UGB222 Management Accounting Assignment Solution and Analysis

VerifiedAdded on 2023/06/10

|12

|2893

|167

Homework Assignment

AI Summary

This document provides a comprehensive solution to a Management Accounting assignment, addressing several key concepts. The solution begins with an analysis using the high-low method to determine variable and fixed costs, followed by calculations for expected operating costs at different occupancy rates. The assignment then delves into cost of goods sold, income statements, and various variance analyses, including material price and usage variances, labor rate and efficiency variances, and variable overhead variances. The solution also explores the causes behind these variances and describes how to examine variance in relation to work performance. Finally, it provides a detailed breakdown of relevant costs, make-or-buy decisions, incremental costs, and opportunity costs, offering a complete overview of the assignment's requirements.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Question 1....................................................................................................................................3

Question 2....................................................................................................................................5

(i)..................................................................................................................................................5

(ii)................................................................................................................................................6

Question 4....................................................................................................................................6

Question 5....................................................................................................................................9

(a).................................................................................................................................................9

(b)...............................................................................................................................................10

(c)...............................................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Question 1....................................................................................................................................3

Question 2....................................................................................................................................5

(i)..................................................................................................................................................5

(ii)................................................................................................................................................6

Question 4....................................................................................................................................6

Question 5....................................................................................................................................9

(a).................................................................................................................................................9

(b)...............................................................................................................................................10

(c)...............................................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Managerial Accounting is process which includes measuring, interpreting, interpreting,

communicating and identifying the transactions of the management. It further deviates from the

financial accounting which assists in knowing internal information of the company. In the

following report it includes how manager performs account work and opportunity cost. This

accounting helps in growing the business by considering various cost and fixed cost which

includes in the organisation. It is different from the bookkeeping which records financial

transactions of the company and administration accounting of the business concern (Brown and

et.al., 2020).

MAIN BODY

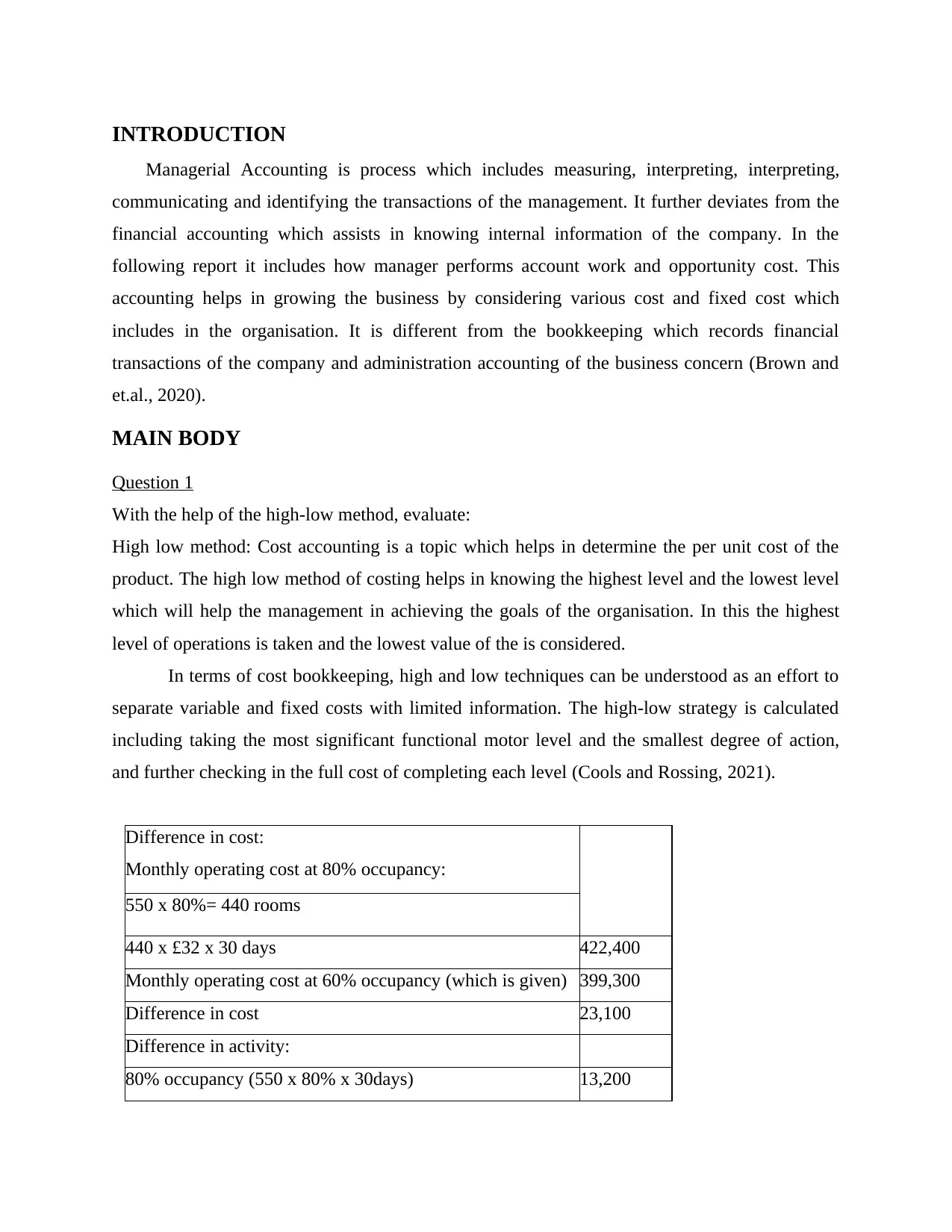

Question 1

With the help of the high-low method, evaluate:

High low method: Cost accounting is a topic which helps in determine the per unit cost of the

product. The high low method of costing helps in knowing the highest level and the lowest level

which will help the management in achieving the goals of the organisation. In this the highest

level of operations is taken and the lowest value of the is considered.

In terms of cost bookkeeping, high and low techniques can be understood as an effort to

separate variable and fixed costs with limited information. The high-low strategy is calculated

including taking the most significant functional motor level and the smallest degree of action,

and further checking in the full cost of completing each level (Cools and Rossing, 2021).

Difference in cost:

Monthly operating cost at 80% occupancy:

550 x 80%= 440 rooms

440 x £32 x 30 days 422,400

Monthly operating cost at 60% occupancy (which is given) 399,300

Difference in cost 23,100

Difference in activity:

80% occupancy (550 x 80% x 30days) 13,200

Managerial Accounting is process which includes measuring, interpreting, interpreting,

communicating and identifying the transactions of the management. It further deviates from the

financial accounting which assists in knowing internal information of the company. In the

following report it includes how manager performs account work and opportunity cost. This

accounting helps in growing the business by considering various cost and fixed cost which

includes in the organisation. It is different from the bookkeeping which records financial

transactions of the company and administration accounting of the business concern (Brown and

et.al., 2020).

MAIN BODY

Question 1

With the help of the high-low method, evaluate:

High low method: Cost accounting is a topic which helps in determine the per unit cost of the

product. The high low method of costing helps in knowing the highest level and the lowest level

which will help the management in achieving the goals of the organisation. In this the highest

level of operations is taken and the lowest value of the is considered.

