Transfer Pricing and Approaches for Determining Transfer Price

VerifiedAdded on 2023/03/20

|17

|4029

|35

AI Summary

This report discusses the concept of transfer pricing and various approaches that can be used to determine the transfer price. It also provides recommendations for optimizing performance and efficiency through the implementation of a performance measurement approach.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management accounting

Group 4|ACC202

Group 4|ACC202

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Executive Summary

The present report is related to the determination of the transfer pricing. There are several issues

involves in the transfer price as each division wants to maximize its divisional profit. This study

shows several approaches to transfer price such as negotiated approach, and dual pricing

approach. Further, it also contains the difference in the profit if the one division sells its goods to

other division on the basis of cost or on the basis of the contribution margin approach. The main

objective of the company is to optimize the performance and efficiency, which can be obtained

by the implementation of the performance measurement approach.

Group 4|ACC202

The present report is related to the determination of the transfer pricing. There are several issues

involves in the transfer price as each division wants to maximize its divisional profit. This study

shows several approaches to transfer price such as negotiated approach, and dual pricing

approach. Further, it also contains the difference in the profit if the one division sells its goods to

other division on the basis of cost or on the basis of the contribution margin approach. The main

objective of the company is to optimize the performance and efficiency, which can be obtained

by the implementation of the performance measurement approach.

Group 4|ACC202

Table of Contents

Introduction......................................................................................................................................4

Assessment 3...................................................................................................................................4

Task 1...........................................................................................................................................4

Task 2.........................................................................................................................................10

Task 3.........................................................................................................................................11

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Group 4|ACC202

Introduction......................................................................................................................................4

Assessment 3...................................................................................................................................4

Task 1...........................................................................................................................................4

Task 2.........................................................................................................................................10

Task 3.........................................................................................................................................11

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Group 4|ACC202

INTRODUCTION

A company may carry out its operations by decentralization method, in which it has several

divisions. In this, one division may transfer its goods or services to other division. Further, the

divisional manager of the division is responsible for the performance of their own department. In

the given study, the company has three divisions; in which one division transfer the goods to

other division. This report contains the determination of the transfer price and several approaches

which can be applied by the company for measuring the transfer price. Further, in this study,

recommendation related to the transfer pricing and performance measurement approach, which

assist in optimizing the performance and efficiency of the company also stated.

ASSESSMENT 3

Task 1

Statement by Cleveland is correct or not

Transfer price is the price at which department of a company transfers its goods or services to

another department. At the time when the divisions are required to make the transactions with

each other, then for determination of the cost, the transfer price is required. Generally, it should

not differ from the market price (Davies & et al. 2018). If there is a significant difference, then it

will not be favourable for one of division, and they may start to transact with the market to get a

better price.

In the given case, the company has three divisions. Among these, cushion division transfers its

product to the furniture division. At present, the division made the transfer at variable cost. in

Group 4|ACC202

A company may carry out its operations by decentralization method, in which it has several

divisions. In this, one division may transfer its goods or services to other division. Further, the

divisional manager of the division is responsible for the performance of their own department. In

the given study, the company has three divisions; in which one division transfer the goods to

other division. This report contains the determination of the transfer price and several approaches

which can be applied by the company for measuring the transfer price. Further, in this study,

recommendation related to the transfer pricing and performance measurement approach, which

assist in optimizing the performance and efficiency of the company also stated.

ASSESSMENT 3

Task 1

Statement by Cleveland is correct or not

Transfer price is the price at which department of a company transfers its goods or services to

another department. At the time when the divisions are required to make the transactions with

each other, then for determination of the cost, the transfer price is required. Generally, it should

not differ from the market price (Davies & et al. 2018). If there is a significant difference, then it

will not be favourable for one of division, and they may start to transact with the market to get a

better price.

In the given case, the company has three divisions. Among these, cushion division transfers its

product to the furniture division. At present, the division made the transfer at variable cost. in

Group 4|ACC202

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

other words, it can be said that cushion division is not generating any profit while making the

transfer to the furniture division. With this aspect, Robert Cleveland, the manager of cushion

division was not happy with the performance of its division. He stated that division is much more

profitable than what has been presented in the given management reports. Therefore, he wants to

sell these goods to furniture division at a cost, which consist of certain profit. Since the division

can sell the goods to outside market at a regular mark up; therefore he believes that performance

of the division should be based on contribution, which can be realized if division makes to the

external market. By considering the above aspect, the statement made by the manager of the

cushion division is correct. Since the division has an outside market; therefore it can sell the

same goods to outside market and earn the profit. Therefore, for measuring the performance,

cushion division should transfer the furniture division at marker price instead of at cost.

Approaches that could be used for the determination of the transfer price

Transfer price is the method implemented to sell goods or services among the divisions of the

same company. The buying behaviour of the division and income tax as a whole company will

be affected by the transfer price of the company (Cristea, and Nguyen, 2016). There are some

problem exist in the determination of transfer price, which is as follows –

If the manager of division has granted a choice to selection related with either to sell

other division or to sell outside customers, then a heavy low price assists the manager to

sell to external customers, and he/she will deny taking the order from internal division.

