Management Accounting

VerifiedAdded on 2023/01/12

|19

|2720

|81

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management

Accounting

1

Accounting

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTRODUCTION

Management accounting is also known as managerial accounting and could be described as

a procedure of providing the managers with financial information and resources when making

decisions (Akbar, 2010). Management accounting is used primarily by the organisation's

2

Management accounting is also known as managerial accounting and could be described as

a procedure of providing the managers with financial information and resources when making

decisions (Akbar, 2010). Management accounting is used primarily by the organisation's

2

management department, and that is the only thing that makes it distinct from financial

accounting. This assignment based on UCK Furniture which is UK based company.

This report includes the various topics such as demonstration of management accounting

system and it include the range of techniques to produce income statement by using appropriate

methods. In addition, it also covers the use of planning tools in management accounting and the

way organizations used to respond their financial problems.

MAIN BODY

PART 1

Section 1

1.1 Explain management accounting and present the essential requirements of different types of

management accounting systems

According to the Institute of Cost and Management Accounting, application of

professional skills in order to manage accounting information in that way which provide useful

information (Callahan, Stetz and Brooks, 2011). By using management accounting, managers

able to formulate policies and build plan to control entire operational activity of organization.

UCK Furniture follow the range of management accounting systems that is essentially required

to maximise their overall productivity and profitability are as follow:

Inventory management system: It is a primarily a discipline which specifies the structure

and positioning of stocked products. It is important to immediately follow the standard and

scheduled course of production and stock of materials at various locations within a facility or

within several locations of a supply network. It is a computer-based system used to monitor

inventory rates, purchases, deliveries, and orders (Hopper and Bui, 2016). This system is used in

the manufacturing sector in some situations to produce a work order, bill of materials, and other

supplies relevant to the product. It is essentially required by UCK Furniture to reduce inventory

over-storage and under-stocking problems.

Job costing system: It is a method of determining the costs they spend to a particular job

that is associated with company. This term is commonly used in the construction industry, which

refers to the distribution of costs at a corporation for specific building projects. Most of the

organizations used this accounting system to set separate cost for each job that is essentially

3

accounting. This assignment based on UCK Furniture which is UK based company.

This report includes the various topics such as demonstration of management accounting

system and it include the range of techniques to produce income statement by using appropriate

methods. In addition, it also covers the use of planning tools in management accounting and the

way organizations used to respond their financial problems.

MAIN BODY

PART 1

Section 1

1.1 Explain management accounting and present the essential requirements of different types of

management accounting systems

According to the Institute of Cost and Management Accounting, application of

professional skills in order to manage accounting information in that way which provide useful

information (Callahan, Stetz and Brooks, 2011). By using management accounting, managers

able to formulate policies and build plan to control entire operational activity of organization.

UCK Furniture follow the range of management accounting systems that is essentially required

to maximise their overall productivity and profitability are as follow:

Inventory management system: It is a primarily a discipline which specifies the structure

and positioning of stocked products. It is important to immediately follow the standard and

scheduled course of production and stock of materials at various locations within a facility or

within several locations of a supply network. It is a computer-based system used to monitor

inventory rates, purchases, deliveries, and orders (Hopper and Bui, 2016). This system is used in

the manufacturing sector in some situations to produce a work order, bill of materials, and other

supplies relevant to the product. It is essentially required by UCK Furniture to reduce inventory

over-storage and under-stocking problems.

Job costing system: It is a method of determining the costs they spend to a particular job

that is associated with company. This term is commonly used in the construction industry, which

refers to the distribution of costs at a corporation for specific building projects. Most of the

organizations used this accounting system to set separate cost for each job that is essentially

3

required to minimise the production cost which further helps in maximising productivity as well

as profitability of UCK Furniture company.

Price optimisation: This system used to seeking the perfect spot pricing or price

maximization against consumer willingness to pay. Business up and down the supply chain, both

in B2B and B2C environments, rightly devote a considerable amount of time to market

management and ensure that their goods are delivered efficiently at the right price while still

making decent profits. It is essential for UCK Furniture to meet their consumer expectation

through fulfilling business objectives.

Above mention management accounting systems helps UCK Furniture to manage their

financial information which required by top management to take further decisions or build

strategies for the development of the business (Lavia López and Hiebl, 2014). It is used to

maximise productivity or profitability through improving overall performance of business

operations.

1.2 Explain different methods used for management accounting reporting

Performance report: This report is produced to assess a company's performance as a

whole and at the end of a year, for each employee. In large organizations even various

departments’ performance reports are produced. These success analyses are used by managers to

make important business decisions about the organisation's future. People are often rewarded for

their contribution to the company, and are laid off or treated as needed under performers.

Managers of UCK Furniture use this report to evaluate their overall organizational or employees

performance and further build strategies accordingly to improve the outcomes.

Cost managerial accounting report: Managerial accounting measures the prices of the

manufactured products. All the prices of raw materials, overheads, wages and any other prices

are taken into account. The sums are divided by the quantities generated. Managers of UCK

Furniture get the opportunity to understand products ' purchase prices against their value for sale.

Through these reports, profit margins are calculated and tracked, due to have a good picture of

all the costs involved in the development or procurement of the posts. Production loss, daily

labour costs and operating expenses are all part of cost accounting reports for managers. They

have a clear view of all costs, which is important for better source of information optimisation in

all departments.

4

as profitability of UCK Furniture company.

Price optimisation: This system used to seeking the perfect spot pricing or price

maximization against consumer willingness to pay. Business up and down the supply chain, both

in B2B and B2C environments, rightly devote a considerable amount of time to market

management and ensure that their goods are delivered efficiently at the right price while still

making decent profits. It is essential for UCK Furniture to meet their consumer expectation

through fulfilling business objectives.

Above mention management accounting systems helps UCK Furniture to manage their

financial information which required by top management to take further decisions or build

strategies for the development of the business (Lavia López and Hiebl, 2014). It is used to

maximise productivity or profitability through improving overall performance of business

operations.

1.2 Explain different methods used for management accounting reporting

Performance report: This report is produced to assess a company's performance as a

whole and at the end of a year, for each employee. In large organizations even various

departments’ performance reports are produced. These success analyses are used by managers to

make important business decisions about the organisation's future. People are often rewarded for

their contribution to the company, and are laid off or treated as needed under performers.

Managers of UCK Furniture use this report to evaluate their overall organizational or employees

performance and further build strategies accordingly to improve the outcomes.

Cost managerial accounting report: Managerial accounting measures the prices of the

manufactured products. All the prices of raw materials, overheads, wages and any other prices

are taken into account. The sums are divided by the quantities generated. Managers of UCK

Furniture get the opportunity to understand products ' purchase prices against their value for sale.

Through these reports, profit margins are calculated and tracked, due to have a good picture of

all the costs involved in the development or procurement of the posts. Production loss, daily

labour costs and operating expenses are all part of cost accounting reports for managers. They

have a clear view of all costs, which is important for better source of information optimisation in

