Management Accounting Report: Analysis of Airdri Company Finances

VerifiedAdded on 2020/10/22

|13

|3957

|346

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, utilizing Airdri Company as a case study. It begins with an introduction to management accounting and its objectives, followed by a detailed calculation of net profit using both marginal and absorption costing methods across three years. The report then delves into the advantages and disadvantages of various planning tools used for budgetary control, including fixed, variable, and zero-based budgets, alongside variance analysis. The analysis includes a comparison of marginal and absorption costing methods, explaining the reasons for differences in profit figures. Furthermore, the report evaluates how organizations adopt different management accounting systems, tracing the evolution of management accounting from pre-1950 to the present. The report also discusses the application of planning tools and their impact on financial problem-solving within an organization, leading to sustainable success.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

PART A.......................................................................................................................................3

Covered in PPT............................................................................................................................3

PART B........................................................................................................................................3

TASK 2............................................................................................................................................6

(a) Explain Advantage & disadvantage of different type of planning tools which is used for

budgetary control.........................................................................................................................6

(b) Analyse different planning tools and it's applications............................................................7

(C) Evaluate how organisation system adopt different management accounting system............8

(d)Analysis of financial problem in respect of management accounting which lead the

organisation for the success.........................................................................................................9

(e)Explain how planning tool solve the financial problem which lead the organisation to

sustainable success.......................................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

PART A.......................................................................................................................................3

Covered in PPT............................................................................................................................3

PART B........................................................................................................................................3

TASK 2............................................................................................................................................6

(a) Explain Advantage & disadvantage of different type of planning tools which is used for

budgetary control.........................................................................................................................6

(b) Analyse different planning tools and it's applications............................................................7

(C) Evaluate how organisation system adopt different management accounting system............8

(d)Analysis of financial problem in respect of management accounting which lead the

organisation for the success.........................................................................................................9

(e)Explain how planning tool solve the financial problem which lead the organisation to

sustainable success.......................................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In business scenario, management accounting is defined as the process of analysing,

gathering, recording and reporting of useful financial information that help the internal manager

to take valuable decision (Abdel-Kader, 2011). Manager of company makes annual accounts by

applying generally accepted accounting principle that help the outsider stakeholder to gather

relevant information about companies happing during an accounting year. In general,

management accounting has major objective of doing so is to accomplish more benefits by

making proper use of resources within an organisation. To better understand the concept of

management accounting Airdri company is selected. This company produces designer hand dryer

with best price within Industry.

The main aim of this project report is to calculate the net profit using absorption and

marginal costing method, advantages and disadvantage of different types of planning tools that

are beneficial in forecasting budgets and controlling them. Apart from this, the report also shows

that various financial tools are used by company in order to resolve the financial issues.

TASK 1

PART A

Covered in PPT

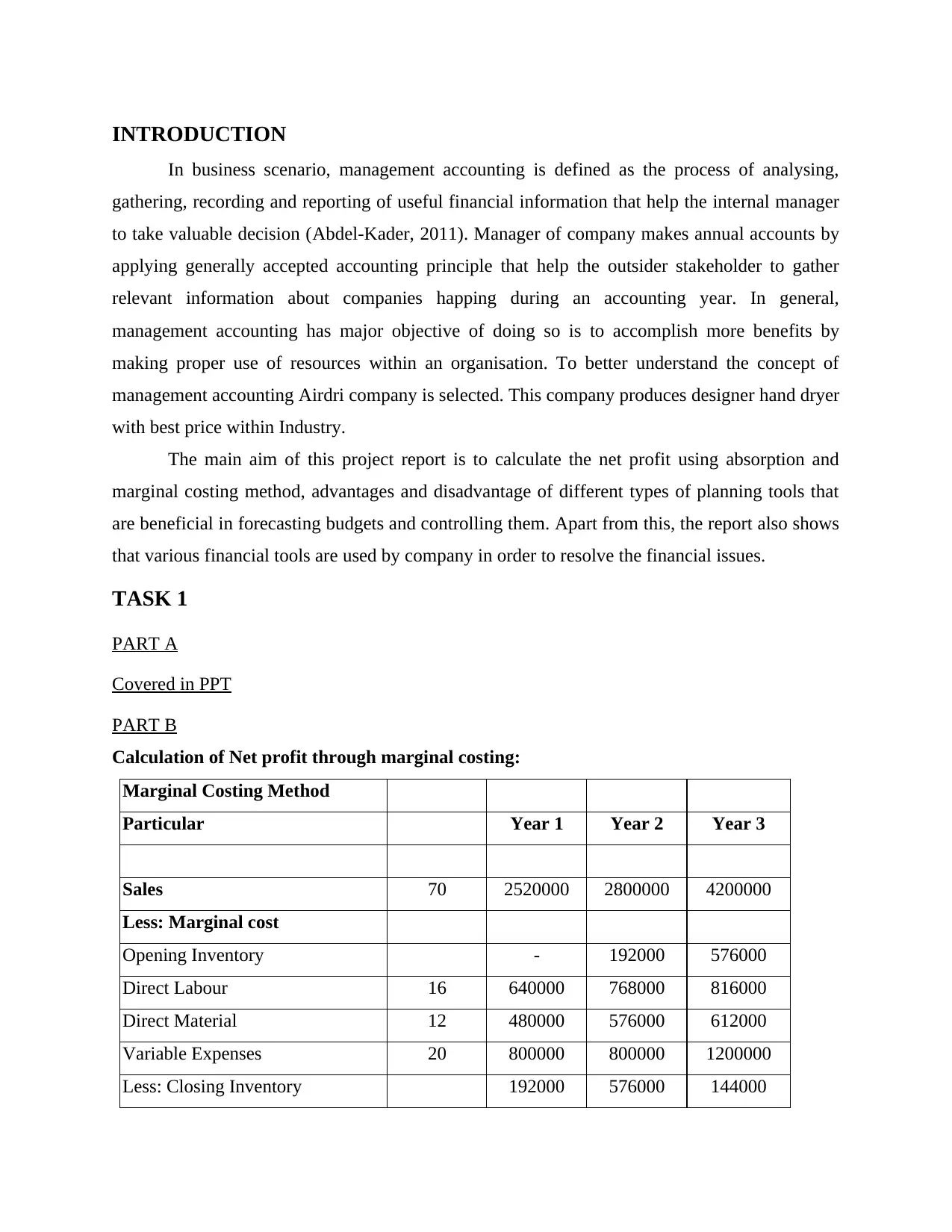

PART B

Calculation of Net profit through marginal costing:

