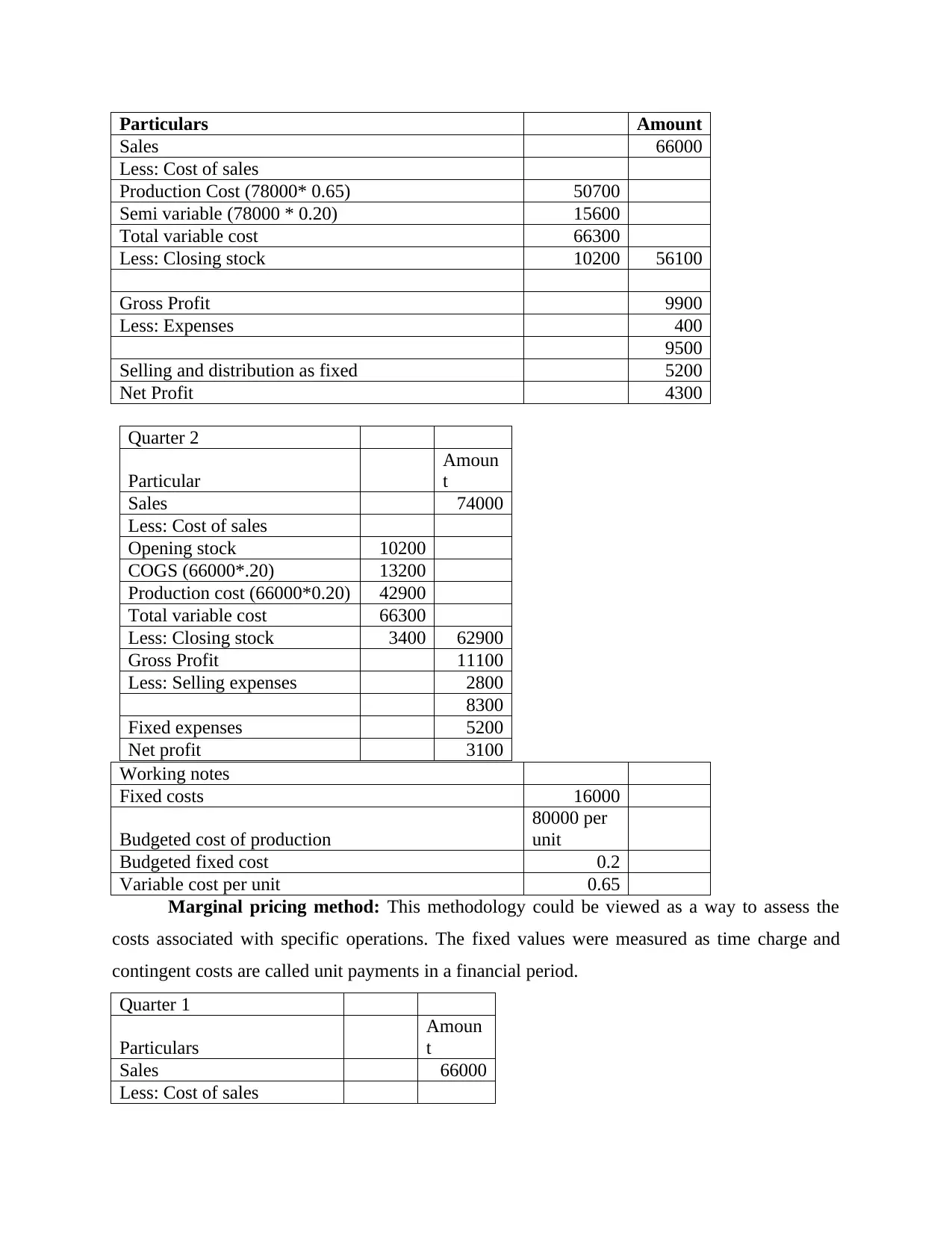

Absorption costing method: It is a category of costing methodology which calculates and

usually allocates the values of different operation of business. The worth of the item is defined as

continuous and unfixed spending (Chenhall and Moers, 2015).

Calculation of net profit as per absorption costing.

