Management Accounting Assignment Solution: MAA262, Deakin University

VerifiedAdded on 2023/06/07

|8

|1342

|196

Homework Assignment

AI Summary

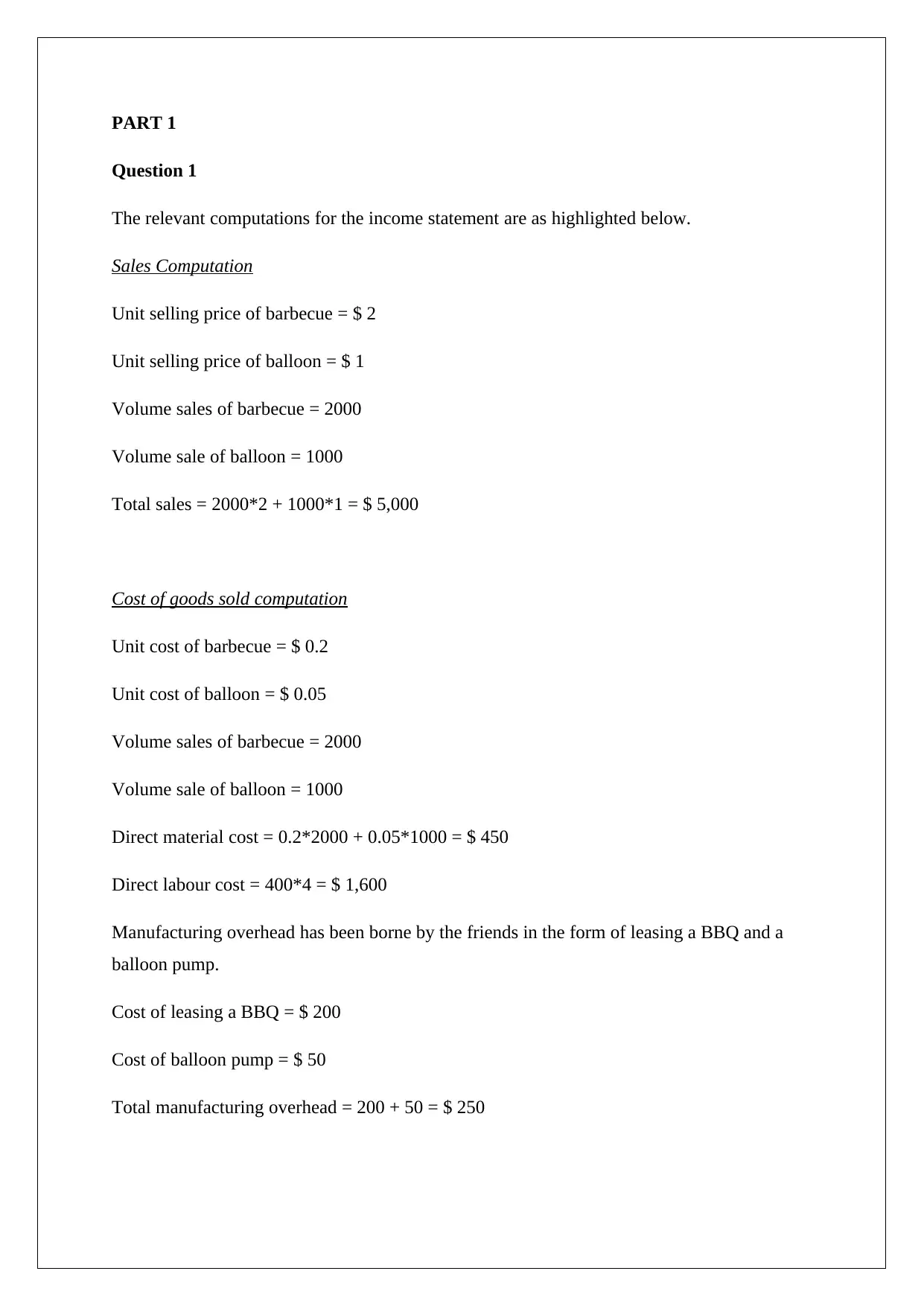

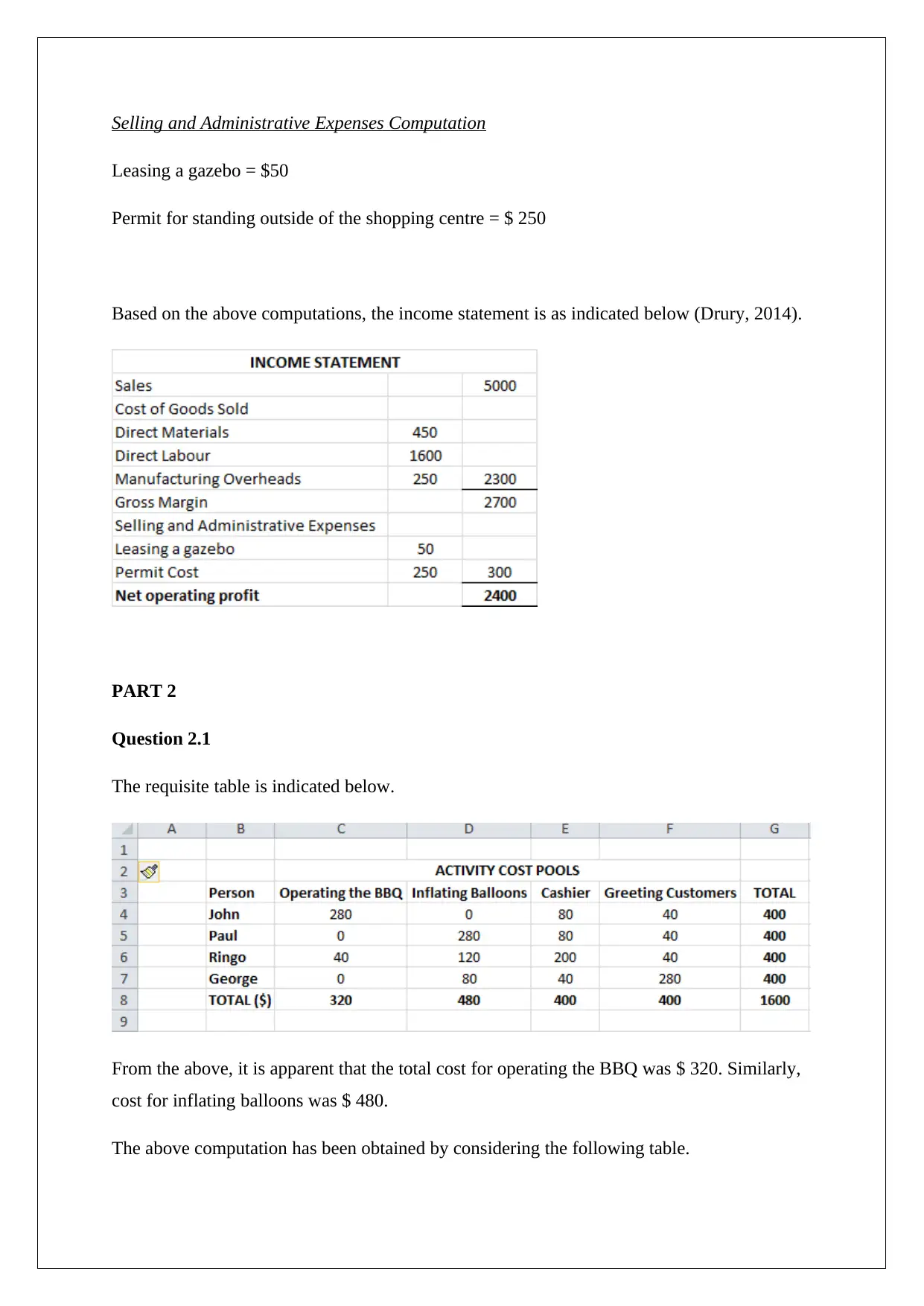

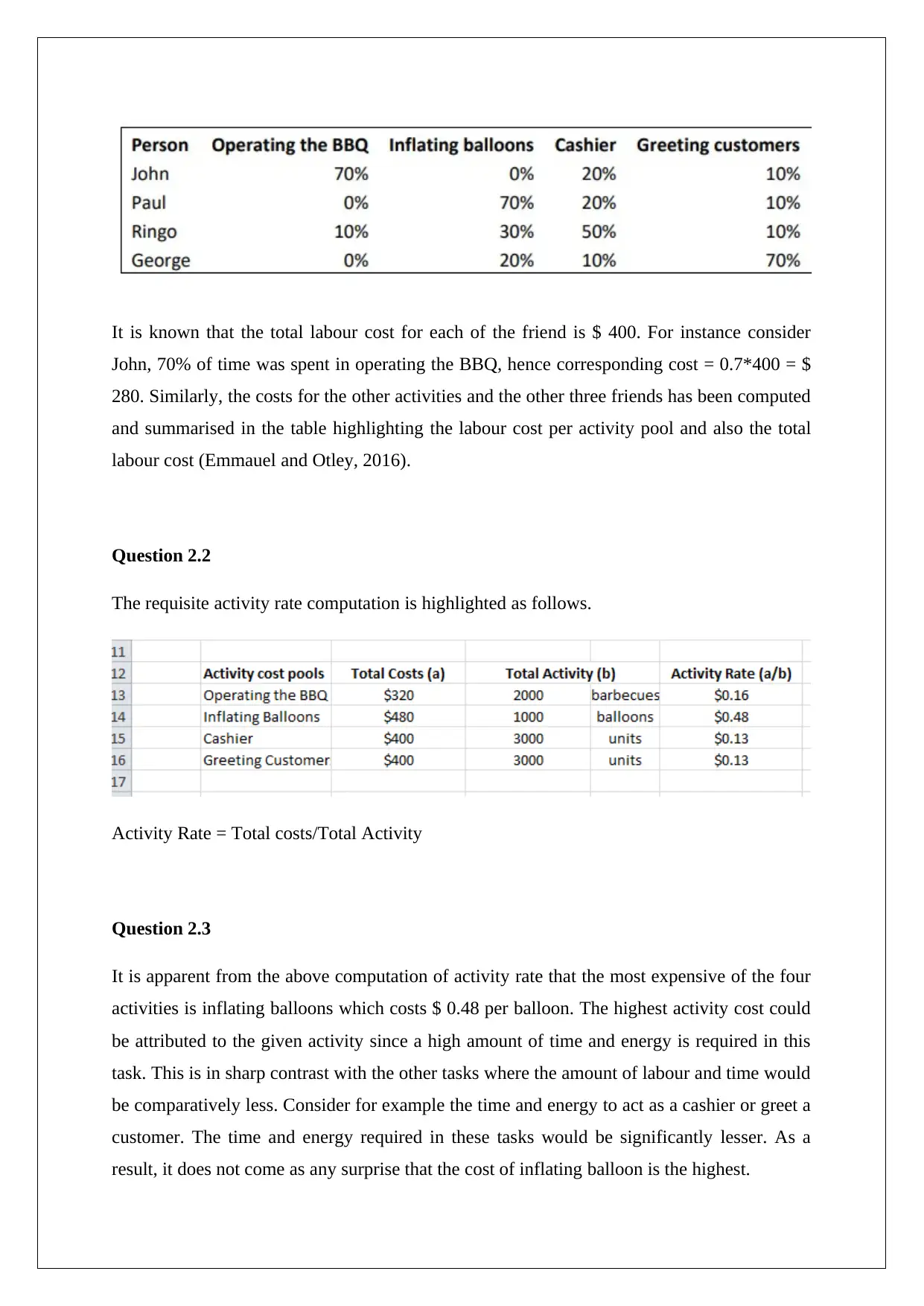