all departments.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

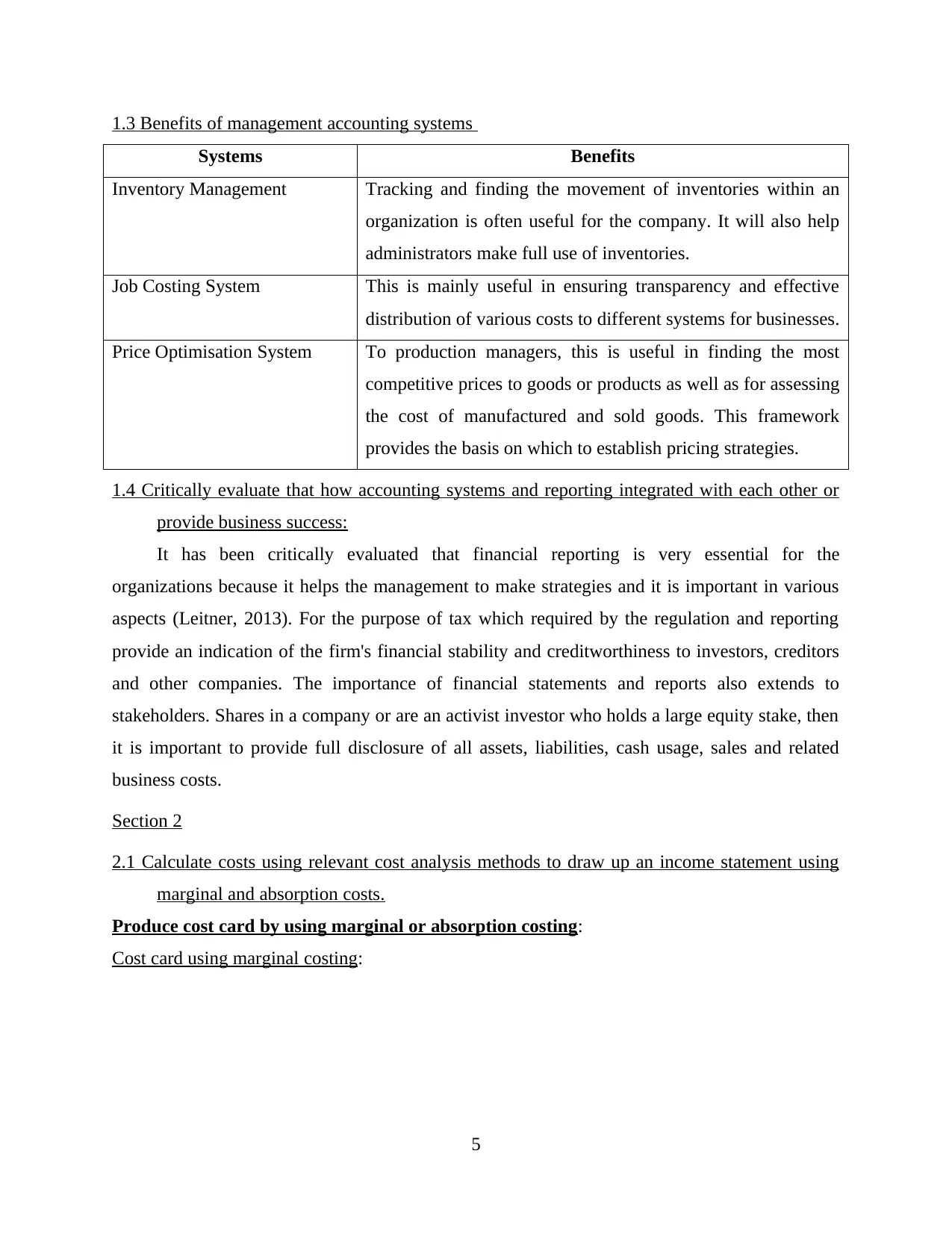

1.3 Benefits of management accounting systems

Systems Benefits

Inventory Management Tracking and finding the movement of inventories within an

organization is often useful for the company. It will also help

administrators make full use of inventories.

Job Costing System This is mainly useful in ensuring transparency and effective

distribution of various costs to different systems for businesses.

Price Optimisation System To production managers, this is useful in finding the most

competitive prices to goods or products as well as for assessing

the cost of manufactured and sold goods. This framework

provides the basis on which to establish pricing strategies.

1.4 Critically evaluate that how accounting systems and reporting integrated with each other or

provide business success:

It has been critically evaluated that financial reporting is very essential for the

organizations because it helps the management to make strategies and it is important in various

aspects (Leitner, 2013). For the purpose of tax which required by the regulation and reporting

provide an indication of the firm's financial stability and creditworthiness to investors, creditors

and other companies. The importance of financial statements and reports also extends to

stakeholders. Shares in a company or are an activist investor who holds a large equity stake, then

it is important to provide full disclosure of all assets, liabilities, cash usage, sales and related

business costs.

Section 2

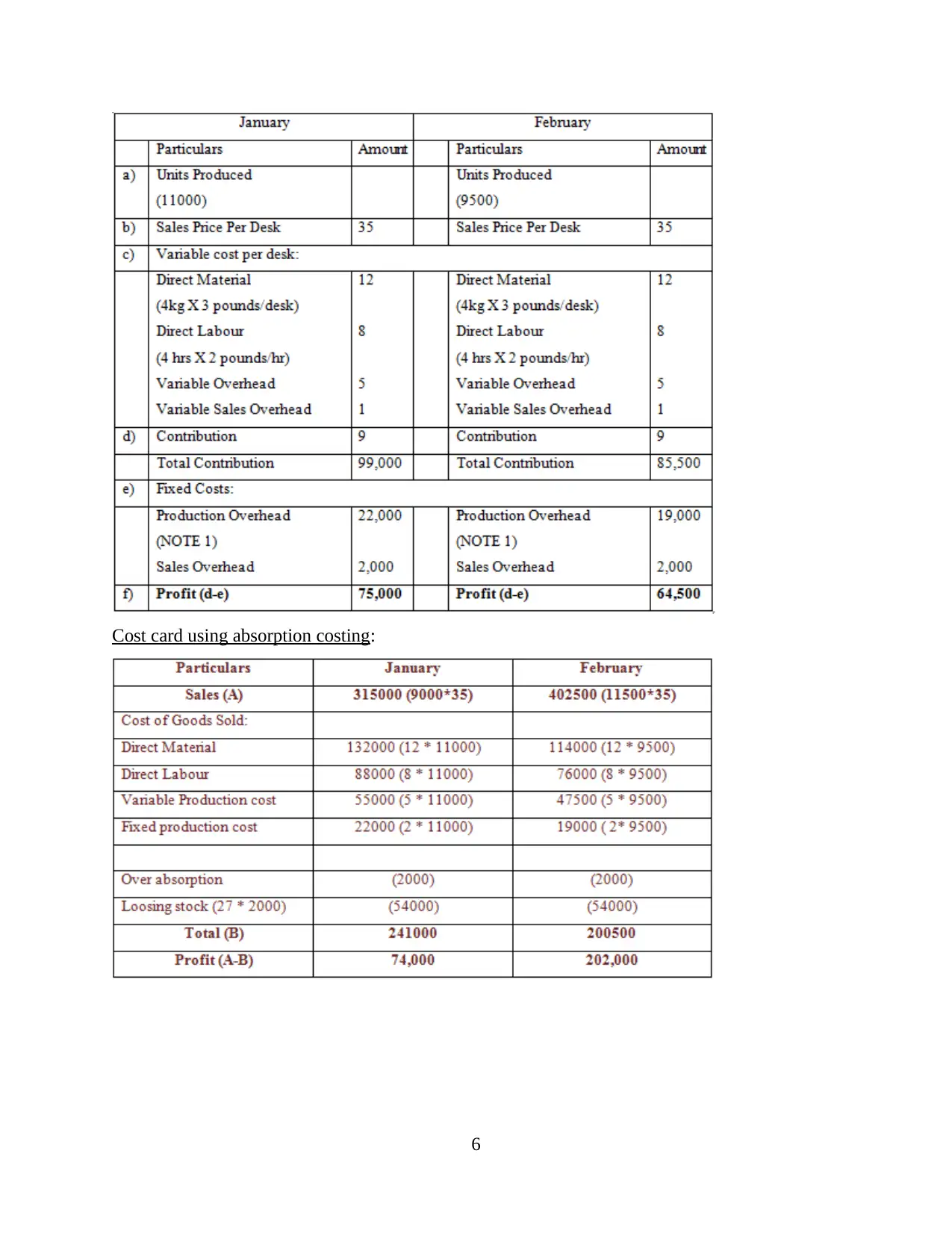

2.1 Calculate costs using relevant cost analysis methods to draw up an income statement using

marginal and absorption costs.

Produce cost card by using marginal or absorption costing:

Cost card using marginal costing:

5

Systems Benefits

Inventory Management Tracking and finding the movement of inventories within an

organization is often useful for the company. It will also help

administrators make full use of inventories.

Job Costing System This is mainly useful in ensuring transparency and effective

distribution of various costs to different systems for businesses.

Price Optimisation System To production managers, this is useful in finding the most

competitive prices to goods or products as well as for assessing

the cost of manufactured and sold goods. This framework

provides the basis on which to establish pricing strategies.