As the division will generate more profit from selling to outside market (Klassen,

Lisowsky, and Mescall, 2017).

Group 4|ACC202

transfer to the furniture division. With this aspect, Robert Cleveland, the manager of cushion

division was not happy with the performance of its division. He stated that division is much more

profitable than what has been presented in the given management reports. Therefore, he wants to

sell these goods to furniture division at a cost, which consist of certain profit. Since the division

can sell the goods to outside market at a regular mark up; therefore he believes that performance

of the division should be based on contribution, which can be realized if division makes to the

external market. By considering the above aspect, the statement made by the manager of the

cushion division is correct. Since the division has an outside market; therefore it can sell the

same goods to outside market and earn the profit. Therefore, for measuring the performance,

cushion division should transfer the furniture division at marker price instead of at cost.

Approaches that could be used for the determination of the transfer price

Transfer price is the method implemented to sell goods or services among the divisions of the

same company. The buying behaviour of the division and income tax as a whole company will

be affected by the transfer price of the company (Cristea, and Nguyen, 2016). There are some

problem exist in the determination of transfer price, which is as follows –

If the manager of division has granted a choice to selection related with either to sell

other division or to sell outside customers, then a heavy low price assists the manager to

sell to external customers, and he/she will deny taking the order from internal division.

As the division will generate more profit from selling to outside market (Klassen,

Lisowsky, and Mescall, 2017).

Group 4|ACC202

On the other hand, if the division has the choice to buy the product either from their other

division or from outside, then if there is a high transfer price, then division will definitely

prefer to buy the product from outside market, instead to purchase from their other

department of the company (Ondrušová, 2016).

If the manager of division considers the internal transfer as the same manner as he can

generate the profit from selling the product to outsider market, then it performance

measurement will crucial for the company (Leitner, 2013).

In addition, income tax is paid by the company on the overall profit of the company. If the

division of the company is located in different areas, which has different tax jurisdiction,

therefore transfer price can be used by the company to the reported profit level of each division

(Blouin, Robinson, and Seidman, 2018).

A company should determine the transfer price that results in a higher profit of the whole

company. Generally, in the determination of transfer price, the main objective of the

management is to motivate goal comparison among the manager of the division, that is involved

in the transfer (Lyal, 2015).

Normally the transfer price is determined by the addition of the two elements, which are

described below –

Extra cost incurred by the division due to the transfer.

Opportunity cost per unit to the company due to the transfer.

On the basis of the above two elements, the transfer cost is ascertained. With the aspect of

element one, the cost incurred by the division that manufactures the goods or services to be

transferred (Liu, Zhang, and Tang, 2015). The direct variable cost incurred by the division for

Group 4|ACC202

division or from outside, then if there is a high transfer price, then division will definitely

prefer to buy the product from outside market, instead to purchase from their other

department of the company (Ondrušová, 2016).

If the manager of division considers the internal transfer as the same manner as he can

generate the profit from selling the product to outsider market, then it performance

measurement will crucial for the company (Leitner, 2013).

In addition, income tax is paid by the company on the overall profit of the company. If the

division of the company is located in different areas, which has different tax jurisdiction,

therefore transfer price can be used by the company to the reported profit level of each division

(Blouin, Robinson, and Seidman, 2018).

A company should determine the transfer price that results in a higher profit of the whole

company. Generally, in the determination of transfer price, the main objective of the

management is to motivate goal comparison among the manager of the division, that is involved

in the transfer (Lyal, 2015).

Normally the transfer price is determined by the addition of the two elements, which are

described below –

Extra cost incurred by the division due to the transfer.

Opportunity cost per unit to the company due to the transfer.

On the basis of the above two elements, the transfer cost is ascertained. With the aspect of

element one, the cost incurred by the division that manufactures the goods or services to be

transferred (Liu, Zhang, and Tang, 2015). The direct variable cost incurred by the division for

Group 4|ACC202

the production of goods or services is included in the extra cost of incurred only because of the

transfer. Moreover, with the aspect of element two, the general transfer pricing rule is applicable.

It is the opportunity cost incurred by the company as a whole because of transfer (McNair-

Connolly, Polutnik, and Silvi, 2013). The opportunity cost is an extra benefit foregone because

of the adoption of the specific action. There are several approaches, which can be applied by the

company for the ascertainment of the transfer price. Market price method, cost-based method,

dual prices, negotiated prices are some example of the approaches which assist in the

determination of transfer price (Brandt, 2016).

Ascertainment of transfer price by the negotiated method

Negotiated price method is generally referred as a middle solution among the market price

method and cost-based price method. In this method, managers of the division act in a manner as

they are the manager of the individual company (McWatters, and Zimmerman, 2016). Further,

the strategies related to the negotiation are comprised of the planning and trading with the

external market. If both divisions is free to enter into the deal with each other or in the outside

market, then the negotiated transfer price approximately linked with the external market price.

