Management Accounting

Added on 2022-12-05

32 Pages7071 Words135 Views

Running Text: Management Accounting

Management

Accounting

Management

Accounting

Management Accounting

Contents

INTRODUCTION...................................................................................................... 2

1. Management Accounting and its Applications.................................................2

2. Roles and Principles of Management Accounting............................................3

3. Types of Management Accounting System and Its Application in Organisation

3

A. Job Costing System...................................................................................... 3

B. Price Optimising System.............................................................................. 4

C. Cost Accounting System...............................................................................4

D. Inventory Management System...................................................................5

4. Management Accounting Reporting................................................................5

5. Application of Management Accounting Techniques: Galway PLC...................6

6. Planning Tools used in Budgetary Control.....................................................14

7. Management Accounting: A Solution to the Financial Problems....................18

8. Management Accounting can lead the Organisation to Sustainable Success in

Response to Financial Problems: An Analysis......................................................20

9. Conclusion..................................................................................................... 21

References........................................................................................................... 22

1

Contents

INTRODUCTION...................................................................................................... 2

1. Management Accounting and its Applications.................................................2

2. Roles and Principles of Management Accounting............................................3

3. Types of Management Accounting System and Its Application in Organisation

3

A. Job Costing System...................................................................................... 3

B. Price Optimising System.............................................................................. 4

C. Cost Accounting System...............................................................................4

D. Inventory Management System...................................................................5

4. Management Accounting Reporting................................................................5

5. Application of Management Accounting Techniques: Galway PLC...................6

6. Planning Tools used in Budgetary Control.....................................................14

7. Management Accounting: A Solution to the Financial Problems....................18

8. Management Accounting can lead the Organisation to Sustainable Success in

Response to Financial Problems: An Analysis......................................................20

9. Conclusion..................................................................................................... 21

References........................................................................................................... 22

1

Management Accounting

INTRODUCTION

This report discusses about the management accounting and its methods used

primarily by the organisations as a tool of planning and measurement for

evaluating their performances. To integrate the business activities effectively

with management accounting systems, sound management accounting systems

are required. So, this report would provide clarity over the management

accounting systems too. Additionally, the preparation of income statements

under marginal costing and absorption costing is also being carried out. There

are many tools for planning which are used for the budgetary control and these

also assist in making and forecasting budgets. Further, a comparison is done to

address the users of the report that how management accounting can aid in

resolving financial problems. At the end, we would know how the management

forms strategies and plans by employing management accounting techniques for

making the implementation and execution easy.

1. Management Accounting and its Applications

Management accounting is the process of interpreting, analysing, identifying and

presenting those accounting facts that have been procured with the help of cost

accounting and financial accounting (Drury, 2015). Business managers make use

of management accounting for the policy formulation, decision making and carry

out the day to day business operations.

Management accounting is applicable in the following ways:

1. Performance Measurement- With the help of management accounting,

managers evaluates performance of the employees as well as their

efficiency level. Under this, the actual performance is measured with

standard performance set by the company. In case of any deviation,

necessary steps are taken to eradicate it.

2. Evaluation of Risks- Management accounting aids in the identification of

risk factors arising in the organisation after which, with the help of

effective management proper steps are taken to remove or minimise the

identified risk.

2

INTRODUCTION

This report discusses about the management accounting and its methods used

primarily by the organisations as a tool of planning and measurement for

evaluating their performances. To integrate the business activities effectively

with management accounting systems, sound management accounting systems

are required. So, this report would provide clarity over the management

accounting systems too. Additionally, the preparation of income statements

under marginal costing and absorption costing is also being carried out. There

are many tools for planning which are used for the budgetary control and these

also assist in making and forecasting budgets. Further, a comparison is done to

address the users of the report that how management accounting can aid in

resolving financial problems. At the end, we would know how the management

forms strategies and plans by employing management accounting techniques for

making the implementation and execution easy.

1. Management Accounting and its Applications

Management accounting is the process of interpreting, analysing, identifying and

presenting those accounting facts that have been procured with the help of cost

accounting and financial accounting (Drury, 2015). Business managers make use

of management accounting for the policy formulation, decision making and carry

out the day to day business operations.

Management accounting is applicable in the following ways:

1. Performance Measurement- With the help of management accounting,

managers evaluates performance of the employees as well as their

efficiency level. Under this, the actual performance is measured with

standard performance set by the company. In case of any deviation,

necessary steps are taken to eradicate it.

2. Evaluation of Risks- Management accounting aids in the identification of

risk factors arising in the organisation after which, with the help of

effective management proper steps are taken to remove or minimise the

identified risk.

2

Management Accounting

3. Resource Allocation- With the help of management accounting,

organisations are able to allocate the resources in an efficient manner to

different departments which results in its optimum utilisation of those

resources.

