Management Accounting Research Trends

VerifiedAdded on 2020/02/03

|17

|5572

|30

Literature Review

AI Summary

This assignment delves into the current landscape of management accounting research. It analyzes a collection of academic papers spanning various aspects of management accounting, including its role in sustainability, technology adoption, cost control, and organizational control. The review identifies emerging trends, methodologies, and areas requiring further investigation within this field.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

a) Functions of management accounting ....................................................................................3

b) Types of management accounting system..............................................................................5

TASK 2............................................................................................................................................7

Calculating net profit through adoption of marginal as well as absorption costing tools...........7

TASK 3............................................................................................................................................9

(a) Different types of budget and their advantages and disadvantages.......................................9

(b) Process for preparing budget ..............................................................................................10

(c) Pricing strategies..................................................................................................................11

TASK 4..........................................................................................................................................13

a) Balance score card approach.................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

a) Functions of management accounting ....................................................................................3

b) Types of management accounting system..............................................................................5

TASK 2............................................................................................................................................7

Calculating net profit through adoption of marginal as well as absorption costing tools...........7

TASK 3............................................................................................................................................9

(a) Different types of budget and their advantages and disadvantages.......................................9

(b) Process for preparing budget ..............................................................................................10

(c) Pricing strategies..................................................................................................................11

TASK 4..........................................................................................................................................13

a) Balance score card approach.................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

It is significant for every firm to recording the transactions that are taking place on daily

basis. Therefore in this regard firm needs to carry out concept of management accounting and

offer financial information to several stakeholders (Otley and Emmanuel, 2013). The

organization makes appointment of accountant for recording the financial transactions in order to

record the information within time. However this proves to be effective and leads to directing as

well as controlling the business actions. In the present study management accounting has been

discussed in context of Imda Tech (UK). The report makes analysis of the income statement that

is devised based upon the marginal as well as absorption costing tool.

TASK 1

a) Functions of management accounting

i) Definition of management accounting and distinguish management and financial

accounting

Management accounting is the concept that helps in recording all the financial

information upon which management of firm aims to take crucial decision. Here, top

management analyses, measures and interpret the information related to finance in regard to

obtain significant data (Fullerton, Kennedy and Widener, 2013). Here, manager of Imda Tech

Limited maintain proper management accounting in regard to record daily transactions occurred

within business. Therefore, its main purpose is to prepare accounts and thus identify the areas

where firm is lacking so that crucial decisions could be taken in terms of improving the

performance of firm in market. With the help of management accounting it aids business to look

forwards and attain future goals. Also, it is considered as the crucial part within firm and finance

manager requires to carry out deep study so that they could identify the loopholes and make

appropriate decision in relation to enhance financial performance of firm in market. Imda faces

tough competition in market therefore firm aims to prepare good budget and thus make financial

decisions in relation to attain desired success (Bhimani and et. al., 2013). Management

accounting involves income and cost incurred within business in an accounting year. It also helps

in increasing the sales volume and income of Imda and make proper financial decision in terms

of achieving success. Managers of cited firm requires to allocate resources using Zero based

Budgeting and thus make assumptions regarding set targets could be attained. Below described is

the difference between financial and management accounting which are as follows-

It is significant for every firm to recording the transactions that are taking place on daily

basis. Therefore in this regard firm needs to carry out concept of management accounting and

offer financial information to several stakeholders (Otley and Emmanuel, 2013). The

organization makes appointment of accountant for recording the financial transactions in order to

record the information within time. However this proves to be effective and leads to directing as

well as controlling the business actions. In the present study management accounting has been

discussed in context of Imda Tech (UK). The report makes analysis of the income statement that

is devised based upon the marginal as well as absorption costing tool.

TASK 1

a) Functions of management accounting

i) Definition of management accounting and distinguish management and financial

accounting

Management accounting is the concept that helps in recording all the financial

information upon which management of firm aims to take crucial decision. Here, top

management analyses, measures and interpret the information related to finance in regard to

obtain significant data (Fullerton, Kennedy and Widener, 2013). Here, manager of Imda Tech

Limited maintain proper management accounting in regard to record daily transactions occurred

within business. Therefore, its main purpose is to prepare accounts and thus identify the areas

where firm is lacking so that crucial decisions could be taken in terms of improving the

performance of firm in market. With the help of management accounting it aids business to look

forwards and attain future goals. Also, it is considered as the crucial part within firm and finance

manager requires to carry out deep study so that they could identify the loopholes and make

appropriate decision in relation to enhance financial performance of firm in market. Imda faces

tough competition in market therefore firm aims to prepare good budget and thus make financial

decisions in relation to attain desired success (Bhimani and et. al., 2013). Management

accounting involves income and cost incurred within business in an accounting year. It also helps

in increasing the sales volume and income of Imda and make proper financial decision in terms

of achieving success. Managers of cited firm requires to allocate resources using Zero based

Budgeting and thus make assumptions regarding set targets could be attained. Below described is

the difference between financial and management accounting which are as follows-

Financial Accounting Management Accounting

Financial accounting is prepared in terms of

recording the transactions and tracks the

previous performance of firm. Through

preparing the financial account, manager of

Imda requires to use proper accounting

standards and guidelines so that transactions

could be recorded appropriately (Chan, Wang

and Raffoni, 2014).

On the other hand, management accounting

helps in recording the information related to

business and help managers to take crucial

decision in terms of carrying out effective

functioning (Dobroszek and Szychta, 2015).

Financial accounting requires to record all the

type of information i.e. financial or non

financial.

Further, accountants records only financial

information within management accounting.

It possesses the main objective of preparing

financial reports and thus it could be used by

external stakeholders and make crucial

investment decisions (Schaltegger, Gibassier and

Zvezdov, 2013).

While, preparing management accounting helps

business to provide accounting related

information to internal stakeholders such as

employees so that they make crucial decision

(Cleary, 2015).

Financial accounting is being prepared through

using historic data obtained in past.

Management accounting helps in recording the

data which is useful for firm to be used in

future and make the decisions accordingly

(Fayard and et. al., 2014).

Accountants recording financial information

needs to undertake effective accounting

standards (Gibassier, 2017).

On the other hand, management accounting

undertakes management information system

which helps them to execute the information

and attain success.

With the help of financial accounting it assists

in generating the reports that are related to

prepare appropriate financial reports.

While, in order to prepare management

accounting it aids in recording accurate and

reliable information so that performance could

be improved of Imda (Klychova, Faskhutdinova

and Sadrieva, 2014).

Financial accounting helps in preparing annual Management report aims to generate monthly

Financial accounting is prepared in terms of

recording the transactions and tracks the

previous performance of firm. Through

preparing the financial account, manager of

Imda requires to use proper accounting

standards and guidelines so that transactions

could be recorded appropriately (Chan, Wang

and Raffoni, 2014).

On the other hand, management accounting

helps in recording the information related to

business and help managers to take crucial

decision in terms of carrying out effective

functioning (Dobroszek and Szychta, 2015).

