MGT723 Research: Stakeholder Theory Facilitating Carbon Disclosure

VerifiedAdded on 2023/06/13

|11

|1730

|199

Report

AI Summary

This research proposal explores how stakeholder theory can facilitate addressing carbon disclosure concerns in companies. It reviews the practical and theoretical motivations for carbon disclosure, previous research findings, and key concepts of stakeholder theory. The proposal presents a conceptual framework model illustrating the relationship between slack, information asymmetry, and carbon disclosure. It formulates hypotheses related to the relationship between disclosure and company profitability, target slack, and performance-based incentives. The research method involves primary and secondary data collection, including interviews with managers, and data analysis using MS Excel for correlation and regression analysis. This document is available on Desklib, where students can find a wealth of academic resources, including past papers and solved assignments.

Running head: MANAGEMENT ACCOUNTING ISSUES AND STAKEHOLDER THEORY

MGT723 Research Project

Assessment Task 1: Research Proposal

Student Name: XXX

Your assigned research topic*: Management Accounting Issues: Stakeholder Theory

Draft Research Question: How Stakeholder theory along with its factors can facilitate in

addressing carbon disclosure concerns in companies?

Title: XXX

Submission Date: XXX

MGT723 Research Project

Assessment Task 1: Research Proposal

Student Name: XXX

Your assigned research topic*: Management Accounting Issues: Stakeholder Theory

Draft Research Question: How Stakeholder theory along with its factors can facilitate in

addressing carbon disclosure concerns in companies?

Title: XXX

Submission Date: XXX

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING ISSUES AND AGENCY THEORY

Table of Contents

Literature Review................................................................................................................2

Motivation........................................................................................................................2

Practical Motivation.....................................................................................................2

Theoretical Motivation................................................................................................2

Previous Results...........................................................................................................2

Stakeholder Theory......................................................................................................3

Key Theoretical Concepts............................................................................................3

Relationship between Information Asymmetry and Slack..........................................4

Conceptual Framework Model............................................................................................4

Hypothesis...........................................................................................................................5

Proxy Measures...................................................................................................................5

Research Method.................................................................................................................6

References............................................................................................................................8

Appendices..........................................................................................................................9

Table of Contents

Literature Review................................................................................................................2

Motivation........................................................................................................................2

Practical Motivation.....................................................................................................2

Theoretical Motivation................................................................................................2

Previous Results...........................................................................................................2

Stakeholder Theory......................................................................................................3

Key Theoretical Concepts............................................................................................3

Relationship between Information Asymmetry and Slack..........................................4

Conceptual Framework Model............................................................................................4

Hypothesis...........................................................................................................................5

Proxy Measures...................................................................................................................5

Research Method.................................................................................................................6

References............................................................................................................................8

Appendices..........................................................................................................................9

2MANAGEMENT ACCOUNTING ISSUES AND AGENCY THEORY

Literature Review

Motivation

Practical Motivation

Samaha, Khlif and Hussainey (2015) explained that carbon emissions are deemed to

affect business activities includingcompetition, investment as wee as stakeholder and investment

activities. These researchers also evidenced that there is positive relationship between

performance disclosure of carbon emissions, organizationalgrowth along with its financial

performance. Global warmingand climate changes are increasing risk of carbon emissions of

organizations. This is the reason for which disclosure of carbon emission is important to be

considered by organizations in order to deal with climate changes risks (Shehata 2014).

Theoretical Motivation

The effect of disclosure associated with carbon emission has drastic effect on the

financial performance of the organisations. Hence, the organisations are needed to concentrate on

minimising the environmental issues providing economic advantages. The carbon disclosures

that the organisations undertake need to be rightful and voluntary, as the figures need to be real.

Such information would enable the shareholders to ascertain the actual position and performance

of the organisation. Thus, the research would take into account the impact of carbon disclosure

on the overall business performance of the organisations.

Previous Results

In the words of Khlif, Ahmed and Souissi (2017), carbon emission disclosures draw the

attention of the shareholders in order to invest in the organisation and hence, the latter could

obtain financial benefits. From the administration perspective, it is necessary for a firm to adhere

Literature Review

Motivation

Practical Motivation

Samaha, Khlif and Hussainey (2015) explained that carbon emissions are deemed to

affect business activities includingcompetition, investment as wee as stakeholder and investment

activities. These researchers also evidenced that there is positive relationship between

performance disclosure of carbon emissions, organizationalgrowth along with its financial

performance. Global warmingand climate changes are increasing risk of carbon emissions of

organizations. This is the reason for which disclosure of carbon emission is important to be

considered by organizations in order to deal with climate changes risks (Shehata 2014).

