Management Accounting Report: Snooker England Ltd. Analysis

VerifiedAdded on 2022/11/30

|14

|4189

|1

Report

AI Summary

This report examines the application of management accounting principles within Snooker England Ltd. It begins with an introduction to management accounting, outlining its essential requirements, including cost accounting, inventory management, price optimization, and job costing systems. The report then analyzes management accounting reporting, such as budget reports, account receivable aging reports, and cost accounting managerial reports. It evaluates the benefits of management accounting systems, emphasizing their role in improving organizational efficiency and financial performance. The core of the report focuses on cost calculation, comparing marginal and absorption costing methods, including their advantages, disadvantages, and application through financial statements. The report concludes by evaluating the integration of planning tools to solve financial problems. The report is written from the perspective of Snooker England Limited, an organization that produces goods and equipment for the snooker industry.

Management

Accounting

.

Accounting

.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management accounting and essential requirements of management accounting system3

P2 Management accounting reporting....................................................................................4

M1 Management accounting benefits and their application within organisation...................5

Evaluation of management accounting system and management reporting system within

organisation............................................................................................................................6

TASK 2............................................................................................................................................6

P3 Cost calculation.................................................................................................................6

M2 Application of techniques for engage management accounting......................................9

D2 Production of financial report for apply and interpret in different range of activities.....9

TASK 3............................................................................................................................................9

P4 Advantages and disadvantages of different types of planning budgetary tools................9

M3 Planning tools and their use...........................................................................................11

TASK 4..........................................................................................................................................12

P5 Compare of two organisation on the basis of adoption of management accounting system

for overcome from different financial problems..................................................................12

M4 Financial problems analyse............................................................................................13

D3) Evaluation of planning tools.........................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

.

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management accounting and essential requirements of management accounting system3

P2 Management accounting reporting....................................................................................4

M1 Management accounting benefits and their application within organisation...................5

Evaluation of management accounting system and management reporting system within

organisation............................................................................................................................6

TASK 2............................................................................................................................................6

P3 Cost calculation.................................................................................................................6

M2 Application of techniques for engage management accounting......................................9

D2 Production of financial report for apply and interpret in different range of activities.....9

TASK 3............................................................................................................................................9

P4 Advantages and disadvantages of different types of planning budgetary tools................9

M3 Planning tools and their use...........................................................................................11

TASK 4..........................................................................................................................................12

P5 Compare of two organisation on the basis of adoption of management accounting system

for overcome from different financial problems..................................................................12

M4 Financial problems analyse............................................................................................13

D3) Evaluation of planning tools.........................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

.

INTRODUCTION

Management accounting is the use of different accounting provisions, techniques and tools

which supports an organisation for formulation of effective decisions which improve or

maximise the organisation productivity. With right decisions an organisation enhance their

profitability that is used for formulation of competitive-edge in market. The report is written

from perspective of Snooker England Limited, an organisation that produces goods and

equipment for snooker industry (Charifzadeh and Taschner, 2017). Management accounting

system and management accounting reporting with their integration among organisation process

will be highlight in this report. Formulation of financial report to interpret information from

different range of activities will be included in this report. In the last, evaluation of planning

tools to solve financial problems is undertaken within the report.

TASK 1

P1 Management accounting and essential requirements of management accounting system

Management accounting is explained as a set of accounting system which is used for

completion of work with induce of right decisions. Snooker England Ltd. use management to

achieve their goals and objectives with no issue.

Management accounting system and its essential use are mention as follow:

Cost accounting system- Cost of products is managed and controlled through use of

right techniques and methods of cost accounting system. This aids an organisation and

also, England snooker Ltd. to accomplish its goals within decided budget.

Essential requirements

Cost accounting system is used for minimise the overall cost by controlling variable

expenses related with business and it results in increase of organisational profits.

With monitoring overall operational cost and manufacturing cost of Snooker Ltd.

management improve their cost controlling system by removing unessential cost factors

(Chiarini and Vagnoni,, 2015).

Inventory management system- All resources are utilised by manager in an organised

manner through induced of appropriate inventory system. Along with this Snooker Ltd.

organisation ensure to utilise all inventories with a proper system.

Essential requirements

.

Management accounting is the use of different accounting provisions, techniques and tools

which supports an organisation for formulation of effective decisions which improve or

maximise the organisation productivity. With right decisions an organisation enhance their

profitability that is used for formulation of competitive-edge in market. The report is written

from perspective of Snooker England Limited, an organisation that produces goods and

equipment for snooker industry (Charifzadeh and Taschner, 2017). Management accounting

system and management accounting reporting with their integration among organisation process

will be highlight in this report. Formulation of financial report to interpret information from

different range of activities will be included in this report. In the last, evaluation of planning

tools to solve financial problems is undertaken within the report.