Financial accounting requires to record all the

type of information i.e. financial or non

financial.

Further, accountants records only financial

information within management accounting.

It possesses the main objective of preparing

financial reports and thus it could be used by

external stakeholders and make crucial

investment decisions (Schaltegger, Gibassier and

Zvezdov, 2013).

While, preparing management accounting helps

business to provide accounting related

information to internal stakeholders such as

employees so that they make crucial decision

(Cleary, 2015).

Financial accounting is being prepared through

using historic data obtained in past.

Management accounting helps in recording the

data which is useful for firm to be used in

future and make the decisions accordingly

(Fayard and et. al., 2014).

Accountants recording financial information

needs to undertake effective accounting

standards (Gibassier, 2017).

On the other hand, management accounting

undertakes management information system

which helps them to execute the information

and attain success.

With the help of financial accounting it assists

in generating the reports that are related to

prepare appropriate financial reports.

While, in order to prepare management

accounting it aids in recording accurate and

reliable information so that performance could

be improved of Imda (Klychova, Faskhutdinova

and Sadrieva, 2014).

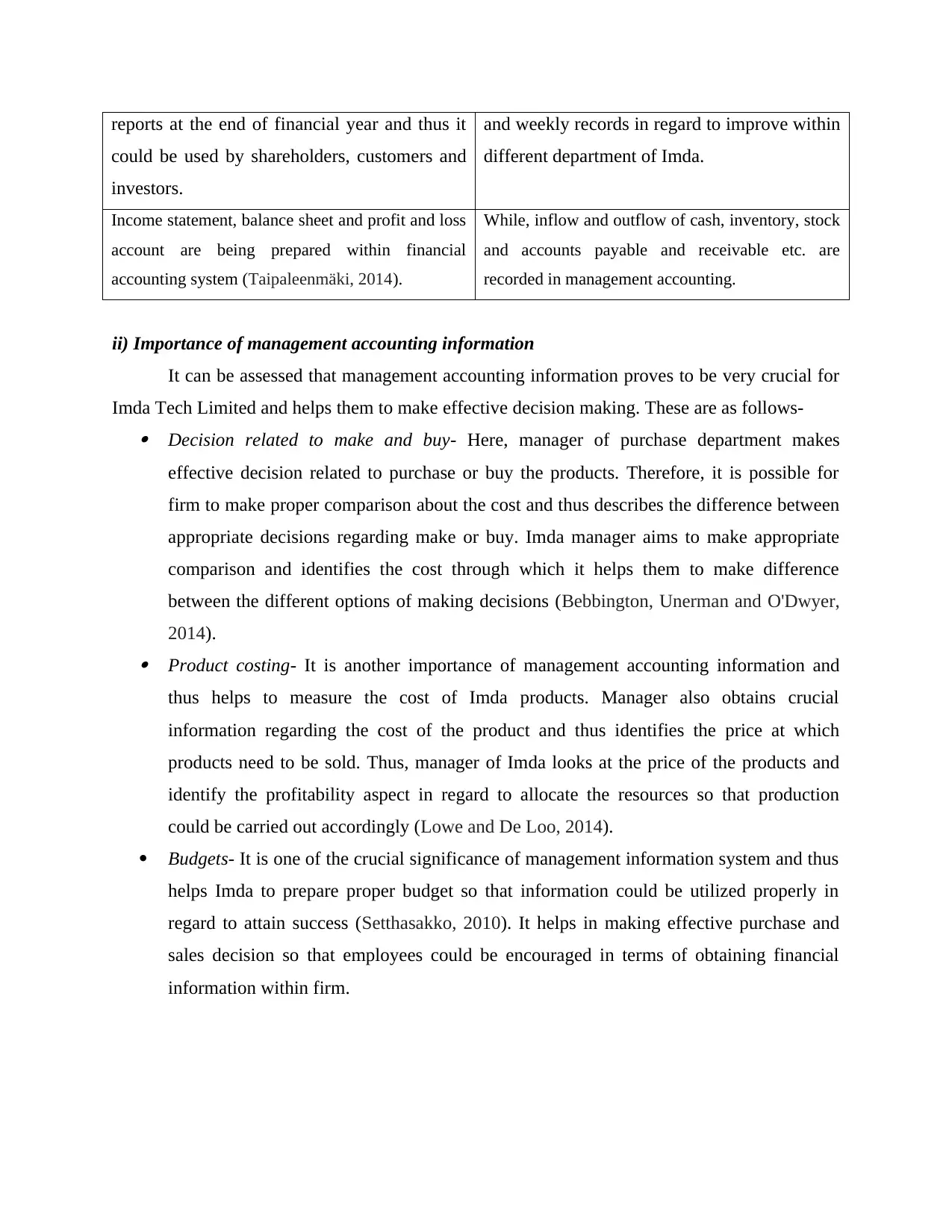

Financial accounting helps in preparing annual Management report aims to generate monthly

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

reports at the end of financial year and thus it

could be used by shareholders, customers and

investors.

and weekly records in regard to improve within

different department of Imda.

Income statement, balance sheet and profit and loss

account are being prepared within financial

accounting system (Taipaleenmäki, 2014).

While, inflow and outflow of cash, inventory, stock

and accounts payable and receivable etc. are

recorded in management accounting.

ii) Importance of management accounting information

It can be assessed that management accounting information proves to be very crucial for

Imda Tech Limited and helps them to make effective decision making. These are as follows- Decision related to make and buy- Here, manager of purchase department makes

effective decision related to purchase or buy the products. Therefore, it is possible for

firm to make proper comparison about the cost and thus describes the difference between

appropriate decisions regarding make or buy. Imda manager aims to make appropriate

comparison and identifies the cost through which it helps them to make difference

between the different options of making decisions (Bebbington, Unerman and O'Dwyer,

2014). Product costing- It is another importance of management accounting information and

thus helps to measure the cost of Imda products. Manager also obtains crucial

information regarding the cost of the product and thus identifies the price at which

products need to be sold. Thus, manager of Imda looks at the price of the products and

identify the profitability aspect in regard to allocate the resources so that production

could be carried out accordingly (Lowe and De Loo, 2014).

Budgets- It is one of the crucial significance of management information system and thus

helps Imda to prepare proper budget so that information could be utilized properly in

regard to attain success (Setthasakko, 2010). It helps in making effective purchase and

sales decision so that employees could be encouraged in terms of obtaining financial

information within firm.

could be used by shareholders, customers and

investors.

and weekly records in regard to improve within

different department of Imda.

Income statement, balance sheet and profit and loss

account are being prepared within financial

accounting system (Taipaleenmäki, 2014).