4. Presentation of Financial Statement- The data like cost data as well as

financial data can be obtained through Management accounting. When

these data are entered in the final financial statements it makes it even

more useful for the readers and further it supports in the managerial

process like decision-making.

2. Roles and Principles of Management Accounting

There are many roles and principles of Management accounting. Some of them

are as follows:

1. Influence- Management accounting emphasises more on an effective

communication as it benefits in making significant decisions after

considering all the other factors. An effective communication is one

which consists of all the important information required for correct

decision making.

2. Relevancy- Management accounting aids the management of the

organisation in making important decisions. Therefore, it should consist

of such information which are high on quality as well as are relevant

and could assist in taking quality decisions.

3. Focuses on Generating Value- Management accounting focus more on

the generation of values instead of simply analysing the data.

Generation of values means focusing more on the factors like costs,

risks and opportunities relating to value generation.

3

3. Resource Allocation- With the help of management accounting,

organisations are able to allocate the resources in an efficient manner to

different departments which results in its optimum utilisation of those

resources.

4. Presentation of Financial Statement- The data like cost data as well as

financial data can be obtained through Management accounting. When

these data are entered in the final financial statements it makes it even

more useful for the readers and further it supports in the managerial

process like decision-making.

2. Roles and Principles of Management Accounting

There are many roles and principles of Management accounting. Some of them

are as follows:

1. Influence- Management accounting emphasises more on an effective

communication as it benefits in making significant decisions after

considering all the other factors. An effective communication is one

which consists of all the important information required for correct

decision making.

2. Relevancy- Management accounting aids the management of the

organisation in making important decisions. Therefore, it should consist

of such information which are high on quality as well as are relevant

and could assist in taking quality decisions.

3. Focuses on Generating Value- Management accounting focus more on

the generation of values instead of simply analysing the data.

Generation of values means focusing more on the factors like costs,

risks and opportunities relating to value generation.

3

Management Accounting

3. Types of Management Accounting System and Its Application in

Organisation

There are many kinds of management accounting systems whose requirements

are discussed as follows:

A. Job Costing System

It refers to a system where manufacturing cost are assigned to each of the

distinct product. At the same time, expenses are also monitored and

proper records are kept. The company producing the identical products

can employ this system for tracking their order expenses. The system

works in the following manner:

a) Enquiry is Received- The quality, price and time taken for the order

completion are the factors which actually matter to the consumers.

b) Estimation of Job’s Price- The price of the job is estimated by the

accounted after considering the factors like tastes and preferences

of the customers.

c) Receiving order- The order gets confirmed once the customer is

satisfied with the price associated with the offered product.

d) Order for Production- Production process starts after order for

production is placed with the production department.

e) Cost Recording-Each cost arising during the process of production is

recorded.

f) Job Completion- Once the production is done, a final completion

report is forwarded to the accounts department of the organisation.

Then accounts department decides on the final costing for the job

after making proper comparison with the budgeted or estimated

cost.

B. Price Optimising System

To control the prices of the resources price optimising system is used. The

prices of the multiple products at a time can be decided by the companies

with the help of price optimising system. This system also aids in

understanding how demand fluctuation takes place at the different levels

of prices. The factors like product life cycle, competitors pricing strategies

4

3. Types of Management Accounting System and Its Application in

Organisation

There are many kinds of management accounting systems whose requirements

are discussed as follows:

A. Job Costing System

It refers to a system where manufacturing cost are assigned to each of the

distinct product. At the same time, expenses are also monitored and

proper records are kept. The company producing the identical products

can employ this system for tracking their order expenses. The system

works in the following manner:

a) Enquiry is Received- The quality, price and time taken for the order

completion are the factors which actually matter to the consumers.

b) Estimation of Job’s Price- The price of the job is estimated by the

accounted after considering the factors like tastes and preferences

of the customers.

c) Receiving order- The order gets confirmed once the customer is

satisfied with the price associated with the offered product.

d) Order for Production- Production process starts after order for

production is placed with the production department.

e) Cost Recording-Each cost arising during the process of production is

recorded.

f) Job Completion- Once the production is done, a final completion

report is forwarded to the accounts department of the organisation.

Then accounts department decides on the final costing for the job

after making proper comparison with the budgeted or estimated

cost.

B. Price Optimising System

To control the prices of the resources price optimising system is used. The

prices of the multiple products at a time can be decided by the companies

with the help of price optimising system. This system also aids in

understanding how demand fluctuation takes place at the different levels

of prices. The factors like product life cycle, competitors pricing strategies

4

Management Accounting

etc. are taken into account by the price optimisation system before

deciding the final prices of the product within the organisation. Sometimes

the prices are optimised to satisfy the business strategy. No doubt, that

the management accounting system is placed to increase the price of the

product as much as the same product’s demand is maximised. However,

the management sometimes need to set the prices to affect or change the

competitors’ market positioning.