Quarter 1

The term MA is defined as a method of actually creating records, with the support of

monetary and non - monetary details within company to make crucial decision. There is a range

of methods, including absorption, marginal for creating financial reports to describe the net

income (Arroyo, 2012). The report includes detailed information relevant to particular

accounting processes, planning techniques and MAS to address monetary issues. The company

selected for this particular project is Prime Furniture Limited.

TASK 2

P3. Cost assessment and review of the financial statements by the method of marginal

and absorption.

Micro business methods:

Cost: this might be expressed as the total amount of expenses that emerges to complete various

types of operations as well as facilities of businesses. There are specific costs to regard as fixed

costs that continue with increases in supply level while variable costs tend to adjust as per

increases in output volume. Direct rates are directly connected to the conduct of company

operations, and additional costs are conversely.

CV analysis: Cost-benefit assessment is a structured method for the definition of advantages and

disadvantages of options used to determine the right effect approach while maintaining costs,

also referred to as cost-benefit assessment.

Variability in cost: this can be regarded as a process of assessing the variability proportion

between real cost as well as expected cost throughout a particular program within business

during accounting period. This is presented in ways that are unfavourable and beneficial to the

company.

The description of some costing methods which help to prepare statement and extract net

profit is stated as follows:

Absorption costing method: It is a category of costing methodology which calculates and

usually allocates the values of different operation of business. The worth of the item is defined as

continuous and unfixed spending (Chenhall and Moers, 2015).

Calculation of net profit as per absorption costing.

Quarter 1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars Amount

Sales 66000

Less: Cost of sales

Production Cost (78000* 0.65) 50700

Semi variable (78000 * 0.20) 15600

Total variable cost 66300

Less: Closing stock 10200 56100

Gross Profit 9900

Less: Expenses 400

9500

Selling and distribution as fixed 5200

Net Profit 4300

Quarter 2

Particular

Amoun

t

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*.20) 13200

Production cost (66000*0.20) 42900

Total variable cost 66300

Less: Closing stock 3400 62900

Gross Profit 11100

Less: Selling expenses 2800

8300

Fixed expenses 5200

Net profit 3100

Working notes

Fixed costs 16000

Budgeted cost of production

80000 per

unit

Budgeted fixed cost 0.2

Variable cost per unit 0.65

Marginal pricing method: This methodology could be viewed as a way to assess the

costs associated with specific operations. The fixed values were measured as time charge and

contingent costs are called unit payments in a financial period.

Quarter 1

Particulars

Amoun

t

Sales 66000

Less: Cost of sales

Sales 66000

Less: Cost of sales

Production Cost (78000* 0.65) 50700

Semi variable (78000 * 0.20) 15600

Total variable cost 66300

Less: Closing stock 10200 56100

Gross Profit 9900

Less: Expenses 400

9500

Selling and distribution as fixed 5200

Net Profit 4300

Quarter 2

Particular

Amoun

t

Sales 74000

Less: Cost of sales

Opening stock 10200

COGS (66000*.20) 13200

Production cost (66000*0.20) 42900

Total variable cost 66300

Less: Closing stock 3400 62900

Gross Profit 11100

Less: Selling expenses 2800

8300

Fixed expenses 5200

Net profit 3100

Working notes

Fixed costs 16000

Budgeted cost of production

80000 per

unit

Budgeted fixed cost 0.2

Variable cost per unit 0.65

Marginal pricing method: This methodology could be viewed as a way to assess the

costs associated with specific operations. The fixed values were measured as time charge and

contingent costs are called unit payments in a financial period.

