BTEC HNC Unit 5: Management Accounting Report - Primark Analysis

VerifiedAdded on 2022/12/15

|14

|2929

|493

Report

AI Summary

This report examines management accounting principles and their application within the context of Primark, a leading fast-fashion retailer. The introduction outlines the role of management accounting in aiding managerial decision-making through financial data analysis. Task 1 covers the fundamental concepts of management accounting and its reporting methods. Task 2 delves into cost analysis techniques, including marginal costing and absorption costing, illustrating their use in preparing financial statements. Task 3 focuses on budgetary control, exploring planning tools like cash budgets, capital budgeting, and variance analysis. Task 4 discusses financial problems faced by businesses, such as inconsistent cash flow and unnecessary expenditure, and explores management accounting systems and techniques like benchmarking and KPIs to address these challenges. The report concludes with a summary of the key findings and references.

Management accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Concept of management accounting.................................................................................3

P2. Methods of management accounting reporting................................................................6

TASK 2............................................................................................................................................7

P3 Techniques of cost analysis .............................................................................................7

TASK 3..........................................................................................................................................13

P4 Planning tools used for budgetary controlling................................................................13

TASK 4..........................................................................................................................................15

P5 Management Accounting System....................................................................................15

CONCLUSION ............................................................................................................................17

REFERENCES..............................................................................................................................19

2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Concept of management accounting.................................................................................3

P2. Methods of management accounting reporting................................................................6

TASK 2............................................................................................................................................7

P3 Techniques of cost analysis .............................................................................................7

TASK 3..........................................................................................................................................13

P4 Planning tools used for budgetary controlling................................................................13

TASK 4..........................................................................................................................................15

P5 Management Accounting System....................................................................................15

CONCLUSION ............................................................................................................................17

REFERENCES..............................................................................................................................19

2

INTRODUCTION

Management accounting refers to an assistance tool used by managers, this tool helps

them to formulate plans to achieve long term and short term objectives of the firm. It helps

managers by analysing and interpreting results provided by financial accounting. It is determine

that management accounting is used for the planning of future requirements of an organization

by using financial information which are given to plan budget & execute strategies to enhance

profitability. Another purpose of management accounting is directing and motivating staff

members in a proper manner. Management accounting aims at improving quality of information

provided to management about business operations, with the help of this information, managers

decide their future course of action (Bobryshev and et.al., 2015). This report is drafted on

Primark which is leading fast fashion retail venture that performs key operations from

headquarters situated at Dublin, Ireland. It have around 7000 employee size and aims to become

most preferred retail organisation globally.

This document focuses on application of management accounting techniques on a given

set of data. Further, it covers use of different type of planning tools in order to solve financial

problems faced by Primark.

