Management Accounting Report: Cost Analysis and Systems

VerifiedAdded on 2023/01/18

|22

|5191

|99

Report

AI Summary

This management accounting report delves into the significance of management accounting in contemporary business environments, emphasizing its role in decision-making and wealth creation. It examines the management accounting systems employed by Alpha Ltd, a medium-sized manufacturing company, including cost accounting, price optimization, inventory management, and job costing systems. The report analyzes various management accounting reports, such as cost reports, stock reports, and accounts receivable reports, and their benefits. It also explores the integration of these systems and reports with organizational processes. Furthermore, the report presents a numerical sum to assess costs through techniques like CVP analysis, absorption costing, and marginal costing, along with income statements. It discusses budgetary control methods and their planning tools, followed by a comparison of how organizations adapt management accounting systems to address financial challenges, offering valuable insights for business development and financial problem-solving.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................4

LO 1.................................................................................................................................................4

P1. Management accounting and different types of systems.......................................................4

M1. Benefit of MAS....................................................................................................................6

D1. Integration of MAS and MA reports with organisational process........................................7

LO 2.................................................................................................................................................7

P3. Numerical sum to assess costs through techniques/methods of cost analysis for preparing

income statement:........................................................................................................................7

M2. Application of MA techniques and preparation of financial reporting reports:.................15

D2. Interpretation:......................................................................................................................15

LO 3...............................................................................................................................................16

P4.Advantages and downsides of many forms of budgetary control's planning tools:.............16

M3 Use of planning tools to estimate financial plans................................................................18

D3 Planning to solve monetary issues.......................................................................................18

LO 4...............................................................................................................................................18

P5. Compare how organisations are adapting management accounting systems to responds to

financial problems.....................................................................................................................18

M4 MAS to solve the issues......................................................................................................20

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................22

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................4

LO 1.................................................................................................................................................4

P1. Management accounting and different types of systems.......................................................4

M1. Benefit of MAS....................................................................................................................6

D1. Integration of MAS and MA reports with organisational process........................................7

LO 2.................................................................................................................................................7

P3. Numerical sum to assess costs through techniques/methods of cost analysis for preparing

income statement:........................................................................................................................7

M2. Application of MA techniques and preparation of financial reporting reports:.................15

D2. Interpretation:......................................................................................................................15

LO 3...............................................................................................................................................16

P4.Advantages and downsides of many forms of budgetary control's planning tools:.............16

M3 Use of planning tools to estimate financial plans................................................................18

D3 Planning to solve monetary issues.......................................................................................18

LO 4...............................................................................................................................................18

P5. Compare how organisations are adapting management accounting systems to responds to

financial problems.....................................................................................................................18

M4 MAS to solve the issues......................................................................................................20

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................22

INTRODUCTION

In present time the business environment in the context of the management accounting

plays vital role due to companies take important decision that based on the profit maximization

as well as wealth creation (Gray III, 2015).Each company wants to track the performance

information that mainly depends on the cost based information and generate the historical

general ledger system that based on the financial accounting information. The management

accounting is the procedure of the determining of the business costs and operations to produce

the internal report, records and account that supports to business in decision making procedure

and effectively accomplish the goals and objectives. To better understand of the report selected

organisation Alpha Ltd which is medium sized manufacturing company. The company have only

50 employees and turn over about 50000 per annum. The company manufacturing of the local

made Pizzas and franchising the business. In this report consist of various kind of the

management accounting system as well as report that produce by the company to analysis overall

information. Along with analysis the different types of cost techniques that apply by the

organisation to sort out the numerical. Apart from the report, discuss several budget that produce

by the companies to determine the accurate situation and how to take well step and identify

different financial problem that sort out through management tool. For this implement

management accounting system and compare with other organisation to adopt strategy.

LO 1

P1. Management accounting and different types of systems.

Management accounting- Management accounting is the method for assessing the business and

economic costs of producing an internal report, documents and account that endorses business in

the judgment-making process and efficiently achieves the goals and targets.

Types of MAS:

Cost accounting system- It is an accounting system that is connected to the mechanism of

projecting forward-looking expenses of businesses in an effective way (Smith, 2015).The

function of this accounting is not restricted to prediction; this also helps to identify

variations in expenditure. For businesses, this accounting is necessary for proper

management of economic operations, so that the sum of spending can be reduced. Under

the corporation listed above, Alpha limited company this accounting system is

In present time the business environment in the context of the management accounting

plays vital role due to companies take important decision that based on the profit maximization

as well as wealth creation (Gray III, 2015).Each company wants to track the performance

information that mainly depends on the cost based information and generate the historical

general ledger system that based on the financial accounting information. The management

accounting is the procedure of the determining of the business costs and operations to produce

the internal report, records and account that supports to business in decision making procedure

and effectively accomplish the goals and objectives. To better understand of the report selected

organisation Alpha Ltd which is medium sized manufacturing company. The company have only

50 employees and turn over about 50000 per annum. The company manufacturing of the local

made Pizzas and franchising the business. In this report consist of various kind of the

management accounting system as well as report that produce by the company to analysis overall

information. Along with analysis the different types of cost techniques that apply by the

organisation to sort out the numerical. Apart from the report, discuss several budget that produce

by the companies to determine the accurate situation and how to take well step and identify

different financial problem that sort out through management tool. For this implement

management accounting system and compare with other organisation to adopt strategy.

LO 1

P1. Management accounting and different types of systems.

Management accounting- Management accounting is the method for assessing the business and

economic costs of producing an internal report, documents and account that endorses business in

the judgment-making process and efficiently achieves the goals and targets.

Types of MAS:

Cost accounting system- It is an accounting system that is connected to the mechanism of

projecting forward-looking expenses of businesses in an effective way (Smith, 2015).The

function of this accounting is not restricted to prediction; this also helps to identify

variations in expenditure. For businesses, this accounting is necessary for proper

management of economic operations, so that the sum of spending can be reduced. Under

the corporation listed above, Alpha limited company this accounting system is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

implemented with the intention of keeping the price of producing beer lighter from the

estimate.

Price optimisation system- In conjunction with the title, this accounting system is related

to the process of establishing prices for products and services on the basis of the

requirement and value of each commodity. This is feasible since, according to this,

information is collected on customer requirements and the value is established. As in the

above-mentioned company dimension, on the basis of this value, their sales department

uses key information on the demand for their product in different market sectors.