In terms of cost bookkeeping, high and low techniques can be understood as an effort to

separate variable and fixed costs with limited information. The high-low strategy is calculated

including taking the most significant functional motor level and the smallest degree of action,

and further checking in the full cost of completing each level (Cools and Rossing, 2021).

Difference in cost:

Monthly operating cost at 80% occupancy:

550 x 80%= 440 rooms

440 x £32 x 30 days 422,400

Monthly operating cost at 60% occupancy (which is given) 399,300

Difference in cost 23,100

Difference in activity:

80% occupancy (550 x 80% x 30days) 13,200

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

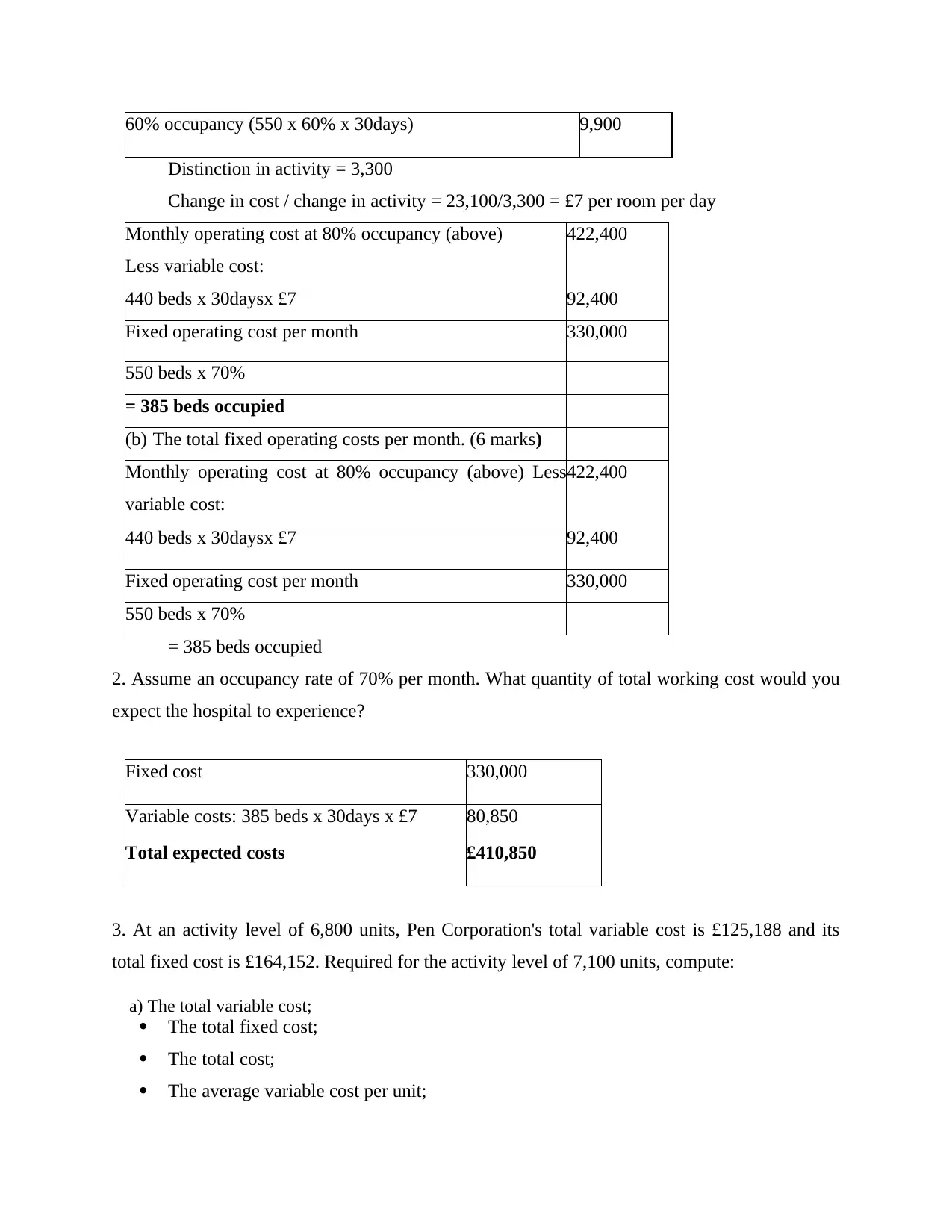

60% occupancy (550 x 60% x 30days) 9,900

Distinction in activity = 3,300

Change in cost / change in activity = 23,100/3,300 = £7 per room per day

Monthly operating cost at 80% occupancy (above)

Less variable cost:

422,400

440 beds x 30daysx £7 92,400

Fixed operating cost per month 330,000

550 beds x 70%

= 385 beds occupied

(b) The total fixed operating costs per month. (6 marks)

Monthly operating cost at 80% occupancy (above) Less

variable cost:

422,400

440 beds x 30daysx £7 92,400

Fixed operating cost per month 330,000

550 beds x 70%

= 385 beds occupied

2. Assume an occupancy rate of 70% per month. What quantity of total working cost would you

expect the hospital to experience?

Fixed cost 330,000

Variable costs: 385 beds x 30days x £7 80,850

Total expected costs £410,850

3. At an activity level of 6,800 units, Pen Corporation's total variable cost is £125,188 and its

total fixed cost is £164,152. Required for the activity level of 7,100 units, compute:

a) The total variable cost;

The total fixed cost;

The total cost;

The average variable cost per unit;

Distinction in activity = 3,300

Change in cost / change in activity = 23,100/3,300 = £7 per room per day

Monthly operating cost at 80% occupancy (above)

Less variable cost:

422,400

440 beds x 30daysx £7 92,400

Fixed operating cost per month 330,000

550 beds x 70%

= 385 beds occupied

(b) The total fixed operating costs per month. (6 marks)

Monthly operating cost at 80% occupancy (above) Less

variable cost:

422,400

440 beds x 30daysx £7 92,400

Fixed operating cost per month 330,000

550 beds x 70%

= 385 beds occupied

2. Assume an occupancy rate of 70% per month. What quantity of total working cost would you

expect the hospital to experience?

Fixed cost 330,000

Variable costs: 385 beds x 30days x £7 80,850

Total expected costs £410,850

3. At an activity level of 6,800 units, Pen Corporation's total variable cost is £125,188 and its

total fixed cost is £164,152. Required for the activity level of 7,100 units, compute:

a) The total variable cost;

The total fixed cost;

The total cost;

The average variable cost per unit;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