TASK 1

P1 Management accounting and essential requirements of management accounting system

Management accounting is explained as a set of accounting system which is used for

completion of work with induce of right decisions. Snooker England Ltd. use management to

achieve their goals and objectives with no issue.

Management accounting system and its essential use are mention as follow:

Cost accounting system- Cost of products is managed and controlled through use of

right techniques and methods of cost accounting system. This aids an organisation and

also, England snooker Ltd. to accomplish its goals within decided budget.

Essential requirements

Cost accounting system is used for minimise the overall cost by controlling variable

expenses related with business and it results in increase of organisational profits.

With monitoring overall operational cost and manufacturing cost of Snooker Ltd.

management improve their cost controlling system by removing unessential cost factors

(Chiarini and Vagnoni,, 2015).

Inventory management system- All resources are utilised by manager in an organised

manner through induced of appropriate inventory system. Along with this Snooker Ltd.

organisation ensure to utilise all inventories with a proper system.

Essential requirements

.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management system tracks the use of inventories so it helps organisation for

manage and utilise all inventories in an organised manner.

The inventory management system also control the number of resources and it helps to

manufacture snooker equipment with no problems (Flachère, 2014). Example- lack of

resource stop production system but inventory management systems help to overcome

from this.

Price optimisation system- The price optimisation system is utilised by organisation for

decided right and actual price of its products and services. Moreover, management of

snooker limited ensure that it profits are margins are maintained properly.

Essential requirements

Price optimisation system is required for decide right price of services and products that

help to cover operation cost and then add appropriate profit margin within business.

Profits are required by the organisation to increase their business size so it is essential for

Snooker ltd. to engage price optimisation system in proper manner.

Job costing system- This is primarily used by the organisation which performs their

roles in the manufacturing system. Snooker England Ltd. manufactures equipment so it

helps them for managing all jobs in a coordinated manner and also in minimum time-

period (Ghasemi and et. al., 2019).

Essential requirements

Job orders ensure all task are managed and completed in an effective manner and it helps

them for managing jobs in proper manner.

On the other side, another important requirement of job costing is used for satisfying

customers and clients needs in proper manner by improving values in products.

P2 Management accounting reporting

Management account reports are used by organisation for analyse as well as interpret all

information in an appropriate manner. On the other side, Snooker Ltd. interpret all data to

perform their task with no issue and problems with use of various management accounting

reporting system that are mention as follow:

Budget report- This report is based on the various segments that relates with budget and

it includes production budget, master budget, cash budget, etc. Snooker Ltd. improves

.

manage and utilise all inventories in an organised manner.

The inventory management system also control the number of resources and it helps to

manufacture snooker equipment with no problems (Flachère, 2014). Example- lack of

resource stop production system but inventory management systems help to overcome

from this.

Price optimisation system- The price optimisation system is utilised by organisation for

decided right and actual price of its products and services. Moreover, management of

snooker limited ensure that it profits are margins are maintained properly.

Essential requirements

Price optimisation system is required for decide right price of services and products that

help to cover operation cost and then add appropriate profit margin within business.

Profits are required by the organisation to increase their business size so it is essential for

Snooker ltd. to engage price optimisation system in proper manner.

Job costing system- This is primarily used by the organisation which performs their

roles in the manufacturing system. Snooker England Ltd. manufactures equipment so it

helps them for managing all jobs in a coordinated manner and also in minimum time-

period (Ghasemi and et. al., 2019).

Essential requirements

Job orders ensure all task are managed and completed in an effective manner and it helps

them for managing jobs in proper manner.

On the other side, another important requirement of job costing is used for satisfying

customers and clients needs in proper manner by improving values in products.

P2 Management accounting reporting

Management account reports are used by organisation for analyse as well as interpret all

information in an appropriate manner. On the other side, Snooker Ltd. interpret all data to

perform their task with no issue and problems with use of various management accounting

reporting system that are mention as follow:

Budget report- This report is based on the various segments that relates with budget and

it includes production budget, master budget, cash budget, etc. Snooker Ltd. improves

.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

their efficiency through completing task with use of right information system. Also,

budget report maximise company efficiency by performing task with a certain amount.

Account receivable aging report- With use of account receivable report management is

able to analyse the number of trade receivables. It results that appropriate number of

debtors is identified by organisation to collect all payments. Snooker Ltd. use account

receivable report for achieve their goals with ensure that there is no issue of monetary

factor.

Cost accounting managerial report- The cost accounting report is used by organisation

for analyse of all cost level. It is used for improve and interpret cost management system

by understanding the overall cost factors (Jinga and DUMITRU, 2015). On the other side,

cost accounting report reduces the operation cost by reducing unnecessary expense from

process. It results profits of Snooker ltd. are increased if cost is reduced.

