7032ACC - Management Accounting Issues Report for AV Roe Plc

VerifiedAdded on 2023/01/12

|10

|1606

|38

Report

AI Summary

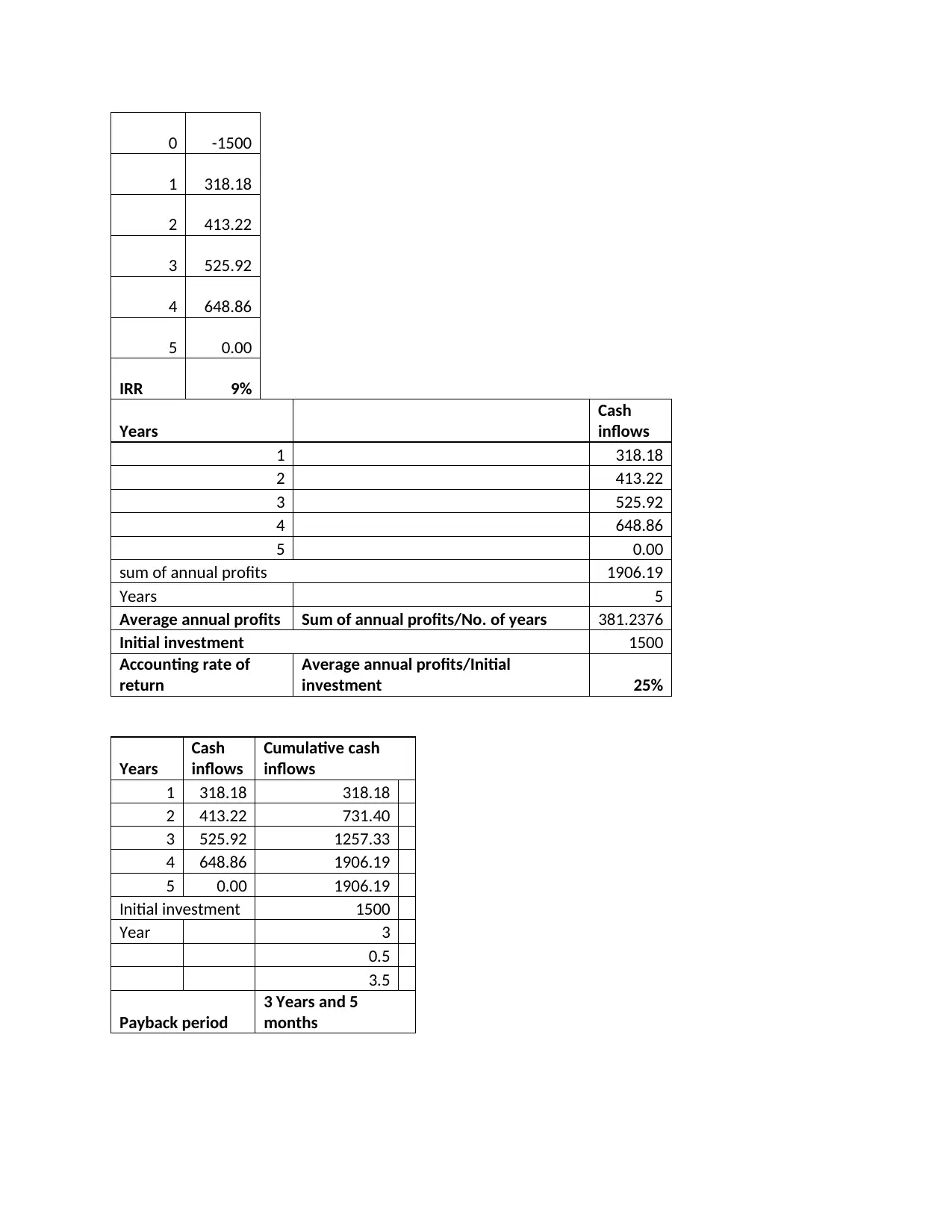

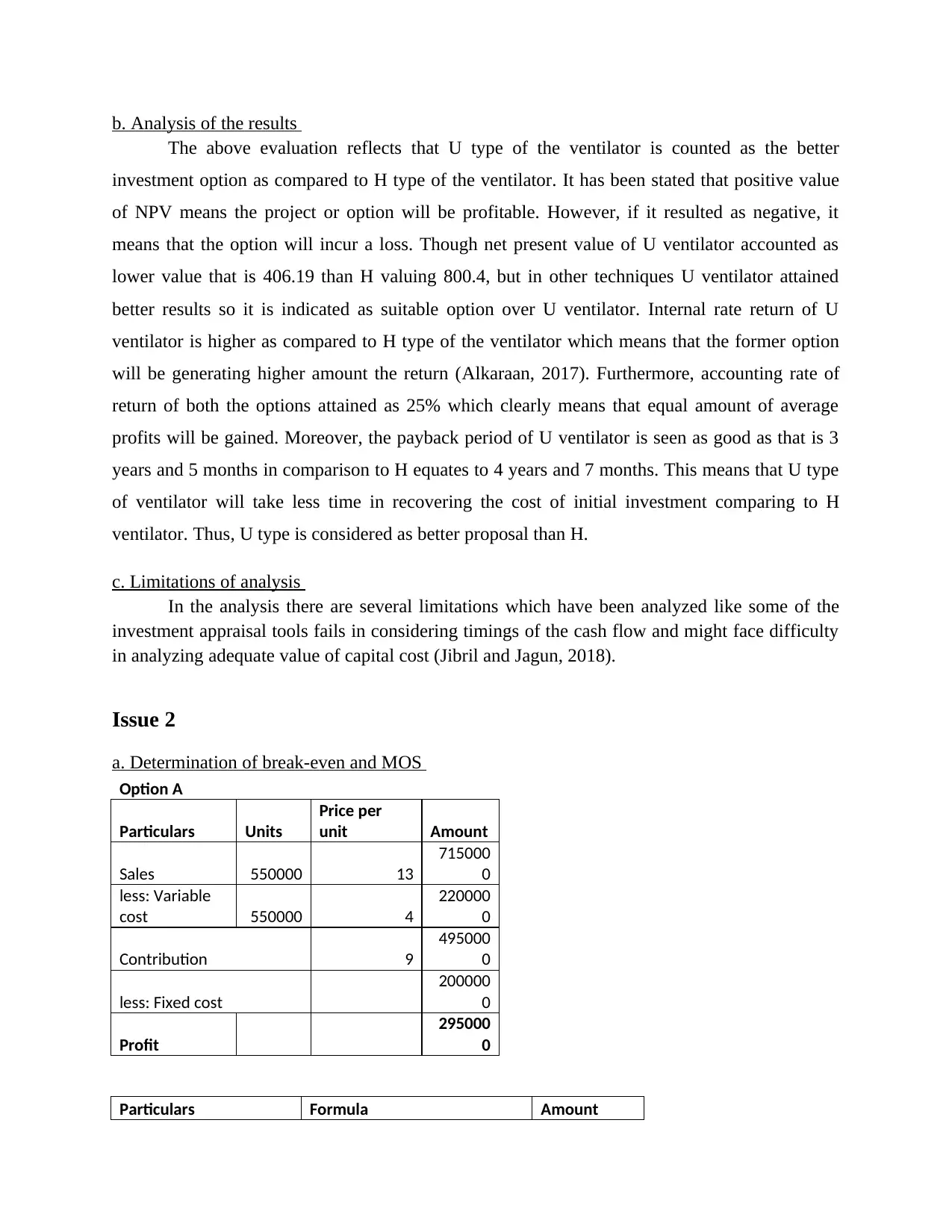

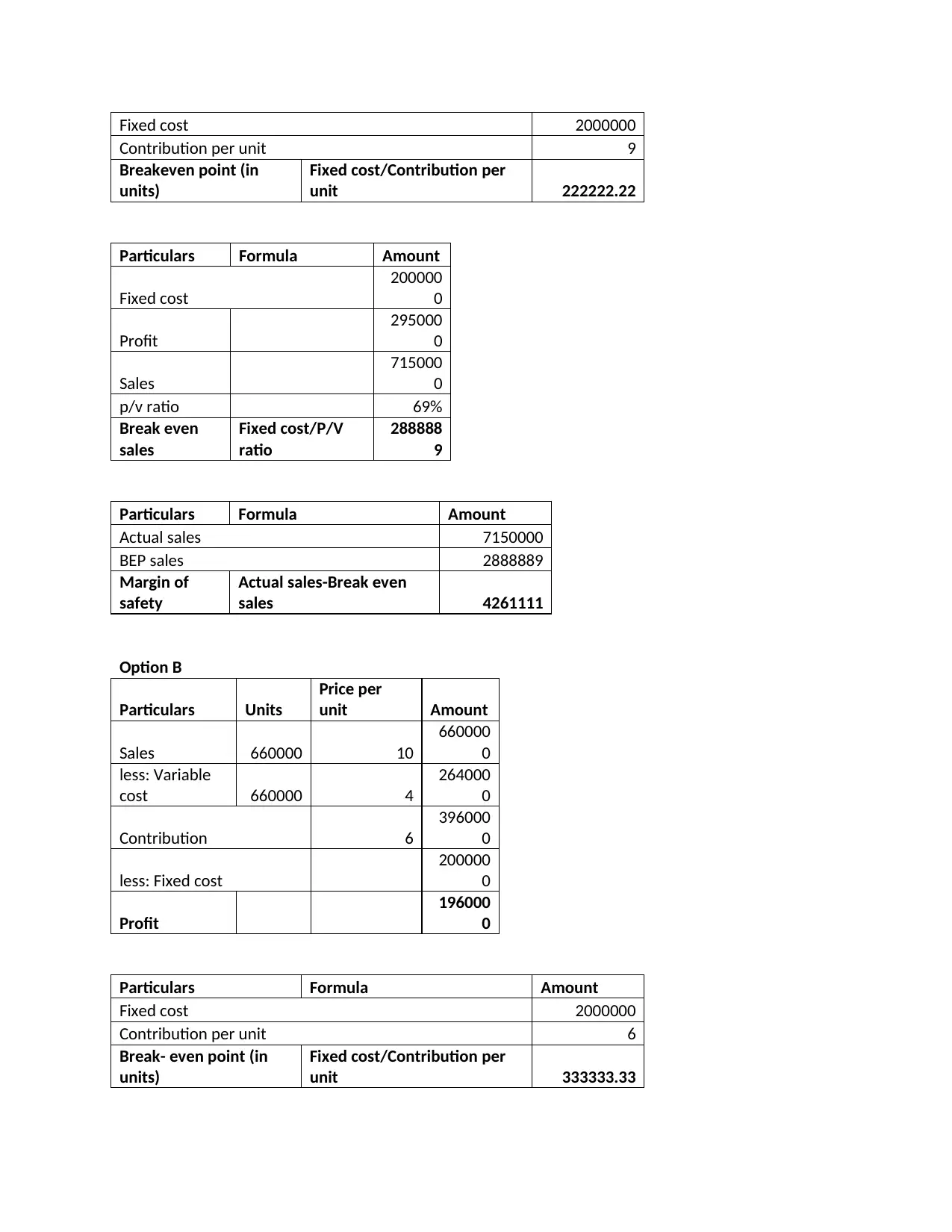

