Management Accounting - Desklib

VerifiedAdded on 2023/06/08

|9

|1406

|233

AI Summary

This article discusses the importance of Management Accounting and the concept of Cost-Volume-Profit (CVP) analysis. It explains the assumptions made in CVP analysis and its role in decision-making. The article also includes a table showing various calculations for Crystal Wellness Center. Subject: Management Accounting, Course Code: Not mentioned, Course Name: Not mentioned, College/University: Not mentioned.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note

Management Accounting

Name of the Student:

Name of the University:

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

MANAGEMENT ACCOUNTING

Table of Contents

Requirement of Task 3.....................................................................................................................2

Requirement to Task 4.....................................................................................................................4

Reference.........................................................................................................................................8

MANAGEMENT ACCOUNTING

Table of Contents

Requirement of Task 3.....................................................................................................................2

Requirement to Task 4.....................................................................................................................4

Reference.........................................................................................................................................8

2

MANAGEMENT ACCOUNTING

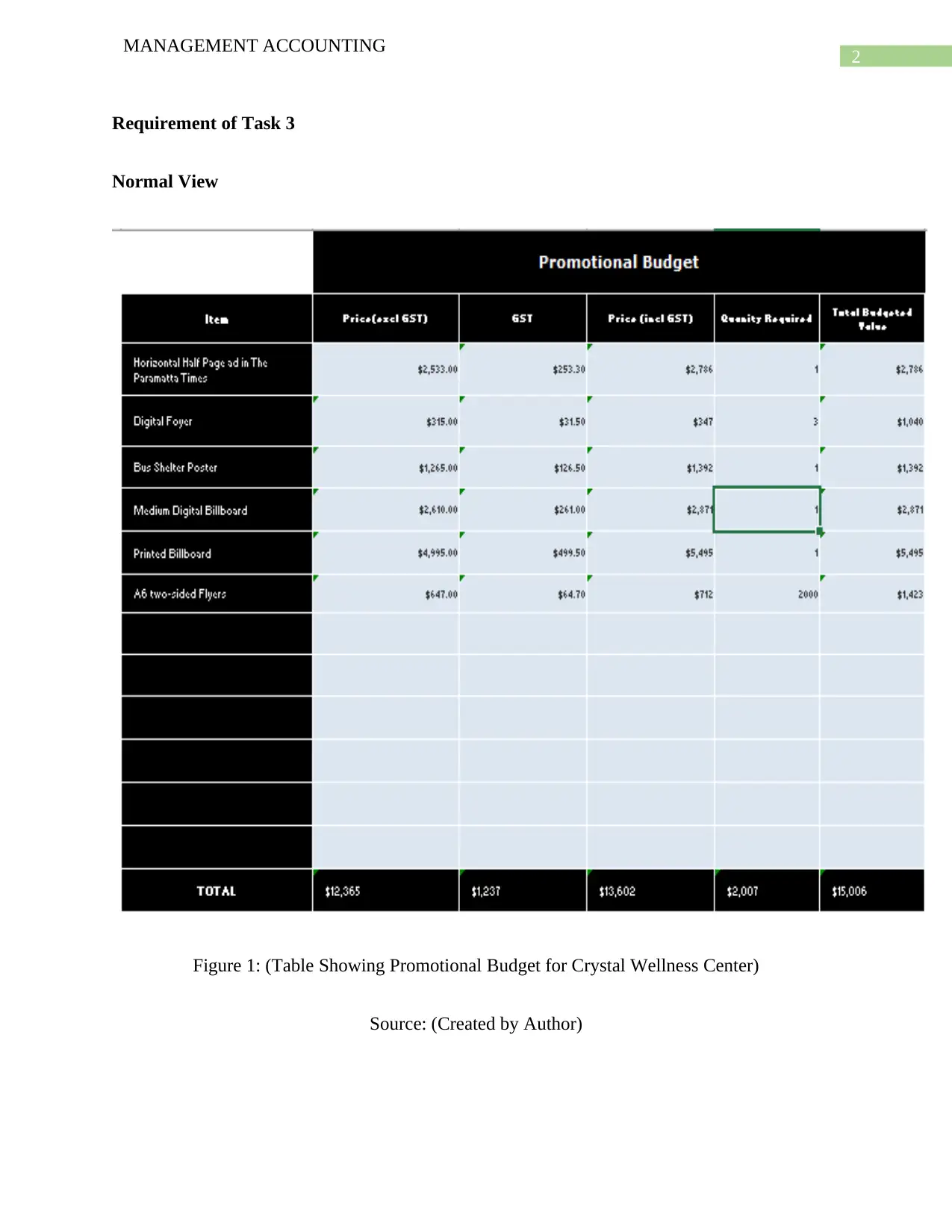

Requirement of Task 3

Normal View

Figure 1: (Table Showing Promotional Budget for Crystal Wellness Center)

Source: (Created by Author)

MANAGEMENT ACCOUNTING

Requirement of Task 3

Normal View

Figure 1: (Table Showing Promotional Budget for Crystal Wellness Center)

Source: (Created by Author)

3

MANAGEMENT ACCOUNTING

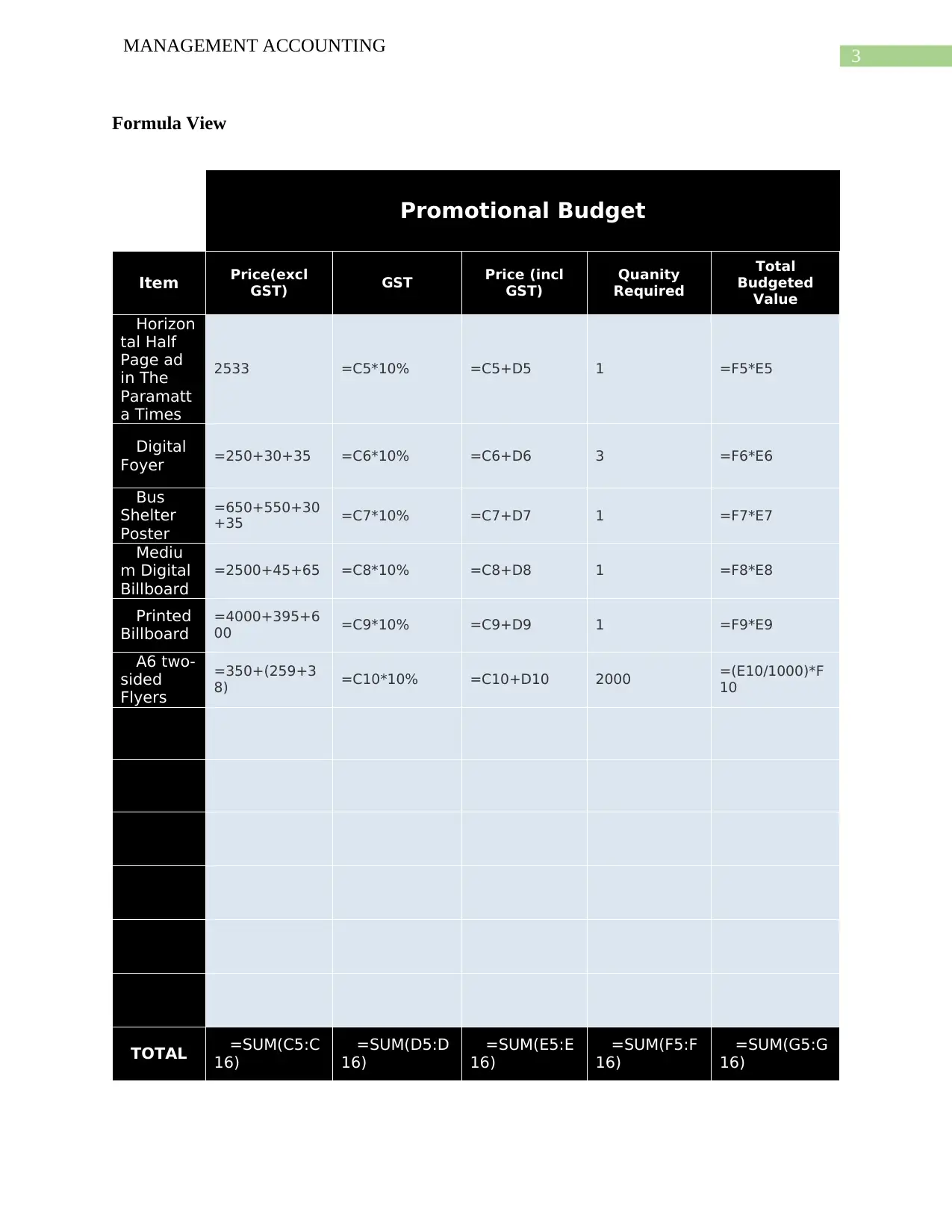

Formula View

Promotional Budget

Item Price(excl

GST) GST Price (incl

GST)