Inventory management system- This is a type of accounting system that is affiliated with

the system of keeping a close eye on those products that are bought and sold by firms

over a certain length of time. Under this accounting system, stock value is carried out in

compliance with different methods, such as the last in the first out method, the first in the

first out method and the weighted average cost method. All of these strategies play an

important role for businesses in monitoring the exact quantity of product at a time when it

is required. Such as in the aspect of above chosen business entity, their research

department uses information on processed raw materials for production purposes.

Job costing system- It can be defined as a form of accounting system which relates to the

method of calculating costs of each unit generated in an accurate way. The goal of this

accounting system is to reduce total labour costs in a better manner. The goal of this

accounting system is to reduce total labour costs in a better manner. Due to the small

product range, this management system is not ideal for small companies. It is ideal for

businesses with a larger product line. In the context of above company, this accounting

system is used to determine the value of each unit generated.

Various methods of MA reports:

The term MA reports can be described as those detailed notes that comprise of

information on monetary and non-monetary segments in a systematic way. Such reported data

are commonly used by the management department of businesses in order to take effective and

prompt response.

Cost report- This report is being planned through the implementation of the cost

accounting system. The report comprises of details on the costs incurred in carrying out a

estimate.

Price optimisation system- In conjunction with the title, this accounting system is related

to the process of establishing prices for products and services on the basis of the

requirement and value of each commodity. This is feasible since, according to this,

information is collected on customer requirements and the value is established. As in the

above-mentioned company dimension, on the basis of this value, their sales department

uses key information on the demand for their product in different market sectors.

Inventory management system- This is a type of accounting system that is affiliated with

the system of keeping a close eye on those products that are bought and sold by firms

over a certain length of time. Under this accounting system, stock value is carried out in

compliance with different methods, such as the last in the first out method, the first in the

first out method and the weighted average cost method. All of these strategies play an

important role for businesses in monitoring the exact quantity of product at a time when it

is required. Such as in the aspect of above chosen business entity, their research

department uses information on processed raw materials for production purposes.

Job costing system- It can be defined as a form of accounting system which relates to the

method of calculating costs of each unit generated in an accurate way. The goal of this

accounting system is to reduce total labour costs in a better manner. The goal of this

accounting system is to reduce total labour costs in a better manner. Due to the small

product range, this management system is not ideal for small companies. It is ideal for

businesses with a larger product line. In the context of above company, this accounting

system is used to determine the value of each unit generated.

Various methods of MA reports:

The term MA reports can be described as those detailed notes that comprise of

information on monetary and non-monetary segments in a systematic way. Such reported data

are commonly used by the management department of businesses in order to take effective and

prompt response.

Cost report- This report is being planned through the implementation of the cost

accounting system. The report comprises of details on the costs incurred in carrying out a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

critical range of business transactions and operations. In addition to this study, it

categorizes activities as per their rate of expenditure. The aim of generating this

document is to concentrate on those components and facets that consume increased costs.

In the context of above company, , their accounting department uses essential information

through such report, which helps them reduce the overall cost.

Stock report- It can be described as a type of report that comprises of information on the

measured quantities of the product stored in the store (Harrison and Lock, 2017). As with

the above-mentioned accounting report, this document is also primed by means of an

inventory control system. The primary objective of this document is to help the

manufacturing ministry to take appropriate action on how many units are required to be

generated. In the context of the above mentioned corporation, their production

department produces products in an expense-effective manner by consuming crucial

information via this document.

Accounts receivable report- This is a type of document that gives information on the

amount of borrowers who are responsible to entities along with the period of the payment

in an appropriate way. In the context of the above-mentioned corporation, their

accounting department uses key information by means of this document, which helps to

figure out ways to raise the debt from specific borrowers.