Marginal Costing Method

Particular Year 1 Year 2 Year 3

Sales 70 2520000 2800000 4200000

Less: Marginal cost

Opening Inventory - 192000 576000

Direct Labour 16 640000 768000 816000

Direct Material 12 480000 576000 612000

Variable Expenses 20 800000 800000 1200000

Less: Closing Inventory 192000 576000 144000

In business scenario, management accounting is defined as the process of analysing,

gathering, recording and reporting of useful financial information that help the internal manager

to take valuable decision (Abdel-Kader, 2011). Manager of company makes annual accounts by

applying generally accepted accounting principle that help the outsider stakeholder to gather

relevant information about companies happing during an accounting year. In general,

management accounting has major objective of doing so is to accomplish more benefits by

making proper use of resources within an organisation. To better understand the concept of

management accounting Airdri company is selected. This company produces designer hand dryer

with best price within Industry.

The main aim of this project report is to calculate the net profit using absorption and

marginal costing method, advantages and disadvantage of different types of planning tools that

are beneficial in forecasting budgets and controlling them. Apart from this, the report also shows

that various financial tools are used by company in order to resolve the financial issues.

TASK 1

PART A

Covered in PPT

PART B

Calculation of Net profit through marginal costing:

Marginal Costing Method

Particular Year 1 Year 2 Year 3

Sales 70 2520000 2800000 4200000

Less: Marginal cost

Opening Inventory - 192000 576000

Direct Labour 16 640000 768000 816000

Direct Material 12 480000 576000 612000

Variable Expenses 20 800000 800000 1200000

Less: Closing Inventory 192000 576000 144000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