Quarter 1

Particulars

Amoun

t

Sales 66000

Less: Cost of sales

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

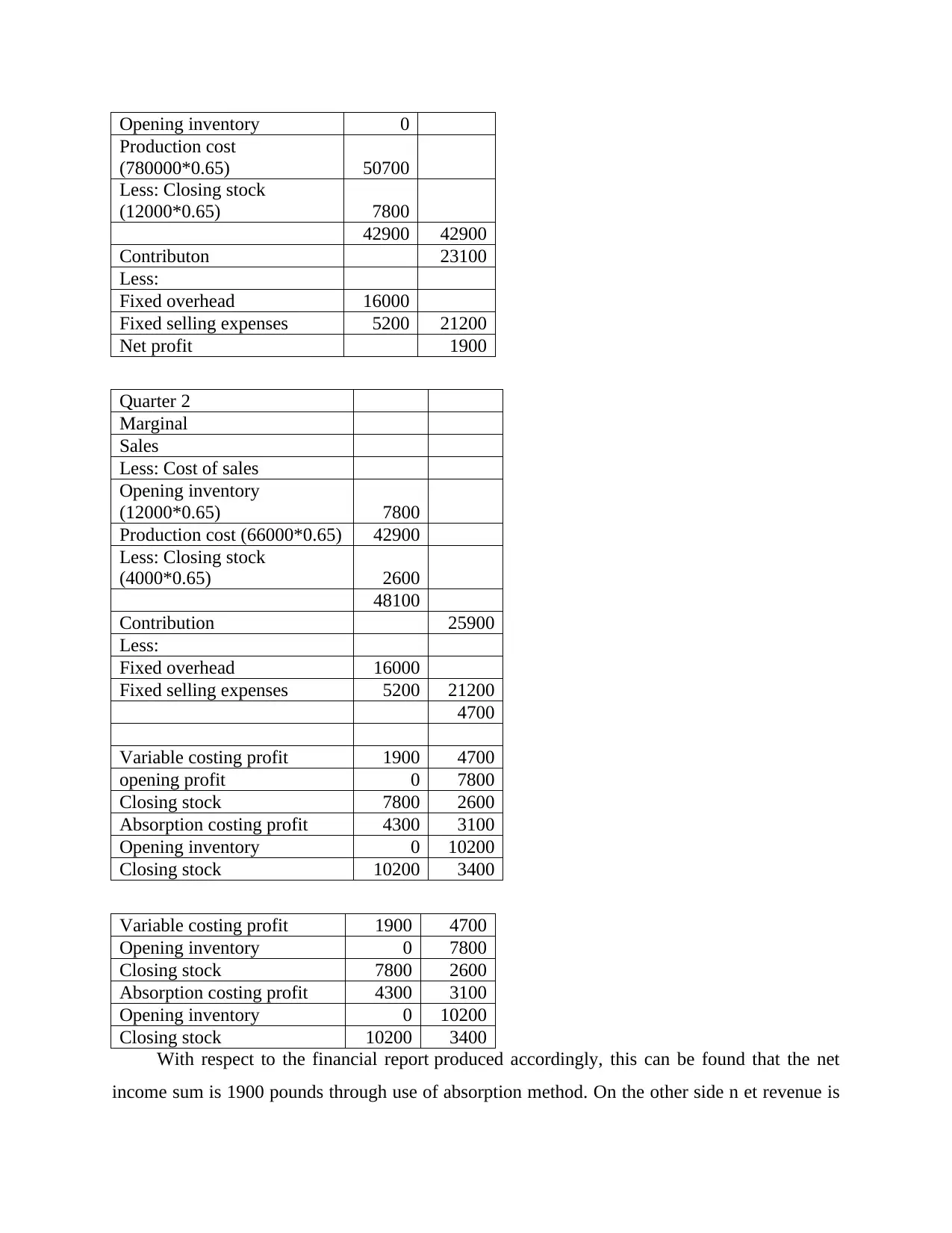

Opening inventory 0

Production cost

(780000*0.65) 50700

Less: Closing stock

(12000*0.65) 7800

42900 42900

Contributon 23100

Less:

Fixed overhead 16000

Fixed selling expenses 5200 21200

Net profit 1900

Quarter 2

Marginal

Sales

Less: Cost of sales

Opening inventory

(12000*0.65) 7800

Production cost (66000*0.65) 42900

Less: Closing stock

(4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed selling expenses 5200 21200

4700

Variable costing profit 1900 4700

opening profit 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

Variable costing profit 1900 4700

Opening inventory 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

With respect to the financial report produced accordingly, this can be found that the net

income sum is 1900 pounds through use of absorption method. On the other side n et revenue is

Production cost

(780000*0.65) 50700

Less: Closing stock

(12000*0.65) 7800

42900 42900

Contributon 23100

Less:

Fixed overhead 16000

Fixed selling expenses 5200 21200

Net profit 1900

Quarter 2

Marginal

Sales

Less: Cost of sales

Opening inventory

(12000*0.65) 7800

Production cost (66000*0.65) 42900

Less: Closing stock

(4000*0.65) 2600

48100

Contribution 25900

Less:

Fixed overhead 16000

Fixed selling expenses 5200 21200

4700

Variable costing profit 1900 4700

opening profit 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

Variable costing profit 1900 4700

Opening inventory 0 7800

Closing stock 7800 2600

Absorption costing profit 4300 3100

Opening inventory 0 10200

Closing stock 10200 3400

With respect to the financial report produced accordingly, this can be found that the net

income sum is 1900 pounds through use of absorption method. On the other side n et revenue is

4700 pounds through using marginal costing method. Under both approaches, cost consideration

is the explanation for the income volatility in different situations. Along with handling of fixed

costs under absorption as the degree of output is measured for entire period.

