Management Accounting Report: Cost Analysis for Jeffrey & Sons Ltd

VerifiedAdded on 2020/01/07

|20

|4687

|70

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on a case study of Jeffrey & Sons Ltd. It begins by classifying different types of costs and calculating unit and total job costs using job costing methods. The report then calculates the cost of a product, 'Exquisite,' using various allocation techniques and analyzes the cost data. It further includes the preparation and analysis of a cost report for September, along with the use of performance indicators to identify areas for improvement. The report also delves into budgeting processes, including production, purchase, and cash budgets. Finally, it covers the computation and analysis of variances, culminating in an operating statement and a variance analysis report, providing recommendations for cost reduction and value enhancement.

Management

accounting

accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

1.1 Classification of different types of cost.................................................................................3

1.2 Computation of unit cost and total job cost for Job 444........................................................4

1.3 Calculation of the cost of Exquisite using appropriate techniques........................................4

1.4 Analysis of cost data of exquisite using appropriate techniques...........................................8

Task 2...............................................................................................................................................8

2.1 Preparation and analysis of the cost report for the month of September...............................8

2.2 Use of several performance indicators in order to identify area for further improvement. .10

2.3 Recommendations for reduction of cost and enhancement of value and quality................10

Task 3.............................................................................................................................................11

3.1 Purpose and nature of budgeting process............................................................................11

3.2 Selection of appropriable budgeting methods in accordance with the needs of organization

...................................................................................................................................................11

3.3 Production and purchase budget..........................................................................................11

3.4 Preparation of cash budget...................................................................................................12

Task 4.............................................................................................................................................14

4.1Computation and analysis of variances................................................................................14

4.2 Operating statement for reconciliation of budgeted and actual results................................16

4.3 Variance analysis report.......................................................................................................16

Conclusion.....................................................................................................................................17

References......................................................................................................................................18

2

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

1.1 Classification of different types of cost.................................................................................3

1.2 Computation of unit cost and total job cost for Job 444........................................................4

1.3 Calculation of the cost of Exquisite using appropriate techniques........................................4

1.4 Analysis of cost data of exquisite using appropriate techniques...........................................8

Task 2...............................................................................................................................................8

2.1 Preparation and analysis of the cost report for the month of September...............................8

2.2 Use of several performance indicators in order to identify area for further improvement. .10

2.3 Recommendations for reduction of cost and enhancement of value and quality................10

Task 3.............................................................................................................................................11

3.1 Purpose and nature of budgeting process............................................................................11

3.2 Selection of appropriable budgeting methods in accordance with the needs of organization

...................................................................................................................................................11

3.3 Production and purchase budget..........................................................................................11

3.4 Preparation of cash budget...................................................................................................12

Task 4.............................................................................................................................................14

4.1Computation and analysis of variances................................................................................14

4.2 Operating statement for reconciliation of budgeted and actual results................................16

4.3 Variance analysis report.......................................................................................................16

Conclusion.....................................................................................................................................17

References......................................................................................................................................18

2

INDEX OF TABLES

Table 1: Statement showing total and unit cost of Job 444.............................................................5

Table 2: Statement showing computation of total cost of exquisite................................................5

Table 3: Allocation of cost of support departments on the basis of machine hours........................7

Table 4: Allocation Criteria of cost ...............................................................................................8

Table 5: Units to be produced .........................................................................................................8

Table 6: Statement showing computation of exquisite....................................................................8

Table 7: Statement showing computation of exquisite....................................................................9

Table 8: Production budget of Jeffrey and Son ...........................................................................12

Table 9: Material purchase budget of Jeffrey and Son's ...............................................................13

Table 10: Cash budget of Jeffrey and Son's...................................................................................13

3

Table 1: Statement showing total and unit cost of Job 444.............................................................5

Table 2: Statement showing computation of total cost of exquisite................................................5

Table 3: Allocation of cost of support departments on the basis of machine hours........................7

Table 4: Allocation Criteria of cost ...............................................................................................8

Table 5: Units to be produced .........................................................................................................8

Table 6: Statement showing computation of exquisite....................................................................8

Table 7: Statement showing computation of exquisite....................................................................9

Table 8: Production budget of Jeffrey and Son ...........................................................................12

Table 9: Material purchase budget of Jeffrey and Son's ...............................................................13

Table 10: Cash budget of Jeffrey and Son's...................................................................................13

3

You're viewing a preview

Unlock full access by subscribing today!

INTRODUCTION

Management accounting is used in business to provide accurate and reliable information

to the managers so they can make viable decisions for their growth and success. Approaches of

management accounting consists of strategic, performance and risk management (Burns and et.

al, 2004). Present report foucues on case study of Jeffrey and Sons Ltd. In this report description

will be provided regarding theoretical and practical application of various costing approaches by

considering information of provided business. Further, cost report will be prepared in order to

provide recommendations to the company for resolving current issues by making improvement

in their operational strategies.

TASK 1

1.1 Classification of different types of cost

Cost can be defined as expenses incurred by business in order to attain an economic

benefit for business. In a business, cost can be bifurcated on the basis of following aspects: On the basis of element: According to the factor of element, cost can be segregated in

direct and indirect cost. Direct cost is incurred for the production activities while indirect

cost is incurred for attaining value added benefits (Jiambalvo, 2001). Example of direct

cost is raw material and labour and of indirect cost is rent and lightning expense. On the basis of function: Cost can also be bifurcated as per functional activities of a

business organization. General classification of the cost on the basis of function are

administration, distribution, production, advertising, research and development and

selling. On the basis of nature: As per the nature, cost can be classified into material, labour and

expenditure of overhead. Material expenses are incurred for the purchase of goods

required for production activities (Keown, 2005). Labour cost is incurred for the payment

of wages and salaries to the employees for services provided by them.

On the basis of behaviour: By considering behaviour as a factor, cost can be bifurcated

into fixed, variable and semi-variable cost. Fixed cost are those expenses which does not

alter with the change in production units (Kont, 2013). Example of fixed cost is salary,

rent and depreciation. Variable cost is just opposite to the fixed cost as it is in direct

4

Management accounting is used in business to provide accurate and reliable information

to the managers so they can make viable decisions for their growth and success. Approaches of

management accounting consists of strategic, performance and risk management (Burns and et.

al, 2004). Present report foucues on case study of Jeffrey and Sons Ltd. In this report description

will be provided regarding theoretical and practical application of various costing approaches by

considering information of provided business. Further, cost report will be prepared in order to

provide recommendations to the company for resolving current issues by making improvement

in their operational strategies.

TASK 1

1.1 Classification of different types of cost

Cost can be defined as expenses incurred by business in order to attain an economic

benefit for business. In a business, cost can be bifurcated on the basis of following aspects: On the basis of element: According to the factor of element, cost can be segregated in

direct and indirect cost. Direct cost is incurred for the production activities while indirect

cost is incurred for attaining value added benefits (Jiambalvo, 2001). Example of direct

cost is raw material and labour and of indirect cost is rent and lightning expense. On the basis of function: Cost can also be bifurcated as per functional activities of a

business organization. General classification of the cost on the basis of function are

administration, distribution, production, advertising, research and development and

selling. On the basis of nature: As per the nature, cost can be classified into material, labour and

expenditure of overhead. Material expenses are incurred for the purchase of goods

required for production activities (Keown, 2005). Labour cost is incurred for the payment

of wages and salaries to the employees for services provided by them.

On the basis of behaviour: By considering behaviour as a factor, cost can be bifurcated

into fixed, variable and semi-variable cost. Fixed cost are those expenses which does not

alter with the change in production units (Kont, 2013). Example of fixed cost is salary,

rent and depreciation. Variable cost is just opposite to the fixed cost as it is in direct

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

proportion to the units to be produced. Example of variable cost is raw material and

packaging expenses. Cost having semi-variable behaviour has element of both fixed and

variable cost. Example of semi-variable is electricity expenses.

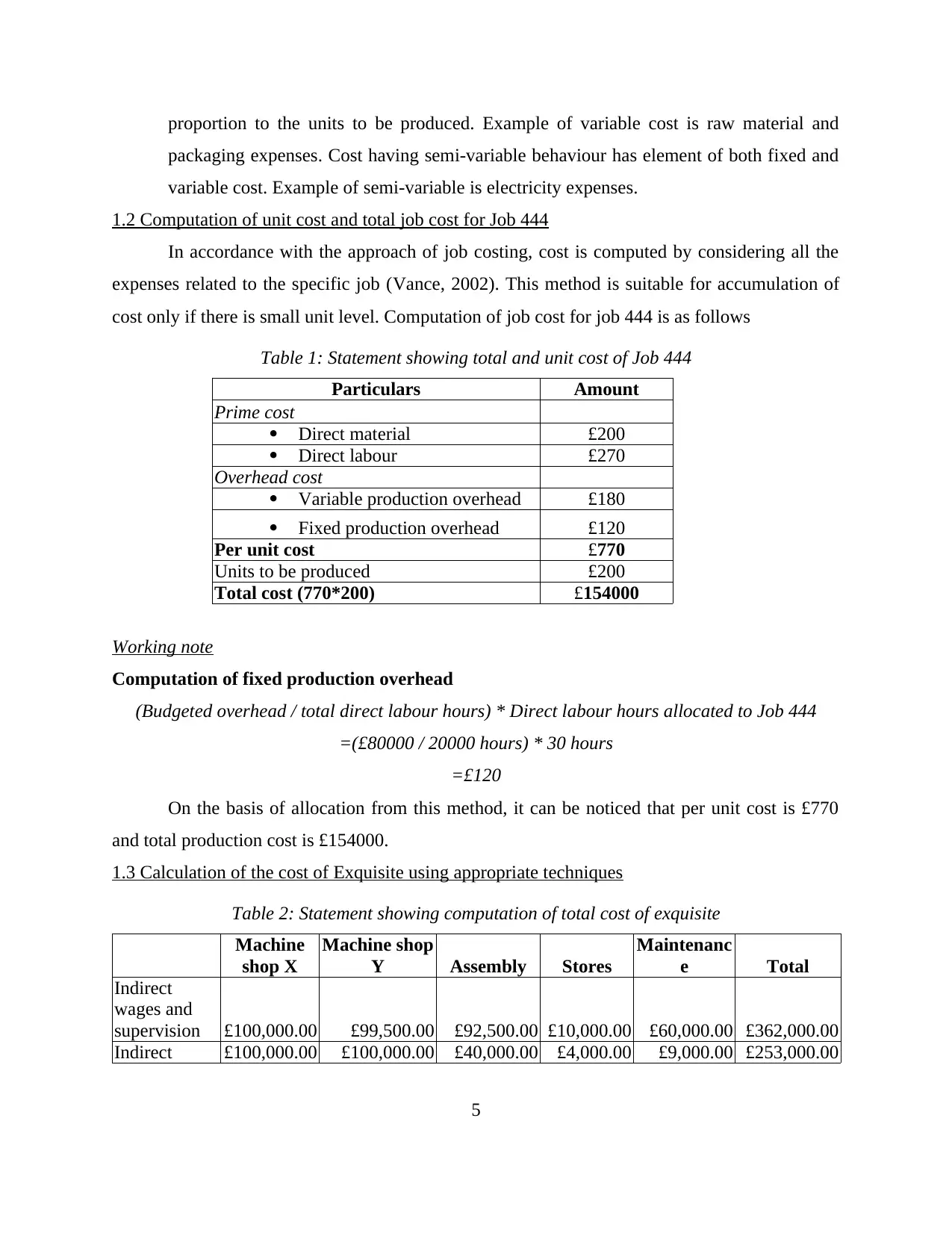

1.2 Computation of unit cost and total job cost for Job 444

In accordance with the approach of job costing, cost is computed by considering all the

expenses related to the specific job (Vance, 2002). This method is suitable for accumulation of

cost only if there is small unit level. Computation of job cost for job 444 is as follows

Table 1: Statement showing total and unit cost of Job 444

Particulars Amount

Prime cost

Direct material £200

Direct labour £270

Overhead cost

Variable production overhead £180

Fixed production overhead £120

Per unit cost £770

Units to be produced £200

Total cost (770*200) £154000

Working note

Computation of fixed production overhead

(Budgeted overhead / total direct labour hours) * Direct labour hours allocated to Job 444

=(£80000 / 20000 hours) * 30 hours

=£120

On the basis of allocation from this method, it can be noticed that per unit cost is £770

and total production cost is £154000.