Quanity

Required

Total

Budgeted

Value

Horizon

tal Half

Page ad

in The

Paramatt

a Times

2533 =C5*10% =C5+D5 1 =F5*E5

Digital

Foyer =250+30+35 =C6*10% =C6+D6 3 =F6*E6

Bus

Shelter

Poster

=650+550+30

+35 =C7*10% =C7+D7 1 =F7*E7

Mediu

m Digital

Billboard

=2500+45+65 =C8*10% =C8+D8 1 =F8*E8

Printed

Billboard

=4000+395+6

00 =C9*10% =C9+D9 1 =F9*E9

A6 two-

sided

Flyers

=350+(259+3

8) =C10*10% =C10+D10 2000 =(E10/1000)*F

10

TOTAL =SUM(C5:C

16)

=SUM(D5:D

16)

=SUM(E5:E

16)

=SUM(F5:F

16)

=SUM(G5:G

16)

MANAGEMENT ACCOUNTING

Formula View

Promotional Budget

Item Price(excl

GST) GST Price (incl

GST)

Quanity

Required

Total

Budgeted

Value

Horizon

tal Half

Page ad

in The

Paramatt

a Times

2533 =C5*10% =C5+D5 1 =F5*E5

Digital

Foyer =250+30+35 =C6*10% =C6+D6 3 =F6*E6

Bus

Shelter

Poster

=650+550+30

+35 =C7*10% =C7+D7 1 =F7*E7

Mediu

m Digital

Billboard

=2500+45+65 =C8*10% =C8+D8 1 =F8*E8

Printed

Billboard

=4000+395+6

00 =C9*10% =C9+D9 1 =F9*E9

A6 two-

sided

Flyers

=350+(259+3

8) =C10*10% =C10+D10 2000 =(E10/1000)*F

10

TOTAL =SUM(C5:C

16)

=SUM(D5:D

16)

=SUM(E5:E

16)

=SUM(F5:F

16)

=SUM(G5:G

16)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

MANAGEMENT ACCOUNTING

As per the plan of the management of Crystal Hotels a luncheon is planned for the

opening day of Wellness Center. In order to reach out to the existing and new customers of the

business, the management has undertaken expenses for promotional activities which is shown in

the table above. As per the budget, the management has kept aside an amount of $ 35,350 in

order to promote the wellness center among the customers. The above table shows that the

management has expended significantly on printed billboards which is the most costly among

other promotion medium used by business and it is also considered to be one of the most

effective form of promotion medium.