Theoretical Motivation

The effect of disclosure associated with carbon emission has drastic effect on the

financial performance of the organisations. Hence, the organisations are needed to concentrate on

minimising the environmental issues providing economic advantages. The carbon disclosures

that the organisations undertake need to be rightful and voluntary, as the figures need to be real.

Such information would enable the shareholders to ascertain the actual position and performance

of the organisation. Thus, the research would take into account the impact of carbon disclosure

on the overall business performance of the organisations.

Previous Results

In the words of Khlif, Ahmed and Souissi (2017), carbon emission disclosures draw the

attention of the shareholders in order to invest in the organisation and hence, the latter could

obtain financial benefits. From the administration perspective, it is necessary for a firm to adhere

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING ISSUES AND AGENCY THEORY

to the CSR policy so that it could form positive association with the governmental and regulatory

bodies. Such association improves the brand image of the organisation in the eyes of its

associated stakeholders. Moreover, the association between the suppliers and the customers helps

in adoption of environment-friendly measures.

Stakeholder Theory

As laid out by Habbash, Hussaineyand Awad (2016), Stakeholder theory could be

explained in the form of a supposition depicting the relationship between agents and principals in

business organisations. This is concerned with resolving those issues, which could take place in

Stakeholder relationships because of unadjusted goals and diversified levels of risk aversion. The

most inherent Stakeholder relationship could be identified between the shareholders and business

executives. The shareholders are adjudged as the principal, while the business executives are

considered as the agents.

Key Theoretical Concepts

Martínez‐Ferrero, Garcia‐Sanchez and Cuadrado‐Ballesteros (2015)evidenced that in the

recent years a drastic development in the sustainability accounting literature has obtained

increased attention. These researchers explained that carbon performance and impacts can be

measured relied on per employee emissions, each employee reductions and operations or cost

centre emissions. From the administrative viewpoint, it is also evidenced that there is a

positiveassociation between the environment and company’s sustainable performance. Samaha,

Khlif and Hussainey (2015) stated that the accountants that are involved in defining the

indicators, designing methods along with gathering sustainability information are observed to

have a methodological role. This facilitates in supporting and promoting sustainability

accounting within the company.

to the CSR policy so that it could form positive association with the governmental and regulatory

bodies. Such association improves the brand image of the organisation in the eyes of its

associated stakeholders. Moreover, the association between the suppliers and the customers helps

in adoption of environment-friendly measures.

Stakeholder Theory

As laid out by Habbash, Hussaineyand Awad (2016), Stakeholder theory could be

explained in the form of a supposition depicting the relationship between agents and principals in

business organisations. This is concerned with resolving those issues, which could take place in

Stakeholder relationships because of unadjusted goals and diversified levels of risk aversion. The

most inherent Stakeholder relationship could be identified between the shareholders and business

executives. The shareholders are adjudged as the principal, while the business executives are

considered as the agents.

Key Theoretical Concepts

Martínez‐Ferrero, Garcia‐Sanchez and Cuadrado‐Ballesteros (2015)evidenced that in the

recent years a drastic development in the sustainability accounting literature has obtained

increased attention. These researchers explained that carbon performance and impacts can be

measured relied on per employee emissions, each employee reductions and operations or cost

centre emissions. From the administrative viewpoint, it is also evidenced that there is a

positiveassociation between the environment and company’s sustainable performance. Samaha,

Khlif and Hussainey (2015) stated that the accountants that are involved in defining the

indicators, designing methods along with gathering sustainability information are observed to

have a methodological role. This facilitates in supporting and promoting sustainability

accounting within the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING ISSUES AND AGENCY THEORY

Relationship between Information Asymmetry and Slack

Liao, Luo and Tang (2015) focussed on the Stakeholder theory in explaining the

relationship between slack and information asymmetry in carbon disclosure of the organizations.

In explaining the relationship between these independent and dependent factors it has been

gathered that few zones are features to improve disclosure and environment risk improvement

strategies. This supports stability within the climatic surrounding that encompass environment

regulation state of affairs and market valuation for carbon disclosure.