Moreover, if the division is not capable of selling its goods or services to the outside market,

then the negotiated price will be less than the market price and the divisions will share the total

profit (Gao, and Zhao, 2015).

Further, the negotiated method of transfer price will be successful only if some conditions are

satisfied, which are described as below –

The division has full knowledge of entire market information, by which they can

determine the negotiated transfer price closely linked with the external market price.

Group 4|ACC202

transfer. Moreover, with the aspect of element two, the general transfer pricing rule is applicable.

It is the opportunity cost incurred by the company as a whole because of transfer (McNair-

Connolly, Polutnik, and Silvi, 2013). The opportunity cost is an extra benefit foregone because

of the adoption of the specific action. There are several approaches, which can be applied by the

company for the ascertainment of the transfer price. Market price method, cost-based method,

dual prices, negotiated prices are some example of the approaches which assist in the

determination of transfer price (Brandt, 2016).

Ascertainment of transfer price by the negotiated method

Negotiated price method is generally referred as a middle solution among the market price

method and cost-based price method. In this method, managers of the division act in a manner as

they are the manager of the individual company (McWatters, and Zimmerman, 2016). Further,

the strategies related to the negotiation are comprised of the planning and trading with the

external market. If both divisions is free to enter into the deal with each other or in the outside

market, then the negotiated transfer price approximately linked with the external market price.

Moreover, if the division is not capable of selling its goods or services to the outside market,

then the negotiated price will be less than the market price and the divisions will share the total

profit (Gao, and Zhao, 2015).

Further, the negotiated method of transfer price will be successful only if some conditions are

satisfied, which are described as below –

The division has full knowledge of entire market information, by which they can

determine the negotiated transfer price closely linked with the external market price.

Group 4|ACC202

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There should be freedom to division to buy or sell products or services to the external

market; it assists in providing the essential discipline to the bargaining process

(Clempner, and Poznyak, 2018).

For the implementation of this technique, there must be assistance and the involvement of

the top management of the company. The division must settle the disputes by themselves;

otherwise, the advantages of the decentralization cannot be avail by the company. The

top management of the company should be available for addressing the disputes, but it

does not lead to undermining the process of negotiation (Tinkelman, 2015).

Along with the above aspect, this process must avoid the mistrusts, undesirable bargaining

interests among the managers of division. Moreover, it should also achieve the main objective of

goal realization and reliable assessment of performance. Only if the selling or purchasing

division gets agree with the mutual transfer price, then only overall company can obtain the

benefits (Löffler, 2018).

Apart from the above aspects, there are some disadvantages of implementation of negotiated

price method, which are as follows –

For this process, the management of the company has to incur the significant time,

resources, and efforts.

The decision may have some private information; however, while making the negotiated

process, there are chances that the other division may aware about the confidential

information of other departments (Watts, Yapa, and Dellaportas, 2014).

Managers have to incur the time for a negotiated process.

Group 4|ACC202

market; it assists in providing the essential discipline to the bargaining process

(Clempner, and Poznyak, 2018).

For the implementation of this technique, there must be assistance and the involvement of

the top management of the company. The division must settle the disputes by themselves;

otherwise, the advantages of the decentralization cannot be avail by the company. The

top management of the company should be available for addressing the disputes, but it

does not lead to undermining the process of negotiation (Tinkelman, 2015).

Along with the above aspect, this process must avoid the mistrusts, undesirable bargaining

interests among the managers of division. Moreover, it should also achieve the main objective of

goal realization and reliable assessment of performance. Only if the selling or purchasing

division gets agree with the mutual transfer price, then only overall company can obtain the

benefits (Löffler, 2018).

Apart from the above aspects, there are some disadvantages of implementation of negotiated

price method, which are as follows –

For this process, the management of the company has to incur the significant time,

resources, and efforts.

The decision may have some private information; however, while making the negotiated

process, there are chances that the other division may aware about the confidential

information of other departments (Watts, Yapa, and Dellaportas, 2014).

Managers have to incur the time for a negotiated process.

Group 4|ACC202

If the negotiated prices are more than the opportunity cost of supplying the goods or

services, then it may assist in sub-optimum level of output.

Ascertainment of transfer price by dual prices

In the dual price method, selling division of the goods or services transfer at the market price or

negotiated market price or cost including some profit margin. However, for the buying division,

the transfer price will be cost based amount, which generally consists of the variable cost of the

transferor department. The particular centralized department, account for the differences in the

transfer price of the two departments. The cost data related to transfer prices are preserved by

this system, which is used by the subsequent buyer (Fernandes, Pinho, and Gouveia, 2015). This

would motivate the internal transfer by reflecting the profit on such transfer for selling the

division. It is a good technique for determination of the transfer price, because of the following

reasons –

It motivates and provides incentives to the selling departments as it makes the transfer at

the external market price or by addition of some margin in the cost. This division makes a

profit. The market price of the product is considered a suitable base for the selling

departments (Johnson, Johnson, and Pfeiffer, 2016).