TASK 2

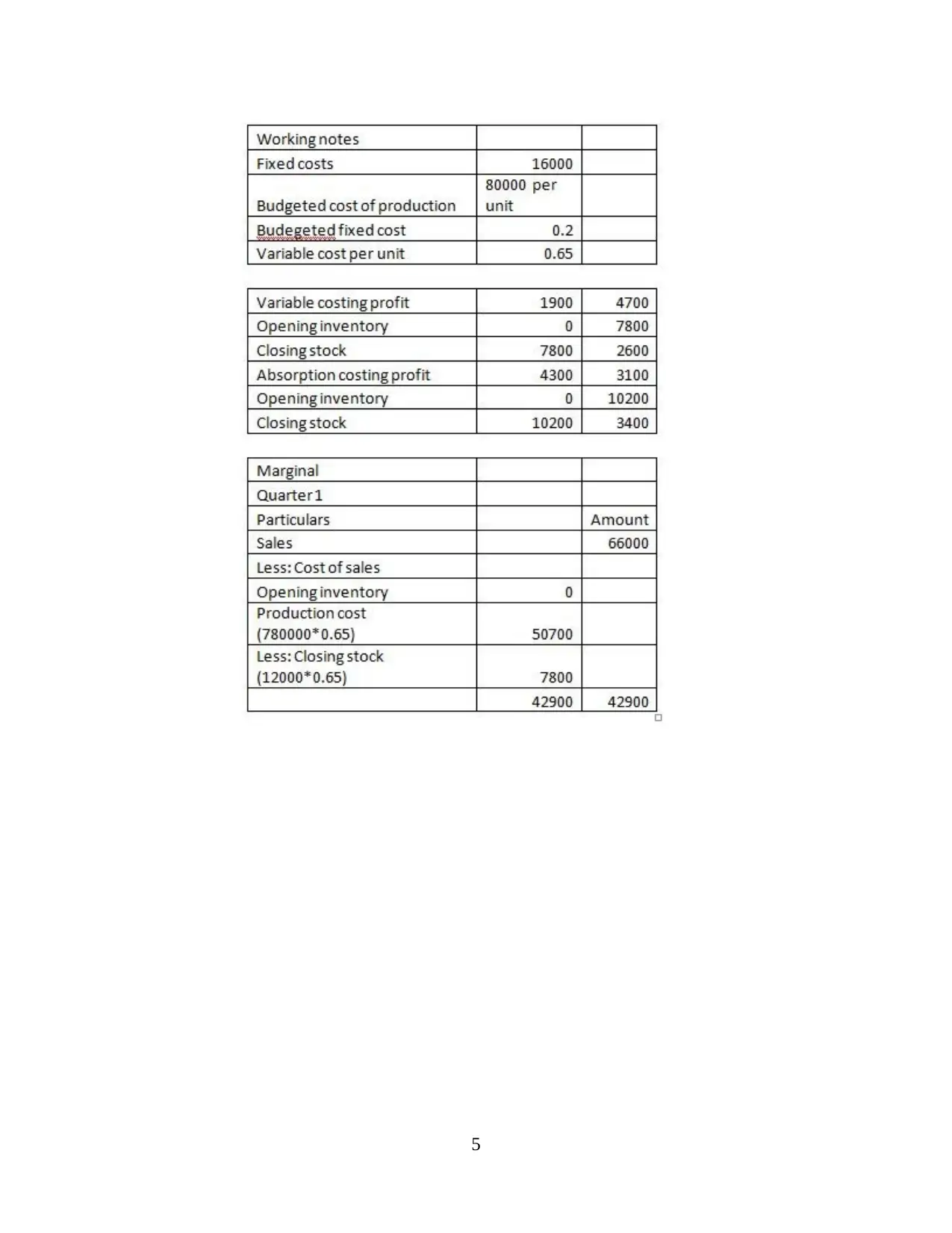

P3 Techniques of cost analysis

For the purpose of producing something including products and services, it is essential

for all organisations to analyse cost that is involved at different levels. Key costs types that are

occurred at Primark are indirect, fixed, sunk, opportunity, variable and so many other costs. Cost

analysis benefits managers to measure advantages of decision making about relevant cost that are

part of undertaken action. Flexible budgeting guides managers to make adjustments in changes

that are part or real revenue levels. Similarly, cost variance permits in monitoring financial

progression about activities that are performed in business. Within Primark, essential cost

analysis techniques that have assisted financial accountant in preparing income statement are as

elaborated:

Marginal costing: This is a costing technique used to determine relationship between

volume produced and the cost incurred in that production. Marginal cost can be defined as the

additional cost of producing an additional unit (Johansson and Kriström, 2018).

3

Management accounting refers to an assistance tool used by managers, this tool helps

them to formulate plans to achieve long term and short term objectives of the firm. It helps

managers by analysing and interpreting results provided by financial accounting. It is determine

that management accounting is used for the planning of future requirements of an organization

by using financial information which are given to plan budget & execute strategies to enhance

profitability. Another purpose of management accounting is directing and motivating staff

members in a proper manner. Management accounting aims at improving quality of information

provided to management about business operations, with the help of this information, managers

decide their future course of action (Bobryshev and et.al., 2015). This report is drafted on

Primark which is leading fast fashion retail venture that performs key operations from

headquarters situated at Dublin, Ireland. It have around 7000 employee size and aims to become

most preferred retail organisation globally.

This document focuses on application of management accounting techniques on a given

set of data. Further, it covers use of different type of planning tools in order to solve financial

problems faced by Primark.

TASK 2

P3 Techniques of cost analysis

For the purpose of producing something including products and services, it is essential

for all organisations to analyse cost that is involved at different levels. Key costs types that are

occurred at Primark are indirect, fixed, sunk, opportunity, variable and so many other costs. Cost

analysis benefits managers to measure advantages of decision making about relevant cost that are

part of undertaken action. Flexible budgeting guides managers to make adjustments in changes

that are part or real revenue levels. Similarly, cost variance permits in monitoring financial

progression about activities that are performed in business. Within Primark, essential cost

analysis techniques that have assisted financial accountant in preparing income statement are as

elaborated:

Marginal costing: This is a costing technique used to determine relationship between

volume produced and the cost incurred in that production. Marginal cost can be defined as the

additional cost of producing an additional unit (Johansson and Kriström, 2018).