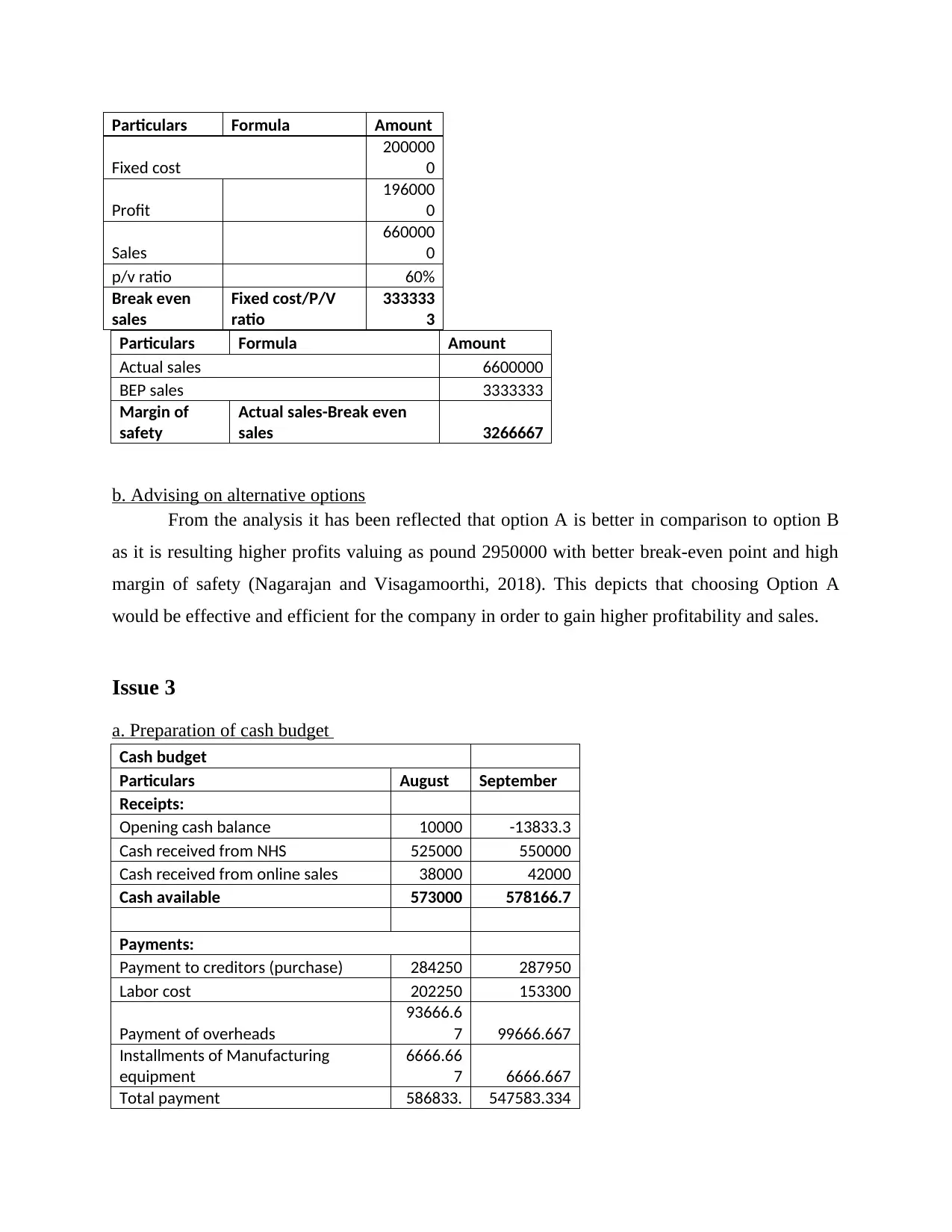

This report analyzes management accounting issues for AV Roe Plc, a company specializing in medical equipment. The report evaluates investment options using capital budgeting techniques like NPV, IRR, ARR, and payback period, comparing two ventilator types to determine the better investment. It further addresses break-even analysis and margin of safety for different options, advising on the most profitable choice. Finally, the report presents a cash budget for AV Roe Plc, analyzes its cash flow, and suggests improvements, emphasizing the importance of cash budgets for managing liquidity and financial obligations. The analysis and evaluations are based on the company's financial data and industry standards.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.