1.3 Calculation of the cost of Exquisite using appropriate techniques

Table 2: Statement showing computation of total cost of exquisite

Machine

shop X

Machine shop

Y Assembly Stores

Maintenanc

e Total

Indirect

wages and

supervision £100,000.00 £99,500.00 £92,500.00 £10,000.00 £60,000.00 £362,000.00

Indirect £100,000.00 £100,000.00 £40,000.00 £4,000.00 £9,000.00 £253,000.00

5

packaging expenses. Cost having semi-variable behaviour has element of both fixed and

variable cost. Example of semi-variable is electricity expenses.

1.2 Computation of unit cost and total job cost for Job 444

In accordance with the approach of job costing, cost is computed by considering all the

expenses related to the specific job (Vance, 2002). This method is suitable for accumulation of

cost only if there is small unit level. Computation of job cost for job 444 is as follows

Table 1: Statement showing total and unit cost of Job 444

Particulars Amount

Prime cost

Direct material £200

Direct labour £270

Overhead cost

Variable production overhead £180

Fixed production overhead £120

Per unit cost £770

Units to be produced £200

Total cost (770*200) £154000

Working note

Computation of fixed production overhead

(Budgeted overhead / total direct labour hours) * Direct labour hours allocated to Job 444

=(£80000 / 20000 hours) * 30 hours

=£120

On the basis of allocation from this method, it can be noticed that per unit cost is £770

and total production cost is £154000.

1.3 Calculation of the cost of Exquisite using appropriate techniques

Table 2: Statement showing computation of total cost of exquisite

Machine

shop X

Machine shop

Y Assembly Stores

Maintenanc

e Total

Indirect

wages and

supervision £100,000.00 £99,500.00 £92,500.00 £10,000.00 £60,000.00 £362,000.00

Indirect £100,000.00 £100,000.00 £40,000.00 £4,000.00 £9,000.00 £253,000.00

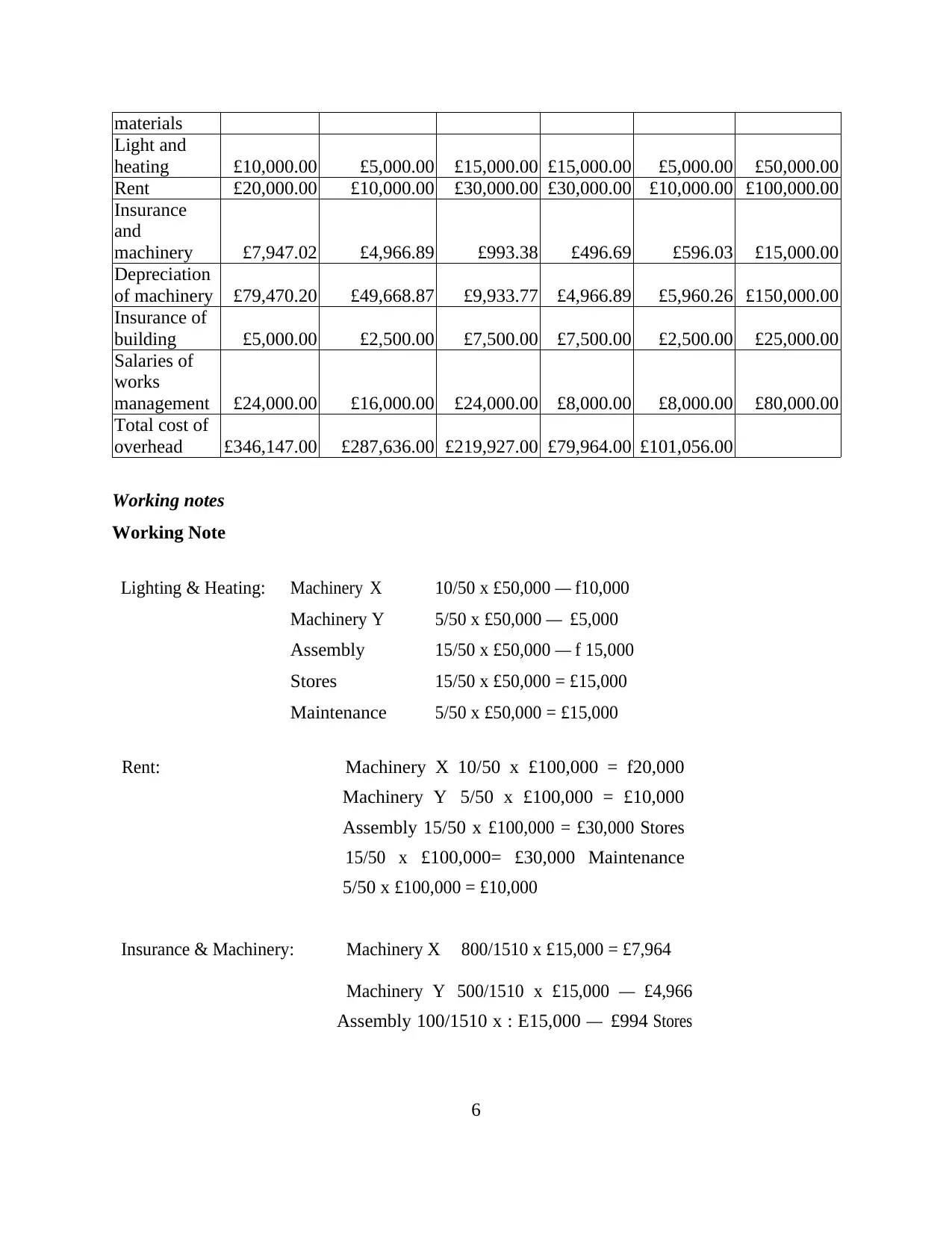

5

materials

Light and

heating £10,000.00 £5,000.00 £15,000.00 £15,000.00 £5,000.00 £50,000.00

Rent £20,000.00 £10,000.00 £30,000.00 £30,000.00 £10,000.00 £100,000.00

Insurance

and

machinery £7,947.02 £4,966.89 £993.38 £496.69 £596.03 £15,000.00

Depreciation

of machinery £79,470.20 £49,668.87 £9,933.77 £4,966.89 £5,960.26 £150,000.00

Insurance of

building £5,000.00 £2,500.00 £7,500.00 £7,500.00 £2,500.00 £25,000.00

Salaries of

works

management £24,000.00 £16,000.00 £24,000.00 £8,000.00 £8,000.00 £80,000.00

Total cost of

overhead £346,147.00 £287,636.00 £219,927.00 £79,964.00 £101,056.00

Working notes

Working Note

Lighting & Heating: Machinery X 10/50 x £50,000 — f10,000

Machinery Y 5/50 x £50,000 — £5,000

Assembly 15/50 x £50,000 — f 15,000

Stores 15/50 x £50,000 = £15,000

Maintenance 5/50 x £50,000 = £15,000

Rent: Machinery X 10/50 x £100,000 = f20,000

Machinery Y 5/50 x £100,000 = £10,000

Assembly 15/50 x £100,000 = £30,000 Stores

15/50 x £100,000= £30,000 Maintenance

5/50 x £100,000 = £10,000

Insurance & Machinery: Machinery X 800/1510 x £15,000 = £7,964

Machinery Y 500/1510 x £15,000 — £4,966

Assembly 100/1510 x : E15,000 — £994 Stores

6

Light and

heating £10,000.00 £5,000.00 £15,000.00 £15,000.00 £5,000.00 £50,000.00

Rent £20,000.00 £10,000.00 £30,000.00 £30,000.00 £10,000.00 £100,000.00

Insurance

and

machinery £7,947.02 £4,966.89 £993.38 £496.69 £596.03 £15,000.00

Depreciation

of machinery £79,470.20 £49,668.87 £9,933.77 £4,966.89 £5,960.26 £150,000.00

Insurance of

building £5,000.00 £2,500.00 £7,500.00 £7,500.00 £2,500.00 £25,000.00

Salaries of

works

management £24,000.00 £16,000.00 £24,000.00 £8,000.00 £8,000.00 £80,000.00

Total cost of

overhead £346,147.00 £287,636.00 £219,927.00 £79,964.00 £101,056.00

Working notes

Working Note

Lighting & Heating: Machinery X 10/50 x £50,000 — f10,000

Machinery Y 5/50 x £50,000 — £5,000

Assembly 15/50 x £50,000 — f 15,000

Stores 15/50 x £50,000 = £15,000

Maintenance 5/50 x £50,000 = £15,000

Rent: Machinery X 10/50 x £100,000 = f20,000

Machinery Y 5/50 x £100,000 = £10,000

Assembly 15/50 x £100,000 = £30,000 Stores

15/50 x £100,000= £30,000 Maintenance

5/50 x £100,000 = £10,000

Insurance & Machinery: Machinery X 800/1510 x £15,000 = £7,964

Machinery Y 500/1510 x £15,000 — £4,966

Assembly 100/1510 x : E15,000 — £994 Stores

6

You're viewing a preview

Unlock full access by subscribing today!