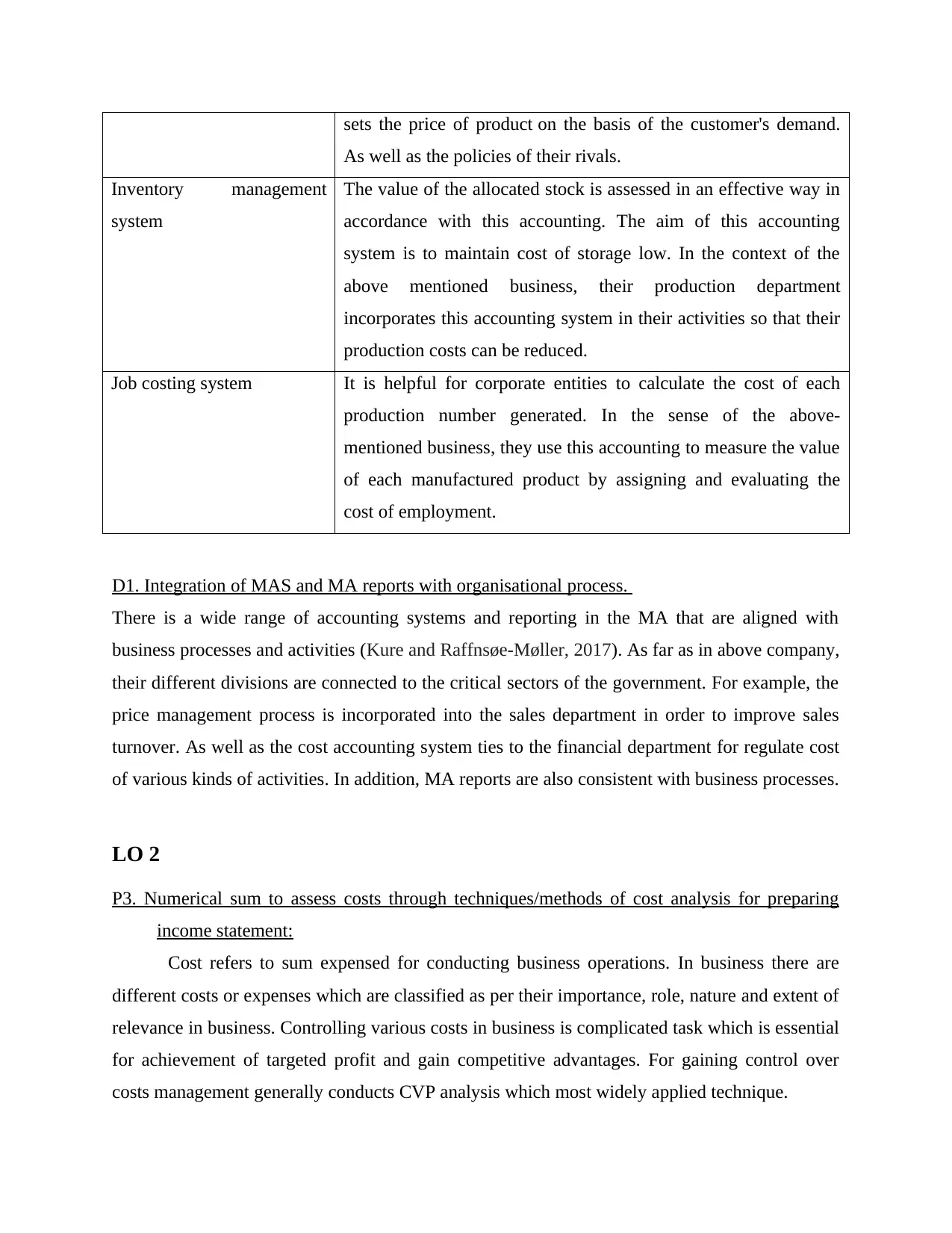

M1. Benefit of MAS

Name of MAS Benefit

Cost accounting system It is associated with the dimension of monitoring the overall costs

of various operations by measuring the reliability of the

fluctuations. In the sense of the above-mentioned business, they

use this accounting system for tracking the true costs of

production and control certain operations, the value of which is

beyond estimated.

Price optimisation system This is advantageous for businesses in order to set the price of

goods and services in line with the recent economic phenomenon.

In the context of the above mentioned company, their sales team

categorizes activities as per their rate of expenditure. The aim of generating this

document is to concentrate on those components and facets that consume increased costs.

In the context of above company, , their accounting department uses essential information

through such report, which helps them reduce the overall cost.

Stock report- It can be described as a type of report that comprises of information on the

measured quantities of the product stored in the store (Harrison and Lock, 2017). As with

the above-mentioned accounting report, this document is also primed by means of an

inventory control system. The primary objective of this document is to help the

manufacturing ministry to take appropriate action on how many units are required to be

generated. In the context of the above mentioned corporation, their production

department produces products in an expense-effective manner by consuming crucial

information via this document.

Accounts receivable report- This is a type of document that gives information on the

amount of borrowers who are responsible to entities along with the period of the payment

in an appropriate way. In the context of the above-mentioned corporation, their

accounting department uses key information by means of this document, which helps to

figure out ways to raise the debt from specific borrowers.

M1. Benefit of MAS

Name of MAS Benefit

Cost accounting system It is associated with the dimension of monitoring the overall costs

of various operations by measuring the reliability of the

fluctuations. In the sense of the above-mentioned business, they

use this accounting system for tracking the true costs of

production and control certain operations, the value of which is

beyond estimated.

Price optimisation system This is advantageous for businesses in order to set the price of

goods and services in line with the recent economic phenomenon.

In the context of the above mentioned company, their sales team

sets the price of product on the basis of the customer's demand.

As well as the policies of their rivals.

Inventory management

system

The value of the allocated stock is assessed in an effective way in

accordance with this accounting. The aim of this accounting

system is to maintain cost of storage low. In the context of the

above mentioned business, their production department

incorporates this accounting system in their activities so that their

production costs can be reduced.

Job costing system It is helpful for corporate entities to calculate the cost of each

production number generated. In the sense of the above-

mentioned business, they use this accounting to measure the value

of each manufactured product by assigning and evaluating the

cost of employment.

D1. Integration of MAS and MA reports with organisational process.

There is a wide range of accounting systems and reporting in the MA that are aligned with

business processes and activities (Kure and Raffnsøe-Møller, 2017). As far as in above company,

their different divisions are connected to the critical sectors of the government. For example, the

price management process is incorporated into the sales department in order to improve sales

turnover. As well as the cost accounting system ties to the financial department for regulate cost

of various kinds of activities. In addition, MA reports are also consistent with business processes.

