Management Accounting Practices and Research

VerifiedAdded on 2020/10/05

|19

|5458

|483

AI Summary

This document is a comprehensive study on management accounting practices and research. It covers various aspects of management accounting, such as cost analysis, budgeting, and performance evaluation. The assignment also delves into the research-practice gap in management accounting, discussing the differences between academic research and practical applications. It provides an overview of the key concepts, theories, and methodologies related to management accounting, making it a valuable resource for students and professionals in the field.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INRODUCTION..............................................................................................................................1

LO1..................................................................................................................................................1

Management accounting and its different types of system....................................................1

Difference between management accounting and financial accounting................................3

2 Explain different method of management accounting reporting........................................3

Evaluation of benefits of various management accounting systems......................................4

Evaluation of Management Accounting System and Reporting............................................5

LO 2.................................................................................................................................................6

Calculation of income statement using marginal and absorption costs:.................................6

Application of a range of management accounting techniques..............................................9

LO3................................................................................................................................................11

Advantages and disadvantages of different types of planning tools used for budgetary control

..............................................................................................................................................11

Use of different accounting tools and their application for preparing and forecasting budgets.

..............................................................................................................................................13

LO 4...............................................................................................................................................13

How organisation adapting management accounting respond to financial problems..........13

How management accounting can deal with financial problems and attains sustainable

success..................................................................................................................................15

Planning tools to solve financial problems:..........................................................................15

REFRENCES.................................................................................................................................17

Books and journals...............................................................................................................17

INRODUCTION..............................................................................................................................1

LO1..................................................................................................................................................1

Management accounting and its different types of system....................................................1

Difference between management accounting and financial accounting................................3

2 Explain different method of management accounting reporting........................................3

Evaluation of benefits of various management accounting systems......................................4

Evaluation of Management Accounting System and Reporting............................................5

LO 2.................................................................................................................................................6

Calculation of income statement using marginal and absorption costs:.................................6

Application of a range of management accounting techniques..............................................9

LO3................................................................................................................................................11

Advantages and disadvantages of different types of planning tools used for budgetary control

..............................................................................................................................................11

Use of different accounting tools and their application for preparing and forecasting budgets.

..............................................................................................................................................13

LO 4...............................................................................................................................................13

How organisation adapting management accounting respond to financial problems..........13

How management accounting can deal with financial problems and attains sustainable

success..................................................................................................................................15

Planning tools to solve financial problems:..........................................................................15

REFRENCES.................................................................................................................................17

Books and journals...............................................................................................................17

INRODUCTION

Management accounting refers to the process of recording, estimating, analysing and

summarizing the data associated with operations of organisation. It is field of accounting that

studies every features related to company's operation (Erserim, 2012). The main purpose of

preparing such accounts is to ensure the smooth running of business. Techniques and tools such

as cost analysis, budgetary control helps in assessing the expenditure incurred and how the

expenses can be controlled. There are different types of management system we will discuss

them in detail in the following report. Equilibrium asset management is medium-sized financial

consulting firm that lends variety of services to it's clients. This company incorporates different

forms of systems in order to maintain information concerning enterprise to efficiently achieve

goals of the organisation. This method helps in systematically organising functions performed by

several department. Equilibrium asset management provides advices with respect to investment

and wealth management. The following report contains detailed description of management

accounting systems, analysis and advantages and disadvantages of planning tools. Let's examine

them step by step.

LO1

Management accounting and its different types of system.

Management accounting is the systematic process of recording the transaction which

occur daily in the business. The financial transactions which occur daily are recorded in the

books. The process of analysing, summarizing of the these transactions for the top level of

management is known as accounting. Financial statements such as balance sheet, cash flows are

also included in the accounting process and these transactions are recorded by the employees

working in the finance division of the company.

The process in which the business analyse its cost for the preparation of the financial

statements to see the actual position of the company is called the management accounting also

known as the managerial accounting or cost accounting. This helps the management to find out

the problems related to the financial accounting in analysing the financial reports and preparing

it. The main objective of the management accounting is cost optimization and reduce the cost to

help company to survive in the market and stand against its competitors. Management

accounting helps the organisation in decision-making process and planning for the future in order

1

Management accounting refers to the process of recording, estimating, analysing and

summarizing the data associated with operations of organisation. It is field of accounting that

studies every features related to company's operation (Erserim, 2012). The main purpose of

preparing such accounts is to ensure the smooth running of business. Techniques and tools such

as cost analysis, budgetary control helps in assessing the expenditure incurred and how the

expenses can be controlled. There are different types of management system we will discuss

them in detail in the following report. Equilibrium asset management is medium-sized financial

consulting firm that lends variety of services to it's clients. This company incorporates different

forms of systems in order to maintain information concerning enterprise to efficiently achieve

goals of the organisation. This method helps in systematically organising functions performed by

several department. Equilibrium asset management provides advices with respect to investment

and wealth management. The following report contains detailed description of management

accounting systems, analysis and advantages and disadvantages of planning tools. Let's examine

them step by step.

LO1

Management accounting and its different types of system.

Management accounting is the systematic process of recording the transaction which

occur daily in the business. The financial transactions which occur daily are recorded in the

books. The process of analysing, summarizing of the these transactions for the top level of

management is known as accounting. Financial statements such as balance sheet, cash flows are

also included in the accounting process and these transactions are recorded by the employees

working in the finance division of the company.

The process in which the business analyse its cost for the preparation of the financial

statements to see the actual position of the company is called the management accounting also

known as the managerial accounting or cost accounting. This helps the management to find out

the problems related to the financial accounting in analysing the financial reports and preparing

it. The main objective of the management accounting is cost optimization and reduce the cost to

help company to survive in the market and stand against its competitors. Management

accounting helps the organisation in decision-making process and planning for the future in order

1

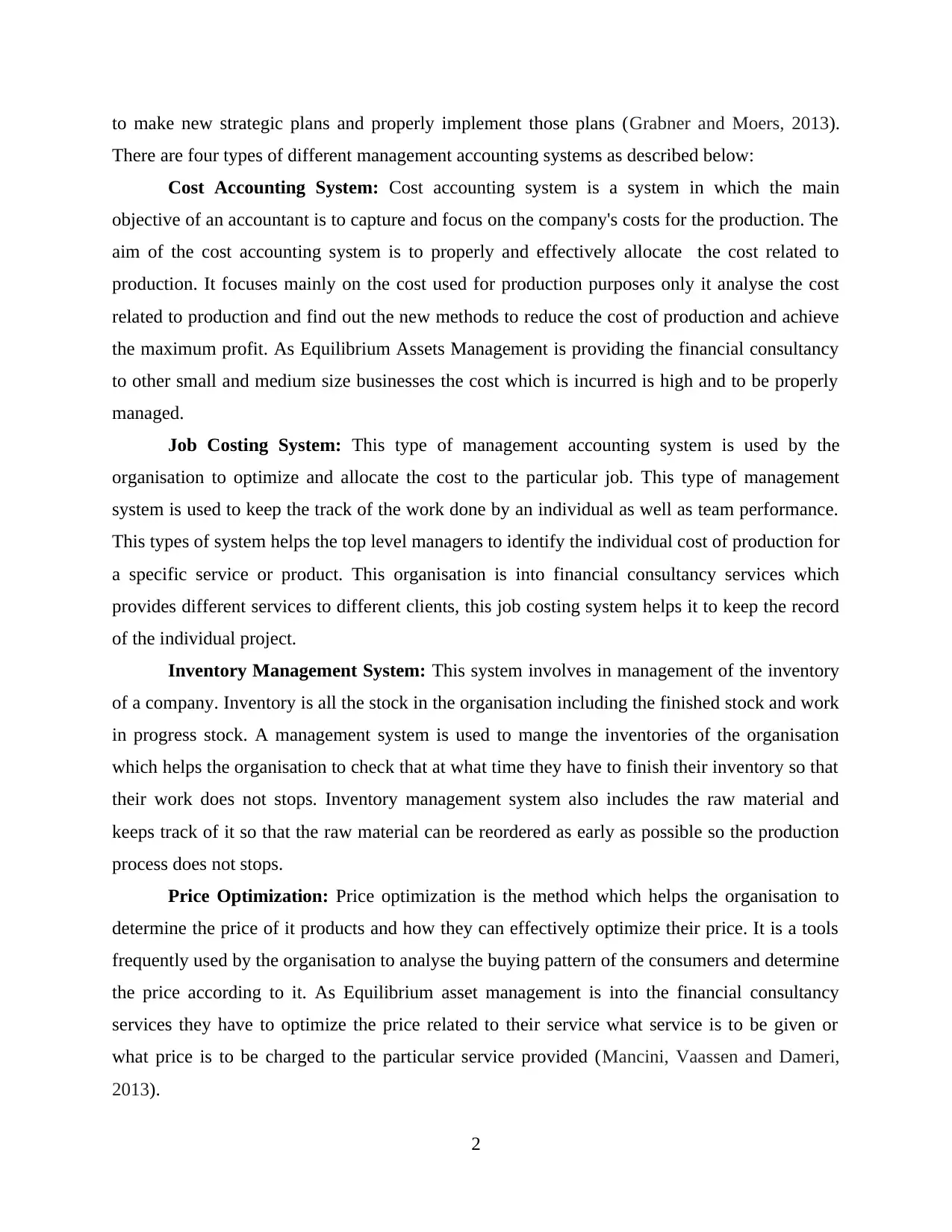

to make new strategic plans and properly implement those plans (Grabner and Moers, 2013).