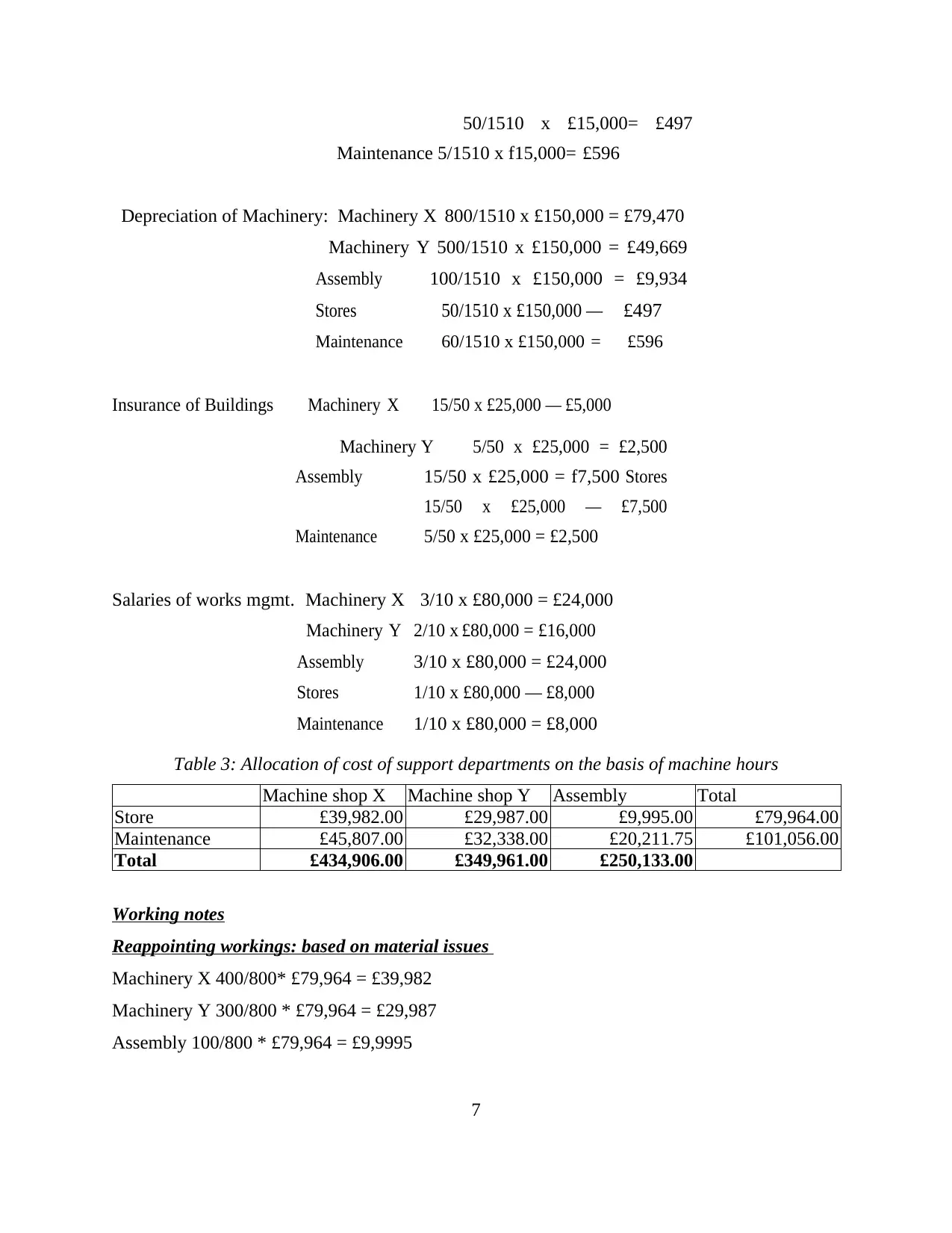

50/1510 x £15,000= £497

Maintenance 5/1510 x f15,000= £596

Depreciation of Machinery: Machinery X 800/1510 x £150,000 = £79,470

Machinery Y 500/1510 x £150,000 = £49,669

Assembly 100/1510 x £150,000 = £9,934

Stores 50/1510 x £150,000 — £497

Maintenance 60/1510 x £150,000 = £596

Insurance of Buildings Machinery X 15/50 x £25,000 — £5,000

Machinery Y 5/50 x £25,000 = £2,500

Assembly 15/50 x £25,000 = f7,500 Stores

15/50 x £25,000 — £7,500

Maintenance 5/50 x £25,000 = £2,500

Salaries of works mgmt. Machinery X 3/10 x £80,000 = £24,000

Machinery Y 2/10 x £80,000 = £16,000

Assembly 3/10 x £80,000 = £24,000

Stores 1/10 x £80,000 — £8,000

Maintenance 1/10 x £80,000 = £8,000

Table 3: Allocation of cost of support departments on the basis of machine hours

Machine shop X Machine shop Y Assembly Total

Store £39,982.00 £29,987.00 £9,995.00 £79,964.00

Maintenance £45,807.00 £32,338.00 £20,211.75 £101,056.00

Total £434,906.00 £349,961.00 £250,133.00

Working notes

Reappointing workings: based on material issues

Machinery X 400/800* £79,964 = £39,982

Machinery Y 300/800 * £79,964 = £29,987

Assembly 100/800 * £79,964 = £9,9995

7

Maintenance 5/1510 x f15,000= £596

Depreciation of Machinery: Machinery X 800/1510 x £150,000 = £79,470

Machinery Y 500/1510 x £150,000 = £49,669

Assembly 100/1510 x £150,000 = £9,934

Stores 50/1510 x £150,000 — £497

Maintenance 60/1510 x £150,000 = £596

Insurance of Buildings Machinery X 15/50 x £25,000 — £5,000

Machinery Y 5/50 x £25,000 = £2,500

Assembly 15/50 x £25,000 = f7,500 Stores

15/50 x £25,000 — £7,500

Maintenance 5/50 x £25,000 = £2,500

Salaries of works mgmt. Machinery X 3/10 x £80,000 = £24,000

Machinery Y 2/10 x £80,000 = £16,000

Assembly 3/10 x £80,000 = £24,000

Stores 1/10 x £80,000 — £8,000

Maintenance 1/10 x £80,000 = £8,000

Table 3: Allocation of cost of support departments on the basis of machine hours

Machine shop X Machine shop Y Assembly Total

Store £39,982.00 £29,987.00 £9,995.00 £79,964.00

Maintenance £45,807.00 £32,338.00 £20,211.75 £101,056.00

Total £434,906.00 £349,961.00 £250,133.00

Working notes

Reappointing workings: based on material issues

Machinery X 400/800* £79,964 = £39,982

Machinery Y 300/800 * £79,964 = £29,987

Assembly 100/800 * £79,964 = £9,9995

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

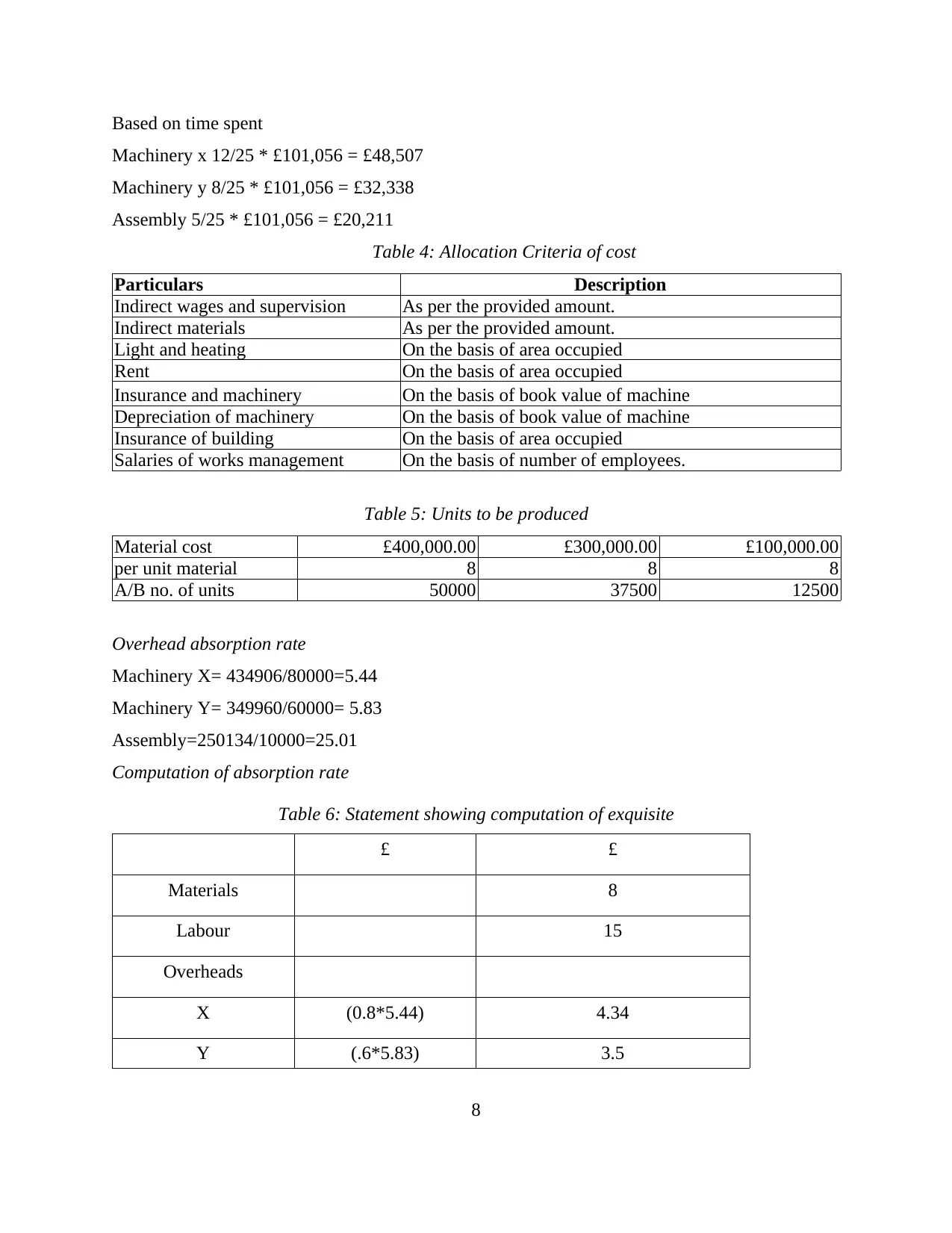

Based on time spent

Machinery x 12/25 * £101,056 = £48,507

Machinery y 8/25 * £101,056 = £32,338

Assembly 5/25 * £101,056 = £20,211

Table 4: Allocation Criteria of cost

Particulars Description

Indirect wages and supervision As per the provided amount.

Indirect materials As per the provided amount.

Light and heating On the basis of area occupied

Rent On the basis of area occupied

Insurance and machinery On the basis of book value of machine

Depreciation of machinery On the basis of book value of machine

Insurance of building On the basis of area occupied

Salaries of works management On the basis of number of employees.

Table 5: Units to be produced

Material cost £400,000.00 £300,000.00 £100,000.00

per unit material 8 8 8

A/B no. of units 50000 37500 12500

Overhead absorption rate

Machinery X= 434906/80000=5.44

Machinery Y= 349960/60000= 5.83

Assembly=250134/10000=25.01

Computation of absorption rate

Table 6: Statement showing computation of exquisite

£ £

Materials 8

Labour 15

Overheads

X (0.8*5.44) 4.34

Y (.6*5.83) 3.5

8

Machinery x 12/25 * £101,056 = £48,507

Machinery y 8/25 * £101,056 = £32,338

Assembly 5/25 * £101,056 = £20,211

Table 4: Allocation Criteria of cost

Particulars Description

Indirect wages and supervision As per the provided amount.

Indirect materials As per the provided amount.

Light and heating On the basis of area occupied

Rent On the basis of area occupied

Insurance and machinery On the basis of book value of machine

Depreciation of machinery On the basis of book value of machine

Insurance of building On the basis of area occupied

Salaries of works management On the basis of number of employees.