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

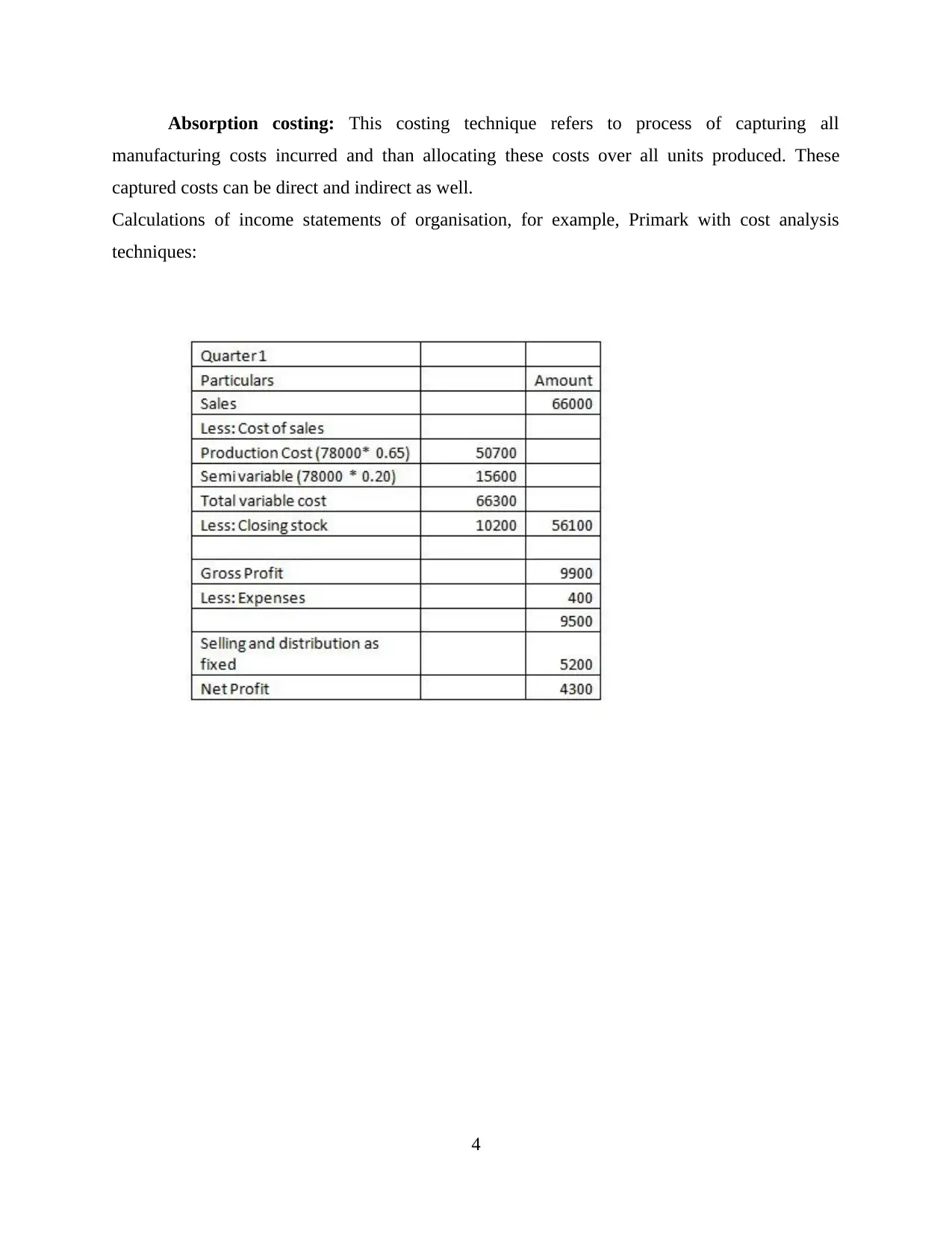

Absorption costing: This costing technique refers to process of capturing all

manufacturing costs incurred and than allocating these costs over all units produced. These

captured costs can be direct and indirect as well.