There are four types of different management accounting systems as described below:

Cost Accounting System: Cost accounting system is a system in which the main

objective of an accountant is to capture and focus on the company's costs for the production. The

aim of the cost accounting system is to properly and effectively allocate the cost related to

production. It focuses mainly on the cost used for production purposes only it analyse the cost

related to production and find out the new methods to reduce the cost of production and achieve

the maximum profit. As Equilibrium Assets Management is providing the financial consultancy

to other small and medium size businesses the cost which is incurred is high and to be properly

managed.

Job Costing System: This type of management accounting system is used by the

organisation to optimize and allocate the cost to the particular job. This type of management

system is used to keep the track of the work done by an individual as well as team performance.

This types of system helps the top level managers to identify the individual cost of production for

a specific service or product. This organisation is into financial consultancy services which

provides different services to different clients, this job costing system helps it to keep the record

of the individual project.

Inventory Management System: This system involves in management of the inventory

of a company. Inventory is all the stock in the organisation including the finished stock and work

in progress stock. A management system is used to mange the inventories of the organisation

which helps the organisation to check that at what time they have to finish their inventory so that

their work does not stops. Inventory management system also includes the raw material and

keeps track of it so that the raw material can be reordered as early as possible so the production

process does not stops.

Price Optimization: Price optimization is the method which helps the organisation to

determine the price of it products and how they can effectively optimize their price. It is a tools

frequently used by the organisation to analyse the buying pattern of the consumers and determine

the price according to it. As Equilibrium asset management is into the financial consultancy

services they have to optimize the price related to their service what service is to be given or

what price is to be charged to the particular service provided (Mancini, Vaassen and Dameri,

2013).

2

There are four types of different management accounting systems as described below:

Cost Accounting System: Cost accounting system is a system in which the main

objective of an accountant is to capture and focus on the company's costs for the production. The

aim of the cost accounting system is to properly and effectively allocate the cost related to

production. It focuses mainly on the cost used for production purposes only it analyse the cost

related to production and find out the new methods to reduce the cost of production and achieve

the maximum profit. As Equilibrium Assets Management is providing the financial consultancy

to other small and medium size businesses the cost which is incurred is high and to be properly

managed.

Job Costing System: This type of management accounting system is used by the

organisation to optimize and allocate the cost to the particular job. This type of management

system is used to keep the track of the work done by an individual as well as team performance.

This types of system helps the top level managers to identify the individual cost of production for

a specific service or product. This organisation is into financial consultancy services which

provides different services to different clients, this job costing system helps it to keep the record

of the individual project.

Inventory Management System: This system involves in management of the inventory

of a company. Inventory is all the stock in the organisation including the finished stock and work

in progress stock. A management system is used to mange the inventories of the organisation

which helps the organisation to check that at what time they have to finish their inventory so that

their work does not stops. Inventory management system also includes the raw material and

keeps track of it so that the raw material can be reordered as early as possible so the production

process does not stops.

Price Optimization: Price optimization is the method which helps the organisation to

determine the price of it products and how they can effectively optimize their price. It is a tools

frequently used by the organisation to analyse the buying pattern of the consumers and determine

the price according to it. As Equilibrium asset management is into the financial consultancy

services they have to optimize the price related to their service what service is to be given or

what price is to be charged to the particular service provided (Mancini, Vaassen and Dameri,

2013).

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

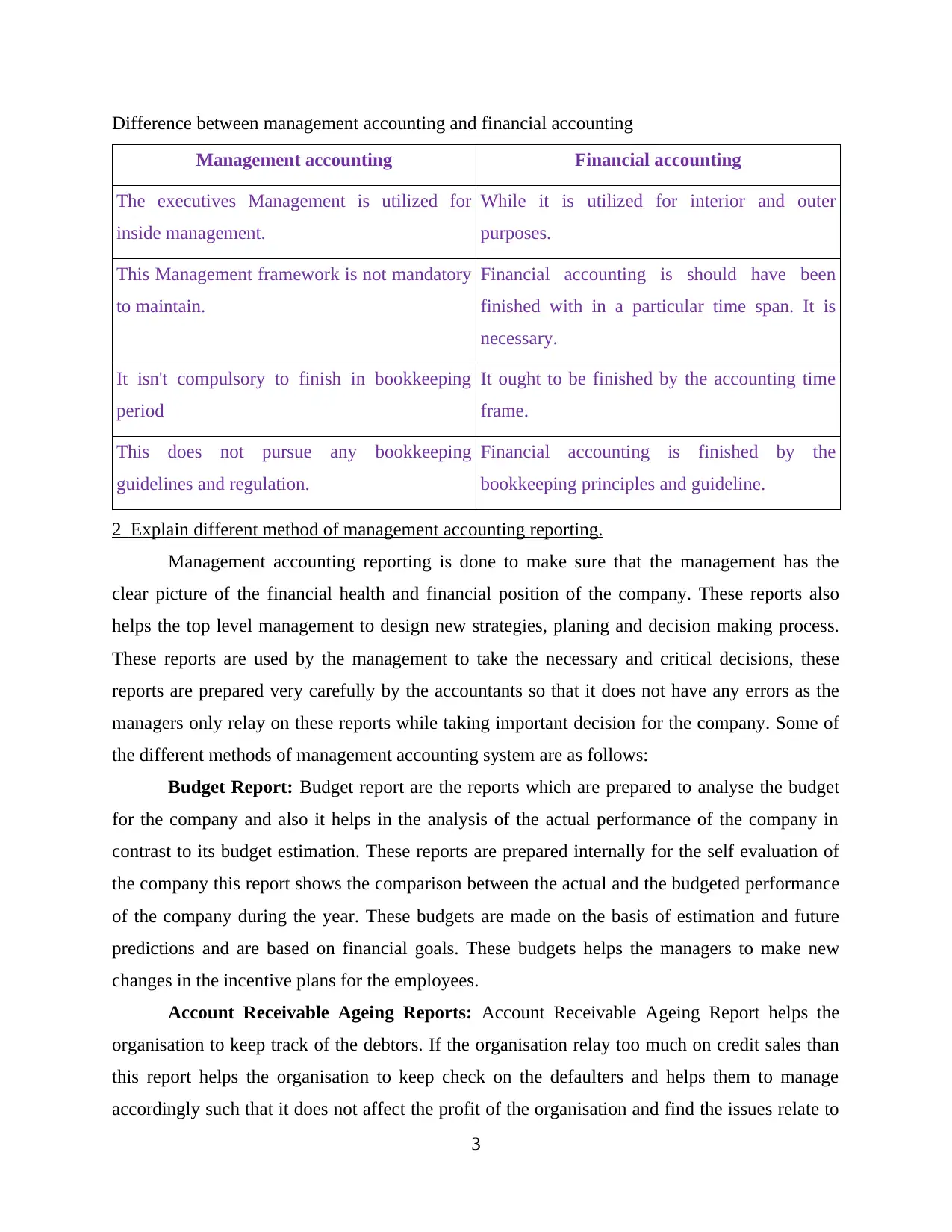

Difference between management accounting and financial accounting

Management accounting Financial accounting

The executives Management is utilized for

inside management.

While it is utilized for interior and outer

purposes.

This Management framework is not mandatory

to maintain.

Financial accounting is should have been

finished with in a particular time span. It is

necessary.

It isn't compulsory to finish in bookkeeping

period

It ought to be finished by the accounting time

frame.

This does not pursue any bookkeeping

guidelines and regulation.

Financial accounting is finished by the

bookkeeping principles and guideline.