C. Cost Accounting System

Cost Accounting system assist companies in computing product

production cost. A cost accounting system is considered good and

effective only if it meets the following two essentials:

a. Total support and cooperation of different departments are required in

the formation of an effective cost accounting system. It would facilitate

in correct decision relating to ascertainment of product price.

b. The cost accounting system should be such that it adapts itself as per

the needs of users and the company. The system should not be

complex and rather it should be easy to understand and execute.

D. Inventory Management System

This system helps in managing and supervising the non-capitalized assets

plus stocks of the organisation. Integration with such system could help

the companies to maintain an effective and efficient inventory flow inside

the company and also at the sales point.

4. Management Accounting Reporting

Management Accounting Reports are prepared for assisting the management of

the organisation in doing proper forecasts and making sound decisions. There

are various reports which are prepared in an organisation which contains the

important statistical data as well as financial data. These data plays a key role in

making quality decisions for the growth and profitability of an organisation.

1. Budgeting Reports- Budgets are an important part of managerial

accounting which are prepared on the basis of past figures and

accordingly projections are made. Companies try to meet their expenses

5

etc. are taken into account by the price optimisation system before

deciding the final prices of the product within the organisation. Sometimes

the prices are optimised to satisfy the business strategy. No doubt, that

the management accounting system is placed to increase the price of the

product as much as the same product’s demand is maximised. However,

the management sometimes need to set the prices to affect or change the

competitors’ market positioning.

C. Cost Accounting System

Cost Accounting system assist companies in computing product

production cost. A cost accounting system is considered good and

effective only if it meets the following two essentials:

a. Total support and cooperation of different departments are required in

the formation of an effective cost accounting system. It would facilitate

in correct decision relating to ascertainment of product price.

b. The cost accounting system should be such that it adapts itself as per

the needs of users and the company. The system should not be

complex and rather it should be easy to understand and execute.

D. Inventory Management System

This system helps in managing and supervising the non-capitalized assets

plus stocks of the organisation. Integration with such system could help

the companies to maintain an effective and efficient inventory flow inside

the company and also at the sales point.

4. Management Accounting Reporting

Management Accounting Reports are prepared for assisting the management of

the organisation in doing proper forecasts and making sound decisions. There

are various reports which are prepared in an organisation which contains the

important statistical data as well as financial data. These data plays a key role in

making quality decisions for the growth and profitability of an organisation.

1. Budgeting Reports- Budgets are an important part of managerial

accounting which are prepared on the basis of past figures and

accordingly projections are made. Companies try to meet their expenses

5

Management Accounting

as per the budget and these budgets help the managers in reducing

unnecessary costs.

2. Job Cost Report- This report is prepared after considering the costs

associated with raw material, overhead, labour etc. This facilitates the

managers to compare between the cost of product and the selling price of

the product which ultimately assist in increasing the profit margin.

3. Performance Report- The actual revenues and expenditures are

compared with the budgeted revenues and expenditures. The difference

arising in the actual and budgeted and other such related information are

recorded in the performance report. This report would be analysed and

then required changes would be made at the time of making new budgets.

This would help the managers in planning the demand for future.

Other reports like, Order Information Report- Order Information Reports

makes the comparison between the orders placed and orders received and also

defines the backlog information (Edmonds and Olds, 2013).

Table A: Integration of Management Accounting Systems and Management

Accounting Reporting with Company X

Let us assume the name of the company given in the case as "Company X"

Type of Reporting Integration with Organisational Process

Budgeting Reports

If the organisational process of the Company X

would be integrated with the budgeting

reports, it would facilitate the company's

activities to be carried out in a more target

and objective oriented manner.

Job Cost Report

The process of company X should be carried

out in a way to reduce or minimise cost. These

Job cost reports would further help the

Company X in understanding and formulating

proper pricing strategies and minimising the

cost of production.

Performance Reports

When the activities of Company X would be

integrated with the performance report, it

would help the company to formulate its

strategies for future regarding productions,

6

as per the budget and these budgets help the managers in reducing

unnecessary costs.

2. Job Cost Report- This report is prepared after considering the costs

associated with raw material, overhead, labour etc. This facilitates the

managers to compare between the cost of product and the selling price of

the product which ultimately assist in increasing the profit margin.

3. Performance Report- The actual revenues and expenditures are

compared with the budgeted revenues and expenditures. The difference

arising in the actual and budgeted and other such related information are

recorded in the performance report. This report would be analysed and

then required changes would be made at the time of making new budgets.

This would help the managers in planning the demand for future.

Other reports like, Order Information Report- Order Information Reports

makes the comparison between the orders placed and orders received and also

defines the backlog information (Edmonds and Olds, 2013).