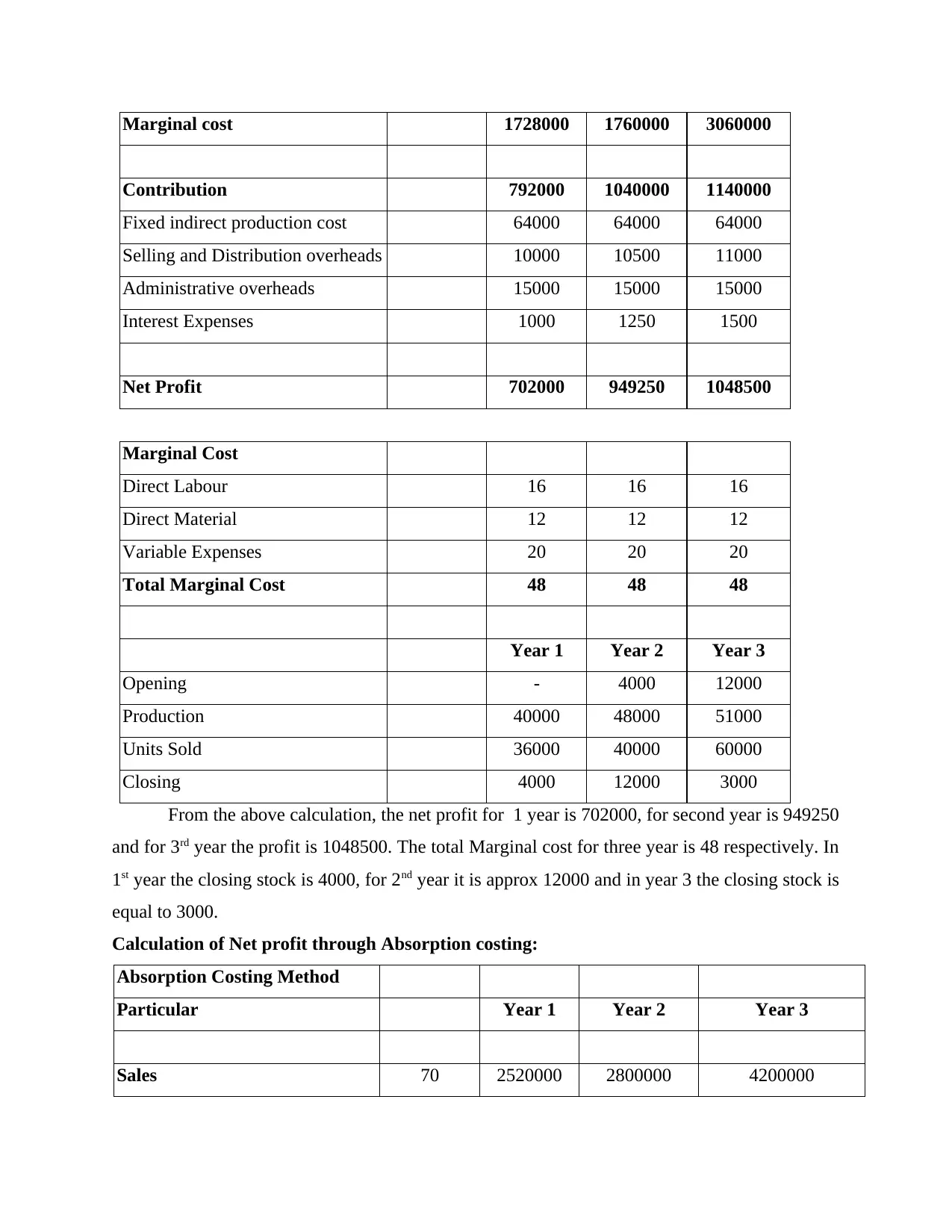

Marginal cost 1728000 1760000 3060000

Contribution 792000 1040000 1140000

Fixed indirect production cost 64000 64000 64000

Selling and Distribution overheads 10000 10500 11000

Administrative overheads 15000 15000 15000

Interest Expenses 1000 1250 1500

Net Profit 702000 949250 1048500

Marginal Cost

Direct Labour 16 16 16

Direct Material 12 12 12

Variable Expenses 20 20 20

Total Marginal Cost 48 48 48

Year 1 Year 2 Year 3

Opening - 4000 12000

Production 40000 48000 51000

Units Sold 36000 40000 60000

Closing 4000 12000 3000

From the above calculation, the net profit for 1 year is 702000, for second year is 949250

and for 3rd year the profit is 1048500. The total Marginal cost for three year is 48 respectively. In

1st year the closing stock is 4000, for 2nd year it is approx 12000 and in year 3 the closing stock is

equal to 3000.

Calculation of Net profit through Absorption costing:

Absorption Costing Method

Particular Year 1 Year 2 Year 3

Sales 70 2520000 2800000 4200000

Contribution 792000 1040000 1140000

Fixed indirect production cost 64000 64000 64000

Selling and Distribution overheads 10000 10500 11000

Administrative overheads 15000 15000 15000

Interest Expenses 1000 1250 1500

Net Profit 702000 949250 1048500

Marginal Cost

Direct Labour 16 16 16

Direct Material 12 12 12

Variable Expenses 20 20 20

Total Marginal Cost 48 48 48

Year 1 Year 2 Year 3

Opening - 4000 12000

Production 40000 48000 51000

Units Sold 36000 40000 60000

Closing 4000 12000 3000

From the above calculation, the net profit for 1 year is 702000, for second year is 949250

and for 3rd year the profit is 1048500. The total Marginal cost for three year is 48 respectively. In

1st year the closing stock is 4000, for 2nd year it is approx 12000 and in year 3 the closing stock is

equal to 3000.

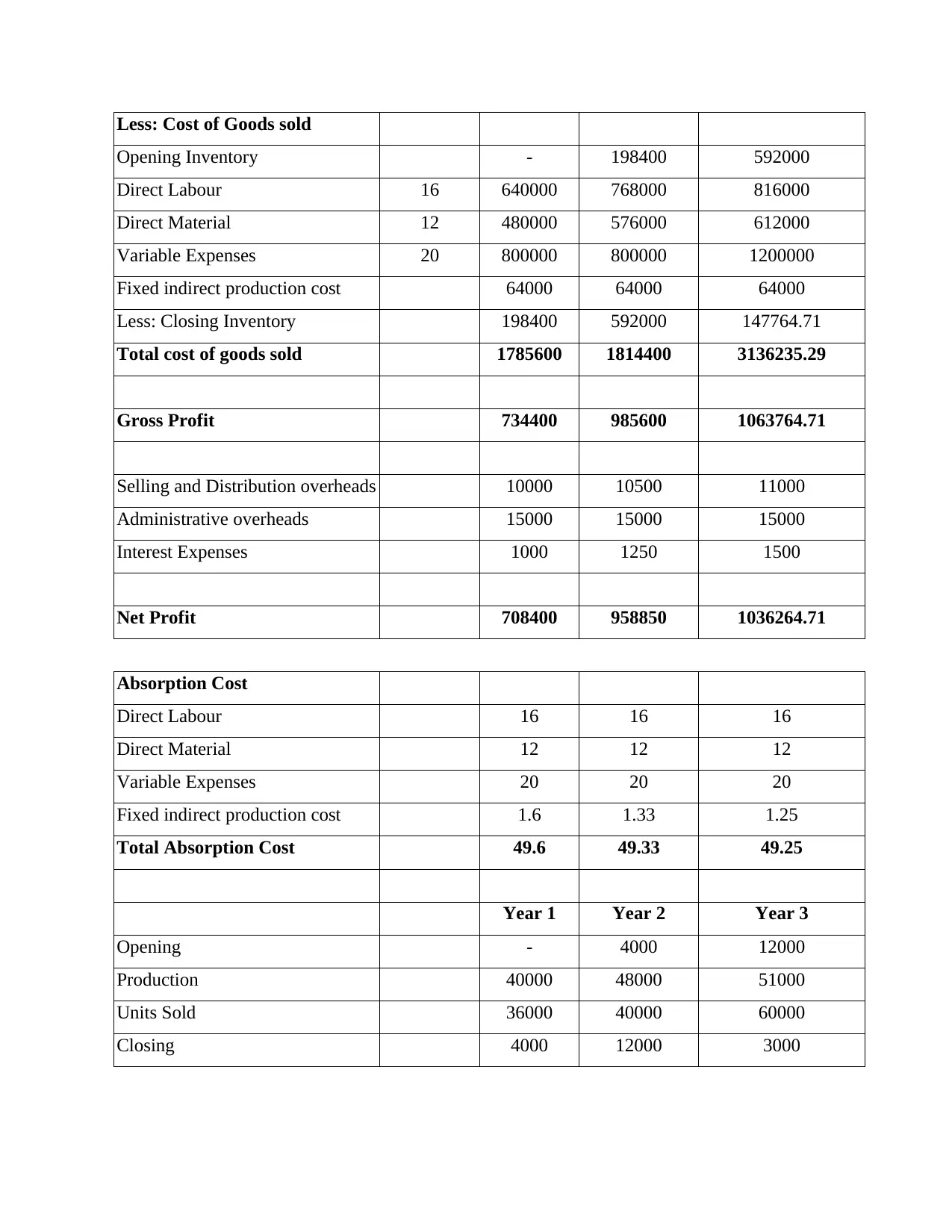

Calculation of Net profit through Absorption costing:

Absorption Costing Method

Particular Year 1 Year 2 Year 3

Sales 70 2520000 2800000 4200000

Less: Cost of Goods sold

Opening Inventory - 198400 592000

Direct Labour 16 640000 768000 816000

Direct Material 12 480000 576000 612000

Variable Expenses 20 800000 800000 1200000

Fixed indirect production cost 64000 64000 64000

Less: Closing Inventory 198400 592000 147764.71

Total cost of goods sold 1785600 1814400 3136235.29

Gross Profit 734400 985600 1063764.71

Selling and Distribution overheads 10000 10500 11000

Administrative overheads 15000 15000 15000

Interest Expenses 1000 1250 1500

Net Profit 708400 958850 1036264.71

Absorption Cost

Direct Labour 16 16 16

Direct Material 12 12 12

Variable Expenses 20 20 20

Fixed indirect production cost 1.6 1.33 1.25

Total Absorption Cost 49.6 49.33 49.25

Year 1 Year 2 Year 3

Opening - 4000 12000

Production 40000 48000 51000

Units Sold 36000 40000 60000

Closing 4000 12000 3000

Opening Inventory - 198400 592000

Direct Labour 16 640000 768000 816000

Direct Material 12 480000 576000 612000

Variable Expenses 20 800000 800000 1200000

Fixed indirect production cost 64000 64000 64000

Less: Closing Inventory 198400 592000 147764.71

Total cost of goods sold 1785600 1814400 3136235.29

Gross Profit 734400 985600 1063764.71

Selling and Distribution overheads 10000 10500 11000

Administrative overheads 15000 15000 15000

Interest Expenses 1000 1250 1500

Net Profit 708400 958850 1036264.71

Absorption Cost

Direct Labour 16 16 16

Direct Material 12 12 12

Variable Expenses 20 20 20

Fixed indirect production cost 1.6 1.33 1.25

Total Absorption Cost 49.6 49.33 49.25

Year 1 Year 2 Year 3

Opening - 4000 12000

Production 40000 48000 51000

Units Sold 36000 40000 60000

Closing 4000 12000 3000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

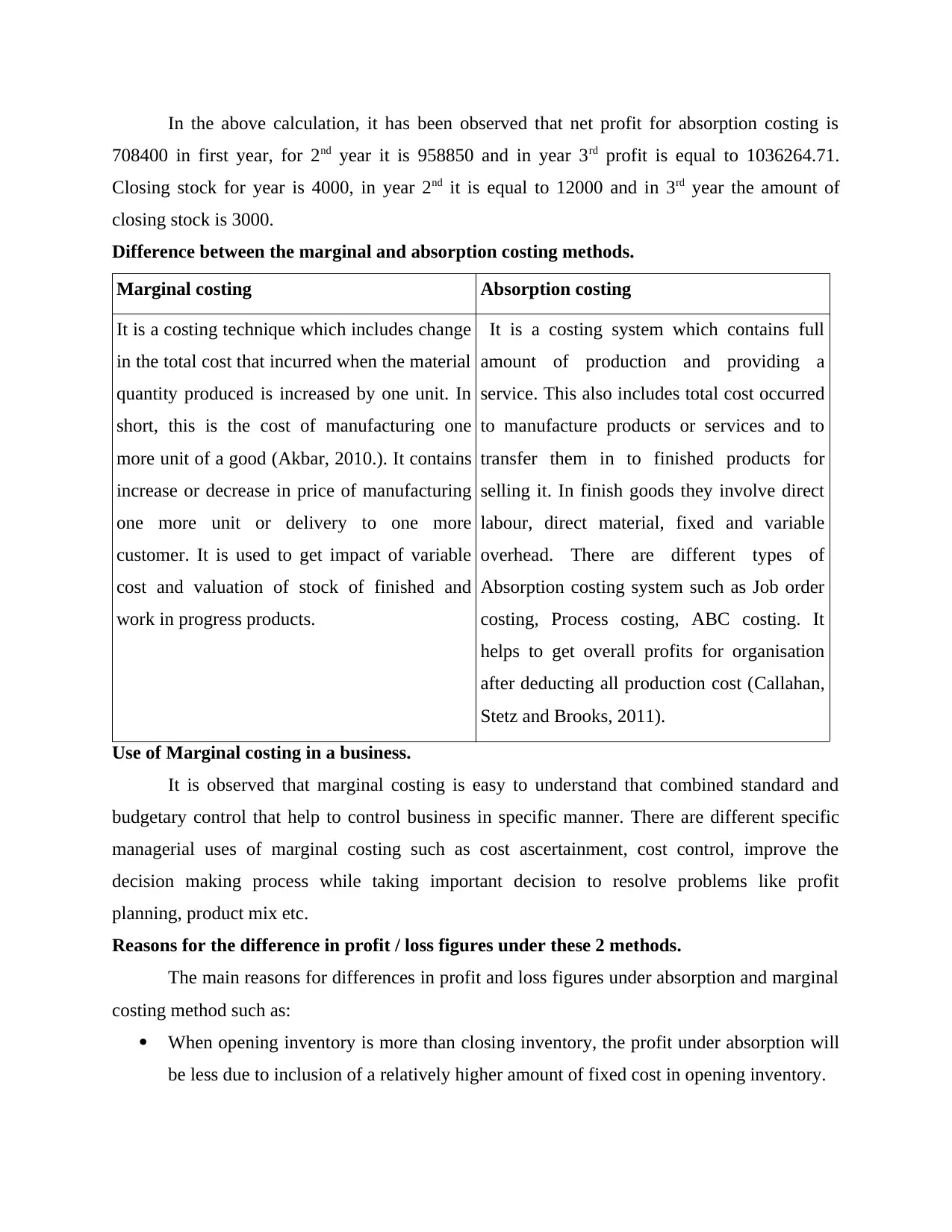

In the above calculation, it has been observed that net profit for absorption costing is

708400 in first year, for 2nd year it is 958850 and in year 3rd profit is equal to 1036264.71.