LO 2

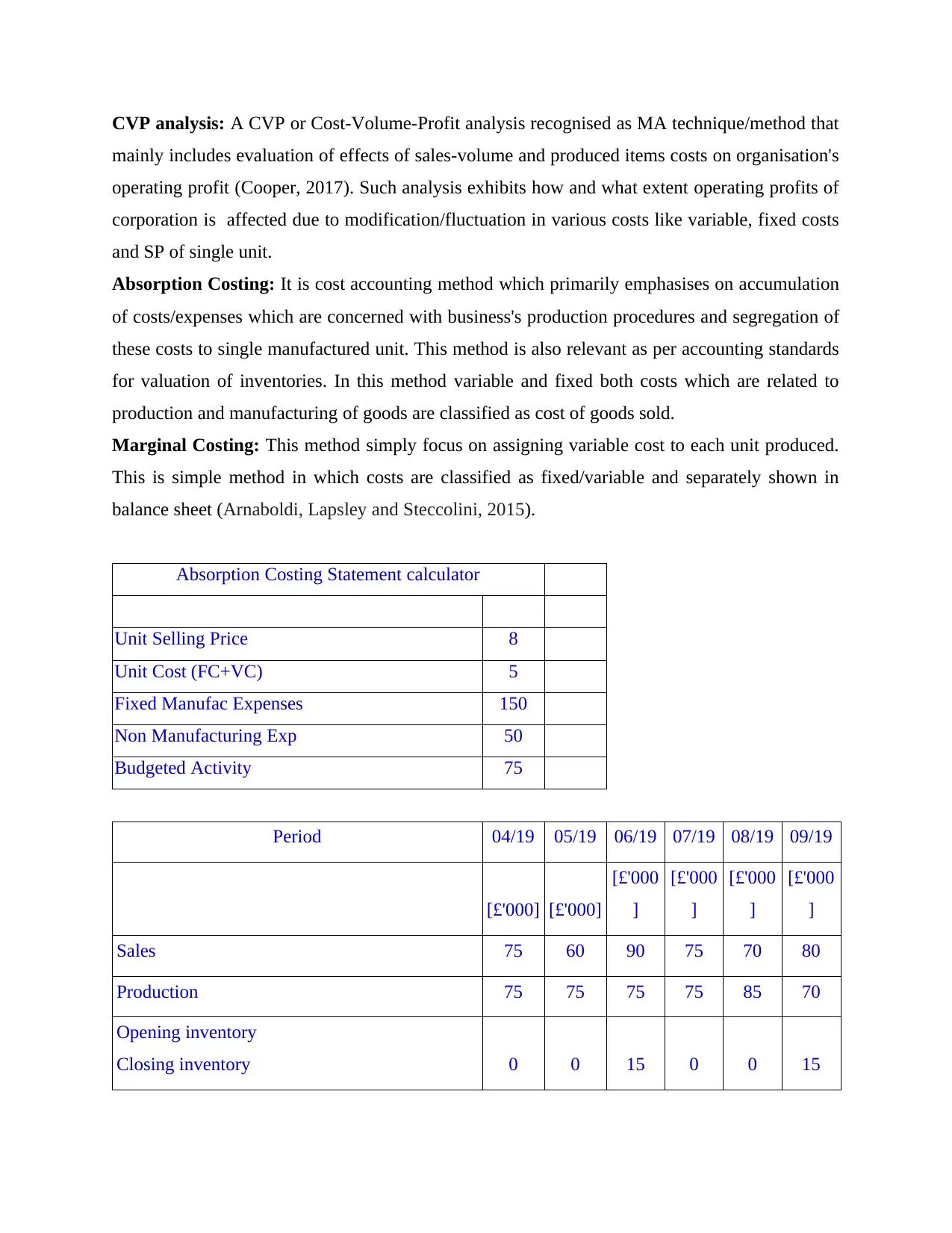

P3. Numerical sum to assess costs through techniques/methods of cost analysis for preparing

income statement:

Cost refers to sum expensed for conducting business operations. In business there are

different costs or expenses which are classified as per their importance, role, nature and extent of

relevance in business. Controlling various costs in business is complicated task which is essential

for achievement of targeted profit and gain competitive advantages. For gaining control over

costs management generally conducts CVP analysis which most widely applied technique.

As well as the policies of their rivals.

Inventory management

system

The value of the allocated stock is assessed in an effective way in

accordance with this accounting. The aim of this accounting

system is to maintain cost of storage low. In the context of the

above mentioned business, their production department

incorporates this accounting system in their activities so that their

production costs can be reduced.

Job costing system It is helpful for corporate entities to calculate the cost of each

production number generated. In the sense of the above-

mentioned business, they use this accounting to measure the value

of each manufactured product by assigning and evaluating the

cost of employment.

D1. Integration of MAS and MA reports with organisational process.

There is a wide range of accounting systems and reporting in the MA that are aligned with

business processes and activities (Kure and Raffnsøe-Møller, 2017). As far as in above company,

their different divisions are connected to the critical sectors of the government. For example, the

price management process is incorporated into the sales department in order to improve sales

turnover. As well as the cost accounting system ties to the financial department for regulate cost

of various kinds of activities. In addition, MA reports are also consistent with business processes.

LO 2

P3. Numerical sum to assess costs through techniques/methods of cost analysis for preparing

income statement:

Cost refers to sum expensed for conducting business operations. In business there are

different costs or expenses which are classified as per their importance, role, nature and extent of

relevance in business. Controlling various costs in business is complicated task which is essential

for achievement of targeted profit and gain competitive advantages. For gaining control over

costs management generally conducts CVP analysis which most widely applied technique.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CVP analysis: A CVP or Cost-Volume-Profit analysis recognised as MA technique/method that

mainly includes evaluation of effects of sales-volume and produced items costs on organisation's

operating profit (Cooper, 2017). Such analysis exhibits how and what extent operating profits of

corporation is affected due to modification/fluctuation in various costs like variable, fixed costs

and SP of single unit.

Absorption Costing: It is cost accounting method which primarily emphasises on accumulation

of costs/expenses which are concerned with business's production procedures and segregation of

these costs to single manufactured unit. This method is also relevant as per accounting standards

for valuation of inventories. In this method variable and fixed both costs which are related to

production and manufacturing of goods are classified as cost of goods sold.

Marginal Costing: This method simply focus on assigning variable cost to each unit produced.

This is simple method in which costs are classified as fixed/variable and separately shown in

balance sheet (Arnaboldi, Lapsley and Steccolini, 2015).

