Introduction to Management Accounting

VerifiedAdded on 2023/06/07

|15

|2864

|497

AI Summary

This report discusses cost allocation, traditional costing, activity based costing, ethical dilemmas, and their effects on profitability. It also includes a case study on Beztec Limited and their decision to continue with a new product. The report emphasizes the importance of using correct costing methods for accurate decision making. Course code, course name, and college/university are not mentioned.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Introduction to Management Accounting

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Executive Summary

The report below discusses the basis of cost allocation by concerns engaged in production.

The cost allocation process depends on the complexity of the production process and also the

number of divisions. In order to ensure correct data is used by the management for decision

making, proper cost allocation techniques should be applied.

2

The report below discusses the basis of cost allocation by concerns engaged in production.

The cost allocation process depends on the complexity of the production process and also the

number of divisions. In order to ensure correct data is used by the management for decision

making, proper cost allocation techniques should be applied.

2

Contents

Introduction...........................................................................................................................................4

Importance of use of correct manner of costing.....................................................................................5

Tradition costing and its disadvantages.................................................................................................6

Activity based costing...........................................................................................................................7

Ethical dilemma in change of costing methods......................................................................................9

Effect of costing method on profitability.............................................................................................10

Under and over recovery of overheads and there treatment.................................................................12

Conclusion and Recommendation.......................................................................................................14

Bibliography........................................................................................................................................15

3

Introduction...........................................................................................................................................4

Importance of use of correct manner of costing.....................................................................................5

Tradition costing and its disadvantages.................................................................................................6

Activity based costing...........................................................................................................................7

Ethical dilemma in change of costing methods......................................................................................9

Effect of costing method on profitability.............................................................................................10

Under and over recovery of overheads and there treatment.................................................................12

Conclusion and Recommendation.......................................................................................................14

Bibliography........................................................................................................................................15

3

Introduction

In a production facility, it is important that all cost are collected appropriately and allocated

amongst the products in order to ensure correct pricing of the product (Holtzman, 2013). The

costing data helps the management take important decisions, regarding the operations of the

business. Beztec Limited had two major products, Lexon and Protox. Lexon is an old product

and Protox in the newly introduced model. The management is in a fix about the decision of

whether they should continue with the new model or not. It is important that the profitability

of the product be checked in order to take the appropriate decision. Using a correct costing

system is important so that correct profitability can be determined (Horngren, 2012).

4

In a production facility, it is important that all cost are collected appropriately and allocated

amongst the products in order to ensure correct pricing of the product (Holtzman, 2013). The

costing data helps the management take important decisions, regarding the operations of the

business. Beztec Limited had two major products, Lexon and Protox. Lexon is an old product

and Protox in the newly introduced model. The management is in a fix about the decision of

whether they should continue with the new model or not. It is important that the profitability

of the product be checked in order to take the appropriate decision. Using a correct costing

system is important so that correct profitability can be determined (Horngren, 2012).

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Importance of use of correct manner of costing

The costs which are directly related to the particular product are wholly allocated to that

particular product. There are other costs also, which are incurred jointly (Menifield, 2014).

These joint costs are required to be allocated amongst the product so that total cost the

product can be determined. This allocation of overhead cost needs to be done using an

appropriate allocation rate. It is important that the allocation rate determined is based on

actual consumption and use of resources. If improper allocation rate is applied to the products

then it results in wrong decision making by the management (Atkinson, 2012). This leads to

wrong pricing of the product, which results in wrong profitability. When the company is

unable to rely on its costs data then it becomes difficult to take any decisions. Therefore, it is

important that correct allocation methods is applied in order to allocate the costs.

5

The costs which are directly related to the particular product are wholly allocated to that

particular product. There are other costs also, which are incurred jointly (Menifield, 2014).

These joint costs are required to be allocated amongst the product so that total cost the

product can be determined. This allocation of overhead cost needs to be done using an

appropriate allocation rate. It is important that the allocation rate determined is based on

actual consumption and use of resources. If improper allocation rate is applied to the products

then it results in wrong decision making by the management (Atkinson, 2012). This leads to

wrong pricing of the product, which results in wrong profitability. When the company is

unable to rely on its costs data then it becomes difficult to take any decisions. Therefore, it is

important that correct allocation methods is applied in order to allocate the costs.

5

Tradition costing and its disadvantages

Traditional costing is the costing system which uses one single overhead rate in order to

allocate the joint products. In this system the costs are allocated amongst various products

based on single attribute or cost driver (Berry, 2009). This method fails to incorporate the

concept of actual consumption of resources while allocating the cost. This leads to improper

cost allocation. Even if the services used by a product are very less, a large portion of costs

can be allocated (Noreen, 2015). This increases the cost of the product, which increases the

selling price. When the customer finds the same product from other manufacturer at cheaper

rate, they would definitely go for it. This affects the demands. Therefore we see that

traditional costing can be wrong to be implemented in some cases. Where there are various

costs and various products using one cost attribute to allocate cost, it will lead to wrong

results (Boyd, 2013). The main disadvantages of traditional costing include improper

allocation, ignorance of actual consumption and use of improper data for cost allocation.

In the given scenario we see that production overhead is allocated amongst the product using

the rate of $27.50 per machine hour used. But when we see the table for consumption of the

activity, we see that the activities are not evenly used by both the projects, some activities are

used more than the other by all the products. Distribution of production overheads based on

one overhead rate has resulted in shift of the major expense to the Lexon model. Therefore,

we see that traditional costing can result in improper accounting of cost data (Raun, 1962).