Closing stock for year is 4000, in year 2nd it is equal to 12000 and in 3rd year the amount of

closing stock is 3000.

Difference between the marginal and absorption costing methods.

Marginal costing Absorption costing

It is a costing technique which includes change

in the total cost that incurred when the material

quantity produced is increased by one unit. In

short, this is the cost of manufacturing one

more unit of a good (Akbar, 2010.). It contains

increase or decrease in price of manufacturing

one more unit or delivery to one more

customer. It is used to get impact of variable

cost and valuation of stock of finished and

work in progress products.

It is a costing system which contains full

amount of production and providing a

service. This also includes total cost occurred

to manufacture products or services and to

transfer them in to finished products for

selling it. In finish goods they involve direct

labour, direct material, fixed and variable

overhead. There are different types of

Absorption costing system such as Job order

costing, Process costing, ABC costing. It

helps to get overall profits for organisation

after deducting all production cost (Callahan,

Stetz and Brooks, 2011).

Use of Marginal costing in a business.

It is observed that marginal costing is easy to understand that combined standard and

budgetary control that help to control business in specific manner. There are different specific

managerial uses of marginal costing such as cost ascertainment, cost control, improve the

decision making process while taking important decision to resolve problems like profit

planning, product mix etc.

Reasons for the difference in profit / loss figures under these 2 methods.

The main reasons for differences in profit and loss figures under absorption and marginal

costing method such as:

When opening inventory is more than closing inventory, the profit under absorption will

be less due to inclusion of a relatively higher amount of fixed cost in opening inventory.

708400 in first year, for 2nd year it is 958850 and in year 3rd profit is equal to 1036264.71.

Closing stock for year is 4000, in year 2nd it is equal to 12000 and in 3rd year the amount of

closing stock is 3000.

Difference between the marginal and absorption costing methods.

Marginal costing Absorption costing

It is a costing technique which includes change

in the total cost that incurred when the material

quantity produced is increased by one unit. In

short, this is the cost of manufacturing one

more unit of a good (Akbar, 2010.). It contains

increase or decrease in price of manufacturing

one more unit or delivery to one more

customer. It is used to get impact of variable

cost and valuation of stock of finished and

work in progress products.

It is a costing system which contains full

amount of production and providing a

service. This also includes total cost occurred

to manufacture products or services and to

transfer them in to finished products for

selling it. In finish goods they involve direct

labour, direct material, fixed and variable

overhead. There are different types of

Absorption costing system such as Job order

costing, Process costing, ABC costing. It

helps to get overall profits for organisation

after deducting all production cost (Callahan,

Stetz and Brooks, 2011).

Use of Marginal costing in a business.

It is observed that marginal costing is easy to understand that combined standard and

budgetary control that help to control business in specific manner. There are different specific

managerial uses of marginal costing such as cost ascertainment, cost control, improve the

decision making process while taking important decision to resolve problems like profit

planning, product mix etc.

Reasons for the difference in profit / loss figures under these 2 methods.

The main reasons for differences in profit and loss figures under absorption and marginal

costing method such as:

When opening inventory is more than closing inventory, the profit under absorption will

be less due to inclusion of a relatively higher amount of fixed cost in opening inventory.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

When opening inventory is less than closing inventory, the profit under absorption

costing will be higher due to inclusion of a relatively higher amount of fixed cost in

closing inventory.