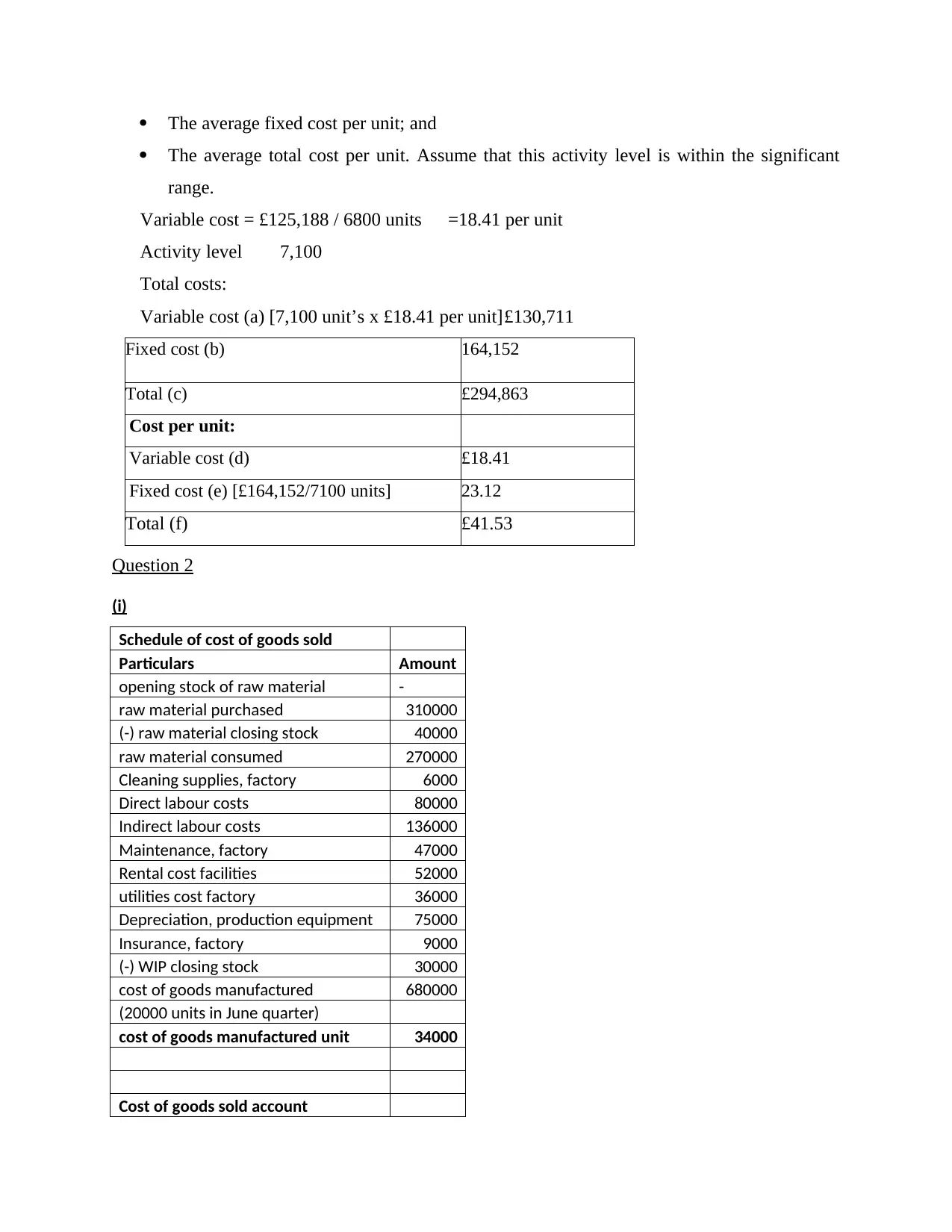

The average fixed cost per unit; and

The average total cost per unit. Assume that this activity level is within the significant

range.

Variable cost = £125,188 / 6800 units =18.41 per unit

Activity level 7,100

Total costs:

Variable cost (a) [7,100 unit’s x £18.41 per unit]£130,711

Fixed cost (b) 164,152

Total (c) £294,863

Cost per unit:

Variable cost (d) £18.41

Fixed cost (e) [£164,152/7100 units] 23.12

Total (f) £41.53

Question 2

(i)

Schedule of cost of goods sold

Particulars Amount

opening stock of raw material -

raw material purchased 310000

(-) raw material closing stock 40000

raw material consumed 270000

Cleaning supplies, factory 6000

Direct labour costs 80000

Indirect labour costs 136000

Maintenance, factory 47000

Rental cost facilities 52000

utilities cost factory 36000

Depreciation, production equipment 75000

Insurance, factory 9000

(-) WIP closing stock 30000

cost of goods manufactured 680000

(20000 units in June quarter)

cost of goods manufactured unit 34000

Cost of goods sold account

The average total cost per unit. Assume that this activity level is within the significant

range.

Variable cost = £125,188 / 6800 units =18.41 per unit

Activity level 7,100

Total costs:

Variable cost (a) [7,100 unit’s x £18.41 per unit]£130,711

Fixed cost (b) 164,152

Total (c) £294,863

Cost per unit:

Variable cost (d) £18.41

Fixed cost (e) [£164,152/7100 units] 23.12

Total (f) £41.53

Question 2

(i)

Schedule of cost of goods sold

Particulars Amount

opening stock of raw material -

raw material purchased 310000

(-) raw material closing stock 40000

raw material consumed 270000

Cleaning supplies, factory 6000

Direct labour costs 80000

Indirect labour costs 136000

Maintenance, factory 47000

Rental cost facilities 52000

utilities cost factory 36000

Depreciation, production equipment 75000

Insurance, factory 9000

(-) WIP closing stock 30000

cost of goods manufactured 680000

(20000 units in June quarter)