Absorption Costing Statement calculator

Unit Selling Price 8

Unit Cost (FC+VC) 5

Fixed Manufac Expenses 150

Non Manufacturing Exp 50

Budgeted Activity 75

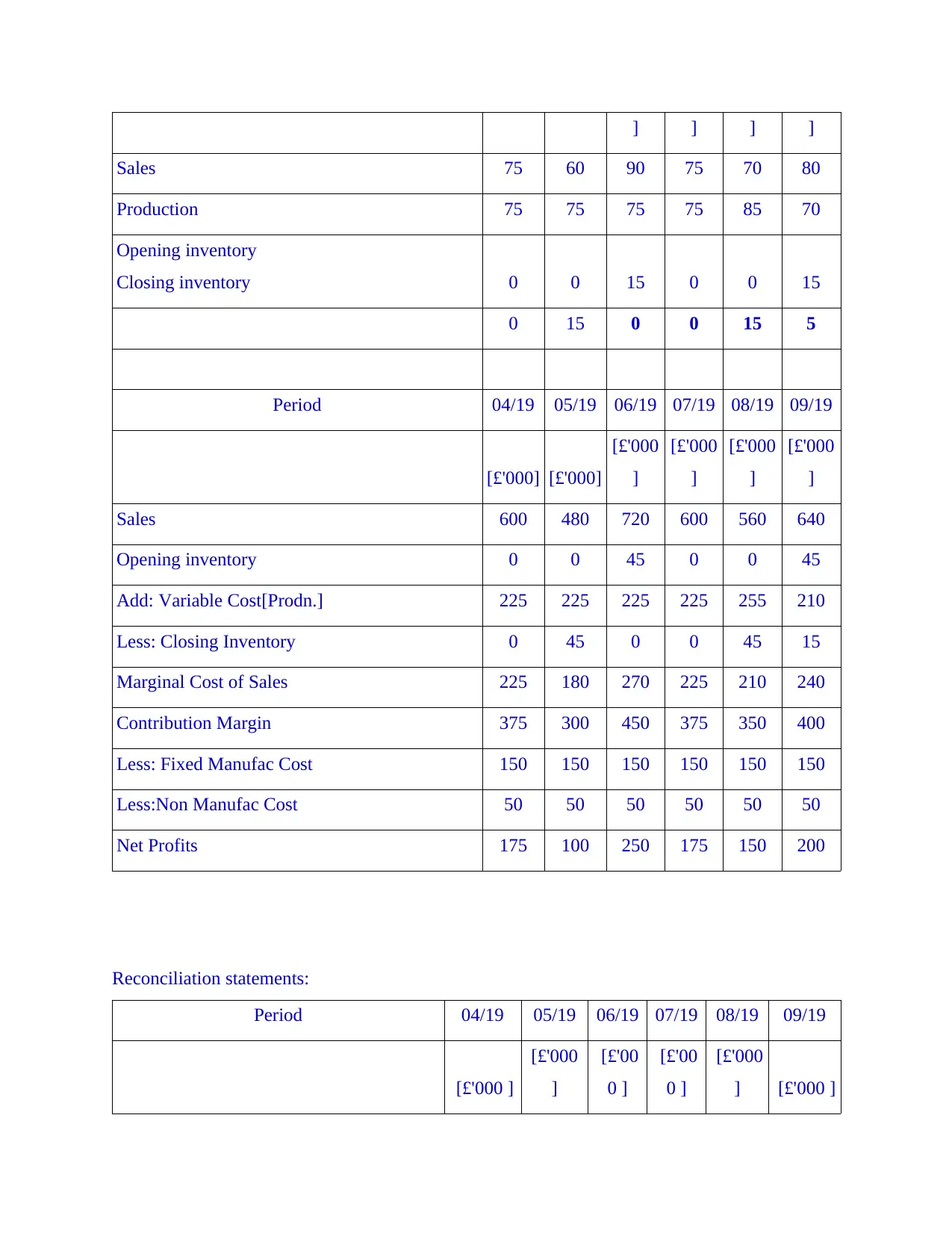

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

Opening inventory

Closing inventory 0 0 15 0 0 15

mainly includes evaluation of effects of sales-volume and produced items costs on organisation's

operating profit (Cooper, 2017). Such analysis exhibits how and what extent operating profits of

corporation is affected due to modification/fluctuation in various costs like variable, fixed costs

and SP of single unit.

Absorption Costing: It is cost accounting method which primarily emphasises on accumulation

of costs/expenses which are concerned with business's production procedures and segregation of

these costs to single manufactured unit. This method is also relevant as per accounting standards

for valuation of inventories. In this method variable and fixed both costs which are related to

production and manufacturing of goods are classified as cost of goods sold.

Marginal Costing: This method simply focus on assigning variable cost to each unit produced.

This is simple method in which costs are classified as fixed/variable and separately shown in

balance sheet (Arnaboldi, Lapsley and Steccolini, 2015).