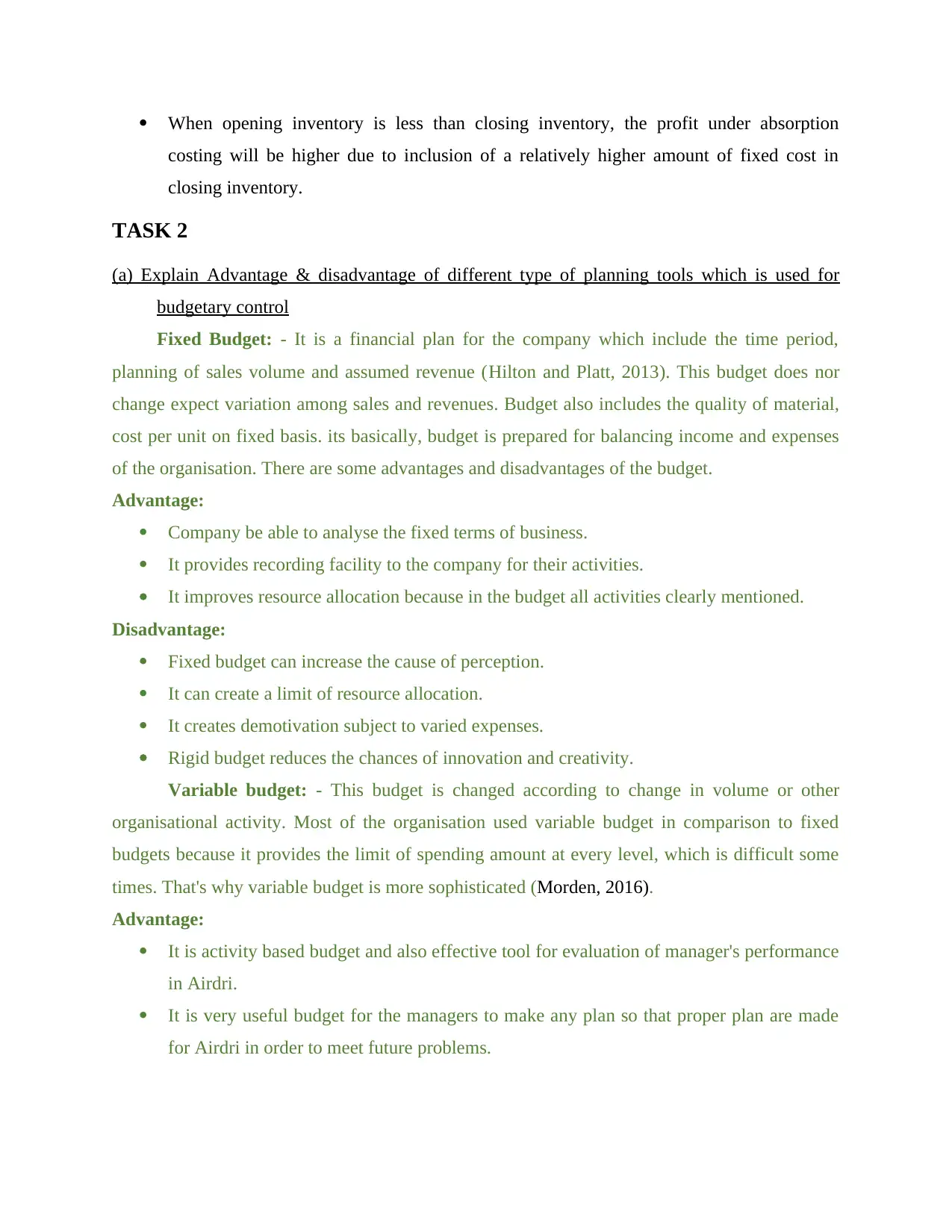

TASK 2

(a) Explain Advantage & disadvantage of different type of planning tools which is used for

budgetary control

Fixed Budget: - It is a financial plan for the company which include the time period,

planning of sales volume and assumed revenue (Hilton and Platt, 2013). This budget does nor

change expect variation among sales and revenues. Budget also includes the quality of material,

cost per unit on fixed basis. its basically, budget is prepared for balancing income and expenses

of the organisation. There are some advantages and disadvantages of the budget.

Advantage:

Company be able to analyse the fixed terms of business.

It provides recording facility to the company for their activities.

It improves resource allocation because in the budget all activities clearly mentioned.

Disadvantage:

Fixed budget can increase the cause of perception.

It can create a limit of resource allocation.

It creates demotivation subject to varied expenses.

Rigid budget reduces the chances of innovation and creativity.

Variable budget: - This budget is changed according to change in volume or other

organisational activity. Most of the organisation used variable budget in comparison to fixed

budgets because it provides the limit of spending amount at every level, which is difficult some

times. That's why variable budget is more sophisticated (Morden, 2016).

Advantage:

It is activity based budget and also effective tool for evaluation of manager's performance

in Airdri.

It is very useful budget for the managers to make any plan so that proper plan are made

for Airdri in order to meet future problems.

costing will be higher due to inclusion of a relatively higher amount of fixed cost in

closing inventory.

TASK 2

(a) Explain Advantage & disadvantage of different type of planning tools which is used for

budgetary control

Fixed Budget: - It is a financial plan for the company which include the time period,

planning of sales volume and assumed revenue (Hilton and Platt, 2013). This budget does nor

change expect variation among sales and revenues. Budget also includes the quality of material,

cost per unit on fixed basis. its basically, budget is prepared for balancing income and expenses

of the organisation. There are some advantages and disadvantages of the budget.

Advantage:

Company be able to analyse the fixed terms of business.

It provides recording facility to the company for their activities.

It improves resource allocation because in the budget all activities clearly mentioned.

Disadvantage:

Fixed budget can increase the cause of perception.

It can create a limit of resource allocation.

It creates demotivation subject to varied expenses.

Rigid budget reduces the chances of innovation and creativity.

Variable budget: - This budget is changed according to change in volume or other

organisational activity. Most of the organisation used variable budget in comparison to fixed

budgets because it provides the limit of spending amount at every level, which is difficult some

times. That's why variable budget is more sophisticated (Morden, 2016).

Advantage:

It is activity based budget and also effective tool for evaluation of manager's performance

in Airdri.

It is very useful budget for the managers to make any plan so that proper plan are made

for Airdri in order to meet future problems.

Variable budget not provide any stress because it provides the facilities to change in the

activities.

Disadvantage:

It creates confusion in the business because this budget accepts the change various time.

According to traditional budget, company need to spend in their limited budget. But

variable budget method breaks this rule and jump the boundaries (Hopper and Bui, 2016).

In this budget, it is difficult to forecast expenses because it can change according to

requirement.

Zero based budget: - This budgeting method calculate the expenses of company at every

new time which is based on actual expenses. In this budget every expenses need to be justify by

the manager (Endenich, 2014).

Advantage:

This method provides the accuracy and efficiency to allocated the resources.

It is helpful for the identification of opportunity and also very cost effective.

Disadvantage:

It is time-consuming method and required huge manpower.

Manager need to justify every line item, so it required training for this.

Variance analysis

This is one of the type of budgetary analysis that helps to identify the differences between

actual and standard budgets. This is one of the effective tool that helps to manage the available

resources in more strategic and impactful manner.

Advantage:

This method provides the Appropriateness and efficiency subject to available resources.

It assist in managing the variation among different sections .

Disadvantage:

It does not provide clear aspects regarding available financial resources.

This is one of the statistical aspect that helps in determining the regulatory framework of

business and operations.