Product costing:

Fixed cost: This is a type of costing that cannot be changed or adjusted result of a change in

output volume.

Variable cost: This is really a component of cost that can be changed or influenced as a result of

variability throughout the production quantity.

Standard or normal costing: It calculation contrasts the expected expense to the actual cost in

the financial records. The variations between the estimated as well as the actual expense are then

identified and explanations for variance are determined.

ABC technique of pricing: It really is a type of cost accounting that recognises company's

operations and regulations fees between each procedure according to the real use from each other

product / service. The approach applies to indirect expenditures and more real losses than normal

costs.

Costing role in price setting: Costing literally performs an crucial role in determining costs, as

companies change pricing on the basis of the same. This means that, if premiums are greater than

estimates, firms set low costs which really enable them deliver fewer units of products by paying

enough attention to a wide range of consumers and vise - versa.

Cost of inventory:

Inventory costs: These are the charges involved in gathering, transportation and enhancement of

an inventory stock management during a financial year. There were different categories of

inventory expenditures that are as defined in the following:

• Order costs

• Extra features to bear

• Retail Costs

• Recruitment Expenses

Types of Stock Assessment:

• FIFO: This is also a form of device connected with the manufacture of products that

comes first in the factories to be included in every current market at the very first.

is the explanation for the income volatility in different situations. Along with handling of fixed

costs under absorption as the degree of output is measured for entire period.

Product costing:

Fixed cost: This is a type of costing that cannot be changed or adjusted result of a change in

output volume.

Variable cost: This is really a component of cost that can be changed or influenced as a result of

variability throughout the production quantity.

Standard or normal costing: It calculation contrasts the expected expense to the actual cost in

the financial records. The variations between the estimated as well as the actual expense are then

identified and explanations for variance are determined.

ABC technique of pricing: It really is a type of cost accounting that recognises company's

operations and regulations fees between each procedure according to the real use from each other

product / service. The approach applies to indirect expenditures and more real losses than normal

costs.

Costing role in price setting: Costing literally performs an crucial role in determining costs, as

companies change pricing on the basis of the same. This means that, if premiums are greater than

estimates, firms set low costs which really enable them deliver fewer units of products by paying

enough attention to a wide range of consumers and vise - versa.

Cost of inventory:

Inventory costs: These are the charges involved in gathering, transportation and enhancement of

an inventory stock management during a financial year. There were different categories of

inventory expenditures that are as defined in the following:

• Order costs

• Extra features to bear

• Retail Costs

• Recruitment Expenses

Types of Stock Assessment:

• FIFO: This is also a form of device connected with the manufacture of products that

comes first in the factories to be included in every current market at the very first.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

• LIFO: It is basically a technique that can be related to collecting products for final output

from the warehouse on the grounds from last through first out.

• Weighted average costing method: The technique aims to determine the stock prices of

the business, and measures the total price of a consumer commodity based on the position

of some other item’s amount.

TASK 3

P4. Limitations and drawbacks of budget management techniques in planning.

Budgetary control: It can also be defined as a sort of policy that aims to govern both

financial that pro-financial results on the basis of several different forms of budget.

Throughout this element of budget component is crucial even though, with the support of

these strategic strategy, business organization takes proper measures to generate further

outcomes. It contains a variety of budgets that are used by the manager of prime furniture

these are defined as follows:

• Operation budget: it really is a form of budget allowing managers to determine the

quantity of products necessary to finish the different operations over a given time

period (Tucker and Lowe, 2014). The auditors use this budget prepares the

calculation of various projects and tasks within Prime Furniture Limited that also

helps management to make appropriate decisions. Under this program, the

management take corrective measures to meet the objectives by carrying out the

actions stated. The primary benefits and drawbacks below were mentioned:

Benefits: Manager Benefit from this framework when calculating the supply of alternative types

of technology used throughout prime furniture to meet the optimal goal in specified timeframe.