Table A: Integration of Management Accounting Systems and Management

Accounting Reporting with Company X

Let us assume the name of the company given in the case as "Company X"

Type of Reporting Integration with Organisational Process

Budgeting Reports

If the organisational process of the Company X

would be integrated with the budgeting

reports, it would facilitate the company's

activities to be carried out in a more target

and objective oriented manner.

Job Cost Report

The process of company X should be carried

out in a way to reduce or minimise cost. These

Job cost reports would further help the

Company X in understanding and formulating

proper pricing strategies and minimising the

cost of production.

Performance Reports

When the activities of Company X would be

integrated with the performance report, it

would help the company to formulate its

strategies for future regarding productions,

6

Management Accounting

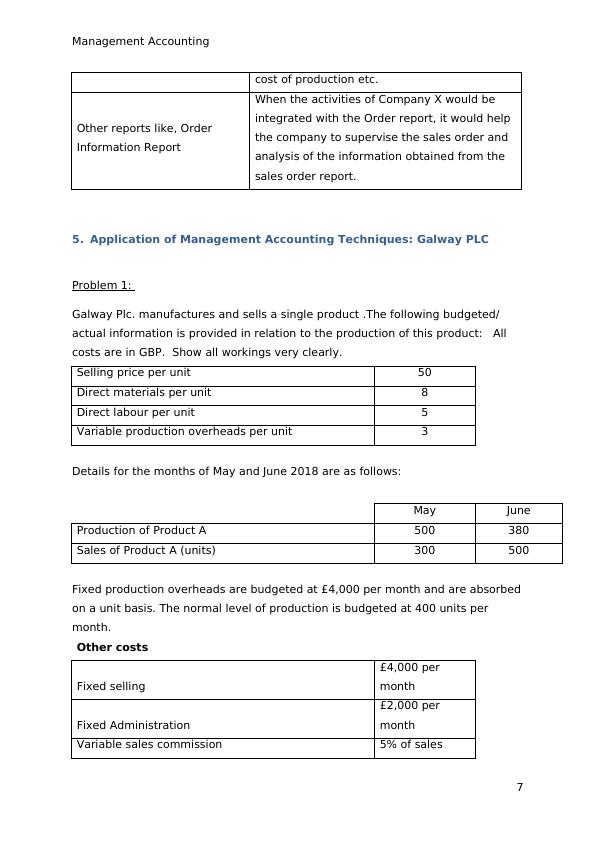

cost of production etc.

Other reports like, Order

Information Report

When the activities of Company X would be

integrated with the Order report, it would help

the company to supervise the sales order and

analysis of the information obtained from the

sales order report.

5. Application of Management Accounting Techniques: Galway PLC

Problem 1:

Galway Plc. manufactures and sells a single product .The following budgeted/

actual information is provided in relation to the production of this product: All

costs are in GBP. Show all workings very clearly.

Selling price per unit 50

Direct materials per unit 8

Direct labour per unit 5

Variable production overheads per unit 3

Details for the months of May and June 2018 are as follows:

May June

Production of Product A 500 380

Sales of Product A (units) 300 500

Fixed production overheads are budgeted at £4,000 per month and are absorbed

on a unit basis. The normal level of production is budgeted at 400 units per

month.

Other costs

Fixed selling

£4,000 per

month

Fixed Administration

£2,000 per

month

Variable sales commission 5% of sales

7

cost of production etc.

Other reports like, Order

Information Report

When the activities of Company X would be

integrated with the Order report, it would help

the company to supervise the sales order and

analysis of the information obtained from the

sales order report.

5. Application of Management Accounting Techniques: Galway PLC

Problem 1:

Galway Plc. manufactures and sells a single product .The following budgeted/

actual information is provided in relation to the production of this product: All

costs are in GBP. Show all workings very clearly.

Selling price per unit 50

Direct materials per unit 8

Direct labour per unit 5

Variable production overheads per unit 3

Details for the months of May and June 2018 are as follows:

May June

Production of Product A 500 380

Sales of Product A (units) 300 500

Fixed production overheads are budgeted at £4,000 per month and are absorbed

on a unit basis. The normal level of production is budgeted at 400 units per

month.

Other costs

Fixed selling

£4,000 per

month

Fixed Administration

£2,000 per

month

Variable sales commission 5% of sales

7

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

TASK 11 P1 Management Accounting INTRODUCTION 1 TASK 11 P1 Management Accounting INTRODUCTION 3 D1 Benefits of management accounting system 4 M2 Preparation of Income statelg...

|20

|3972

|257

Management Accounting and its Essential Requirementslg...

|19

|5325

|21

Concept of Management Accounting - Doclg...

|18

|5303

|370

Management Accounting and Reporting: Essential Requirements and Methodslg...

|18

|5545

|54

Management Accounting Assignment - Excite Entertainment Ltdlg...

|17

|5572

|50

Essential Requirement of Management Accounting.lg...

|22

|6249

|150