Comparative Analysis of Costing Systems: Traditional vs. ABC

VerifiedAdded on 2021/05/30

|9

|1367

|228

Report

AI Summary

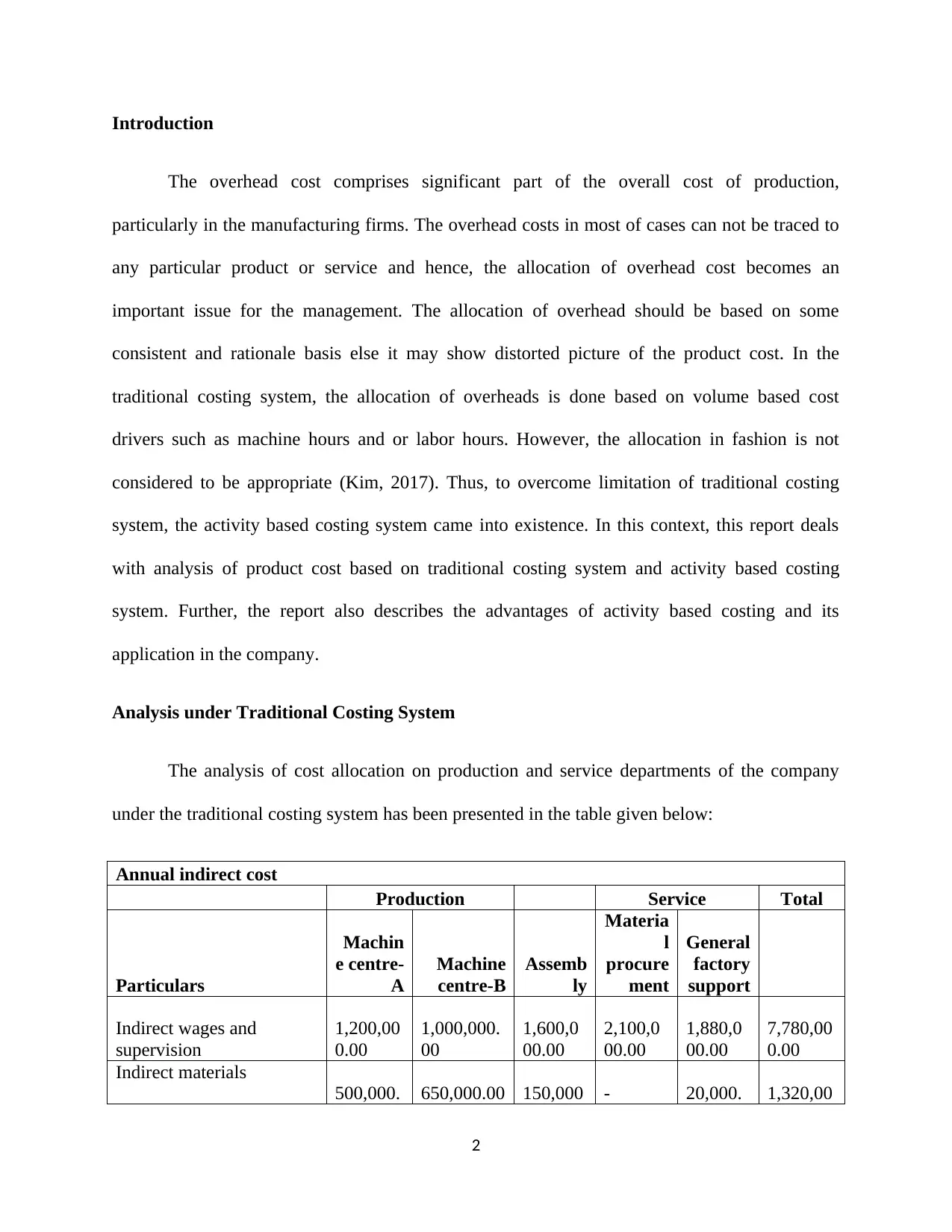

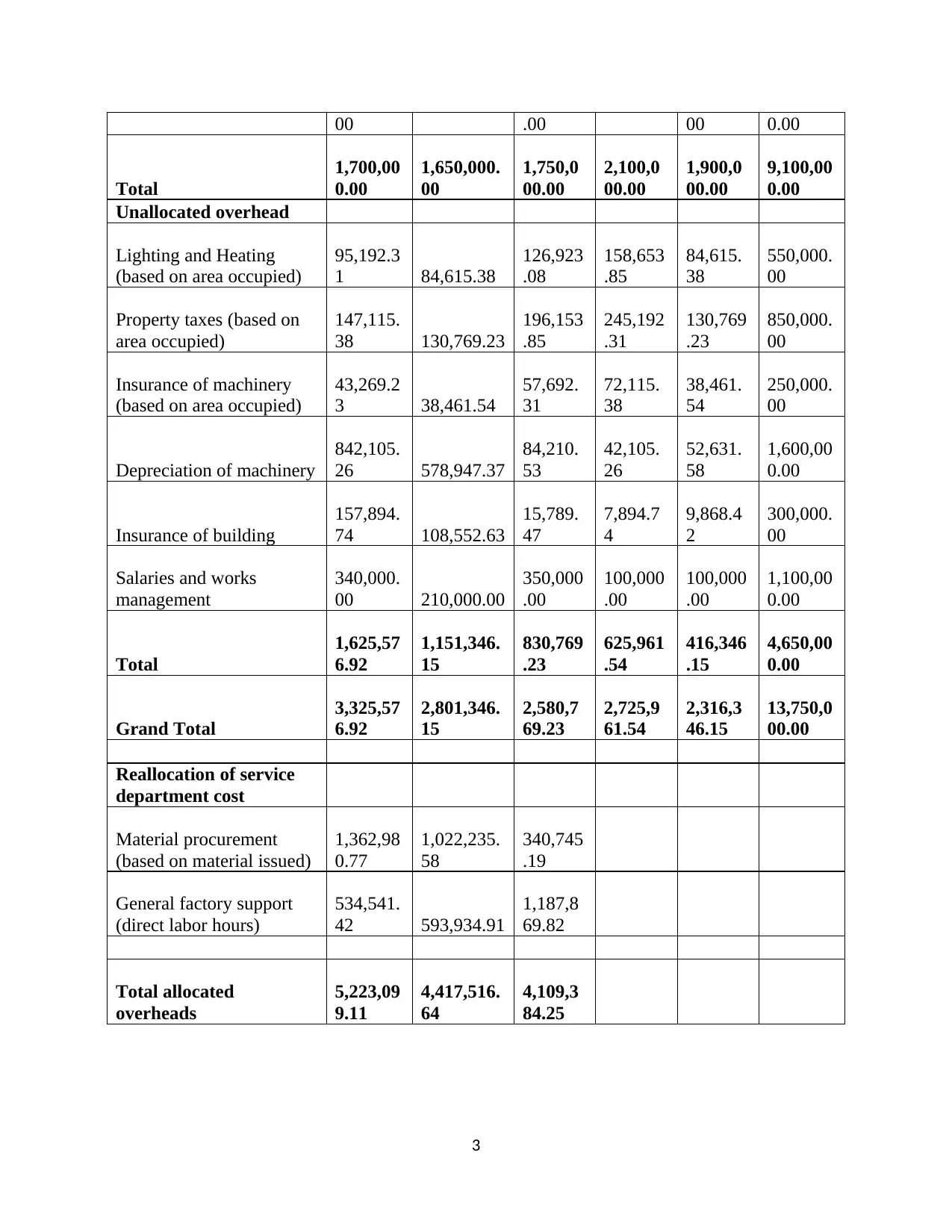

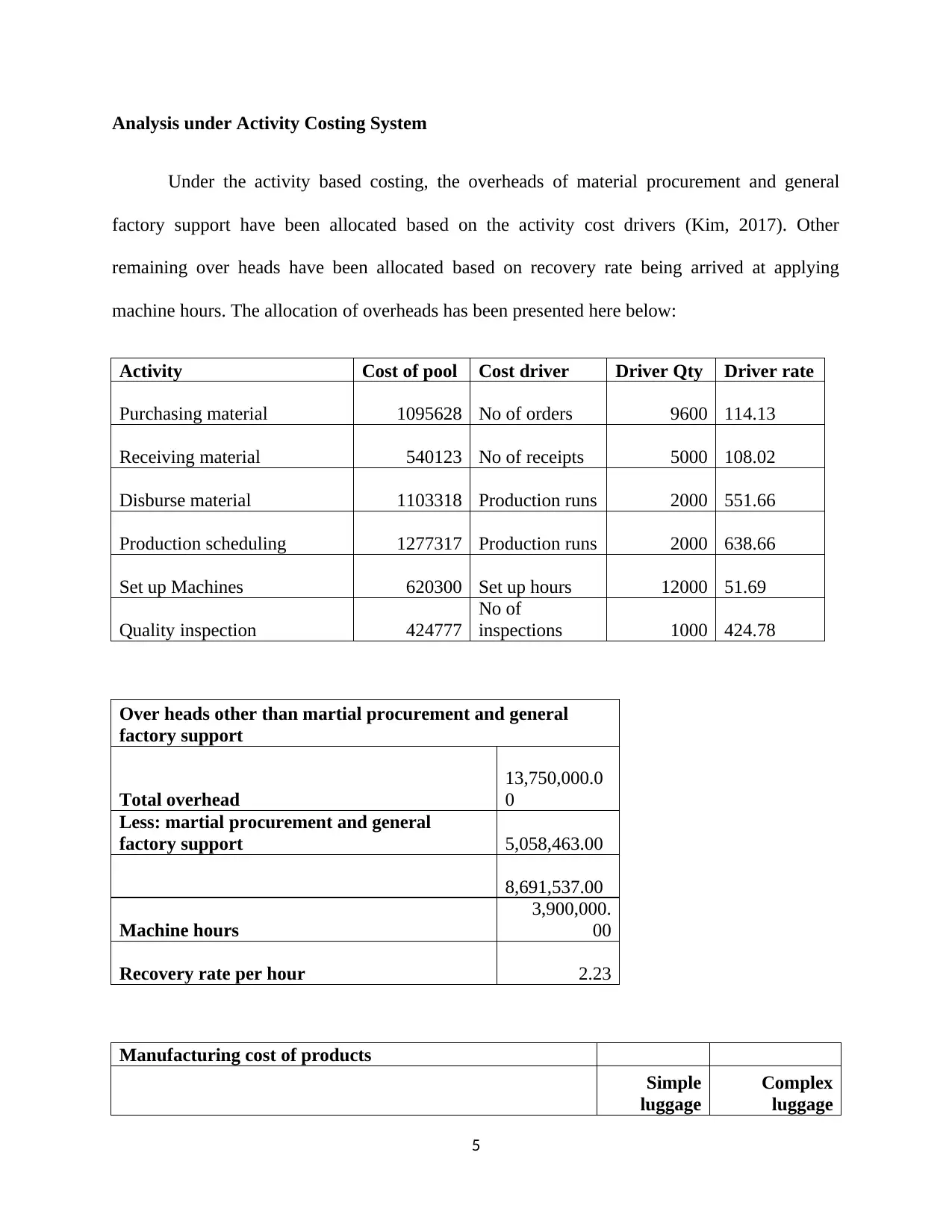

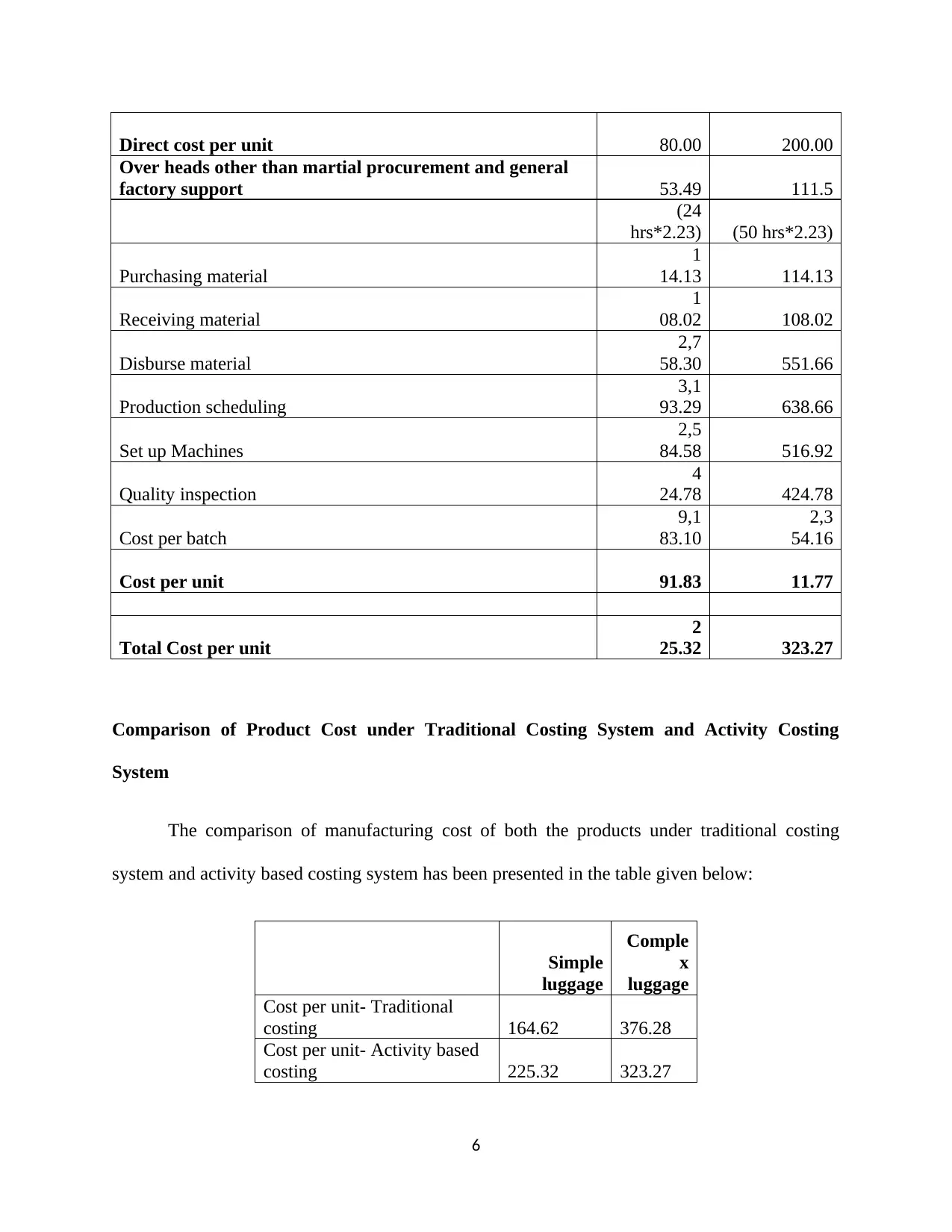

This report provides a comprehensive analysis of product costing using traditional and activity-based costing systems. It begins by outlining the limitations of traditional costing, which often allocates overhead based on volume-based cost drivers like machine or labor hours, potentially distorting product costs. The report then presents a detailed cost allocation analysis for a company, Happy Traveller Ltd, under both traditional and activity-based costing methods. Under the traditional system, overheads are allocated using a single overhead recovery rate based on machine hours, while the activity-based costing (ABC) method allocates overheads based on activity cost drivers. The report compares the manufacturing costs of two products, simple and complex luggage, under both systems, highlighting how ABC provides a more accurate picture of product costs. It concludes by discussing the advantages of ABC, such as improved decision-making and cost management, and its application within the company, emphasizing the need for identifying activities, cost drivers, and driver rates for effective implementation. The report references relevant literature to support its analysis and findings.

1 out of 9

Related Documents

![Management Accounting: Costing Analysis of Office Desks - [Company]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fjv%2Fc197923795a34b81bdce50f667d18d4c.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.