On the other hand, buying division buys the products or services from selling division at

the minimum cost. Therefore they will also be encouraged buying the products from

internal departments.

On the basis of above facts, it has been drawn that by the implementation of the dual pricing

system, the selling division as well as the buying division get motivated to make the decision

which are consistent with the overall objective of decentralization such as reliable performance

Group 4|ACC202

services, then it may assist in sub-optimum level of output.

Ascertainment of transfer price by dual prices

In the dual price method, selling division of the goods or services transfer at the market price or

negotiated market price or cost including some profit margin. However, for the buying division,

the transfer price will be cost based amount, which generally consists of the variable cost of the

transferor department. The particular centralized department, account for the differences in the

transfer price of the two departments. The cost data related to transfer prices are preserved by

this system, which is used by the subsequent buyer (Fernandes, Pinho, and Gouveia, 2015). This

would motivate the internal transfer by reflecting the profit on such transfer for selling the

division. It is a good technique for determination of the transfer price, because of the following

reasons –

It motivates and provides incentives to the selling departments as it makes the transfer at

the external market price or by addition of some margin in the cost. This division makes a

profit. The market price of the product is considered a suitable base for the selling

departments (Johnson, Johnson, and Pfeiffer, 2016).

On the other hand, buying division buys the products or services from selling division at

the minimum cost. Therefore they will also be encouraged buying the products from

internal departments.

On the basis of above facts, it has been drawn that by the implementation of the dual pricing

system, the selling division as well as the buying division get motivated to make the decision

which are consistent with the overall objective of decentralization such as reliable performance

Group 4|ACC202

measurement, sufficient encouragement to divisional manager, autonomy, and many others

(Epstein, and Malina ,(eds), 2016).

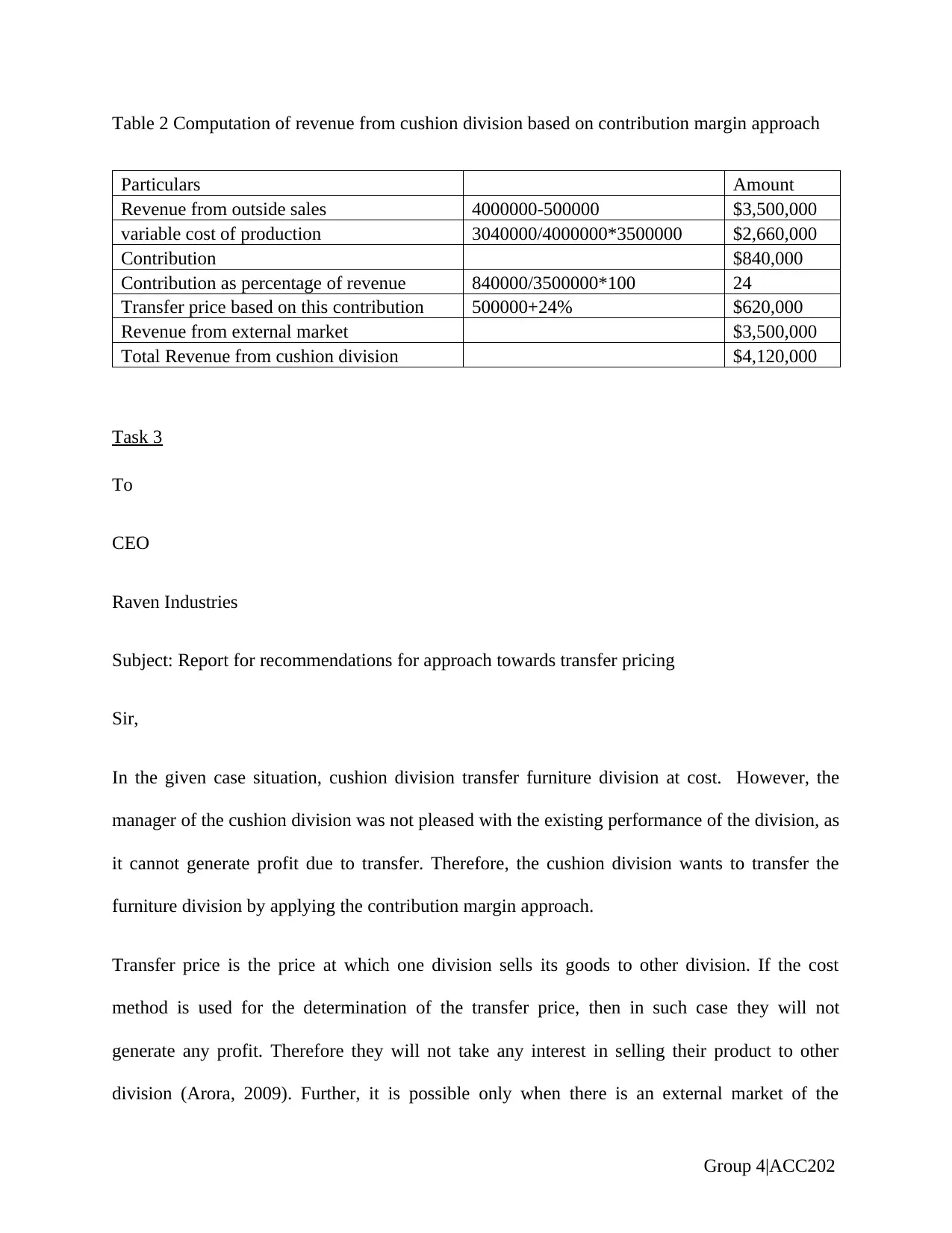

Task 2

In the present case of Raven Industries, the company has three divisions, namely carpet division,