While, inflow and outflow of cash, inventory, stock

and accounts payable and receivable etc. are

recorded in management accounting.

ii) Importance of management accounting information

It can be assessed that management accounting information proves to be very crucial for

Imda Tech Limited and helps them to make effective decision making. These are as follows- Decision related to make and buy- Here, manager of purchase department makes

effective decision related to purchase or buy the products. Therefore, it is possible for

firm to make proper comparison about the cost and thus describes the difference between

appropriate decisions regarding make or buy. Imda manager aims to make appropriate

comparison and identifies the cost through which it helps them to make difference

between the different options of making decisions (Bebbington, Unerman and O'Dwyer,

2014). Product costing- It is another importance of management accounting information and

thus helps to measure the cost of Imda products. Manager also obtains crucial

information regarding the cost of the product and thus identifies the price at which

products need to be sold. Thus, manager of Imda looks at the price of the products and

identify the profitability aspect in regard to allocate the resources so that production

could be carried out accordingly (Lowe and De Loo, 2014).

Budgets- It is one of the crucial significance of management information system and thus

helps Imda to prepare proper budget so that information could be utilized properly in

regard to attain success (Setthasakko, 2010). It helps in making effective purchase and

sales decision so that employees could be encouraged in terms of obtaining financial

information within firm.

b) Types of management accounting system

Management accounting system helps in obtaining crucial information and thus helps

business to make crucial decisions. Thus, Imda Tech Limited uses such management accounting

system in regard to be used by other departments and improve their reports which are as follows-

i) Cost accounting system- Imda uses such management accounting system and thus

helps business to make proper estimation regarding cost of its products and value

inventory, profitability and controlling cost. Within manufacturing department helps

in estimating the cost of products in regard to identify the profit earned by firm.

Further, such method is also being used in regard to prepare financial statements and

thus cited organization estimate the closing inventory, work in progress and finished

stock (Otley and Emmanuel, 2013).

ii) Inventory management systems- Further, such management accounting system

helps in assessing the inventory management system and thus helps Imda to manage

the stock to satisfy the needs of customers. However, such information is crucial for

manager of business to identify the level of stock available and required so that needs

could be fulfilled (Fullerton, Kennedy and Widener, 2013). It is essential for

management accountant to record the daily transactions and thus maintain record of

inventory control and thus take orders from customers in regard to maintain the

inventory level and helps in minimizing the wastage of resources.

iii) Job costing systems- It is also one of the crucial management accounting system

helps in executing job costing method and thus proper procedure is being carried out

in regard to manufacture the Imda products in market. Also, such information is being

utilized by other departments in regard to track the cost of raw material and thus

execute the job operations effectively and efficiently. Within job costing it involves

three different types of information i.e. direct material, labor and overhead expenses.

However, all such information is being used by accountants in regard to track the

record of cost and revenue earned by firm (Bhimani and et. al., 2013).

iv) Price optimizing systems- It is another type of management accounting system and

thus helps Imda selling department to use such system in regard to identify the

responsiveness of clients and chard different prices charged by firm in regard to

analyze the prices of products produced by cited firm. It also helps firm to make

Management accounting system helps in obtaining crucial information and thus helps

business to make crucial decisions. Thus, Imda Tech Limited uses such management accounting

system in regard to be used by other departments and improve their reports which are as follows-

i) Cost accounting system- Imda uses such management accounting system and thus

helps business to make proper estimation regarding cost of its products and value

inventory, profitability and controlling cost. Within manufacturing department helps

in estimating the cost of products in regard to identify the profit earned by firm.

Further, such method is also being used in regard to prepare financial statements and

thus cited organization estimate the closing inventory, work in progress and finished

stock (Otley and Emmanuel, 2013).

ii) Inventory management systems- Further, such management accounting system

helps in assessing the inventory management system and thus helps Imda to manage

the stock to satisfy the needs of customers. However, such information is crucial for

manager of business to identify the level of stock available and required so that needs

could be fulfilled (Fullerton, Kennedy and Widener, 2013). It is essential for

management accountant to record the daily transactions and thus maintain record of

inventory control and thus take orders from customers in regard to maintain the

inventory level and helps in minimizing the wastage of resources.

iii) Job costing systems- It is also one of the crucial management accounting system

helps in executing job costing method and thus proper procedure is being carried out

in regard to manufacture the Imda products in market. Also, such information is being

utilized by other departments in regard to track the cost of raw material and thus

execute the job operations effectively and efficiently. Within job costing it involves

three different types of information i.e. direct material, labor and overhead expenses.

However, all such information is being used by accountants in regard to track the

record of cost and revenue earned by firm (Bhimani and et. al., 2013).

iv) Price optimizing systems- It is another type of management accounting system and

thus helps Imda selling department to use such system in regard to identify the

responsiveness of clients and chard different prices charged by firm in regard to

analyze the prices of products produced by cited firm. It also helps firm to make

analytics based prices which are reasonable for both business and consumers

(Dobroszek and Szychta, 2015). Moreover, it helps consumers to make them ready in

regard to pay the prices for the products and receive best quality goods.