M1 Management accounting benefits and their application within organisation

All systems that are related with management accounting system provide different benefits

to the organisation and all of them work with motive of improving organisation efficiency and

effectiveness. From the perspective of Snooker Limited it is identified that management is

focused for improve of overall financial perspective. So cost accounting system help

organisation to ensure that cost is reduced and controlled by management. Overheads cost

monitoring is one of the major advantages of cost accounting system. Inventory management

system also ensures stocks as well as inventory is managed by organisation in proper manner.

Snooker England limited ensure that at the time of manufacturing all resources are utilised in

proper manner. One the other side, job costing system ensure that job orders is tracked and

completed in proper manner. Along with this job orders also helps to complete and then deliver

order in minimum time (Kaminska and Kolesnikova, 2014). Price optimisation system benefits

the organisation by utilising all price factors including fixed and variable. In the last, right prices

benefit management for earn accurate margin on their products offering.

D1) Evaluation of management accounting system and management reporting system within

organisation

The term management accounting system is utilised by organisation for performing their

task according to the desired and essential level of efficiency. From the perspective of respective

.

budget report maximise company efficiency by performing task with a certain amount.

Account receivable aging report- With use of account receivable report management is

able to analyse the number of trade receivables. It results that appropriate number of

debtors is identified by organisation to collect all payments. Snooker Ltd. use account

receivable report for achieve their goals with ensure that there is no issue of monetary

factor.

Cost accounting managerial report- The cost accounting report is used by organisation

for analyse of all cost level. It is used for improve and interpret cost management system

by understanding the overall cost factors (Jinga and DUMITRU, 2015). On the other side,

cost accounting report reduces the operation cost by reducing unnecessary expense from

process. It results profits of Snooker ltd. are increased if cost is reduced.

M1 Management accounting benefits and their application within organisation

All systems that are related with management accounting system provide different benefits

to the organisation and all of them work with motive of improving organisation efficiency and

effectiveness. From the perspective of Snooker Limited it is identified that management is

focused for improve of overall financial perspective. So cost accounting system help

organisation to ensure that cost is reduced and controlled by management. Overheads cost

monitoring is one of the major advantages of cost accounting system. Inventory management

system also ensures stocks as well as inventory is managed by organisation in proper manner.

Snooker England limited ensure that at the time of manufacturing all resources are utilised in

proper manner. One the other side, job costing system ensure that job orders is tracked and

completed in proper manner. Along with this job orders also helps to complete and then deliver

order in minimum time (Kaminska and Kolesnikova, 2014). Price optimisation system benefits

the organisation by utilising all price factors including fixed and variable. In the last, right prices

benefit management for earn accurate margin on their products offering.

D1) Evaluation of management accounting system and management reporting system within

organisation

The term management accounting system is utilised by organisation for performing their

task according to the desired and essential level of efficiency. From the perspective of respective

.

organisation management accounting is integrated among organisation process to increase their

profits level. Similarly, management accounting reporting is also integrated in the organisation

process of Snooker Ltd because this helps to perform all work with use of right and appropriate

information. It results that all task are completed by management according to systems that

enhance company performance and also maximise company profits. This results work is

managed to solve problems for managing task in decided budget.

TASK 2

P3 Cost calculation

Marginal costing- This is explained as the technique through which overall marginal cost

is managed by charging it from unit of cost. Snooker Ltd. utilise the marginal costing technique

because it helps for calculation of profits in proper manner.

Advantages

Marginal costing technique is simplified so this is easy to understand and it also helps

organisation for determine appropriate level of profits (Kharlamova and et. al., 2020).

This minimise the problems for completion of task according to decided goals.

Marginal costing technique determine all profits and it aids organisation for completion

of task in an accurate manner by engage of right approach within business. This is also

used for interpretation better decision by deciding accurate margins for organisation.

Disadvantage

It relies on various assumptions related with business so sometimes they not generate

right statement for organisation to perform business properly.

Sometimes marginal costing is not able for control overheads and it create problems for

organisation to perform all business in proper manner.

Absorption costing- This is explained as the technique by which organisation identify all

cost that relates with process of production (Lavia López and Hiebl, 2015). Snooker ltd. ensures

profits are utilised in proper manner and it also reduce all problems for treating or overcome

from the overheads related issue.

Advantages

This technique is more beneficial for organisation as it ensures that they are able for

identify of production cost. Snooker Ltd. calculates all cost by use of absorption costing.

.

profits level. Similarly, management accounting reporting is also integrated in the organisation

process of Snooker Ltd because this helps to perform all work with use of right and appropriate

information. It results that all task are completed by management according to systems that

enhance company performance and also maximise company profits. This results work is

managed to solve problems for managing task in decided budget.

TASK 2

P3 Cost calculation

Marginal costing- This is explained as the technique through which overall marginal cost

is managed by charging it from unit of cost. Snooker Ltd. utilise the marginal costing technique

because it helps for calculation of profits in proper manner.