(b) Analyse different planning tools and it's applications

According to the above mentioned various types of planning tools, it has been examining

that all of them are equally helpful for earning sufficient amount of profitability by controlling

activities.

Disadvantage:

It creates confusion in the business because this budget accepts the change various time.

According to traditional budget, company need to spend in their limited budget. But

variable budget method breaks this rule and jump the boundaries (Hopper and Bui, 2016).

In this budget, it is difficult to forecast expenses because it can change according to

requirement.

Zero based budget: - This budgeting method calculate the expenses of company at every

new time which is based on actual expenses. In this budget every expenses need to be justify by

the manager (Endenich, 2014).

Advantage:

This method provides the accuracy and efficiency to allocated the resources.

It is helpful for the identification of opportunity and also very cost effective.

Disadvantage:

It is time-consuming method and required huge manpower.

Manager need to justify every line item, so it required training for this.

Variance analysis

This is one of the type of budgetary analysis that helps to identify the differences between

actual and standard budgets. This is one of the effective tool that helps to manage the available

resources in more strategic and impactful manner.

Advantage:

This method provides the Appropriateness and efficiency subject to available resources.

It assist in managing the variation among different sections .

Disadvantage:

It does not provide clear aspects regarding available financial resources.

This is one of the statistical aspect that helps in determining the regulatory framework of

business and operations.

(b) Analyse different planning tools and it's applications

According to the above mentioned various types of planning tools, it has been examining

that all of them are equally helpful for earning sufficient amount of profitability by controlling

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the budgets of the company (Grabner and Moers, 2013). By the help of variablebudgets manager

are can easily be able to determine their upcoming issues those are affecting the operation on

regular interval. While with the use of Zero based budgets manager are able to calculate business

outflows that are related with company’s promotion or other activity in coming period of time. It

has been found that there are specific kind of risk that can affect the overall growth and

efficiency at the time of production process whose entire influence is been seen on reputation of

the company.

(C) Evaluate how organisation system adopt different management accounting system

History of management accounting

Pre 1950: In recent time management accounting is more involved with regression

analysis, linear programming and probability theory. So manager use to do the manual

recording of transaction to keep the day to day records (Cleary, 2015). The accounting is

done by recording data on every day transaction at the end of the day. This was the stage in

which financial control and cost determination was the main objective of business. In

managerial accounting it this age was so diminising.

1950-1970: After the end of 1950, the government established an institution called

AIA which are responsible to set accounting standards that were founded in early 1936. The

(SOX) Sarbanes-Oxley Act was enforced to heighten accounting regulation so that auditing

can be made easily for the accuracy of company financial statements (Zoni Dossi and Morelli,

2012). In interrelation market feasibility of management accounting was one of the complex

factor highlighted in different countries. Diverse culture and strategies is the major aspect to

be related with these scenarios.

1970-1990: From there, there has been drastic changes in the system of management

accounting, as it has been observed that 1970s, inflation and political uncertainty put

maximum pressure on the accountancy profession to shape up as per the requirement of the

company. In this age the IAFC (International Federation of Accounts was concerned about

the purpose of management accounting and underpins the accounting concepts in various

forms.

1990 to current time: It has been determine that there is huge modification is seen in

the recording of financial transactions. With the use of Key performance indicators, financial

are can easily be able to determine their upcoming issues those are affecting the operation on

regular interval. While with the use of Zero based budgets manager are able to calculate business

outflows that are related with company’s promotion or other activity in coming period of time. It

has been found that there are specific kind of risk that can affect the overall growth and

efficiency at the time of production process whose entire influence is been seen on reputation of

the company.

(C) Evaluate how organisation system adopt different management accounting system

History of management accounting

Pre 1950: In recent time management accounting is more involved with regression

analysis, linear programming and probability theory. So manager use to do the manual

recording of transaction to keep the day to day records (Cleary, 2015). The accounting is

done by recording data on every day transaction at the end of the day. This was the stage in

which financial control and cost determination was the main objective of business. In

managerial accounting it this age was so diminising.

1950-1970: After the end of 1950, the government established an institution called

AIA which are responsible to set accounting standards that were founded in early 1936. The

(SOX) Sarbanes-Oxley Act was enforced to heighten accounting regulation so that auditing

can be made easily for the accuracy of company financial statements (Zoni Dossi and Morelli,

2012). In interrelation market feasibility of management accounting was one of the complex

factor highlighted in different countries. Diverse culture and strategies is the major aspect to

be related with these scenarios.

1970-1990: From there, there has been drastic changes in the system of management

accounting, as it has been observed that 1970s, inflation and political uncertainty put

maximum pressure on the accountancy profession to shape up as per the requirement of the

company. In this age the IAFC (International Federation of Accounts was concerned about

the purpose of management accounting and underpins the accounting concepts in various

forms.

1990 to current time: It has been determine that there is huge modification is seen in

the recording of financial transactions. With the use of Key performance indicators, financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

governance and benchmarking tools are taken into consideration. This will make easy for the

accountant to because of automatic data tools. Another caveat, recognized by the statement,

is that the scope, role, and organizational positioning of management accounting differ

across

organizations, cultures and countries How companies use it to detect their financial

problems.

In recent time, companies are helpful in determining the financial problems with the

support of different accounting tools that follows the concept of management accounting. So

there are different techniques that are used by Airdri in order to detect the financial problems. All

of them are discussed below:

Ratio analysis: - It is a quantitative analysis of company's information and it evaluate the

various aspect of organisational financial and operational performance. Such as company's

liquidity, efficiency, solvency and profitability (Takeda and Boyns, 2014). It is also called

financial ratio of the company and it includes the 5 major type of ratio analysis like activity,

liquidity, profitability, debt and market ratio. This analysis is often used by the accountant for the

comparison of their records. There is an ongoing problem in Airdri that they are not able manage

so manager use the Ratio analyses to determine the excess loss company is bearing for a longer

period. They are helpful to determine that because of addition expense on advertising and less

profit generation company is bearing losses.