Table 5: Units to be produced

Material cost £400,000.00 £300,000.00 £100,000.00

per unit material 8 8 8

A/B no. of units 50000 37500 12500

Overhead absorption rate

Machinery X= 434906/80000=5.44

Machinery Y= 349960/60000= 5.83

Assembly=250134/10000=25.01

Computation of absorption rate

Table 6: Statement showing computation of exquisite

£ £

Materials 8

Labour 15

Overheads

X (0.8*5.44) 4.34

Y (.6*5.83) 3.5

8

Assembly (.1*25.01) 2.5

Total cost 33.35

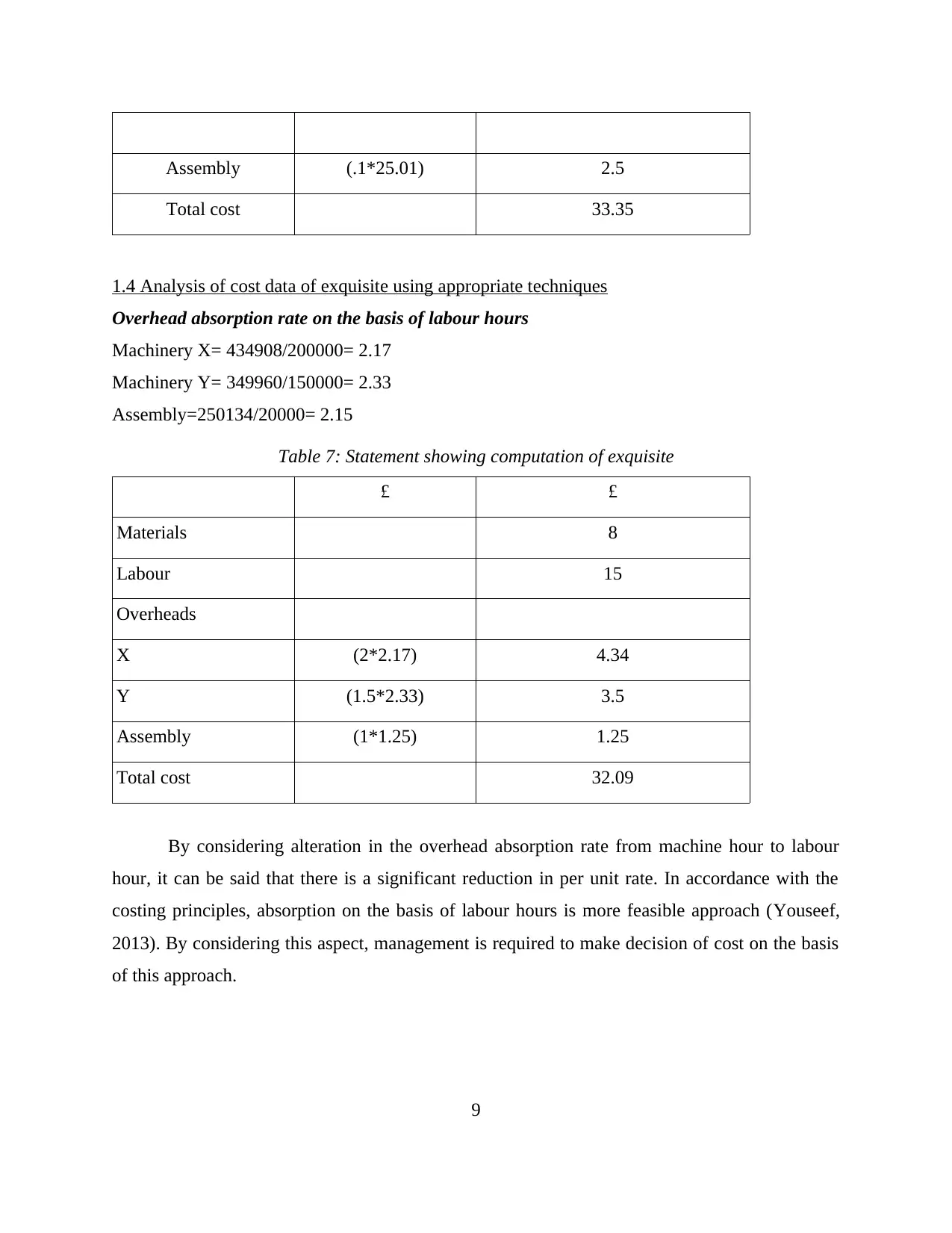

1.4 Analysis of cost data of exquisite using appropriate techniques

Overhead absorption rate on the basis of labour hours

Machinery X= 434908/200000= 2.17

Machinery Y= 349960/150000= 2.33

Assembly=250134/20000= 2.15

Table 7: Statement showing computation of exquisite

£ £

Materials 8

Labour 15

Overheads

X (2*2.17) 4.34

Y (1.5*2.33) 3.5

Assembly (1*1.25) 1.25

Total cost 32.09

By considering alteration in the overhead absorption rate from machine hour to labour

hour, it can be said that there is a significant reduction in per unit rate. In accordance with the

costing principles, absorption on the basis of labour hours is more feasible approach (Youseef,

2013). By considering this aspect, management is required to make decision of cost on the basis

of this approach.

9

Total cost 33.35

1.4 Analysis of cost data of exquisite using appropriate techniques

Overhead absorption rate on the basis of labour hours

Machinery X= 434908/200000= 2.17

Machinery Y= 349960/150000= 2.33

Assembly=250134/20000= 2.15

Table 7: Statement showing computation of exquisite

£ £

Materials 8

Labour 15

Overheads

X (2*2.17) 4.34

Y (1.5*2.33) 3.5

Assembly (1*1.25) 1.25

Total cost 32.09

By considering alteration in the overhead absorption rate from machine hour to labour

hour, it can be said that there is a significant reduction in per unit rate. In accordance with the

costing principles, absorption on the basis of labour hours is more feasible approach (Youseef,

2013). By considering this aspect, management is required to make decision of cost on the basis

of this approach.

9

You're viewing a preview

Unlock full access by subscribing today!

TASK 2

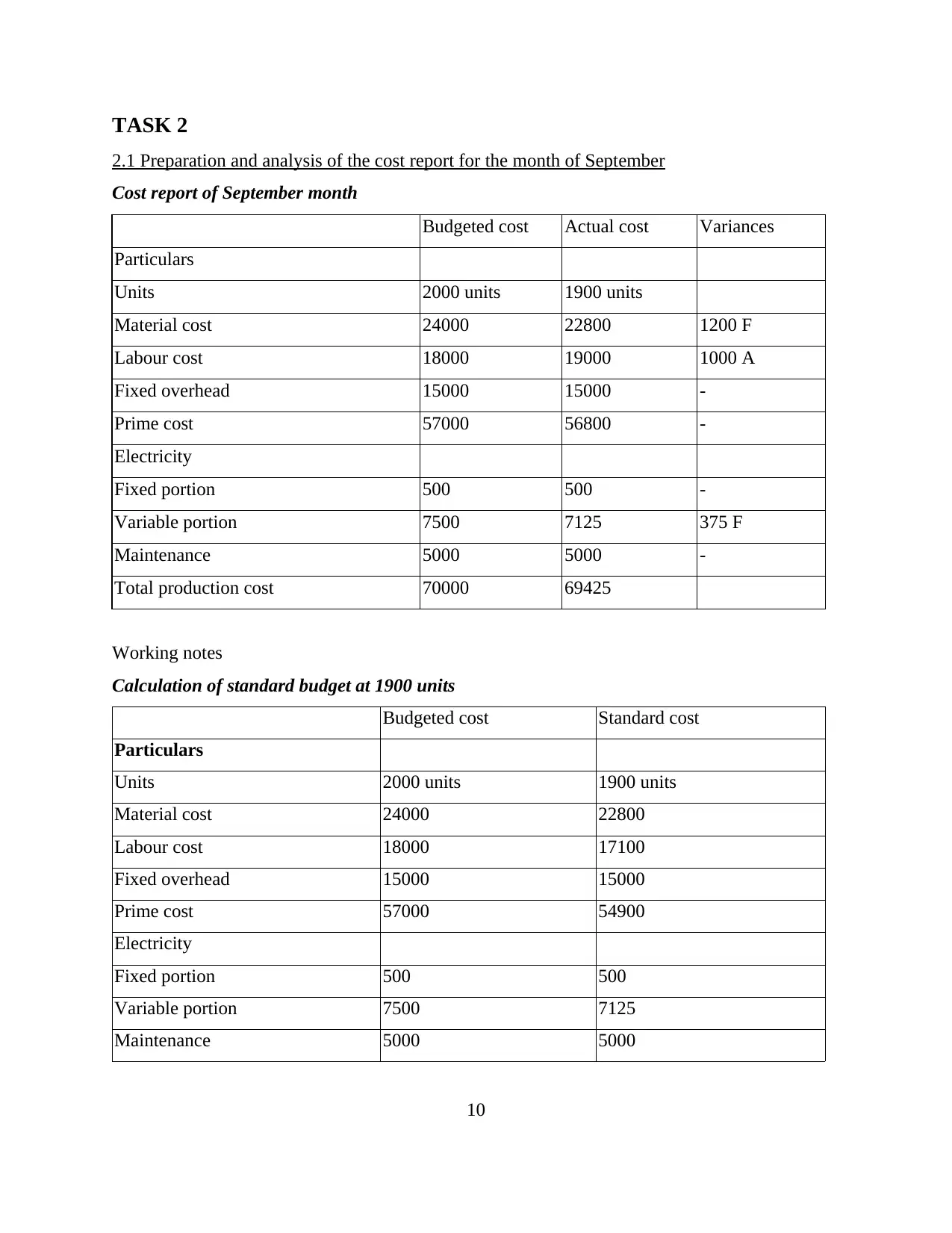

2.1 Preparation and analysis of the cost report for the month of September

Cost report of September month

Budgeted cost Actual cost Variances

Particulars

Units 2000 units 1900 units

Material cost 24000 22800 1200 F

Labour cost 18000 19000 1000 A

Fixed overhead 15000 15000 -

Prime cost 57000 56800 -

Electricity

Fixed portion 500 500 -

Variable portion 7500 7125 375 F

Maintenance 5000 5000 -

Total production cost 70000 69425

Working notes

Calculation of standard budget at 1900 units

Budgeted cost Standard cost

Particulars

Units 2000 units 1900 units

Material cost 24000 22800

Labour cost 18000 17100

Fixed overhead 15000 15000

Prime cost 57000 54900

Electricity

Fixed portion 500 500

Variable portion 7500 7125

Maintenance 5000 5000

10

2.1 Preparation and analysis of the cost report for the month of September

Cost report of September month

Budgeted cost Actual cost Variances

Particulars

Units 2000 units 1900 units

Material cost 24000 22800 1200 F

Labour cost 18000 19000 1000 A

Fixed overhead 15000 15000 -

Prime cost 57000 56800 -

Electricity

Fixed portion 500 500 -

Variable portion 7500 7125 375 F

Maintenance 5000 5000 -

Total production cost 70000 69425

Working notes

Calculation of standard budget at 1900 units

Budgeted cost Standard cost

Particulars

Units 2000 units 1900 units

Material cost 24000 22800

Labour cost 18000 17100

Fixed overhead 15000 15000

Prime cost 57000 54900

Electricity

Fixed portion 500 500

Variable portion 7500 7125

Maintenance 5000 5000

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

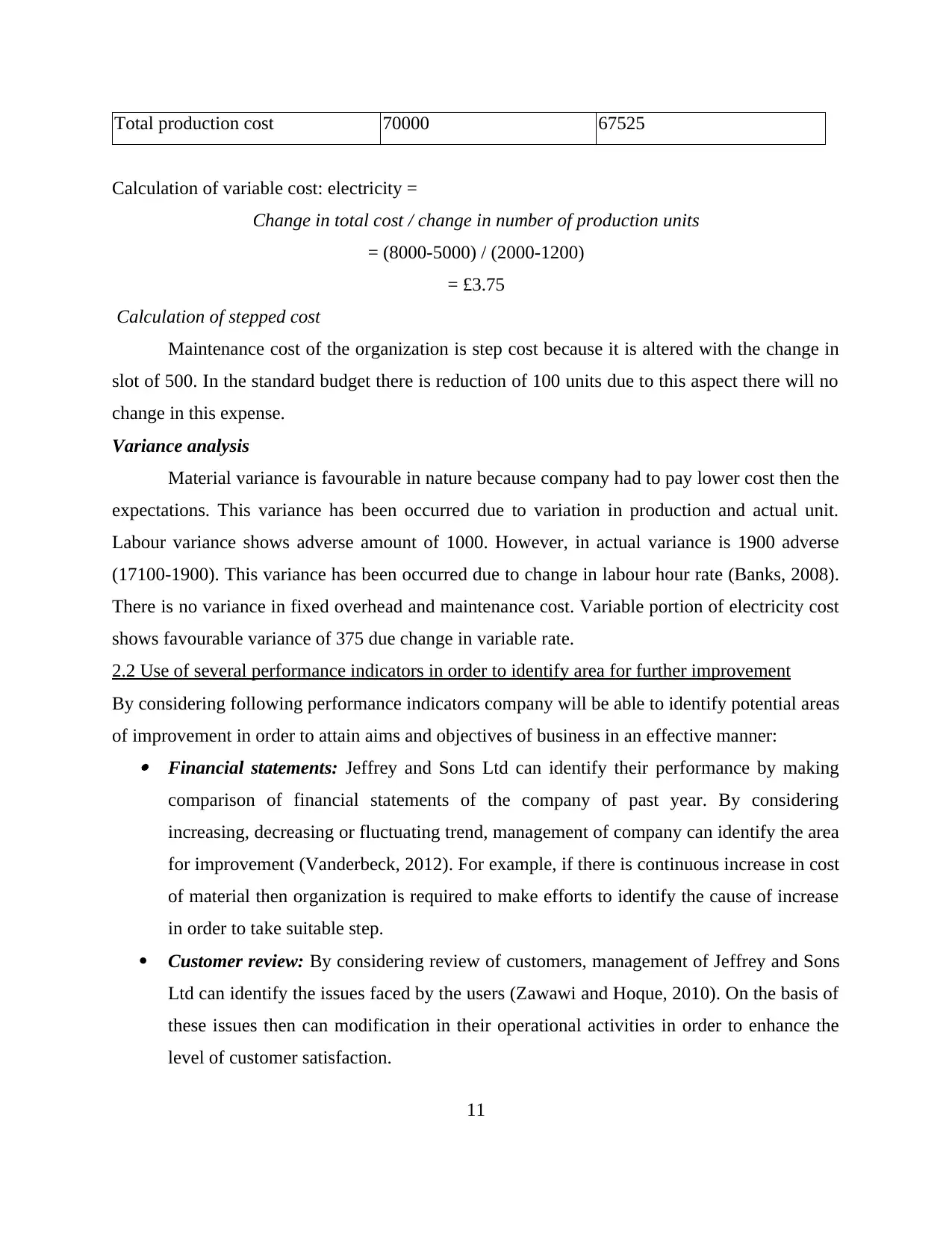

Total production cost 70000 67525

Calculation of variable cost: electricity =

Change in total cost / change in number of production units

= (8000-5000) / (2000-1200)

= £3.75

Calculation of stepped cost

Maintenance cost of the organization is step cost because it is altered with the change in

slot of 500. In the standard budget there is reduction of 100 units due to this aspect there will no

change in this expense.