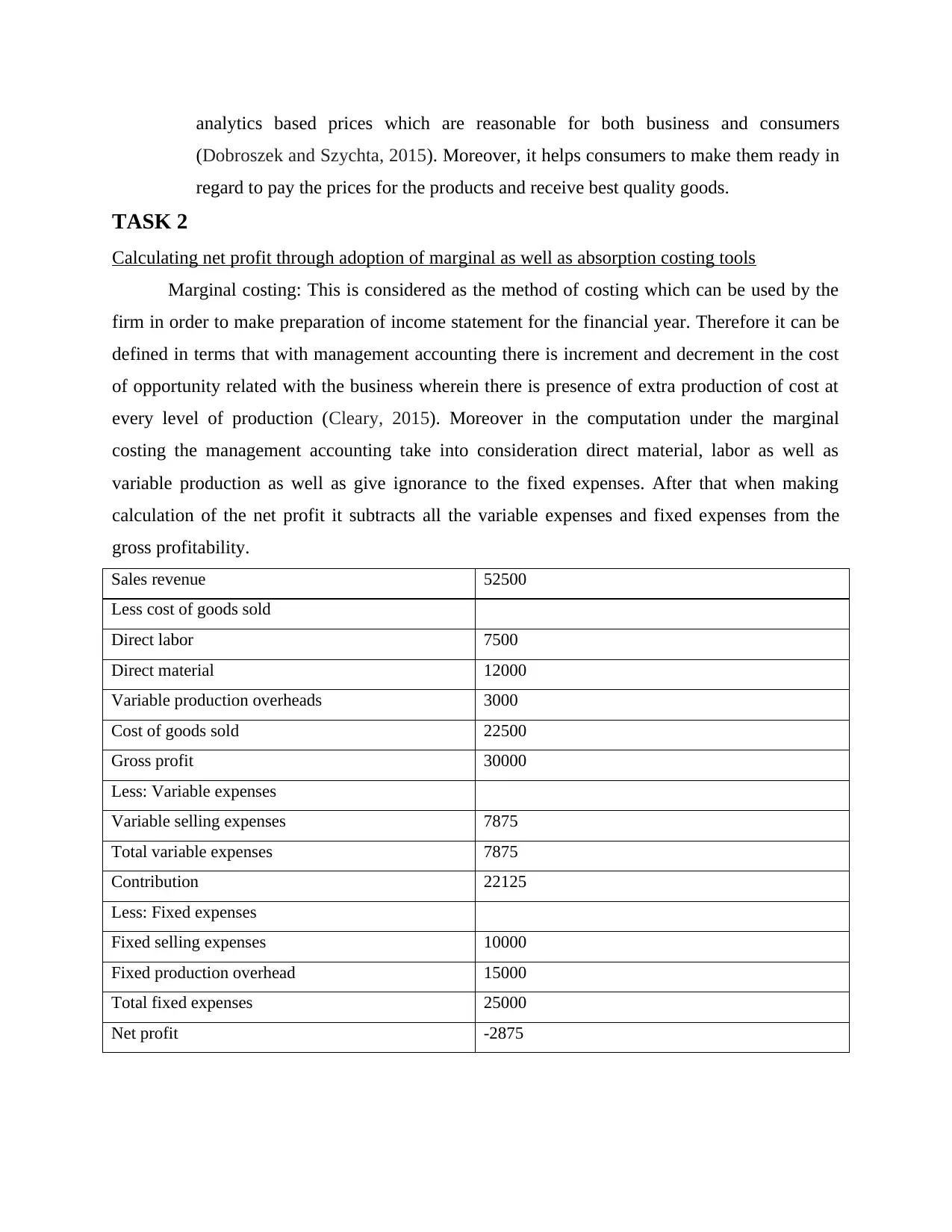

TASK 2

Calculating net profit through adoption of marginal as well as absorption costing tools

Marginal costing: This is considered as the method of costing which can be used by the

firm in order to make preparation of income statement for the financial year. Therefore it can be

defined in terms that with management accounting there is increment and decrement in the cost

of opportunity related with the business wherein there is presence of extra production of cost at

every level of production (Cleary, 2015). Moreover in the computation under the marginal

costing the management accounting take into consideration direct material, labor as well as

variable production as well as give ignorance to the fixed expenses. After that when making

calculation of the net profit it subtracts all the variable expenses and fixed expenses from the

gross profitability.

Sales revenue 52500

Less cost of goods sold

Direct labor 7500

Direct material 12000

Variable production overheads 3000

Cost of goods sold 22500

Gross profit 30000

Less: Variable expenses

Variable selling expenses 7875

Total variable expenses 7875

Contribution 22125

Less: Fixed expenses

Fixed selling expenses 10000

Fixed production overhead 15000

Total fixed expenses 25000

Net profit -2875

(Dobroszek and Szychta, 2015). Moreover, it helps consumers to make them ready in

regard to pay the prices for the products and receive best quality goods.

TASK 2

Calculating net profit through adoption of marginal as well as absorption costing tools

Marginal costing: This is considered as the method of costing which can be used by the

firm in order to make preparation of income statement for the financial year. Therefore it can be

defined in terms that with management accounting there is increment and decrement in the cost

of opportunity related with the business wherein there is presence of extra production of cost at

every level of production (Cleary, 2015). Moreover in the computation under the marginal

costing the management accounting take into consideration direct material, labor as well as

variable production as well as give ignorance to the fixed expenses. After that when making

calculation of the net profit it subtracts all the variable expenses and fixed expenses from the

gross profitability.

Sales revenue 52500

Less cost of goods sold

Direct labor 7500

Direct material 12000

Variable production overheads 3000

Cost of goods sold 22500

Gross profit 30000

Less: Variable expenses

Variable selling expenses 7875

Total variable expenses 7875

Contribution 22125

Less: Fixed expenses

Fixed selling expenses 10000

Fixed production overhead 15000

Total fixed expenses 25000

Net profit -2875

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Absorption costing: It is considered other kind of management costing tool which can be

utilized by the firm in which it takes all kind of expenditure that are fixed in nature. Therefore it

can be referred to as full costing at the time goods are sold wherein it takes direct material,

material labor, variable expenses as well as fixed production expenditure (Fayard and et. al.,

2014). Therefore in this absorption costing method subtracts the variable production as well as

fixed expenses from the cost of goods sold. With this calculation of the gross profit is being

done.

Sales revenue 52500

Less cost of goods sold

Direct labor 7500

Direct material 12000

Variable production overheads 3000

Fixed production overheads 15000

Cost of goods sold 37500

Gross profit 15000

Less: Variable expenses

Variable selling expenses 7875

Less: Fixed expenses

Fixed selling expenses 10000

Total expenditure 17875

Net profit -2875

Interpretation: From the table above the computation of the net profit is being carried out

by the means of marginal as well as absorption costing tools. Imda Tech Limited business makes

calculation of the net profit through use of marginal as well as absorption costing method. This

can be interpreted from the information above that in table 1 the calculation of the net profit is

being done. Such is being done through summing direct material that is 7500, direct labor 12000

as well as variable production overhead 3000 there is summation of 22500. After this calculation

of the gross profit is being done through deduction of the sales revenue 52500 from the cost of

goods sold 22500 wherein the gross profit is 30000. Furthermore while making computation of

the net profit the whole expenses are deducted wherein total variable expenses is 7875 as well as

utilized by the firm in which it takes all kind of expenditure that are fixed in nature. Therefore it

can be referred to as full costing at the time goods are sold wherein it takes direct material,

material labor, variable expenses as well as fixed production expenditure (Fayard and et. al.,

2014). Therefore in this absorption costing method subtracts the variable production as well as

fixed expenses from the cost of goods sold. With this calculation of the gross profit is being

done.

Sales revenue 52500

Less cost of goods sold

Direct labor 7500

Direct material 12000

Variable production overheads 3000

Fixed production overheads 15000

Cost of goods sold 37500

Gross profit 15000

Less: Variable expenses

Variable selling expenses 7875

Less: Fixed expenses

Fixed selling expenses 10000

Total expenditure 17875

Net profit -2875

Interpretation: From the table above the computation of the net profit is being carried out

by the means of marginal as well as absorption costing tools. Imda Tech Limited business makes

calculation of the net profit through use of marginal as well as absorption costing method. This

can be interpreted from the information above that in table 1 the calculation of the net profit is

being done. Such is being done through summing direct material that is 7500, direct labor 12000

as well as variable production overhead 3000 there is summation of 22500. After this calculation

of the gross profit is being done through deduction of the sales revenue 52500 from the cost of

goods sold 22500 wherein the gross profit is 30000. Furthermore while making computation of

the net profit the whole expenses are deducted wherein total variable expenses is 7875 as well as

fixed total expenses is 25000. This is from the gross profit which is 30000 because the net loss

determined is -2875.

determined is -2875.

TASK 3

(a) Different types of budget and their advantages and disadvantages

Budget is effective approach assist to forecast and make decisions within the enterprise.