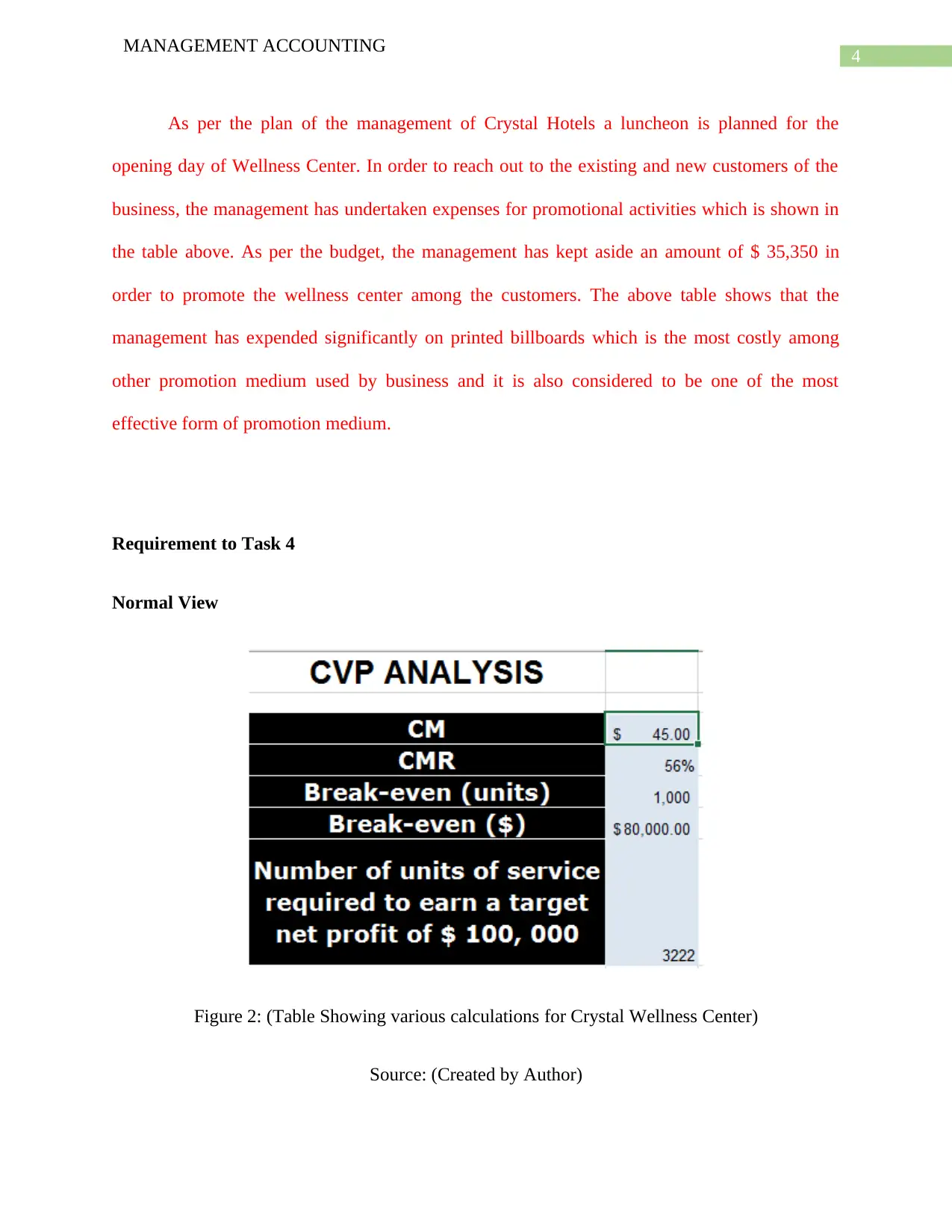

Requirement to Task 4

Normal View

Figure 2: (Table Showing various calculations for Crystal Wellness Center)

Source: (Created by Author)

MANAGEMENT ACCOUNTING

As per the plan of the management of Crystal Hotels a luncheon is planned for the

opening day of Wellness Center. In order to reach out to the existing and new customers of the

business, the management has undertaken expenses for promotional activities which is shown in

the table above. As per the budget, the management has kept aside an amount of $ 35,350 in

order to promote the wellness center among the customers. The above table shows that the

management has expended significantly on printed billboards which is the most costly among

other promotion medium used by business and it is also considered to be one of the most

effective form of promotion medium.

Requirement to Task 4

Normal View

Figure 2: (Table Showing various calculations for Crystal Wellness Center)

Source: (Created by Author)