Variance analysis

Material variance is favourable in nature because company had to pay lower cost then the

expectations. This variance has been occurred due to variation in production and actual unit.

Labour variance shows adverse amount of 1000. However, in actual variance is 1900 adverse

(17100-1900). This variance has been occurred due to change in labour hour rate (Banks, 2008).

There is no variance in fixed overhead and maintenance cost. Variable portion of electricity cost

shows favourable variance of 375 due change in variable rate.

2.2 Use of several performance indicators in order to identify area for further improvement

By considering following performance indicators company will be able to identify potential areas

of improvement in order to attain aims and objectives of business in an effective manner: Financial statements: Jeffrey and Sons Ltd can identify their performance by making

comparison of financial statements of the company of past year. By considering

increasing, decreasing or fluctuating trend, management of company can identify the area

for improvement (Vanderbeck, 2012). For example, if there is continuous increase in cost

of material then organization is required to make efforts to identify the cause of increase

in order to take suitable step.

Customer review: By considering review of customers, management of Jeffrey and Sons

Ltd can identify the issues faced by the users (Zawawi and Hoque, 2010). On the basis of

these issues then can modification in their operational activities in order to enhance the

level of customer satisfaction.

11

Calculation of variable cost: electricity =

Change in total cost / change in number of production units

= (8000-5000) / (2000-1200)

= £3.75

Calculation of stepped cost

Maintenance cost of the organization is step cost because it is altered with the change in

slot of 500. In the standard budget there is reduction of 100 units due to this aspect there will no

change in this expense.

Variance analysis

Material variance is favourable in nature because company had to pay lower cost then the

expectations. This variance has been occurred due to variation in production and actual unit.

Labour variance shows adverse amount of 1000. However, in actual variance is 1900 adverse

(17100-1900). This variance has been occurred due to change in labour hour rate (Banks, 2008).

There is no variance in fixed overhead and maintenance cost. Variable portion of electricity cost

shows favourable variance of 375 due change in variable rate.

2.2 Use of several performance indicators in order to identify area for further improvement

By considering following performance indicators company will be able to identify potential areas

of improvement in order to attain aims and objectives of business in an effective manner: Financial statements: Jeffrey and Sons Ltd can identify their performance by making

comparison of financial statements of the company of past year. By considering

increasing, decreasing or fluctuating trend, management of company can identify the area

for improvement (Vanderbeck, 2012). For example, if there is continuous increase in cost

of material then organization is required to make efforts to identify the cause of increase

in order to take suitable step.

Customer review: By considering review of customers, management of Jeffrey and Sons

Ltd can identify the issues faced by the users (Zawawi and Hoque, 2010). On the basis of

these issues then can modification in their operational activities in order to enhance the

level of customer satisfaction.

11

2.3 Recommendations for reduction of cost and enhancement of value and quality

Management of Jeffrey and Sons Ltd is recommended to take suitable steps for the

prevention of variances in actual and budgeted values. For this aspect, management can use

following aspects: Just in time and economic order quantity: By the applicability of this technique,

organization can reduce their material cost as there will be optimization is store and order

cost. By ordering economic order quantity, there will be prevention of stock out issue and

reduction in abnormal loss. TQM and Kaizen costing: TQM approach is focused on improvement of overall

production process in order to enhance the quality. With the use of this approach, Jeffrey

and Sons Ltd can resolve quality issues in production process (Cohen and Kaimenaki,

2011). Further, Kaizen costing can be used by organization for the reduction of wastage.

Management audit: This approach is suitable to develop effective internal control in a

business organization. With this technique, organization can monitor the performance of

employees in order to assure standard outcome.

TASK 3

3.1 Purpose and nature of budgeting process

Budgetary statements are prepared by business entity to make estimation of future

expenses and revenue on the basis of previous financial facts and current market trends. On the

basis of budget estimations, resources are allocated into various business activities in order to

enhance its revenue and profitability. Budgets are also used by business to make comparison to

actual and expected outcome to make improvement in operational strategies. Preparation of

budgets is accomplished on the basis of forecasting by managers (Kastantin, 2005). This budget

is reviewed by senior managers to finalize the statement. In this statement, expected revenues are

deducted from the revenues of business to determine budgeted profit of the accounting period.

3.2 Selection of appropriable budgeting methods in accordance with the needs of organization

Following methods can be used by management for the preparation of budgetary

statements:

12

Management of Jeffrey and Sons Ltd is recommended to take suitable steps for the

prevention of variances in actual and budgeted values. For this aspect, management can use

following aspects: Just in time and economic order quantity: By the applicability of this technique,

organization can reduce their material cost as there will be optimization is store and order

cost. By ordering economic order quantity, there will be prevention of stock out issue and

reduction in abnormal loss. TQM and Kaizen costing: TQM approach is focused on improvement of overall

production process in order to enhance the quality. With the use of this approach, Jeffrey

and Sons Ltd can resolve quality issues in production process (Cohen and Kaimenaki,

2011). Further, Kaizen costing can be used by organization for the reduction of wastage.

Management audit: This approach is suitable to develop effective internal control in a

business organization. With this technique, organization can monitor the performance of

employees in order to assure standard outcome.

TASK 3

3.1 Purpose and nature of budgeting process

Budgetary statements are prepared by business entity to make estimation of future

expenses and revenue on the basis of previous financial facts and current market trends. On the

basis of budget estimations, resources are allocated into various business activities in order to

enhance its revenue and profitability. Budgets are also used by business to make comparison to

actual and expected outcome to make improvement in operational strategies. Preparation of

budgets is accomplished on the basis of forecasting by managers (Kastantin, 2005). This budget

is reviewed by senior managers to finalize the statement. In this statement, expected revenues are

deducted from the revenues of business to determine budgeted profit of the accounting period.

3.2 Selection of appropriable budgeting methods in accordance with the needs of organization

Following methods can be used by management for the preparation of budgetary

statements:

12

You're viewing a preview

Unlock full access by subscribing today!

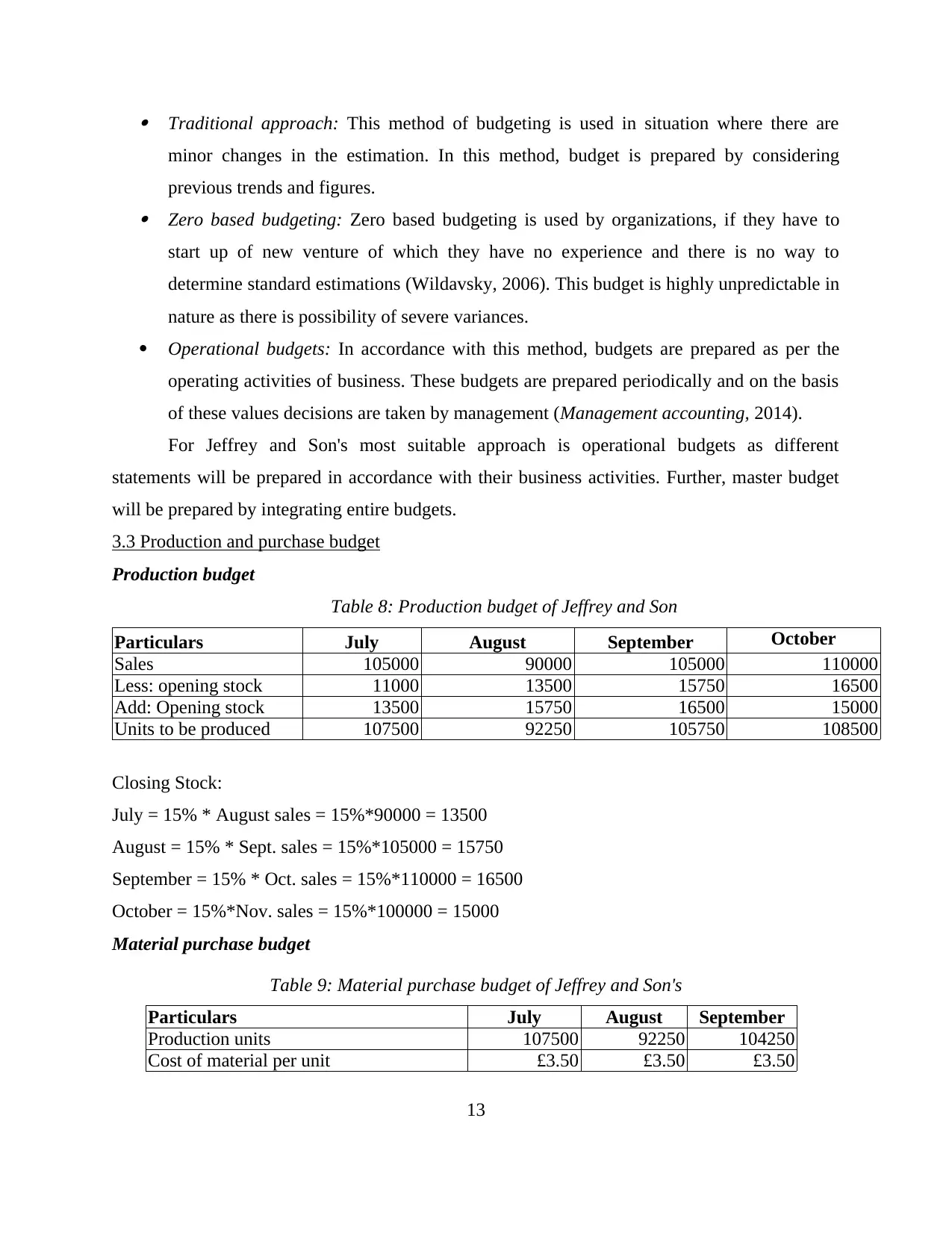

Traditional approach: This method of budgeting is used in situation where there are

minor changes in the estimation. In this method, budget is prepared by considering

previous trends and figures. Zero based budgeting: Zero based budgeting is used by organizations, if they have to

start up of new venture of which they have no experience and there is no way to

determine standard estimations (Wildavsky, 2006). This budget is highly unpredictable in

nature as there is possibility of severe variances.

Operational budgets: In accordance with this method, budgets are prepared as per the

operating activities of business. These budgets are prepared periodically and on the basis

of these values decisions are taken by management (Management accounting, 2014).

For Jeffrey and Son's most suitable approach is operational budgets as different

statements will be prepared in accordance with their business activities. Further, master budget

will be prepared by integrating entire budgets.