1.4 Critically evaluate that how accounting systems and reporting integrated with each other or

provide business success:

It has been critically evaluated that financial reporting is very essential for the

organizations because it helps the management to make strategies and it is important in various

aspects (Leitner, 2013). For the purpose of tax which required by the regulation and reporting

provide an indication of the firm's financial stability and creditworthiness to investors, creditors

and other companies. The importance of financial statements and reports also extends to

stakeholders. Shares in a company or are an activist investor who holds a large equity stake, then

it is important to provide full disclosure of all assets, liabilities, cash usage, sales and related

business costs.

Section 2

2.1 Calculate costs using relevant cost analysis methods to draw up an income statement using

marginal and absorption costs.

Produce cost card by using marginal or absorption costing:

Cost card using marginal costing:

5

Cost card using absorption costing:

6

6

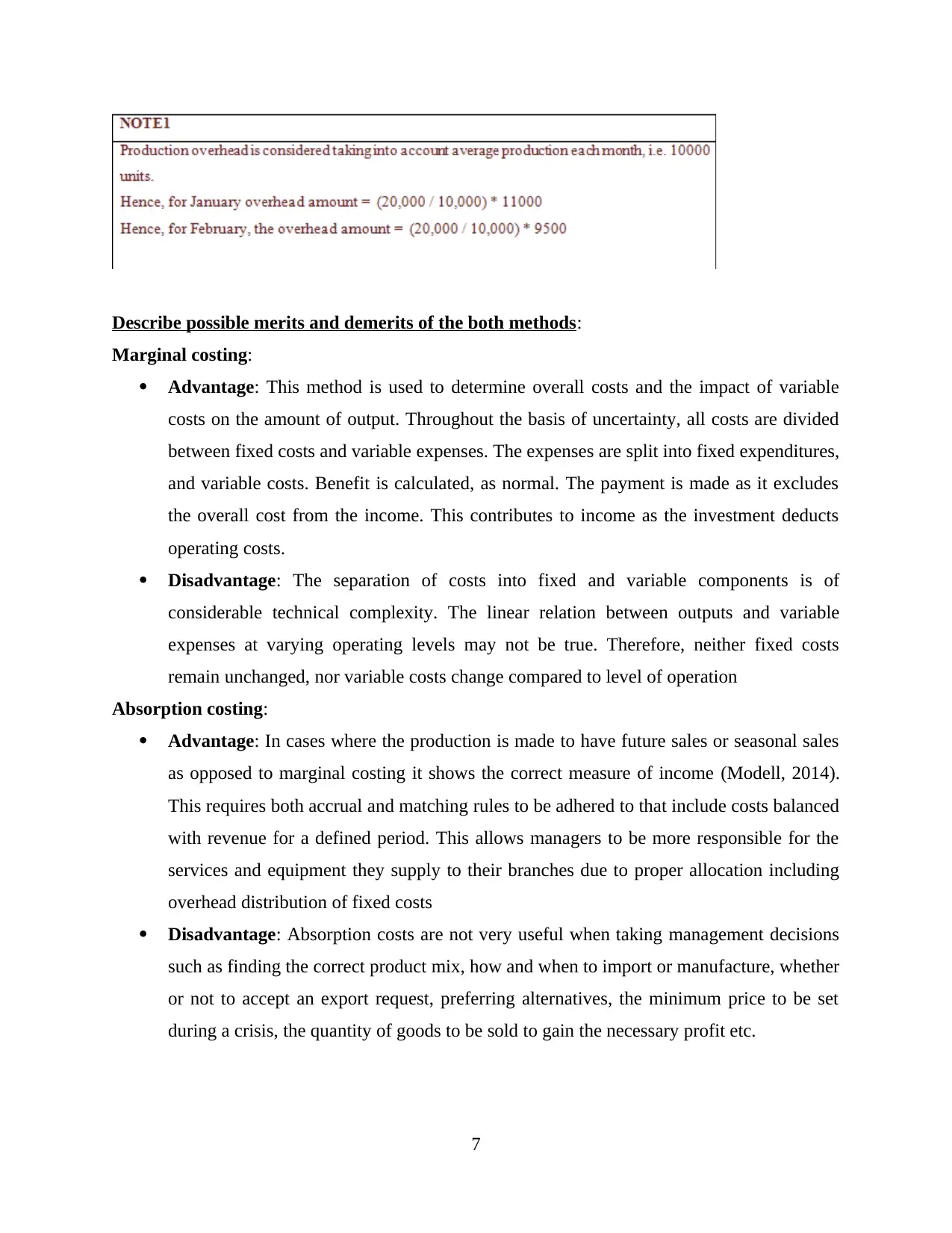

Describe possible merits and demerits of the both methods:

Marginal costing:

Advantage: This method is used to determine overall costs and the impact of variable

costs on the amount of output. Throughout the basis of uncertainty, all costs are divided

between fixed costs and variable expenses. The expenses are split into fixed expenditures,

and variable costs. Benefit is calculated, as normal. The payment is made as it excludes

the overall cost from the income. This contributes to income as the investment deducts

operating costs.

Disadvantage: The separation of costs into fixed and variable components is of

considerable technical complexity. The linear relation between outputs and variable

expenses at varying operating levels may not be true. Therefore, neither fixed costs

remain unchanged, nor variable costs change compared to level of operation

Absorption costing:

Advantage: In cases where the production is made to have future sales or seasonal sales

as opposed to marginal costing it shows the correct measure of income (Modell, 2014).

This requires both accrual and matching rules to be adhered to that include costs balanced

with revenue for a defined period. This allows managers to be more responsible for the

services and equipment they supply to their branches due to proper allocation including

overhead distribution of fixed costs

Disadvantage: Absorption costs are not very useful when taking management decisions

such as finding the correct product mix, how and when to import or manufacture, whether

or not to accept an export request, preferring alternatives, the minimum price to be set

during a crisis, the quantity of goods to be sold to gain the necessary profit etc.

7

Marginal costing:

Advantage: This method is used to determine overall costs and the impact of variable

costs on the amount of output. Throughout the basis of uncertainty, all costs are divided

between fixed costs and variable expenses. The expenses are split into fixed expenditures,

and variable costs. Benefit is calculated, as normal. The payment is made as it excludes

the overall cost from the income. This contributes to income as the investment deducts

operating costs.

Disadvantage: The separation of costs into fixed and variable components is of

considerable technical complexity. The linear relation between outputs and variable

expenses at varying operating levels may not be true. Therefore, neither fixed costs

remain unchanged, nor variable costs change compared to level of operation

Absorption costing:

Advantage: In cases where the production is made to have future sales or seasonal sales

as opposed to marginal costing it shows the correct measure of income (Modell, 2014).

This requires both accrual and matching rules to be adhered to that include costs balanced

with revenue for a defined period. This allows managers to be more responsible for the

services and equipment they supply to their branches due to proper allocation including

overhead distribution of fixed costs

Disadvantage: Absorption costs are not very useful when taking management decisions

such as finding the correct product mix, how and when to import or manufacture, whether

or not to accept an export request, preferring alternatives, the minimum price to be set

during a crisis, the quantity of goods to be sold to gain the necessary profit etc.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