furniture division, and cushion division. The Cushion division transfers its product to the

furniture division. At present the cushion division transfer product at $ 500000 to furniture

division. This transfer price reflects at variable cost. The manager of the cushion division was

not happy with the operating profit of the division. Therefore, the manager wants to earn the

profit from transfer equivalent to the profit derived by selling the product at the external market.

Computation of Revised profit statement

Table 1 Statement of profit or loss

Particulars Carpet Division Furniture Division Cushion Division

Total Revenue $3,000,000 $3,000,000 $4,120,000

Less - variable Cost

Direct Material $500,000 $1,000,000 $1,030,000

Direct Labor $500,000 $200,000 $1,030,000

Variable overhead $750,000 $50,000 $1,030,000

Selling expenses $480,000 $480,000 $412,000

Administrative Expenses $85,000 $140,000 41200

Contribution $685,000 $1,130,000 $576,800

Less -Fixed Cost $250,000 $50,000

Selling expenses 120000 120000 100000

Administrative Expenses $215,000 $360,000 $360,000

Net Profit $100,000 $600,000 $116,800

Working Notes

1. Calculation of contribution

Group 4|ACC202

(Epstein, and Malina ,(eds), 2016).

Task 2

In the present case of Raven Industries, the company has three divisions, namely carpet division,

furniture division, and cushion division. The Cushion division transfers its product to the

furniture division. At present the cushion division transfer product at $ 500000 to furniture

division. This transfer price reflects at variable cost. The manager of the cushion division was

not happy with the operating profit of the division. Therefore, the manager wants to earn the

profit from transfer equivalent to the profit derived by selling the product at the external market.

Computation of Revised profit statement

Table 1 Statement of profit or loss

Particulars Carpet Division Furniture Division Cushion Division

Total Revenue $3,000,000 $3,000,000 $4,120,000

Less - variable Cost

Direct Material $500,000 $1,000,000 $1,030,000

Direct Labor $500,000 $200,000 $1,030,000

Variable overhead $750,000 $50,000 $1,030,000

Selling expenses $480,000 $480,000 $412,000

Administrative Expenses $85,000 $140,000 41200

Contribution $685,000 $1,130,000 $576,800

Less -Fixed Cost $250,000 $50,000

Selling expenses 120000 120000 100000

Administrative Expenses $215,000 $360,000 $360,000

Net Profit $100,000 $600,000 $116,800

Working Notes

1. Calculation of contribution

Group 4|ACC202

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table 2 Computation of revenue from cushion division based on contribution margin approach

Particulars Amount

Revenue from outside sales 4000000-500000 $3,500,000

variable cost of production 3040000/4000000*3500000 $2,660,000

Contribution $840,000

Contribution as percentage of revenue 840000/3500000*100 24

Transfer price based on this contribution 500000+24% $620,000

Revenue from external market $3,500,000

Total Revenue from cushion division $4,120,000

Task 3

To

CEO

Raven Industries

Subject: Report for recommendations for approach towards transfer pricing

Sir,

In the given case situation, cushion division transfer furniture division at cost. However, the

manager of the cushion division was not pleased with the existing performance of the division, as

it cannot generate profit due to transfer. Therefore, the cushion division wants to transfer the

furniture division by applying the contribution margin approach.

Transfer price is the price at which one division sells its goods to other division. If the cost

method is used for the determination of the transfer price, then in such case they will not

generate any profit. Therefore they will not take any interest in selling their product to other

division (Arora, 2009). Further, it is possible only when there is an external market of the

Group 4|ACC202

Particulars Amount

Revenue from outside sales 4000000-500000 $3,500,000

variable cost of production 3040000/4000000*3500000 $2,660,000

Contribution $840,000

Contribution as percentage of revenue 840000/3500000*100 24

Transfer price based on this contribution 500000+24% $620,000

Revenue from external market $3,500,000

Total Revenue from cushion division $4,120,000

Task 3

To

CEO

Raven Industries

Subject: Report for recommendations for approach towards transfer pricing

Sir,

In the given case situation, cushion division transfer furniture division at cost. However, the

manager of the cushion division was not pleased with the existing performance of the division, as

it cannot generate profit due to transfer. Therefore, the cushion division wants to transfer the

furniture division by applying the contribution margin approach.