3.3 Production and purchase budget

Production budget

Table 8: Production budget of Jeffrey and Son

Particulars July August September October

Sales 105000 90000 105000 110000

Less: opening stock 11000 13500 15750 16500

Add: Opening stock 13500 15750 16500 15000

Units to be produced 107500 92250 105750 108500

Closing Stock:

July = 15% * August sales = 15%*90000 = 13500

August = 15% * Sept. sales = 15%*105000 = 15750

September = 15% * Oct. sales = 15%*110000 = 16500

October = 15%*Nov. sales = 15%*100000 = 15000

Material purchase budget

Table 9: Material purchase budget of Jeffrey and Son's

Particulars July August September

Production units 107500 92250 104250

Cost of material per unit £3.50 £3.50 £3.50

13

minor changes in the estimation. In this method, budget is prepared by considering

previous trends and figures. Zero based budgeting: Zero based budgeting is used by organizations, if they have to

start up of new venture of which they have no experience and there is no way to

determine standard estimations (Wildavsky, 2006). This budget is highly unpredictable in

nature as there is possibility of severe variances.

Operational budgets: In accordance with this method, budgets are prepared as per the

operating activities of business. These budgets are prepared periodically and on the basis

of these values decisions are taken by management (Management accounting, 2014).

For Jeffrey and Son's most suitable approach is operational budgets as different

statements will be prepared in accordance with their business activities. Further, master budget

will be prepared by integrating entire budgets.

3.3 Production and purchase budget

Production budget

Table 8: Production budget of Jeffrey and Son

Particulars July August September October

Sales 105000 90000 105000 110000

Less: opening stock 11000 13500 15750 16500

Add: Opening stock 13500 15750 16500 15000

Units to be produced 107500 92250 105750 108500

Closing Stock:

July = 15% * August sales = 15%*90000 = 13500

August = 15% * Sept. sales = 15%*105000 = 15750

September = 15% * Oct. sales = 15%*110000 = 16500

October = 15%*Nov. sales = 15%*100000 = 15000

Material purchase budget

Table 9: Material purchase budget of Jeffrey and Son's

Particulars July August September

Production units 107500 92250 104250

Cost of material per unit £3.50 £3.50 £3.50

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

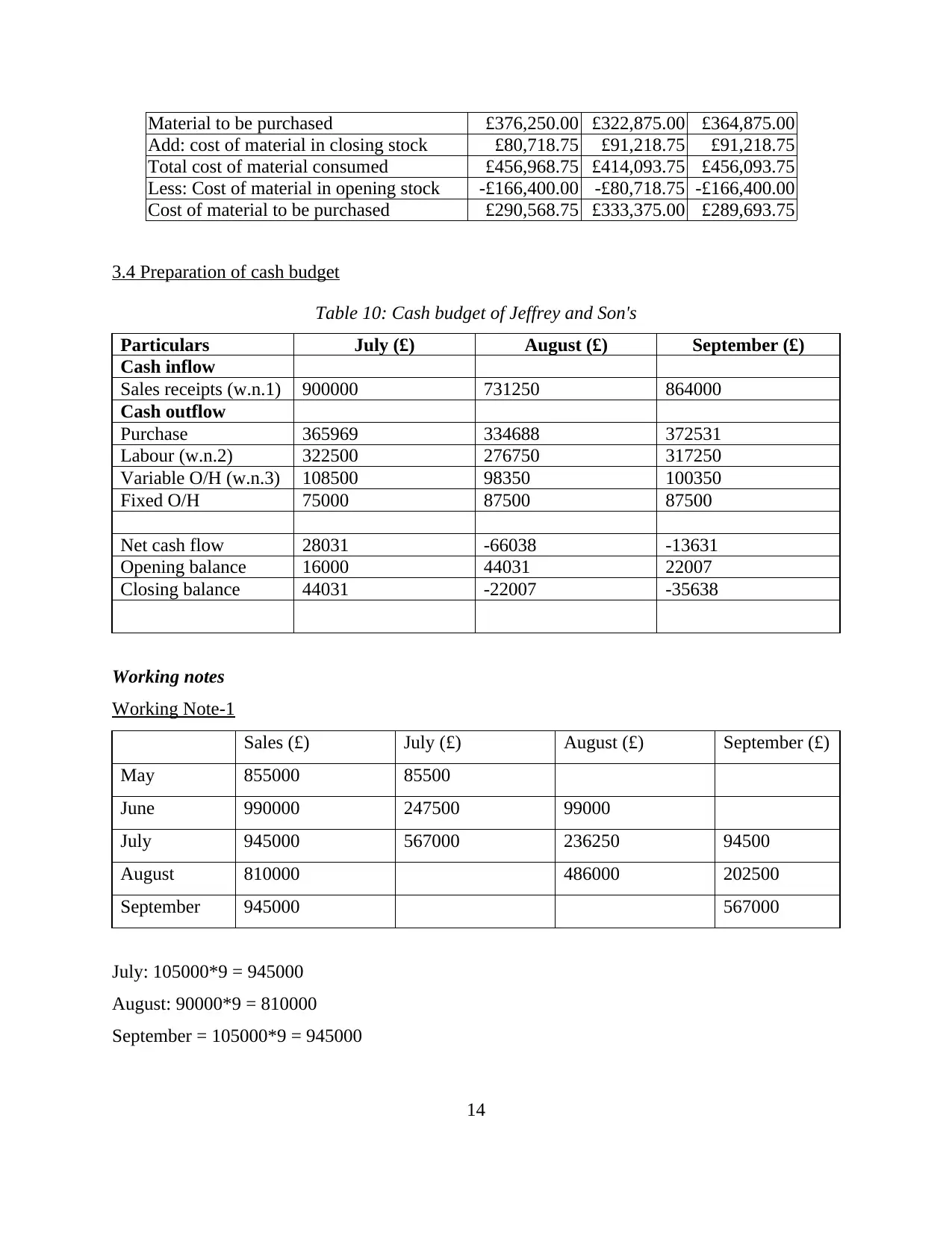

Material to be purchased £376,250.00 £322,875.00 £364,875.00

Add: cost of material in closing stock £80,718.75 £91,218.75 £91,218.75

Total cost of material consumed £456,968.75 £414,093.75 £456,093.75

Less: Cost of material in opening stock -£166,400.00 -£80,718.75 -£166,400.00

Cost of material to be purchased £290,568.75 £333,375.00 £289,693.75

3.4 Preparation of cash budget

Table 10: Cash budget of Jeffrey and Son's

Particulars July (£) August (£) September (£)

Cash inflow

Sales receipts (w.n.1) 900000 731250 864000

Cash outflow

Purchase 365969 334688 372531

Labour (w.n.2) 322500 276750 317250

Variable O/H (w.n.3) 108500 98350 100350

Fixed O/H 75000 87500 87500

Net cash flow 28031 -66038 -13631

Opening balance 16000 44031 22007

Closing balance 44031 -22007 -35638

Working notes

Working Note-1

Sales (£) July (£) August (£) September (£)

May 855000 85500

June 990000 247500 99000

July 945000 567000 236250 94500

August 810000 486000 202500

September 945000 567000

July: 105000*9 = 945000

August: 90000*9 = 810000

September = 105000*9 = 945000

14

Add: cost of material in closing stock £80,718.75 £91,218.75 £91,218.75

Total cost of material consumed £456,968.75 £414,093.75 £456,093.75

Less: Cost of material in opening stock -£166,400.00 -£80,718.75 -£166,400.00

Cost of material to be purchased £290,568.75 £333,375.00 £289,693.75

3.4 Preparation of cash budget

Table 10: Cash budget of Jeffrey and Son's

Particulars July (£) August (£) September (£)

Cash inflow

Sales receipts (w.n.1) 900000 731250 864000

Cash outflow

Purchase 365969 334688 372531

Labour (w.n.2) 322500 276750 317250

Variable O/H (w.n.3) 108500 98350 100350

Fixed O/H 75000 87500 87500

Net cash flow 28031 -66038 -13631

Opening balance 16000 44031 22007

Closing balance 44031 -22007 -35638

Working notes

Working Note-1

Sales (£) July (£) August (£) September (£)

May 855000 85500

June 990000 247500 99000

July 945000 567000 236250 94500

August 810000 486000 202500

September 945000 567000

July: 105000*9 = 945000

August: 90000*9 = 810000

September = 105000*9 = 945000

14

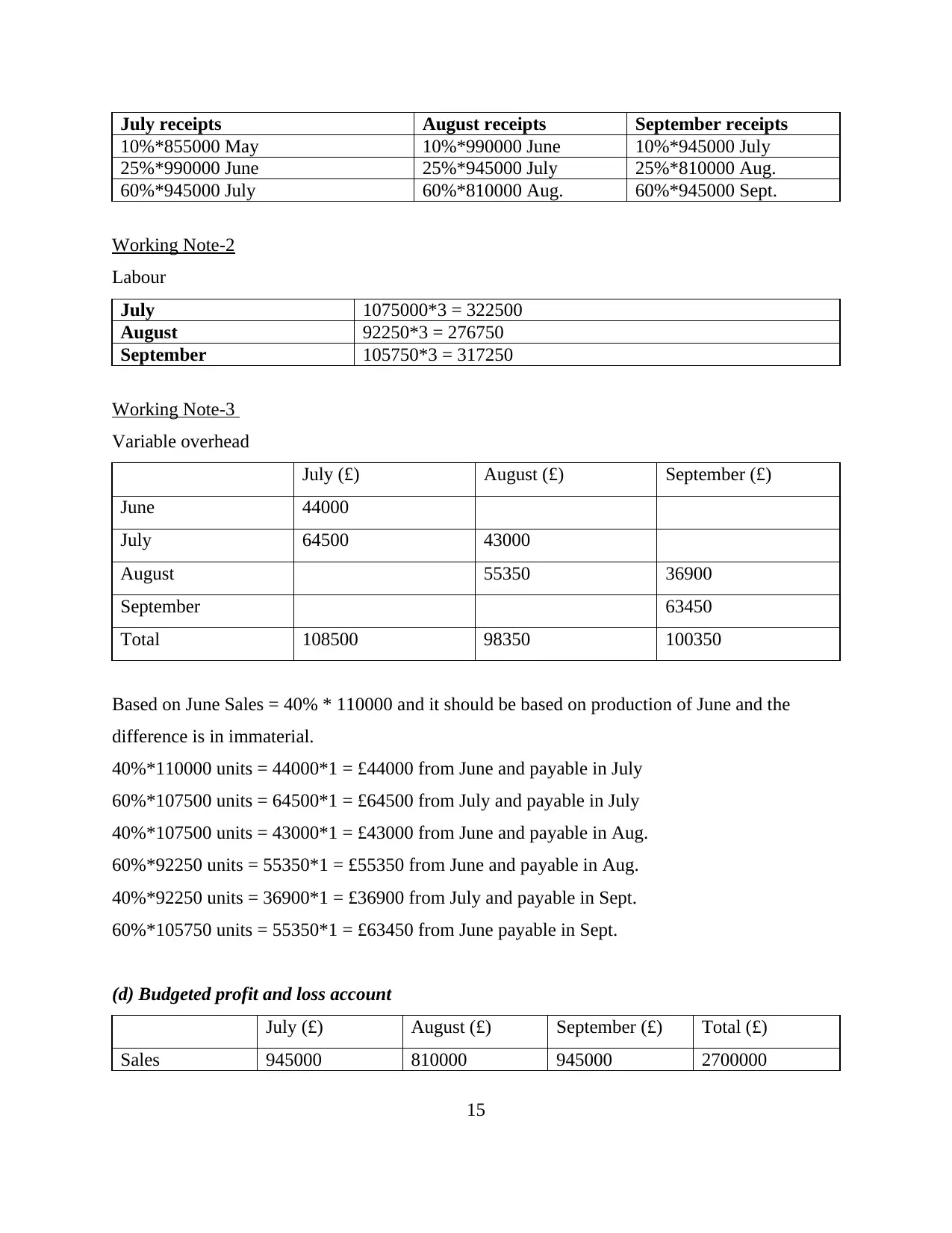

July receipts August receipts September receipts

10%*855000 May 10%*990000 June 10%*945000 July

25%*990000 June 25%*945000 July 25%*810000 Aug.