cost of goods manufactured unit 34000

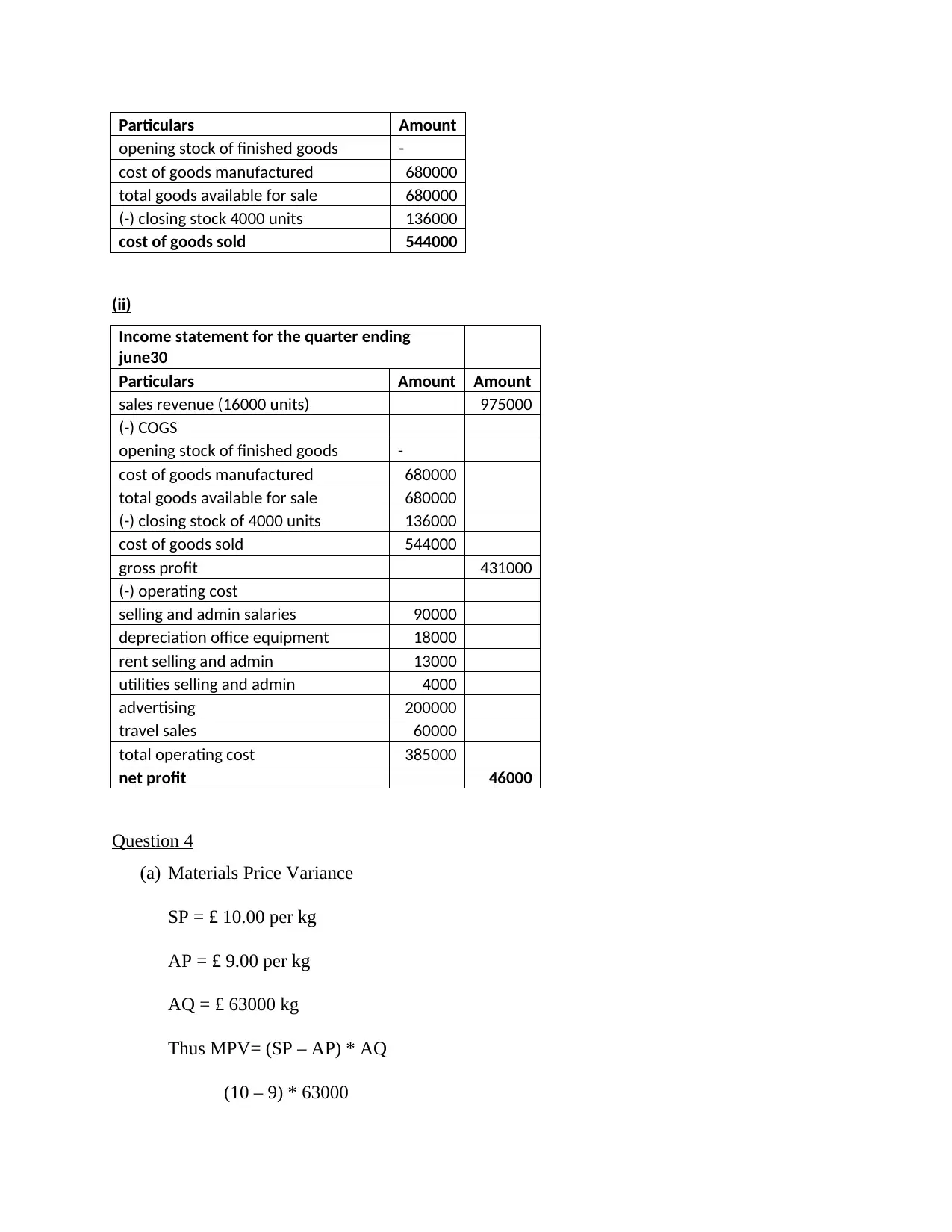

Cost of goods sold account

Particulars Amount

opening stock of finished goods -

cost of goods manufactured 680000

total goods available for sale 680000

(-) closing stock 4000 units 136000

cost of goods sold 544000

(ii)

Income statement for the quarter ending

june30

Particulars Amount Amount

sales revenue (16000 units) 975000

(-) COGS

opening stock of finished goods -

cost of goods manufactured 680000

total goods available for sale 680000

(-) closing stock of 4000 units 136000

cost of goods sold 544000

gross profit 431000

(-) operating cost

selling and admin salaries 90000

depreciation office equipment 18000

rent selling and admin 13000

utilities selling and admin 4000

advertising 200000

travel sales 60000

total operating cost 385000

net profit 46000

Question 4

(a) Materials Price Variance

SP = £ 10.00 per kg

AP = £ 9.00 per kg

AQ = £ 63000 kg

Thus MPV= (SP – AP) * AQ

(10 – 9) * 63000

opening stock of finished goods -

cost of goods manufactured 680000

total goods available for sale 680000

(-) closing stock 4000 units 136000

cost of goods sold 544000

(ii)

Income statement for the quarter ending

june30

Particulars Amount Amount

sales revenue (16000 units) 975000

(-) COGS

opening stock of finished goods -

cost of goods manufactured 680000

total goods available for sale 680000

(-) closing stock of 4000 units 136000

cost of goods sold 544000

gross profit 431000

(-) operating cost

selling and admin salaries 90000

depreciation office equipment 18000

rent selling and admin 13000

utilities selling and admin 4000

advertising 200000

travel sales 60000

total operating cost 385000

net profit 46000

Question 4

(a) Materials Price Variance

SP = £ 10.00 per kg

AP = £ 9.00 per kg

AQ = £ 63000 kg

Thus MPV= (SP – AP) * AQ

(10 – 9) * 63000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

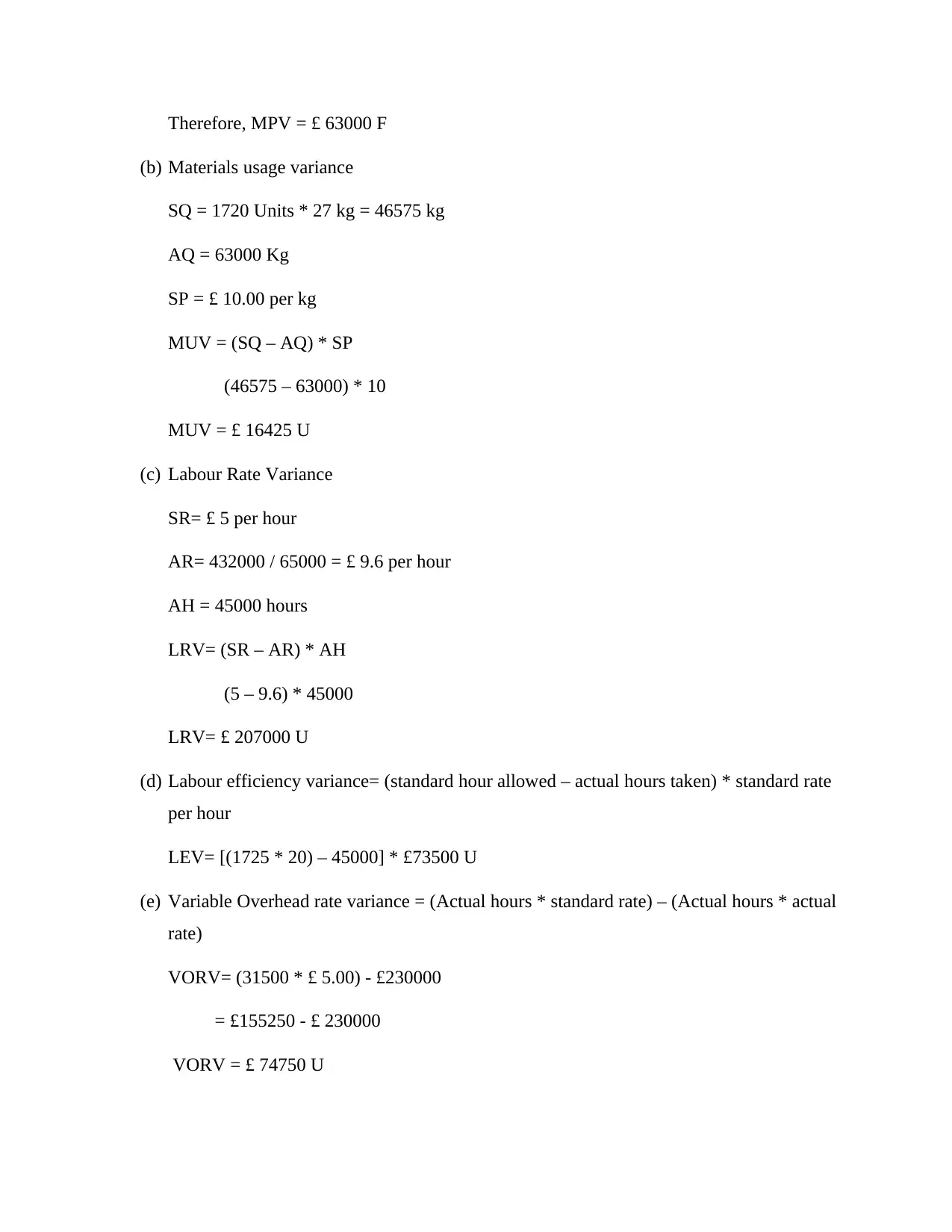

Therefore, MPV = £ 63000 F

(b) Materials usage variance

SQ = 1720 Units * 27 kg = 46575 kg

AQ = 63000 Kg

SP = £ 10.00 per kg

MUV = (SQ – AQ) * SP

(46575 – 63000) * 10

MUV = £ 16425 U

(c) Labour Rate Variance

SR= £ 5 per hour

AR= 432000 / 65000 = £ 9.6 per hour

AH = 45000 hours

LRV= (SR – AR) * AH

(5 – 9.6) * 45000

LRV= £ 207000 U

(d) Labour efficiency variance= (standard hour allowed – actual hours taken) * standard rate

per hour

LEV= [(1725 * 20) – 45000] * £73500 U

(e) Variable Overhead rate variance = (Actual hours * standard rate) – (Actual hours * actual

rate)