5

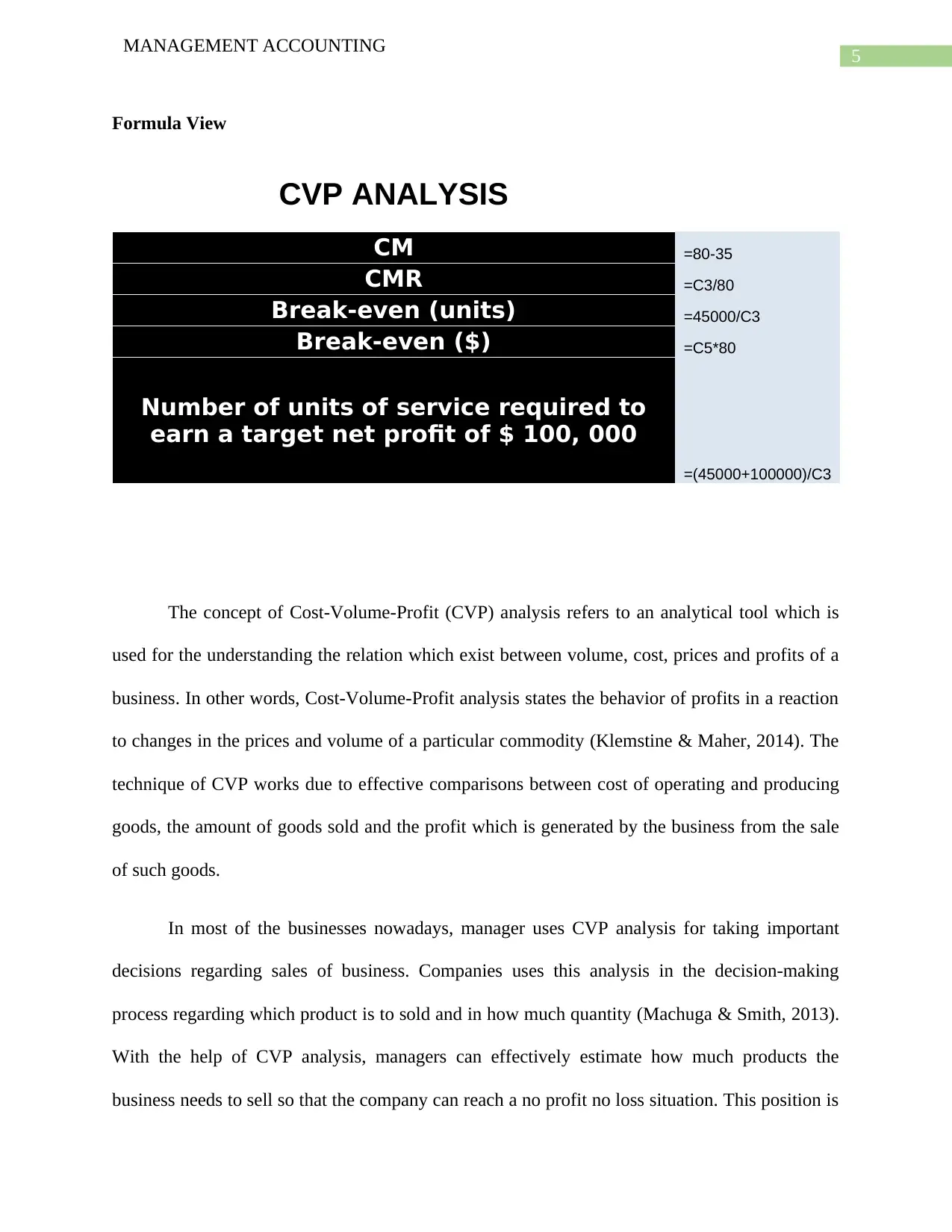

MANAGEMENT ACCOUNTING

Formula View

CVP ANALYSIS

CM =80-35

CMR =C3/80

Break-even (units) =45000/C3

Break-even ($) =C5*80

Number of units of service required to

earn a target net profit of $ 100, 000

=(45000+100000)/C3

The concept of Cost-Volume-Profit (CVP) analysis refers to an analytical tool which is

used for the understanding the relation which exist between volume, cost, prices and profits of a

business. In other words, Cost-Volume-Profit analysis states the behavior of profits in a reaction

to changes in the prices and volume of a particular commodity (Klemstine & Maher, 2014). The

technique of CVP works due to effective comparisons between cost of operating and producing

goods, the amount of goods sold and the profit which is generated by the business from the sale

of such goods.

In most of the businesses nowadays, manager uses CVP analysis for taking important

decisions regarding sales of business. Companies uses this analysis in the decision-making

process regarding which product is to sold and in how much quantity (Machuga & Smith, 2013).