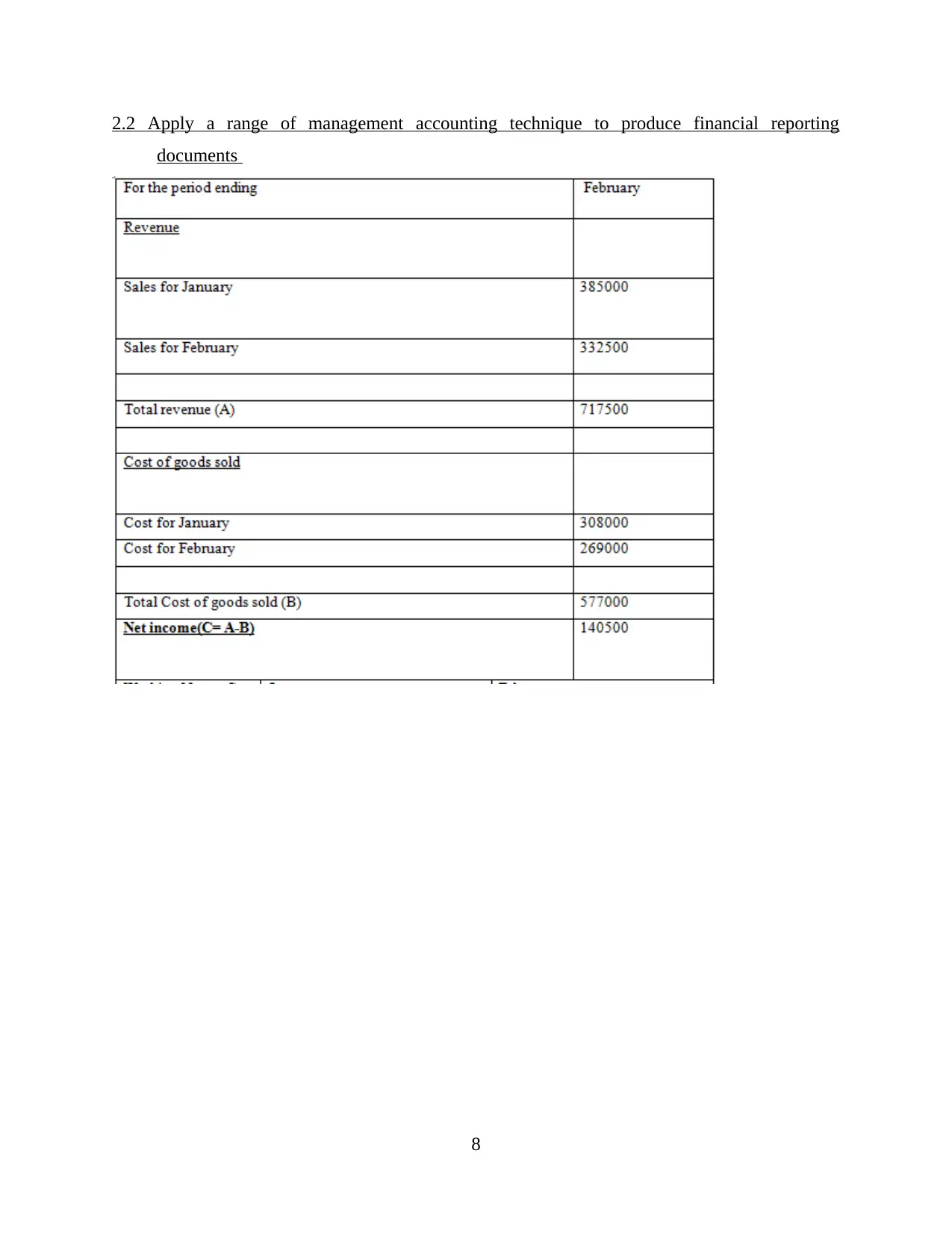

2.2 Apply a range of management accounting technique to produce financial reporting

documents

8

documents

8

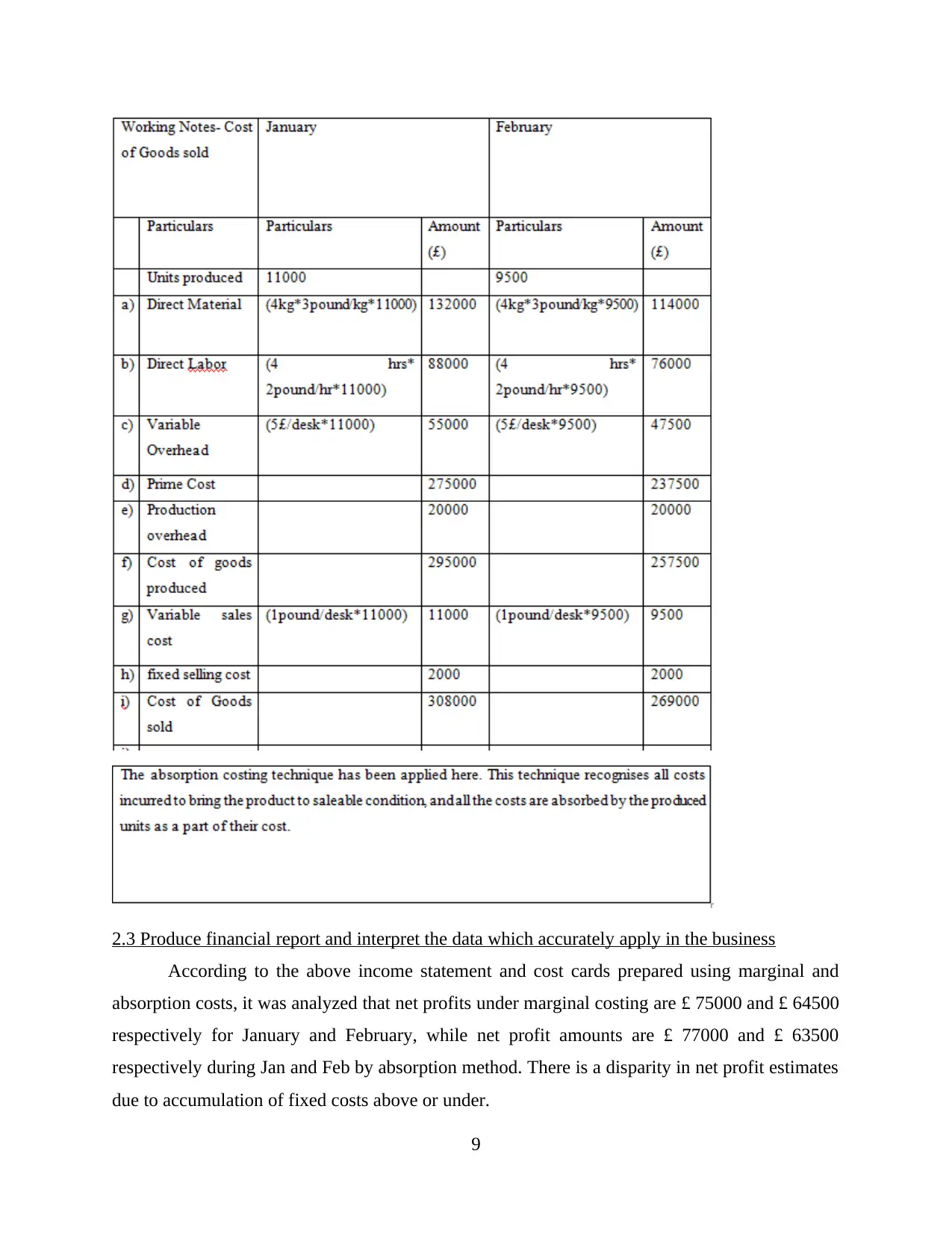

2.3 Produce financial report and interpret the data which accurately apply in the business

According to the above income statement and cost cards prepared using marginal and

absorption costs, it was analyzed that net profits under marginal costing are £ 75000 and £ 64500

respectively for January and February, while net profit amounts are £ 77000 and £ 63500

respectively during Jan and Feb by absorption method. There is a disparity in net profit estimates

due to accumulation of fixed costs above or under.

9

According to the above income statement and cost cards prepared using marginal and

absorption costs, it was analyzed that net profits under marginal costing are £ 75000 and £ 64500

respectively for January and February, while net profit amounts are £ 77000 and £ 63500

respectively during Jan and Feb by absorption method. There is a disparity in net profit estimates

due to accumulation of fixed costs above or under.