Conceptual Framework Model

The conceptual framework model explained in the figure below explained the

relationship among the dependent and independent variables that includes slack and information

asymmetry. It is gathered from this theoretical framework that Stakeholder theory is employed in

climate changeimpacton the economy (Habbash, Hussaine and Awad 2016). It will also explain

the ways in which slack and information asymmetry are making drastic attempts in decreasing

emission disclosure. Moreover, there is a case there is decreased carbon risk management it will

comparatively present more affirmative carbon disclosures. Stakeholder theory explains financial

market factor pressure that can facilitate in dealing with risks associated with climate changes.

Relationship between Information Asymmetry and Slack

Liao, Luo and Tang (2015) focussed on the Stakeholder theory in explaining the

relationship between slack and information asymmetry in carbon disclosure of the organizations.

In explaining the relationship between these independent and dependent factors it has been

gathered that few zones are features to improve disclosure and environment risk improvement

strategies. This supports stability within the climatic surrounding that encompass environment

regulation state of affairs and market valuation for carbon disclosure.

Conceptual Framework Model

The conceptual framework model explained in the figure below explained the

relationship among the dependent and independent variables that includes slack and information

asymmetry. It is gathered from this theoretical framework that Stakeholder theory is employed in

climate changeimpacton the economy (Habbash, Hussaine and Awad 2016). It will also explain

the ways in which slack and information asymmetry are making drastic attempts in decreasing

emission disclosure. Moreover, there is a case there is decreased carbon risk management it will

comparatively present more affirmative carbon disclosures. Stakeholder theory explains financial

market factor pressure that can facilitate in dealing with risks associated with climate changes.

5MANAGEMENT ACCOUNTING ISSUES AND AGENCY THEORY

Figure 1: Theoretical Framework

(Source: Khlif, Ahmed and Souissi 2017)

Hypothesis

Research hypotheses that is set in this exploration is deemed to be tested in order to analyse

the accounting issues in consideration to carbon disclosure and Stakeholder theory. These

hypotheses are explained under:

H1: There is positive relationship between disclosure andcompany profitability

H2: Target slack is deemed to be high in the first year of which the targets are set

H3: Target slack is deemed to be high in the presence of performance-based incentives