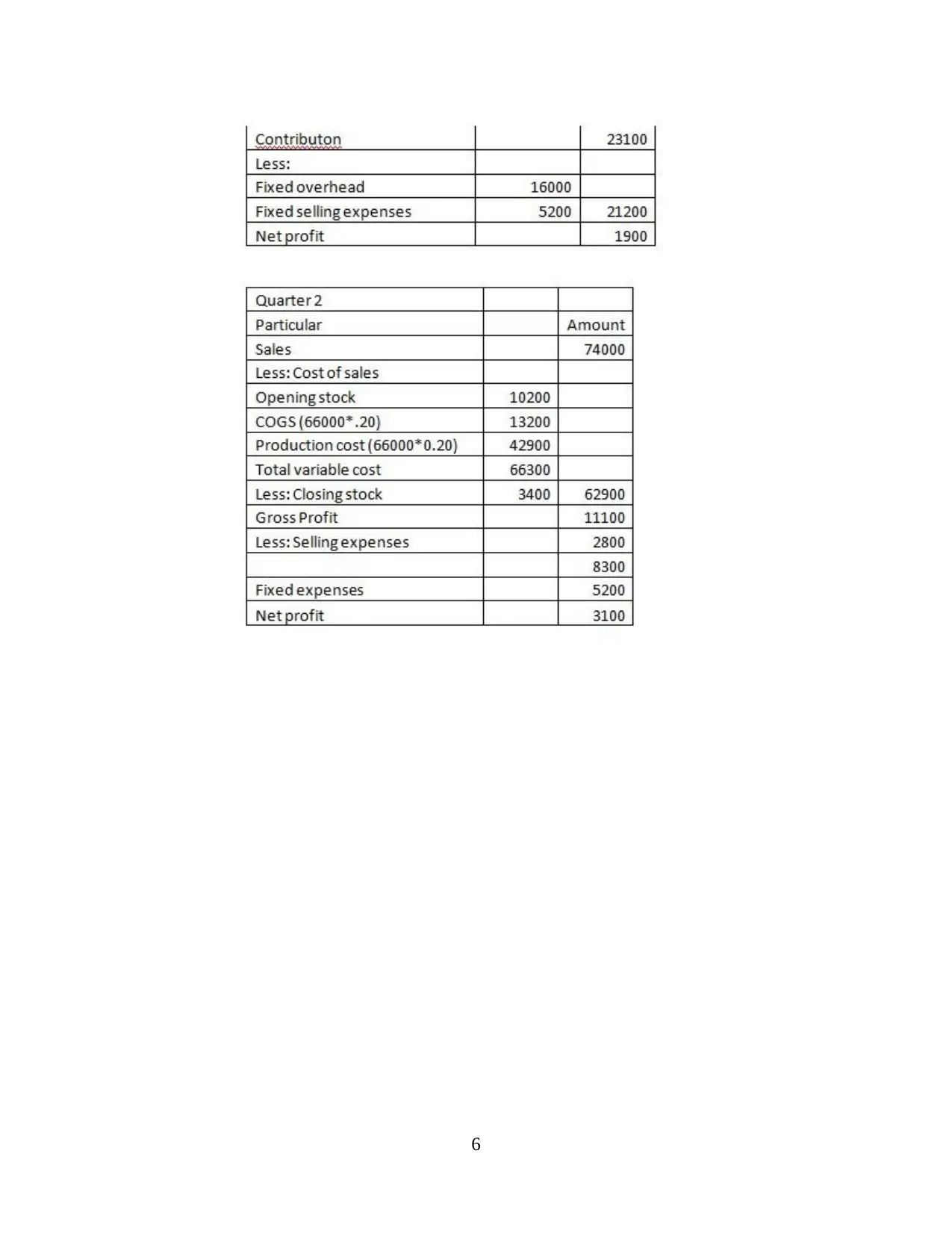

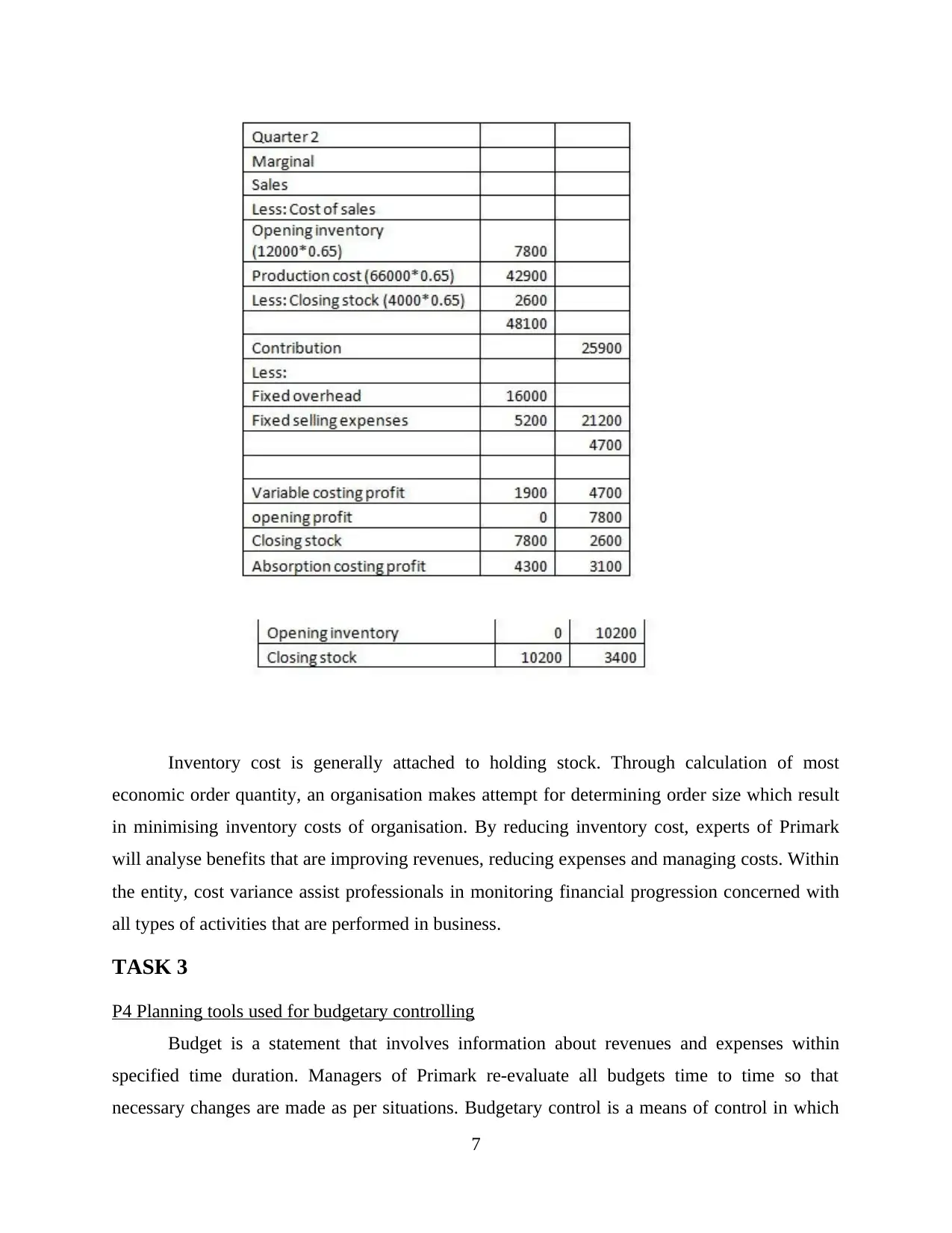

Calculations of income statements of organisation, for example, Primark with cost analysis

techniques:

4

manufacturing costs incurred and than allocating these costs over all units produced. These

captured costs can be direct and indirect as well.

Calculations of income statements of organisation, for example, Primark with cost analysis

techniques:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory cost is generally attached to holding stock. Through calculation of most

economic order quantity, an organisation makes attempt for determining order size which result

in minimising inventory costs of organisation. By reducing inventory cost, experts of Primark

will analyse benefits that are improving revenues, reducing expenses and managing costs. Within

the entity, cost variance assist professionals in monitoring financial progression concerned with

all types of activities that are performed in business.

TASK 3

P4 Planning tools used for budgetary controlling

Budget is a statement that involves information about revenues and expenses within

specified time duration. Managers of Primark re-evaluate all budgets time to time so that

necessary changes are made as per situations. Budgetary control is a means of control in which

7

economic order quantity, an organisation makes attempt for determining order size which result

in minimising inventory costs of organisation. By reducing inventory cost, experts of Primark

will analyse benefits that are improving revenues, reducing expenses and managing costs. Within

the entity, cost variance assist professionals in monitoring financial progression concerned with

all types of activities that are performed in business.

TASK 3

P4 Planning tools used for budgetary controlling

Budget is a statement that involves information about revenues and expenses within