9

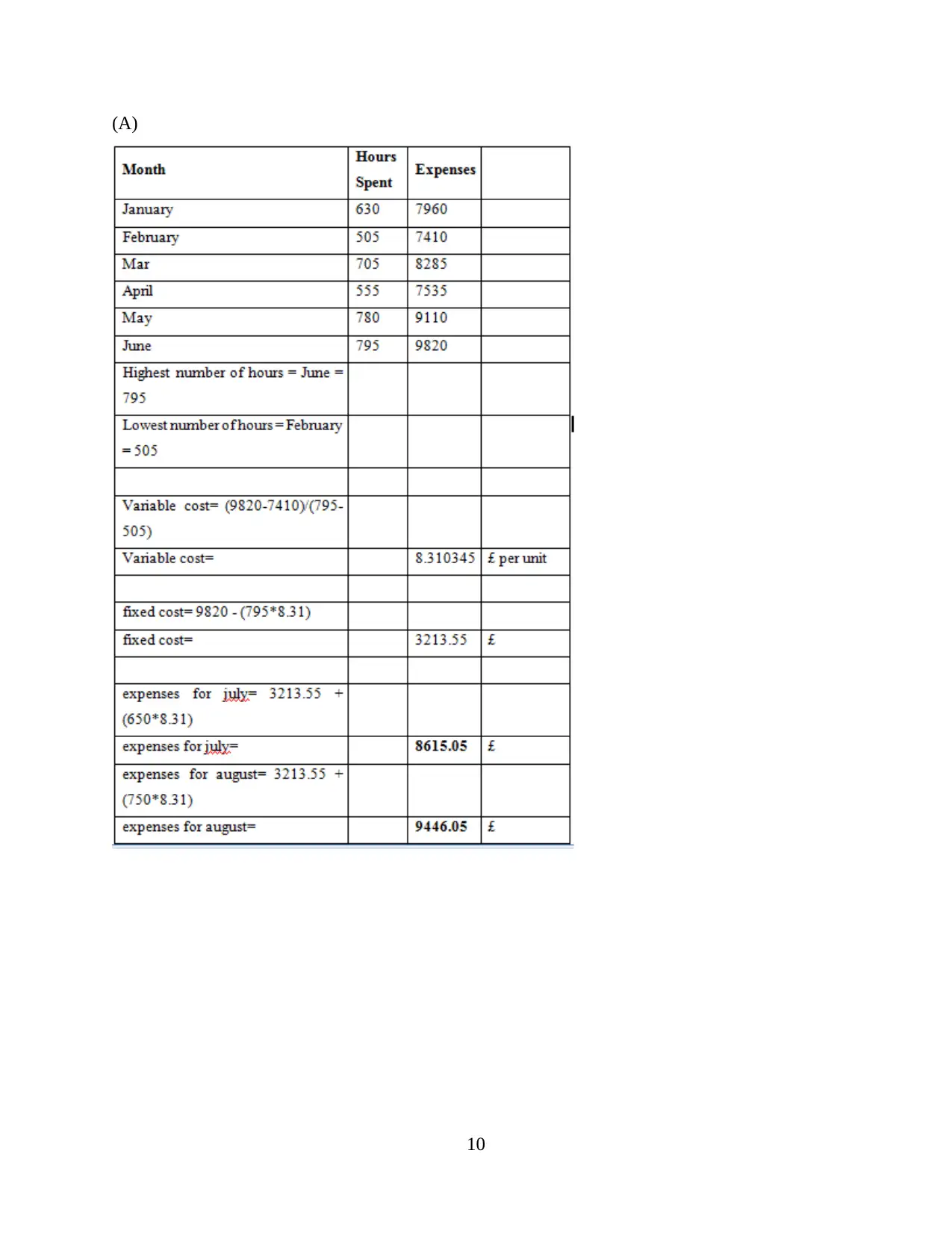

(A)

10

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

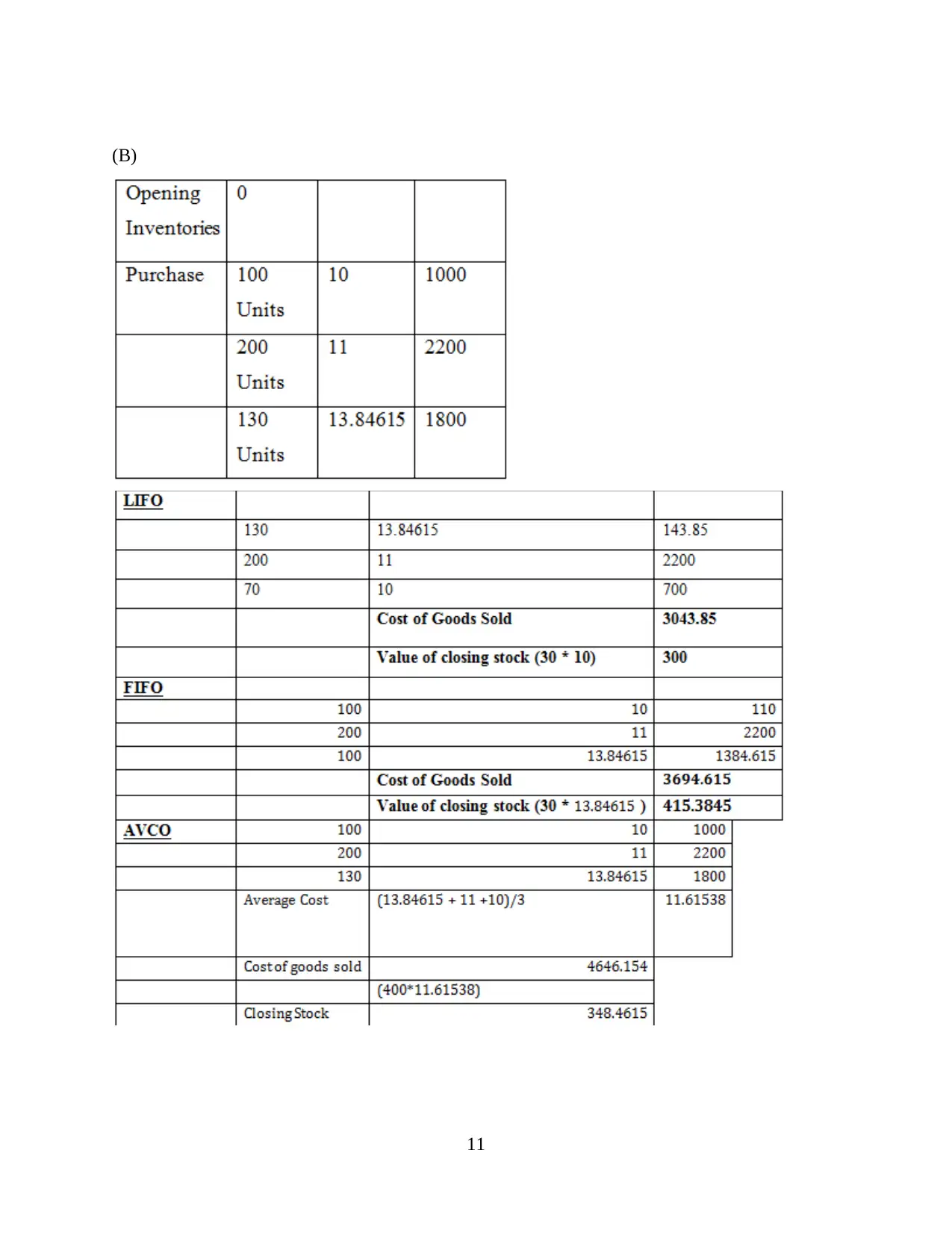

(B)