Drawbacks: The key concerns with that kind of expenditure plan is that it still requires a lot of

extra time as well as expenses for the allocation of funds which directly increase the total costs

for prime furniture.

• Capital expenditure plan: All departments and units would include total monthly

expenditure plan about capital requirement within company. This finds that

monitoring sales income; production efficiency etc. is a dynamic and costly market

practice. In accordance with Prime Furniture, manager use take advantage through

from the warehouse on the grounds from last through first out.

• Weighted average costing method: The technique aims to determine the stock prices of

the business, and measures the total price of a consumer commodity based on the position

of some other item’s amount.

TASK 3

P4. Limitations and drawbacks of budget management techniques in planning.

Budgetary control: It can also be defined as a sort of policy that aims to govern both

financial that pro-financial results on the basis of several different forms of budget.

Throughout this element of budget component is crucial even though, with the support of

these strategic strategy, business organization takes proper measures to generate further

outcomes. It contains a variety of budgets that are used by the manager of prime furniture

these are defined as follows:

• Operation budget: it really is a form of budget allowing managers to determine the

quantity of products necessary to finish the different operations over a given time

period (Tucker and Lowe, 2014). The auditors use this budget prepares the

calculation of various projects and tasks within Prime Furniture Limited that also

helps management to make appropriate decisions. Under this program, the

management take corrective measures to meet the objectives by carrying out the

actions stated. The primary benefits and drawbacks below were mentioned:

Benefits: Manager Benefit from this framework when calculating the supply of alternative types

of technology used throughout prime furniture to meet the optimal goal in specified timeframe.

Drawbacks: The key concerns with that kind of expenditure plan is that it still requires a lot of

extra time as well as expenses for the allocation of funds which directly increase the total costs

for prime furniture.

• Capital expenditure plan: All departments and units would include total monthly

expenditure plan about capital requirement within company. This finds that

monitoring sales income; production efficiency etc. is a dynamic and costly market

practice. In accordance with Prime Furniture, manager use take advantage through

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

this budget and make sure that no extra capital must be used in any operation if once

the capital is allocated.

Benefits: The financial condition of Prime Limited Furniture has been assessed with a

description of the detailed budget which manager maintain while allocating and using capital.

Drawback: The greatest drawback about this program is that improvements under it are

difficult to implement, resulting in a pressure on the management of the relevant organization

impacting the amount of efficiency within the given period of time (Kokubu and Kitada,

2015).

Alternative budgeting method

Cash budget: This is a document describing both monetary sales and costs as well as

reflecting on expectations over a particular time span in the financial statements. The final cash

budget is produced after preparing of all expenses such as overall budget, capital expenditure,

profit planning, and transaction spending plan (Hiebl, 2014). Consequently financial products

and investments and expenditure can be reported in this budget. It really is a document that is

designed primarily for external players which is not readily modifiable after publication. This

budget is structured in the sense of the Prime furniture that has some benefits and drawbacks:

Benefits: This allows Prime furniture to manage cash expenses and income on a daily basis and

allow clear provisions that could be used to cover any constraints that occur and impair market

efficiency.

Drawbacks: This strategy relies on estimates, and for long term financial plans, businesses

cannot fully rely upon the same. Therefore, each procedure must be closely checked by the boss

of the particular organization and identify the cash used throughout the project which can be an

exhausting and labour intensive task.

Price:

Strategies for pricing:

• Pricing penetration strategy: The penetration sales model effectively reduces the

expenses of products and services to quickly reach a large market share. The approach

operates for consumers who turn into another new company and consume products at a

reasonable price.

• Skimming pricing strategy: Price skimming is basically a successful pricing technique

whereby a selling firm initially sets a fairly hefty premium per service or product and

the capital is allocated.

Benefits: The financial condition of Prime Limited Furniture has been assessed with a

description of the detailed budget which manager maintain while allocating and using capital.

Drawback: The greatest drawback about this program is that improvements under it are

difficult to implement, resulting in a pressure on the management of the relevant organization

impacting the amount of efficiency within the given period of time (Kokubu and Kitada,

2015).