Benchmarking: Benchmarking is the process of comparing company's process and

performance. The dimension of the comparison is based on time, quality and cost invest by the

company on any product (Lavia López and Hiebl, 2014). Main objective of the organisation is to

understand the current position of the business. Follow best practice for the identification of best

area of improving performance. This method supports the selection, planning and delivery of

projects of the company. Manager of Airdri use to detect the problem of excess use of resources

and less result due to profitability and productivity of company is keeps on reducing.

Balance scorecard: It is a strategic approach used as matrix in order to determine the

gaps and improve the section by implementing valid action plans. Data collection is type of

information used in more preferable and determined manner (Holsapple, 2013). This approach

was introduced by Dr. Robert Kaplan and the business executive Dr. David Norton.

accountant to because of automatic data tools. Another caveat, recognized by the statement,

is that the scope, role, and organizational positioning of management accounting differ

across

organizations, cultures and countries How companies use it to detect their financial

problems.

In recent time, companies are helpful in determining the financial problems with the

support of different accounting tools that follows the concept of management accounting. So

there are different techniques that are used by Airdri in order to detect the financial problems. All

of them are discussed below:

Ratio analysis: - It is a quantitative analysis of company's information and it evaluate the

various aspect of organisational financial and operational performance. Such as company's

liquidity, efficiency, solvency and profitability (Takeda and Boyns, 2014). It is also called

financial ratio of the company and it includes the 5 major type of ratio analysis like activity,

liquidity, profitability, debt and market ratio. This analysis is often used by the accountant for the

comparison of their records. There is an ongoing problem in Airdri that they are not able manage

so manager use the Ratio analyses to determine the excess loss company is bearing for a longer

period. They are helpful to determine that because of addition expense on advertising and less

profit generation company is bearing losses.

Benchmarking: Benchmarking is the process of comparing company's process and

performance. The dimension of the comparison is based on time, quality and cost invest by the

company on any product (Lavia López and Hiebl, 2014). Main objective of the organisation is to

understand the current position of the business. Follow best practice for the identification of best

area of improving performance. This method supports the selection, planning and delivery of

projects of the company. Manager of Airdri use to detect the problem of excess use of resources

and less result due to profitability and productivity of company is keeps on reducing.

Balance scorecard: It is a strategic approach used as matrix in order to determine the

gaps and improve the section by implementing valid action plans. Data collection is type of

information used in more preferable and determined manner (Holsapple, 2013). This approach

was introduced by Dr. Robert Kaplan and the business executive Dr. David Norton.

Key Performance Indicator (KPI): It is measurement tool which identify the

performance in comparison to business objective. It shows that how organisation achieve their

goals in effectively manner (Armitage, Webb and Glynn, 2016). It also includes two type of KPI

such as low or high level, low level KPI focus on employees in the department like marketing

and sales. Overall performance measured by the high level KPI. With the help of this tool

company is able to detect the problem of increasing employee’s turnover due to which profit is

reducing in a specific time period.

Airdri Tesco

In the Airdri company, manager find the

problem in the financial statements. That is

about cash flow of the organisation. Cash

outflow is higher than cash inflow.

Tesco company find the problem which is

related to wastage of stock or some time

shortage too. So they can order enough raw

material because higher inventory cause

carrying cost and lower inventory can face the

shortage of material which affect the

production level.

It used balanced scorecard approach to detect

the problem in more effective way.

Financial KPI is used to understand the key

strategic problems occurred in inventory

management and operations.

Airdri adopt cost control system to reduce

their outflow of money. This method helps the

company to reduce their expenses which can

increase profitability.

So company follow the inventory management

system for effective work. Company make

proper team for managing inventory and give

instruction to keep their regular eyes on

inventory.

(d)Analysis of financial problem in respect of management accounting which lead the

organisation for the success

Airdri company's manager follow the different management accounting systems to solve

the financial problem which develop in the organisation. For example: - company face the issue

regarding their cash flow (Schaltegger, Burritt and Petersen, 2017). So the manager of the

company follows the cost control method which provide the better efficiency to the Airdri.

performance in comparison to business objective. It shows that how organisation achieve their

goals in effectively manner (Armitage, Webb and Glynn, 2016). It also includes two type of KPI

such as low or high level, low level KPI focus on employees in the department like marketing

and sales. Overall performance measured by the high level KPI. With the help of this tool

company is able to detect the problem of increasing employee’s turnover due to which profit is

reducing in a specific time period.

Airdri Tesco

In the Airdri company, manager find the

problem in the financial statements. That is

about cash flow of the organisation. Cash

outflow is higher than cash inflow.

Tesco company find the problem which is

related to wastage of stock or some time

shortage too. So they can order enough raw

material because higher inventory cause

carrying cost and lower inventory can face the

shortage of material which affect the

production level.

It used balanced scorecard approach to detect

the problem in more effective way.

Financial KPI is used to understand the key

strategic problems occurred in inventory

management and operations.

Airdri adopt cost control system to reduce

their outflow of money. This method helps the

company to reduce their expenses which can

increase profitability.

So company follow the inventory management

system for effective work. Company make

proper team for managing inventory and give

instruction to keep their regular eyes on

inventory.

(d)Analysis of financial problem in respect of management accounting which lead the

organisation for the success

Airdri company's manager follow the different management accounting systems to solve

the financial problem which develop in the organisation. For example: - company face the issue

regarding their cash flow (Schaltegger, Burritt and Petersen, 2017). So the manager of the

company follows the cost control method which provide the better efficiency to the Airdri.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.