In this aspect, business operations of Imda limited can also gain various ideas which improve

financial position of budget program that is prepares for planning procedure. In addition to this,

it can be stated that budget is a fixed plan that are expressed quantitative elements that can be

specify with different resources (Ibarrondo-Dávila, López-Alonso and Rubio-Gámez, 2015). As

per the resources requirement, the company can deal with specified time period. There are

various kinds of budget can be prepared that are explains under here:

Fixed budget

In this types of management system, every organisation analysis their account with

assessing current business performances. With the help of preparing fixed pricing strategy it can

be implements for upcoming months (Breuer, Frumusanu and Manciu, 2013). Hence, certain

ideas and opinion assist to grow operations and outcomes in systematic way for development of

the company and its operations. With the help of ideas, the chosen business can deal with various

elements easily. As results, they will gain pore profits and revenue within the business

environment.

Flexible budget

It is quite different from fixed budget. It determines dynamic in planning strategies. In

this type of process, management account of Imda Limited play dynamic role. In this way, the

company is analysis there all month performances and sales which assist to grow operations and

functions in systematic way (Bodie, Kane and Marcus, 2014). Although, statistic plan take

place for occurring effective results and performances within the business environment. It can be

affects to productivity and outcomes of the chosen business enterprise. Due to continue

fluctuations, economy is widely impacted that create issues in productivity and distribution of

goods in different areas. Various part of the planning process can be as certain at workplace for

delivering results and performances in positive way (Ibarrondo-Dávila, López-Alonso and

Rubio-Gámez, 2015).

Master budget

In this type of budget, the firm carry various elements which serve effective results and

performances within the business environment. In this aspect, the company should analysis all

(a) Different types of budget and their advantages and disadvantages

Budget is effective approach assist to forecast and make decisions within the enterprise.

In this aspect, business operations of Imda limited can also gain various ideas which improve

financial position of budget program that is prepares for planning procedure. In addition to this,

it can be stated that budget is a fixed plan that are expressed quantitative elements that can be

specify with different resources (Ibarrondo-Dávila, López-Alonso and Rubio-Gámez, 2015). As

per the resources requirement, the company can deal with specified time period. There are

various kinds of budget can be prepared that are explains under here:

Fixed budget

In this types of management system, every organisation analysis their account with

assessing current business performances. With the help of preparing fixed pricing strategy it can

be implements for upcoming months (Breuer, Frumusanu and Manciu, 2013). Hence, certain

ideas and opinion assist to grow operations and outcomes in systematic way for development of

the company and its operations. With the help of ideas, the chosen business can deal with various

elements easily. As results, they will gain pore profits and revenue within the business

environment.

Flexible budget

It is quite different from fixed budget. It determines dynamic in planning strategies. In

this type of process, management account of Imda Limited play dynamic role. In this way, the

company is analysis there all month performances and sales which assist to grow operations and

functions in systematic way (Bodie, Kane and Marcus, 2014). Although, statistic plan take

place for occurring effective results and performances within the business environment. It can be

affects to productivity and outcomes of the chosen business enterprise. Due to continue

fluctuations, economy is widely impacted that create issues in productivity and distribution of

goods in different areas. Various part of the planning process can be as certain at workplace for

delivering results and performances in positive way (Ibarrondo-Dávila, López-Alonso and

Rubio-Gámez, 2015).

Master budget

In this type of budget, the firm carry various elements which serve effective results and

performances within the business environment. In this aspect, the company should analysis all

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

detail programs for activities that create effective results and performances at workplace. In this

way, sales, production and material budget take place which assist to grow effective operations

and functions for ascertain results and performances (Carlsson-Wall, Kraus and Lind, 2015). For

assessment of this type of budget, Imda Limited using income statement, balance sheet and cash

flow statement.

Advantages of budget

These are very useful elements which assist to grow operations and functions in

systematic way. With the help of budget assessment, Imda Limited can easily enhance their

profits and revenue for their future investment. In addition to this, productivity and efficiency

can be enhances with the help of different approach (Quinn, Strauss and Kristandl, 2014). Thus,

the chosen firm can frame goals and objectives that are related to the enterprise. It is also

maintains relations with various people through getting participation from them. As results, it

can be consider essential and appropriate tool.

Disadvantage of budget

Beside this, wrong prediction for future can hamper to enhance profits and effective

results at workplace (Bodie, Kane and Marcus, 2014). It is very difficult to analysis business

activities that prepare planning strategies for assess the performances of company. Tough task at

workplace regarding business plan demonstrate various functions which assist to grow

operations and outcomes.

(b) Process for preparing budget

In order to prepare the budget program, it is important to assess effectiveness of the

business in systematic way (Breuer, Frumusanu and Manciu, 2013). It will assist to grow

operations and functions in successful manner. With the help of implementing budget program

Imda limited can gain various benefits at workplace. Process can be considers as follows:

Update budget assumptions

In this stage, the chosen organisation can consider their operations and functions with

update assumptions. In this step, they have to take various aspects which are needed to create

programs and results in effective manner (Ibarrondo-Dávila, López-Alonso and Rubio-Gámez,

2015). In this element management of Imda Limited recognise their performances. Hence, as per

the found data, they can make solutions for ascertain negative impact. As results, further

operations can be created within the business environment.

way, sales, production and material budget take place which assist to grow effective operations

and functions for ascertain results and performances (Carlsson-Wall, Kraus and Lind, 2015). For

assessment of this type of budget, Imda Limited using income statement, balance sheet and cash

flow statement.

Advantages of budget

These are very useful elements which assist to grow operations and functions in

systematic way. With the help of budget assessment, Imda Limited can easily enhance their

profits and revenue for their future investment. In addition to this, productivity and efficiency

can be enhances with the help of different approach (Quinn, Strauss and Kristandl, 2014). Thus,

the chosen firm can frame goals and objectives that are related to the enterprise. It is also

maintains relations with various people through getting participation from them. As results, it

can be consider essential and appropriate tool.

Disadvantage of budget

Beside this, wrong prediction for future can hamper to enhance profits and effective

results at workplace (Bodie, Kane and Marcus, 2014). It is very difficult to analysis business

activities that prepare planning strategies for assess the performances of company. Tough task at

workplace regarding business plan demonstrate various functions which assist to grow

operations and outcomes.

(b) Process for preparing budget

In order to prepare the budget program, it is important to assess effectiveness of the

business in systematic way (Breuer, Frumusanu and Manciu, 2013). It will assist to grow

operations and functions in successful manner. With the help of implementing budget program

Imda limited can gain various benefits at workplace. Process can be considers as follows:

Update budget assumptions

In this stage, the chosen organisation can consider their operations and functions with

update assumptions. In this step, they have to take various aspects which are needed to create

programs and results in effective manner (Ibarrondo-Dávila, López-Alonso and Rubio-Gámez,

2015). In this element management of Imda Limited recognise their performances. Hence, as per

the found data, they can make solutions for ascertain negative impact. As results, further

operations can be created within the business environment.

Review bottlenecks

In this step, the company analysis their maximum achievement, according to review of

different activities (Kihn and Ihantola, 2015). As results, effectiveness can be ascertain at

workplace which support to objectives with the help of investment plan, capabilities can be

enhance that support to implement actions plan as per the enhancing profitability within the

organisation.