6

Traditional costing is the costing system which uses one single overhead rate in order to

allocate the joint products. In this system the costs are allocated amongst various products

based on single attribute or cost driver (Berry, 2009). This method fails to incorporate the

concept of actual consumption of resources while allocating the cost. This leads to improper

cost allocation. Even if the services used by a product are very less, a large portion of costs

can be allocated (Noreen, 2015). This increases the cost of the product, which increases the

selling price. When the customer finds the same product from other manufacturer at cheaper

rate, they would definitely go for it. This affects the demands. Therefore we see that

traditional costing can be wrong to be implemented in some cases. Where there are various

costs and various products using one cost attribute to allocate cost, it will lead to wrong

results (Boyd, 2013). The main disadvantages of traditional costing include improper

allocation, ignorance of actual consumption and use of improper data for cost allocation.

In the given scenario we see that production overhead is allocated amongst the product using

the rate of $27.50 per machine hour used. But when we see the table for consumption of the

activity, we see that the activities are not evenly used by both the projects, some activities are

used more than the other by all the products. Distribution of production overheads based on

one overhead rate has resulted in shift of the major expense to the Lexon model. Therefore,

we see that traditional costing can result in improper accounting of cost data (Raun, 1962).

6

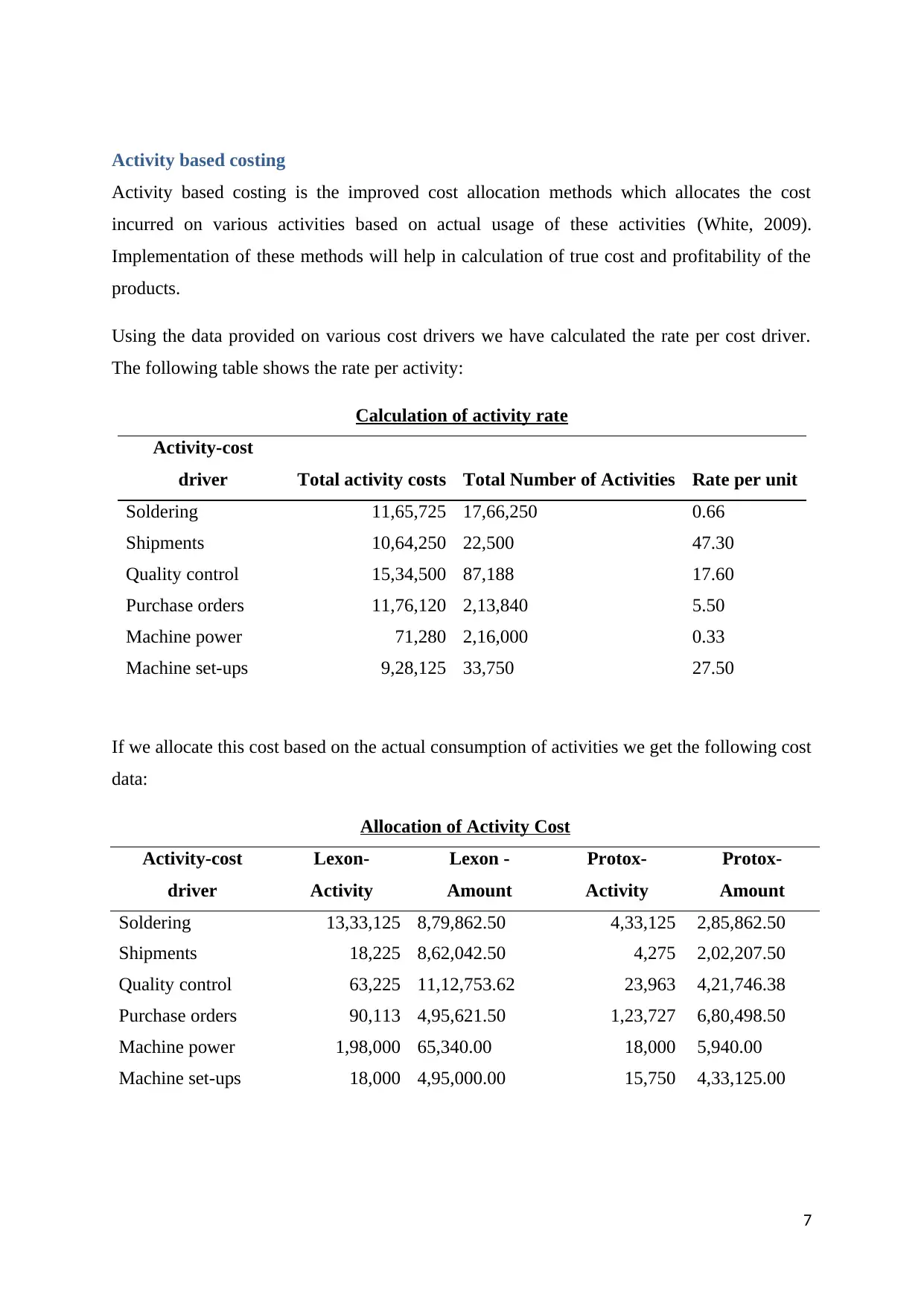

Activity based costing

Activity based costing is the improved cost allocation methods which allocates the cost

incurred on various activities based on actual usage of these activities (White, 2009).