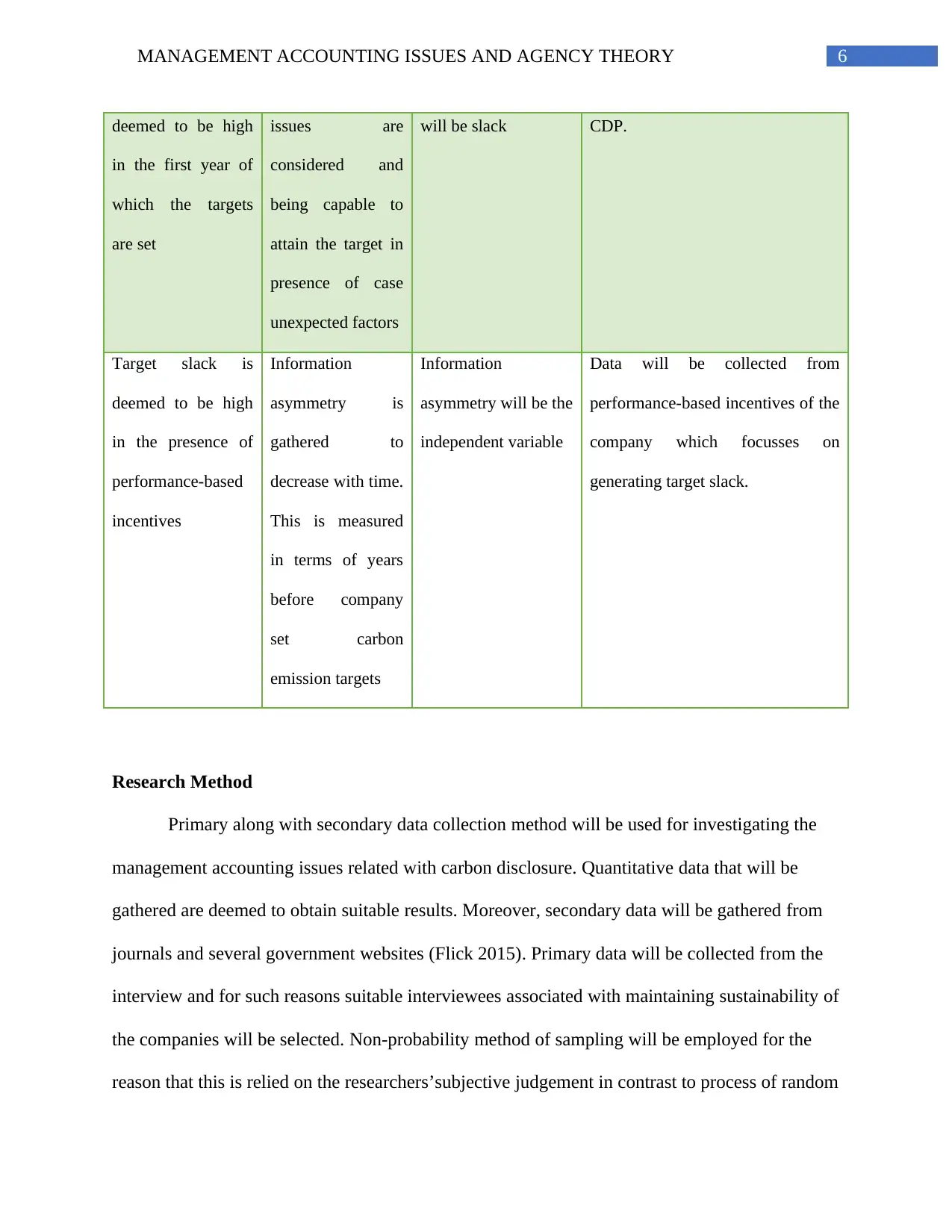

Proxy Measures

Theoretical

Aspects

Proxy measure Dependent (DV),

Independent (IV)

Source

Target slack is Remuneration Dependent variable The target that is mentioned in

Slack

Figure 1: Theoretical Framework

(Source: Khlif, Ahmed and Souissi 2017)

Hypothesis

Research hypotheses that is set in this exploration is deemed to be tested in order to analyse

the accounting issues in consideration to carbon disclosure and Stakeholder theory. These

hypotheses are explained under:

H1: There is positive relationship between disclosure andcompany profitability

H2: Target slack is deemed to be high in the first year of which the targets are set

H3: Target slack is deemed to be high in the presence of performance-based incentives

Proxy Measures

Theoretical

Aspects

Proxy measure Dependent (DV),

Independent (IV)

Source

Target slack is Remuneration Dependent variable The target that is mentioned in

Slack

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING ISSUES AND AGENCY THEORY

deemed to be high

in the first year of

which the targets

are set

issues are

considered and

being capable to

attain the target in

presence of case

unexpected factors

will be slack CDP.

Target slack is

deemed to be high

in the presence of

performance-based

incentives

Information

asymmetry is

gathered to

decrease with time.

This is measured

in terms of years

before company

set carbon

emission targets

Information

asymmetry will be the

independent variable

Data will be collected from

performance-based incentives of the

company which focusses on

generating target slack.

Research Method

Primary along with secondary data collection method will be used for investigating the

management accounting issues related with carbon disclosure. Quantitative data that will be

gathered are deemed to obtain suitable results. Moreover, secondary data will be gathered from

journals and several government websites (Flick 2015). Primary data will be collected from the

interview and for such reasons suitable interviewees associated with maintaining sustainability of

the companies will be selected. Non-probability method of sampling will be employed for the

reason that this is relied on the researchers’subjective judgement in contrast to process of random

deemed to be high

in the first year of

which the targets

are set

issues are

considered and

being capable to

attain the target in

presence of case

unexpected factors

will be slack CDP.

Target slack is

deemed to be high

in the presence of

performance-based

incentives

Information

asymmetry is

gathered to

decrease with time.

This is measured

in terms of years

before company

set carbon

emission targets

Information

asymmetry will be the

independent variable

Data will be collected from

performance-based incentives of the

company which focusses on

generating target slack.