2 Explain different method of management accounting reporting.

Management accounting reporting is done to make sure that the management has the

clear picture of the financial health and financial position of the company. These reports also

helps the top level management to design new strategies, planing and decision making process.

These reports are used by the management to take the necessary and critical decisions, these

reports are prepared very carefully by the accountants so that it does not have any errors as the

managers only relay on these reports while taking important decision for the company. Some of

the different methods of management accounting system are as follows:

Budget Report: Budget report are the reports which are prepared to analyse the budget

for the company and also it helps in the analysis of the actual performance of the company in

contrast to its budget estimation. These reports are prepared internally for the self evaluation of

the company this report shows the comparison between the actual and the budgeted performance

of the company during the year. These budgets are made on the basis of estimation and future

predictions and are based on financial goals. These budgets helps the managers to make new

changes in the incentive plans for the employees.

Account Receivable Ageing Reports: Account Receivable Ageing Report helps the

organisation to keep track of the debtors. If the organisation relay too much on credit sales than

this report helps the organisation to keep check on the defaulters and helps them to manage

accordingly such that it does not affect the profit of the organisation and find the issues relate to

3

Management accounting Financial accounting

The executives Management is utilized for

inside management.

While it is utilized for interior and outer

purposes.

This Management framework is not mandatory

to maintain.

Financial accounting is should have been

finished with in a particular time span. It is

necessary.

It isn't compulsory to finish in bookkeeping

period

It ought to be finished by the accounting time

frame.

This does not pursue any bookkeeping

guidelines and regulation.

Financial accounting is finished by the

bookkeeping principles and guideline.

2 Explain different method of management accounting reporting.

Management accounting reporting is done to make sure that the management has the

clear picture of the financial health and financial position of the company. These reports also

helps the top level management to design new strategies, planing and decision making process.

These reports are used by the management to take the necessary and critical decisions, these

reports are prepared very carefully by the accountants so that it does not have any errors as the

managers only relay on these reports while taking important decision for the company. Some of

the different methods of management accounting system are as follows:

Budget Report: Budget report are the reports which are prepared to analyse the budget

for the company and also it helps in the analysis of the actual performance of the company in

contrast to its budget estimation. These reports are prepared internally for the self evaluation of

the company this report shows the comparison between the actual and the budgeted performance

of the company during the year. These budgets are made on the basis of estimation and future

predictions and are based on financial goals. These budgets helps the managers to make new

changes in the incentive plans for the employees.

Account Receivable Ageing Reports: Account Receivable Ageing Report helps the

organisation to keep track of the debtors. If the organisation relay too much on credit sales than

this report helps the organisation to keep check on the defaulters and helps them to manage

accordingly such that it does not affect the profit of the organisation and find the issues relate to

3

the debtors payment. This report is generally made to see that how much money is stuck in the

market in the form of debtors. This report also helps to reframe its credit policy if the number of

defaulters are more in any organisation.

Performance Report: Performance reports are made to check the performance of the

company in order to see that they are performing well or not than their competitors (Ramljak and

Rogošić, 2012). This report helps the management to re think their strategies in order to compete

with their competitors. These reports play an important role in helping the mangers to make the

strategic decisions for the future of the company as this report show the clear picture of the

health and performance of the company. Managers analyse these reports very carefully to find

out the flaws and overcome them in the near future by making the necessary changes in the

system.

Financial Report: Financial reports shows the actual financial position and financial

capabilities of the organisation. These are prepared by the finance department, financial reports

include all the financial statements such as balance sheet, profit and loss statements and cash

flow statement of the company in a report form which helps the management to decide that from

which sources it need to raise its capital and where to invest to grow and expand its business.

The information from these reports helps the management to see that how there profit and losses

have fluctuated over the period of time.

Cost Managerial Accounting Reports: This report computes the cost of the product and

the cost of procurement of the raw material, labour, overhead and all the direct and in direct cost

related to the manufacturing of product. This report helps the managers to identify the cost and

the profit which is charged against that product. This report consist of the cost which is incurred

by the production department to produce the goods and the profit which is to be charged on that

particular product.

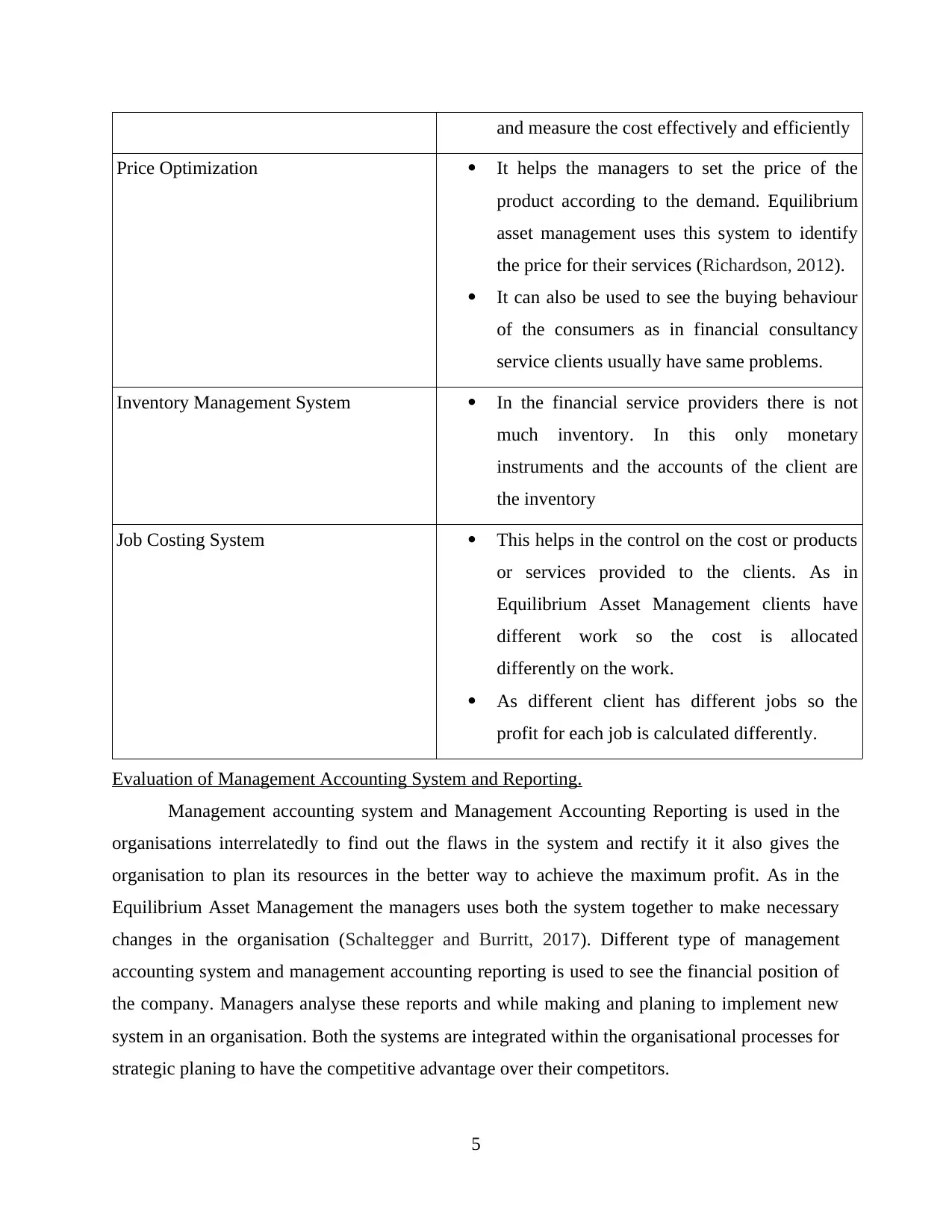

Evaluation of benefits of various management accounting systems.

Management Accounting System Benefits

Cost Accounting System Cost accounting system helps the organisation

to fix its price more efficiently, as this system

provides the details of the cost.

This system helps the management to improve

4

market in the form of debtors. This report also helps to reframe its credit policy if the number of

defaulters are more in any organisation.

Performance Report: Performance reports are made to check the performance of the

company in order to see that they are performing well or not than their competitors (Ramljak and

Rogošić, 2012). This report helps the management to re think their strategies in order to compete

with their competitors. These reports play an important role in helping the mangers to make the

strategic decisions for the future of the company as this report show the clear picture of the

health and performance of the company. Managers analyse these reports very carefully to find

out the flaws and overcome them in the near future by making the necessary changes in the

system.