Alternative budgeting method

Cash budget: This is a document describing both monetary sales and costs as well as

reflecting on expectations over a particular time span in the financial statements. The final cash

budget is produced after preparing of all expenses such as overall budget, capital expenditure,

profit planning, and transaction spending plan (Hiebl, 2014). Consequently financial products

and investments and expenditure can be reported in this budget. It really is a document that is

designed primarily for external players which is not readily modifiable after publication. This

budget is structured in the sense of the Prime furniture that has some benefits and drawbacks:

Benefits: This allows Prime furniture to manage cash expenses and income on a daily basis and

allow clear provisions that could be used to cover any constraints that occur and impair market

efficiency.

Drawbacks: This strategy relies on estimates, and for long term financial plans, businesses

cannot fully rely upon the same. Therefore, each procedure must be closely checked by the boss

of the particular organization and identify the cash used throughout the project which can be an

exhausting and labour intensive task.

Price:

Strategies for pricing:

• Pricing penetration strategy: The penetration sales model effectively reduces the

expenses of products and services to quickly reach a large market share. The approach

operates for consumers who turn into another new company and consume products at a

reasonable price.

• Skimming pricing strategy: Price skimming is basically a successful pricing technique

whereby a selling firm initially sets a fairly hefty premium per service or product and

then reduces the price over time. The business, when first market demand is satisfied,

then lowers the price to draw more market-sensitive parties.

How competitors determine prices?

By maintaining in agree with the current global business dynamics and activities of

competing companies in the same sector, enterprises have used to determine the most acceptable

costs. They analyse essential components that have now been done by other businesses and

develop strategies that concentrate on lowering operational costs and maintaining a reasonable

quality of goods and services which help in generating real income and raise market share.

Consideration of supply-demand: Supply and demand are an economic theory from

which rates are set within each market. This means that, unless the appropriate amount (at

current prices) for a given commodity, such as labour and liquid capital resources, is set at a rate

equal to the total sold (at current prices), which will be equal to organized economic demand and

supply.

Strategic planning:

SWOT Analysis: It really is a process of measuring the institution's strength, weakness,

opportunities and threats over a specified period of time. This provides a strong base for

company to make crucial decision which can lead to expanding of business in shorter time. Some

of its benefits and disadvantages as:

Benefits: The SWOT analysis can involve an agency, an organizational unit, a person or a team.

The SWOT approach, for example, can be used to evaluate a product or service, merger or

partnership or to relocate an existing sector. This also assists in assessing a particular production

point, economic process and also sales volume or implementation of Prime furniture.

Drawbacks: This method lacks a structure to rank the significance of one component above

others. Additionally it is difficult to assess the true effect of each aspect on the target.

TASK 4

P5.MAS use to resolve and overcome financial issues.

In general, the absence of sources of funding causes financial difficulties that cause

problems for firms to conduct competitive operations (Otley and Emmanuel, 2013). Two of the

biggest economic challenges Prime Furniture faces are:

then lowers the price to draw more market-sensitive parties.

How competitors determine prices?

By maintaining in agree with the current global business dynamics and activities of

competing companies in the same sector, enterprises have used to determine the most acceptable

costs. They analyse essential components that have now been done by other businesses and

develop strategies that concentrate on lowering operational costs and maintaining a reasonable

quality of goods and services which help in generating real income and raise market share.

Consideration of supply-demand: Supply and demand are an economic theory from

which rates are set within each market. This means that, unless the appropriate amount (at

current prices) for a given commodity, such as labour and liquid capital resources, is set at a rate

equal to the total sold (at current prices), which will be equal to organized economic demand and

supply.

Strategic planning:

SWOT Analysis: It really is a process of measuring the institution's strength, weakness,

opportunities and threats over a specified period of time. This provides a strong base for

company to make crucial decision which can lead to expanding of business in shorter time. Some

of its benefits and disadvantages as:

Benefits: The SWOT analysis can involve an agency, an organizational unit, a person or a team.

The SWOT approach, for example, can be used to evaluate a product or service, merger or

partnership or to relocate an existing sector. This also assists in assessing a particular production

point, economic process and also sales volume or implementation of Prime furniture.

Drawbacks: This method lacks a structure to rank the significance of one component above

others. Additionally it is difficult to assess the true effect of each aspect on the target.