Assess available fund

After review of all activities, operations and budget assumptions, Imda Limited analysis

available fund. It will assist to grow profitability and performances through assessing

expenditure and gained revenue (Bodie, Kane and Marcus, 2014). As results, targets and goals

can be maintain at workplace as per the operating of further activities.

Creating budget packages

In this step, Imda Limited creates their budget packages which assist to make effective

results at workplace. In this way, they are analysis adequate production and distribution services

which make results and performances profitable (Gibassier, 2017). Hence, it can be support to

determine different goals and objectives of the company.

Obtain revenue and department budget

After creating budget packages, revenue and department functions can be forecasted by

Imda Limited. On that basis, they are take decision to invest their money and operations in

different areas of the world (Carlsson-Wall, Kraus and Lind, 2015). It makes successful

operations and targets that made for implementation. Estimated incomes and expenditure assist

to move towards the goals and objectives within the business enterprise.

As per the following mention process, Imda Limited has various benefits to operate

functions and operations in systematic way. Decision making regarding business operation in

future assist to make effective results and performances that make results and performances

positive (Breuer, Frumusanu and Manciu, 2013).

(c) Pricing strategies

In this type of approach, there are effective management system take place which assists

to grow more profits and revenue in systematic way. Major it is used by government, non profit

organisation and other businesses (Shuttleworth, 2014). It will assist to align activities which

enhance external and internal outcomes. As per the various factors, cost is determines market

In this step, the company analysis their maximum achievement, according to review of

different activities (Kihn and Ihantola, 2015). As results, effectiveness can be ascertain at

workplace which support to objectives with the help of investment plan, capabilities can be

enhance that support to implement actions plan as per the enhancing profitability within the

organisation.

Assess available fund

After review of all activities, operations and budget assumptions, Imda Limited analysis

available fund. It will assist to grow profitability and performances through assessing

expenditure and gained revenue (Bodie, Kane and Marcus, 2014). As results, targets and goals

can be maintain at workplace as per the operating of further activities.

Creating budget packages

In this step, Imda Limited creates their budget packages which assist to make effective

results at workplace. In this way, they are analysis adequate production and distribution services

which make results and performances profitable (Gibassier, 2017). Hence, it can be support to

determine different goals and objectives of the company.

Obtain revenue and department budget

After creating budget packages, revenue and department functions can be forecasted by

Imda Limited. On that basis, they are take decision to invest their money and operations in

different areas of the world (Carlsson-Wall, Kraus and Lind, 2015). It makes successful

operations and targets that made for implementation. Estimated incomes and expenditure assist

to move towards the goals and objectives within the business enterprise.

As per the following mention process, Imda Limited has various benefits to operate

functions and operations in systematic way. Decision making regarding business operation in

future assist to make effective results and performances that make results and performances

positive (Breuer, Frumusanu and Manciu, 2013).

(c) Pricing strategies

In this type of approach, there are effective management system take place which assists

to grow more profits and revenue in systematic way. Major it is used by government, non profit

organisation and other businesses (Shuttleworth, 2014). It will assist to align activities which

enhance external and internal outcomes. As per the various factors, cost is determines market

demand, competition and product value. As results target and positive outcomes can be measure

that assist to grow operations and performances. Pricing strategies are interrelated which prepare

planning for ascertain cost element at workplace. In addition to this, different determiners are

also take place which recognised as raw material and convert into finished goods (Van Hai and

Van Dung, 2017). This type of strategy is beneficial to finance manager who take part to

demonstrate functions and operations. It stated different types of cost in Imda Limited that help

to ascertain product cost and pricing.

In order to determines price for product and services in Imda Limited, there are different

elements which influence to set pricing decision. It includes customer demand, competitor, costs

and political, legal and many other elements (Boyns and Edwards, 2013). It can be set as market

and subject determination which assist to grow operations and performances in effective way.

The chosen firm is using flexibility system which assists to enhance their sales gradually.

Following are such pricing strategies which can be used at workplace:

Cost plus pricing

It demonstrates as price equal to cost plus make up percentage on cost. This is used to

ascertain total cost of the company which they determine to operate functions and operations in

systematic way (Ibarrondo-Dávila, López-Alonso and Rubio-Gámez, 2015). As results, targets

and other measurement assist to grow profitability and performances for assess the business

environment.

Absorption cost pricing

Absorption costing pricing covers all types of cost which assist to make effective results

and performances. It perceive as equitable for assess business results and performances at

workplace. However, it considers distinction between variable and fixed cost which assist to

demonstrate effective results (Quinn, Strauss and Kristandl, 2014).

Variable cost pricing

In this aspect, cost obscure cost pattern cannot be taken so that company can enhance

their profit and revenue in systematic way. It is not require fixed allocation cost for deliver

effective results and performances. However, there is disadvantage to use this method such as

fixed cost may be overlooked towards the pricing which assist to grow business operations

(Mistry, Sharma and Low, 2014).

that assist to grow operations and performances. Pricing strategies are interrelated which prepare

planning for ascertain cost element at workplace. In addition to this, different determiners are

also take place which recognised as raw material and convert into finished goods (Van Hai and

Van Dung, 2017). This type of strategy is beneficial to finance manager who take part to

demonstrate functions and operations. It stated different types of cost in Imda Limited that help

to ascertain product cost and pricing.

In order to determines price for product and services in Imda Limited, there are different

elements which influence to set pricing decision. It includes customer demand, competitor, costs

and political, legal and many other elements (Boyns and Edwards, 2013). It can be set as market

and subject determination which assist to grow operations and performances in effective way.

The chosen firm is using flexibility system which assists to enhance their sales gradually.

Following are such pricing strategies which can be used at workplace:

Cost plus pricing

It demonstrates as price equal to cost plus make up percentage on cost. This is used to

ascertain total cost of the company which they determine to operate functions and operations in

systematic way (Ibarrondo-Dávila, López-Alonso and Rubio-Gámez, 2015). As results, targets

and other measurement assist to grow profitability and performances for assess the business

environment.

Absorption cost pricing

Absorption costing pricing covers all types of cost which assist to make effective results

and performances. It perceive as equitable for assess business results and performances at

workplace. However, it considers distinction between variable and fixed cost which assist to

demonstrate effective results (Quinn, Strauss and Kristandl, 2014).

Variable cost pricing

In this aspect, cost obscure cost pattern cannot be taken so that company can enhance

their profit and revenue in systematic way. It is not require fixed allocation cost for deliver

effective results and performances. However, there is disadvantage to use this method such as

fixed cost may be overlooked towards the pricing which assist to grow business operations

(Mistry, Sharma and Low, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 4

a) Balance score card approach

In past the firms implement traditional methods for the sake of making evaluation of the

performance of past years. But at presence of various techniques that acts as an aid in

measurement of business performance. The approach that is Balance scorecard is regarded as the

approach which is being used by the firm in order measure the entire performance. It evaluates

the working in the basis of four major criteria. This is comprised of financial, internal process,

learning or growth and customers (Gibassier, 2017). It evaluates efforts of the firm in order to

improve the business for future. This not only emphasize on the financial performance but,

considers financial performance of Balance scorecard approach instead in consider non financial

perspective also.