Transfer price is the price at which one division sells its goods to other division. If the cost

method is used for the determination of the transfer price, then in such case they will not

generate any profit. Therefore they will not take any interest in selling their product to other

division (Arora, 2009). Further, it is possible only when there is an external market of the

Group 4|ACC202

product, if it is not, then in such case, they have to transfer other division at a cost which is

incurred for the production of one unit. Along with this, if there is an external market, but it is

limited, then transfer price should be determined differently with the unit that can be sold to the

external market, and that cannot be sold to external market (Eldenburg, 2017). Apart from this,

for performance measurement, the contribution based margin approach is a good method. In this,

it has been seen that cushion division has the external market in which it can sell their product.

On the basis of the above analysis, it has been recommended that the company should use the

performance measurement approach, by which it can optimize the performance and the

efficiency. As in this approach, the divisional manager would encourage to sell the product to

other division, as by which it can enhance their profitability (Epstein, and Malina, (eds), 2015).

Moreover, the performance measurement is the effective technique for the management which

assists in the review and estimate whether the divisional performance is effective or what are the

actions that are required to implement to improve its performance (Eldenburg, Krishan, and

Krishan, 2017). Further, the performance of the division would influence the other division to

motivate towards improvising its activities. It can be said that through this management can

identify any problem that exists in the department, clarify the expectations and make plans for

the future. By this, identification of the underdeveloped division is also possible and implements

the necessary action for improving their performance (Ette, 2015). Overall it can be said that the

overall performance of the company, productivity of a company, can be improved by applying

the performance management system in the organizations. In addition, it prescribes the clear

accountabilities of each divisional manager, by which they take all actions carefully and make

the efforts for enhancing the performance. On the other hand, sometime this approach may lead

to difficulty, as if the divisional manager only wants to improve their profitability of department

Group 4|ACC202

incurred for the production of one unit. Along with this, if there is an external market, but it is

limited, then transfer price should be determined differently with the unit that can be sold to the

external market, and that cannot be sold to external market (Eldenburg, 2017). Apart from this,

for performance measurement, the contribution based margin approach is a good method. In this,

it has been seen that cushion division has the external market in which it can sell their product.

On the basis of the above analysis, it has been recommended that the company should use the

performance measurement approach, by which it can optimize the performance and the

efficiency. As in this approach, the divisional manager would encourage to sell the product to

other division, as by which it can enhance their profitability (Epstein, and Malina, (eds), 2015).

Moreover, the performance measurement is the effective technique for the management which

assists in the review and estimate whether the divisional performance is effective or what are the

actions that are required to implement to improve its performance (Eldenburg, Krishan, and

Krishan, 2017). Further, the performance of the division would influence the other division to

motivate towards improvising its activities. It can be said that through this management can

identify any problem that exists in the department, clarify the expectations and make plans for

the future. By this, identification of the underdeveloped division is also possible and implements

the necessary action for improving their performance (Ette, 2015). Overall it can be said that the

overall performance of the company, productivity of a company, can be improved by applying

the performance management system in the organizations. In addition, it prescribes the clear

accountabilities of each divisional manager, by which they take all actions carefully and make

the efforts for enhancing the performance. On the other hand, sometime this approach may lead

to difficulty, as if the divisional manager only wants to improve their profitability of department

Group 4|ACC202

and do not consider the company as a whole, then there is a possibility that conflict may arise

(Jack, and Mundy, 2013). Further, if plans and strategies of divisional performance are not

consistent with the overall strategies of the company, then the issue may arise.

By considering all the above analysis, it has been recommended that the company should apply

performance measurement approach which leads to optimizing the performance and efficiency of

the company.

From

Xyz

Date: May 16, 2019

CONCLUSION

By considering the above analysis, it has been drawn that, the main objective of the company to

encourage the divisional manner in such a way by which they are guided towards for

improvising the performance of the overall company. In this report, the divisional manager

(Cleveland), was correct, as because if he transfers the product of its department to the outside

market, then definitely the division will generate profit. Further, the division through the

negotiated pricing approach as well as dual pricing approach determines the transfer price. In

addition, if the contribution margin approach is applied on sale to furniture division by the

cushion division, then it has been observed that overall profit will increase. Moreover, through

the performance measurement approach, performance and efficiency of the company can be

maximized.

Group 4|ACC202

(Jack, and Mundy, 2013). Further, if plans and strategies of divisional performance are not

consistent with the overall strategies of the company, then the issue may arise.

By considering all the above analysis, it has been recommended that the company should apply

performance measurement approach which leads to optimizing the performance and efficiency of

the company.

From

Xyz

Date: May 16, 2019

CONCLUSION

By considering the above analysis, it has been drawn that, the main objective of the company to

encourage the divisional manner in such a way by which they are guided towards for

improvising the performance of the overall company. In this report, the divisional manager

(Cleveland), was correct, as because if he transfers the product of its department to the outside

market, then definitely the division will generate profit. Further, the division through the

negotiated pricing approach as well as dual pricing approach determines the transfer price. In

addition, if the contribution margin approach is applied on sale to furniture division by the

cushion division, then it has been observed that overall profit will increase. Moreover, through

the performance measurement approach, performance and efficiency of the company can be

maximized.