Financial Report: Financial reports shows the actual financial position and financial

capabilities of the organisation. These are prepared by the finance department, financial reports

include all the financial statements such as balance sheet, profit and loss statements and cash

flow statement of the company in a report form which helps the management to decide that from

which sources it need to raise its capital and where to invest to grow and expand its business.

The information from these reports helps the management to see that how there profit and losses

have fluctuated over the period of time.

Cost Managerial Accounting Reports: This report computes the cost of the product and

the cost of procurement of the raw material, labour, overhead and all the direct and in direct cost

related to the manufacturing of product. This report helps the managers to identify the cost and

the profit which is charged against that product. This report consist of the cost which is incurred

by the production department to produce the goods and the profit which is to be charged on that

particular product.

Evaluation of benefits of various management accounting systems.

Management Accounting System Benefits

Cost Accounting System Cost accounting system helps the organisation

to fix its price more efficiently, as this system

provides the details of the cost.

This system helps the management to improve

4

and measure the cost effectively and efficiently

Price Optimization It helps the managers to set the price of the

product according to the demand. Equilibrium

asset management uses this system to identify

the price for their services (Richardson, 2012).

It can also be used to see the buying behaviour

of the consumers as in financial consultancy

service clients usually have same problems.

Inventory Management System In the financial service providers there is not

much inventory. In this only monetary

instruments and the accounts of the client are

the inventory

Job Costing System This helps in the control on the cost or products

or services provided to the clients. As in

Equilibrium Asset Management clients have

different work so the cost is allocated

differently on the work.

As different client has different jobs so the

profit for each job is calculated differently.

Evaluation of Management Accounting System and Reporting.

Management accounting system and Management Accounting Reporting is used in the

organisations interrelatedly to find out the flaws in the system and rectify it it also gives the

organisation to plan its resources in the better way to achieve the maximum profit. As in the

Equilibrium Asset Management the managers uses both the system together to make necessary

changes in the organisation (Schaltegger and Burritt, 2017). Different type of management

accounting system and management accounting reporting is used to see the financial position of

the company. Managers analyse these reports and while making and planing to implement new

system in an organisation. Both the systems are integrated within the organisational processes for

strategic planing to have the competitive advantage over their competitors.

5

Price Optimization It helps the managers to set the price of the

product according to the demand. Equilibrium

asset management uses this system to identify

the price for their services (Richardson, 2012).

It can also be used to see the buying behaviour

of the consumers as in financial consultancy

service clients usually have same problems.

Inventory Management System In the financial service providers there is not

much inventory. In this only monetary

instruments and the accounts of the client are

the inventory

Job Costing System This helps in the control on the cost or products

or services provided to the clients. As in

Equilibrium Asset Management clients have

different work so the cost is allocated

differently on the work.

As different client has different jobs so the

profit for each job is calculated differently.

Evaluation of Management Accounting System and Reporting.

Management accounting system and Management Accounting Reporting is used in the

organisations interrelatedly to find out the flaws in the system and rectify it it also gives the

organisation to plan its resources in the better way to achieve the maximum profit. As in the

Equilibrium Asset Management the managers uses both the system together to make necessary

changes in the organisation (Schaltegger and Burritt, 2017). Different type of management

accounting system and management accounting reporting is used to see the financial position of

the company. Managers analyse these reports and while making and planing to implement new

system in an organisation. Both the systems are integrated within the organisational processes for

strategic planing to have the competitive advantage over their competitors.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LO 2

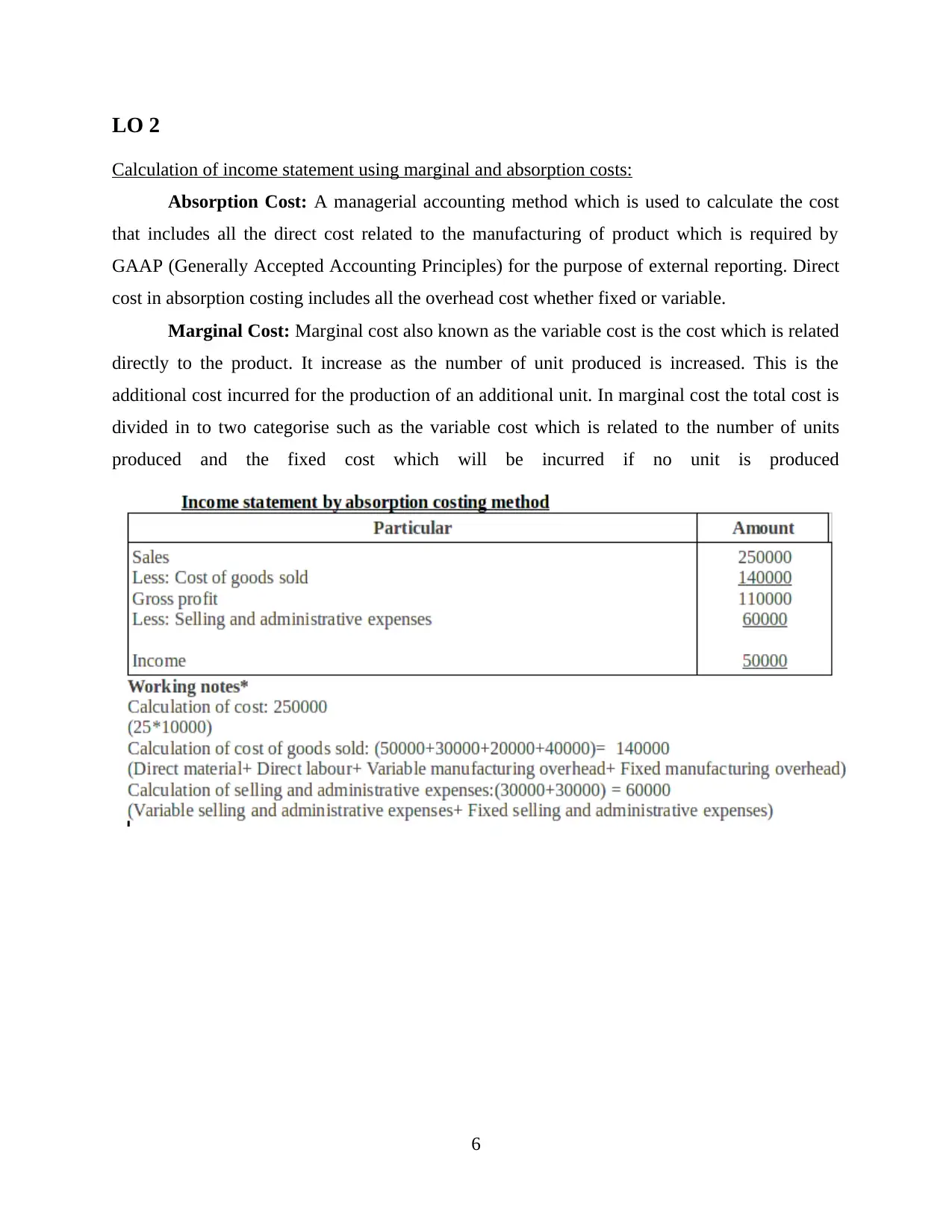

Calculation of income statement using marginal and absorption costs:

Absorption Cost: A managerial accounting method which is used to calculate the cost

that includes all the direct cost related to the manufacturing of product which is required by

GAAP (Generally Accepted Accounting Principles) for the purpose of external reporting. Direct

cost in absorption costing includes all the overhead cost whether fixed or variable.

Marginal Cost: Marginal cost also known as the variable cost is the cost which is related

directly to the product. It increase as the number of unit produced is increased. This is the

additional cost incurred for the production of an additional unit. In marginal cost the total cost is

divided in to two categorise such as the variable cost which is related to the number of units

produced and the fixed cost which will be incurred if no unit is produced

6

Calculation of income statement using marginal and absorption costs:

Absorption Cost: A managerial accounting method which is used to calculate the cost

that includes all the direct cost related to the manufacturing of product which is required by

GAAP (Generally Accepted Accounting Principles) for the purpose of external reporting. Direct

cost in absorption costing includes all the overhead cost whether fixed or variable.

Marginal Cost: Marginal cost also known as the variable cost is the cost which is related

directly to the product. It increase as the number of unit produced is increased. This is the

additional cost incurred for the production of an additional unit. In marginal cost the total cost is

divided in to two categorise such as the variable cost which is related to the number of units

produced and the fixed cost which will be incurred if no unit is produced

6

Interpretation: From the above calculations we can see that the net income from both

marginal and absorption cost are same i.e.,50000 when 10000 goods are produced company can

use any of the two methods of costing.