11

11

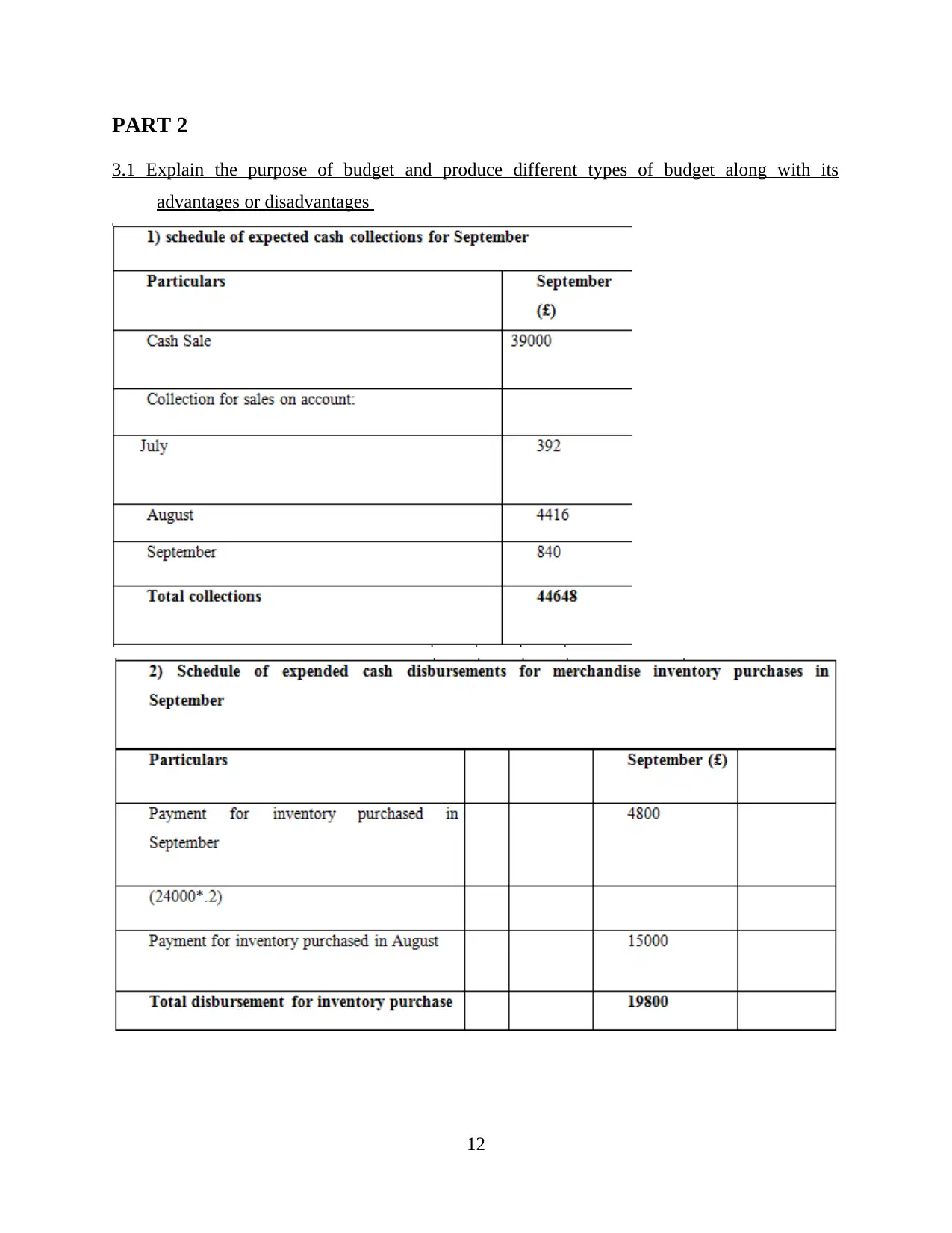

PART 2

3.1 Explain the purpose of budget and produce different types of budget along with its

advantages or disadvantages

12

3.1 Explain the purpose of budget and produce different types of budget along with its

advantages or disadvantages

12

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

14

Purpose of Budget: There are mainly three purpose of budgeting which encourages

organization to produce budget and estimate their activity cost accordingly. All are mentioned

below:

Projection of income and expenses: Budgeting is a vital aspect of the strategic cycle for

enterprises. Company owners and managers must be able to determine whether or not a business

is making a profit (Senftlechner and Hiebl, 2015). Purpose of the budgeting is essentially to

provide Managers of UCK furniture tries to estimate revenue and expenditure and therefore

productivity at the time of developing business plan. It helps in estimating how the company will

work financially if certain policies, events, plan is carried out.

Used for decision making process: Main purpose of budgeting is to have a financial

structure for the decision-making process i.e. something that we have prepared for or not is the

proposed direction action. Expenditure needs to be closely managed when running a company

responsibly. Once the marketing budget has been completely invested, the decision on "will they

spend money on ads" would probably be "no"

Monitor business performance: Budgeting is intended to allow the actual business

performance to be calculated against the company performance prediction, i.e. the business that

lives up to our expectations.

Due to above mention budgeting purpose, UCK furniture produce budget and take all the

advantages which they can or manage their spending patter.

Types of budgets:

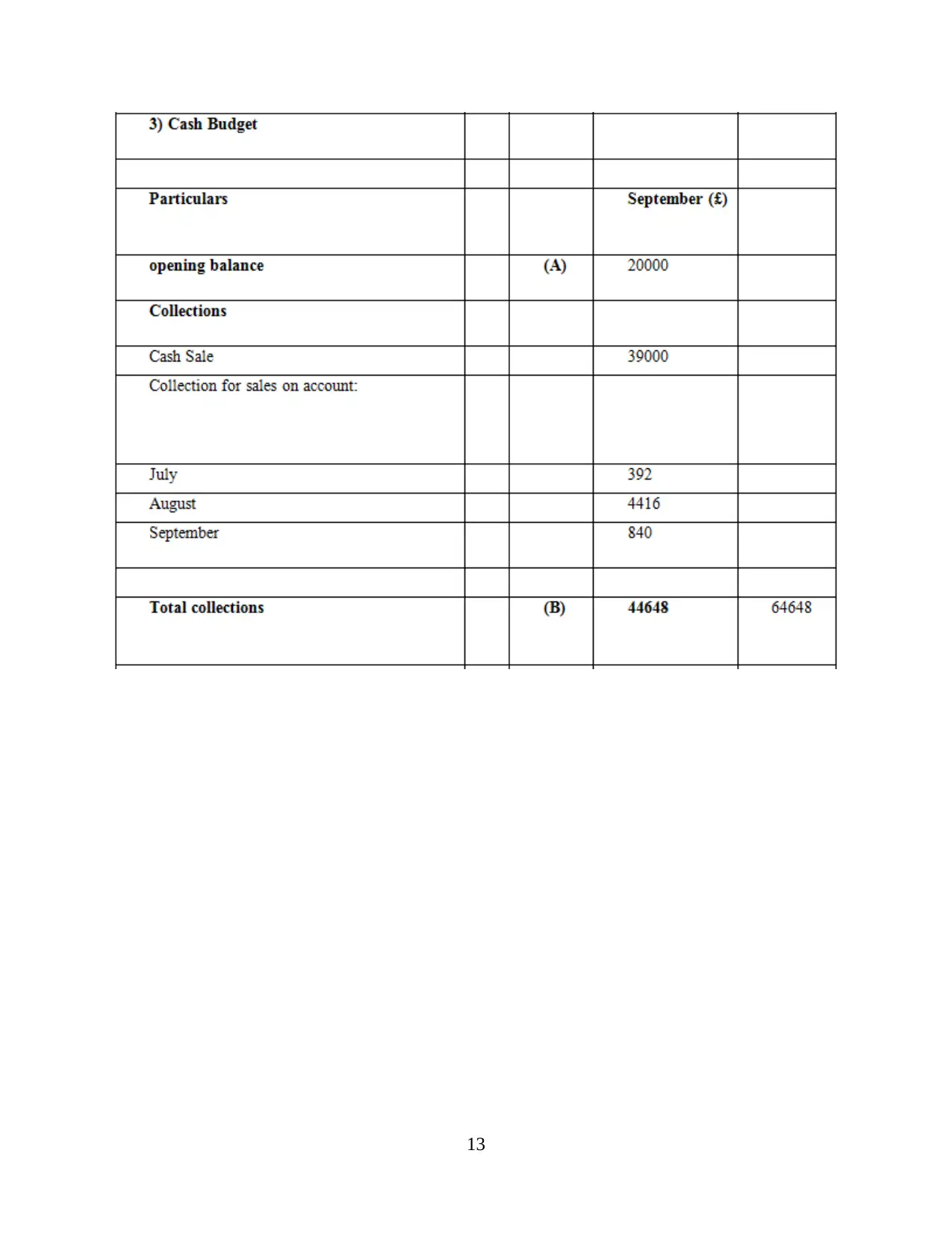

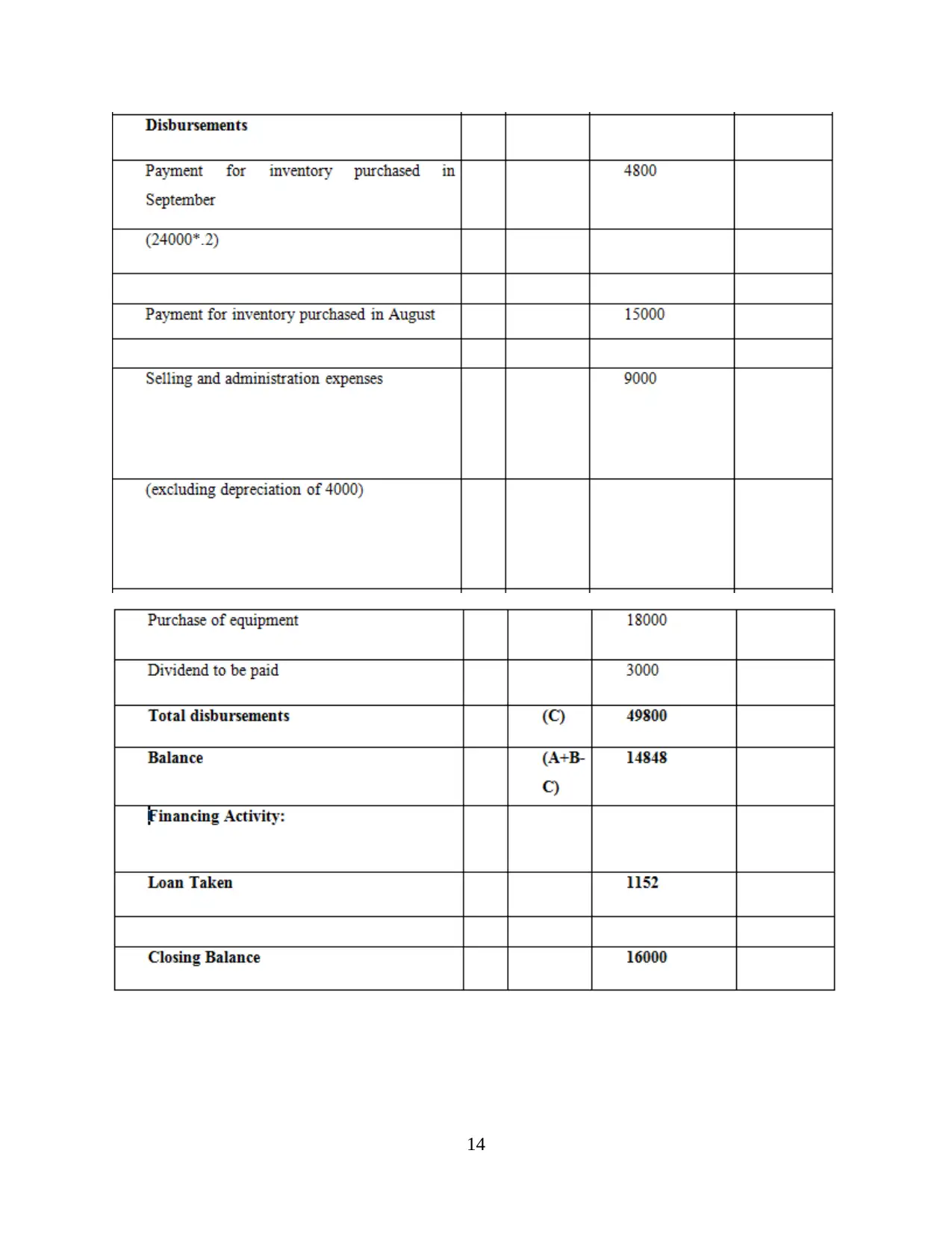

Cash budget: A cash budget is a projection of the cash flows over a given period of time for

a company. A budget is used to determine if there is enough cash in the company to function.

Companies use revenue and production estimates to construct a cash budget, along with

projections on expected expenses and collections of receivables accounts. A cash budget is

required to determine whether a firm will have sufficient financial to continue its operations.

Flexible budget: A Flexible Budget is a plan that shifts or bends with volume or activity

changes (Soin and Collier, 2013). A flexible budget is more sophisticated and practical than a

static budget. The static budget figures remain unchanged from the amounts set at the time of

planning and approval of the static budget.

15

organization to produce budget and estimate their activity cost accordingly. All are mentioned

below:

Projection of income and expenses: Budgeting is a vital aspect of the strategic cycle for

enterprises. Company owners and managers must be able to determine whether or not a business

is making a profit (Senftlechner and Hiebl, 2015). Purpose of the budgeting is essentially to

provide Managers of UCK furniture tries to estimate revenue and expenditure and therefore

productivity at the time of developing business plan. It helps in estimating how the company will

work financially if certain policies, events, plan is carried out.

Used for decision making process: Main purpose of budgeting is to have a financial

structure for the decision-making process i.e. something that we have prepared for or not is the

proposed direction action. Expenditure needs to be closely managed when running a company

responsibly. Once the marketing budget has been completely invested, the decision on "will they

spend money on ads" would probably be "no"

Monitor business performance: Budgeting is intended to allow the actual business

performance to be calculated against the company performance prediction, i.e. the business that

lives up to our expectations.

Due to above mention budgeting purpose, UCK furniture produce budget and take all the

advantages which they can or manage their spending patter.

Types of budgets:

Cash budget: A cash budget is a projection of the cash flows over a given period of time for

a company. A budget is used to determine if there is enough cash in the company to function.

Companies use revenue and production estimates to construct a cash budget, along with

projections on expected expenses and collections of receivables accounts. A cash budget is

required to determine whether a firm will have sufficient financial to continue its operations.

Flexible budget: A Flexible Budget is a plan that shifts or bends with volume or activity

changes (Soin and Collier, 2013). A flexible budget is more sophisticated and practical than a

static budget. The static budget figures remain unchanged from the amounts set at the time of

planning and approval of the static budget.

15

4.1 Compare the Performance of organizations by using following three measures

Financial problems: It's a type of a problem that's connected to lack of resources or

assets. Because of these challenges, companies face many other issues such as financial crises

and unable to run business activities and operations. Below are some of the issues which UCK

Furniture faces below:

Spend more than income: It's a sort of problem that happens when a business spent more

money but receives less relative to that. Because of this firm face the problem of shortage of

money.

Unequal cash flow: This is some kind of problem that does not suit the cash flow of the

company. Finally, cash inflow and outflow will balance but financial problems arise in the

absence of it.

Techniques:

Benchmarking: It is the method of comparing the performance of a organization in

terms of products, services or operations against those of another company that is perceived to be

the best in the business. Benchmarking is about finding internal opportunities for change and

further implement in the business strategies to achieve organizational goals & objectives.

Key Performance Indicator (KPI): KPI is a measured metric showing how efficiently

a company meets main business goals. Organizations adopt KPIs to measure their success in

reaching goals. Picking the right one depends on your company, and which part of the business

you want to track (Ward, 2012). Each division can use various forms of KPI to assess

performance based on common business goals and targets. Figure out what kinds of main

performance metrics are important to your department, sector or position. Managers of UCK

Furniture’s identify relevant KPIs and take actions accordingly.

Financial governance: It is sort of a system related to the processing, tracking and

management of financial transactions. This plays an important part in evaluating the financial

issues. Ultimately, it acts as a control tool to recognize the company's financial issue.

4.2 Comparison of organizations and evaluate that how they adopt management accounting

system to respond their financial issues:

Basis UCK Furniture UCK Woodwork

Financial problem This division of UCK group face

the financial issue regarding

They are faced with an uneven

cash flow problem. This results in

16

Financial problems: It's a type of a problem that's connected to lack of resources or

assets. Because of these challenges, companies face many other issues such as financial crises

and unable to run business activities and operations. Below are some of the issues which UCK

Furniture faces below:

Spend more than income: It's a sort of problem that happens when a business spent more

money but receives less relative to that. Because of this firm face the problem of shortage of

money.

Unequal cash flow: This is some kind of problem that does not suit the cash flow of the

company. Finally, cash inflow and outflow will balance but financial problems arise in the

absence of it.