With the help of CVP analysis, managers can effectively estimate how much products the

business needs to sell so that the company can reach a no profit no loss situation. This position is

MANAGEMENT ACCOUNTING

Formula View

CVP ANALYSIS

CM =80-35

CMR =C3/80

Break-even (units) =45000/C3

Break-even ($) =C5*80

Number of units of service required to

earn a target net profit of $ 100, 000

=(45000+100000)/C3

The concept of Cost-Volume-Profit (CVP) analysis refers to an analytical tool which is

used for the understanding the relation which exist between volume, cost, prices and profits of a

business. In other words, Cost-Volume-Profit analysis states the behavior of profits in a reaction

to changes in the prices and volume of a particular commodity (Klemstine & Maher, 2014). The

technique of CVP works due to effective comparisons between cost of operating and producing

goods, the amount of goods sold and the profit which is generated by the business from the sale

of such goods.

In most of the businesses nowadays, manager uses CVP analysis for taking important

decisions regarding sales of business. Companies uses this analysis in the decision-making

process regarding which product is to sold and in how much quantity (Machuga & Smith, 2013).

With the help of CVP analysis, managers can effectively estimate how much products the

business needs to sell so that the company can reach a no profit no loss situation. This position is

6

MANAGEMENT ACCOUNTING

also known to be breakeven point. In this way, CVP analysis can also be used by the business for

determining the number of units which are to be sold by the business in order to generate a

determined level of operating income for the business (Baral, 2016). Therefore, it is clear that the

technique forms an integral part of the profit planning process and thereby also forms part of the

managerial decision-making process.

The assumptions which are undertaken by the business in case of CVP analysis and the

following assumptions are made for the purpose of analyzing and conducting CVP analysis of a

business. The assumptions are given below in details:

All necessary costs of the business such as manufacturing, administrative and overhead

costs which can be either identified as fixed in nature or variable in nature (Walther &

Skousen, 2014).

The selling price per unit of the product is considered to be constant and changes in

activity are the only factors which affects the costs of the business.

It is also assumed that all units which are manufactured are sold during the year.

The importance of CVP analysis is very useful in the overall revenue generation of the

business. CVP analysis provides insights into inter relational factors and the effects of the same

on the profits which is generated by the business. The relationship which exist between cost,

volume, profits of the business are essential in the overall decision-making process of the

business. Therefore, it is clear that CVP relationship is very crucial in the process of budget

estimations and planning for profits of the business (EFinanceManagement.com., 2018). In the

planning for profits of the business, it is very useful in determining the maximum sales which the

business needs to achieve in order to generate revenue for the business. The methods is very

MANAGEMENT ACCOUNTING

also known to be breakeven point. In this way, CVP analysis can also be used by the business for

determining the number of units which are to be sold by the business in order to generate a

determined level of operating income for the business (Baral, 2016). Therefore, it is clear that the

technique forms an integral part of the profit planning process and thereby also forms part of the

managerial decision-making process.

The assumptions which are undertaken by the business in case of CVP analysis and the

following assumptions are made for the purpose of analyzing and conducting CVP analysis of a

business. The assumptions are given below in details:

All necessary costs of the business such as manufacturing, administrative and overhead

costs which can be either identified as fixed in nature or variable in nature (Walther &

Skousen, 2014).

The selling price per unit of the product is considered to be constant and changes in

activity are the only factors which affects the costs of the business.

It is also assumed that all units which are manufactured are sold during the year.

The importance of CVP analysis is very useful in the overall revenue generation of the

business. CVP analysis provides insights into inter relational factors and the effects of the same

on the profits which is generated by the business. The relationship which exist between cost,

volume, profits of the business are essential in the overall decision-making process of the

business. Therefore, it is clear that CVP relationship is very crucial in the process of budget

estimations and planning for profits of the business (EFinanceManagement.com., 2018). In the

planning for profits of the business, it is very useful in determining the maximum sales which the

business needs to achieve in order to generate revenue for the business. The methods is very

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGEMENT ACCOUNTING

useful for the purpose of estimating the different combinations which are essential to generate

profits which are essential for the business.

In addition to this, CVP analysis can bring about a change in the dynamic management of the

business and is essential in the decision-making process of the business. The implication of CVP

decision-making process can help management to predict and evaluate the implications of short

term decision regarding fixed costs of the business. In addition to this, the analysis of CVP will

also help in making long-term decision-making process (Jakupi, Statovci & Hajrizi 2017). The

selling prices and profits of the business will be help the management on making profits plans on

a continuous basis. The analysis of CVP analysis considers marginal costs, fixed costs and

profits of the business for the purpose estimating the relevant computations.