Research Method

Primary along with secondary data collection method will be used for investigating the

management accounting issues related with carbon disclosure. Quantitative data that will be

gathered are deemed to obtain suitable results. Moreover, secondary data will be gathered from

journals and several government websites (Flick 2015). Primary data will be collected from the

interview and for such reasons suitable interviewees associated with maintaining sustainability of

the companies will be selected. Non-probability method of sampling will be employed for the

reason that this is relied on the researchers’subjective judgement in contrast to process of random

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING ISSUES AND AGENCY THEORY

sampling method. 11 managers from the organizations in Australia will be selected in the

interview process. Moreover, their responses will be analysed for obtaining their opinion

regarding the Stakeholder theory along with itsimportance on dealing with concerns related with

carbon disclosure (Hoque 2018). Dataanalysis will be carried out in MS excel and correlation

and regression analysis will be carried out for testing relationship between dependent and

independent variables.

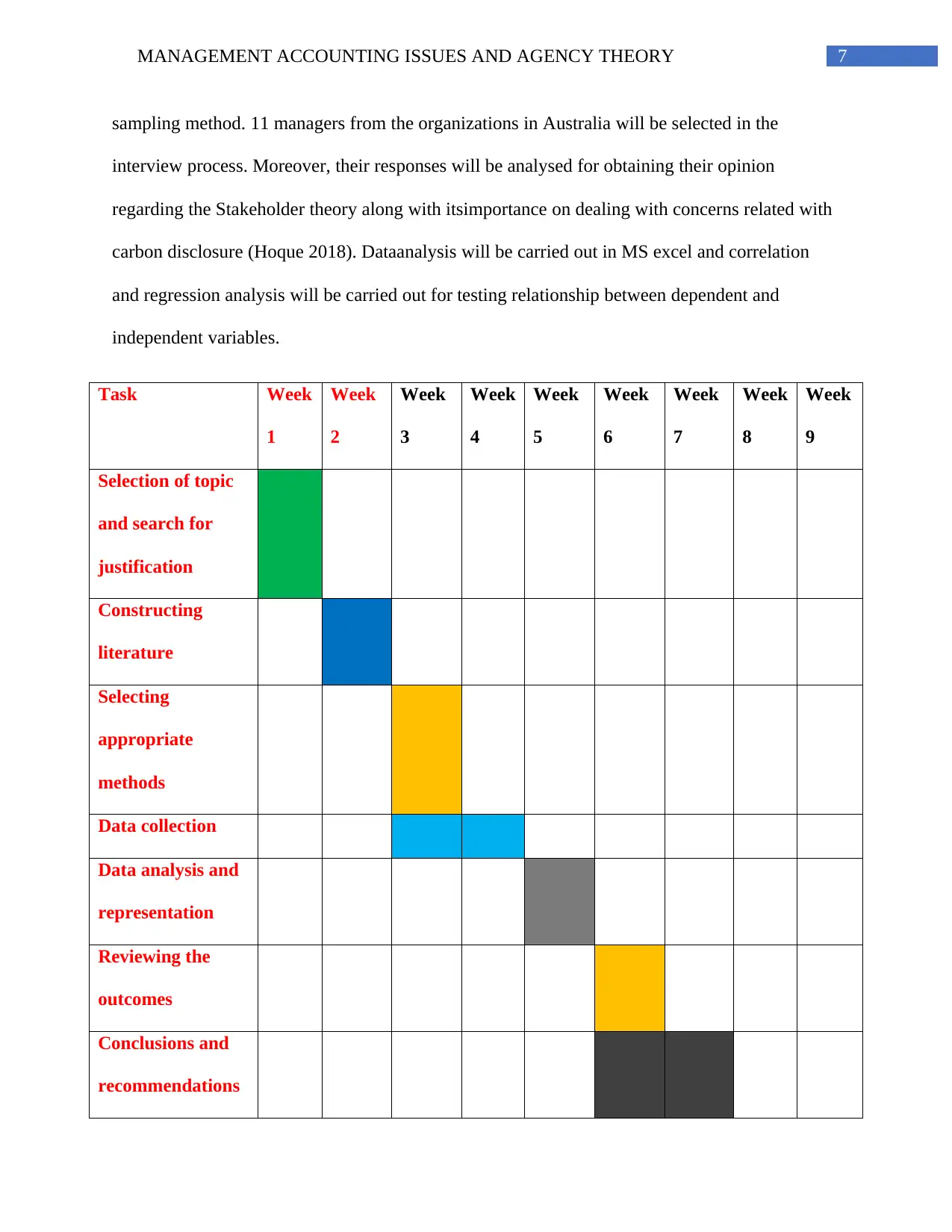

Task Week

1

Week

2

Week

3

Week

4

Week

5

Week

6

Week

7

Week

8

Week

9

Selection of topic

and search for

justification

Constructing

literature

Selecting

appropriate

methods

Data collection

Data analysis and

representation

Reviewing the

outcomes

Conclusions and

recommendations

sampling method. 11 managers from the organizations in Australia will be selected in the

interview process. Moreover, their responses will be analysed for obtaining their opinion

regarding the Stakeholder theory along with itsimportance on dealing with concerns related with

carbon disclosure (Hoque 2018). Dataanalysis will be carried out in MS excel and correlation

and regression analysis will be carried out for testing relationship between dependent and

independent variables.