Implementation of these methods will help in calculation of true cost and profitability of the

products.

Using the data provided on various cost drivers we have calculated the rate per cost driver.

The following table shows the rate per activity:

Calculation of activity rate

Activity-cost

driver Total activity costs Total Number of Activities Rate per unit

Soldering 11,65,725 17,66,250 0.66

Shipments 10,64,250 22,500 47.30

Quality control 15,34,500 87,188 17.60

Purchase orders 11,76,120 2,13,840 5.50

Machine power 71,280 2,16,000 0.33

Machine set-ups 9,28,125 33,750 27.50

If we allocate this cost based on the actual consumption of activities we get the following cost

data:

Allocation of Activity Cost

Activity-cost

driver

Lexon-

Activity

Lexon -

Amount

Protox-

Activity

Protox-

Amount

Soldering 13,33,125 8,79,862.50 4,33,125 2,85,862.50

Shipments 18,225 8,62,042.50 4,275 2,02,207.50

Quality control 63,225 11,12,753.62 23,963 4,21,746.38

Purchase orders 90,113 4,95,621.50 1,23,727 6,80,498.50

Machine power 1,98,000 65,340.00 18,000 5,940.00

Machine set-ups 18,000 4,95,000.00 15,750 4,33,125.00

7

Activity based costing is the improved cost allocation methods which allocates the cost

incurred on various activities based on actual usage of these activities (White, 2009).

Implementation of these methods will help in calculation of true cost and profitability of the

products.

Using the data provided on various cost drivers we have calculated the rate per cost driver.

The following table shows the rate per activity:

Calculation of activity rate

Activity-cost

driver Total activity costs Total Number of Activities Rate per unit

Soldering 11,65,725 17,66,250 0.66

Shipments 10,64,250 22,500 47.30

Quality control 15,34,500 87,188 17.60

Purchase orders 11,76,120 2,13,840 5.50

Machine power 71,280 2,16,000 0.33

Machine set-ups 9,28,125 33,750 27.50

If we allocate this cost based on the actual consumption of activities we get the following cost

data:

Allocation of Activity Cost

Activity-cost

driver

Lexon-

Activity

Lexon -

Amount

Protox-

Activity

Protox-

Amount

Soldering 13,33,125 8,79,862.50 4,33,125 2,85,862.50

Shipments 18,225 8,62,042.50 4,275 2,02,207.50

Quality control 63,225 11,12,753.62 23,963 4,21,746.38

Purchase orders 90,113 4,95,621.50 1,23,727 6,80,498.50

Machine power 1,98,000 65,340.00 18,000 5,940.00

Machine set-ups 18,000 4,95,000.00 15,750 4,33,125.00

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

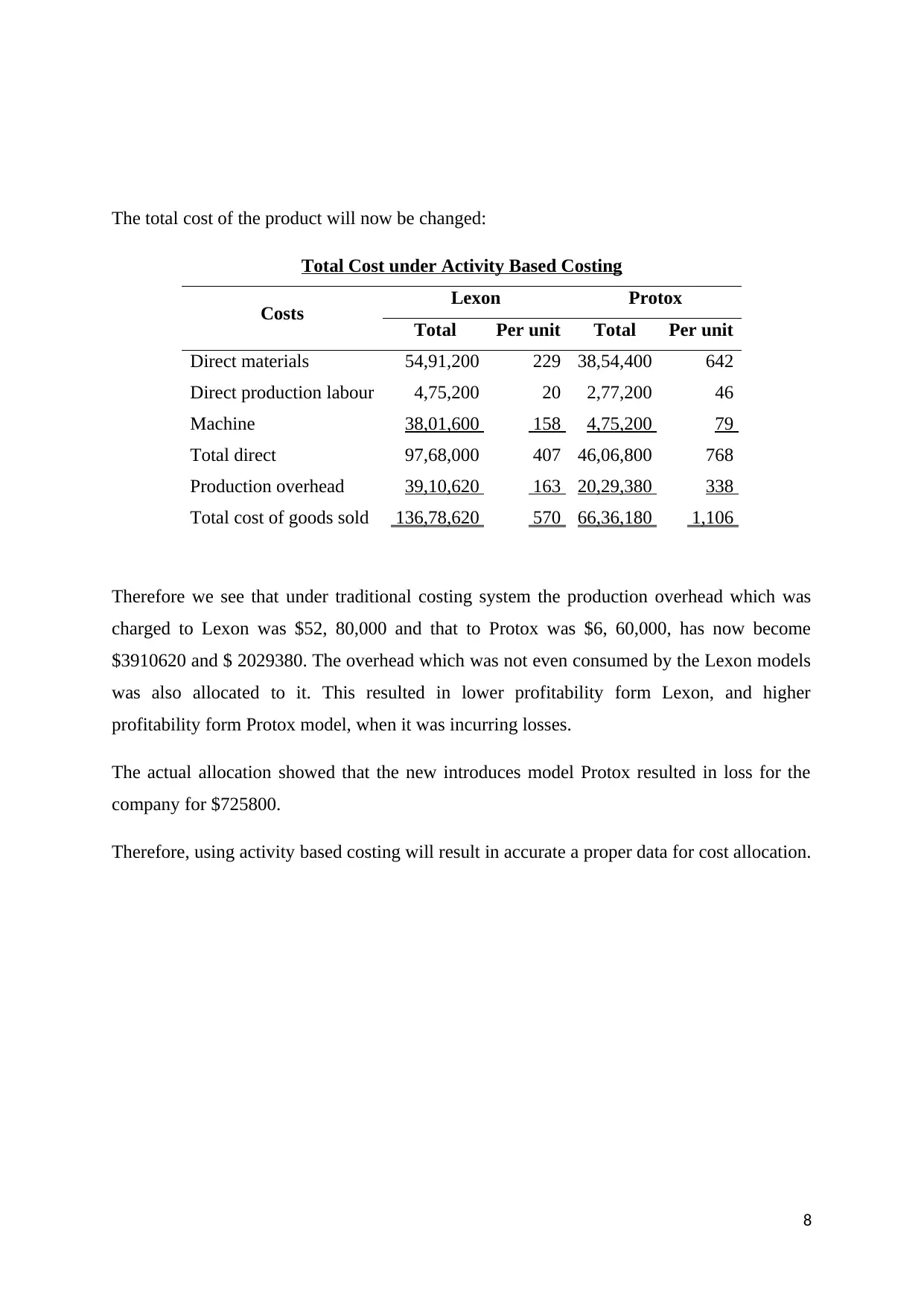

The total cost of the product will now be changed:

Total Cost under Activity Based Costing

Costs Lexon Protox

Total Per unit Total Per unit

Direct materials 54,91,200 229 38,54,400 642

Direct production labour 4,75,200 20 2,77,200 46

Machine 38,01,600 158 4,75,200 79

Total direct 97,68,000 407 46,06,800 768

Production overhead 39,10,620 163 20,29,380 338

Total cost of goods sold 136,78,620 570 66,36,180 1,106

Therefore we see that under traditional costing system the production overhead which was

charged to Lexon was $52, 80,000 and that to Protox was $6, 60,000, has now become

$3910620 and $ 2029380. The overhead which was not even consumed by the Lexon models

was also allocated to it. This resulted in lower profitability form Lexon, and higher

profitability form Protox model, when it was incurring losses.

The actual allocation showed that the new introduces model Protox resulted in loss for the

company for $725800.

Therefore, using activity based costing will result in accurate a proper data for cost allocation.

8

Total Cost under Activity Based Costing

Costs Lexon Protox

Total Per unit Total Per unit

Direct materials 54,91,200 229 38,54,400 642

Direct production labour 4,75,200 20 2,77,200 46

Machine 38,01,600 158 4,75,200 79

Total direct 97,68,000 407 46,06,800 768

Production overhead 39,10,620 163 20,29,380 338

Total cost of goods sold 136,78,620 570 66,36,180 1,106

Therefore we see that under traditional costing system the production overhead which was

charged to Lexon was $52, 80,000 and that to Protox was $6, 60,000, has now become

$3910620 and $ 2029380. The overhead which was not even consumed by the Lexon models

was also allocated to it. This resulted in lower profitability form Lexon, and higher

profitability form Protox model, when it was incurring losses.

The actual allocation showed that the new introduces model Protox resulted in loss for the

company for $725800.

Therefore, using activity based costing will result in accurate a proper data for cost allocation.

8

Ethical dilemma in change of costing methods

In the given scenario we see that the CEO of the company Beztec Ltd, Steven Kay, is not

convinced that the activity based costing should be implemented. It is important that

decisions like these be taken based on the advantage of company and not for individual

advantage for the management.

Being an accountant it is important that Sue Smith carry professionalism and integrity in her

work. The APES 110 Code of ethics for professional accountant lay down that the work

conducted by the professional accountants should be carried with professional competence

and due care. She should also use professional scepticism in her work (Cochran, 2017). Her

understanding of applicability of Activity based costing is correct and she should continue

with it (Datar M. S., 2015).

Not reporting the overheads as per activity based costing will lead to projection that the

product Protox is profitable to the company, when in actual they line of Protox models have

been resulting in losses.

The management is likely to phase out the line with losses. But the CEO does not want Sue to

implement the activity based costing as it will phase out this line. The CEO has a personal

interest in the running of the segment of the Protox model. His bonus is dependent on the

revenues of the different divisions. Due to indulgence of his personal interest the decision

made by Kay becomes biased. The decision to report the numbers based on activity based

costing should be taken after taking into consideration the advantages it will generate to the

company (Siciliano, 2015).

9

In the given scenario we see that the CEO of the company Beztec Ltd, Steven Kay, is not

convinced that the activity based costing should be implemented. It is important that

decisions like these be taken based on the advantage of company and not for individual

advantage for the management.

Being an accountant it is important that Sue Smith carry professionalism and integrity in her

work. The APES 110 Code of ethics for professional accountant lay down that the work

conducted by the professional accountants should be carried with professional competence

and due care. She should also use professional scepticism in her work (Cochran, 2017). Her

understanding of applicability of Activity based costing is correct and she should continue

with it (Datar M. S., 2015).

Not reporting the overheads as per activity based costing will lead to projection that the

product Protox is profitable to the company, when in actual they line of Protox models have

been resulting in losses.