60%*945000 July 60%*810000 Aug. 60%*945000 Sept.

Working Note-2

Labour

July 1075000*3 = 322500

August 92250*3 = 276750

September 105750*3 = 317250

Working Note-3

Variable overhead

July (£) August (£) September (£)

June 44000

July 64500 43000

August 55350 36900

September 63450

Total 108500 98350 100350

Based on June Sales = 40% * 110000 and it should be based on production of June and the

difference is in immaterial.

40%*110000 units = 44000*1 = £44000 from June and payable in July

60%*107500 units = 64500*1 = £64500 from July and payable in July

40%*107500 units = 43000*1 = £43000 from June and payable in Aug.

60%*92250 units = 55350*1 = £55350 from June and payable in Aug.

40%*92250 units = 36900*1 = £36900 from July and payable in Sept.

60%*105750 units = 55350*1 = £63450 from June payable in Sept.

(d) Budgeted profit and loss account

July (£) August (£) September (£) Total (£)

Sales 945000 810000 945000 2700000

15

10%*855000 May 10%*990000 June 10%*945000 July

25%*990000 June 25%*945000 July 25%*810000 Aug.

60%*945000 July 60%*810000 Aug. 60%*945000 Sept.

Working Note-2

Labour

July 1075000*3 = 322500

August 92250*3 = 276750

September 105750*3 = 317250

Working Note-3

Variable overhead

July (£) August (£) September (£)

June 44000

July 64500 43000

August 55350 36900

September 63450

Total 108500 98350 100350

Based on June Sales = 40% * 110000 and it should be based on production of June and the

difference is in immaterial.

40%*110000 units = 44000*1 = £44000 from June and payable in July

60%*107500 units = 64500*1 = £64500 from July and payable in July

40%*107500 units = 43000*1 = £43000 from June and payable in Aug.

60%*92250 units = 55350*1 = £55350 from June and payable in Aug.

40%*92250 units = 36900*1 = £36900 from July and payable in Sept.

60%*105750 units = 55350*1 = £63450 from June payable in Sept.

(d) Budgeted profit and loss account

July (£) August (£) September (£) Total (£)

Sales 945000 810000 945000 2700000

15

You're viewing a preview

Unlock full access by subscribing today!

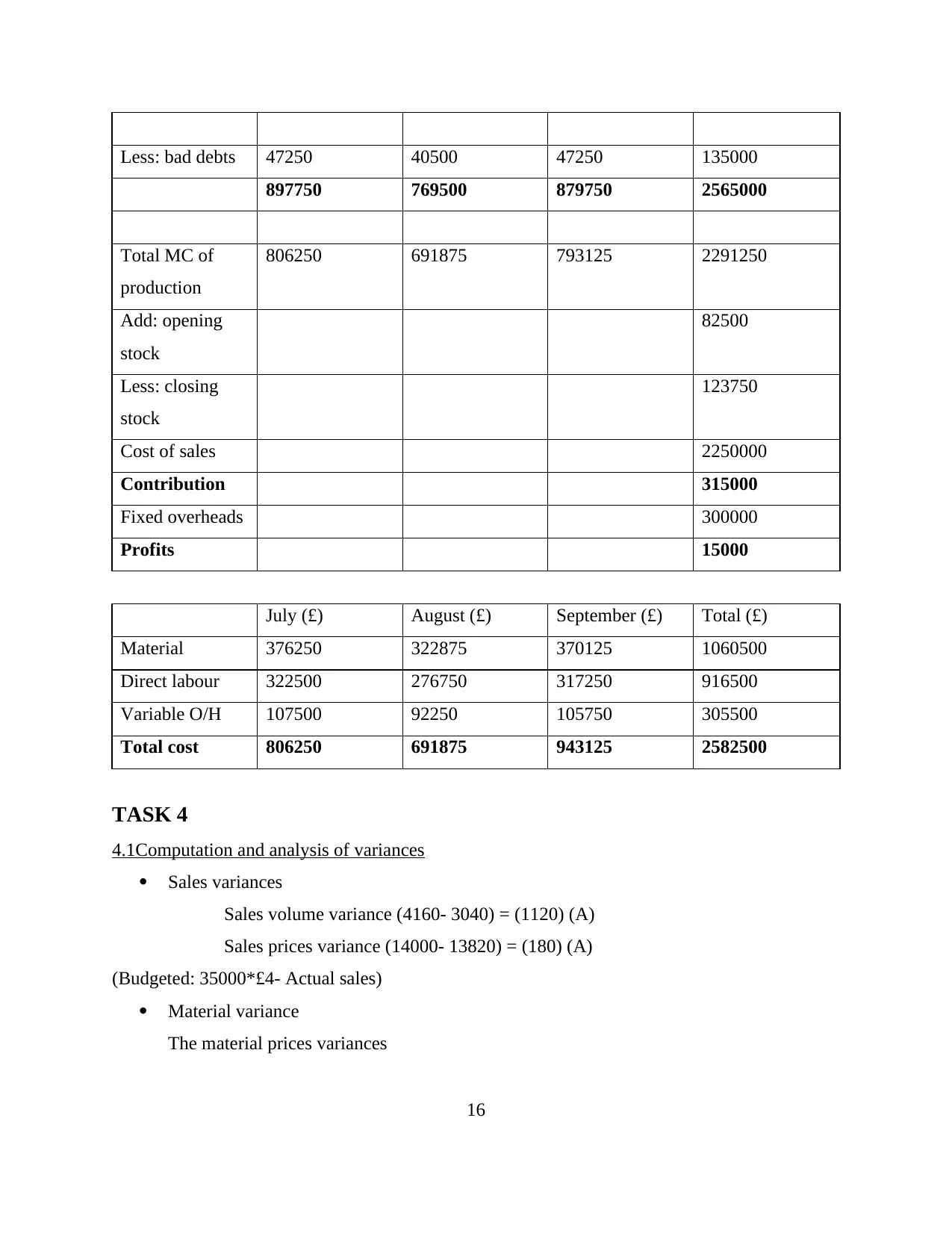

Less: bad debts 47250 40500 47250 135000

897750 769500 879750 2565000

Total MC of

production

806250 691875 793125 2291250

Add: opening

stock

82500

Less: closing

stock

123750

Cost of sales 2250000

Contribution 315000

Fixed overheads 300000

Profits 15000

July (£) August (£) September (£) Total (£)

Material 376250 322875 370125 1060500

Direct labour 322500 276750 317250 916500

Variable O/H 107500 92250 105750 305500

Total cost 806250 691875 943125 2582500

TASK 4

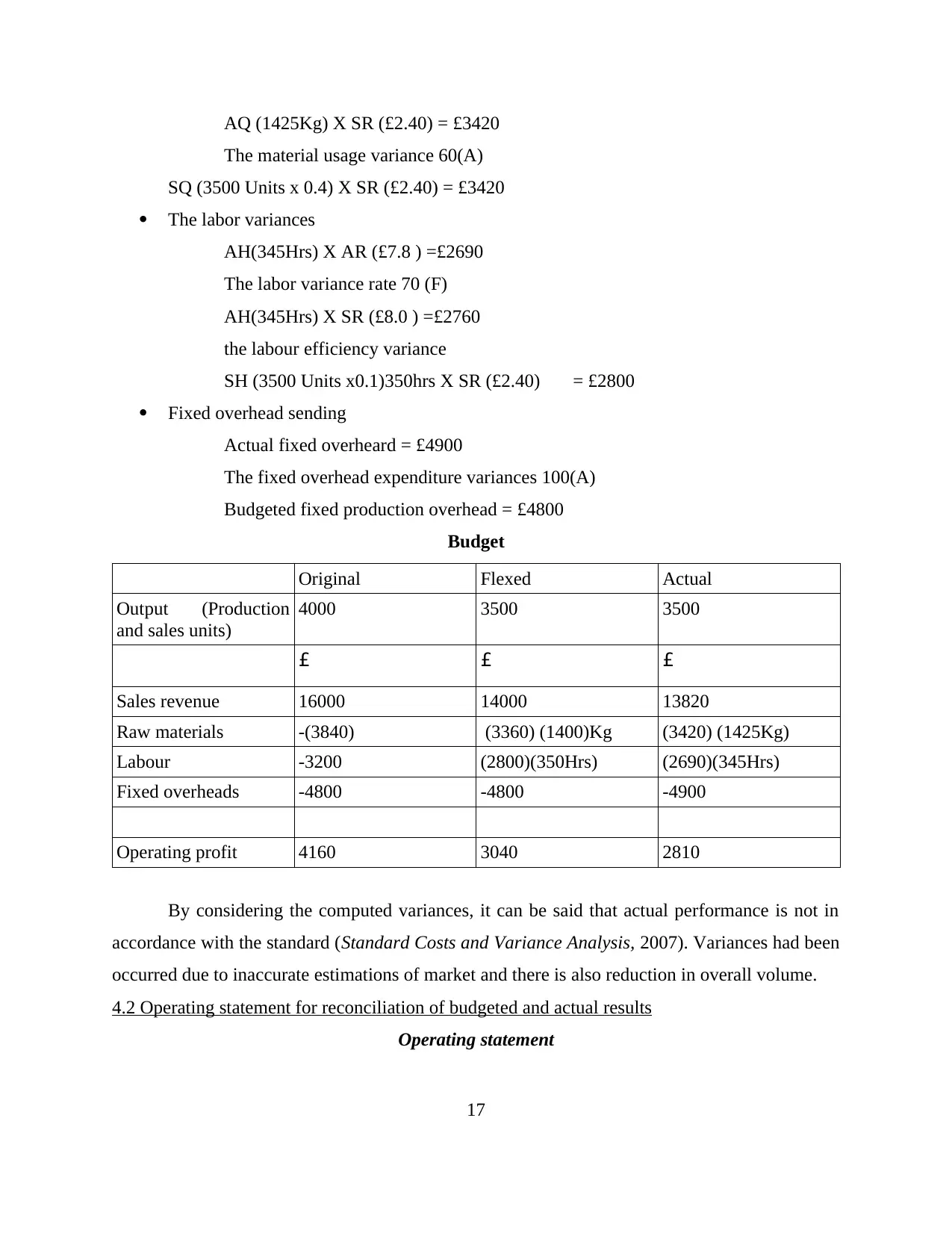

4.1Computation and analysis of variances

Sales variances

Sales volume variance (4160- 3040) = (1120) (A)

Sales prices variance (14000- 13820) = (180) (A)

(Budgeted: 35000*£4- Actual sales)

Material variance

The material prices variances

16

897750 769500 879750 2565000

Total MC of

production

806250 691875 793125 2291250

Add: opening

stock

82500

Less: closing

stock

123750

Cost of sales 2250000

Contribution 315000

Fixed overheads 300000

Profits 15000

July (£) August (£) September (£) Total (£)

Material 376250 322875 370125 1060500

Direct labour 322500 276750 317250 916500

Variable O/H 107500 92250 105750 305500

Total cost 806250 691875 943125 2582500

TASK 4

4.1Computation and analysis of variances

Sales variances

Sales volume variance (4160- 3040) = (1120) (A)

Sales prices variance (14000- 13820) = (180) (A)

(Budgeted: 35000*£4- Actual sales)

Material variance

The material prices variances

16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AQ (1425Kg) X SR (£2.40) = £3420

The material usage variance 60(A)

SQ (3500 Units x 0.4) X SR (£2.40) = £3420

The labor variances

AH(345Hrs) X AR (£7.8 ) =£2690

The labor variance rate 70 (F)

AH(345Hrs) X SR (£8.0 ) =£2760

the labour efficiency variance

SH (3500 Units x0.1)350hrs X SR (£2.40) = £2800

Fixed overhead sending

Actual fixed overheard = £4900

The fixed overhead expenditure variances 100(A)

Budgeted fixed production overhead = £4800

Budget

Original Flexed Actual

Output (Production

and sales units)

4000 3500 3500

£ £ £

Sales revenue 16000 14000 13820

Raw materials -(3840) (3360) (1400)Kg (3420) (1425Kg)

Labour -3200 (2800)(350Hrs) (2690)(345Hrs)

Fixed overheads -4800 -4800 -4900

Operating profit 4160 3040 2810

By considering the computed variances, it can be said that actual performance is not in

accordance with the standard (Standard Costs and Variance Analysis, 2007). Variances had been

occurred due to inaccurate estimations of market and there is also reduction in overall volume.