Techniques:

Benchmarking: It is the method of comparing the performance of a organization in

terms of products, services or operations against those of another company that is perceived to be

the best in the business. Benchmarking is about finding internal opportunities for change and

further implement in the business strategies to achieve organizational goals & objectives.

Key Performance Indicator (KPI): KPI is a measured metric showing how efficiently

a company meets main business goals. Organizations adopt KPIs to measure their success in

reaching goals. Picking the right one depends on your company, and which part of the business

you want to track (Ward, 2012). Each division can use various forms of KPI to assess

performance based on common business goals and targets. Figure out what kinds of main

performance metrics are important to your department, sector or position. Managers of UCK

Furniture’s identify relevant KPIs and take actions accordingly.

Financial governance: It is sort of a system related to the processing, tracking and

management of financial transactions. This plays an important part in evaluating the financial

issues. Ultimately, it acts as a control tool to recognize the company's financial issue.

4.2 Comparison of organizations and evaluate that how they adopt management accounting

system to respond their financial issues:

Basis UCK Furniture UCK Woodwork

Financial problem This division of UCK group face

the financial issue regarding

They are faced with an uneven

cash flow problem. This results in

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

expenses are more than earnings. a huge financial dilemma.

Management

accounting system

In order to resolve this issue,

company follow the cost

accounting system and estimate

each unity cost and after that

build strategies accordingly.

This company adopt inventory

management system to track their

stock and make sure to order raw

material accordingly.

Technique Company should follow

benchmarking technique to

evaluate financial performance.

They need to adopt key

performance indicator technique

to measure that which aspect

affect the most and focus on ot

accordingly.

Notes:

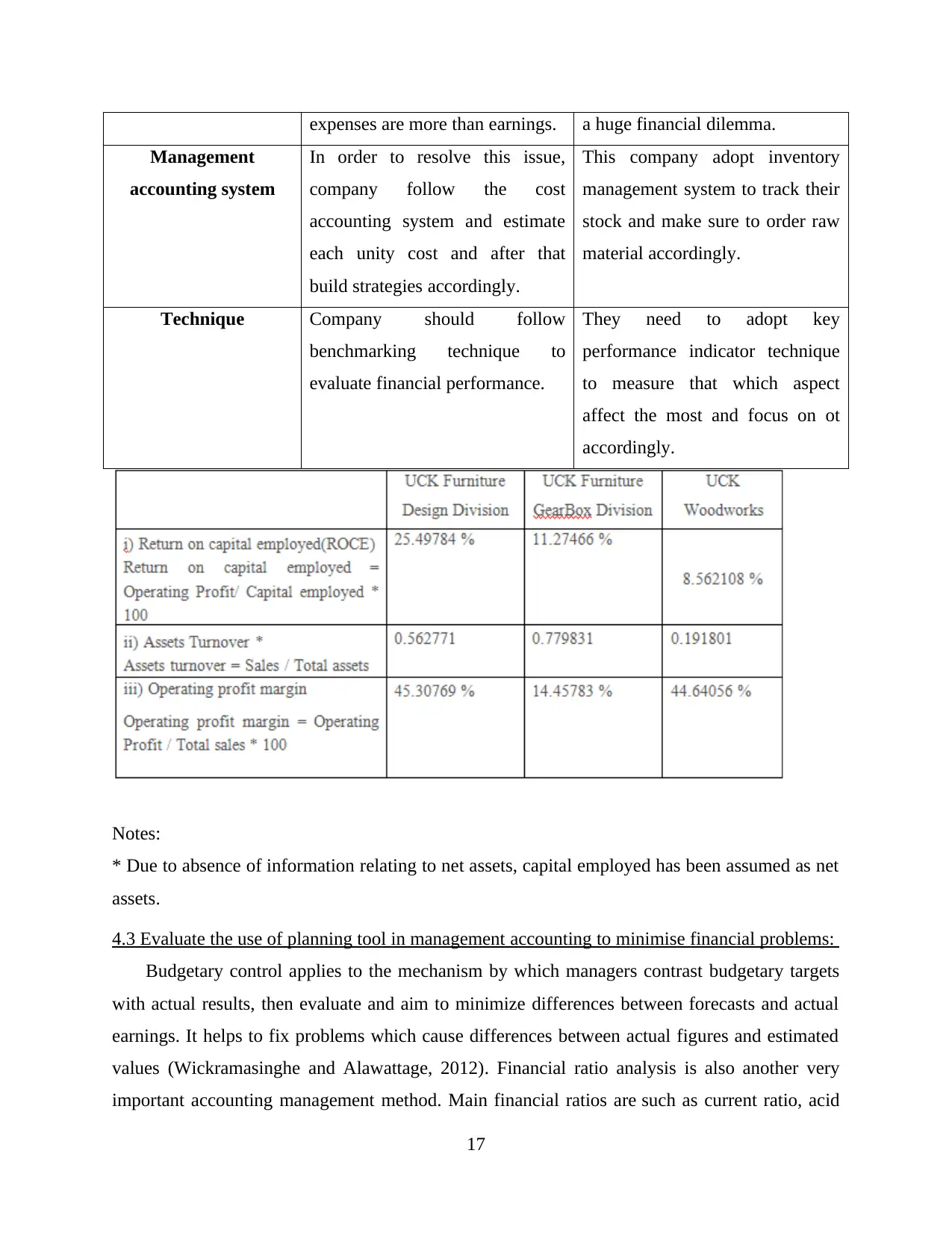

* Due to absence of information relating to net assets, capital employed has been assumed as net

assets.

4.3 Evaluate the use of planning tool in management accounting to minimise financial problems:

Budgetary control applies to the mechanism by which managers contrast budgetary targets

with actual results, then evaluate and aim to minimize differences between forecasts and actual

earnings. It helps to fix problems which cause differences between actual figures and estimated

values (Wickramasinghe and Alawattage, 2012). Financial ratio analysis is also another very

important accounting management method. Main financial ratios are such as current ratio, acid

17

Management

accounting system

In order to resolve this issue,

company follow the cost

accounting system and estimate

each unity cost and after that

build strategies accordingly.

This company adopt inventory

management system to track their

stock and make sure to order raw

material accordingly.

Technique Company should follow

benchmarking technique to

evaluate financial performance.

They need to adopt key

performance indicator technique

to measure that which aspect

affect the most and focus on ot

accordingly.

Notes:

* Due to absence of information relating to net assets, capital employed has been assumed as net

assets.

4.3 Evaluate the use of planning tool in management accounting to minimise financial problems:

Budgetary control applies to the mechanism by which managers contrast budgetary targets

with actual results, then evaluate and aim to minimize differences between forecasts and actual

earnings. It helps to fix problems which cause differences between actual figures and estimated

values (Wickramasinghe and Alawattage, 2012). Financial ratio analysis is also another very

important accounting management method. Main financial ratios are such as current ratio, acid

17

test ratio, equity ratio, asset turnover ratio, leverage coverage ratio, etc., are measured and

evaluated to evaluate the business performance and to decide the corrective steps to be taken to

correct negative ratios. Also every planning technique used in management accounting allows

financial results to be improved and financial issues reduced in order to achieve success. In

addition, project estimation, evaluation, costing methods, ratio analysis help in management

accounting minimise financial problems and get success.

CONCLUSION

From the above discussion it has been concluded that management accounting is very

essential for the organization where they follow various techniques to manage company’s

financial information. Management accounting systems helps managers to make effective

decisions by using relevant outcomes and these informational mentioned in the reports which

prepared by the management for future references.

18

evaluated to evaluate the business performance and to decide the corrective steps to be taken to

correct negative ratios. Also every planning technique used in management accounting allows

financial results to be improved and financial issues reduced in order to achieve success. In

addition, project estimation, evaluation, costing methods, ratio analysis help in management

accounting minimise financial problems and get success.

CONCLUSION

From the above discussion it has been concluded that management accounting is very

essential for the organization where they follow various techniques to manage company’s

financial information. Management accounting systems helps managers to make effective

decisions by using relevant outcomes and these informational mentioned in the reports which

prepared by the management for future references.

18

REFERENCES

Books & Journals

19

Books & Journals

19

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.