Task Week

1

Week

2

Week

3

Week

4

Week

5

Week

6

Week

7

Week

8

Week

9

Selection of topic

and search for

justification

Constructing

literature

Selecting

appropriate

methods

Data collection

Data analysis and

representation

Reviewing the

outcomes

Conclusions and

recommendations

8MANAGEMENT ACCOUNTING ISSUES AND AGENCY THEORY

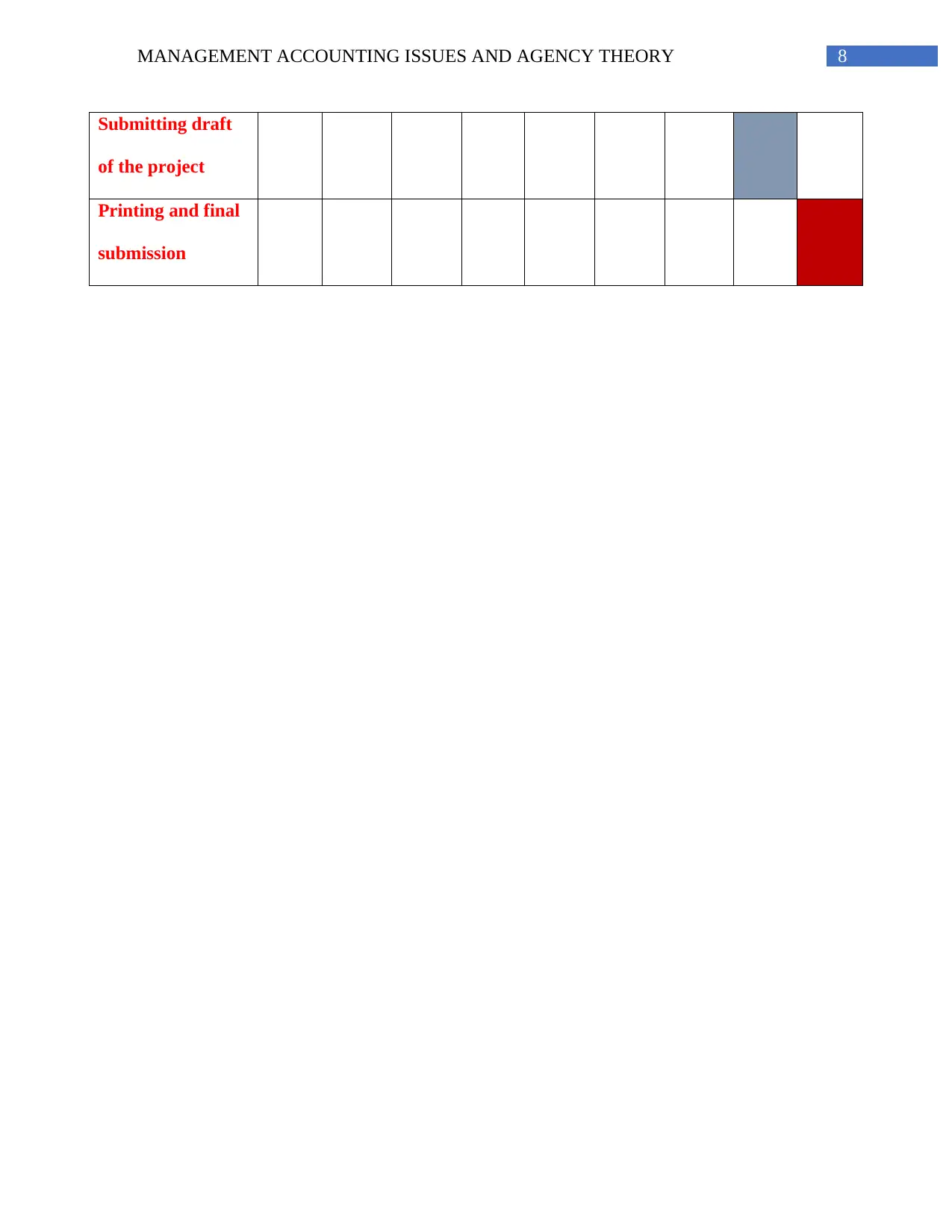

Submitting draft

of the project

Printing and final

submission

Submitting draft

of the project

Printing and final

submission

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING ISSUES AND AGENCY THEORY