Absorption Costing Statement calculator

Unit Selling Price 8

Unit Cost (FC+VC) 5

Fixed Manufac Expenses 150

Non Manufacturing Exp 50

Budgeted Activity 75

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

Opening inventory

Closing inventory 0 0 15 0 0 15

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0 15 0 0 15 5

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

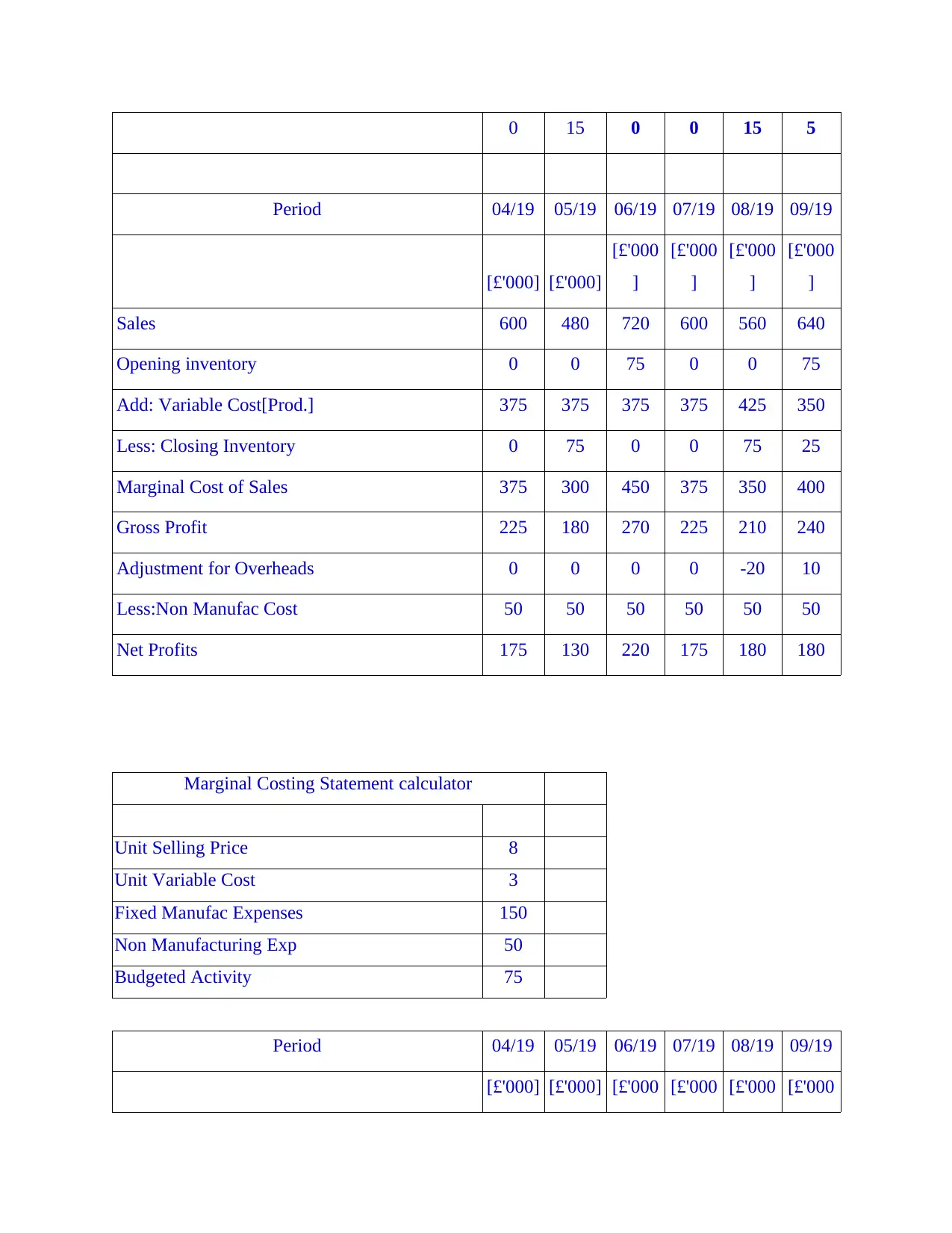

Sales 600 480 720 600 560 640

Opening inventory 0 0 75 0 0 75

Add: Variable Cost[Prod.] 375 375 375 375 425 350

Less: Closing Inventory 0 75 0 0 75 25

Marginal Cost of Sales 375 300 450 375 350 400

Gross Profit 225 180 270 225 210 240

Adjustment for Overheads 0 0 0 0 -20 10

Less:Non Manufac Cost 50 50 50 50 50 50

Net Profits 175 130 220 175 180 180

Marginal Costing Statement calculator

Unit Selling Price 8

Unit Variable Cost 3

Fixed Manufac Expenses 150

Non Manufacturing Exp 50

Budgeted Activity 75

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000] [£'000 [£'000 [£'000 [£'000

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 600 480 720 600 560 640

Opening inventory 0 0 75 0 0 75

Add: Variable Cost[Prod.] 375 375 375 375 425 350

Less: Closing Inventory 0 75 0 0 75 25

Marginal Cost of Sales 375 300 450 375 350 400

Gross Profit 225 180 270 225 210 240

Adjustment for Overheads 0 0 0 0 -20 10

Less:Non Manufac Cost 50 50 50 50 50 50

Net Profits 175 130 220 175 180 180

Marginal Costing Statement calculator

Unit Selling Price 8

Unit Variable Cost 3

Fixed Manufac Expenses 150

Non Manufacturing Exp 50

Budgeted Activity 75

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000] [£'000 [£'000 [£'000 [£'000

] ] ] ]

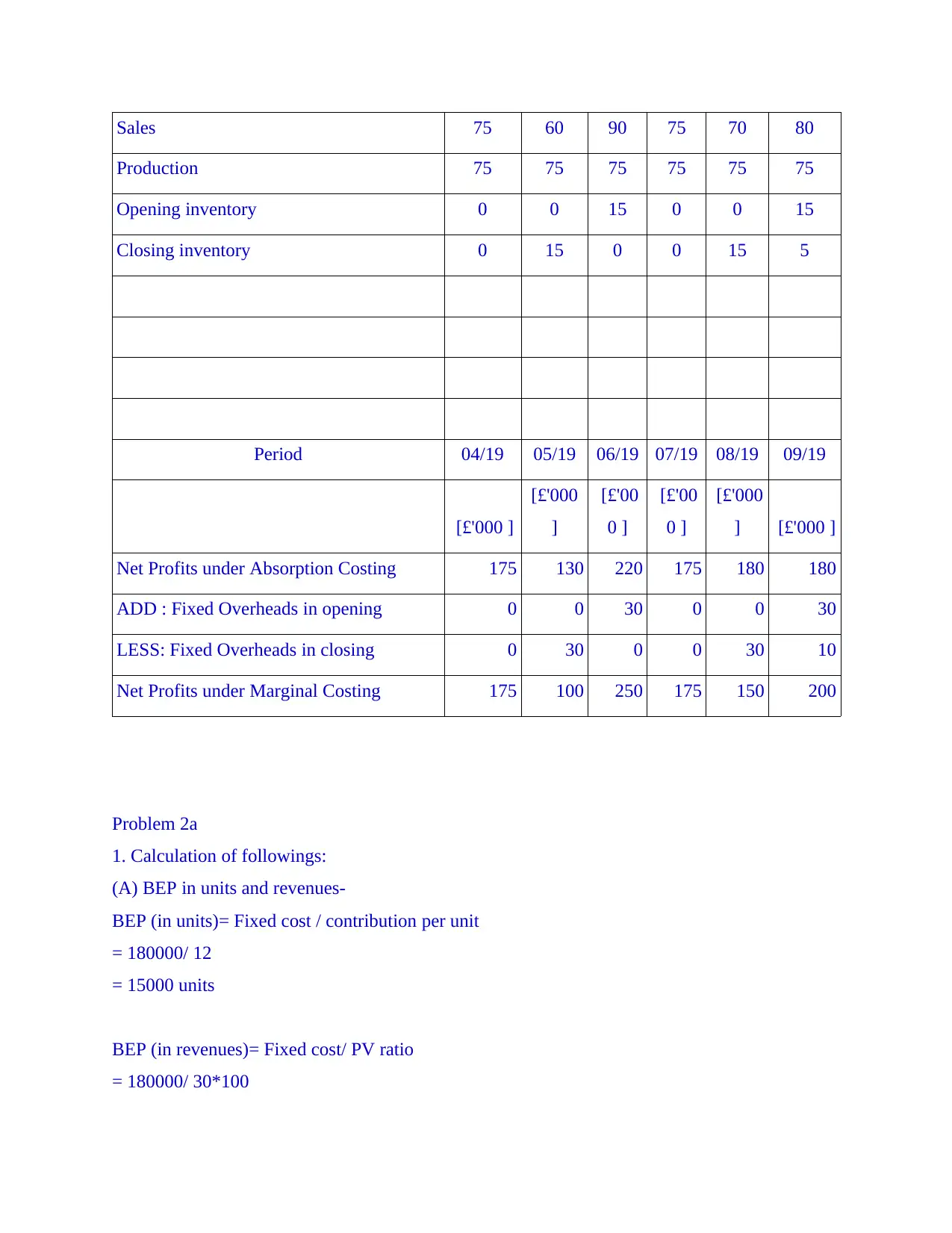

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

Opening inventory

Closing inventory 0 0 15 0 0 15

0 15 0 0 15 5

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 600 480 720 600 560 640

Opening inventory 0 0 45 0 0 45

Add: Variable Cost[Prodn.] 225 225 225 225 255 210

Less: Closing Inventory 0 45 0 0 45 15

Marginal Cost of Sales 225 180 270 225 210 240

Contribution Margin 375 300 450 375 350 400

Less: Fixed Manufac Cost 150 150 150 150 150 150

Less:Non Manufac Cost 50 50 50 50 50 50

Net Profits 175 100 250 175 150 200

Reconciliation statements:

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000 ]

[£'000

]

[£'00

0 ]

[£'00

0 ]

[£'000

] [£'000 ]

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

Opening inventory

Closing inventory 0 0 15 0 0 15

0 15 0 0 15 5

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000] [£'000]

[£'000

]

[£'000

]

[£'000

]

[£'000

]

Sales 600 480 720 600 560 640

Opening inventory 0 0 45 0 0 45

Add: Variable Cost[Prodn.] 225 225 225 225 255 210

Less: Closing Inventory 0 45 0 0 45 15

Marginal Cost of Sales 225 180 270 225 210 240

Contribution Margin 375 300 450 375 350 400

Less: Fixed Manufac Cost 150 150 150 150 150 150

Less:Non Manufac Cost 50 50 50 50 50 50

Net Profits 175 100 250 175 150 200

Reconciliation statements:

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000 ]

[£'000

]

[£'00

0 ]

[£'00

0 ]

[£'000

] [£'000 ]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sales 75 60 90 75 70 80

Production 75 75 75 75 75 75

Opening inventory 0 0 15 0 0 15

Closing inventory 0 15 0 0 15 5

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000 ]

[£'000

]

[£'00

0 ]

[£'00

0 ]

[£'000

] [£'000 ]

Net Profits under Absorption Costing 175 130 220 175 180 180

ADD : Fixed Overheads in opening 0 0 30 0 0 30

LESS: Fixed Overheads in closing 0 30 0 0 30 10

Net Profits under Marginal Costing 175 100 250 175 150 200

Problem 2a

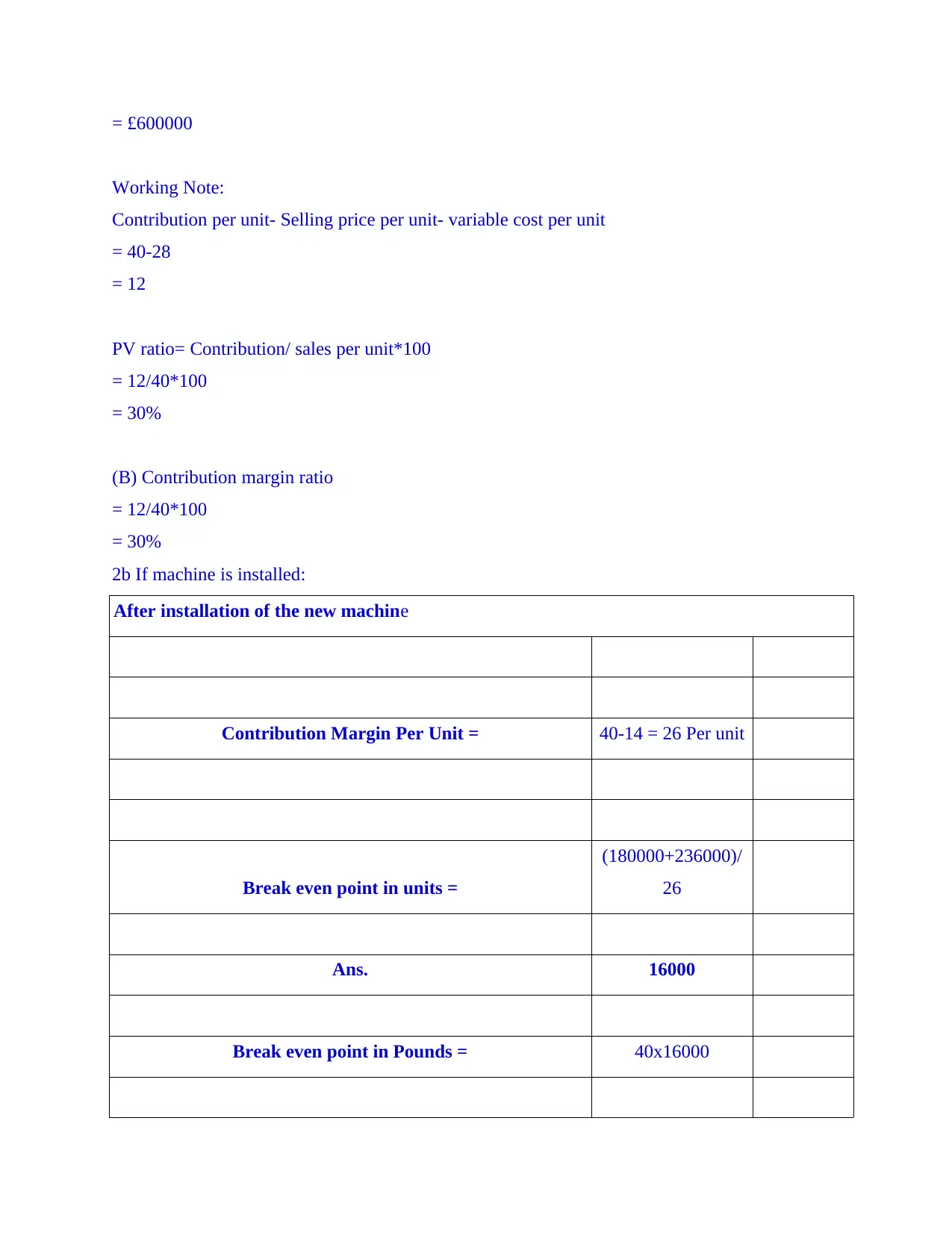

1. Calculation of followings:

(A) BEP in units and revenues-

BEP (in units)= Fixed cost / contribution per unit

= 180000/ 12

= 15000 units

BEP (in revenues)= Fixed cost/ PV ratio

= 180000/ 30*100

Production 75 75 75 75 75 75

Opening inventory 0 0 15 0 0 15

Closing inventory 0 15 0 0 15 5

Period 04/19 05/19 06/19 07/19 08/19 09/19

[£'000 ]

[£'000

]

[£'00

0 ]

[£'00

0 ]

[£'000

] [£'000 ]