The management is likely to phase out the line with losses. But the CEO does not want Sue to

implement the activity based costing as it will phase out this line. The CEO has a personal

interest in the running of the segment of the Protox model. His bonus is dependent on the

revenues of the different divisions. Due to indulgence of his personal interest the decision

made by Kay becomes biased. The decision to report the numbers based on activity based

costing should be taken after taking into consideration the advantages it will generate to the

company (Siciliano, 2015).

9

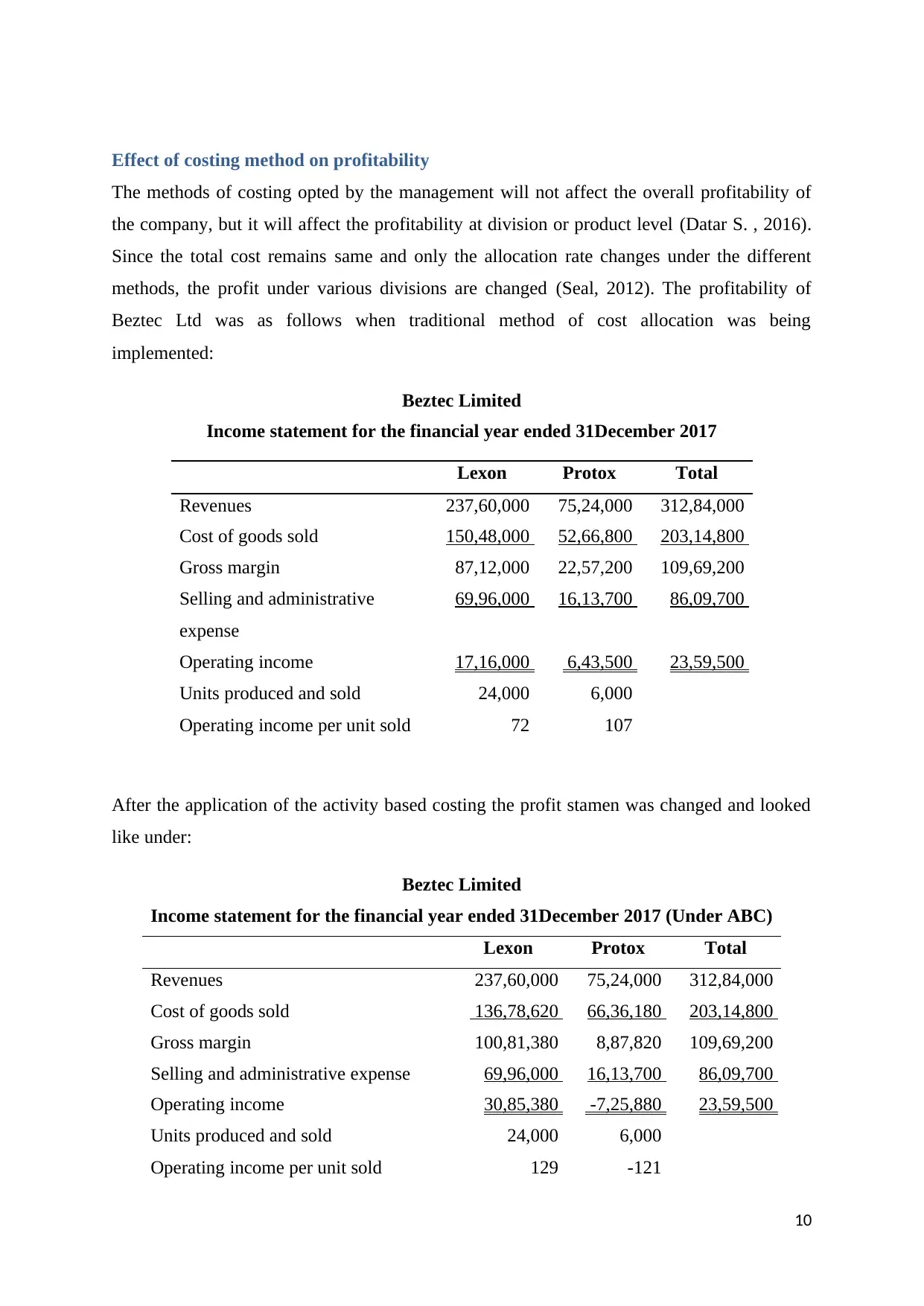

Effect of costing method on profitability

The methods of costing opted by the management will not affect the overall profitability of

the company, but it will affect the profitability at division or product level (Datar S. , 2016).

Since the total cost remains same and only the allocation rate changes under the different

methods, the profit under various divisions are changed (Seal, 2012). The profitability of

Beztec Ltd was as follows when traditional method of cost allocation was being

implemented:

Beztec Limited

Income statement for the financial year ended 31December 2017

Lexon Protox Total

Revenues 237,60,000 75,24,000 312,84,000

Cost of goods sold 150,48,000 52,66,800 203,14,800

Gross margin 87,12,000 22,57,200 109,69,200

Selling and administrative

expense

69,96,000 16,13,700 86,09,700

Operating income 17,16,000 6,43,500 23,59,500

Units produced and sold 24,000 6,000

Operating income per unit sold 72 107

After the application of the activity based costing the profit stamen was changed and looked

like under:

Beztec Limited

Income statement for the financial year ended 31December 2017 (Under ABC)

Lexon Protox Total

Revenues 237,60,000 75,24,000 312,84,000

Cost of goods sold 136,78,620 66,36,180 203,14,800

Gross margin 100,81,380 8,87,820 109,69,200

Selling and administrative expense 69,96,000 16,13,700 86,09,700

Operating income 30,85,380 -7,25,880 23,59,500

Units produced and sold 24,000 6,000

Operating income per unit sold 129 -121

10

The methods of costing opted by the management will not affect the overall profitability of

the company, but it will affect the profitability at division or product level (Datar S. , 2016).