TASK 4

P5.MAS use to resolve and overcome financial issues.

In general, the absence of sources of funding causes financial difficulties that cause

problems for firms to conduct competitive operations (Otley and Emmanuel, 2013). Two of the

biggest economic challenges Prime Furniture faces are:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

• Accounting record errors: This may be described as a financial problem related to

deliberate or accidental misuse of geometric structures due to incorrect account

preparation. Therefore, the question that has consequences for their financial reporting is

discussed in prime furniture (Suomala and Lyly-Yrjänäinen, 2012).

• Lack of money management: This is consider to be the major financial issue faced by

prime furniture, as lack of proper money circulation leads to delay in business process or

even closure of productive business operation.

MA methods for reacting to financial problems:

• Benchmarking: This method measures its financial aspects of the company to competing

firms with a view to predicting negative variances (Sánchez-Rodríguez and Spraakman,

2012). Manager use the criteria in the aforementioned sector to determine their particular

monetary issue. Management uses the strategic aspects to compete with other businesses

dealing in same industry.

• KPI: This approach can be described by a rational estimation of financial and non-

financial components. The financial aspect includes operational efficiency, expenses etc.

while being components included in non-financial terms; employee stress levels,

relationships, etc. In respective, to prime furniture manager uses financial components to

record all relevant money transaction in order to detect the issue of money

mismanagement.

• Financial governance: This is a technique in which a corporate entity's complete

economic activity is recorded over a span of time (Schaltegger and Burritt, 2017). This

approach recognizes true financial issues and analytical approaches are used to resolve

the issue. In prime furniture planner makes use of strategies to alleviate the

aforementioned problems and take proactive action to eliminate these circumstances in

the future.

Expertise’s of management Accountant:

• Better management skills: The willingness of effective auditors to convey financial

details inside the working community with separate activities will be expanded.

• Good knowledge of accounting ideals: They must be capable of producing financial

reports and also provide sufficient accounting details. These strategic techniques can be

deliberate or accidental misuse of geometric structures due to incorrect account

preparation. Therefore, the question that has consequences for their financial reporting is

discussed in prime furniture (Suomala and Lyly-Yrjänäinen, 2012).

• Lack of money management: This is consider to be the major financial issue faced by

prime furniture, as lack of proper money circulation leads to delay in business process or

even closure of productive business operation.

MA methods for reacting to financial problems:

• Benchmarking: This method measures its financial aspects of the company to competing

firms with a view to predicting negative variances (Sánchez-Rodríguez and Spraakman,

2012). Manager use the criteria in the aforementioned sector to determine their particular

monetary issue. Management uses the strategic aspects to compete with other businesses

dealing in same industry.

• KPI: This approach can be described by a rational estimation of financial and non-

financial components. The financial aspect includes operational efficiency, expenses etc.

while being components included in non-financial terms; employee stress levels,

relationships, etc. In respective, to prime furniture manager uses financial components to

record all relevant money transaction in order to detect the issue of money

mismanagement.

• Financial governance: This is a technique in which a corporate entity's complete

economic activity is recorded over a span of time (Schaltegger and Burritt, 2017). This

approach recognizes true financial issues and analytical approaches are used to resolve

the issue. In prime furniture planner makes use of strategies to alleviate the

aforementioned problems and take proactive action to eliminate these circumstances in

the future.

Expertise’s of management Accountant:

• Better management skills: The willingness of effective auditors to convey financial

details inside the working community with separate activities will be expanded.

• Good knowledge of accounting ideals: They must be capable of producing financial

reports and also provide sufficient accounting details. These strategic techniques can be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

used to address financial challenges. That is because, largely on the basis of this,

commitments can address any kinds of issue but can guide business leaders to fix issues..

Comparison of companies in order to solve financial issues by help of MAS:

Basis of

difference

Sainsbury AlDI’s

Monetary

issue

The business faces challenges due to

the scarcity of monetary capital.

The biggest problem facing the

organization is spending for different

work.

Techniques to

solve issues

This corporation uses benchmarking

tools to tackle the financial problem

and classify flaws in financial reporting

relative to other companies

KPI financial factors that continue to

set the benchmarks at various jobs so

that higher expenditures can be

managed are used to handle the

financial problem aspect.

MAS To overcome the problem business

implements cost accounting program to

monitor and control the total cost

activity.