Net Profits under Absorption Costing 175 130 220 175 180 180

ADD : Fixed Overheads in opening 0 0 30 0 0 30

LESS: Fixed Overheads in closing 0 30 0 0 30 10

Net Profits under Marginal Costing 175 100 250 175 150 200

Problem 2a

1. Calculation of followings:

(A) BEP in units and revenues-

BEP (in units)= Fixed cost / contribution per unit

= 180000/ 12

= 15000 units

BEP (in revenues)= Fixed cost/ PV ratio

= 180000/ 30*100

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= £600000

Working Note:

Contribution per unit- Selling price per unit- variable cost per unit

= 40-28

= 12

PV ratio= Contribution/ sales per unit*100

= 12/40*100

= 30%

(B) Contribution margin ratio

= 12/40*100

= 30%

2b If machine is installed:

After installation of the new machine

Contribution Margin Per Unit = 40-14 = 26 Per unit

Break even point in units =

(180000+236000)/

26

Ans. 16000

Break even point in Pounds = 40x16000

Working Note:

Contribution per unit- Selling price per unit- variable cost per unit

= 40-28

= 12

PV ratio= Contribution/ sales per unit*100

= 12/40*100

= 30%

(B) Contribution margin ratio

= 12/40*100

= 30%

2b If machine is installed:

After installation of the new machine

Contribution Margin Per Unit = 40-14 = 26 Per unit

Break even point in units =

(180000+236000)/

26

Ans. 16000

Break even point in Pounds = 40x16000

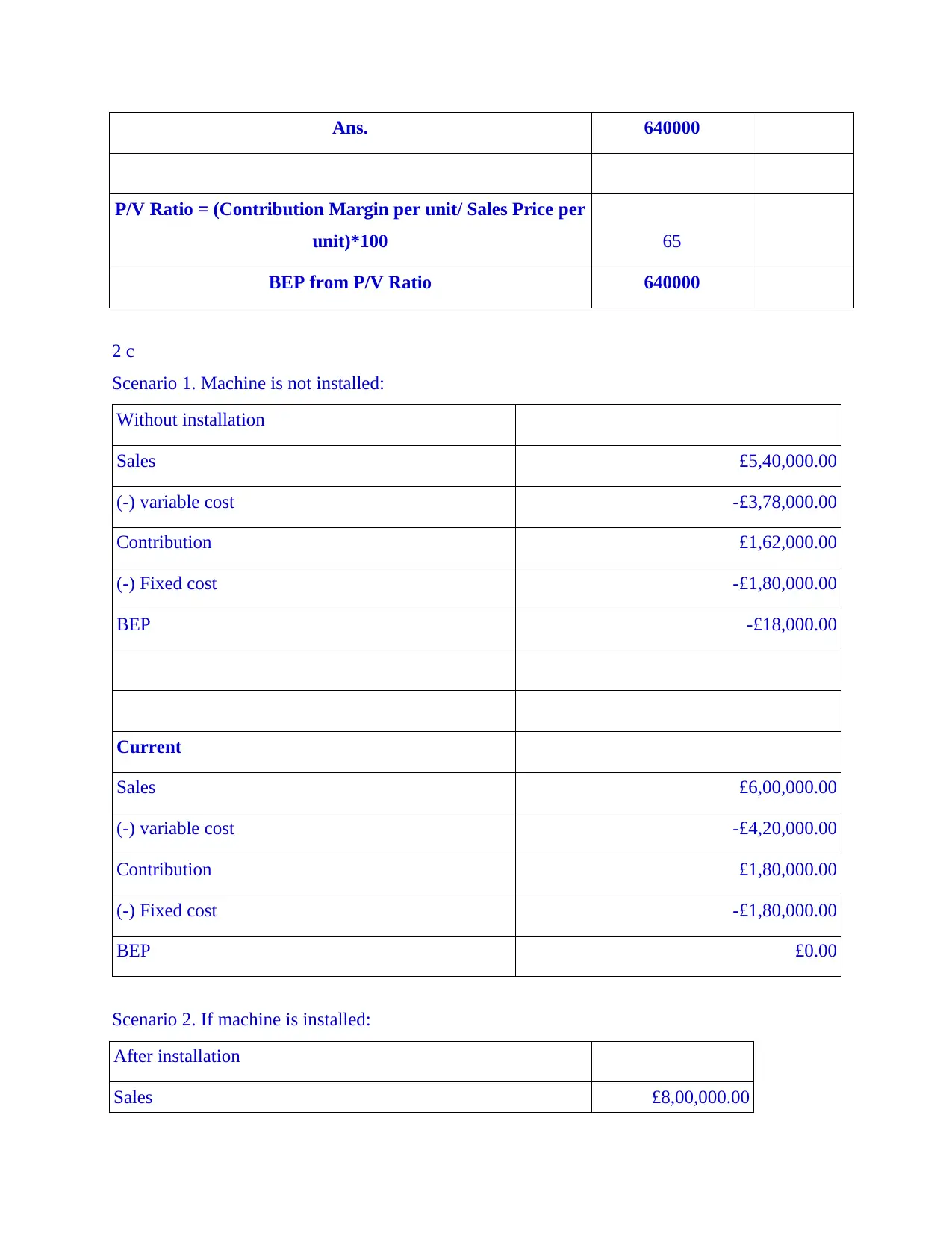

Ans. 640000

P/V Ratio = (Contribution Margin per unit/ Sales Price per

unit)*100 65

BEP from P/V Ratio 640000

2 c

Scenario 1. Machine is not installed:

Without installation

Sales £5,40,000.00

(-) variable cost -£3,78,000.00

Contribution £1,62,000.00

(-) Fixed cost -£1,80,000.00

BEP -£18,000.00

Current

Sales £6,00,000.00

(-) variable cost -£4,20,000.00

Contribution £1,80,000.00

(-) Fixed cost -£1,80,000.00

BEP £0.00

Scenario 2. If machine is installed:

After installation

Sales £8,00,000.00

P/V Ratio = (Contribution Margin per unit/ Sales Price per

unit)*100 65

BEP from P/V Ratio 640000

2 c

Scenario 1. Machine is not installed:

Without installation

Sales £5,40,000.00

(-) variable cost -£3,78,000.00

Contribution £1,62,000.00

(-) Fixed cost -£1,80,000.00

BEP -£18,000.00

Current

Sales £6,00,000.00

(-) variable cost -£4,20,000.00

Contribution £1,80,000.00

(-) Fixed cost -£1,80,000.00

BEP £0.00

Scenario 2. If machine is installed:

After installation

Sales £8,00,000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.