Group 4|ACC202

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Arora,M.,N.,2009. Management Accounting : Theory, Problems and Solutions. Himalaya

Publishing House.Mumbai.Available from:ProQuest Ebook Central.

Blouin, J.L., Robinson, L.A. and Seidman, J.K., 2018. Conflicting transfer pricing incentives and

the role of coordination. Contemporary Accounting Research, 35(1), pp.87-116.

Brandt, A., 2016. Internal transfer pricing as management tool for guiding. Annual Review of

Psychology, 61, pp.467-490.

Clempner, J.B. and Poznyak, A.S., 2018. Solving Transfer Pricing Involving Collaborative and

Non-cooperative Equilibria in Nash and Stackelberg Games: Centralized–Decentralized Decision

Making. Computational Economics, pp.1-29.

Group 4|ACC202

Arora,M.,N.,2009. Management Accounting : Theory, Problems and Solutions. Himalaya

Publishing House.Mumbai.Available from:ProQuest Ebook Central.

Blouin, J.L., Robinson, L.A. and Seidman, J.K., 2018. Conflicting transfer pricing incentives and

the role of coordination. Contemporary Accounting Research, 35(1), pp.87-116.

Brandt, A., 2016. Internal transfer pricing as management tool for guiding. Annual Review of

Psychology, 61, pp.467-490.

Clempner, J.B. and Poznyak, A.S., 2018. Solving Transfer Pricing Involving Collaborative and

Non-cooperative Equilibria in Nash and Stackelberg Games: Centralized–Decentralized Decision

Making. Computational Economics, pp.1-29.

Group 4|ACC202

Cristea, A.D. and Nguyen, D.X., 2016. Transfer pricing by multinational firms: New evidence

from foreign firm ownerships. American Economic Journal: Economic Policy, 8(3), pp.170-202.

Davies, R.B., Martin, J., Parenti, M. and Toubal, F., 2018. Knocking on tax haven’s door:

Multinational firms and transfer pricing. Review of Economics and Statistics, 100(1), pp.120-

134.

Eldenburg,L.G.,2017.Management Accounting,3rd ed. Melbourne Wiley.

Eldenburg.L.G., Krishan,H.A. and Krishan, R., 2017. Management Accounting and Control in

the Hospital Industry: A Review, Journal of Governmental & Non Profit Accounting 6(1).pp. 52-

91. Available From : EBSCO Databases.

Epstein, M. and Malina , M. (eds), 2015. Advances in Management Accounting. Vol.25. Emerald

Publishing Limited. Bingley. Available from: ProQuest Ebook Central.

Epstein, M. and Malina , M. (eds), 2016. Advances in Management Accounting. Vol.26. Emerald

Publishing Limited. Bingley. Available from: ProQuest Ebook Central.

Ette, D., 2015. Responsible management accounting and controlling : a practical handbook for

sustainability, responsibility , and ethics. 1st.ed.New York, NY Business Expert Press.

Fernandes, R., Pinho, C. and Gouveia, B., 2015. Supply chain networks design and transfer-

pricing. The International Journal of Logistics Management, 26(1), pp.128-146.

Gao, L. and Zhao, X., 2015. Determining intra-company transfer pricing for multinational

corporations. International Journal of Production Economics, 168, pp.340-350.

Group 4|ACC202

from foreign firm ownerships. American Economic Journal: Economic Policy, 8(3), pp.170-202.

Davies, R.B., Martin, J., Parenti, M. and Toubal, F., 2018. Knocking on tax haven’s door:

Multinational firms and transfer pricing. Review of Economics and Statistics, 100(1), pp.120-

134.

Eldenburg,L.G.,2017.Management Accounting,3rd ed. Melbourne Wiley.

Eldenburg.L.G., Krishan,H.A. and Krishan, R., 2017. Management Accounting and Control in

the Hospital Industry: A Review, Journal of Governmental & Non Profit Accounting 6(1).pp. 52-

91. Available From : EBSCO Databases.

Epstein, M. and Malina , M. (eds), 2015. Advances in Management Accounting. Vol.25. Emerald

Publishing Limited. Bingley. Available from: ProQuest Ebook Central.

Epstein, M. and Malina , M. (eds), 2016. Advances in Management Accounting. Vol.26. Emerald

Publishing Limited. Bingley. Available from: ProQuest Ebook Central.

Ette, D., 2015. Responsible management accounting and controlling : a practical handbook for

sustainability, responsibility , and ethics. 1st.ed.New York, NY Business Expert Press.

Fernandes, R., Pinho, C. and Gouveia, B., 2015. Supply chain networks design and transfer-

pricing. The International Journal of Logistics Management, 26(1), pp.128-146.

Gao, L. and Zhao, X., 2015. Determining intra-company transfer pricing for multinational

corporations. International Journal of Production Economics, 168, pp.340-350.