Managers use to monitor all

expenditures included in project

expenses and make correct budgets to

eliminate excess spending for the next

cycle.

CONCLUSION

In conclusion, it has been founded that MA is a useful process to make internal decision and

increase the profit figures and remove any sort of financial issues faces by company. Different

costing methods are effective in making financial reports are detecting profit for the specified

period. MA system and budgetary tool are valuable for future planning and eliminating of

financial problems.

commitments can address any kinds of issue but can guide business leaders to fix issues..

Comparison of companies in order to solve financial issues by help of MAS:

Basis of

difference

Sainsbury AlDI’s

Monetary

issue

The business faces challenges due to

the scarcity of monetary capital.

The biggest problem facing the

organization is spending for different

work.

Techniques to

solve issues

This corporation uses benchmarking

tools to tackle the financial problem

and classify flaws in financial reporting

relative to other companies

KPI financial factors that continue to

set the benchmarks at various jobs so

that higher expenditures can be

managed are used to handle the

financial problem aspect.

MAS To overcome the problem business

implements cost accounting program to

monitor and control the total cost

activity.

Managers use to monitor all

expenditures included in project

expenses and make correct budgets to

eliminate excess spending for the next

cycle.

CONCLUSION

In conclusion, it has been founded that MA is a useful process to make internal decision and

increase the profit figures and remove any sort of financial issues faces by company. Different

costing methods are effective in making financial reports are detecting profit for the specified

period. MA system and budgetary tool are valuable for future planning and eliminating of

financial problems.

REFERENCES

Books and journal:

Arroyo, P., 2012. Management accounting change and sustainability: an institutional approach.

Journal of Accounting & Organizational Change. 8(3). pp.286-309.

Chenhall, R. H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society. 47. pp.1-13.

DRURY, C. M., 2013. Management and cost accounting. Springer.

Hiebl, M. R., 2014. Upper echelons theory in management accounting and control

research. Journal of Management Control. 24(3). pp.223-240.

Kokubu, K. and Kitada, H., 2015. Material flow cost accounting and existing management

perspectives. Journal of Cleaner Production. 108. pp.1279-1288.

Kotas, R., 2014. Management accounting for hotels and restaurants. Routledge.

Otley, D. and Emmanuel, K. M. C., 2013. Readings in accounting for management control.

Springer.

Sánchez-Rodríguez, C. and Spraakman, G., 2012. ERP systems and management accounting: A

multiple case study. Qualitative Research in Accounting & Management. 9(4). pp.398-

414.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Suomala, P. and Lyly-Yrjänäinen, J., 2012. Management accounting research in practice:

Lessons learned from an interventionist approach. Routledge.

Tucker, B. P. and Lowe, A. D., 2014. Practitioners are from Mars; academics are from Venus?:

An investigation of the research-practice gap in management accounting. Accounting,

Auditing & Accountability Journal. 27(3). pp.394-425.

Books and journal:

Arroyo, P., 2012. Management accounting change and sustainability: an institutional approach.

Journal of Accounting & Organizational Change. 8(3). pp.286-309.

Chenhall, R. H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society. 47. pp.1-13.

DRURY, C. M., 2013. Management and cost accounting. Springer.

Hiebl, M. R., 2014. Upper echelons theory in management accounting and control

research. Journal of Management Control. 24(3). pp.223-240.

Kokubu, K. and Kitada, H., 2015. Material flow cost accounting and existing management

perspectives. Journal of Cleaner Production. 108. pp.1279-1288.

Kotas, R., 2014. Management accounting for hotels and restaurants. Routledge.

Otley, D. and Emmanuel, K. M. C., 2013. Readings in accounting for management control.

Springer.

Sánchez-Rodríguez, C. and Spraakman, G., 2012. ERP systems and management accounting: A

multiple case study. Qualitative Research in Accounting & Management. 9(4). pp.398-

414.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Suomala, P. and Lyly-Yrjänäinen, J., 2012. Management accounting research in practice:

Lessons learned from an interventionist approach. Routledge.

Tucker, B. P. and Lowe, A. D., 2014. Practitioners are from Mars; academics are from Venus?:

An investigation of the research-practice gap in management accounting. Accounting,

Auditing & Accountability Journal. 27(3). pp.394-425.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.