Financial perspective: Balance scorecard approach focus on the cash flow, sales, growth, income

and equity. In situation cash flow enhances then it reflects that organization has gained profits

and possesses sound performance in the financial year.

Customers: This is regarded as other area which assists in measurement of the performance that

is attached with Balance scorecard approach. Such is customer satisfaction, retention and market

share. This has been determined on the basis of all these areas. For instance, within the fiscal

year approach of balance scorecard has increased number of customers that reflects that there is

satisfaction in the customers by means of products and such is associated with image of the

brand for greater time (Taipaleenmäki, 2014). On the basis of this aspect such is determined that

organization offers quality products and services to the users who have greater satisfaction.

Internal procedure: This includes procurement, production based on such area performance

attached with balance scorecard is being measured.

Learning and growth perspective: Such includes satisfying the personnel, retention of the

employees, skill set etc. For instance, in situation the firm carries out performance in an effective

manner that employees desire to carry out their job at workplace. This is due to the reason that

they make determination of the career opportunity within the organization. With such the skilled

employees are ready to stay in the organization for long term. Such demonstrates that firm has

sound performance and through such they are able to earn greater amount of profits within

specified duration of time (Bebbington, Unerman and O'Dwyer, 2014).

a) Balance score card approach

In past the firms implement traditional methods for the sake of making evaluation of the

performance of past years. But at presence of various techniques that acts as an aid in

measurement of business performance. The approach that is Balance scorecard is regarded as the

approach which is being used by the firm in order measure the entire performance. It evaluates

the working in the basis of four major criteria. This is comprised of financial, internal process,

learning or growth and customers (Gibassier, 2017). It evaluates efforts of the firm in order to

improve the business for future. This not only emphasize on the financial performance but,

considers financial performance of Balance scorecard approach instead in consider non financial

perspective also.

Financial perspective: Balance scorecard approach focus on the cash flow, sales, growth, income

and equity. In situation cash flow enhances then it reflects that organization has gained profits

and possesses sound performance in the financial year.

Customers: This is regarded as other area which assists in measurement of the performance that

is attached with Balance scorecard approach. Such is customer satisfaction, retention and market

share. This has been determined on the basis of all these areas. For instance, within the fiscal

year approach of balance scorecard has increased number of customers that reflects that there is

satisfaction in the customers by means of products and such is associated with image of the

brand for greater time (Taipaleenmäki, 2014). On the basis of this aspect such is determined that

organization offers quality products and services to the users who have greater satisfaction.

Internal procedure: This includes procurement, production based on such area performance

attached with balance scorecard is being measured.

Learning and growth perspective: Such includes satisfying the personnel, retention of the

employees, skill set etc. For instance, in situation the firm carries out performance in an effective

manner that employees desire to carry out their job at workplace. This is due to the reason that

they make determination of the career opportunity within the organization. With such the skilled

employees are ready to stay in the organization for long term. Such demonstrates that firm has

sound performance and through such they are able to earn greater amount of profits within

specified duration of time (Bebbington, Unerman and O'Dwyer, 2014).

Balance Scorecard is considered as an effective method that helps in supporting the

financial issues faced by firm. Thus, such method is crucial and helps Imda to perform its

operations in an effective way so that performance could be raised in different areas. Imda

managers carry out effective performance measurement tools and thus uses balance scorecard

method so that long term business targets could be attained (Lowe and De Loo, 2014). Hence, in

regard to attain such objective it is significant for business to use effective strategies that helps in

allocating the resources so that desired results could be attained. For instance, if Imda customers

are satisfied then it reflects within the payment system and collects crucial information which

helps in increasing the income and cash flow within business.

Further, another effective strategy which is being used in regard to improve financial

governance is using customer based approach and thus prepare appropriate ways so that business

performance could be measured in an effective way. Here, Imda uses such tool in regard to make

effective determination of the issues faced by the managers and thus bring improvement in

regard to prepare financial accounts and obtain significant information so that success could be

attained. Imda also helps in treating the employees properly and thus minimize employees

attrition rate (Setthasakko, 2010).

CONCLUSION

The following report is articulated about management accounting within Imda Limited that

assists to grow operations and outcomes of the company. In this aspect, approach has been used

at workplace which shows allocation of fund that includes preparing of income statement for

ascertains effective results at performances at workplace. Furthermore, critical evaluation

summarized to forecast and decision making within the business environment. In this way,

different types of budget program is take place which create different advantages and

disadvantages for increasing profits and revenue at workplace. Moreover, it includes financial

statement which obtained current performances to reduce problem which faced by the company.

In addition to this, it is also concluded effective strategies which introduce by government at

workplace. it will assists to operate functions and operations in new areas.

financial issues faced by firm. Thus, such method is crucial and helps Imda to perform its

operations in an effective way so that performance could be raised in different areas. Imda

managers carry out effective performance measurement tools and thus uses balance scorecard

method so that long term business targets could be attained (Lowe and De Loo, 2014). Hence, in

regard to attain such objective it is significant for business to use effective strategies that helps in

allocating the resources so that desired results could be attained. For instance, if Imda customers

are satisfied then it reflects within the payment system and collects crucial information which

helps in increasing the income and cash flow within business.

Further, another effective strategy which is being used in regard to improve financial

governance is using customer based approach and thus prepare appropriate ways so that business

performance could be measured in an effective way. Here, Imda uses such tool in regard to make

effective determination of the issues faced by the managers and thus bring improvement in

regard to prepare financial accounts and obtain significant information so that success could be

attained. Imda also helps in treating the employees properly and thus minimize employees

attrition rate (Setthasakko, 2010).

CONCLUSION

The following report is articulated about management accounting within Imda Limited that

assists to grow operations and outcomes of the company. In this aspect, approach has been used

at workplace which shows allocation of fund that includes preparing of income statement for

ascertains effective results at performances at workplace. Furthermore, critical evaluation

summarized to forecast and decision making within the business environment. In this way,

different types of budget program is take place which create different advantages and

disadvantages for increasing profits and revenue at workplace. Moreover, it includes financial

statement which obtained current performances to reduce problem which faced by the company.

In addition to this, it is also concluded effective strategies which introduce by government at

workplace. it will assists to operate functions and operations in new areas.

REFERENCES

Books and Journals

Bebbington, J., Unerman, J. and O'Dwyer, B., 2014. Sustainability accounting and

accountability. Routledge.

Bhimani, A. and et. al., 2013. Introduction to Management Accounting. Pearson Higher Ed.

Bodie, Z., Kane, A. and Marcus, A. J., 2014. Investments, 10e. McGraw-Hill Education.

Boyns, T. and Edwards, J. R., 2013. A history of management accounting: The British

experience (Vol. 12). Routledge.

Breuer, A., Frumusanu, M. L. and Manciu, A., 2013. The role of management accounting in the

decision making process: Case study caras severin county. Annales Universitatis

Apulensis: Series Oeconomica. 15(2). p.355.