Advantages

Marginal costing technique is simplified so this is easy to understand and it also helps

organisation for determine appropriate level of profits (Kharlamova and et. al., 2020).

This minimise the problems for completion of task according to decided goals.

Marginal costing technique determine all profits and it aids organisation for completion

of task in an accurate manner by engage of right approach within business. This is also

used for interpretation better decision by deciding accurate margins for organisation.

Disadvantage

It relies on various assumptions related with business so sometimes they not generate

right statement for organisation to perform business properly.

Sometimes marginal costing is not able for control overheads and it create problems for

organisation to perform all business in proper manner.

Absorption costing- This is explained as the technique by which organisation identify all

cost that relates with process of production (Lavia López and Hiebl, 2015). Snooker ltd. ensures

profits are utilised in proper manner and it also reduce all problems for treating or overcome

from the overheads related issue.

Advantages

This technique is more beneficial for organisation as it ensures that they are able for

identify of production cost. Snooker Ltd. calculates all cost by use of absorption costing.

.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Absorption costing generate advantage for organisation for treat all overheads in proper

manner. Moreover, snooker ltd. calculate gross and net profit both separately by use of

absorption costing.

Disadvantage

This is complex to understand because absorption costing is difficult to engage in

organisation accounting process (Maas, Schaltegger and Crutzen, 2016).

Absorption costing relies on various assumptions so this is not appropriate for obtain

desired results.

Both techniques are useful for organisation and it ensure all profits are determined by

comparison of their previous and current year performance. Deviations and variances are

identified and it is improve for adoption of rectifying action.

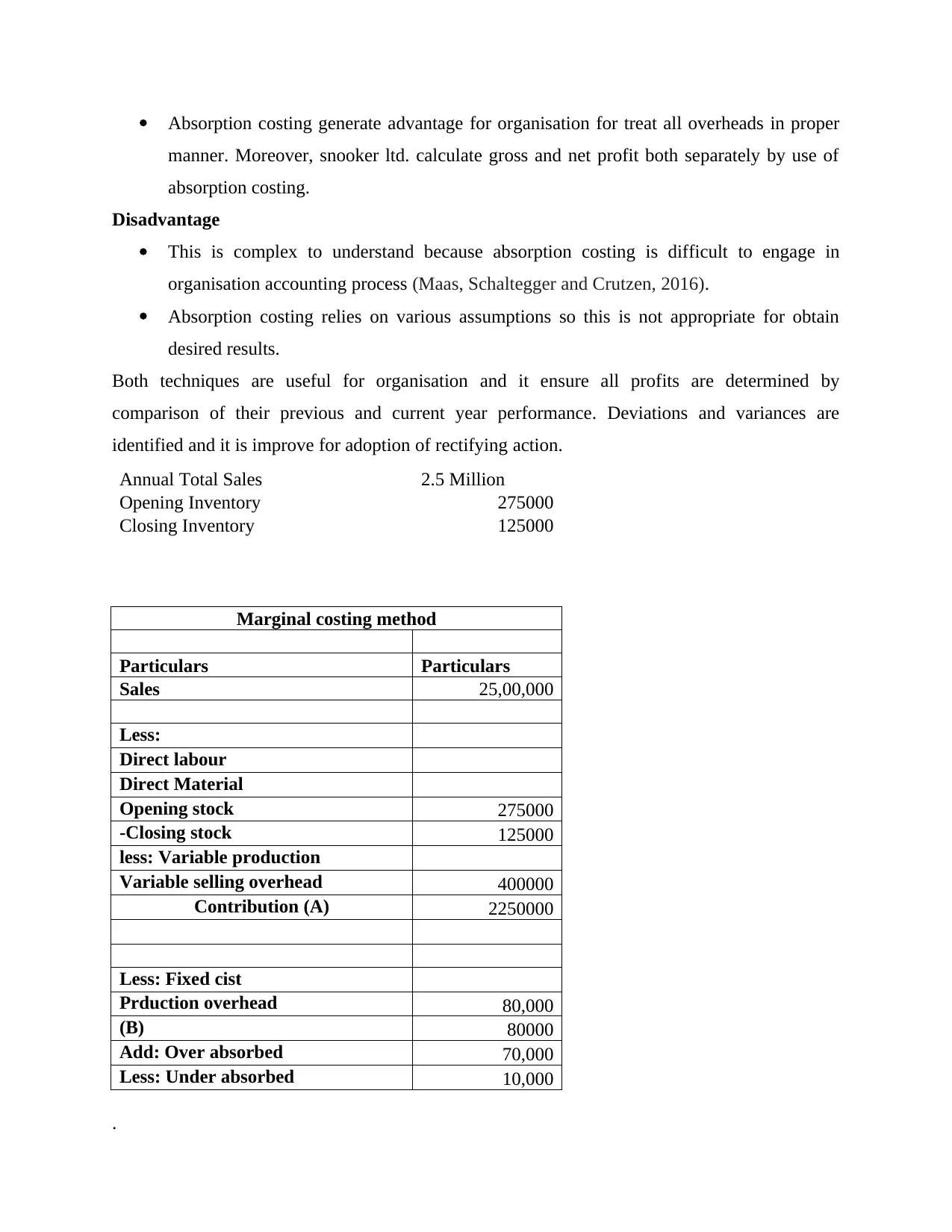

Annual Total Sales 2.5 Million

Opening Inventory 275000

Closing Inventory 125000

Marginal costing method

Particulars Particulars

Sales 25,00,000

Less:

Direct labour

Direct Material

Opening stock 275000

-Closing stock 125000

less: Variable production

Variable selling overhead 400000

Contribution (A) 2250000

Less: Fixed cist

Prduction overhead 80,000

(B) 80000

Add: Over absorbed 70,000

Less: Under absorbed 10,000

.

manner. Moreover, snooker ltd. calculate gross and net profit both separately by use of

absorption costing.

Disadvantage

This is complex to understand because absorption costing is difficult to engage in

organisation accounting process (Maas, Schaltegger and Crutzen, 2016).

Absorption costing relies on various assumptions so this is not appropriate for obtain

desired results.

Both techniques are useful for organisation and it ensure all profits are determined by

comparison of their previous and current year performance. Deviations and variances are

identified and it is improve for adoption of rectifying action.

Annual Total Sales 2.5 Million

Opening Inventory 275000

Closing Inventory 125000

Marginal costing method

Particulars Particulars

Sales 25,00,000

Less:

Direct labour

Direct Material

Opening stock 275000

-Closing stock 125000

less: Variable production

Variable selling overhead 400000

Contribution (A) 2250000

Less: Fixed cist

Prduction overhead 80,000

(B) 80000

Add: Over absorbed 70,000

Less: Under absorbed 10,000

.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Profit (A-B) 22,30,000

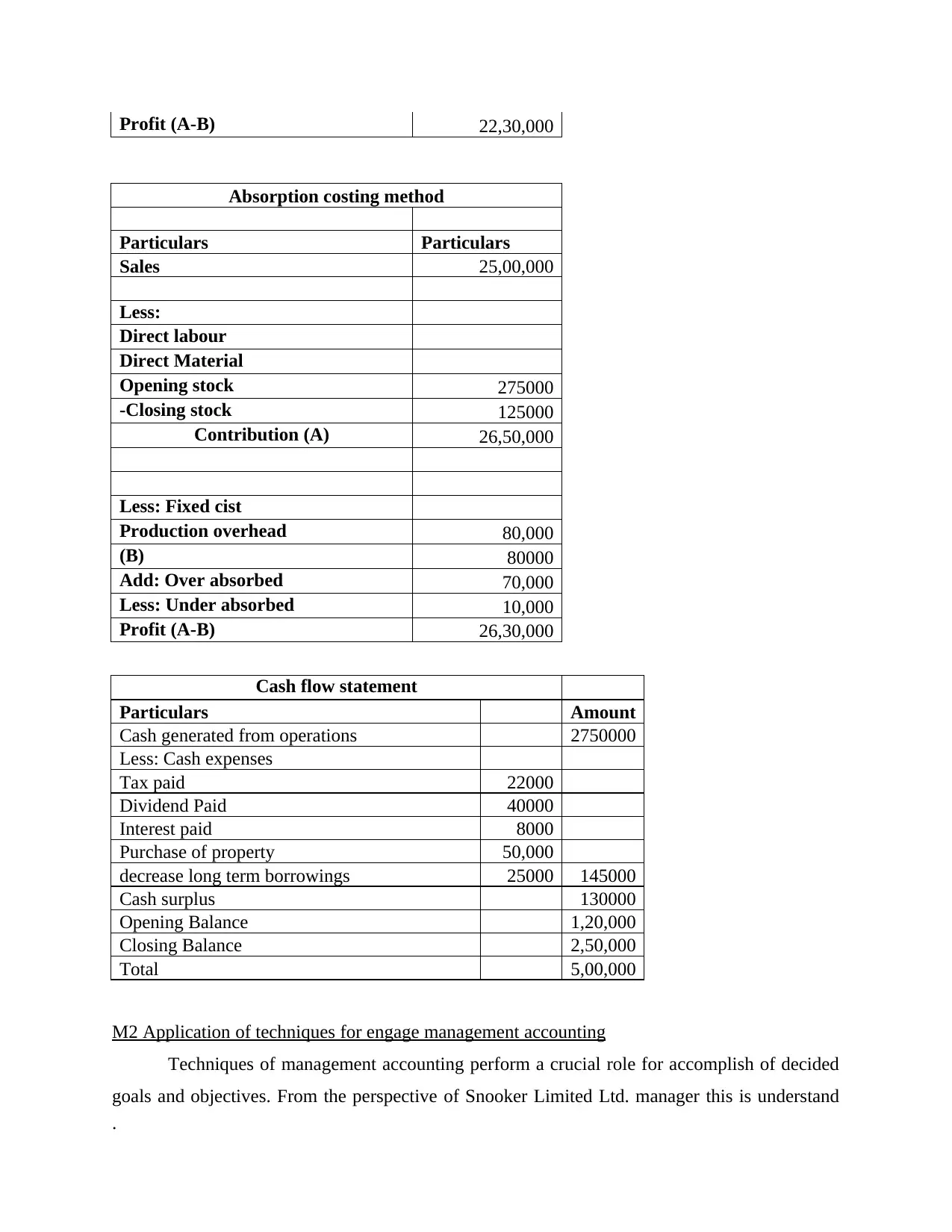

Absorption costing method

Particulars Particulars

Sales 25,00,000

Less:

Direct labour

Direct Material

Opening stock 275000

-Closing stock 125000

Contribution (A) 26,50,000

Less: Fixed cist

Production overhead 80,000

(B) 80000

Add: Over absorbed 70,000

Less: Under absorbed 10,000

Profit (A-B) 26,30,000

Cash flow statement

Particulars Amount

Cash generated from operations 2750000

Less: Cash expenses

Tax paid 22000

Dividend Paid 40000

Interest paid 8000

Purchase of property 50,000

decrease long term borrowings 25000 145000

Cash surplus 130000

Opening Balance 1,20,000

Closing Balance 2,50,000

Total 5,00,000

M2 Application of techniques for engage management accounting

Techniques of management accounting perform a crucial role for accomplish of decided

goals and objectives. From the perspective of Snooker Limited Ltd. manager this is understand

.

Absorption costing method

Particulars Particulars

Sales 25,00,000

Less:

Direct labour

Direct Material

Opening stock 275000

-Closing stock 125000

Contribution (A) 26,50,000

Less: Fixed cist

Production overhead 80,000

(B) 80000

Add: Over absorbed 70,000

Less: Under absorbed 10,000

Profit (A-B) 26,30,000

Cash flow statement

Particulars Amount

Cash generated from operations 2750000

Less: Cash expenses

Tax paid 22000

Dividend Paid 40000

Interest paid 8000

Purchase of property 50,000

decrease long term borrowings 25000 145000

Cash surplus 130000

Opening Balance 1,20,000

Closing Balance 2,50,000

Total 5,00,000

M2 Application of techniques for engage management accounting

Techniques of management accounting perform a crucial role for accomplish of decided