specified time duration. Managers of Primark re-evaluate all budgets time to time so that

necessary changes are made as per situations. Budgetary control is a means of control in which

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the actual results are compared with the budgeted results. It helps management in taking

appropriate actions for the deviations between the two. Budgetary control involves the use of

budget and budgetary reports, throughout the period to co-ordinate, evaluate and control day-to-

day operations in accordance with the goals specified by the budget (Williamson, 2016). It is a

continuous process which helps in planning and coordination. Management of Primark can use

following planning tools in order to control for budgetary aspects:

Cash Budget

Cash budget is an estimation of anticipated cash receipts and cash disbursement for the

budgeted period. In other words, a cash budget is an estimated projection of the company's cash

position in the future. Management of Primark can use this information to determine if the

company has sufficient cash to operate in budget period.

Advantages – It is easier to understand by any stakeholder. It improves the resource

allocation and helps management in fixing responsibility. In Primark, cash budget

provide advantage of avoiding debt, forging budget in better ways, becoming more

resourceful and staying in contacts with real situations.

Disadvantages – Cash budget is based on the past observations of a company for an

uncertain future. It is prepared by the managers on their instincts rather than facts. Thus,

it is not free from personal bias of the managers. Also, non-financial factors which have

a huge effect on finances of a business are completely omitted. Cash budget have

chances to limit organisational spending power, creates condition of theft and restricts

competence to devise effective credit profile that is major disadvantage for Primark.