7

marginal and absorption cost are same i.e.,50000 when 10000 goods are produced company can

use any of the two methods of costing.

7

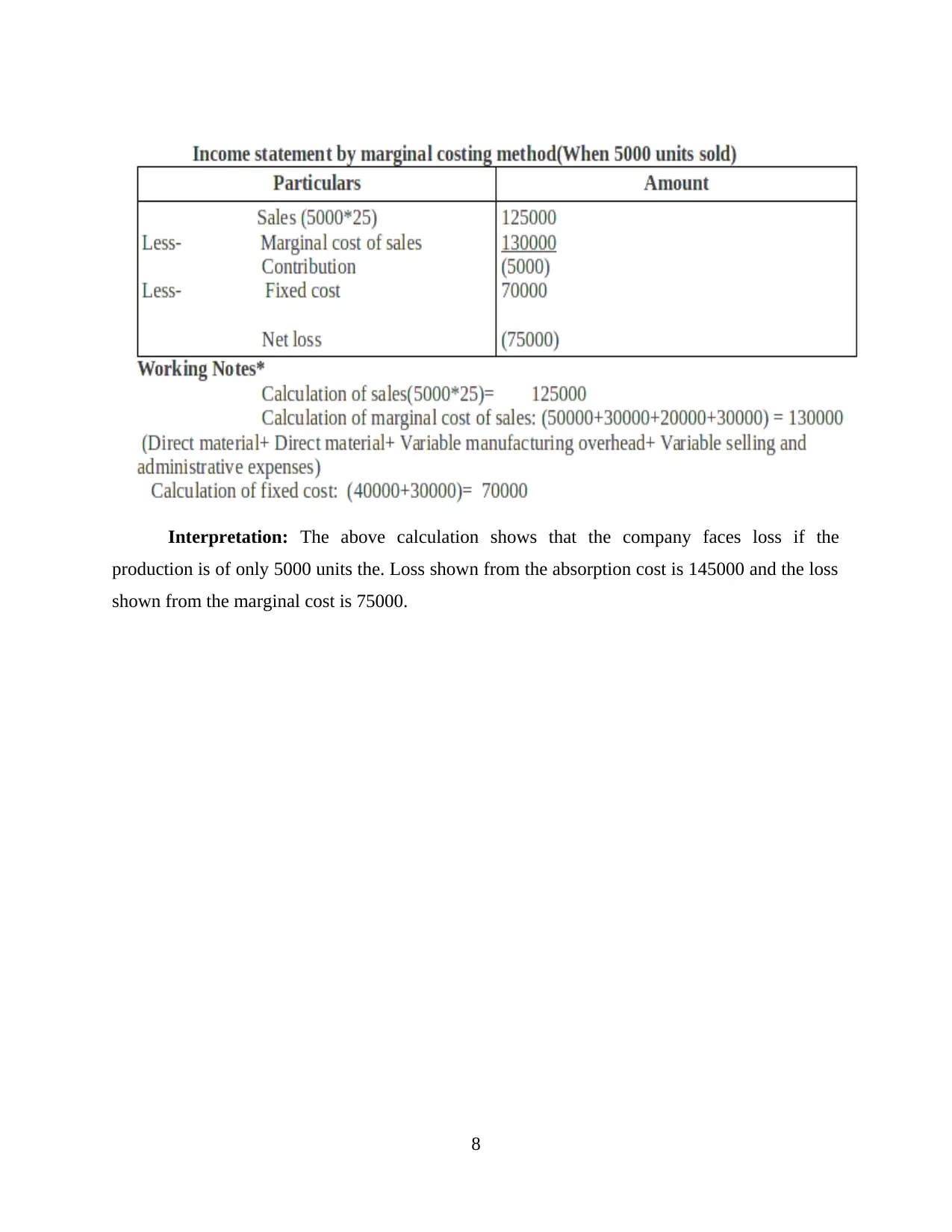

Interpretation: The above calculation shows that the company faces loss if the

production is of only 5000 units the. Loss shown from the absorption cost is 145000 and the loss

shown from the marginal cost is 75000.

8

production is of only 5000 units the. Loss shown from the absorption cost is 145000 and the loss

shown from the marginal cost is 75000.

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

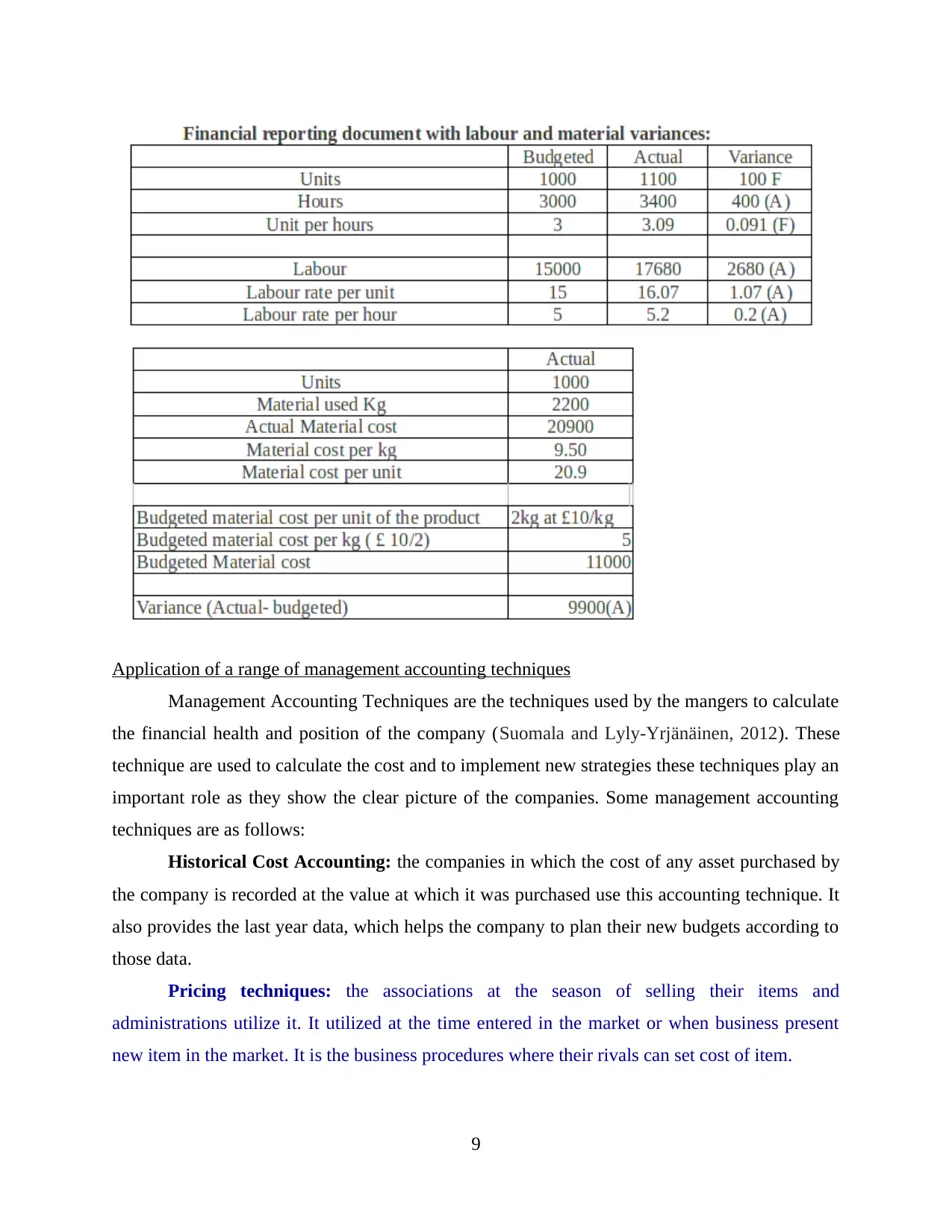

Application of a range of management accounting techniques

Management Accounting Techniques are the techniques used by the mangers to calculate

the financial health and position of the company (Suomala and Lyly-Yrjänäinen, 2012). These

technique are used to calculate the cost and to implement new strategies these techniques play an

important role as they show the clear picture of the companies. Some management accounting

techniques are as follows:

Historical Cost Accounting: the companies in which the cost of any asset purchased by

the company is recorded at the value at which it was purchased use this accounting technique. It

also provides the last year data, which helps the company to plan their new budgets according to

those data.