References

Flick, U., 2015. Introducing research methodology: A beginner's guide to doing a research

project. Sage.

Habbash, M., Hussainey, K. and Awad, A.E., 2016. The determinants of voluntary disclosure in

Saudi Arabia: an empirical study. International Journal of Accounting, Auditing and

Performance Evaluation, 12(3), pp.213-236.

Hoque, Z., 2018. Methodological issues in accounting research. Spiramus Press Ltd.

Khlif, H., Ahmed, K. and Souissi, M., 2017. Ownership structure and voluntary disclosure: A

synthesis of empirical studies. Australian Journal of Management, 42(3), pp.376-403.

Liao, L., Luo, L. and Tang, Q., 2015. Gender diversity, board independence, environmental

committee and greenhouse gas disclosure. The British Accounting Review, 47(4), pp.409-424.

Martínez‐Ferrero, J., Garcia‐Sanchez, I.M. and Cuadrado‐Ballesteros, B., 2015. Effect of

financial reporting quality on sustainability information disclosure. Corporate Social

Responsibility and Environmental Management, 22(1), pp.45-64.

Samaha, K., Khlif, H. and Hussainey, K., 2015. The impact of board and audit committee

characteristics on voluntary disclosure: a meta-analysis. Journal of International Accounting,

Auditing and Taxation, 24, pp.13-28.

Shehata, N., 2014. Theories and determinants of voluntary disclosure.

References

Flick, U., 2015. Introducing research methodology: A beginner's guide to doing a research

project. Sage.

Habbash, M., Hussainey, K. and Awad, A.E., 2016. The determinants of voluntary disclosure in

Saudi Arabia: an empirical study. International Journal of Accounting, Auditing and

Performance Evaluation, 12(3), pp.213-236.

Hoque, Z., 2018. Methodological issues in accounting research. Spiramus Press Ltd.

Khlif, H., Ahmed, K. and Souissi, M., 2017. Ownership structure and voluntary disclosure: A

synthesis of empirical studies. Australian Journal of Management, 42(3), pp.376-403.

Liao, L., Luo, L. and Tang, Q., 2015. Gender diversity, board independence, environmental

committee and greenhouse gas disclosure. The British Accounting Review, 47(4), pp.409-424.

Martínez‐Ferrero, J., Garcia‐Sanchez, I.M. and Cuadrado‐Ballesteros, B., 2015. Effect of

financial reporting quality on sustainability information disclosure. Corporate Social

Responsibility and Environmental Management, 22(1), pp.45-64.

Samaha, K., Khlif, H. and Hussainey, K., 2015. The impact of board and audit committee

characteristics on voluntary disclosure: a meta-analysis. Journal of International Accounting,

Auditing and Taxation, 24, pp.13-28.

Shehata, N., 2014. Theories and determinants of voluntary disclosure.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING ISSUES AND AGENCY THEORY

Appendices

Questionnaire for Managers

1. Does your organization include commitment to legal compliance and continuous in the

environmental performance?

2. Do the organizations have annual objectives along with activities based on the aspects

covered with the environmental policy?

3. How can you explain the business ethics section of the companies in explaining the

carbon disclosure?

4. Explain the ways in which the organization have formal policy in place regarding the

carbon disclosure-based business ethics?

5. Explain the ways in which the company participates within any voluntary sustainability

initiatives?

Appendices

Questionnaire for Managers

1. Does your organization include commitment to legal compliance and continuous in the

environmental performance?

2. Do the organizations have annual objectives along with activities based on the aspects

covered with the environmental policy?

3. How can you explain the business ethics section of the companies in explaining the

carbon disclosure?

4. Explain the ways in which the organization have formal policy in place regarding the

carbon disclosure-based business ethics?

5. Explain the ways in which the company participates within any voluntary sustainability

initiatives?

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.