Group 4|ACC202

Jack,L. and Mundy, J., 2013. Management accounting and control: routine and change, Emerald

Group Publishing Limited.

Johnson, E., Johnson, N.B. and Pfeiffer, T., 2016. Dual transfer pricing with internal and external

trade. Review of Accounting Studies, 21(1), pp.140-164.

Klassen, K.J., Lisowsky, P. and Mescall, D., 2017. Transfer pricing: Strategies, practices, and tax

minimization. Contemporary Accounting Research, 34(1), pp.455-493.

Leitner,S., 2013. Information Quality and Management Accounting: A simulation Analaysis of

Biases in costing system, Springer, Dordrecht. ProQuest Ebook Central.

Liu, G., Zhang, J. and Tang, W., 2015. Strategic transfer pricing in a marketing–operations

interface with quality level and advertising dependent goodwill. Omega, 56, pp.1-15.

Löffler, C., 2018. Transfer Prices for Coordination Under Decentralized Decision Making.

In Game Theory in Management Accounting (pp. 71-89). Springer, Cham.

Lyal, R., 2015. Transfer pricing rules and state aid. Fordham Int'l LJ, 38, p.1017.

McNair-Connolly, C, Polutnik, L. and Silvi, R.,2013. Value Creation in Management

Accounting: Using Information to Capture Customer value. Business Exprert Press. New York.

Available from: ProQuest Ebook Central.

McWatters, C. and Zimmerman, J., 2016. Management accounting in dynamic environment,

New York Routledge. ProQuest Ebook Central.

Ondrušová, L., 2016. Management decisions in transfer pricing. Strategic Management, 21(1),

pp.3-7.

Group 4|ACC202

Group Publishing Limited.

Johnson, E., Johnson, N.B. and Pfeiffer, T., 2016. Dual transfer pricing with internal and external

trade. Review of Accounting Studies, 21(1), pp.140-164.

Klassen, K.J., Lisowsky, P. and Mescall, D., 2017. Transfer pricing: Strategies, practices, and tax

minimization. Contemporary Accounting Research, 34(1), pp.455-493.

Leitner,S., 2013. Information Quality and Management Accounting: A simulation Analaysis of

Biases in costing system, Springer, Dordrecht. ProQuest Ebook Central.

Liu, G., Zhang, J. and Tang, W., 2015. Strategic transfer pricing in a marketing–operations

interface with quality level and advertising dependent goodwill. Omega, 56, pp.1-15.

Löffler, C., 2018. Transfer Prices for Coordination Under Decentralized Decision Making.

In Game Theory in Management Accounting (pp. 71-89). Springer, Cham.

Lyal, R., 2015. Transfer pricing rules and state aid. Fordham Int'l LJ, 38, p.1017.

McNair-Connolly, C, Polutnik, L. and Silvi, R.,2013. Value Creation in Management

Accounting: Using Information to Capture Customer value. Business Exprert Press. New York.

Available from: ProQuest Ebook Central.

McWatters, C. and Zimmerman, J., 2016. Management accounting in dynamic environment,

New York Routledge. ProQuest Ebook Central.

Ondrušová, L., 2016. Management decisions in transfer pricing. Strategic Management, 21(1),

pp.3-7.

Group 4|ACC202

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Tinkelman,D.,2015. Introductory accounting: a measurement approach for managers, London

Routledge. ProQuest Ebook Central.

Watts, D.,Yapa, P.W. and Dellaportas,S.,2014. The Case of a Newly Implemented Modern

Managemnt Accounting System in a Multinational Manufactring Company. Australasian

Accounting, Business and Finance Journal,8(2),pp.121-137. Available from: EBSCo databases.

Wynn,M.T., Low,W.Z. and Nauta, W., 2013. A Framework for Cost – Aware Process

Management: Generation of Accurate and Timely Management Accounting Cost Reports.

Proceedings of the Ninth Asia – Pacific Conference Modelling. CRPIT Conceptual Modelling.

Vol.143 pp. 79-88. Adelaide, Australia. Avaialble from :

http://crpit.com./confpapaers/CRPITV143Wynn.pdf.

Group 4|ACC202

Routledge. ProQuest Ebook Central.

Watts, D.,Yapa, P.W. and Dellaportas,S.,2014. The Case of a Newly Implemented Modern

Managemnt Accounting System in a Multinational Manufactring Company. Australasian

Accounting, Business and Finance Journal,8(2),pp.121-137. Available from: EBSCo databases.

Wynn,M.T., Low,W.Z. and Nauta, W., 2013. A Framework for Cost – Aware Process

Management: Generation of Accurate and Timely Management Accounting Cost Reports.

Proceedings of the Ninth Asia – Pacific Conference Modelling. CRPIT Conceptual Modelling.

Vol.143 pp. 79-88. Adelaide, Australia. Avaialble from :

http://crpit.com./confpapaers/CRPITV143Wynn.pdf.

Group 4|ACC202

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.