Capital Budgeting

Capital Budgeting technique is largely used for long-term investment opportunities. It is a

process by which a company decides whether it should invest in a project or not (Schönbohm

and Zahn, 2016). Construction of a new factory or purchasing a new plant & machinery are two

examples which require capital budgeting. Capital investments are necessary for the growth of

the company but they involve large inflow and outflow of money. Various methods like payback

period, net present value, internal rate of return, etc. are used by management to decide the best

alternative out of options available. Tools of capital budgeting used by management of Primark

limited can help them avert future risk and unnecessary expenses.

8

appropriate actions for the deviations between the two. Budgetary control involves the use of

budget and budgetary reports, throughout the period to co-ordinate, evaluate and control day-to-

day operations in accordance with the goals specified by the budget (Williamson, 2016). It is a

continuous process which helps in planning and coordination. Management of Primark can use

following planning tools in order to control for budgetary aspects:

Cash Budget

Cash budget is an estimation of anticipated cash receipts and cash disbursement for the

budgeted period. In other words, a cash budget is an estimated projection of the company's cash

position in the future. Management of Primark can use this information to determine if the

company has sufficient cash to operate in budget period.

Advantages – It is easier to understand by any stakeholder. It improves the resource

allocation and helps management in fixing responsibility. In Primark, cash budget

provide advantage of avoiding debt, forging budget in better ways, becoming more

resourceful and staying in contacts with real situations.

Disadvantages – Cash budget is based on the past observations of a company for an

uncertain future. It is prepared by the managers on their instincts rather than facts. Thus,

it is not free from personal bias of the managers. Also, non-financial factors which have

a huge effect on finances of a business are completely omitted. Cash budget have

chances to limit organisational spending power, creates condition of theft and restricts

competence to devise effective credit profile that is major disadvantage for Primark.

Capital Budgeting

Capital Budgeting technique is largely used for long-term investment opportunities. It is a

process by which a company decides whether it should invest in a project or not (Schönbohm

and Zahn, 2016). Construction of a new factory or purchasing a new plant & machinery are two

examples which require capital budgeting. Capital investments are necessary for the growth of

the company but they involve large inflow and outflow of money. Various methods like payback

period, net present value, internal rate of return, etc. are used by management to decide the best

alternative out of options available. Tools of capital budgeting used by management of Primark

limited can help them avert future risk and unnecessary expenses.

8

Advantages – It helps a company to estimate which investment option would yield them

best possible returns. It reduces the risk of unnecessary wastage of financial resources. In

regards to Primark, capital budgeting helps managers to understand about certain risks

along with their effects, selecting investment wisely, having control on expenditures and

making rational decisions.

Disadvantages – These techniques are based on estimations and assumptions about the

future which is uncertain. Any wrong decision can affect the financial and operating

health of the business. Disadvantage about capital budgeting that Primark have wider

chances to experience includes expensive in nature, wrong applicability resulting to

uncertainty and needs professionals.

Variance Analysis

In this analysis, a budget is prepared for each department. Then, a comparison is drawn

between actual accounting and budgeted estimated figures. The differences so found are called

variances. This technique helps in reducing cost (Budgets and budgetary control, 2020). These

variances can be favourable or unfavourable. Using this technique, management of Primark

Limited will also be able to decide the deviations of each department individually to initiate the

corrective action.

Advantages – Material variances drawn out of analysis helps the management to identify

the areas of improvement. It also help fixing the responsibility on particular department

which lagged behind the target. Disadvantages – Preparing budgets for each individual department is costly. Therefore, it

is not feasible for small businesses. Also, this analysis takes a long time to determine the

deviations as it is based on comparison of estimated figures with actual results. Actual

results are released after a period and thus, corrective actions also get delayed.

Planning tools used in budgetary control

Planning tools are used by managers to prepare to predict various informations that can

help them run business effectively. They prepare various budgets, analysis, trends and forecasts.

For example, Primark Limited used cash budget, variance analysis and capital budgeting

techniques above to forecast financial values and to check the feasibility of proposed

investments.

9

best possible returns. It reduces the risk of unnecessary wastage of financial resources. In

regards to Primark, capital budgeting helps managers to understand about certain risks

along with their effects, selecting investment wisely, having control on expenditures and

making rational decisions.

Disadvantages – These techniques are based on estimations and assumptions about the

future which is uncertain. Any wrong decision can affect the financial and operating

health of the business. Disadvantage about capital budgeting that Primark have wider

chances to experience includes expensive in nature, wrong applicability resulting to

uncertainty and needs professionals.