VORV= (31500 * £ 5.00) - £230000

= £155250 - £ 230000

VORV = £ 74750 U

(b) Materials usage variance

SQ = 1720 Units * 27 kg = 46575 kg

AQ = 63000 Kg

SP = £ 10.00 per kg

MUV = (SQ – AQ) * SP

(46575 – 63000) * 10

MUV = £ 16425 U

(c) Labour Rate Variance

SR= £ 5 per hour

AR= 432000 / 65000 = £ 9.6 per hour

AH = 45000 hours

LRV= (SR – AR) * AH

(5 – 9.6) * 45000

LRV= £ 207000 U

(d) Labour efficiency variance= (standard hour allowed – actual hours taken) * standard rate

per hour

LEV= [(1725 * 20) – 45000] * £73500 U

(e) Variable Overhead rate variance = (Actual hours * standard rate) – (Actual hours * actual

rate)

VORV= (31500 * £ 5.00) - £230000

= £155250 - £ 230000

VORV = £ 74750 U

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

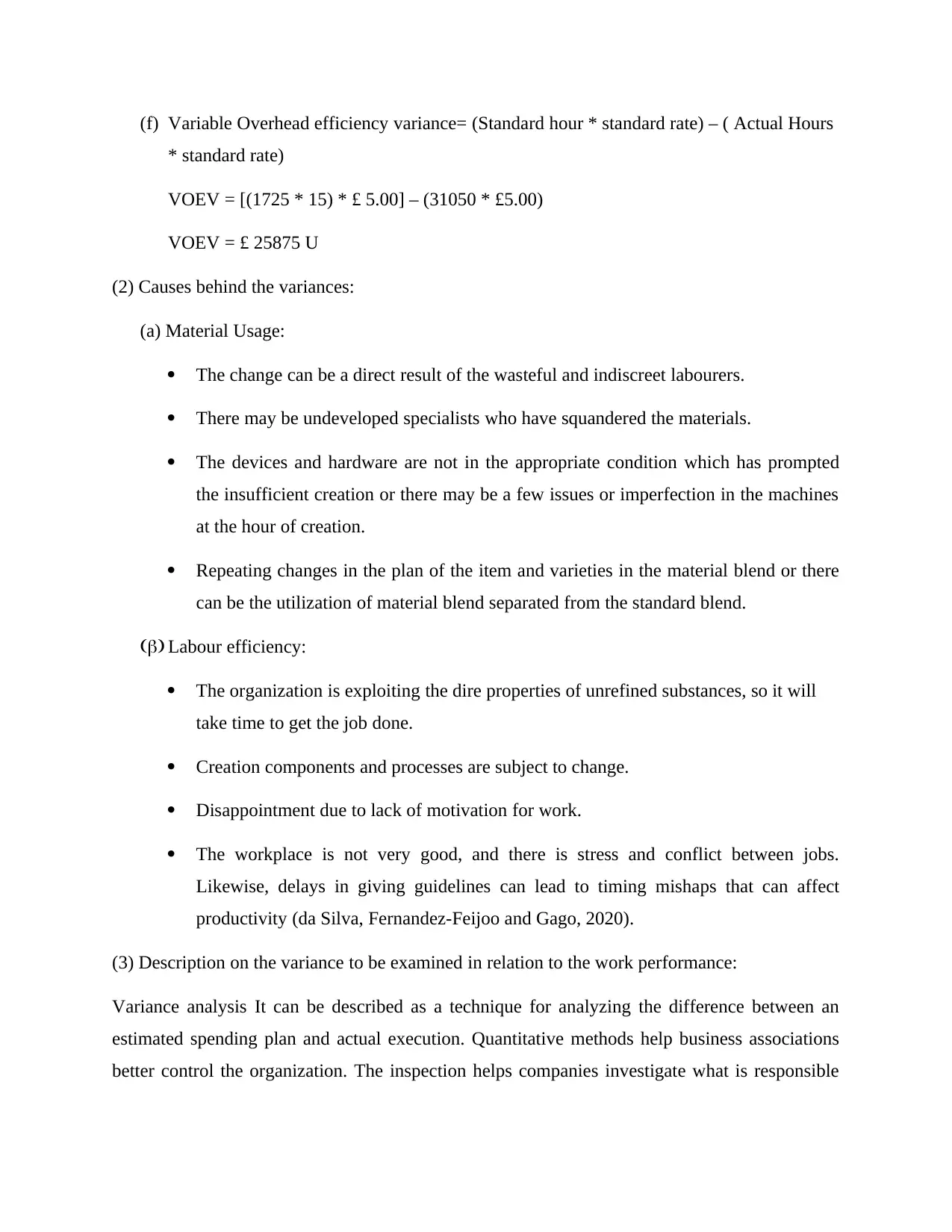

(f) Variable Overhead efficiency variance= (Standard hour * standard rate) – ( Actual Hours

* standard rate)

VOEV = [(1725 * 15) * £ 5.00] – (31050 * £5.00)

VOEV = £ 25875 U

(2) Causes behind the variances:

(a) Material Usage:

The change can be a direct result of the wasteful and indiscreet labourers.

There may be undeveloped specialists who have squandered the materials.

The devices and hardware are not in the appropriate condition which has prompted

the insufficient creation or there may be a few issues or imperfection in the machines

at the hour of creation.

Repeating changes in the plan of the item and varieties in the material blend or there

can be the utilization of material blend separated from the standard blend.

(b) Labour efficiency:

The organization is exploiting the dire properties of unrefined substances, so it will

take time to get the job done.

Creation components and processes are subject to change.

Disappointment due to lack of motivation for work.

The workplace is not very good, and there is stress and conflict between jobs.

Likewise, delays in giving guidelines can lead to timing mishaps that can affect

productivity (da Silva, Fernandez-Feijoo and Gago, 2020).

(3) Description on the variance to be examined in relation to the work performance:

Variance analysis It can be described as a technique for analyzing the difference between an

estimated spending plan and actual execution. Quantitative methods help business associations

better control the organization. The inspection helps companies investigate what is responsible

* standard rate)

VOEV = [(1725 * 15) * £ 5.00] – (31050 * £5.00)

VOEV = £ 25875 U

(2) Causes behind the variances:

(a) Material Usage:

The change can be a direct result of the wasteful and indiscreet labourers.

There may be undeveloped specialists who have squandered the materials.