goals and objectives. From the perspective of Snooker Limited Ltd. manager this is understand

.

organisation consider and analyse all those factors which is used for achieving and interpreting

all detailed plans. Manager of Snooker ltd. aid towards interpret all details in proper manner with

use of all those techniques that implement better management accounting to accomplish about

better results. Along with this methods and techniques define about all those factors through

which techniques of management accounting ensure about all sustainable success to increase

growth related factors. In the last, sustainable success is achieved within future by use of

techniques through formulate of appropriate strategy. The competitive edge is achieved and it

defines by maximising all values related with product and services.

D2 Production of financial report for apply and interpret in different range of activities

Financial report is utilised by organisation for interpretation of all information and data in

an efficient and effective manner. This result towards formulation of techniques which helps of

accomplishing goals by adoption and implement strategy that create no issue and problem within

organisation growth. Moreover, financial report aid business management for improve the

company process and it also ensure sustainable success is achieved within future by analysing

and interpreting all information related with business (Mohamed and Jones, 2014). Also, proper

use of technique helps to accomplish competitive-edge in market by understanding current

market information. It is quite important for top authorities and financial division of organisation

to use financial report because this helps to formulate effective and appropriate strategy for

engage departments. It results all work is managed and complete according to decided

information and also all individuals works for a similar goal.

TASK 3

P4 Advantages and disadvantages of different types of planning budgetary tools

Different tools exist and some of them which is used by the organisation for managing the

budgets are mention as follow:

Cash budget-

A cash price range is prepared by using the different departments of company in order to

get an estimate of the general receipts and payments for the duration of a particular period of

time which is mostly a 12 months. The managers of snooker ltd. can use this budget so that they

may be capable of obtain their decided goals and targets and also, to manipulate their liquidity

level without problems and issues.

.

all detailed plans. Manager of Snooker ltd. aid towards interpret all details in proper manner with

use of all those techniques that implement better management accounting to accomplish about

better results. Along with this methods and techniques define about all those factors through

which techniques of management accounting ensure about all sustainable success to increase

growth related factors. In the last, sustainable success is achieved within future by use of

techniques through formulate of appropriate strategy. The competitive edge is achieved and it

defines by maximising all values related with product and services.