As per the computations of Contribution Margin (CM) for Crystal Wellness center is shown

to be $ 45 and the contribution margin ratio is shown to be 56%. The breakeven analysis shows

the minimum units which the business needs to sale for the purpose of ensuring the business

covers the fixed costs of the business. The breakeven analysis in units show 1000 units and

breakeven in dollars is shown to be $ 80,000. The above figure 2 also shows the number of units

which the business needs to sale for achieving a net profit of $ 100,000 is shown to be 3222

units.

MANAGEMENT ACCOUNTING

useful for the purpose of estimating the different combinations which are essential to generate

profits which are essential for the business.

In addition to this, CVP analysis can bring about a change in the dynamic management of the

business and is essential in the decision-making process of the business. The implication of CVP

decision-making process can help management to predict and evaluate the implications of short

term decision regarding fixed costs of the business. In addition to this, the analysis of CVP will

also help in making long-term decision-making process (Jakupi, Statovci & Hajrizi 2017). The

selling prices and profits of the business will be help the management on making profits plans on

a continuous basis. The analysis of CVP analysis considers marginal costs, fixed costs and

profits of the business for the purpose estimating the relevant computations.

As per the computations of Contribution Margin (CM) for Crystal Wellness center is shown

to be $ 45 and the contribution margin ratio is shown to be 56%. The breakeven analysis shows

the minimum units which the business needs to sale for the purpose of ensuring the business

covers the fixed costs of the business. The breakeven analysis in units show 1000 units and

breakeven in dollars is shown to be $ 80,000. The above figure 2 also shows the number of units

which the business needs to sale for achieving a net profit of $ 100,000 is shown to be 3222

units.

8

MANAGEMENT ACCOUNTING

Reference

Baral, G. (2016). Cost–Value–Profit Analysis and Target Costing with Fuzzy Logic

Theory. Mediterranean Journal of Social Sciences, 7(2), 21.

EFinanceManagement.com. (2018) Cost Volume Profit Analysis | Define, Assumption, Pros,

Cons, Importance.. Retrieved 14 August 2018, from

https://efinancemanagement.com/financial-analysis/cost-volume-profit-analysis

Jakupi, S., Statovci, B., & Hajrizi, B. (2017). Break-Even Analysis as a powerful tool in

Decision-Making. International Journal of Management Excellence, 9(3), 1169-1171.

Klemstine, C. F., & Maher, M. (2014). Management Accounting Research (RLE Accounting): A

Review and Annotated Bibliography. Routledge.

Machuga, S., & Smith, C. (2013). A Case Method Approach of Teaching How Cost-Volume-

Profit Analysis is Connected to the Flexible Budgeting Process and Variance

Analysis. Journal of Accounting and Finance, 13(6), 178-192.

Walther, L. M., & Skousen, C. J. (2014). Cost Analysis. Bookboon.

MANAGEMENT ACCOUNTING

Reference

Baral, G. (2016). Cost–Value–Profit Analysis and Target Costing with Fuzzy Logic

Theory. Mediterranean Journal of Social Sciences, 7(2), 21.

EFinanceManagement.com. (2018) Cost Volume Profit Analysis | Define, Assumption, Pros,

Cons, Importance.. Retrieved 14 August 2018, from

https://efinancemanagement.com/financial-analysis/cost-volume-profit-analysis

Jakupi, S., Statovci, B., & Hajrizi, B. (2017). Break-Even Analysis as a powerful tool in

Decision-Making. International Journal of Management Excellence, 9(3), 1169-1171.

Klemstine, C. F., & Maher, M. (2014). Management Accounting Research (RLE Accounting): A

Review and Annotated Bibliography. Routledge.

Machuga, S., & Smith, C. (2013). A Case Method Approach of Teaching How Cost-Volume-

Profit Analysis is Connected to the Flexible Budgeting Process and Variance

Analysis. Journal of Accounting and Finance, 13(6), 178-192.

Walther, L. M., & Skousen, C. J. (2014). Cost Analysis. Bookboon.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.