The devices and hardware are not in the appropriate condition which has prompted

the insufficient creation or there may be a few issues or imperfection in the machines

at the hour of creation.

Repeating changes in the plan of the item and varieties in the material blend or there

can be the utilization of material blend separated from the standard blend.

(b) Labour efficiency:

The organization is exploiting the dire properties of unrefined substances, so it will

take time to get the job done.

Creation components and processes are subject to change.

Disappointment due to lack of motivation for work.

The workplace is not very good, and there is stress and conflict between jobs.

Likewise, delays in giving guidelines can lead to timing mishaps that can affect

productivity (da Silva, Fernandez-Feijoo and Gago, 2020).

(3) Description on the variance to be examined in relation to the work performance:

Variance analysis It can be described as a technique for analyzing the difference between an

estimated spending plan and actual execution. Quantitative methods help business associations

better control the organization. The inspection helps companies investigate what is responsible

for the deviation. The reason for the distinction depends on economic conditions, job changes,

the above differences, financial planning guidelines, etc.

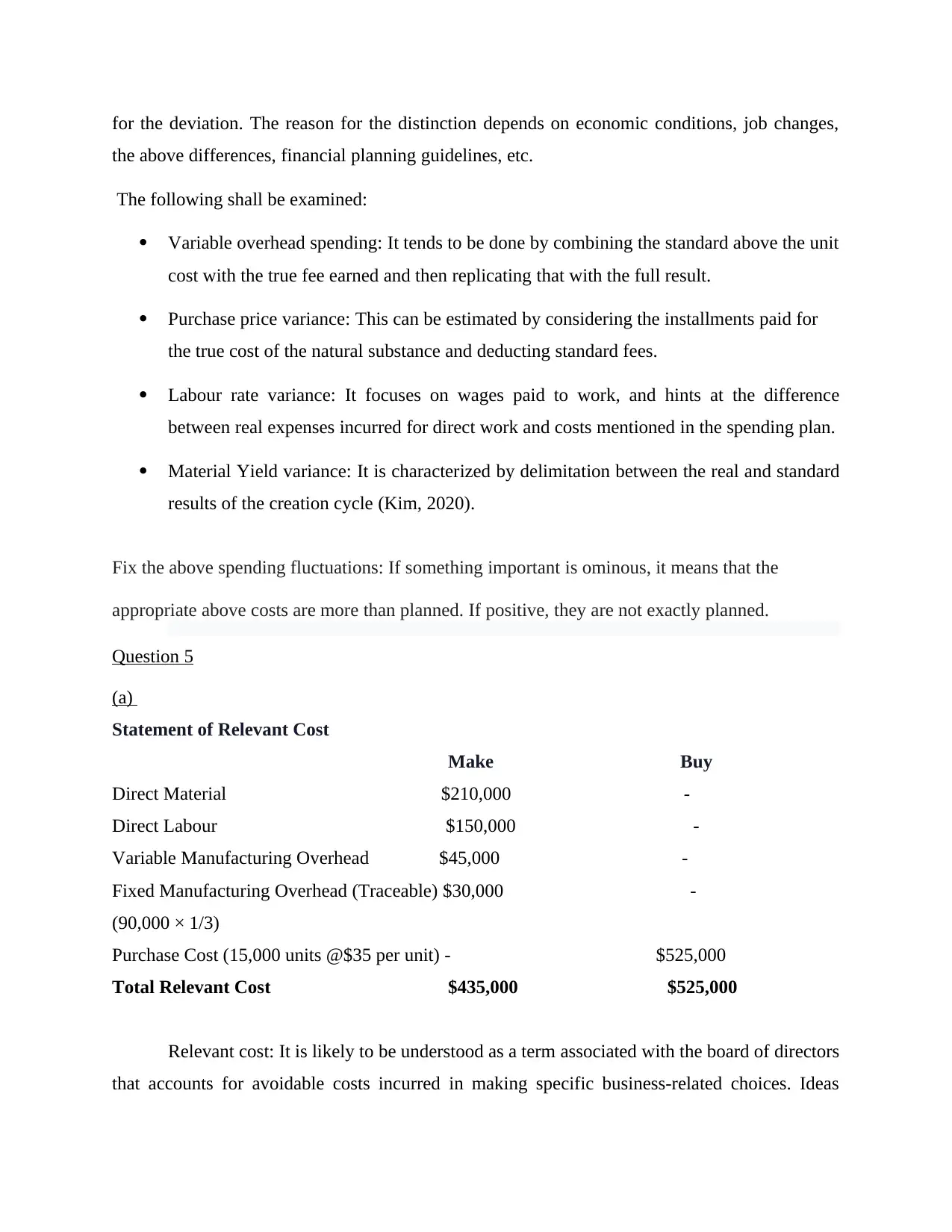

The following shall be examined:

Variable overhead spending: It tends to be done by combining the standard above the unit

cost with the true fee earned and then replicating that with the full result.

Purchase price variance: This can be estimated by considering the installments paid for

the true cost of the natural substance and deducting standard fees.

Labour rate variance: It focuses on wages paid to work, and hints at the difference

between real expenses incurred for direct work and costs mentioned in the spending plan.

Material Yield variance: It is characterized by delimitation between the real and standard

results of the creation cycle (Kim, 2020).

Fix the above spending fluctuations: If something important is ominous, it means that the

appropriate above costs are more than planned. If positive, they are not exactly planned.

Question 5

(a)

Statement of Relevant Cost

Make Buy

Direct Material $210,000 -

Direct Labour $150,000 -

Variable Manufacturing Overhead $45,000 -

Fixed Manufacturing Overhead (Traceable) $30,000 -

(90,000 × 1/3)

Purchase Cost (15,000 units @$35 per unit) - $525,000

Total Relevant Cost $435,000 $525,000

Relevant cost: It is likely to be understood as a term associated with the board of directors

that accounts for avoidable costs incurred in making specific business-related choices. Ideas

the above differences, financial planning guidelines, etc.

The following shall be examined:

Variable overhead spending: It tends to be done by combining the standard above the unit

cost with the true fee earned and then replicating that with the full result.

Purchase price variance: This can be estimated by considering the installments paid for

the true cost of the natural substance and deducting standard fees.

Labour rate variance: It focuses on wages paid to work, and hints at the difference

between real expenses incurred for direct work and costs mentioned in the spending plan.

Material Yield variance: It is characterized by delimitation between the real and standard

results of the creation cycle (Kim, 2020).

Fix the above spending fluctuations: If something important is ominous, it means that the

appropriate above costs are more than planned. If positive, they are not exactly planned.

Question 5

(a)

Statement of Relevant Cost

Make Buy

Direct Material $210,000 -

Direct Labour $150,000 -

Variable Manufacturing Overhead $45,000 -

Fixed Manufacturing Overhead (Traceable) $30,000 -

(90,000 × 1/3)

Purchase Cost (15,000 units @$35 per unit) - $525,000

Total Relevant Cost $435,000 $525,000

Relevant cost: It is likely to be understood as a term associated with the board of directors

that accounts for avoidable costs incurred in making specific business-related choices. Ideas

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

related to associated costs are also valuable for dealing with unwanted and redundant data that

can clutter and clutter the selection process. An important fee is the fee associated with a specific

management decision and will change in the future as a result of that decision. The possibility of

a key fee is very useful to eliminate too much information from a clearly strong collaboration.