Pricing techniques: the associations at the season of selling their items and

administrations utilize it. It utilized at the time entered in the market or when business present

new item in the market. It is the business procedures where their rivals can set cost of item.

9

Management Accounting Techniques are the techniques used by the mangers to calculate

the financial health and position of the company (Suomala and Lyly-Yrjänäinen, 2012). These

technique are used to calculate the cost and to implement new strategies these techniques play an

important role as they show the clear picture of the companies. Some management accounting

techniques are as follows:

Historical Cost Accounting: the companies in which the cost of any asset purchased by

the company is recorded at the value at which it was purchased use this accounting technique. It

also provides the last year data, which helps the company to plan their new budgets according to

those data.

Pricing techniques: the associations at the season of selling their items and

administrations utilize it. It utilized at the time entered in the market or when business present

new item in the market. It is the business procedures where their rivals can set cost of item.

9

Actual costing system: It is the cost which is used at the time of productions, where

actual cost of product incurred and included in the total cost of product. Such as labour, martial

cost etc.

Standard Costing: the companies in order to know the problems related to costing of

any product or service and to plan some remedies to take control of the problems use this

technique. It is the establishment of the cost, which are standard under the most efficient working

conditions.

Normal costing system: It is used when cost have derivation, this cost affect the

actual cost of product & services.

Cost system Job costing Process costing Batch costing Contract costing

It is the cost

bookkeeping

framework where

cost estimation

occur for the

examination of

benefit, stock or

authority over

expense.

It is a strategy

which computing

every unit cost of

item which is

allot various

employments to

singular thing or

salary and costs.

Procedure costing

framework is

helpful for that

association which

produce

homogeneous

item. Where this

technique dole

out expense of

every unit of

creation.

It is a sort of

explicit costing

where each clump

contain

comparative

indistinguishable

units yet each

bunch is not quite

the same as other.

Figure the

expense of each

clump called

group costing.

It is a device of

figuring cost,

which is

identified with

the specific

contract with

their customers.

Interpretation data for a range of business activities.

In the above calculation of the income statements from absorption cost and marginal cost

it was found that absorption cost method was not appropriate as in absorption cost fixed

overhead cost is not shown separately whereas in the marginal cost fixed overhead cost is shown

separately this gives the clear picture of the cost which is associated with the production. The

calculations showed that the profit from the marginal cost and the absorption cost is same in the

case where the production was of 10000 units but when the production was reduced to 5000

units, the company faced the loss. The loss from the marginal cost was 145000 and the loss from

10

actual cost of product incurred and included in the total cost of product. Such as labour, martial

cost etc.

Standard Costing: the companies in order to know the problems related to costing of

any product or service and to plan some remedies to take control of the problems use this

technique. It is the establishment of the cost, which are standard under the most efficient working

conditions.

Normal costing system: It is used when cost have derivation, this cost affect the

actual cost of product & services.

Cost system Job costing Process costing Batch costing Contract costing

It is the cost

bookkeeping

framework where

cost estimation

occur for the

examination of

benefit, stock or

authority over

expense.

It is a strategy

which computing

every unit cost of

item which is

allot various

employments to

singular thing or

salary and costs.

Procedure costing

framework is

helpful for that

association which

produce

homogeneous

item. Where this

technique dole

out expense of

every unit of

creation.

It is a sort of

explicit costing

where each clump

contain

comparative

indistinguishable

units yet each

bunch is not quite

the same as other.

Figure the

expense of each

clump called

group costing.

It is a device of

figuring cost,

which is

identified with

the specific

contract with

their customers.

Interpretation data for a range of business activities.

In the above calculation of the income statements from absorption cost and marginal cost

it was found that absorption cost method was not appropriate as in absorption cost fixed

overhead cost is not shown separately whereas in the marginal cost fixed overhead cost is shown

separately this gives the clear picture of the cost which is associated with the production. The

calculations showed that the profit from the marginal cost and the absorption cost is same in the

case where the production was of 10000 units but when the production was reduced to 5000

units, the company faced the loss. The loss from the marginal cost was 145000 and the loss from

10

the marginal cost method was 75000 which states that the marginal cost method gives the clear

picture of the allocation of the cost.

LO3

Advantages and disadvantages of different types of planning tools used for budgetary control

Planning tools are the sources which provides direction to the business to about what

should be done to run it in an efficient manner (Tucker and Lowe, 2014). It provides guidelines

that guides the managers to take actions needed to increase profits and growth. Let's discuss them

in detail:-

Budget refers to creating a detailed plan for estimation company's financial needs. These

are prepared for the purpose of controlling the cash in order to maintain the performance of

business. These are being established for given time period and then later it is used to compare

the actual results with the estimated amount. It helps in identification of deviation occurred and

measures that needs to be taken to take control of it. Managers of Equilibrium asset management

makes sure that set budget fulfil the organisation requirements. As it is financial consultancy

therefore it is vital to maintain finances appropriately. Budgetary control is process of analysing

what concrete actions that should be taken to take achieve set targets. It requires effective

planning and decision-making.

Cash Budget- Under this type of budget flow of cash in the organisation is maintained.

The amount of money coming and going out is important to determine as it ensures the liquidity.

It keeps records of funds along with the sources from it has been generated. It consist of cash

receivable, stock, shares, dividends, loans, taxes and others. Equilibrium asset management

prepares this and able to estimates company's requirement to avoid deficiency of cash. This

method plays significant role in manager's decision making. It allows them to understand the

changes and their affects on the business.

Advantages

The main advantages of preparing this is that it secure finances availability to perform

required operations of business. It helps managers in identification of potential

alternatives available in the and taking choosing the most effective one after their

evaluation (Tucker and Schaltegger, 2016).

11

picture of the allocation of the cost.

LO3

Advantages and disadvantages of different types of planning tools used for budgetary control

Planning tools are the sources which provides direction to the business to about what

should be done to run it in an efficient manner (Tucker and Lowe, 2014). It provides guidelines

that guides the managers to take actions needed to increase profits and growth. Let's discuss them

in detail:-

Budget refers to creating a detailed plan for estimation company's financial needs. These

are prepared for the purpose of controlling the cash in order to maintain the performance of

business. These are being established for given time period and then later it is used to compare

the actual results with the estimated amount. It helps in identification of deviation occurred and

measures that needs to be taken to take control of it. Managers of Equilibrium asset management

makes sure that set budget fulfil the organisation requirements. As it is financial consultancy

therefore it is vital to maintain finances appropriately. Budgetary control is process of analysing

what concrete actions that should be taken to take achieve set targets. It requires effective

planning and decision-making.

Cash Budget- Under this type of budget flow of cash in the organisation is maintained.

The amount of money coming and going out is important to determine as it ensures the liquidity.

It keeps records of funds along with the sources from it has been generated. It consist of cash

receivable, stock, shares, dividends, loans, taxes and others. Equilibrium asset management

prepares this and able to estimates company's requirement to avoid deficiency of cash. This

method plays significant role in manager's decision making. It allows them to understand the

changes and their affects on the business.

Advantages

The main advantages of preparing this is that it secure finances availability to perform

required operations of business. It helps managers in identification of potential

alternatives available in the and taking choosing the most effective one after their

evaluation (Tucker and Schaltegger, 2016).

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Another advantages attached to it is with the planning ahead provides stability to the

organisation it can deal with the uncertainties which can occurs in future. Identifying the

potential threats and opportunities is essential part of business.

Disadvantages

This budget suffers from lack of accuracy. It can not be called reliable as dependency on

estimation of revenues and expenditure can't be trusted. Business is known for being

complex activity there are changes happening every now then. This put a question on it's

authenticity.

Another disadvantage of this tool is that the managers for their personal preferences can

manipulate it. They can make changes in the budget by either increasing the expenses or

decreasing it. This will affect the working of organisation.

Master budget is concerned with forecasting the expenses and revenues of various divisions of

company. Separate budgets are created for each one of them and in the end all are taken into

accounts collectively. Equilibrium asset management prepares this to analyse profits and losses

earned by departments along with estimating their performance.

Advantages

The main advantage of preparing this is that it provides complete information of entire

organisation. It displays the earnings and expenditures of each division that helps in

identification of how much has been spent and which department requires more funds to

be able to provide sufficient results.

Managers can perform planning distinctively and that will help in increasing the overall

profitability of business.

Disadvantage

This budget suffers from lack of flexibility hence there is difficulty in updating it.

Expensive in nature.

Zero based budgeting refers to create budget from zero after the end of certified time period. It

provides reason for expenditure incurring in business. Organisation's management prepares this

budget while estimating expenses and revenues (Van der Meer-Kooistra and Vosselman, 2012).