Carlsson-Wall, M., Kraus, K. and Lind, J., 2015. Strategic management accounting in close

inter-organisational relationships. Accounting and Business Research. 45(1). pp.27-54.

Chan, H.K., Wang, X. and Raffoni, A., 2014. An integrated approach for green design: Life-

cycle, fuzzy AHP and environmental management accounting. The British Accounting

Review. 46(4). pp.344-360.

Cleary, P., 2015. An empirical investigation of the impact of management accounting on

structural capital and business performance. Journal of Intellectual Capital. 16(3).

pp.566-586.

Dobroszek, J. and Szychta, A., 2015. Indicators as an Instrument of Measurement in

Management Accounting in Logistics Enterprises in Poland.Management and Business

Administration. 23(4). pp.11-33.

Fayard, D. and et. al., 2014. Interorganizational cost management in supply chains: Practices and

payoffs.Management Accounting Quarterly. 15(3). pp.1.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2013. Management accounting and control

practices in a lean manufacturing environment.Accounting, Organizations and Society.

38(1). pp.50-71.

Gibassier, D., 2017. From écobilan to LCA: the elite’s institutional work in the creation of an

environmental management accounting tool. Critical Perspectives on Accounting. 42.

pp.36-58.

Books and Journals

Bebbington, J., Unerman, J. and O'Dwyer, B., 2014. Sustainability accounting and

accountability. Routledge.

Bhimani, A. and et. al., 2013. Introduction to Management Accounting. Pearson Higher Ed.

Bodie, Z., Kane, A. and Marcus, A. J., 2014. Investments, 10e. McGraw-Hill Education.

Boyns, T. and Edwards, J. R., 2013. A history of management accounting: The British

experience (Vol. 12). Routledge.

Breuer, A., Frumusanu, M. L. and Manciu, A., 2013. The role of management accounting in the

decision making process: Case study caras severin county. Annales Universitatis

Apulensis: Series Oeconomica. 15(2). p.355.

Carlsson-Wall, M., Kraus, K. and Lind, J., 2015. Strategic management accounting in close

inter-organisational relationships. Accounting and Business Research. 45(1). pp.27-54.

Chan, H.K., Wang, X. and Raffoni, A., 2014. An integrated approach for green design: Life-

cycle, fuzzy AHP and environmental management accounting. The British Accounting

Review. 46(4). pp.344-360.

Cleary, P., 2015. An empirical investigation of the impact of management accounting on

structural capital and business performance. Journal of Intellectual Capital. 16(3).

pp.566-586.

Dobroszek, J. and Szychta, A., 2015. Indicators as an Instrument of Measurement in

Management Accounting in Logistics Enterprises in Poland.Management and Business

Administration. 23(4). pp.11-33.

Fayard, D. and et. al., 2014. Interorganizational cost management in supply chains: Practices and

payoffs.Management Accounting Quarterly. 15(3). pp.1.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2013. Management accounting and control

practices in a lean manufacturing environment.Accounting, Organizations and Society.

38(1). pp.50-71.

Gibassier, D., 2017. From écobilan to LCA: the elite’s institutional work in the creation of an

environmental management accounting tool. Critical Perspectives on Accounting. 42.

pp.36-58.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Gibassier, D., 2017. From écobilan to LCA: the elite’s institutional work in the creation of an

environmental management accounting tool. Critical Perspectives on Accounting. 42.

pp.36-58.

Ibarrondo-Dávila, M. P., López-Alonso, M. and Rubio-Gámez, M. C., 2015. Managerial

accounting for safety management. The case of a Spanish construction company. Safety

science. 79. pp.116-125.

Kihn, L. A. and Ihantola, E. M., 2015. Approaches to validation and evaluation in qualitative

studies of management accounting. Qualitative Research in Accounting & Management.

12(3). pp.230-255.

Klychova, G. S., Faskhutdinova, М. S. and Sadrieva, E. R., 2014. Budget efficiency for cost

control purposes in management accounting system.Mediterranean Journal of Social

Sciences. 5(24). pp.79.

Lowe, A. and De Loo, I., 2014. The existential perversity of management accounting and

control. In Management Control and Uncertainty (pp. 239-254). Palgrave Macmillan UK.

Mistry, V., Sharma, U. and Low, M., 2014. Management accountants' perception of their role in

accounting for sustainable development: An exploratory study. Pacific Accounting

Review. 26(1/2). pp.112-133.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management control.

Springer.

Quinn, M., Strauss, E. and Kristandl, G., 2014. The effects of cloud technology on management

accounting and business decision-making. Financial Management. 10(6). pp.1-12.

Schaltegger, S., Gibassier, D. and Zvezdov, D., 2013. Is environmental management accounting

a discipline? A bibliometric literature review.Meditari Accountancy Research. 21(1).

pp.4-31.

Setthasakko, W., 2010. Barriers to the development of environmental management accounting:

An exploratory study of pulp and paper companies in Thailand. EuroMed Journal of

Business, 5(3), pp.315-331.

Shuttleworth, C. C., 2014. Perspectives of accounting students and teachers on the changing role

of management accountants in organisations. Southern African Business Review. 18(2).

pp.140-162.

environmental management accounting tool. Critical Perspectives on Accounting. 42.

pp.36-58.

Ibarrondo-Dávila, M. P., López-Alonso, M. and Rubio-Gámez, M. C., 2015. Managerial

accounting for safety management. The case of a Spanish construction company. Safety

science. 79. pp.116-125.

Kihn, L. A. and Ihantola, E. M., 2015. Approaches to validation and evaluation in qualitative

studies of management accounting. Qualitative Research in Accounting & Management.

12(3). pp.230-255.

Klychova, G. S., Faskhutdinova, М. S. and Sadrieva, E. R., 2014. Budget efficiency for cost

control purposes in management accounting system.Mediterranean Journal of Social

Sciences. 5(24). pp.79.

Lowe, A. and De Loo, I., 2014. The existential perversity of management accounting and

control. In Management Control and Uncertainty (pp. 239-254). Palgrave Macmillan UK.

Mistry, V., Sharma, U. and Low, M., 2014. Management accountants' perception of their role in

accounting for sustainable development: An exploratory study. Pacific Accounting

Review. 26(1/2). pp.112-133.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management control.

Springer.

Quinn, M., Strauss, E. and Kristandl, G., 2014. The effects of cloud technology on management

accounting and business decision-making. Financial Management. 10(6). pp.1-12.

Schaltegger, S., Gibassier, D. and Zvezdov, D., 2013. Is environmental management accounting

a discipline? A bibliometric literature review.Meditari Accountancy Research. 21(1).

pp.4-31.

Setthasakko, W., 2010. Barriers to the development of environmental management accounting:

An exploratory study of pulp and paper companies in Thailand. EuroMed Journal of

Business, 5(3), pp.315-331.

Shuttleworth, C. C., 2014. Perspectives of accounting students and teachers on the changing role

of management accountants in organisations. Southern African Business Review. 18(2).

pp.140-162.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.