Furthermore, by managing the cost of bad in decision-making, the board doesn't zero in on

information that could erroneously influence its choices. Significant charges (now aka

fluctuating charges) imply the financial cost of business choices. Charges are certainly not a

uniform measure and will oscillate based on clear decisions. Huge costs are an important

financial metric because it helps associations limit minor or immaterial costs that disrupt

dynamic connections here and there. If something doesn't financially influence your decision, the

fee is meaningless. If a decision is likely to affect compensation, things matter, and the cost of

that decision is worth considering (Liu, 2019).

This idea works well for conference room accounting. It is not used in this case because

the spending selection is not really related to the planning reported by the spending plan.

The motor should be made instead of bought, and the proposal should not be acknowledged as it

would have resulted in a cost increase of $90,000 ($525,000 - $435,000).

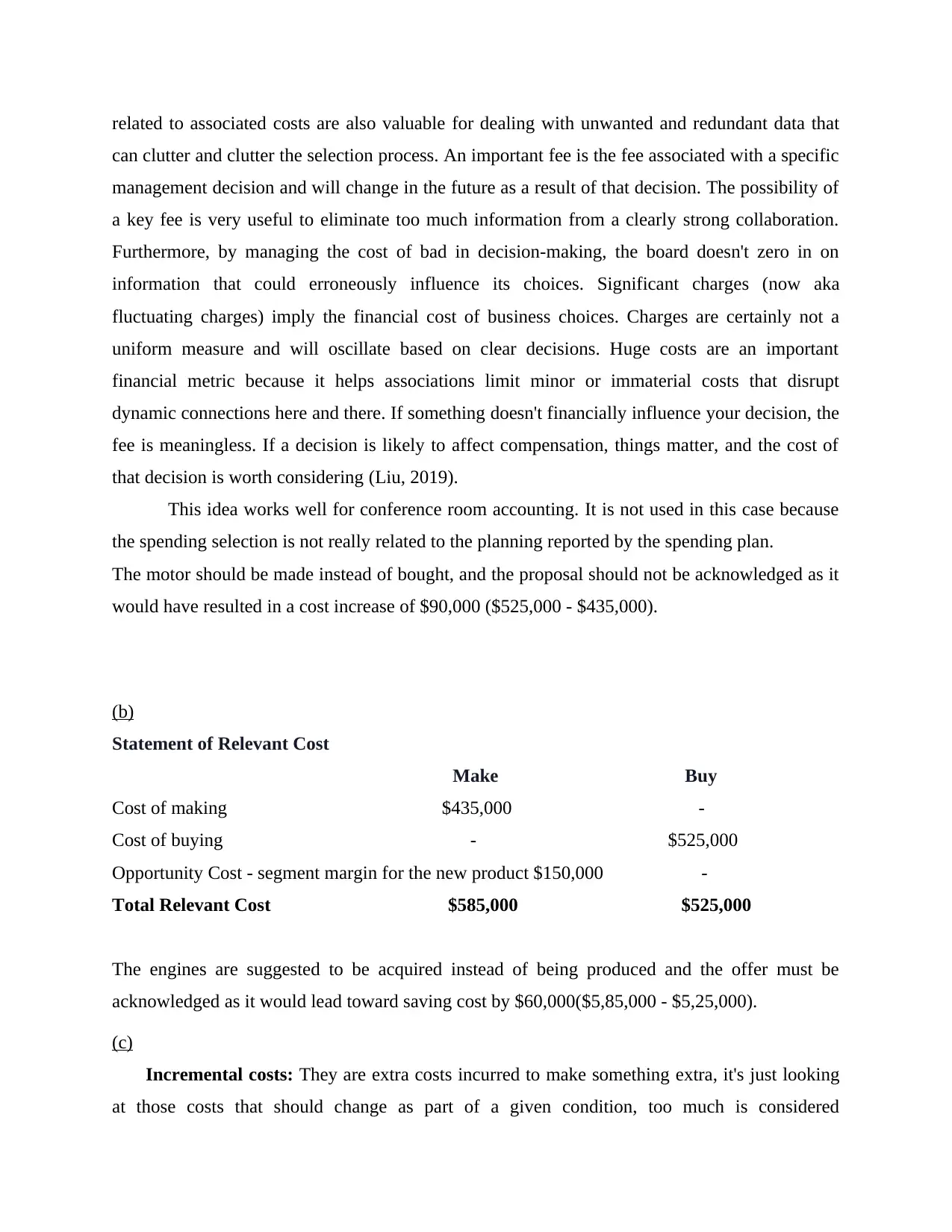

(b)

Statement of Relevant Cost

Make Buy

Cost of making $435,000 -

Cost of buying - $525,000

Opportunity Cost - segment margin for the new product $150,000 -

Total Relevant Cost $585,000 $525,000

The engines are suggested to be acquired instead of being produced and the offer must be

acknowledged as it would lead toward saving cost by $60,000($5,85,000 - $5,25,000).

(c)

Incremental costs: They are extra costs incurred to make something extra, it's just looking

at those costs that should change as part of a given condition, too much is considered

can clutter and clutter the selection process. An important fee is the fee associated with a specific

management decision and will change in the future as a result of that decision. The possibility of

a key fee is very useful to eliminate too much information from a clearly strong collaboration.

Furthermore, by managing the cost of bad in decision-making, the board doesn't zero in on

information that could erroneously influence its choices. Significant charges (now aka

fluctuating charges) imply the financial cost of business choices. Charges are certainly not a

uniform measure and will oscillate based on clear decisions. Huge costs are an important

financial metric because it helps associations limit minor or immaterial costs that disrupt

dynamic connections here and there. If something doesn't financially influence your decision, the

fee is meaningless. If a decision is likely to affect compensation, things matter, and the cost of

that decision is worth considering (Liu, 2019).

This idea works well for conference room accounting. It is not used in this case because

the spending selection is not really related to the planning reported by the spending plan.

The motor should be made instead of bought, and the proposal should not be acknowledged as it

would have resulted in a cost increase of $90,000 ($525,000 - $435,000).

(b)

Statement of Relevant Cost

Make Buy

Cost of making $435,000 -

Cost of buying - $525,000

Opportunity Cost - segment margin for the new product $150,000 -

Total Relevant Cost $585,000 $525,000

The engines are suggested to be acquired instead of being produced and the offer must be

acknowledged as it would lead toward saving cost by $60,000($5,85,000 - $5,25,000).

(c)

Incremental costs: They are extra costs incurred to make something extra, it's just looking

at those costs that should change as part of a given condition, too much is considered

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

unnecessary. This is likely to be understood as an additional expense that the company sees as a

result of changes to the evaluation system related to creation, hardware and innovation upgrades,

or the introduction of reinforcement programs for referenced models. It can also be understood

as a benefit that helps to identify gradual changes in costs under various conditions. For example,

the cost of stabilization on behalf of the purpose would include the cost of additional advantages

given to the individual due to the purpose. Or the steady cost of shutting down a production line,

which includes costs related to local staff, providing unwelcome hardware, and switching offices

entirely for several different purposes (Martin, 2020).

