Ask a question from expert

Management Accounting- Assignment (Doc)

8 Pages2993 Words224 Views

Added on 2020-04-01

Management Accounting- Assignment (Doc)

Added on 2020-04-01

BookmarkShareRelated Documents

MANAGEMENT ACCOUNTING

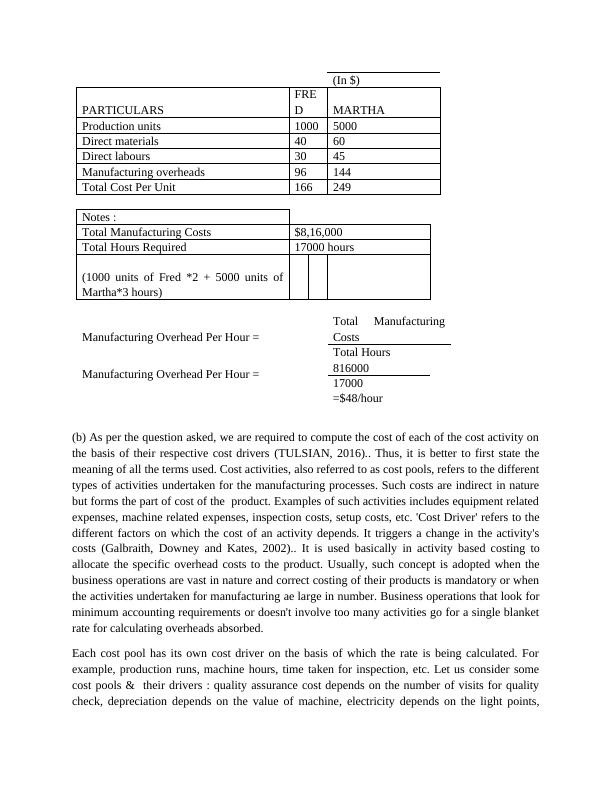

(a) It is important to have a brief description of manufacturing overheads first. Also known asproduction cost, factory overhead & factory burden, manufacturing overheads are incurred in afactory’s manufacturing processes. The cost incurred in the factory for the production purposeother than direct Labour and direct materials cost is termed as manufacturing overhead cost.This is why, it is often referred to as an indirect cost. According to accounting principles,valuation of inventory & cost of goods sold should be made on the basis of direct material cost,direct Labour cost and manufacturing overheads (Berman, Knight and Case, n.d.) . However, it isto be stated that the expenses occurring outside the factory in relation to the said product such asselling & administrative costs, general expenses, etc doesn't form a part of product cost and arenot inventorial. Such expenses are charged in the income statement in the respective accountingyear in which it occurred. Examples of such costs are depreciation on the factory equipment,plant related expenses, inspection costs, etc (Shim and Siegel, 2008). Because manufacturing overheads are considered to be an indirect cost, accountants face the taskof assigning or allocating overheads cost to each of the product units if there are more than oneproduct. There can establish no direct relationship (Bruner, Eades and Schill, 2017). Forexample, the depreciation of the machine is based on the value of the machine and not the unitsactually manufactured (Saltelli, Chan and Scott, 2008). Thus, there are numerous methods of allocating overheads and businesses adopt the methodbased on their operations & the market forces. Two most common approaches are conventionalor traditional costing and activity - based costing (Taylor, 2008).. Coming to conventional approach, it refers to the allocation of manufacturing overheads toproducts on the basis of volume metric such as direct labour hours or production machine hoursor certain percentage of prime costs etc (Clarke and Clarke, 1990).. With a decrease in labourhours or machine hours, the overhead cost increases. As per this approach, accountants deriveone cost for all the activities of the manufacturing excluding direct labour costs and materialscosts and multiples such unit cost with the respective cost driver be it direct labour hours ormachine hours. Such overhead rate is also referred to as 'overhead absorption rate' or 'singleblanket rate' (Fairhurst, 2015). As per the given question, we are required to compute the cost of product unit of Fred andMartha on the basis of single overhead rate (Galbraith, Downey and Kates, 2002).. The singleoverhead rate is calculated by dividing budgeted costs by total hours required as shown in thenotes. The overhead rate comes out as $48/product unit and also, manufacturing overhead costsare to be valued on the basis of direct labour hours (Saunders and Cornett, 2017). So one unit ofFred costs $96 ($48*2 hours for one unit) and one unit of Martha costs $144 ($48*3 hours forone unit). CACLCULATION OF COST PER UNIT USING CONVENTIONALAPPROACH :

(In $)PARTICULARSFREDMARTHAProduction units10005000Direct materials4060Direct labours3045Manufacturing overheads96144Total Cost Per Unit166249Notes :Total Manufacturing Costs$8,16,000 Total Hours Required17000 hours(1000 units of Fred *2 + 5000 units ofMartha*3 hours)Manufacturing Overhead Per Hour =Total ManufacturingCostsTotal HoursManufacturing Overhead Per Hour =81600017000=$48/hour(b) As per the question asked, we are required to compute the cost of each of the cost activity onthe basis of their respective cost drivers (TULSIAN, 2016).. Thus, it is better to first state themeaning of all the terms used. Cost activities, also referred to as cost pools, refers to the differenttypes of activities undertaken for the manufacturing processes. Such costs are indirect in naturebut forms the part of cost of the product. Examples of such activities includes equipment relatedexpenses, machine related expenses, inspection costs, setup costs, etc. 'Cost Driver' refers to thedifferent factors on which the cost of an activity depends. It triggers a change in the activity'scosts (Galbraith, Downey and Kates, 2002).. It is used basically in activity based costing toallocate the specific overhead costs to the product. Usually, such concept is adopted when thebusiness operations are vast in nature and correct costing of their products is mandatory or whenthe activities undertaken for manufacturing ae large in number. Business operations that look forminimum accounting requirements or doesn't involve too many activities go for a single blanketrate for calculating overheads absorbed. Each cost pool has its own cost driver on the basis of which the rate is being calculated. Forexample, production runs, machine hours, time taken for inspection, etc. Let us consider somecost pools & their drivers : quality assurance cost depends on the number of visits for qualitycheck, depreciation depends on the value of machine, electricity depends on the light points,

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

The Manufacturing Overheadlg...

|9

|2796

|35

ACC200 : Introduction to Managerial Accountinglg...

|5

|1479

|439

ACC 200 : Introduction to Management Accounting | KOI universitylg...

|7

|1440

|265

ACC200 Managerial Accounting Assignment | Calculation of ...lg...

|4

|930

|73

T217 Acc200 management accountinglg...

|12

|2308

|142

ACC200 : Introduction to Management Accounting | Assignmentlg...

|5

|1066

|326