Advantages

Keeping track of costs and providing justification provides benefits of complete

information.

12

organisation it can deal with the uncertainties which can occurs in future. Identifying the

potential threats and opportunities is essential part of business.

Disadvantages

This budget suffers from lack of accuracy. It can not be called reliable as dependency on

estimation of revenues and expenditure can't be trusted. Business is known for being

complex activity there are changes happening every now then. This put a question on it's

authenticity.

Another disadvantage of this tool is that the managers for their personal preferences can

manipulate it. They can make changes in the budget by either increasing the expenses or

decreasing it. This will affect the working of organisation.

Master budget is concerned with forecasting the expenses and revenues of various divisions of

company. Separate budgets are created for each one of them and in the end all are taken into

accounts collectively. Equilibrium asset management prepares this to analyse profits and losses

earned by departments along with estimating their performance.

Advantages

The main advantage of preparing this is that it provides complete information of entire

organisation. It displays the earnings and expenditures of each division that helps in

identification of how much has been spent and which department requires more funds to

be able to provide sufficient results.

Managers can perform planning distinctively and that will help in increasing the overall

profitability of business.

Disadvantage

This budget suffers from lack of flexibility hence there is difficulty in updating it.

Expensive in nature.

Zero based budgeting refers to create budget from zero after the end of certified time period. It

provides reason for expenditure incurring in business. Organisation's management prepares this

budget while estimating expenses and revenues (Van der Meer-Kooistra and Vosselman, 2012).

Advantages

Keeping track of costs and providing justification provides benefits of complete

information.

12

It allows proper utilization of resources.

Disadvantages

Preparation of this budget is very difficult task. Main disadvantage associated with this is

that it requires certain skills on manager's part. Deep knowledge and understanding is not

something that everyone possess. Therefore not every enterprise has the ability to afford

this.

It is time consuming as finding expenditure and justifying it takes lot of time.

Balanced scorecard: This methodology help the association to make their vision obvious

alongside it increment inner capacities. It is the devices which measure the execution of workers

just as association to recognize their potential and give input. So basilica this methodology use

for the compelling results which help them to improve and make it viable to accomplish business

objectives and goals. Merlin Financial Consultation organization utilize this way to deal with

distinguish their real exhibitions and after that assess the distinction. It will assist the association

with improving their monetary position by utilization of these key arranging devices.

Use of different accounting tools and their application for preparing and forecasting budgets.

Cash budget helps the Equilibrium asset management by estimating the funds availability

and requirement which are the means of survival for any business. On the other hand master

budget analysis estimates the capabilities and capacity of each divisions. Achievement of goals

established by each one of them helps in betterment of the firm. Zero based budget provides

benefits of improving the productivity. These tools are applied to forecast the the needs and

finding the opportunities and threats.

LO 4

How organisation adapting management accounting respond to financial problems

Every organisation has to deal with insufficiency of finance or other problems related to

it. Due to this they suffers from bankruptcy. Management accounting systems are adapted to

solve these problems let discuss them in details:

Debt- This is the main cause of financial problem. Cost accounting system is used by

Equilibrium asset management to cope up with the uncertainties. Company has to effectively

forecast the needs and take measures to deal with them. Small scale firms face this issue very

often due to lower availability of finance.

13

Disadvantages

Preparation of this budget is very difficult task. Main disadvantage associated with this is

that it requires certain skills on manager's part. Deep knowledge and understanding is not

something that everyone possess. Therefore not every enterprise has the ability to afford

this.

It is time consuming as finding expenditure and justifying it takes lot of time.

Balanced scorecard: This methodology help the association to make their vision obvious

alongside it increment inner capacities. It is the devices which measure the execution of workers

just as association to recognize their potential and give input. So basilica this methodology use

for the compelling results which help them to improve and make it viable to accomplish business

objectives and goals. Merlin Financial Consultation organization utilize this way to deal with

distinguish their real exhibitions and after that assess the distinction. It will assist the association

with improving their monetary position by utilization of these key arranging devices.

Use of different accounting tools and their application for preparing and forecasting budgets.

Cash budget helps the Equilibrium asset management by estimating the funds availability

and requirement which are the means of survival for any business. On the other hand master

budget analysis estimates the capabilities and capacity of each divisions. Achievement of goals

established by each one of them helps in betterment of the firm. Zero based budget provides

benefits of improving the productivity. These tools are applied to forecast the the needs and

finding the opportunities and threats.

LO 4

How organisation adapting management accounting respond to financial problems

Every organisation has to deal with insufficiency of finance or other problems related to

it. Due to this they suffers from bankruptcy. Management accounting systems are adapted to

solve these problems let discuss them in details:

Debt- This is the main cause of financial problem. Cost accounting system is used by

Equilibrium asset management to cope up with the uncertainties. Company has to effectively

forecast the needs and take measures to deal with them. Small scale firms face this issue very

often due to lower availability of finance.

13

Problem of cash flow- Investors will invest in company after evaluating it's liquidity. It

is also major problem that various firms go through. It is important to keep record of cash

receivables and ensuring that creditors pay the required amount.

Financial Governance- It is the process of gathering, managing and analysing the information

related to finance. It is the responsibility of equilibrium management company accountant and

manager to keep track of funds. He governs the requirement of cash and make decisions

regarding it's control.

Management accounting approach is concerned with using different techniques in order

to deal with problems associated with decision-making. Equilibrium management involves in

efficient planning that helps the managers in making the right judgement at appropriate time.

There are two main approaches used are as follows:-

KPI: key performance indicator demonstrates the main elements that contributes towards

the company's success. These are the factors on which organisation success depends. Equilibrium

collects suggestions from department heads, analysts to analyse the performance of of employees

and divisions. This helps in ascertaining the progress of projects needed to be completed to

achieve goals. It provides complete picture of financial position of business. Performance of

divisions depend on the working of every individual. Employees has to put efforts in increasing

their productivity. In doing efficiency of firm will ultimately change.

Benchmarking- According to this approach organisation looks outside of their business

to evaluate their performance. Determining the strengths and the reasons of competitive

advantage of other company provides helps one's business in overcoming it's limitations. The

main purpose of obtaining this approach is to improve the performance by identifying the critical

aspects of organization (Ward, 2012). Here the managers take measures to compare their

business with competitor's. Understanding this can solve many of their financial problems.

Comparison between equilibrium asset management company and Accenture

Equilibrium assessment management Accenture

Problem- The main problem that this company

is dealing with is of insufficient funds. Being

small scale company. Due to this it has not

been able to build effective portfolios. This is

the main function of it's business. Therefore it

It is a well known consultancy providing

variety of services to it's clients. The problem

with which this company suffers is from

inefficiency in employees. changing

technology is great challenge for this.

14

is also major problem that various firms go through. It is important to keep record of cash

receivables and ensuring that creditors pay the required amount.

Financial Governance- It is the process of gathering, managing and analysing the information

related to finance. It is the responsibility of equilibrium management company accountant and

manager to keep track of funds. He governs the requirement of cash and make decisions

regarding it's control.

Management accounting approach is concerned with using different techniques in order

to deal with problems associated with decision-making. Equilibrium management involves in

efficient planning that helps the managers in making the right judgement at appropriate time.

There are two main approaches used are as follows:-

KPI: key performance indicator demonstrates the main elements that contributes towards

the company's success. These are the factors on which organisation success depends. Equilibrium

collects suggestions from department heads, analysts to analyse the performance of of employees

and divisions. This helps in ascertaining the progress of projects needed to be completed to

achieve goals. It provides complete picture of financial position of business. Performance of

divisions depend on the working of every individual. Employees has to put efforts in increasing

their productivity. In doing efficiency of firm will ultimately change.

Benchmarking- According to this approach organisation looks outside of their business

to evaluate their performance. Determining the strengths and the reasons of competitive

advantage of other company provides helps one's business in overcoming it's limitations. The

main purpose of obtaining this approach is to improve the performance by identifying the critical

aspects of organization (Ward, 2012). Here the managers take measures to compare their

business with competitor's. Understanding this can solve many of their financial problems.

Comparison between equilibrium asset management company and Accenture

Equilibrium assessment management Accenture

Problem- The main problem that this company

is dealing with is of insufficient funds. Being

small scale company. Due to this it has not

been able to build effective portfolios. This is

the main function of it's business. Therefore it

It is a well known consultancy providing

variety of services to it's clients. The problem

with which this company suffers is from

inefficiency in employees. changing

technology is great challenge for this.