Since the total cost remains same and only the allocation rate changes under the different

methods, the profit under various divisions are changed (Seal, 2012). The profitability of

Beztec Ltd was as follows when traditional method of cost allocation was being

implemented:

Beztec Limited

Income statement for the financial year ended 31December 2017

Lexon Protox Total

Revenues 237,60,000 75,24,000 312,84,000

Cost of goods sold 150,48,000 52,66,800 203,14,800

Gross margin 87,12,000 22,57,200 109,69,200

Selling and administrative

expense

69,96,000 16,13,700 86,09,700

Operating income 17,16,000 6,43,500 23,59,500

Units produced and sold 24,000 6,000

Operating income per unit sold 72 107

After the application of the activity based costing the profit stamen was changed and looked

like under:

Beztec Limited

Income statement for the financial year ended 31December 2017 (Under ABC)

Lexon Protox Total

Revenues 237,60,000 75,24,000 312,84,000

Cost of goods sold 136,78,620 66,36,180 203,14,800

Gross margin 100,81,380 8,87,820 109,69,200

Selling and administrative expense 69,96,000 16,13,700 86,09,700

Operating income 30,85,380 -7,25,880 23,59,500

Units produced and sold 24,000 6,000

Operating income per unit sold 129 -121

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

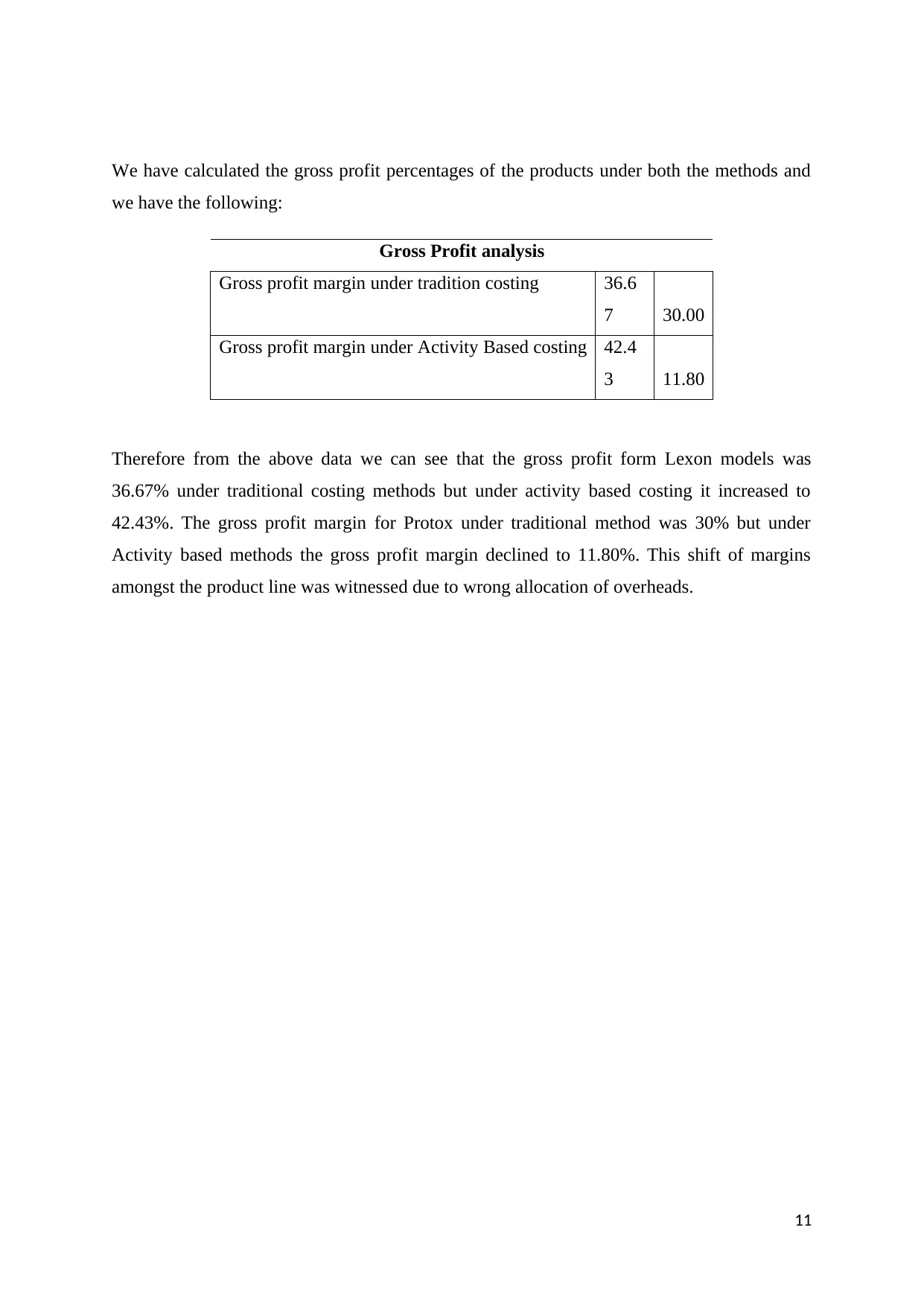

We have calculated the gross profit percentages of the products under both the methods and

we have the following:

Gross Profit analysis

Gross profit margin under tradition costing 36.6

7 30.00

Gross profit margin under Activity Based costing 42.4

3 11.80

Therefore from the above data we can see that the gross profit form Lexon models was

36.67% under traditional costing methods but under activity based costing it increased to

42.43%. The gross profit margin for Protox under traditional method was 30% but under

Activity based methods the gross profit margin declined to 11.80%. This shift of margins

amongst the product line was witnessed due to wrong allocation of overheads.