Variance Analysis

In this analysis, a budget is prepared for each department. Then, a comparison is drawn

between actual accounting and budgeted estimated figures. The differences so found are called

variances. This technique helps in reducing cost (Budgets and budgetary control, 2020). These

variances can be favourable or unfavourable. Using this technique, management of Primark

Limited will also be able to decide the deviations of each department individually to initiate the

corrective action.

Advantages – Material variances drawn out of analysis helps the management to identify

the areas of improvement. It also help fixing the responsibility on particular department

which lagged behind the target. Disadvantages – Preparing budgets for each individual department is costly. Therefore, it

is not feasible for small businesses. Also, this analysis takes a long time to determine the

deviations as it is based on comparison of estimated figures with actual results. Actual

results are released after a period and thus, corrective actions also get delayed.

Planning tools used in budgetary control

Planning tools are used by managers to prepare to predict various informations that can

help them run business effectively. They prepare various budgets, analysis, trends and forecasts.

For example, Primark Limited used cash budget, variance analysis and capital budgeting

techniques above to forecast financial values and to check the feasibility of proposed

investments.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 4

P5 Management Accounting System

Financial Problems

Every business needs financial stability to achieve its objectives. Businesses plan out in

advance several budgets and policies to estimate smooth operations of activities. But the business

environment is unpredictable and the businesses faces several types of financial problems

(Shapiro and Hanouna, 2019). Following are some of the financial problems faced by two

organisations namely, Primark limited and Smoothie King limited:

Inconsistent cash flow – Businesses are in perpetual need of cash to carry out its daily

operations. Thus, a consistent cash flow is always a top priority for company. Companies often

face inconsistent sales and other revenues yet always has some fixed and some variable payouts.

This creates cash deficit position for company.

Unnecessary expenditure – Companies in order to attract more consumers and be at par

with their competitors, often find themselves splurging unnecessarily on advertisement, fancy

assets, etc. which only results in debts and overheads for them (Ghauri, Grønhaug and Strange,

2020). Sometimes, company incurs unforeseen expenditures which also worsen their financial

health.

Accounting Techniques

Benchmarking – It is the process of comparing a firm's performance criteria and

business process to other businesses within their industry. This technique helps in

identifying areas and divisions which require management attention.

Key Performance Indicators (KPI) – These are measures that are used to evaluate the

success of a company in relation to a specified goal. KPIs have two aspects – financial

and non-financial. Financial aspects include net profit, sales growth, current ratio, etc.

Non-financial aspects includes factors such customer satisfaction, employee satisfaction,

company profile, etc.

Management accountant of Primark have certain characteristics that makes them effective

to handle all transactions related to funds. The characteristics are good communicator, decision

maker, trustworthy, relationship handler, forecaster and so on. With these skills, management

accountant of the company is able to prevent or deal with finnacial issues as they have

knowledge about how to handle finance of company. This guides them in expending in the cases

10

P5 Management Accounting System

Financial Problems

Every business needs financial stability to achieve its objectives. Businesses plan out in

advance several budgets and policies to estimate smooth operations of activities. But the business

environment is unpredictable and the businesses faces several types of financial problems

(Shapiro and Hanouna, 2019). Following are some of the financial problems faced by two

organisations namely, Primark limited and Smoothie King limited:

Inconsistent cash flow – Businesses are in perpetual need of cash to carry out its daily

operations. Thus, a consistent cash flow is always a top priority for company. Companies often

face inconsistent sales and other revenues yet always has some fixed and some variable payouts.

This creates cash deficit position for company.

Unnecessary expenditure – Companies in order to attract more consumers and be at par

with their competitors, often find themselves splurging unnecessarily on advertisement, fancy

assets, etc. which only results in debts and overheads for them (Ghauri, Grønhaug and Strange,

2020). Sometimes, company incurs unforeseen expenditures which also worsen their financial

health.

Accounting Techniques

Benchmarking – It is the process of comparing a firm's performance criteria and

business process to other businesses within their industry. This technique helps in

identifying areas and divisions which require management attention.

Key Performance Indicators (KPI) – These are measures that are used to evaluate the

success of a company in relation to a specified goal. KPIs have two aspects – financial

and non-financial. Financial aspects include net profit, sales growth, current ratio, etc.

Non-financial aspects includes factors such customer satisfaction, employee satisfaction,

company profile, etc.

Management accountant of Primark have certain characteristics that makes them effective

to handle all transactions related to funds. The characteristics are good communicator, decision

maker, trustworthy, relationship handler, forecaster and so on. With these skills, management

accountant of the company is able to prevent or deal with finnacial issues as they have

knowledge about how to handle finance of company. This guides them in expending in the cases

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

where they have chances for good returns and make more revenues. Developing strategies

together with systems helps management accountant of Primark to share relevant information

with stakeholders as well as fostering transactions that reduces expenses and improvises

revenues.