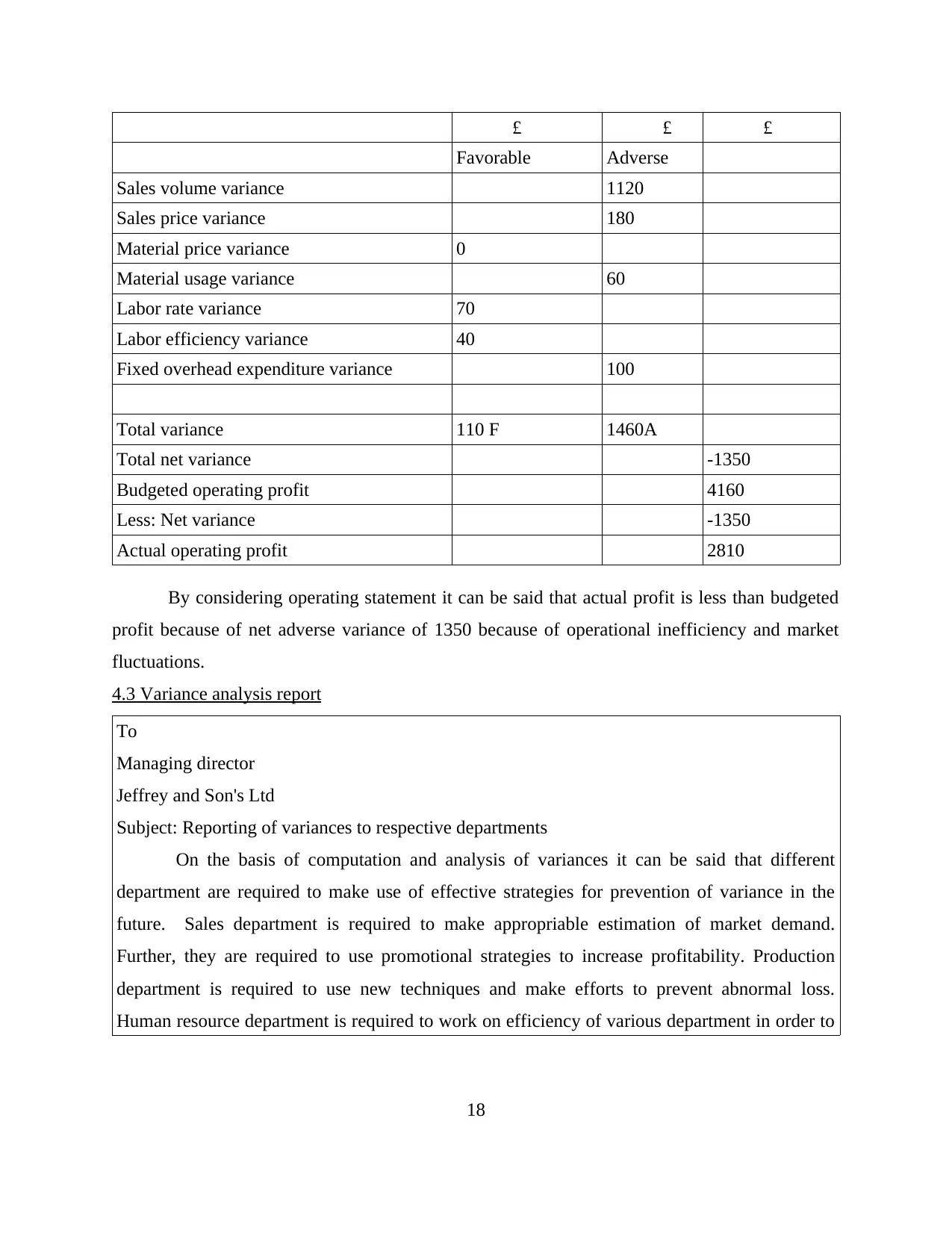

4.2 Operating statement for reconciliation of budgeted and actual results

Operating statement

17

The material usage variance 60(A)

SQ (3500 Units x 0.4) X SR (£2.40) = £3420

The labor variances

AH(345Hrs) X AR (£7.8 ) =£2690

The labor variance rate 70 (F)

AH(345Hrs) X SR (£8.0 ) =£2760

the labour efficiency variance

SH (3500 Units x0.1)350hrs X SR (£2.40) = £2800

Fixed overhead sending

Actual fixed overheard = £4900

The fixed overhead expenditure variances 100(A)

Budgeted fixed production overhead = £4800

Budget

Original Flexed Actual

Output (Production

and sales units)

4000 3500 3500

£ £ £

Sales revenue 16000 14000 13820

Raw materials -(3840) (3360) (1400)Kg (3420) (1425Kg)

Labour -3200 (2800)(350Hrs) (2690)(345Hrs)

Fixed overheads -4800 -4800 -4900

Operating profit 4160 3040 2810

By considering the computed variances, it can be said that actual performance is not in

accordance with the standard (Standard Costs and Variance Analysis, 2007). Variances had been

occurred due to inaccurate estimations of market and there is also reduction in overall volume.

4.2 Operating statement for reconciliation of budgeted and actual results

Operating statement

17

£ £ £

Favorable Adverse

Sales volume variance 1120

Sales price variance 180

Material price variance 0

Material usage variance 60

Labor rate variance 70

Labor efficiency variance 40

Fixed overhead expenditure variance 100

Total variance 110 F 1460A

Total net variance -1350

Budgeted operating profit 4160

Less: Net variance -1350

Actual operating profit 2810

By considering operating statement it can be said that actual profit is less than budgeted

profit because of net adverse variance of 1350 because of operational inefficiency and market

fluctuations.

4.3 Variance analysis report

To

Managing director

Jeffrey and Son's Ltd

Subject: Reporting of variances to respective departments

On the basis of computation and analysis of variances it can be said that different

department are required to make use of effective strategies for prevention of variance in the

future. Sales department is required to make appropriable estimation of market demand.

Further, they are required to use promotional strategies to increase profitability. Production

department is required to use new techniques and make efforts to prevent abnormal loss.

Human resource department is required to work on efficiency of various department in order to

18

Favorable Adverse

Sales volume variance 1120

Sales price variance 180

Material price variance 0

Material usage variance 60

Labor rate variance 70

Labor efficiency variance 40

Fixed overhead expenditure variance 100

Total variance 110 F 1460A

Total net variance -1350

Budgeted operating profit 4160

Less: Net variance -1350

Actual operating profit 2810

By considering operating statement it can be said that actual profit is less than budgeted

profit because of net adverse variance of 1350 because of operational inefficiency and market

fluctuations.

4.3 Variance analysis report

To

Managing director

Jeffrey and Son's Ltd

Subject: Reporting of variances to respective departments

On the basis of computation and analysis of variances it can be said that different

department are required to make use of effective strategies for prevention of variance in the

future. Sales department is required to make appropriable estimation of market demand.

Further, they are required to use promotional strategies to increase profitability. Production

department is required to use new techniques and make efforts to prevent abnormal loss.

Human resource department is required to work on efficiency of various department in order to

18

You're viewing a preview

Unlock full access by subscribing today!

enhance overall productivity.

Finance manager

Name: ____________

Signature: ___________

Date: ____________

CONCLUSION

Present study has been carried out for understanding conceptual framework of

management accounting. In accordance with the present study conclusion can be drawn that

organizations are required to record their cost in an appropriable manner in order to make better

decisions for business. For this aspect, they can make use of various costing and accounting

methods. In order to monitor performance of business, management of companies can compute

variance by comparing actual and budgeted outcome. On this basis of this analysis, they can

identify the area for further improvement in business.

19

Finance manager

Name: ____________

Signature: ___________

Date: ____________

CONCLUSION

Present study has been carried out for understanding conceptual framework of

management accounting. In accordance with the present study conclusion can be drawn that

organizations are required to record their cost in an appropriable manner in order to make better

decisions for business. For this aspect, they can make use of various costing and accounting

methods. In order to monitor performance of business, management of companies can compute

variance by comparing actual and budgeted outcome. On this basis of this analysis, they can

identify the area for further improvement in business.

19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Banks, A., 2008. Budgeting. 3rd ed. McGraw-Hill Australia.Lucey, T., 2002. Costing.

Continuum.

Burns and et. al, 2004. Management accounting education and training: putting management in

and taking accounting out. 1(1). pp.1-29.

Cohen, S. and Kaimenaki, E., 2011. Cost accounting systems structure and information quality

properties: an empirical analysis. Journal of Applied Accounting Research. 12(1). pp.5 –

25.

Jiambalvo, J., 2001. Managerial accounting. Wiley.

Kastantin, T. J., 2005. Beyond earnings management: Using ratios to predict Enron's collapse.

Managerial Finance. 31(9). pp.35–51.

Keown, A., 2005. Financial management. Upper Saddle River, N.J.: Pearson/Prentice Hall.

Kont, R. K., 2013. Cost accounting and scientific management in libraries: a historical overview.

Journal of Management History. 19(2). pp.225 – 240.

Vance, D., 2002. Financial Analysis and Decision Making. McGraw Hill Professional.

Vanderbeck, J. E., 2012. Principles of Cost Accounting. 16th ed. Cengage Learning.

Wildavsky, B. A., 2006. Budgeting And Governing. Transaction Publishers.

Youseef, M., 2013. Management accounting change in an Egyptian organization: an institutional

analysis. Journal of Accounting & Organizational Change. 9(1). pp.50-73.

Zawawi, M. H. N., and Hoque, Z., 2010. Research in management accounting innovations: An

overview of its recent development. Qualitative Research in Accounting &

Management. 7(4). pp.505 – 568.

Online

Management accounting. 2014. [Online]. Available at: <

http://www.e-conomic.co.uk/accountingsystem/glossary/management-accounting>.

[Accessed on 6th February 2016].

20

Books and journals

Banks, A., 2008. Budgeting. 3rd ed. McGraw-Hill Australia.Lucey, T., 2002. Costing.

Continuum.

Burns and et. al, 2004. Management accounting education and training: putting management in

and taking accounting out. 1(1). pp.1-29.

Cohen, S. and Kaimenaki, E., 2011. Cost accounting systems structure and information quality

properties: an empirical analysis. Journal of Applied Accounting Research. 12(1). pp.5 –

25.

Jiambalvo, J., 2001. Managerial accounting. Wiley.

Kastantin, T. J., 2005. Beyond earnings management: Using ratios to predict Enron's collapse.

Managerial Finance. 31(9). pp.35–51.

Keown, A., 2005. Financial management. Upper Saddle River, N.J.: Pearson/Prentice Hall.

Kont, R. K., 2013. Cost accounting and scientific management in libraries: a historical overview.

Journal of Management History. 19(2). pp.225 – 240.

Vance, D., 2002. Financial Analysis and Decision Making. McGraw Hill Professional.

Vanderbeck, J. E., 2012. Principles of Cost Accounting. 16th ed. Cengage Learning.

Wildavsky, B. A., 2006. Budgeting And Governing. Transaction Publishers.

Youseef, M., 2013. Management accounting change in an Egyptian organization: an institutional

analysis. Journal of Accounting & Organizational Change. 9(1). pp.50-73.

Zawawi, M. H. N., and Hoque, Z., 2010. Research in management accounting innovations: An

overview of its recent development. Qualitative Research in Accounting &

Management. 7(4). pp.505 – 568.

Online

Management accounting. 2014. [Online]. Available at: <

http://www.e-conomic.co.uk/accountingsystem/glossary/management-accounting>.

[Accessed on 6th February 2016].

20

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.