11

we have the following:

Gross Profit analysis

Gross profit margin under tradition costing 36.6

7 30.00

Gross profit margin under Activity Based costing 42.4

3 11.80

Therefore from the above data we can see that the gross profit form Lexon models was

36.67% under traditional costing methods but under activity based costing it increased to

42.43%. The gross profit margin for Protox under traditional method was 30% but under

Activity based methods the gross profit margin declined to 11.80%. This shift of margins

amongst the product line was witnessed due to wrong allocation of overheads.

11

Under and over recovery of overheads and there treatment

Under the traditional costing system the overhead allocated to the product are based on some

pre determine overhead rate, even before knowing how much expense are to be incurred. The

management budgets some expense in order to forecast the expense that could incur. Based

on the budgeted units that are expected to be produced and sold, the management divides

these expenses amongst these units. This is how a pre determined rate is calculated

(Strathern, 2010). There is a difference between pre determined and actual overhead rate. The

difference between these amounts is required to be adjusted in the books.

For example, the management expects that total $50000 would be incurred for overhead for

production of 10000 units, using this data we get the predetermined overhead rate as $5 per

unit. Now during the financial year they actually incur an expense of $50500 and produce

11000 units, this makes the overhead rate $4.60 per unit. The difference between the

allocated and actual overhead $0.40 per unit (5-4.6) is to be adjusted in the books.

In order to adjust the said difference there are certain methods which can be followed. The

adjustment in the books can be done in three ways:

- Adjusting the over/ under recovery in the existing units during the financial year:

under this system of adjustment of under and over recovery, the amount which needs to

be adjusted is allocated amongst the existing units produced during the year.

For example, if the amount of over/ under recovery to be adjusted is $10000, and total

2000 units are in stock then the amount of $5 per unit will be adjusted in the price of

these units.

This system of adjustment of recovery amounts is not very popularly used and

implemented, since it shifts the loan of overhead of some units on the other reaming

units. This creates a price difference. Also, implementation of this kind of adjustment is

very complex (Taillard, 2013).

- Adjusting the over/ under recovery by carrying forward the amount to the next

financial year: in the cost records when the overhead accounts are prepared, the

allocated recovery rate is first charged to them, and then the actual amount is transferred,

the reaming balance standing outstanding at the end of the year in these accounts are

carried forward to next year. The overhead rate allocated to the new units is revised in

order to adjust this opening amount. This system of adjustment always has some

12

Under the traditional costing system the overhead allocated to the product are based on some

pre determine overhead rate, even before knowing how much expense are to be incurred. The

management budgets some expense in order to forecast the expense that could incur. Based

on the budgeted units that are expected to be produced and sold, the management divides

these expenses amongst these units. This is how a pre determined rate is calculated

(Strathern, 2010). There is a difference between pre determined and actual overhead rate. The

difference between these amounts is required to be adjusted in the books.

For example, the management expects that total $50000 would be incurred for overhead for

production of 10000 units, using this data we get the predetermined overhead rate as $5 per

unit. Now during the financial year they actually incur an expense of $50500 and produce

11000 units, this makes the overhead rate $4.60 per unit. The difference between the

allocated and actual overhead $0.40 per unit (5-4.6) is to be adjusted in the books.

In order to adjust the said difference there are certain methods which can be followed. The

adjustment in the books can be done in three ways:

- Adjusting the over/ under recovery in the existing units during the financial year:

under this system of adjustment of under and over recovery, the amount which needs to

be adjusted is allocated amongst the existing units produced during the year.

For example, if the amount of over/ under recovery to be adjusted is $10000, and total

2000 units are in stock then the amount of $5 per unit will be adjusted in the price of

these units.

This system of adjustment of recovery amounts is not very popularly used and

implemented, since it shifts the loan of overhead of some units on the other reaming

units. This creates a price difference. Also, implementation of this kind of adjustment is

very complex (Taillard, 2013).

- Adjusting the over/ under recovery by carrying forward the amount to the next

financial year: in the cost records when the overhead accounts are prepared, the

allocated recovery rate is first charged to them, and then the actual amount is transferred,

the reaming balance standing outstanding at the end of the year in these accounts are

carried forward to next year. The overhead rate allocated to the new units is revised in

order to adjust this opening amount. This system of adjustment always has some

12

difference standing in the books. Since this does account for expense in appropriate

manner this method is not very popular.

- Adjusting the over/ under recover by transferring to the profit and loss statement:

this is the most popularly used and the most implemented way to adjust the under and

over recovery amounts. Under this method the difference between the allocation and

actual amount is directly carried forward to the profit and loss statement. The profits is

adjusted for the expenses in the year in which they are incurred, this helps in presentation

of correct data in the books of account, also this is a very simple way to adjust the

differences. Hence, this system is most widely used.