D2 Production of financial report for apply and interpret in different range of activities

Financial report is utilised by organisation for interpretation of all information and data in

an efficient and effective manner. This result towards formulation of techniques which helps of

accomplishing goals by adoption and implement strategy that create no issue and problem within

organisation growth. Moreover, financial report aid business management for improve the

company process and it also ensure sustainable success is achieved within future by analysing

and interpreting all information related with business (Mohamed and Jones, 2014). Also, proper

use of technique helps to accomplish competitive-edge in market by understanding current

market information. It is quite important for top authorities and financial division of organisation

to use financial report because this helps to formulate effective and appropriate strategy for

engage departments. It results all work is managed and complete according to decided

information and also all individuals works for a similar goal.

TASK 3

P4 Advantages and disadvantages of different types of planning budgetary tools

Different tools exist and some of them which is used by the organisation for managing the

budgets are mention as follow:

Cash budget-

A cash price range is prepared by using the different departments of company in order to

get an estimate of the general receipts and payments for the duration of a particular period of

time which is mostly a 12 months. The managers of snooker ltd. can use this budget so that they

may be capable of obtain their decided goals and targets and also, to manipulate their liquidity

level without problems and issues.

.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advantages

A cash price range can be utilized by the corporations in order that the liquidity stage is

maintained. This is a bonus for the managers of Snooker England Ltd.

Cash price range can be utilized by the groups so that they may be able to maintain the

desired stage of efficiency as well as effectiveness in their business operations.

Disadvantage

A cash budget does not offer the power to the corporations in their cash operations which

could create a drawback for the companies to use it properly.

Formulation of cash budget is a time-consuming process and also expensive so this is not

used by each company. This is also a disadvantage for the selected business enterprise.

Production budget-

Manufacturing price range may be utilized by the agencies in order that they may be able

to forecast their numerous types of necessities which they have to get while match with the level

of manufacturing inside the decided time period (Pelz,, 2019). The managers of Snooker England

Ltd. can use this budget for making correct forecasts for the future term.

Advantages-

Production budget can help the corporations to identify their various kinds of

requirements which they have concerning the production of products. For this reason it's

work as an advantage for organisation.

Production budget can assist the companies in ensuring that the production occurs on

time and consistent with the necessities. Therefore this creates an advantage for the

businesses like harmless liquids.

Disadvantages

Production budget is based on various assumptions for the cause of forecasting the

statistics that may bring about unreliable conclusions. Accordingly this is a drawback for

the selected organisation.

Production budget can't be adjusted in step with the future modifications in demand and

supply and accordingly in dynamic enterprise surroundings this leads to a drawback for

business.

Master Budget

.

A cash price range can be utilized by the corporations in order that the liquidity stage is

maintained. This is a bonus for the managers of Snooker England Ltd.

Cash price range can be utilized by the groups so that they may be able to maintain the

desired stage of efficiency as well as effectiveness in their business operations.

Disadvantage

A cash budget does not offer the power to the corporations in their cash operations which

could create a drawback for the companies to use it properly.

Formulation of cash budget is a time-consuming process and also expensive so this is not

used by each company. This is also a disadvantage for the selected business enterprise.

Production budget-

Manufacturing price range may be utilized by the agencies in order that they may be able

to forecast their numerous types of necessities which they have to get while match with the level

of manufacturing inside the decided time period (Pelz,, 2019). The managers of Snooker England

Ltd. can use this budget for making correct forecasts for the future term.

Advantages-

Production budget can help the corporations to identify their various kinds of

requirements which they have concerning the production of products. For this reason it's

work as an advantage for organisation.

Production budget can assist the companies in ensuring that the production occurs on

time and consistent with the necessities. Therefore this creates an advantage for the

businesses like harmless liquids.

Disadvantages

Production budget is based on various assumptions for the cause of forecasting the

statistics that may bring about unreliable conclusions. Accordingly this is a drawback for

the selected organisation.

Production budget can't be adjusted in step with the future modifications in demand and

supply and accordingly in dynamic enterprise surroundings this leads to a drawback for

business.

Master Budget

.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This is used by the organisation for formulation of better and effective operating as well

as financial plans that work better for the future. One of the most important factors consider

about all techniques and it summarize about all details due to which work is managed with

decided financial budgets.

Advantages

Master budget support organisation for preparation of budgets related with all

departments by forecasting overall operations and functions (Phan, Baird and Su, 2017).

It work all operations are tracked in proper manner.

Goals and objectives are accomplished by organisation through induce of master budget.

This also defines about all tasks which are accomplished without issue in proper manner.

Disadvantage

Master budget is a time-consuming process and this is because it relates with overall

organisation operations.

Master budget are not flexible so this is a disadvantage for organisation because it create

problems to adopt quick changes.