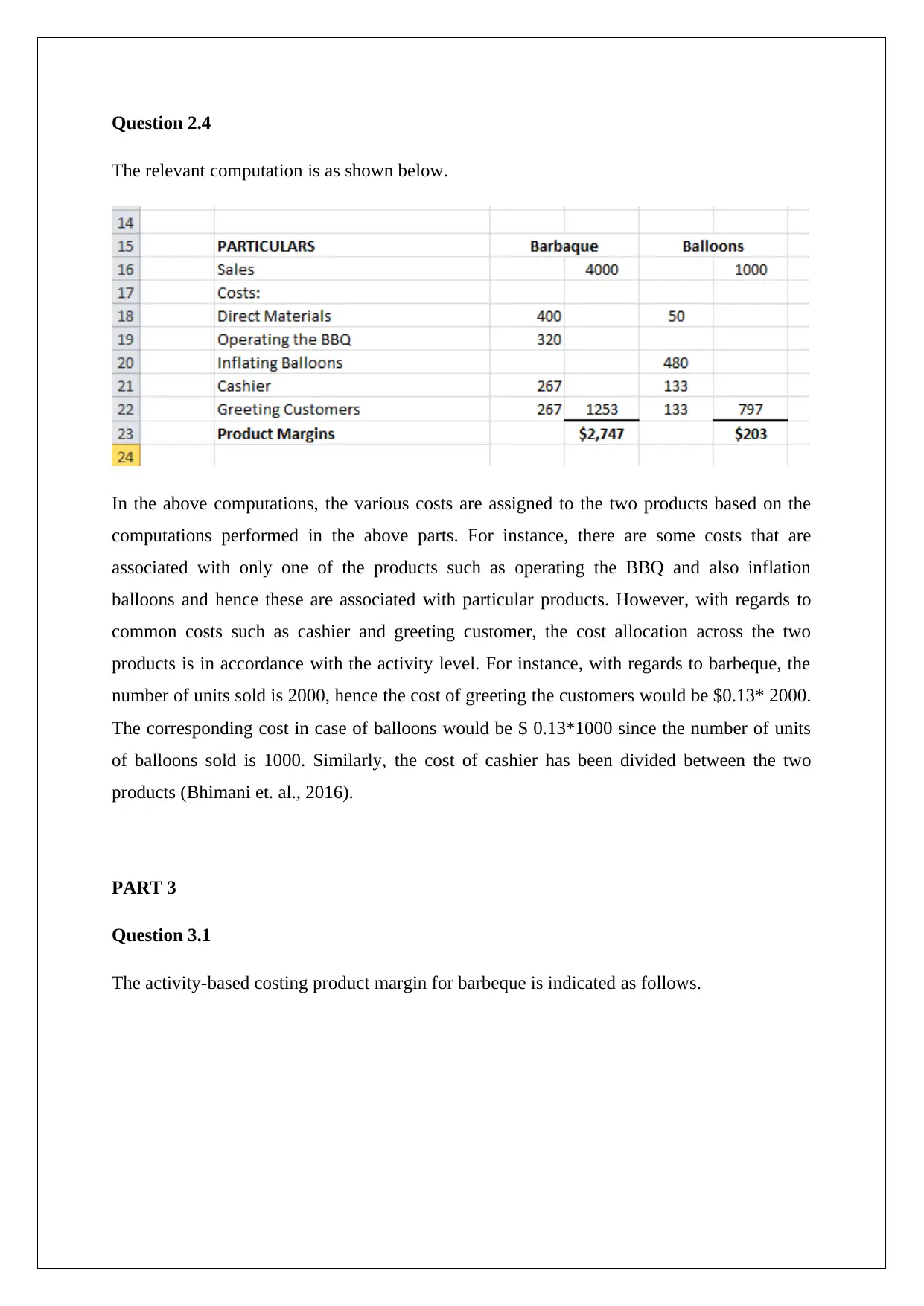

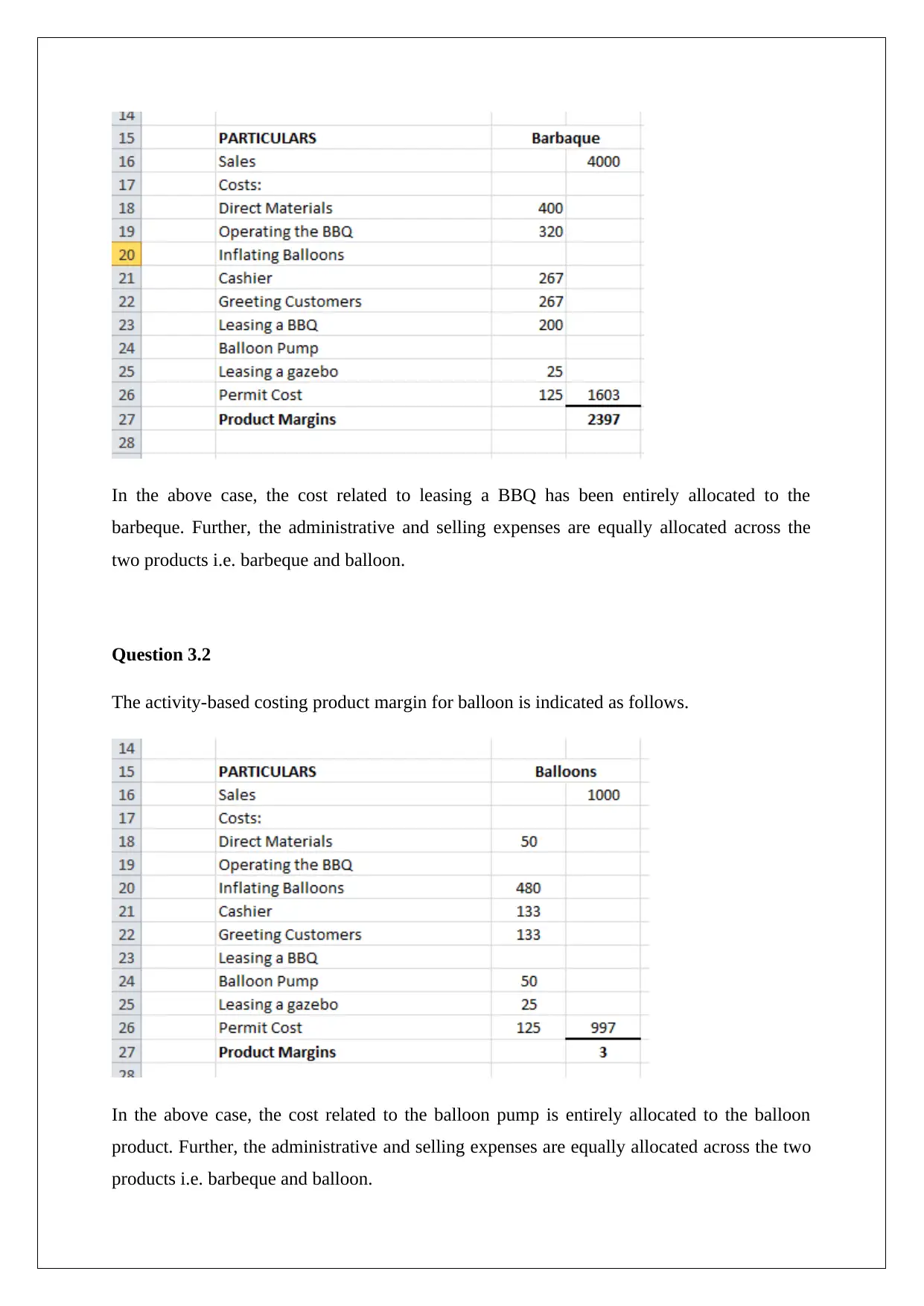

This document presents a comprehensive solution to a management accounting assignment, covering key concepts such as income statement preparation, cost of goods sold calculation, and activity-based costing (ABC). The assignment analyzes a business scenario involving the sale of barbecues and balloons, including detailed computations of sales, costs, and expenses. It explores cost allocation across different activities like operating the BBQ, inflating balloons, and customer service. The solution provides tables illustrating labor costs per activity and activity rate calculations. Furthermore, it includes the computation of activity-based costing product margins for both barbecue and balloon sales, alongside a critical analysis of the business's profitability and the strategic decisions made by the team. The assignment concludes with a discussion on the accuracy of statements made by team members, evaluating the contributions of each member and the viability of the balloon sales.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.