Therefore the management can deal with under/ over recovery of overheads by the method

which is most suitable to them.

13

manner this method is not very popular.

- Adjusting the over/ under recover by transferring to the profit and loss statement:

this is the most popularly used and the most implemented way to adjust the under and

over recovery amounts. Under this method the difference between the allocation and

actual amount is directly carried forward to the profit and loss statement. The profits is

adjusted for the expenses in the year in which they are incurred, this helps in presentation

of correct data in the books of account, also this is a very simple way to adjust the

differences. Hence, this system is most widely used.

Therefore the management can deal with under/ over recovery of overheads by the method

which is most suitable to them.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conclusion and Recommendation

From the above discussion we can see that the product Lexon was generating profits for the

company but Protox has been incurring losses. Implementation of activity based costing helps

us analyse the cost data more appropriately. Implementation of traditional costing by the

company will lead to wrong decision making by the management. This will harm the future

viability of the company’s performance. If the company continues to produce Protox, it will

keep incurring losses. Continuing the loss will harm the financial position of the company.

We would recommend Sue to implement the activity based costing as it helps to present the

correct data to the management. Management should also consider data based on activity

based costing as it is more authenticated form of cost allocation. Eradicating the production

of Protox model will be in the interest of the company and hence same should be moved

forward with.

14

From the above discussion we can see that the product Lexon was generating profits for the

company but Protox has been incurring losses. Implementation of activity based costing helps

us analyse the cost data more appropriately. Implementation of traditional costing by the

company will lead to wrong decision making by the management. This will harm the future

viability of the company’s performance. If the company continues to produce Protox, it will

keep incurring losses. Continuing the loss will harm the financial position of the company.

We would recommend Sue to implement the activity based costing as it helps to present the

correct data to the management. Management should also consider data based on activity

based costing as it is more authenticated form of cost allocation. Eradicating the production

of Protox model will be in the interest of the company and hence same should be moved

forward with.

14

Bibliography

Atkinson, A. A. (2012). Management accounting. Upper Saddle River, N.J.: Paerson.

Berry, L. E. (2009). Management accounting demystified. New York: McGraw-Hill.

Boyd, W. K. (2013). Cost Accounting For Dummies. Hoboken: Wiley.

Cochran, C. (2017). Internal auditing in plain English. Chico, California: Paton Professional.

Datar, M. S. (2015). Cost accounting. Boston: Pearson.

Datar, S. (2016). Horngren's Cost Accounting: A Managerial Emphasis. Hoboken: Wiley.

Holtzman, M. (2013). Managerial Accounting For Dummies. Hoboken, NJ: Wiley.

Horngren, C. (2012). Cost accounting. Upper Saddle River, N.J.: Pearson/Prentice Hall.

Menifield, C. E. (2014). The Basics of Public Budgeting and Financial Management: A

Handbook for Academics and Practitioners. Lanham, Md.: University Press of America.

Noreen, E. (2015). The theory of constraints and its implications for management accounting.

Great Barrington, MA: North River Press.

Raun, D. L. (1962). What is Accounting? The Accounting Review , 769-773.

Seal, W. (2012). Management accounting. Maidenhead: McGraw-Hill Higher Education.

Siciliano, G. (2015). Finance for Nonfinancial Managers. New York: McGraw-Hill.

Strathern, M. (2010). Audit cultures: anthropological studies in accountability, ethics and the

academy. London: Routledge.

Taillard, M. (2013). Corporate finance for dummies. Hoboken, N.J.: Wiley.

White, T. S. (2009). The 60 minute ABC book. Bedford: Consortium for Advanced

Manufacturing International.

15

Atkinson, A. A. (2012). Management accounting. Upper Saddle River, N.J.: Paerson.

Berry, L. E. (2009). Management accounting demystified. New York: McGraw-Hill.

Boyd, W. K. (2013). Cost Accounting For Dummies. Hoboken: Wiley.

Cochran, C. (2017). Internal auditing in plain English. Chico, California: Paton Professional.

Datar, M. S. (2015). Cost accounting. Boston: Pearson.

Datar, S. (2016). Horngren's Cost Accounting: A Managerial Emphasis. Hoboken: Wiley.

Holtzman, M. (2013). Managerial Accounting For Dummies. Hoboken, NJ: Wiley.

Horngren, C. (2012). Cost accounting. Upper Saddle River, N.J.: Pearson/Prentice Hall.

Menifield, C. E. (2014). The Basics of Public Budgeting and Financial Management: A

Handbook for Academics and Practitioners. Lanham, Md.: University Press of America.

Noreen, E. (2015). The theory of constraints and its implications for management accounting.

Great Barrington, MA: North River Press.

Raun, D. L. (1962). What is Accounting? The Accounting Review , 769-773.

Seal, W. (2012). Management accounting. Maidenhead: McGraw-Hill Higher Education.

Siciliano, G. (2015). Finance for Nonfinancial Managers. New York: McGraw-Hill.

Strathern, M. (2010). Audit cultures: anthropological studies in accountability, ethics and the

academy. London: Routledge.

Taillard, M. (2013). Corporate finance for dummies. Hoboken, N.J.: Wiley.

White, T. S. (2009). The 60 minute ABC book. Bedford: Consortium for Advanced

Manufacturing International.

15

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.