Opportunity cost: When a respective person gives comments regarding “opportunity cost”

of an item, they have been discussing regarding the valuation of the product’s next highest

valued substitute utilisation. If someone is able to devote a bunch of money for attending movies

for instance, you are not able to expend additional time in reading textbooks at home or use the

funds towards something else. If reading such books is next best option considered after

watching a movie is the price of ticket and furthers the fun which would lose out on by not going

through the textbooks. It would present the possible benefits which a respective person, business

misses or investors on when selecting one alternative over other. Because opportunity costs are

unwanted through definition, they can be simply ignored. It can be defined as an economic

terminology which states the value of what you need to give up in related to choose something

else (Modell, 2022).

CONCLUSION

From the above report, it can be concluded that administrative bookkeeping plays an

important role in handling the different functions within a business association. It is critical for

associations to manage their records to understand where they need to contribute and where they

don't. Administrative bookkeeping is happy to incur costs for business purposes. Bookkeeping

plays an important role in promoting the growth of business associations. This is considered the

process of deciphering various viewpoints to deal with the monetary part of business activities.

The chamber of commerce must really manage its own expenses in order to be strong and

effective, and to have business development. There are various costs that need to be controlled in

order to benefit from business efforts.

result of changes to the evaluation system related to creation, hardware and innovation upgrades,

or the introduction of reinforcement programs for referenced models. It can also be understood

as a benefit that helps to identify gradual changes in costs under various conditions. For example,

the cost of stabilization on behalf of the purpose would include the cost of additional advantages

given to the individual due to the purpose. Or the steady cost of shutting down a production line,

which includes costs related to local staff, providing unwelcome hardware, and switching offices

entirely for several different purposes (Martin, 2020).

Opportunity cost: When a respective person gives comments regarding “opportunity cost”

of an item, they have been discussing regarding the valuation of the product’s next highest

valued substitute utilisation. If someone is able to devote a bunch of money for attending movies

for instance, you are not able to expend additional time in reading textbooks at home or use the

funds towards something else. If reading such books is next best option considered after

watching a movie is the price of ticket and furthers the fun which would lose out on by not going

through the textbooks. It would present the possible benefits which a respective person, business

misses or investors on when selecting one alternative over other. Because opportunity costs are

unwanted through definition, they can be simply ignored. It can be defined as an economic

terminology which states the value of what you need to give up in related to choose something

else (Modell, 2022).

CONCLUSION

From the above report, it can be concluded that administrative bookkeeping plays an

important role in handling the different functions within a business association. It is critical for

associations to manage their records to understand where they need to contribute and where they

don't. Administrative bookkeeping is happy to incur costs for business purposes. Bookkeeping

plays an important role in promoting the growth of business associations. This is considered the

process of deciphering various viewpoints to deal with the monetary part of business activities.

The chamber of commerce must really manage its own expenses in order to be strong and

effective, and to have business development. There are various costs that need to be controlled in

order to benefit from business efforts.

REFERENCES

Books and Journals

Brown, P. and et.al., 2020. Automation and management control in dynamic environments:

Managing organisational flexibility and energy efficiency in service sectors. The British

Accounting Review, 52(2), p.100840.

Cools, M. and Rossing, J.C.P., 2021. International Transfer Pricing: MNE Dependency on

Knowledge of External Tax Consultants. Journal of Management Accounting

Research, 33(1), pp.33-51.

da Silva, A.F., Fernandez-Feijoo, B. and Gago, S., 2020. Accounting information tools in

managerial clinical service decision-making processes: Evidence from Portuguese

public hospitals. International Public Management Journal, 23(4), pp.535-563.

Kim, J., 2020. When Organizational Performance Matters for Personnel Decisions: Executives’

Career Patterns in a Conglomerate. Management Accounting Research, 49, p.100695.

Liu, M., 2019. Accruals, managerial operating decisions, and firm growth: Implications for tests

of earnings management. Journal of Management Accounting Research, 31(1), pp.153-

193.

Martin, M.A., 2020. An evolutionary approach to management control systems research: A

prescription for future research. Accounting, Organizations and Society, 86, p.101186.

Modell, S., 2022. Accounting for institutional work: a critical review. European Accounting

Review, 31(1), pp.33-58.

Ostaev, G.Y. and et.al., 2019. Biological fixed assets: Accounting and management problems of

commissioning in horticultural enterprises. Research Journal of Pharmaceutical,

Biological and Chemical Sciences, 10(1), pp.1258-1266.

Qawasmeh, S.Y. and Azzam, M.J., 2020. CEO characteristics and earnings management.

Accounting, 6 (7), 1403–1410.

Shawver, T.J. and Miller, W.F., 2019. Giving voice to values in accounting. New York:

Routledge.

Svirko, S.V. and Trostenyuk, T.M., 2019. Funktsiyi, zavdannya, elementy ta pryntsypy

upravlinskoho obliku v derzhavnykh zakladakh vyshchoyi osvity [Functions, tasks,

elements and principles of management accounting in public institutions of higher

education]. Ekonomika ta derzhava [Economy and state], 2, pp.41-46.

Books and Journals

Brown, P. and et.al., 2020. Automation and management control in dynamic environments:

Managing organisational flexibility and energy efficiency in service sectors. The British

Accounting Review, 52(2), p.100840.

Cools, M. and Rossing, J.C.P., 2021. International Transfer Pricing: MNE Dependency on

Knowledge of External Tax Consultants. Journal of Management Accounting

Research, 33(1), pp.33-51.

da Silva, A.F., Fernandez-Feijoo, B. and Gago, S., 2020. Accounting information tools in

managerial clinical service decision-making processes: Evidence from Portuguese

public hospitals. International Public Management Journal, 23(4), pp.535-563.

Kim, J., 2020. When Organizational Performance Matters for Personnel Decisions: Executives’

Career Patterns in a Conglomerate. Management Accounting Research, 49, p.100695.

Liu, M., 2019. Accruals, managerial operating decisions, and firm growth: Implications for tests

of earnings management. Journal of Management Accounting Research, 31(1), pp.153-

193.

Martin, M.A., 2020. An evolutionary approach to management control systems research: A

prescription for future research. Accounting, Organizations and Society, 86, p.101186.

Modell, S., 2022. Accounting for institutional work: a critical review. European Accounting

Review, 31(1), pp.33-58.

Ostaev, G.Y. and et.al., 2019. Biological fixed assets: Accounting and management problems of

commissioning in horticultural enterprises. Research Journal of Pharmaceutical,

Biological and Chemical Sciences, 10(1), pp.1258-1266.

Qawasmeh, S.Y. and Azzam, M.J., 2020. CEO characteristics and earnings management.

Accounting, 6 (7), 1403–1410.

Shawver, T.J. and Miller, W.F., 2019. Giving voice to values in accounting. New York:

Routledge.

Svirko, S.V. and Trostenyuk, T.M., 2019. Funktsiyi, zavdannya, elementy ta pryntsypy

upravlinskoho obliku v derzhavnykh zakladakh vyshchoyi osvity [Functions, tasks,

elements and principles of management accounting in public institutions of higher

education]. Ekonomika ta derzhava [Economy and state], 2, pp.41-46.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.