M3 Planning tools and their use

Planning tool that is related with budgetary control is used by organisation in an efficient

and effective manner and it helps for completion of task according to desired level. With the

analysis of all above task an organisation leads towards accomplishment of goals by adopting

productivity related factors (Procházka, 2017). This define future performance is improved by

the management and it helps to engage company functions and operations as per the goals. The

main role of budgetary tools is to complete their work in decided budget and values. It results

organisation profits is improved by reducing issue related with budgets.

TASK 4

P5 Compare of two organisation on the basis of adoption of management accounting system for

overcome from different financial problems

Financial problem- This is explained as the situation in which organisation face

challenge or problems for performing their work in proper manner. It results management is not

able for accomplish of their goals and objectives in an accurate manner due to financial problems

.

as financial plans that work better for the future. One of the most important factors consider

about all techniques and it summarize about all details due to which work is managed with

decided financial budgets.

Advantages

Master budget support organisation for preparation of budgets related with all

departments by forecasting overall operations and functions (Phan, Baird and Su, 2017).

It work all operations are tracked in proper manner.

Goals and objectives are accomplished by organisation through induce of master budget.

This also defines about all tasks which are accomplished without issue in proper manner.

Disadvantage

Master budget is a time-consuming process and this is because it relates with overall

organisation operations.

Master budget are not flexible so this is a disadvantage for organisation because it create

problems to adopt quick changes.

M3 Planning tools and their use

Planning tool that is related with budgetary control is used by organisation in an efficient

and effective manner and it helps for completion of task according to desired level. With the

analysis of all above task an organisation leads towards accomplishment of goals by adopting

productivity related factors (Procházka, 2017). This define future performance is improved by

the management and it helps to engage company functions and operations as per the goals. The

main role of budgetary tools is to complete their work in decided budget and values. It results

organisation profits is improved by reducing issue related with budgets.

TASK 4

P5 Compare of two organisation on the basis of adoption of management accounting system for

overcome from different financial problems

Financial problem- This is explained as the situation in which organisation face

challenge or problems for performing their work in proper manner. It results management is not

able for accomplish of their goals and objectives in an accurate manner due to financial problems

.

and challenges. It also impacts on the profit level of organisation so some techniques to minimise

the financial problems are mention as follow:

KPI- Key performance indicators are financial as well as non-financial in nature. The

main use of KPI is to identify the deviations and variances that exist in business and

impact on financial departments of organisation. From the perspective of Snooker

England Ltd. this is identified by management that KPI aid towards formulation of

methods that helps to overcome from the excessive cost problem (Quattrone, 2016). For

minimise the challenge related with excessive cost KPI indicator measure all

performance due to which it is to identify the problem.

Benchmarking- This technique is used for deciding the financial standards of respective

organisation so they are achieved in future. In simple terms, excessive cost financial

problem is solved by management through deciding the standards and numbers by which

all issues are controlled. It refer all work is completed in a decided amount of budget so

excessive cost will not generate problems for organisation.

Financial governance- It is explained as a set of action and measures which is implemented by

the organisation for maintaining financial discipline. This ensure all work is completed by

management by adopting and maintaining techniques that helps for minimising the problems of

excessive cost.

Comparison between two organisations

Basis Snooker England Ltd. FcSnooker

Financial problem Excessive cost is the major

problem that creates challenge

for organisation to perform

work in proper manner.

Due to mismanagement of job

orders FcSnooker face

problems to perform their its

operations properly.

Accounting system Inventory management system

is used for controlling the cost

by tracking use of all

resources.

Job costing system is

appropriate for the business

because this helps in

minimising problems of job

order.

.

the financial problems are mention as follow:

KPI- Key performance indicators are financial as well as non-financial in nature. The

main use of KPI is to identify the deviations and variances that exist in business and

impact on financial departments of organisation. From the perspective of Snooker

England Ltd. this is identified by management that KPI aid towards formulation of

methods that helps to overcome from the excessive cost problem (Quattrone, 2016). For

minimise the challenge related with excessive cost KPI indicator measure all

performance due to which it is to identify the problem.

Benchmarking- This technique is used for deciding the financial standards of respective

organisation so they are achieved in future. In simple terms, excessive cost financial

problem is solved by management through deciding the standards and numbers by which

all issues are controlled. It refer all work is completed in a decided amount of budget so

excessive cost will not generate problems for organisation.

Financial governance- It is explained as a set of action and measures which is implemented by

the organisation for maintaining financial discipline. This ensure all work is completed by

management by adopting and maintaining techniques that helps for minimising the problems of

excessive cost.

Comparison between two organisations

Basis Snooker England Ltd. FcSnooker

Financial problem Excessive cost is the major

problem that creates challenge

for organisation to perform

work in proper manner.

Due to mismanagement of job

orders FcSnooker face

problems to perform their its

operations properly.

Accounting system Inventory management system

is used for controlling the cost

by tracking use of all

resources.

Job costing system is

appropriate for the business

because this helps in

minimising problems of job

order.

.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.