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

has to take control of it's expenses along with

determination of potential sources from where

the funds can be generated.

Requirement of talented workforce is what the

company is aiming for.

Key point indicator is the approach used by

this company. It evaluates the performance of

functions being performed and implementing

actions to for their further improvement.

Benchmarking approach is used by this

organisation. It has achieved success by

adopting this. It manages it's weaker areas

effectively through determining the strategies

adopted by the competitors. It also identifies

it's strengths and compare it with other

successful business.

Management accounting is process of

managing the working of business. It deeply

elaborates about the benefits of various system

that should be adopted by the management

such as Cost accounting, Inventory, Price

optimisation, and Job costing. Equilibrium use

cost accounting system to track expenditures

and keep track of company finances.

Accenture adopted price optimisation system.

It ensures that company charges right prices for

the services that it provides to it's clients.

How management accounting can deal with financial problems and attains sustainable success.

As per the problem mentioned above firms can prepare and plan in advance in order to maintain

financial status. Management accounting helps organisation in achieving sustainable success by

effectively estimating company's resources and through their optimum utilization. Adopting

various systems based on business structure can provide growth and profits by leaps and bounds.

Equilibrium asset maintains data about financial transactions and compare it's performance based

on past and present results (Wickramasinghe and Alawattage, 2012).

Planning tools to solve financial problems:

Solving financial problems should be the main concern for every business organisation. Planning

tools as discussed above is used on various occasions by the management to ensure smooth

functioning of company. Equilibrium asset management builds effective portfolios and conducts

15

determination of potential sources from where

the funds can be generated.

Requirement of talented workforce is what the

company is aiming for.

Key point indicator is the approach used by

this company. It evaluates the performance of

functions being performed and implementing

actions to for their further improvement.

Benchmarking approach is used by this

organisation. It has achieved success by

adopting this. It manages it's weaker areas

effectively through determining the strategies

adopted by the competitors. It also identifies

it's strengths and compare it with other

successful business.

Management accounting is process of

managing the working of business. It deeply

elaborates about the benefits of various system

that should be adopted by the management

such as Cost accounting, Inventory, Price

optimisation, and Job costing. Equilibrium use

cost accounting system to track expenditures

and keep track of company finances.

Accenture adopted price optimisation system.

It ensures that company charges right prices for

the services that it provides to it's clients.

How management accounting can deal with financial problems and attains sustainable success.

As per the problem mentioned above firms can prepare and plan in advance in order to maintain

financial status. Management accounting helps organisation in achieving sustainable success by

effectively estimating company's resources and through their optimum utilization. Adopting

various systems based on business structure can provide growth and profits by leaps and bounds.

Equilibrium asset maintains data about financial transactions and compare it's performance based

on past and present results (Wickramasinghe and Alawattage, 2012).

Planning tools to solve financial problems:

Solving financial problems should be the main concern for every business organisation. Planning

tools as discussed above is used on various occasions by the management to ensure smooth

functioning of company. Equilibrium asset management builds effective portfolios and conducts

15

wealth management through development of cash budgets manages it's requirement. Preparing

such budgets gives important information about the money which has been spent and how

revenues can be generated by controlling it and making investments at appropriate projects.

Managers take decisions based on the reports prepared by them.

CONCLUSION

It has been concluded from above discussed report that using accounting management

helps in building the organisation effectively. These techniques are essential to use to keep

collection of records associated with stocks such as it's location, cost incurred etc. Information

about cash availability and handling it's flow is also main aspect performed by this.. Cost

concerning different jobs such as labour rates, working hours and others are determined. This

helps in identifying the errors and unproductive tasks which are not adding value to the product

instead bringing down the quality and increasing prices unnecessary. Later cost analysis studies

the marginal and absorption costing. It shows the overall profitability of company. Small scale

company uses absorption costing to analyse job costs and and revenue generated from them. At

the end planning tools are explained.

16

such budgets gives important information about the money which has been spent and how

revenues can be generated by controlling it and making investments at appropriate projects.

Managers take decisions based on the reports prepared by them.

CONCLUSION

It has been concluded from above discussed report that using accounting management

helps in building the organisation effectively. These techniques are essential to use to keep

collection of records associated with stocks such as it's location, cost incurred etc. Information

about cash availability and handling it's flow is also main aspect performed by this.. Cost

concerning different jobs such as labour rates, working hours and others are determined. This

helps in identifying the errors and unproductive tasks which are not adding value to the product

instead bringing down the quality and increasing prices unnecessary. Later cost analysis studies

the marginal and absorption costing. It shows the overall profitability of company. Small scale

company uses absorption costing to analyse job costs and and revenue generated from them. At

the end planning tools are explained.

16

REFRENCES

Books and journals

Erserim, A., 2012. The impacts of organizational culture, firm's characteristics and external

environment of firms on management accounting practices: an empirical research on

industrial firms in Turkey. Procedia-Social and Behavioral Sciences. 62. pp.372-376.

Grabner, I. and Moers, F., 2013. Management control as a system or a package? Conceptual and

empirical issues. Accounting, Organizations and Society. 38(6-7). pp.407-419.

Mancini, D., Vaassen, E. H. and Dameri, R. P., 2013. Accounting information systems for

decision making.

Ramljak, B. and Rogošić, A., 2012. Strategic management accounting practices in Croatia.

Journal of international management studies. 7(2). p.93.

Richardson, A. J., 2012. Paradigms, theory and management accounting practice: A comment on

Parker (forthcoming)“Qualitative management accounting research: Assessing

deliverables and relevance”. Critical Perspectives on Accounting. 23(1), pp.83-88.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Suomala, P. and Lyly-Yrjänäinen, J., 2012. Management accounting research in practice:

Lessons learned from an interventionist approach. Routledge.

Tucker, B. P. and Lowe, A. D., 2014. Practitioners are from Mars; academics are from Venus?:

An investigation of the research-practice gap in management accounting. Accounting,

Auditing & Accountability Journal. 27(3). pp.394-425.

Tucker, B. P. and Schaltegger, S., 2016. Comparing the research-practice gap in management

accounting: A view from professional accounting bodies in Australia and Germany.

Accounting, Auditing & Accountability Journal. 29(3). pp.362-400.

Van der Meer-Kooistra, J. and Vosselman, E., 2012. Research paradigms, theoretical pluralism

and the practical relevance of management accounting knowledge. Qualitative Research

in Accounting & Management. 9(3). pp.245-264.

Ward, K., 2012.Strategic management accounting. Routledge.

Wickramasinghe, D. and Alawattage, C., 2012. Management accounting change: approaches

and perspectives. Routledge.

17

Books and journals

Erserim, A., 2012. The impacts of organizational culture, firm's characteristics and external

environment of firms on management accounting practices: an empirical research on

industrial firms in Turkey. Procedia-Social and Behavioral Sciences. 62. pp.372-376.

Grabner, I. and Moers, F., 2013. Management control as a system or a package? Conceptual and

empirical issues. Accounting, Organizations and Society. 38(6-7). pp.407-419.

Mancini, D., Vaassen, E. H. and Dameri, R. P., 2013. Accounting information systems for

decision making.

Ramljak, B. and Rogošić, A., 2012. Strategic management accounting practices in Croatia.

Journal of international management studies. 7(2). p.93.

Richardson, A. J., 2012. Paradigms, theory and management accounting practice: A comment on

Parker (forthcoming)“Qualitative management accounting research: Assessing

deliverables and relevance”. Critical Perspectives on Accounting. 23(1), pp.83-88.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Suomala, P. and Lyly-Yrjänäinen, J., 2012. Management accounting research in practice:

Lessons learned from an interventionist approach. Routledge.

Tucker, B. P. and Lowe, A. D., 2014. Practitioners are from Mars; academics are from Venus?:

An investigation of the research-practice gap in management accounting. Accounting,

Auditing & Accountability Journal. 27(3). pp.394-425.

Tucker, B. P. and Schaltegger, S., 2016. Comparing the research-practice gap in management

accounting: A view from professional accounting bodies in Australia and Germany.

Accounting, Auditing & Accountability Journal. 29(3). pp.362-400.

Van der Meer-Kooistra, J. and Vosselman, E., 2012. Research paradigms, theoretical pluralism

and the practical relevance of management accounting knowledge. Qualitative Research

in Accounting & Management. 9(3). pp.245-264.

Ward, K., 2012.Strategic management accounting. Routledge.

Wickramasinghe, D. and Alawattage, C., 2012. Management accounting change: approaches

and perspectives. Routledge.

17

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.