Basis for

comparison

Primark Tesco

Financial Issue Inconsistent sales revenue in the existing

outlets is the biggest issue for the company. It

has resulted in stunted growth of the company.

Tesco had introduced new

outlets which had increased

their operational cost. The

outlets are not yet profitable.

This has declined their profit

margin.

Techniques to

recognise issue

Benchmarking technique helped Primark

limited identify the reason of decline in sales.

It also paved way for correction and control

Financial Key performance

indicators were used to assess

causes of financial strain.

11

Illustration 1: 5 marketing key performance indicators you need to

track, 2020

together with systems helps management accountant of Primark to share relevant information

with stakeholders as well as fostering transactions that reduces expenses and improvises

revenues.

Basis for

comparison

Primark Tesco

Financial Issue Inconsistent sales revenue in the existing

outlets is the biggest issue for the company. It

has resulted in stunted growth of the company.

Tesco had introduced new

outlets which had increased

their operational cost. The

outlets are not yet profitable.

This has declined their profit

margin.

Techniques to

recognise issue

Benchmarking technique helped Primark

limited identify the reason of decline in sales.

It also paved way for correction and control

Financial Key performance

indicators were used to assess

causes of financial strain.

11

Illustration 1: 5 marketing key performance indicators you need to

track, 2020

by management.

Management

Accounting

System

Price optimisation technique – this technique

determines the most effective pricing of

product based on customer feedback and

market analysis. Market analysis found out

that at some outlets sales were decreasing

because of better priced products available

from competitor. At such locations, company

implemented differential pricing strategy to

regain customers.

Job costing system – it is the

process of assigning the costs

to incur a specific job the

business is involved with.

Company measured costs of

each particular job to identify

the areas where they can

increase profitability.

Management accounting system to solve financial problems:

An effective management accounting system reaches into all departments of a business:

finance, IT, marketing, human resources, operational and sales. An effective system helps

management identify the stress areas and then formulate required strategies and policies to

overcome those financial strains (Guinea, 2016). Ultimate aim is to increase business

profitability and to ensure its sustainable growth. For it, managers evaluate multiple techniques

and their impacts to decide the correct technique to be used. As in the above comparison,

management applied price optimisation technique and job costing system to solve the financial

issues their companies were facing.

Planning tools to solve financial problems:

The purpose of budgetary planning is to mitigate the risk that an organisation's financial

results are expecting (Jannesson and Nilsson, 2020). Planning tools are instrumental in helping

organisations take corrective actions that help company solve financial issues, it is facing. There

are various planning tools that a company can use for example, responsibility accounting,

adjustment of funds, zero based budgeting, etc. Management of Primark Limited found the

preparation of variance analysis, capital budgeting and cash budget useful to achieve its financial

objectives. Planning tools of budgetary control enhances co-ordination, planning and control in

an organisation, because of these benefits, financial problems can easily be solved.

12

Management

Accounting

System

Price optimisation technique – this technique

determines the most effective pricing of

product based on customer feedback and

market analysis. Market analysis found out

that at some outlets sales were decreasing

because of better priced products available

from competitor. At such locations, company

implemented differential pricing strategy to

regain customers.

Job costing system – it is the

process of assigning the costs

to incur a specific job the

business is involved with.

Company measured costs of

each particular job to identify

the areas where they can

increase profitability.

Management accounting system to solve financial problems:

An effective management accounting system reaches into all departments of a business:

finance, IT, marketing, human resources, operational and sales. An effective system helps

management identify the stress areas and then formulate required strategies and policies to

overcome those financial strains (Guinea, 2016). Ultimate aim is to increase business

profitability and to ensure its sustainable growth. For it, managers evaluate multiple techniques

and their impacts to decide the correct technique to be used. As in the above comparison,

management applied price optimisation technique and job costing system to solve the financial

issues their companies were facing.

Planning tools to solve financial problems:

The purpose of budgetary planning is to mitigate the risk that an organisation's financial

results are expecting (Jannesson and Nilsson, 2020). Planning tools are instrumental in helping

organisations take corrective actions that help company solve financial issues, it is facing. There

are various planning tools that a company can use for example, responsibility accounting,

adjustment of funds, zero based budgeting, etc. Management of Primark Limited found the

preparation of variance analysis, capital budgeting and cash budget useful to achieve its financial

objectives. Planning tools of budgetary control enhances co-ordination, planning and control in

an organisation, because of these benefits, financial problems can easily be solved.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.